Languages

Pages

Legal

25 January 2018

Minimising unintended risks to enhance client outcomes

This document is intended for Professional Clients as defined by MIFID only and should not be distributed to or relied upon by Non

professional clients. The information contained in this publication is not intended as investment advice or recommendation. This

information has no contractual value and is not by any means intended as a solicitation, nor an investment advice for the purchase or

sale of any financial instrument in any jurisdiction in which such an offer is not lawful.

Non contractual document

Equity Factor Investing

2

• Smart Beta / Factor Investing Landscape Section 1

• Equity Factor Investing: our Story Section 2

• Multi-factor equity: our approach Section 3

• Multi-factor equity: pure factor solutions Section 4

− Equity Multi-factor Core Section 5

− Equity Multi-Factor Income Section 6

− Equity Multi-Factor Stable Volatility Section 7

− Equity Multi-factor Stable ESG Section 8

− Equity Multi-Factor Stable Lower Carbon Section 9

• Conclusions Section 10

• Key risks to consider when investing

• Appendix

− Biographies

− Thought leadership

− GIPS® reporting

− Important information

Contents

Smart Beta / Factor Investing Landscape

4 Non contractual document

Smart Beta / Factor Investing Landscape

Nearly 3/4 of Asset Owners are

currently evaluating Multi-Factor

strategies

2/3 of Asset Owners who have

adopted smart beta are using one or

two smart beta strategies

14%

15%

16%

18%

19%

23%

25%

36%

44%

44%

74%

0% 20% 40% 60% 80%

Minimum variance

Risk parity

Maximum diversification

Equal weight

Dividend/Income/yield

Fundamentally weighted

High quality

Momentum

Value

Low Volatility

Multi-factor combination

2017

2016

Source: FTSE Smart Beta Global Survey 2017, S&P Dow Jones, EDHEC, HSBC

S&P Dow Jones Indices

December 2017

EDHEC-Risk Smart Beta Day Amsterdam 2017

21 November 2017

“Whether it involves factor investing or diversification

strategies, the vast majority of smart beta funds and

indices have underperformed over the past 12 months.”

Illustration: client preferences by expertise

“Multi-factor strategies are the

most commonly evaluated and

adopted smart beta strategies

among asset owners today.”

5 Non contractual document

Smart Beta / Factor Investing LandscapeFTSE 2017 Smart Beta global survey key findings

Why are investors moving into Smart Beta strategies?

• In 2017, Risk reduction (55%) took the lead vs return enhancement

• Cost savings’ is becoming more important

Source: FTSE Smart Beta Global Survey 2017

0% 10% 20% 30% 40% 50% 60% 70%

Other

Income generation

Provide specific factor exposure

Cost savings

Improve diversification

Return Enhancement

Risk reduction2017

2016

2015

2014

Equity Factor Investing

Our story

7 Non contractual document

1st Mandate

launched for

Institutional

client seeking

to outperform

the MSCI World

(gross)

benchmark

Global Equities

(MSCI ACWI

based) strategy

launched

UK Mutual

funds launched

– US, UK and

Japan country

funds

Systematic

Research team

restructured

within HSBC

Global Asset

Management

Research

alignment and

model

alignment

Resource

increase within

Systematic

Equity

Research team

and update to

risk modeling

February 2017

Income

strategy

launched

September

2017

HSBC GIF

Global Equity

Lower Carbon

Fund Launch

October 2017

Multi-Factor

Worldwide ETF

launched

Resource

increase in

both Research

and Portfolio

Management

alongside AUM

growth

HSBC Global Asset ManagementA story of strong growth in equity factor investing

Any performance information shown refers to the past and should not be seen as an indication of future returns.

Source: HSBC Global Asset Management as at end of December 2017. For illustrative purposes only.

HSBC Equity

Factor

Investing

1st mandate: Launched in 2004; benchmark MSCI World (gross)

MSCI ACWI mandate running for over 10 years : Launched in 2006

Track record Information Ratio of 0.7 since inception

Pooled funds: core, income tilted & Carbon constrained exposure

USD 10+ bnAUM USD 5+ bn

2011

2013

20

17

2006

20

04

2016

2015

8 Non contractual document

HSBC Equity capabilitiesAll strategies share a responsible investment philosophy

Source: HSBC Global Asset Management as at 31 December 2017. Representative overview of the investment process, which may differ by product, client mandate or market conditions.

For informational purposes only and should not be construed as a recommendation for any investment product or strategy. Not an exhaustive list of capabilities. For illustrative purposes only.

Cost efficient index replication

Efficient exposure to reference cap-weighted indices

Transparent end-to-end process focused on minimising implementation costs

Risk managed efficient portfolio replication

Physical replication; fully replicated or optimised

Intelligent implementation of index changes

Passive Strategies

Global, regional & single country

Customised implementation

– Full replication

– Enhanced Implementation

– Optimised implementation

Enhanced risk adjusted returns

Aims to improve risk-adjusted return relative to cap-weighted indices

Cost efficient equity fulfilment & customized solutions

Proprietary insights driven by experienced & well resourced research & portfolio

management teams

Diversifies risk through portfolio construction & the combination of multiple factors

Intelligent implementation of portfolio rebalances

Active Systematic Global, regional & single country

– Core Multi Factor

– Stable Volatility

– Enhanced Income

– Lower Carbon and ESG Tilt

– Fundamental weighting

Stock selection driving alpha

Common philosophy across strategies: captures deviations from the well established

relationship between profitability & valuation

Proprietary fundamental research & integrated ESG analysis confirms the

opportunity

Shared insights & perspectives from the broad global investment team

Proprietary decision-support tools reinforce disciplined approach

Active Fundamental

Global, regional & single country

– Core

– Volatility Focus

– Income

– Small Cap

– Thematic/ESG

Integregated

ESG Research

Active Ownership

Policy & Advocacy

HSBC

Equity

Factor

Investing

9 Non contractual document

Investment and product teamIndex and systematic equities

An experienced investment team with strong industry experience (Yrs in HSBC in brackets)

1. Also provide implementation support in Hong Kong

Source: HSBC Global Asset Management as of 31 December 2017.

Vis Nayar, Deputy CIO Equities (22) Head of Systematic Strategies

CORE TRADING TEAMTrade Execution and

Analysis

CORE RESEARCH TEAMStrategy, Portfolio Construction and

Research

CORE IMPLEMENTATION TEAMPortfolio management and

Implementation

PRODUCT SPECIALIST TEAMPassive Equities: Market Capitalisation

and Smart Beta

Vis Nayar (22)

Head of Systematic Strategies

London

Ioannis Kampouris

(5)

Shan Jiang (2)

Lucy Dimtcheva (2)

Olivia Skilbeck (4)

Paul Denham (3)

Stamatis Sivitos (2)

Hans Hlynsson (7)

Helgi Magnusson (4)

Tunde Ajekigbe (3)

Antony Giles (2)

Vadim Karp (1)

Peng Xiao (<1)

Hong Kong

Wai Man Ko (13)

Cecil Li1 (13)

Plennie Mak1 (10)

Taipei

Scott Yu (8)

Weikuo Lin (6)

Paris

Cedric Carpentier

(15)

Joseph Molloy (3)

Head of Index and Systematic Equity

Portfolio Management

Natalie Kedgley

(10)

Portfolio Manager

Ed Gurung (10)

Portfolio Manager

Tiphaine

Kannangara (7)

Portfolio Manager

Nelson Gu (4)

Index Analyst

Peter Gray (6)

Portfolio Manager

Patricia

Keogh (5)

Portfolio Manager

Nina Assamany (3)

Assistant Fund

Manager

Haodong Gu (<1)

Assistant Fund

Manager

Simon Conroy (9)

Passive Technology

Puspal Roy (1)

Passive Technology

James Levy

Global Head Of Dealing

London

Steve Chappell

Kerem Onder

Adam Ottewill

John Stafford

Elena Ripca

David Carter

Aaron Water

Hong Kong

Samuel Lai

Anand Narayan

Kee Mung

Danny Kwok

Bosco Mok

Alexander Davey

Senior Product Specialist

Carmen Gonzalez-Calatayud

Senior Product Specialist

Emmanuelle Harboun

Passive Product Specialist

George Taylor

Passive Product Specialist

Michael (Xiaochen) Sun

Smart Beta Product Specialist

Equity Factor Investing: our approach

11 Non contractual document

Why HSBC for Equity factor investingBlending experience and understanding

Any performance information shown refers to the past and should not be seen as an indication of future returns. Source: HSBC Global Asset Management.. Representative overview of the investment process, which may differ by product, client mandate or market conditions. The commentary and analysis presented

in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Global

Asset Management. For illustrative purposes only. For illustrative purposes only.

We have the scale,

resource and

platform to be

partners for our

clients who wish to

implement factor

based strategies

We have over a

decade of

experience helping

clients benefit from

equity factor

exposures in their

equity investment

portfolios, delivering

client based

solutions

We understand the

roles that both risk

and return play in a

portfolio

This is critical to our

investment process,

implementation and

performance.

Peer group analysis

shows that we

delivering improved

risk adjusted returns

12 Non contractual document

Why use a Multi-Factor equity solution?Equity factors and how they may be helpful

Value Momentum

Quality Low Risk

Size

Best

Performer

Worst

Performer

0

Value Quality Momentum Low Risk Size

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 YTD

18.2% 7.9% 19.1%

17.5% 22.6% 10.7% 7.6% 11.9% 2.4%

12.6% 44.2% 13.2% 16.4% 9.2% 7.3% 6.8% 17.6% 12.7% 3.9% 28.2% 10.7% 2.2% 11.3%

16.0% 22.9% 4.9% 12.5% 11.0% 16.0% 5.1% 4.2% 1.3% 12.2% 11.2% 46.5% 2.8% 7.0% 9.7% 2.1% 14.5% 2.3%

3.1% 9.4% 4.0% 5.6% 10.0% 9.0% 2.0% 2.3% 0.5% 10.3% 8.2% 10.6% 2.3% 5.5% 0.8% 4.4% 0.8% 22.0% 5.9% 0.9%

-5.5% -3.6% -3.6% -2.8% -7.5% -5.8% -0.8% -5.9% -1.6% -3.6% -2.8% -1.1% -0.9% -1.0% -0.2% -1.6% -0.2%

-7.2% -6.8% -9.9% -11.9% -16.9% -2.8% -4.1% -7.4% -2.0% -1.2% -1.7% -2.2% -2.1% -4.1%

-14.3% -26.1% -16.5% -2.5% -5.6% -8.0%

-5.1% -13.1%

Simulated data is shown for illustrative purposes only, refers to the past and should not be relied on as indication for future returns. Source: HSBC Global Asset Management, FactSet, Worldscope, IBES, Bloomberg as of June 2017. Figures have been calculated using monthly total returns in USD from 30/01/1998 – 28/04/2017 with

S&P 500 Index as universe.

Simulations are based on Back Testing assuming that the optimisation models and rules in place today are applied to historical data. As with any mathematical model that calculates results from inputs,

results may vary significantly according to the values inputted. Prospective investors should understand the assumptions and evaluate whether they are appropriate for their purposes. Some relevant

events or conditions may not have been considered in the assumptions. Actual events or conditions may differ materially from assumptions.

• Factors drive stock risk and return, potentially enabling

outperformance of a standard ‘index’

• 5 key factors have been identified by academics and more

widely adopted by investors over the years

• Individual factors perform differently in different economic

cycles, multi-factor strategies highlight the benefits of

diversification and potentially enhancing returns across a

variety of economic regimes

Equity Multi-Factor Investing

“Pure” factor solutions

14 Non contractual document

• Bottom-up methodology

combines factor scores at the

stock level

• Portfolio construction process

optimises exposure to alpha

signals in a transparent and

consistent way

• We apply active limits at the

sector, country and factor

level to avoid taking

unrewarded risks

Equity Multi-Factor InvestingHighlights

• Selected factors

• Investment options: multi-factor to diversify factor risk,

customised single or combined factor Portfolios

• Implementation: direct securities

• Geographies: global, regional or country

• Customisation: client driven constraints such as tracking

error levels, factor blends, volatility targets and carbon

constraints can be accommodated

• Target information ratio: 0.5 - 1.0 (gross of fees)

Our proposalOur process

Source: HSBC Global Asset Management. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only.

15 Non contractual document

Simple & SophisticatedIntuitive approach to factor investing

Maximise the exposure to intended factor premia; minimize exposure to unintended sources of risk

Construct

• Create factor composites with weighted sub definitions

• Weighted on ‘explanatory’ relevance of factor

• Careful management of stocks with multiple risk

dimensions

Advantages:

• More robust calculations across

the universe

• Increased explanatory power

• Removing ‘false signals’

Combine

• Combination designed to benefit from independence of

each factor

• Consider factor tilts to benefit from regimes

Advantages:

• Each factor contributes to the

overall score effectively

• Truly complementary

• Benefit from factor regimes

Calibrate

• Understanding stock risk is critical

• Maximise the portfolio exposure to desired factors

• Minimise idiosyncratic risk at the stock level

• Manage constraints

Advantages:

• Delivers optimal portfolio given

risk, constraints and objectives

1

2

3

Source: HSBC Global Asset Management.. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only.

16 Non contractual document

I. Constructing a composite factorCarefully considered factor composites

Historic value

Current value

Risk adjusted

value

Forward value

Profitability

Leverage

Earnings quality

Group

momentum

Multiple

specification

periods

Predicted beta

Uses estimated

volatilities and

correlations

Market

capitalization

Sales

Total assets

Value Quality Momentum Low risk Size

Typically

pro-cyclicalTypically

defensiveDynamic

Typically

pro-cyclical

Typically

defensive

Construct

II. Combine

Advantages:

• More robust calculations across the universe

• Increased explanatory power

• Removing ‘false signals’

• Create factor composites with weighted sub components

• Weighted on ‘explanatory’ relevance of components

• Careful management of stocks with multiple risk dimensions1

Source: HSBC Global Asset Management.. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only.

17 Non contractual document

II. Combine - the Multi Factors Signal TiltTilted Weights – small but positive expected benefits

• Portfolios can benefit from the observation that factor regimes:

― Tend to be persistent for a number of months

― Transition points are difficult to time

• We focus our portfolios on a tilt towards factors that are working today, however this tilt is anchored around an equal weighting point.

• This ‘tilt’ enables capital to remain deployed in less correlated factors, which can be advantageous as performance regimes develop

0

200

400

600

800

avr.-01 avr.-03 avr.-05 avr.-07 avr.-09 avr.-11 avr.-13 avr.-15

Equally Weighted Raw Factor

Equally Weighted StatisticallyIndependentTilted Model

0%

20%

40%

60%

80%

100%

Mar-01 Mar-03 Mar-05 Mar-07 Mar-09 Mar-11 Mar-13 Mar-15Value Quality Momentum Lowbeta Size

Simulated data is shown for illustrative purposes only, refers to the past and should not be relied on as indication for future returns. Source: HSBC Global Asset Management, FactSet, Worldscope, IBES, Bloomberg as of 31 December 2016. Figures have been calculated using monthly total returns in USD from 01 March 2001 – 31

December 2016. Simulations are based on Back Tested results. Backtested results have inherent limitations, some of which are described below. Backtested returns do not represent the performance

results of actual trading or portfolio asset allocations for any client assets or portfolios. Backtested returns are calculated through the retroactive application of the proposed asset allocation to its relevant

benchmark and are produced with the benefit of hindsight. Therefore, the performance results are not indicative of the skill of HSBC Global Asset Management or of future results. Since backtested

performance results do not represent actual trading or portfolio asset allocations they may not reflect the impact that material economic and market factors might have had on decisions made in actual

trading or portfolio asset allocations. No representation is being made that any portfolio will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently significant material

differences between backtested performance and performance results subsequently achieved by following a particular strategy. See the Important Information section for additional information on

backtested results. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only.

Combine

Advantages:

• Each factor contributes to the overall

score effectively

• Truly complementary

• Benefit from factor cyclicality

• Combination designed to benefit from independence of each

factor

• Consider factor tilts to benefit from regimes2

18 Non contractual document

Calibrate

II. Combine

Advantages:

• Delivers optimal portfolio given risk,

constraints and objectives

• Understanding stock risk is critical

• Maximise the portfolio exposure to desired factors

• Minimise idiosyncratic risk at the stock level

• Manage constraints3

III. Calibrate – Understanding stock risk is criticalStocks exhibit multiple factor characteristics

Source: HSBC Global Asset Management, illustration as of April 2017. Representative overview of the investment process, which may differ by product, client mandate or market conditions.

For illustrative purposes only.

• Stocks may exhibit multiple factor characteristics simultaneously

• Issue: If we combine multiple stocks ‘naively’, we may suffer a loss of diversification

• Why: Simple or naïve combinations of factors may lead to one set of factor exposures - quality, low risk,

size - cancelling exposures to another factor, such as value

• Risk can potentially increase, and the benefits of factor diversification are diluted

-3,00

-1,00

1,00

3,00Value

Quality

MomentumLow Risk

Size

JOHNSON & JOHNSON

-3,00

-2,00

-1,00

0,00

1,00

2,00

3,00Value

Quality

MomentumLow Risk

Size

APPLE INC

-3,00

-2,00

-1,00

0,00

1,00

2,00

3,00Value

Quality

MomentumLow Risk

Size

MICROSOFT CORP

19 Non contractual document

III. Calibrate - Intuitive Portfolio ConstructionCalibrated signal serves to drive stock weightings

Name Sector Country

Multi-

Factor

Score

Value Quality MomentumLow

RiskSize

Trade

Weight

KLA TENCORInformation

TechnologyUS 2.43 -0.37 1.04 2.79 0.72 0.5 0.2

STAPLESConsumer

DiscretionaryUS 1.76 1.43 -0.11 0.63 -0.27 -0.1 0.13

CONOCOPHILLIPS Energy US -0.26 0.16 -1.78 1.12 -1.05 -1.38 0.13

SEGATE

TECHNOLOGY

Information

TechnologyUS -0.48 0.27 -0.27 -0.5 -1.34 -0.07 -0.18

PAY CHEXInformation

TechnologyUS -0.44 -1.47 1.4 -0.93 1.57 0.09 -0.23

driven by the initial portfolio’s underweight in the Energy

sector.

driven by a high ranking on our combined multi-factor score

due to a low ranking on our combined multi-factor score

Individual factor scores are made independent to

enable us to calibrate the final multi factor score with

tilting towards factors that are working today

Portfolio Optimisation

Initial Portfolio

Optimal Portfolio

Multi-Factor Score

Risk Model

Constraints

Information Coefficient

\

Simulated data is shown for illustrative purposes only, refers to the past and should not be relied on as indication for future returns. Source: HSBC Global Asset Management. Simulated data is shown for illustrative purposes only, and should not be relied on as indication for future returns. Simulations are based on Back Tested results.

Backtested results have inherent limitations, some of which are described below. Backtested returns do not represent the performance results of actual trading or portfolio asset allocations for any client

assets or portfolios. Backtested returns are calculated through the retroactive application of the proposed asset allocation to its relevant benchmark and are produced with the benefit of hindsight.

Therefore, the performance results are not indicative of the skill of HSBC Global Asset Management or of future results. Since backtested performance results do not represent actual trading or portfolio

asset allocations they may not reflect the impact that material economic and market factors might have had on decisions made in actual trading or portfolio asset allocations. No representation is being

made that any portfolio will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently significant material differences between backtested performance and performance

results subsequently achieved by following a particular strategy. See the Important Information section for additional information on backtested results. Representative overview of the investment process,

which may differ by product, client mandate or market conditions. For illustrative purposes only.

20 Non contractual document

Passive and Systematic Equity InvestingFocus on investment process and efficient implementation

Teams input Process flow for each trade

Investment universe: liquid, investable stocks on-benchmark

Add value on rebalancing & benchmark events: ultimate goal of maximising risk-adjusted returns after all costs

Recommended trades: cost effective implementation, compatible with portfolio risk parameters

Continuous Review : Post-trade stock and Attribution analysis, Performance impact & monitoring

Active Systematic Models

Proprietary risk model

Corporate Actions

Transaction Costs

Tracking Error Budget Allocation

Defined Operating Parameters

Customised portfolio tools

Generate optimised basket trades

Corporate Actions

Client Exclusions

Dividend Elections

Proprietary Index Predictions

Additional Analytics & Data

Tracking Error Budget Allocation

Multi horizon trading periods

Best Execution

Portfolio Implementation

Enhancement strategy

Portfolio construction

Trading strategy

Model Portfolio Changes

Filters & Exclusions

Holdings

Optimisation / Replicated

Pre Trade Analysis

Size

Timing

Liquidity & Risk

Portfolio Construction

Corporate Actions

Index Changes

Implementation

Systematic Equity Research

Systematic and Index Equity

Portfolio Management

Global Trading Team

Source: HSBC Global Asset Management.. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only.

Equity Multi-Factor CoreControlled exposure to 5 robust factors

22 Non contractual document

Equity Multi-Factor Core

Objectives

• Provide consistent outperformance against a

market-capitalisation weighted equity index

• Generate attractive, risk adjusted returns

through exposure to a suite of diversified

sources of factor premia, over the medium to

long term

• Managed with tracking error from enhanced

(0.5%) to alpha seeking (2-3%)

• Provide cost efficiency within a transparent and

intuitive investment process

We only accept factors that boast strong

empirical support with credible economic

rationale. We embrace the use of factor

composites to harvest the returns of each

anomaly and deliver our proprietary

research insights’

Five robust factors

Value: favour cheap vs expensive

aTypically pro-cyclical

Quality: favour high quality vs low quality

aTypically defensive

Momentum: favour long term trends

aDynamic

Low risk: favour low risk

vs high risk

a Typically defensive

Size: favour

smallest vs largest

a Typically pro-

cyclical

Source: HSBC Global Asset Management. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only

23 Non contractual document

Multi-Factor Global Equity – superior risk-adjusted returnsSupplemental information and external peer comparison

Performance % in USD – low tracking error (~50bps)1

Any performance information shown refers to the past and should not be seen as an indication of future returns.

Performance is gross of fees and would be lowered after deduction of management and administrative fees. 1 Source: HSBC Global Asset Management as at end of September 2017. * Annualised Returns.3 Prior to Oct 2006 benchmark was MSCI World ex Energy. From Oct 2006-Dec07 the benchmark was 45% S&P 500 Gross, 30% DJ Euro Stoxx Gross 50, 10% Nikkei 225 Price, 10% FTSE 100 Gross,

5% S&P / ASX 200 Gross. From Jan 08 to Nov 11 benchmark was 40% S&P 500 Gross, 35% DJ Euro Stoxx 50 Gross, 10% Nikkei 225 Price, 10% FTSE 100 Gross, 5% S&P / ASX 200 Gross. From

Nov11 the benchmark is MSCI World Index with Gross Dividend reinvested, unhedged.2 Source: eVestment Alliance, LLC and its affiliated entities (collectively, “eVestment”) collect information directly from investment management firms and other sources believed to be reliable, however,

eVestment does not guarantee or warrant the accuracy, timeliness, or completeness of the information provided and is not responsible for any errors or omissions. Performance results may be provided

with additional disclosures available on eVestment’s systems and other important considerations such as fees that may be applicable. Not for general distribution and limited distribution may only be made

pursuant to client’s agreement terms. All categories not necessarily included, Totals may not equal 100%. Copyright 2012-2017 eVestment Alliance, LLC. All Rights Reserved.

2,3

4,9

16,3

8,5

11,8

2,3

5,0

16,5

8,3

11,6

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

1m 3m YTD 3Y* 5Y*

Composite - Equity Enhanced Global Low TE

Benchmark: MSCI World (Gross)

1 2

We have a strong track record of delivering strong risk adjusted returns in core Multi-Factor Equity

portfolios

3

Three year statistics vs. eVestment Global Smart Beta Equity vs.

MSCI World-ND displayed in vehicle base currency USD2

The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute

any kind of commitment from HSBC Global Asset Management

From Core to Customised Solutions

Equity Multi-Factor IncomeTilted to enhance portfolio income

26 Non contractual document

Equity Multi-Factor IncomeTilted for income & minimise risk characteristics

How do we tilt for ‘income’?

1. Identify stocks from a universe of investable securities

2. Rank the stocks based on income characteristics: dividend yield, cash flow

yield & return of investment capital

3. Screen the universe of stocks according to the amount of dividends paid to

stock holders relative to the amount of total income of a company

How do we implement a multi-factor portfolio for income?

1. We seek to isolate income opportunities within our ‘bottom up’ process

− We have embedded income embedded into our proprietary

systematic investment process

− We will build a portfolio that maximises exposure to stocks with the

most attractive income characteristics

2. Alongside, we will minimise the portfolio’s risk characteristics by applying a

series of constraints:

− Sector, country and stock weights

Source: HSBC Global Asset Management. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only

We view ‘income

characteristics’ as

embedded in our

broader factor

definitions

MSCI defines ‘Dividend’

as a ‘6th’ factor’

Equity Multi-Factor Stable VolatilityTilted for sensitivity to volatility

28 Non contractual document

Equity Multi-Factor Stable VolatilityPortfolio implementation and management

• The portfolio combines equities, cash & index futures

• Ongoing volatility is monitored (1) on a weekly basis & (2) based on a volatility target

• Participation rate: we increase money allocated to cash if we are running close to the volatility target

• Smaller drawdowns & smoother ride over time by balancing downside mitigation with upside

participation regardless of the market environment

• We optionally short the market to hedge against the “allocation volatility”, maintaining (1) lower

turnover & (2) higher average equity exposure

We aim to be fully invested over the cycle to enhance returns

Source: HSBC Global Asset Management. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only

29 Non contractual document

Existing sell-side solutions

Volatility targeting is attractive under Solvency II (and lower

option costs)

Underlying typically limited to index strategies (market beta)

Frequent rebalancing between cash and equities is

unappealing

Multi Factor Stable Volatility aims to improve

risk-adjusted returns

• We can customize for clients, incorporating additional

requirements such as ESG improvement

• Manage volatility through weekly rebalances and use short

index futures as appropriate. Only allocate to cash if absolutely

necessary. This will improve participation rate

0%

20%

40%

60%

80%

100%

120%

févr.

05

août 05

févr.

06

août 06

févr.

07

août 07

févr.

08

août 08

févr.

09

août 09

févr.

10

août 10

févr.

11

août 11

févr.

12

août 12

févr.

13

août 13

févr.

14

août 14

févr.

15

août 15

févr.

16

août 16

févr.

17

août 17

Equity Multi-Factor Stable Volatility Innovation aligned with Clients needs

Source: HSBC Global Asset Management, 15 December 2017. Source: HSBC Global Asset Management, 15 November 2017. Since strategy inception in 2004.

Participation: Standard Target Volatility Strategy (10%)Participation: Stable Volatility Multi-Factor Strategy 10%

Target

Simulated data is shown for illustrative purposes only, refers to the past and should not be relied on as indication for future returns. Simulations are based on Back Tested results. Backtested results have inherent limitations, some of which are described below. Backtested returns do not represent the performance results of actual

trading or portfolio asset allocations for any client assets or portfolios. Backtested returns are calculated through the retroactive application of the proposed asset allocation to its relevant benchmark and

are produced with the benefit of hindsight. Therefore, the performance results are not indicative of the skill of HSBC Global Asset Management or of future results. Since backtested performance results

do not represent actual trading or portfolio asset allocations they may not reflect the impact that material economic and market factors might have had on decisions made in actual trading or portfolio

asset allocations. No representation is being made that any portfolio will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently significant material differences between

backtested performance and performance results subsequently achieved by following a particular strategy. See the Important Information section for additional information on backtested results

0%

20%

40%

60%

80%

100%

120%

févr.

05

août 05

févr.

06

août 06

févr.

07

août 07

févr.

08

août 08

févr.

09

août 09

févr.

10

août 10

févr.

11

août 11

févr.

12

août 12

févr.

13

août 13

févr.

14

août 14

févr.

15

août 15

févr.

16

août 16

févr.

17

août 17

The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute

any kind of commitment from HSBC Global Asset Management

Equity Multi-Factor ESGTilted to beat an index with ESG improvement

31 Non contractual document

Equity Factor-based ESG investingYour options…

Source: HSBC Global Asset Management. For illustrative purposes only.

Passive

tiltingTrack the index

with ESG

improvement

Factor

ESGBeat the index

with ESG

improvement

ESG is a risk

& an opportunity

ESG is integrated

in our processVoting and engagement

Our investment approach…

Equity Multi-Factor Lower Carbon

HSBC GIF Global Equity Lower CarbonTilted to reduce climate-related financial risk

33 Non contractual document

Global landscape: our changing climate

Temperature rising

Source: NASA. Temperature data from four international science institutions show rapid

warming in the past few decades and that the last decade has been the warmest on record.

NASA Goddard Institute for Space Studies

Hadley Centre/Climatic Research Unit

NOAA National Centre for Environmental Information

Japanese Meteorological Agency

0.8

0.6

0.4

0.2

0.0

0.2

0.4

0.6

1880 1900 1920 1940 1960 1980 2000 2020

Temperature Anomaly (0C)

Source: Earth System Research Laboratory (NOAA)

CO2 concentration on the rise

385

390

395

400

405

410

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

ppm

2015 2016 2014

2013

Source: NSIDC, NOAA

March Arctic sea ice extent

14.25

14.75

15.25

15.75

16.25

1981 1987 1993 1999 2005 2011 2017

Million km2

Mean sea level rise

9.0

Cm

7.0

5.0

3.0

1.0

-1.0

1996 1998 2001 2003 2005 2008 2010 2012 2014 2016

Source: Univ. of Colorado; Shows the global mean sea level rise over 1996 level

34 Non contractual document

Viewpoint: we believe that climate change is an investment risk

Source: World Economic Forum Global Risks Perception Survey 2016, 12th edition

1 Extreme weather events

2 Large-scale involuntary migration

3 Natural disasters

4 Terrorist attacks

5 Data fraud or theft

6 Cyber attacks

7 Illicit Trade

8 Man-made environmental disasters

9 Interstate conflict

10 Failure of national governance

1 Weapons of mass destruction

2 Extreme weather events

3 Water crises

4 Natural disasters

5 Failure of climate-change mitigation and adaptation

6 Large-scale involuntary migration

7 Food crises

8 Terrorist attacks

9 interstate conflict

10 Unemployment or underemployment

Top 10 risks in terms of

Likelihood

Top 10 risks in terms of

Impact

Economic

Environmental

Geopolitical

Societal

Technological

Categories

35 Non contractual document

Viewpoint: investors are taking action to address climate risk

Source: HSBC Global Asset Management. For illustrative purposes only. The views expressed were held at the time of preparation and are subject to change without notice.

• Investors globally are under pressure from regulators and beneficiaries to reduce climate risks

• Analysis indicates that stranded asset risk has already led to financial losses in extractive industries

and power generation

• Carbon-intensive companies and industries face the greatest challenge, but stock exchanges and

market-cap based indices are carbon intensive

• Energy transition will drive new technology solutions and reduce the cost of existing clean

technology

• Effective carbon pricing will drive the energy transition

Managing climate-related investment risk for our clients is a material priority

36 Non contractual document

HSBC GIF Global Equity Lower CarbonKey portfolio characteristics

Base currency USD

Investment Universe /

Target Asset Allocation

Primarily in lower- carbon equities

issued by companies in developed

markets

Reference Benchmark MSCI World Net

Performance Target Aims to outperform the reference

benchmark over the medium to long

term with a 2-3% TE

Expected returns: aims to outperform

its reference benchmark per annum

before fees

Ex-ante TE range versus the

reference benchmark of 2-3%

Country Exposure Developed markets

Share Class Offering Denominated in USD and other

dealing currencies

Base currency hedged share classes

subject to approval

Objectives

• The strategy is intended to benefit from the

returns of equities, deliver outperformance

and reduce meaningfully the carbon impact

of the equity portfolio

• To achieve this we use a multi-factor

investment process to benefit from the

opportunity factors offer for outperformance

• All stocks in the portfolio undergo a

rigorous carbon footprint analysis

• A proprietary systematic investment

process is used to create a portfolio which

maximises the exposure to the most

attractive stocks and reduces the total

portfolio carbon footprint

Source: HSBC Global Asset Management, illustrations at 30 September 2017. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For

illustrative purposes only

37 Non contractual document

HSBC GIF Global Equity Lower CarbonMaximise equity returns while reducing portfolio carbon intensity

• Investment objective is to outperform the benchmark with a lower carbon footprint

• Portfolio stock selection & sizing is driven with consideration of company carbon intensity data

• As per our Multi-Factor equity process, we maximise exposure to 5 factors, with carbon &

governance integrated into our model

• Broad ESG constraints deliver ESG enhancement

• We minimise the portfolio’s risk characteristics by applying a series of constraints: Sector, country &

stock weights

Quality Momentum Low risk SizeValue

We use carbon footprint analysis to measure the carbon associated with the fund, assess

climate-related investment risk & capture the market shift to a lower-carbon economy

ESG

Source: HSBC Global Asset Management. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only

38

HSBC GIF Global Equity Lower Carbon Focused on carbon constraints to reduce carbon risk exposure

Carbon constrained (Lower Carbon) portfolio

• Improved benchmark returns - controlling

volatility & TE with a 60% carbon reduction

• Achieved by integrating into the investment

management process an assessment of the

carbon intensity of all stocks

Source: Data provided by independent third party carbon data providers, providing data on every company in the model portfolio, as at end of December 2017.

Representative overview of the investment process, which may differ by product, client mandate or market conditions. The commentary and analysis presented in this document reflect the opinion of HSBC

Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. For illustrative purposes

only. For illustrative purposes only

0

50

100

150

200

CO2e mt/$ m revenue

Benchmark - MSCI World Lower Carbon

-60 %

Reduction

Outcome comparison

Relative carbon intensities of MSCI World vs a carbon constrained portfolio Carbon Intensity (tCO2e/USD mn revenue)

Our process and portfolio construction integrate carbon

constraints, allowing us to significantly reduce carbon risk

exposure (as measured by portfolio carbon intensity) while at the

same time seeking to generate returns that are better than the

benchmark

This investment solutions allows clients to maintain or outperform

their existing benchmark and also meet fiduciary obligations

We believe that “exclusion” is of

limited appeal given fiduciary

concerns that portfolio

performance may differ

substantially relative to a

traditional benchmark such as

the MSCI World

39

HSBC GIF Global Lower Carbon Equity Our approach: summary

Our lower-carbon equity fund is designed to capture the shift to the lower-carbon economy

without giving up on today’s market performance opportunity

The portfolio is implemented

by the passive equity portfolio

management team, benefitting

from their day-to-day market-

based experience in

implementing indices and

model portfolios

We use our established Multi-

Factor investment process to

identify and rank the most

attractive stocks in the

investment universe

To lower the exposure to

carbon intensive businesses, all

stocks in the portfolio are

assessed for their carbon

footprint

We then use our systematic

process to create a portfolio

which maximizes the exposure

to the most attractive stocks

and reduces its carbon footprint

Our investment teams use

proprietary alpha models,

customised risk models and

bespoke portfolio construction

tools to manage the fund’s

exposures whilst avoiding

unrewarded risks relative to

the benchmark

Source: HSBC Global Asset Management. Representative overview of the investment process, which may differ by product, client mandate or market conditions. For illustrative purposes only

Conclusions

41 Non contractual document

We understand the roles that

both risk and return play in a

portfolio – this is critical to

our investment process,

implementation and

performance. We deliver

better risk adjusted returns

than many of our peers

We have the scale, resource

and platform to be partners

for our clients who wish to

implement factor based

strategies

We have over a decade of

experience helping clients

benefit from equity factor

exposures in their equity

investment portfolios,

delivering client based

solutions

Equity Factor investing? Why consider HSBC as a partner?

Source: HSBC Global Asset Management.. For illustrative purposes only.

42

Key risks HSBC Multi Factor Equity Strategies & HSBC GIF Lower Carbon Equity

The value of an investment in the portfolios and any income from them can go down as well as up and as with

any investment you may not receive back the amount originally invested.

• Exchange Rate risk: Investing in assets denominated in a currency other than that of the investor’s own currency

perspective exposes the value of the investment to exchange rate fluctuations.

• Operational risk: The main risks are related to systems and process failures. Investment processes are overseen by

independent risk functions which are subject to independent audit and supervised by regulators.

• Derivative risk: The value of derivative contracts is dependent upon the performance of an underlying asset. A small

movement in the value of the underlying can cause a large movement in the value of the derivative. Unlike exchange

traded derivatives, over-the-counter (OTC) derivatives have credit risk associated with the counterparty or institution

facilitating the trade.

Appendix

44 Non contractual document

Source : HSBC Global Asset Management.

HSBC Global Asset ManagementToday’s speakers

Vis has been working in the industry since 1988, joining HSBC Markets

in 1996, and then HSBC Global Asset Management in 1999.

Vis has extensive research and portfolio management experience in

long only equity, alternative investments and structured products

businesses.

Vis holds a BSc in Electrical Engineering from Imperial College,

University of London and a Masters in Finance from London Business

School. He is a CFA charterholder, holds a Certificate in Quantitative

Finance (CQF) and also qualified as a Chartered Accountant in the UK.

Vis is also a member of the advisory board for the Masters in Finance

programmes at Imperial College.

Vis Nayar

Deputy CIO, Equities &

Responsible for

investment research

Sandra joined HSBC in 2017 and has been working in the industry since

1986.

Previously, Sandra was head of responsible investment at Newton

Investment Management in London. Before this, she spent several years at

F&C Investments and Citi, where she set up and ran the sustainable and RI

team in global markets and the European equity sales team respectively.

She also worked for Deutsche Bank in Paris and London as equity specialist

and for JPMorgan Chase in London and NY as part of the sovereign debt

restructuring team.

Sandra is a recognised industry spokeswoman and a board member of the

Principles for Responsible Investment (since 2016) and a visiting business

fellow at the Oxford Smith School for the Environment.

Sandra Carlisle

Head of Responsible

Investment (RI)

Specialists

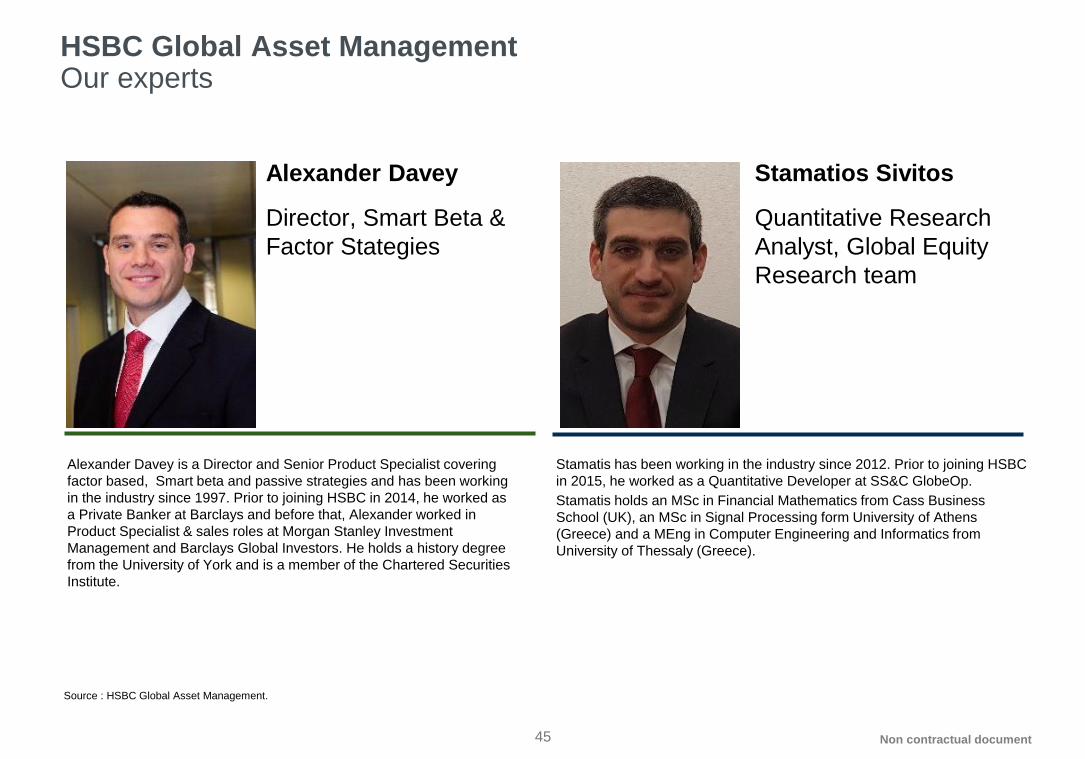

45 Non contractual document

Source : HSBC Global Asset Management.

HSBC Global Asset ManagementOur experts

Alexander Davey is a Director and Senior Product Specialist covering

factor based, Smart beta and passive strategies and has been working

in the industry since 1997. Prior to joining HSBC in 2014, he worked as

a Private Banker at Barclays and before that, Alexander worked in

Product Specialist & sales roles at Morgan Stanley Investment

Management and Barclays Global Investors. He holds a history degree

from the University of York and is a member of the Chartered Securities

Institute.

Alexander Davey

Director, Smart Beta &

Factor Stategies

Stamatis has been working in the industry since 2012. Prior to joining HSBC

in 2015, he worked as a Quantitative Developer at SS&C GlobeOp.

Stamatis holds an MSc in Financial Mathematics from Cass Business

School (UK), an MSc in Signal Processing form University of Athens

(Greece) and a MEng in Computer Engineering and Informatics from

University of Thessaly (Greece).

Stamatios Sivitos

Quantitative Research

Analyst, Global Equity

Research team

46

HSBC Factor InvestingEquity factor investing landing page

47 Non contractual document

HSBC Active SystematicAn illustration of our research

For illustrative purposes only.

48 Non contractual document

Multi Factor Global EquitySupplemental information

Any performance information shown refers to the past and should not be seen as an indication of future returns.

Performance is gross of fees and would be lowered after deduction of management and administrative fees.

Source: HSBC Global Asset Management, as at 30 September 2017. Data is supplemental to the GIPS compliant report in the appendix.

Rolling year returns (%)

Equity Enhanced Global Low TE Combined30/09/2016

to 30/09/2017

30/09/2015 to

30/09/2016

30/09/2014 to

30/09/2015

30/09/2013 to

30/09/2014

30/09/2012 to

30/09/2013

Cumulated Composite Return 18.99 12.19 -4.29 13.11 20.92

Cumulated Benchmark Return 18.83 12.02 -4.57 12.80 20.90

Relative Difference 0.16 0.17 0.27 0.31 0.02

Strategy presented on pg 23

Low tracking error (~50bps)

49 Non contractual document

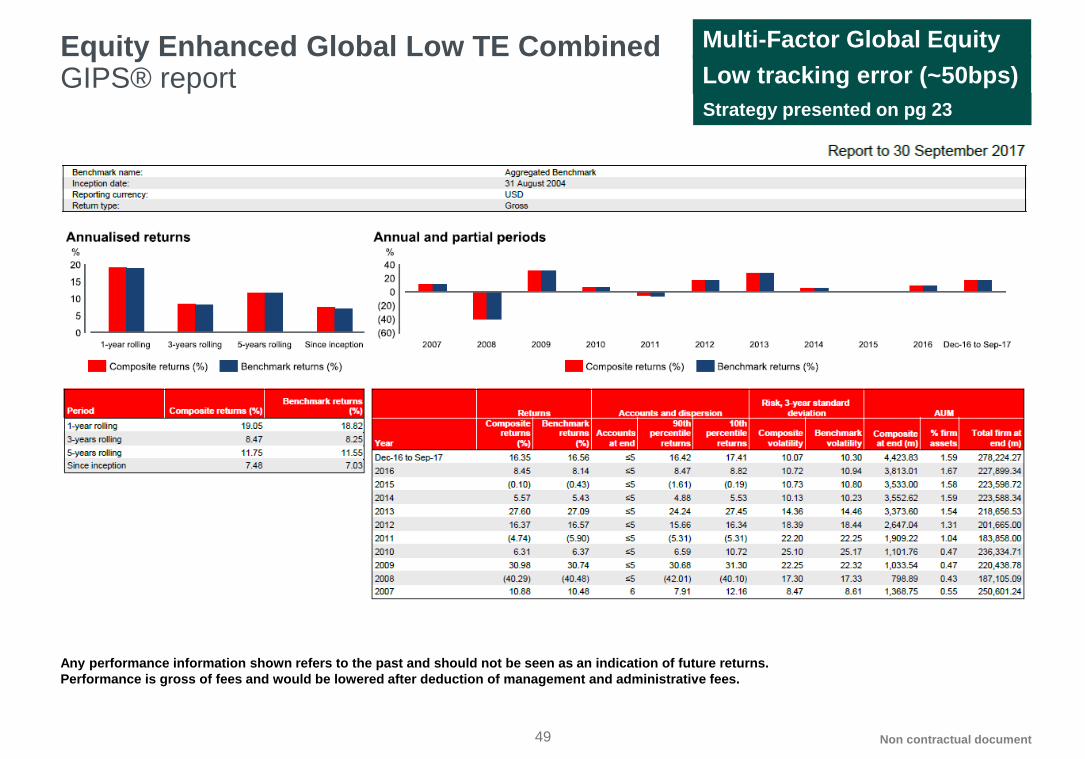

Equity Enhanced Global Low TE CombinedGIPS® report

Any performance information shown refers to the past and should not be seen as an indication of future returns.

Performance is gross of fees and would be lowered after deduction of management and administrative fees.

Multi-Factor Global Equity

Low tracking error (~50bps)

Strategy presented on pg 23

50 Non contractual document

Equity Enhanced Global Tow TE CombinedDisclosure

Multi-Factor Global Equity

Low tracking error (~50bps)

Same strategy as on pg 23

Important information

52 Non contractual document

Important information

This document is distributed in France, Italy, Spain and Sweden by HSBC Global Asset Management (France), in Switzerland by HSBC Global Asset Management (Switzerland) Ltd and is only intended for professional investors as defined

by MIFID. It is incomplete without the oral briefing provided by the representatives of HSBC Global Asset Management. The information contained herein is subject to change without notice. All non-authorised reproduction or use of this

commentary and analysis will be the responsibility of the user and will be likely to lead to legal proceedings. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase

or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the

information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management will not be held responsible for any investment or disinvestment decision

taken on the basis of the commentary and/or analysis in this document. All data from HSBC Global Asset Management unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but

which we have not independently verified.

The performance figures displayed in the document relate to the past and past performance should not be seen as an indication of future returns. The value of investments and any income from them can go down as well as up.

Capital is not guaranteed. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in established markets.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Where overseas investments are held the rate of currency exchange may cause the value of

such investments to go down as well as up. Stock market investments should be viewed as a medium to long term investment and should be held for at least five years. Investments in emerging markets are by their nature higher risk and

potentially more volatile than those inherent in some established markets.

The funds presented in this document may not be registered and/or authorised for sale in your country. It is important to remember that the value of investments and any income from them can go down as well as up and is not guaranteed.

Capital is not guaranteed. Where overseas investments are held the rate of exchange may cause the value to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those

inherent in established markets. Funds that invest in securities listed on a stock exchange or market could be affected by general changes in the stock market. The value of investments can go down as well as up due to equity markets

movements.

HSBC Global Equity Lower Carbon is a subfund of HSBC Global Investment Funds, a Luxemburg domiciled SICAV. Shares of the Company may not be offered or sold for sale or sold to any "U.S. Person within the meaning of the Articles

of Incorporation, i.e. a citizen or resident of the United States of America (the "United States"), a partnership organised or existing under the laws of any state, territory or possession of the United States, or a corporation organised or

existing under the laws of the United States or of any state, territory or possession thereof, or any estate or trust, other than an estate or trust the income of which from sources outside the United States is not includible in gross income for

purposes of computing United States income tax payable by it. All subscriptions in any fund presented in this document are accepted only on the basis of the current prospectus, available on request from HSBC Global Asset Management

(France), the centralisation agent, the financial department or the usual representative. Before subscription, investors should refer to the Key Investors Information Document (KIID) of the fund as well as its complete prospectus. For more

detailed information on the risk associated with this fund, investors should refer to the complete prospectus of the fund. Subscriptions are accepted only on the basis of the current prospectus accompanied by the latest annual or half-yearly

report, available on request.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used to create any financial instruments or products or any indices. The MSCI information

is provided on an 'as is' basis and the user of this information assumes the entire risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates or any other person involved in or related to compiling,

computing or creating the MSCI information (collectively, the 'MSCI Parties') makes any express or implied warranties or representations with respect to such information or the results to be obtained by the use thereof, and the MSCI

Parties hereby expressly disclaim all warranties (including, without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this

information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential or any other damages (including, without limitation, lost profits) even if

notified of, or if it might otherwise have anticipated, the possibility of such damages.

Important information for Luxembourg investors: HSBC entities in Luxembourg are regulated and authorised by the Commission de Surveillance du Secteur Financier (CSSF).

Important information for Swiss investors: This document may be distributed in Switzerland only to qualified investors according to Art. 10 para 3, 3bis and 3ter of the Federal Collective Investment Schemes Act (CISA). The presented fund

is authorised for distribution in Switzerland in the meaning of Art. 120 of the Federal Collective Investment Schemes Act. (Potential) investors are kindly asked to consult the latest issued Key Investor Information Document (KIID),

prospectus, articles of incorporation and the (semi-)annual report of the fund which may be obtained free of charge at the head office of the representative: HSBC Global Asset Management (Switzerland) Ltd., Gartenstrasse 26, P.O. Box,

CH-8002 Zurich. Paying agent in Switzerland: HSBC Private Bank (Suisse) SA, Quai des Bergues 9-17, P.O Box 2888, CH-1211 Genève 1.

HSBC Global Asset Management is the brand name for the asset management business of HSBC Group. The above document has been produced by HSBC Global Asset Management (France) and has been approved for

distribution/issue by the following entities :

HSBC Global Asset Management (France)

HSBC Global Asset Management (France) - 421 345 489 RCS Nanterre. Portfolio management company authorised by the French regulatory authority AMF (no. GP99026) with capital of 8.050.320 euros.

Offices: HSBC Global Asset Management (France) - Immeuble Coeur Défense - 110, esplanade du Général Charles de Gaulle - 92400 Courbevoie - La Défense 4 – France.

(Website: www.assetmanagement.hsbc.com/fr).

HSBC Global Asset Management (Switzerland) Limited

Gartenstrasse 26, P.O. Box, CH-8002 Zurich. Paying agent: HSBC Private Bank (Suisse) S.A., Quai des Bergues 9-17, P. O. Box 2888, CH-1211 Geneva 1(Website: www.assetmanagement.hsbc.com/ch)

Copyright © 2018. HSBC Global Asset Management (France). All rights reserved.

Non contractual document updated in January 2018 - AMFR_Ext_66_2018

Top Related