Languages

Pages

Legal

Enhance Investments, 9 Hope Street, St. Helier, Jersey, JE2 3NSwww.enhanceinvestments.com

+44 (0)1534 832434

The Securities and Investment Institute

“2008/9, a stark reminder….”

Richard Sayers FSIEnhance Investments Limited

“Fiduciary liability is not determined by investment performance, but rather on

whether prudent investment practices were followed.”Donald Trone

The Foundation for Fiduciary Studies

Presentation overview

• 2008/9 – Every type of investment risk?

• Unprecedented?

• Questioning the roles…

• The Investment Policy Statement

• Case Study 1: Return and volatility

• Regulation

• Benchmarks

• Case Study 2: Qualitative risks

• Case Study 3: Monitoring Multiple portfolios

• Conclusions

1. Stock specific risk – Royal Bank of Scotland

2. Sector risk – financials, property, commodities

3. Strategy risk – ‘absolute return’

4. Liquidity risk – ability to trade

5. Counterparty risk - Lehmans

6. Country risk - Iceland

7. Default risk – General Motors

8. Reinvestment risk – 0.25% yields

9. Currency risk – Sterling -27% vs. Dollar

10.Return on cash – negative real rates

11.Return of cash – bankruptcies

2008 - Every type of investment related risk?

Unprecedented or history repeating itself?

• FTSE 100 Index 1996 – 2009

• Does the long term case for equities hold?

• Nowhere to hide?

• Strategy collapse?

• Confidence lost

• Banks blamed

• Fraud uncovered

• Litigation

Unprecedented?

1. Government

2. Regulator

3. Auditor

4. Rating agencies

5. Banks

6. Performance measurement

7. Fund manager due diligence

2008 – Questions asked of the roles of

Fiduciary responsibility

“The legal and practical scrutiny a fiduciary undergoes is tremendous, and it comes from multiple directions and for various reasons. It is likely that complaints and/or lawsuits alleging fiduciary misconduct will increase. Although some of these allegations may be entirely justified, most can be avoided by following the five step decision making process outlined in ‘Investment Ethos’.

Donald Trone – The Foundation for Fiduciary Studies

Investment Ethos – The five step decision making process

Source: Donald Trone, President The Foundation for Fiduciary StudiesSTEP Bermuda – November 2008

The Investment Policy Statement

Statement should cover:

• Level of expected return

• Level of risk

• Expected outcomes

• Restrictions

• Income requirements

• Tax considerations

• Time Horizon

Provides a detailed and concise instruction of what is expected

Wants?

Investment Manager

• Realistic expectations• Facility to manage• Fair appraisal

Investor

• Good risk adjusted performance• Confirmation• Peace of mind

Regulator

• Confirmation that risks are being identified and actions taken• Proof of process• Mitigation of jurisdiction reputational risk

Case Study 1 – Return and volatility

Source: Enhance Mosaic

Returns can look good, but do not identify risk

Case Study 1 –Return and volatility

Volatility is twice that of the benchmark…..

Source: Enhance Mosaic / E-MAP Report

Case Study 1 – Return and volatility

Source: Enhance Mosaic

Market corrects, high volatility, portfolio suffers sharp falls

Oversight of a single portfolio is one thing but how does a Trustee monitor a large number, say 50, investment portfolios?

• To a standard to which you would scrutinise your own investment portfolio

• Where there are possibly 50 different investment managers

• 50 different account opening documents

• 50 different mandates/strategies

• 50 different report formats

Process needs to be efficient and consistent

The challenge for the professional Trustee - Volume

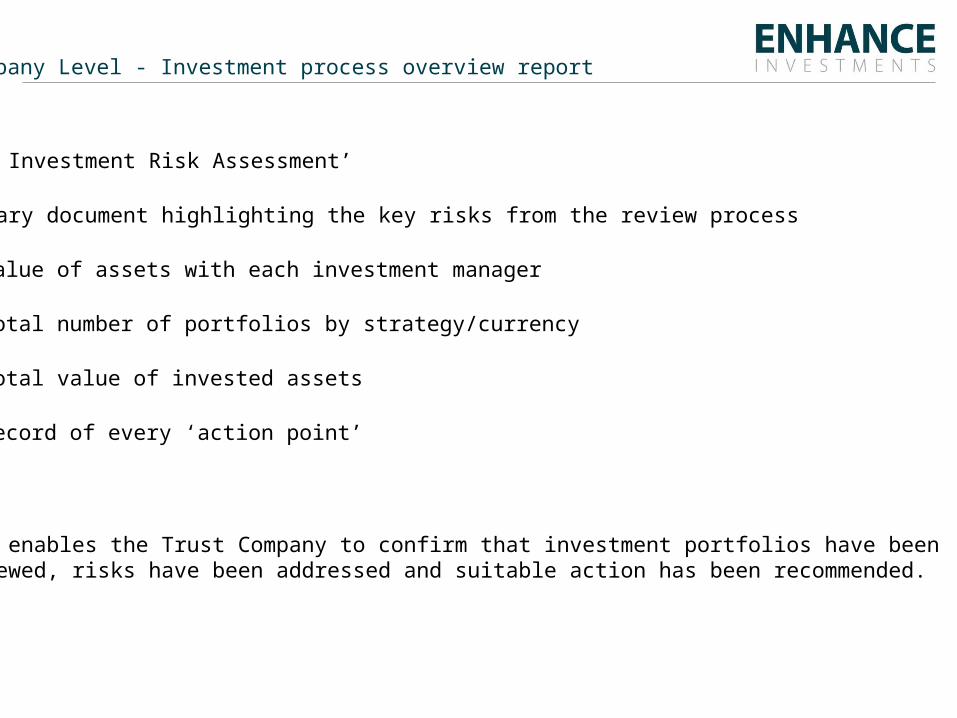

Company Level - Investment process overview report

‘The Investment Risk Assessment’

Summary document highlighting the key risks from the review process

• Value of assets with each investment manager

• Total number of portfolios by strategy/currency

• Total value of invested assets

• Record of every ‘action point’

This enables the Trust Company to confirm that investment portfolios have been reviewed, risks have been addressed and suitable action has been recommended.

• Are regular investment reviews performed?

• What is the frequency?

• How is the performance assessed?

• Are benchmarks used and how are they agreed?

• What action is taken if performance is unsatisfactory?

• Are reviews conducted in respect of all trusts or are they triggered by a specific event such as the receipt of valuations?

• Does the organisation employ specific staff to review investment performance or is an external supplier used?

• What level of expertise is available within the firm to review investment possibilities and the performance of managers?

• Is the process documented?

Jersey Financial Services Commission Key Themes – Investment Monitoring

Source: Letter from JFSC to Enhance April 2007

• Is there a documented process for the selection of an investment manager or advisor?

• Is there an approved list of investment managers?

• Has a beauty parade been undertaken?

• Are settlors acting as investment advisors? Are they properly qualified to do so?

• Are written investment objectives provided to the investment manager?

• Are there procedures for managing the potential conflict of interest where in-house investment products are selected?

• Is there transparency in relation to commissions received from managers?

JFSC – Key Themes - Selection of Investment Manager

Source: Letter from JFSC to Enhance April 2007

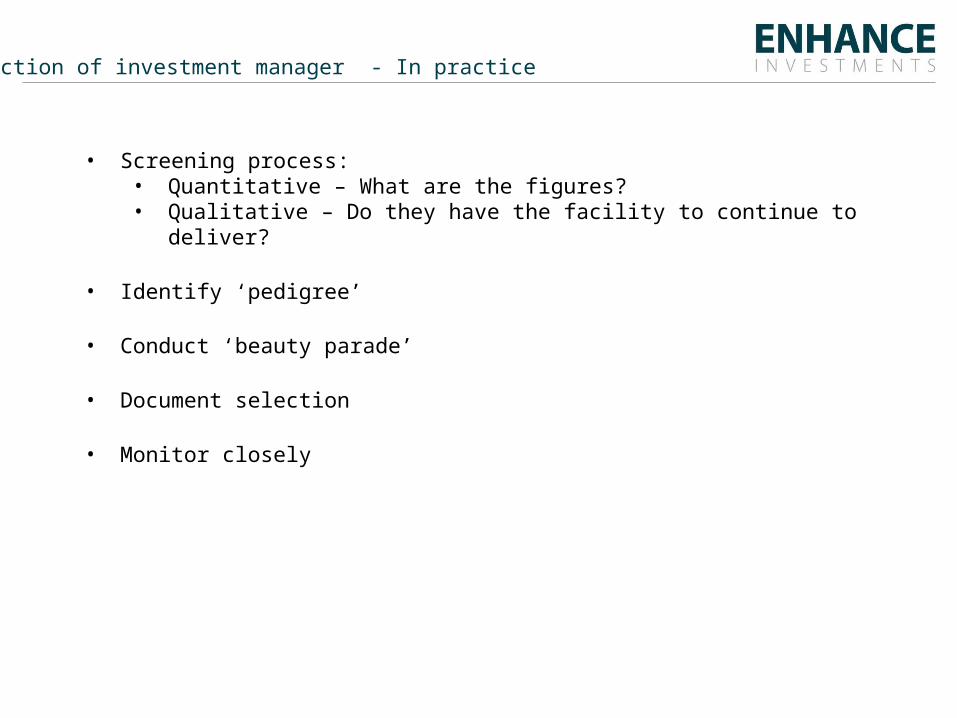

• Screening process:• Quantitative – What are the figures?• Qualitative – Do they have the facility to continue to deliver?

• Identify ‘pedigree’

• Conduct ‘beauty parade’

• Document selection

• Monitor closely

Selection of investment manager - In practice

Benchmark – The debate

• Subjective?

• Backward looking

• Does not address risk

• Index used as a benchmarks can be “net” not “gross”

• Composite indices can be complex

• Have they changed?

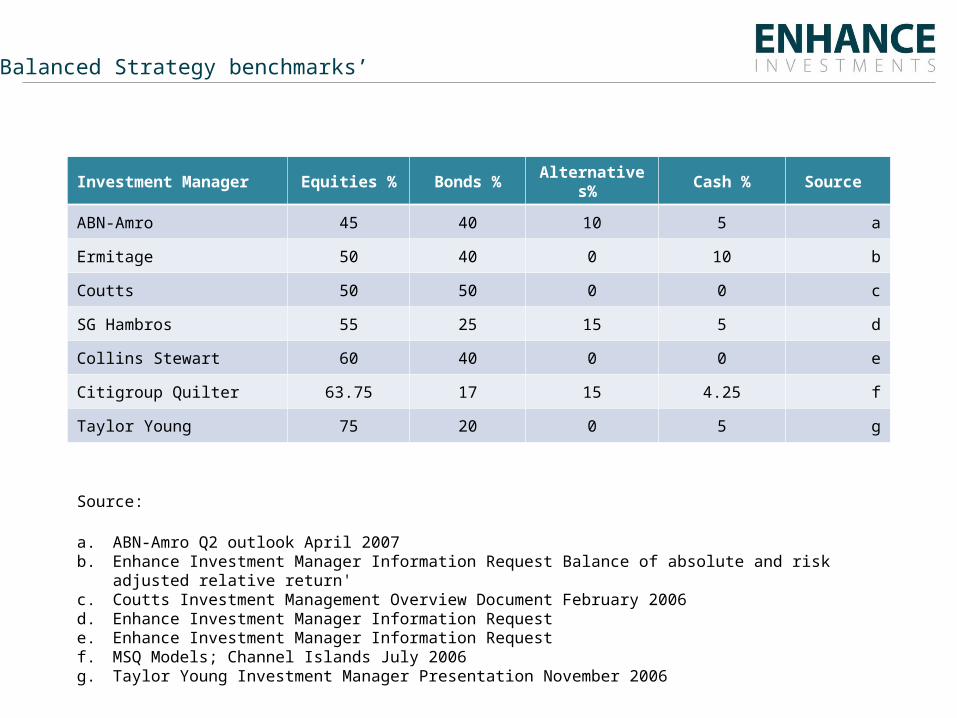

‘Balanced Strategy benchmarks’

Source:

a. ABN-Amro Q2 outlook April 2007b. Enhance Investment Manager Information Request Balance of absolute and risk adjusted

relative return'c. Coutts Investment Management Overview Document February 2006d. Enhance Investment Manager Information Requeste. Enhance Investment Manager Information Requestf. MSQ Models; Channel Islands July 2006g. Taylor Young Investment Manager Presentation November 2006

Investment Manager Equities % Bonds %Alternatives

% Cash % Source

ABN-Amro 45 40 10 5 a

Ermitage 50 40 0 10 b

Coutts 50 50 0 0 c

SG Hambros 55 25 15 5 d

Collins Stewart 60 40 0 0 e

Citigroup Quilter 63.75 17 15 4.25 f

Taylor Young 75 20 0 5 g

Case Study - 2 Qualitative risks – Recent examples

• Suitability – wrong or ineffective strategy

• Downgraded or junk bonds or subordinated debt

• Stock specific risk – 18% of portfolio value in RioTinto shares

• Sector specific risk – High bond and equity exposure to the financial sector

• Market specific risk – All investments are in the UK market

• Cash – Held on call with low interest rate

• Funds are suspended - Property

• Prices on valuation not up to date – ‘Autocall’ structured products

Case Study 3- Multiple Investment Managers – Diversification Failure

1. Structure - 2 existing portfolios

Portfolio 1 – Traditional portfolio – Growth strategy

Portfolio 2 – Traditional portfolio – Balanced Strategy

2. Third portfolio added to the structure

Portfolio 3 was added to provide an ‘absolute return strategy’ to compliment existing portfolios and provide better overall risk profile.

3. Investment manager for portfolio 3 used a ‘long/short’ strategy

Result: Correlation to equity increased rather than reduced

Conclusion: Right idea, wrong manager

Tools for successfully diversifying management – Position Risk

If Managers are duplicating trades diversification benefits may be reduced

Source: Enhance Consolidated Report

Conclusions

• Strong foundation – The Investment Policy Statement

• Open communication can have significant benefits for theprincipal/beneficiary, the fiduciary/trustee and the investment manager.

• Endorse

• Good performance

• Address• Direct risk –inappropriate holdings• Indirect risk –is the optimal strategy being applied?

• Provide peace of mind

“The financial services industry today offers more investment alternatives than ever before. Evaluating these offerings can be a confusing and overwhelming task since there are so many factors to consider. Among the most important factors are risk, cost, and suitability and it is these factors that are most litigated.”

Source: Golin Consulting

Final Thoughts

© Original Artist - Reproduction rights obtained from CSL

Sign of the times…..

Disclaimer

This document is for information purposes only and is not to be construed as a solicitation or an offer for financial services. The information contained herein is based on materials and sources that we believe to be reliable, however, EIL make no representation or warranty, either express or implied, in relation to the accuracy, completeness or reliability of the information contained herein. All opinions and estimates included in this document are subject to change without notice and EIL are under no obligation to update the information contained herein. None of EIL employees shall have any liability whatsoever for any indirect or consequential loss or damage arising from any use of this document. This document is issued by Enhance Investments Limited (EIL)Registered Office: 9 Hope Street, St Helier, Jersey JE2 3FX

Top Related