Languages

Pages

Legal

ACTIVITY BASED COSTING

EMBA SessionNovember 15,2012

Overview of Lecture

Review of cost behaviors Rationale for ABC approach Factors supporting an ABC system Cost flows Steps in implementation Examples Level of acceptance of ABC costing

Types of Costs

Fixed costs Variable costs Mixed costs

Relating Costs to Objectives Traceable costs

Direct labor Direct material

Allocated costs Fixed overhead Variable overhead

Traditional Allocation Method

Purchasing

Warehousing

Engineering

Maintenance Product B

Product A

Direct Labor Hours

Rational for ABC Approach

Single allocation rate not sufficient Currently many firms must target

price their products ABC assists in target pricing Advent of high speed computing

power made ABC feasible

Environmental Factors Supporting ABC Approach

High levels of competition Very diverse product mix Low cost of measurement for

additional data required

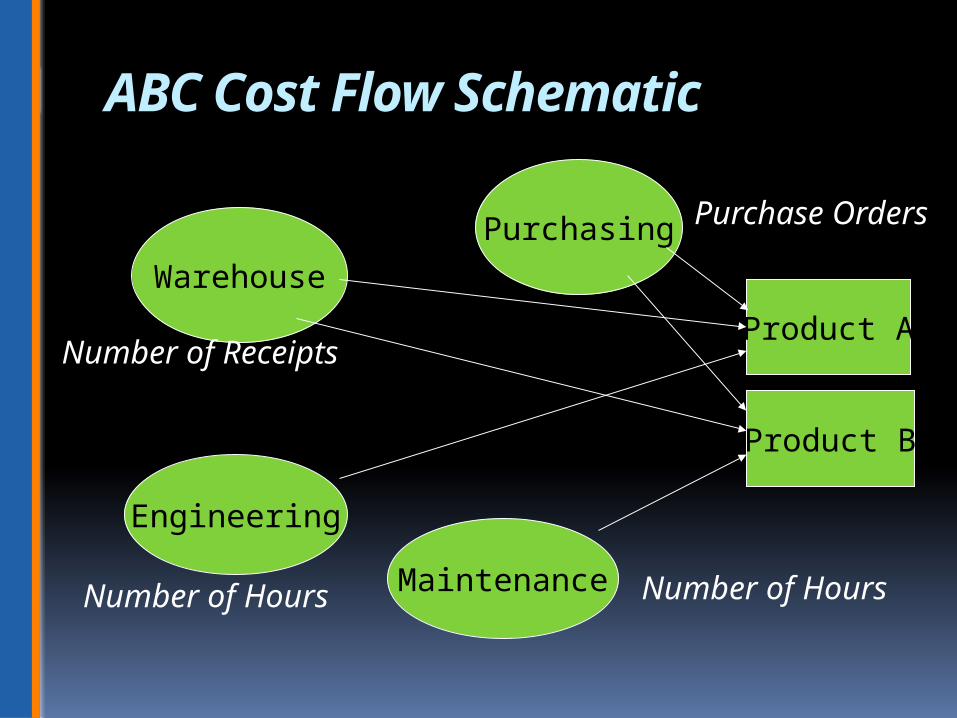

ABC Cost Flow Schematic

Warehouse

Maintenance

Purchasing

Engineering

Product A

Product B

Purchase Orders

Number of Receipts

Number of Hours Number of Hours

Implementation Steps

Identify the cost objectives Identify the direct costs of the

products Identify the overhead cost pools Select the appropriate drivers Test the assumptions Install

Example of Product Costing

Raw Material $150,000

15,000 Receipts

Purchased Parts$600,000

1,000 Receipts

Material Movements250,000

250 Setups

Product A Product B Product C Product D

Raw Materials Department$1,000,000

Allocation Using Single Driver

$1,000,000 16,000 Receipts = $62.50 per receipt

No. ofProduct Receipts Rate Allocated Cost

A 4,040 $62.50 $252,500 B 6,200 $62.50 387,500 C 2,000 $62.50 125,000 D 3,750 $62.50 235,000

16,000 $1,000,000

Calculation of Multiple Rates

No. of Per Cost Pool Pool Dollars Drivers Driver Driver

Raw Material $ 150,000 15,000 $10 Per ReceiptPurchased Parts 600,000 1,000 $600 Per Receipt

Material Handling 250,000 250 $1,000 Per Setup

$1,000,000

Products Number Rate Number Rate Number Rate

A 4,000 $10 40 $600 50 $1,000

B 6,000 $10 200 $600 80 $1,000

C 1,500 $10 500 $600 70 $1,000

D 3,500 $10 260 $600 50 $1,000

Totals 15,000 1,000 250

Raw Materials Purchased Parts Setups

Use of Activities by Products

Allocation to Products

A B C D Total

Raw Materials 40,000$ 60,000$ 15,000$ 35,000$ 150,000$

Purchased Parts 24,000 120,000 300,000 156,000 600,000

Material Handling 50,000 80,000 70,000 50,000 250,000

Totals 114,000$ 260,000$ 385,000$ 241,000$ 1,000,000$

Comparison of Two Methods

Product Traditional ABC Method Variance

A $ 252,500 $ 114,000 $ 138,500 Over

B 387,500 260,000 127,500 Over

C 125,000 385,000 260,000 Under

D 235,000 241,000 6,000 Under

Totals $1,000,000 $1,000,000 $ 0

Retail Example of ABC Costing

Traditional Allocation

Soft Fresh Package Drinks Produce Goods Totals

Percent of Sale 19.30% 51.20% 29.50% 100.00%

Sales 26,450$ 70,020$ 40,330$ 136,800$

Costs: Cost of Goods Sold 20,000 50,000 30,000 100,000 Store Support Costs 5,790 15,360 8,850 30,000 Totals 25,790 65,360 38,850 130,000

Operating Income 660$ 4,660$ 1,480$ 6,800$

Operating Income as Percent of Sales 0.0250 0.0666 0.0367 0.0497

Identify Cost Pools and Drivers

No. of Cost perActivity Driver Cost Pool Drivers Driver

Ordering # of P.O. $5,200 52 $100

Delivery # of Del. $8,400 105 $ 80

Stocking # of L.H. $5,760 280 $ 20

Cust. Sup. # of Items $10,240 51,200 .20

Bottle Return $400

Total $30,000

New Cost Drivers

Soft Fresh Package Activity Cost Per Driver Drinks Produce Goods Totals

Ordering $100 per P. O. 12 28 12 52

Delivery $80 per delivery 10 73 22 105

Stocking $20 per labor hour 18 180 90 288

Customer Support $.20 per item sold 4,200 36,800 10,200 51,200

Bottle Return Direct allocation $400 $400

Results Applying ABCSoft

DrinksFresh

ProducePackageGoods Totals

Sales 26,450$ 70,020$ 40,330$ 136,800$ Costs: Cost of sales 20,000 50,000 30,000 100,000 Bottle return 400 400 Ordering 1,200 2,800 1,200 5,200 Delivery 800 5,840 1,760 8,400 Stocking 360 3,600 1,800 5,760 Customer support 840 7,360 2,040 10,240 Totals 23,600 69,600 36,800 130,000

Operating Income 2,850$ 420$ 3,530$ 6,800$

Percent of Operating Income to Sales 0.1078 0.0060 0.0875 0.0497

Acceptance of ABC Costing

Approximately 60% of manufacturing firms in the US have tried ABC

10%-20% finally kept it in place Reasons for rejection:

Cost of gathering information Complexity outweighs usefulness Disagreement on proper drivers

Copyright by Frank Ilett, 2012

Top Related