Languages

Pages

Legal

Econometric Analysis of Financial Market Data1

ZONGWU CAI

E-mail address: [email protected]

Department of Mathematics & Statistics and Department of Economics,

University of North Carolina, Charlotte, NC 28223, U.S.A.

Wang Yanan Institute for Studies in Economics, Xiamen University, China

February 3, 2010

c©2010, ALL RIGHTS RESERVED by ZONGWU CAI

1This manuscript may be printed and reproduced for individual or instructional use, but maynot be printed for commercial purposes.

i

Preface

The main purpose of this lecture notes is to provide you with a foundation to pursue thebasic theory and methodology as well as applied projects involving the skills to analyzingfinancial data. This course also gives an overview of the econometric methods (models andtheir modeling techniques) applicable to financial economic modeling. More importantly, itis the ultimate goal of bringing you to the research frontier of the empirical (quantitative)finance. To model financial data, some packages will be used such as R, which is a veryconvenient programming language for doing homework assignments and projects. You candownload it for free from the web site at http://www.r-project.org/.

Several projects, including the heavy computer works, are assigned throughout the semester.The group discussion is allowed to do the projects and the computer related homework, par-ticularly writing the computer codes. But, writing the final report to each project or homeassignment must be in your own language. Copying each other will be regarded as a cheating.If you use the R language, similar to SPLUS, you can download it from the public web siteat http://www.r-project.org/ and install it into your own computer or you can use PCs atour labs. You are STRONGLY encouraged to use (but not limited to) the package R sinceit is a very convenient programming language for doing statistical analysis and Monte Carolsimulations as well as various applications in quantitative economics and finance. Of course,you are welcome to use any one of other packages such as SAS, MATLAB, GAUSS, andSTATA. But, I might not have an ability of giving you a help if doing so.

How to Install R ?

The main package used is R, which is free from R-Project for Statistical Computing.

(1) go to the web site http://www.r-project.org/;

(2) click CRAN;

(3) choose a site for downloading, say http://cran.cnr.Berkeley.edu;

(4) click Windows (95 and later);

(5) click base;

(6) click R-2.10.1-win32.exe (Version of December 14, 2009) to save this file first andthen run it to install (Note that the setup program is 32 megabytes and it is updatedalmost every three months).

The above steps install the basic R into your computer. If you need to install otherpackages, you need to do the followings:

(7) After it is installed, there is an icon on the screen. Click the icon to get into R;

(8) Go to the top and find packages and then click it;

ii

(9) Go down to Install package(s)... and click it;

(10) There is a new window. Choose a location to download packages, say USA(CA1),move mouse to there and click OK;

(11) There is a new window listing all packages. You can select any one of packages andclick OK, or you can select all of them and then click OK.

Data Analysis and Graphics Using R – An Introduction (109 pages)

I encourage you to download the file r-notes.pdf (109 pages) which can be downloadedfrom http://www.math.uncc.edu/˜ zcai/r-notes.pdf and learn it by yourself. Pleasesee me if any questions.

CRAN Task View: Empirical Finance

This CRAN Task View contains a list of packages useful for empirical work in Finance andit can be downloaded from the web site athttp://cran.cnr.berkeley.edu/src/contrib/Views/Finance.html.

CRAN Task View: Computational Econometrics

Base R ships with a lot of functionality useful for computational econometrics, in particularin the stats package. This functionality is complemented by many packages on CRAN. Itcan be downloaded from the web site athttp://cran.cnr.berkeley.edu/src/contrib/Views/Econometrics.html.

Contents

1 A Motivation Example 11.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Preliminary Statistical Analysis . . . . . . . . . . . . . . . . . . . . . . . . . 21.3 Jump-Diffusion Modeling Procedures . . . . . . . . . . . . . . . . . . . . . . 61.4 Pricing American-style Options Using Stratification Simulation Method . . . 81.5 Hedging Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101.6 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111.7 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2 Basic Concepts of Prices and Returns 132.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.2 Basic Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.2.1 Time Value of Money . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.2.2 Assets and Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152.2.3 Financial Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2.3 Statistical Features . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.3.1 Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.3.2 Frequency of Observations . . . . . . . . . . . . . . . . . . . . . . . . 172.3.3 Definition of Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.4 Stylized Facts for Financial Returns . . . . . . . . . . . . . . . . . . . . . . . 212.5 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 262.6 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3 Linear Time Series Models and Their Applications 313.1 Stationary Stochastic Process . . . . . . . . . . . . . . . . . . . . . . . . . . 323.2 Constant Expected Return Model . . . . . . . . . . . . . . . . . . . . . . . . 34

3.2.1 Model Assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 343.2.2 Regression Model Representation . . . . . . . . . . . . . . . . . . . . 343.2.3 CER Model of Asset Returns and Random Walk Model of Asset Prices 353.2.4 Monte Carlo Simulation Method . . . . . . . . . . . . . . . . . . . . . 363.2.5 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363.2.6 Statistical Properties of Estimates . . . . . . . . . . . . . . . . . . . . 38

3.3 AR(1) Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 383.3.1 Estimation and Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . 403.3.2 White Noise Hypothesis . . . . . . . . . . . . . . . . . . . . . . . . . 41

iii

CONTENTS iv

3.3.3 Unit Root . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 413.3.4 Estimation and Tests in the Presence of a Unit Root . . . . . . . . . 42

3.4 MA(1) Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 453.5 ARMA, ARIMA, and ARFIMA Processes . . . . . . . . . . . . . . . . . . . 45

3.5.1 ARMA(1,1) Process . . . . . . . . . . . . . . . . . . . . . . . . . . . 453.5.2 ARMA(p,q) Process . . . . . . . . . . . . . . . . . . . . . . . . . . . 463.5.3 AR(p) Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 483.5.4 MA(q) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 503.5.5 AR(∞) Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 523.5.6 MA(∞) Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 523.5.7 ARIMA Processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 523.5.8 ARFIMA Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

3.6 R Commands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563.7 Regression Models With Correlated Errors . . . . . . . . . . . . . . . . . . . 563.8 Comments on Nonlinear Models and Their Applications . . . . . . . . . . . . 563.9 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

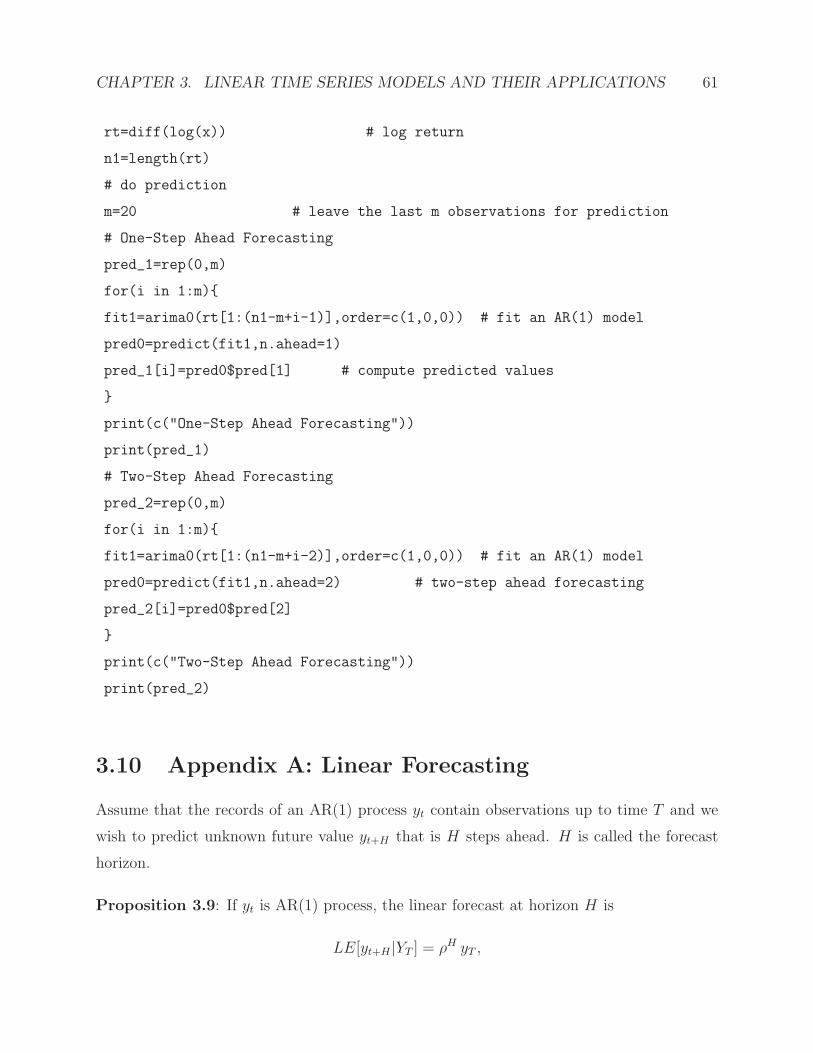

3.9.1 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 573.9.2 R Code . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

3.10 Appendix A: Linear Forecasting . . . . . . . . . . . . . . . . . . . . . . . . . 613.11 Appendix B: Forecasting Based on AR(p) Model . . . . . . . . . . . . . . . . 623.12 Appendix C: Random Variables . . . . . . . . . . . . . . . . . . . . . . . . . 643.13 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

4 Predictability of Asset Returns 694.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

4.1.1 Martingale Hypothesis . . . . . . . . . . . . . . . . . . . . . . . . 694.1.2 Tests of MD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

4.2 Random Walk Hypotheses . . . . . . . . . . . . . . . . . . . . . . . . . . . . 714.2.1 IID Increments (RW1) . . . . . . . . . . . . . . . . . . . . . . . . . . 714.2.2 Independent Increments (RW2) . . . . . . . . . . . . . . . . . . . . . 714.2.3 Uncorrelated Increments (RW3) . . . . . . . . . . . . . . . . . . . . . 724.2.4 Unconditional Mean is the Best Predictor (RW4) . . . . . . . . . . . 72

4.3 Tests of Predictability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 724.3.1 Nonparametric Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . 734.3.2 Autocorrelation Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . 764.3.3 Variance Ratio Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . 774.3.4 Trading Rules and Market Efficiency . . . . . . . . . . . . . . . . . . 80

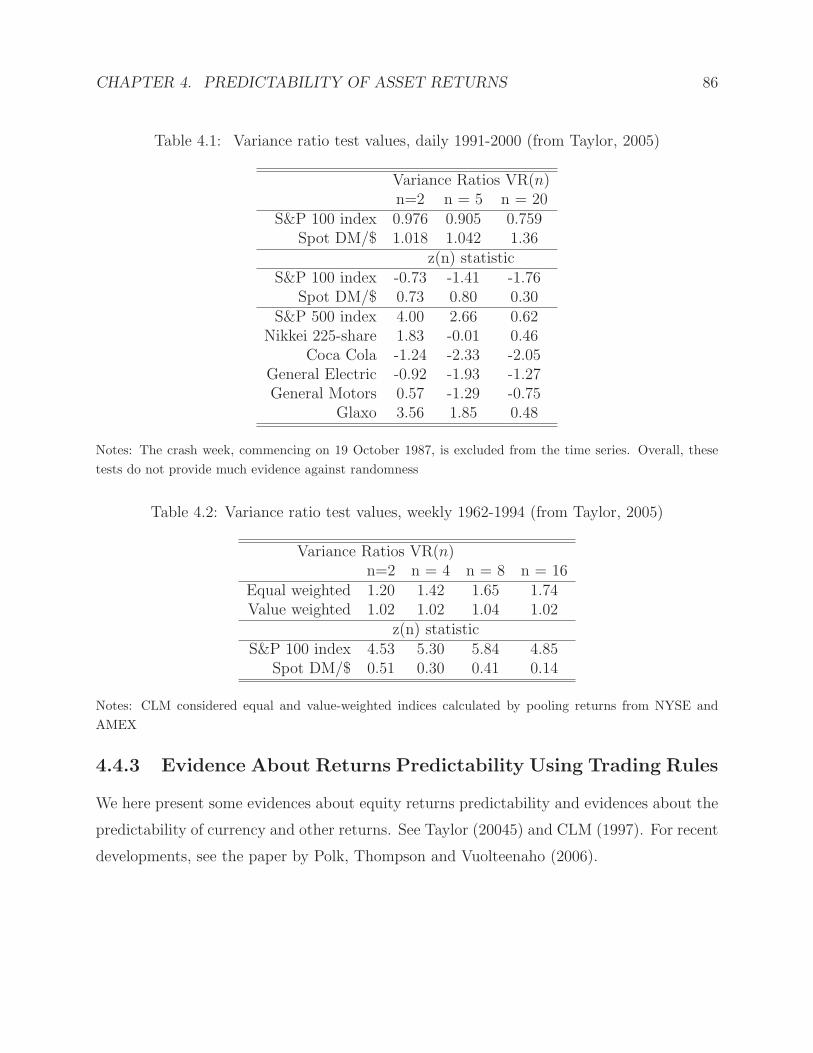

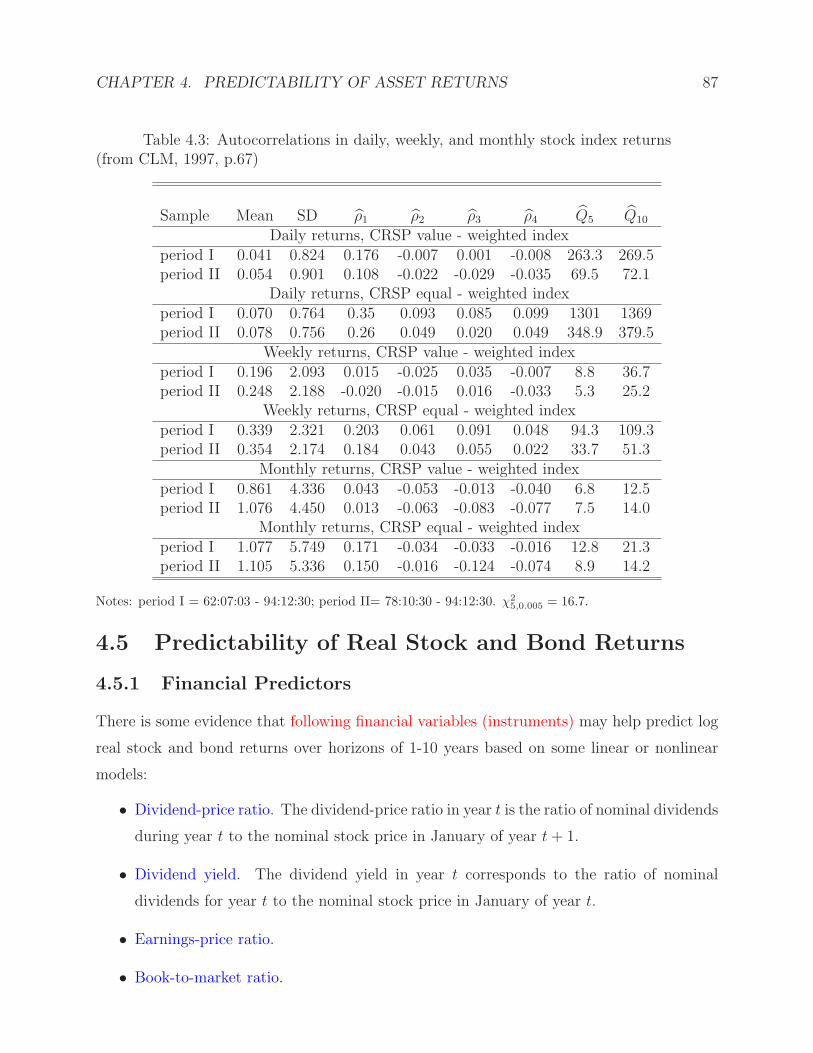

4.4 Empirical Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 844.4.1 Evidence About Returns Predictability Using VR and Autocorrelation Tests 844.4.2 Cross Lag Autocorrelations and Lead-Lag Relations . . . . . . . . . . 854.4.3 Evidence About Returns Predictability Using Trading Rules . . . . . 86

4.5 Predictability of Real Stock and Bond Returns . . . . . . . . . . . . . . . . . 874.5.1 Financial Predictors . . . . . . . . . . . . . . . . . . . . . . . . . . . 874.5.2 Models and Modeling Methods . . . . . . . . . . . . . . . . . . . . . 88

4.6 A Recent Perspective on Predictability of Asset Return . . . . . . . . . . . . 95

CONTENTS v

4.6.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 964.6.2 Conditional Means . . . . . . . . . . . . . . . . . . . . . . . . . . . . 964.6.3 Conditional Variances . . . . . . . . . . . . . . . . . . . . . . . . . . 984.6.4 Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 984.6.5 The future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

4.7 Comments on Predictability Based on Nonlinear Models . . . . . . . . . . . 1014.8 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

4.8.1 Exercises for Homework . . . . . . . . . . . . . . . . . . . . . . . . . 1014.8.2 R Codes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1024.8.3 Project #1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

4.9 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

5 Market Model 1115.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1115.2 Assumptions About Asset Returns . . . . . . . . . . . . . . . . . . . . . . . 1125.3 Unconditional Properties of Returns . . . . . . . . . . . . . . . . . . . . . . . 1125.4 Conditional Properties of Returns . . . . . . . . . . . . . . . . . . . . . . . . 1135.5 Beta as a Measure of Portfolio Risk . . . . . . . . . . . . . . . . . . . . . . . 1145.6 Diagnostics for Constant Parameters . . . . . . . . . . . . . . . . . . . . . . 1155.7 Estimation and Hypothesis Testing . . . . . . . . . . . . . . . . . . . . . . . 1165.8 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1165.9 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

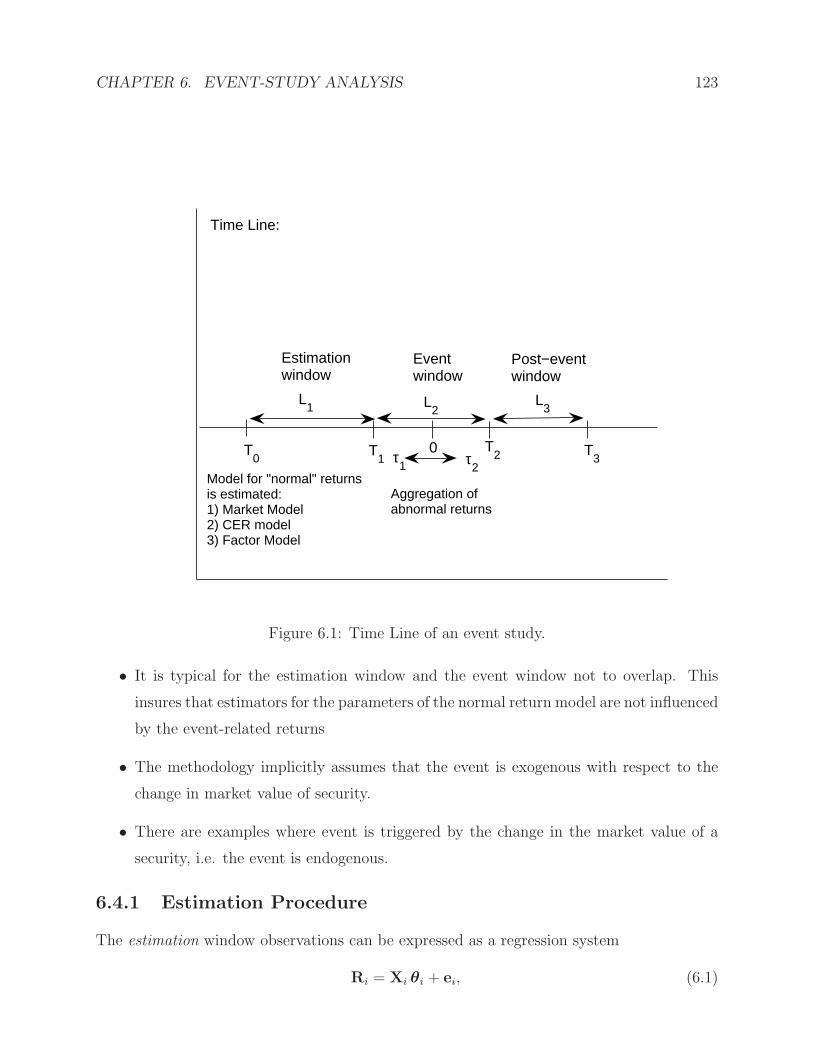

6 Event-Study Analysis 1196.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1196.2 Outline of an Event Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1206.3 Models for Measuring Normal Returns . . . . . . . . . . . . . . . . . . . . . 1216.4 Measuring and Analyzing Abnormal Returns . . . . . . . . . . . . . . . . . . 122

6.4.1 Estimation Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . 1236.4.2 Aggregation of Abnormal Returns . . . . . . . . . . . . . . . . . . . . 1246.4.3 Modifying the Null Hypothesis: . . . . . . . . . . . . . . . . . . . . . 1276.4.4 Nonparametric Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . 1276.4.5 Cross-Sectional Models . . . . . . . . . . . . . . . . . . . . . . . . . . 1296.4.6 Power of Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

6.5 Further Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1326.6 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1346.7 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135

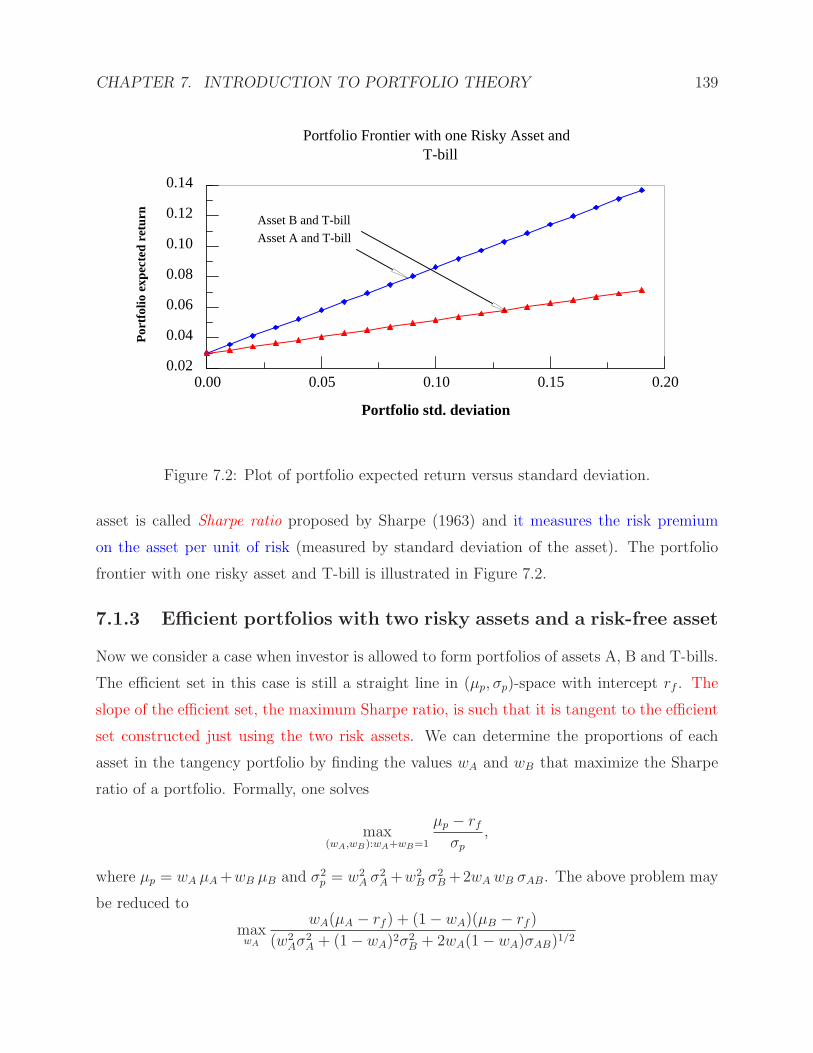

7 Introduction to Portfolio Theory 1367.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

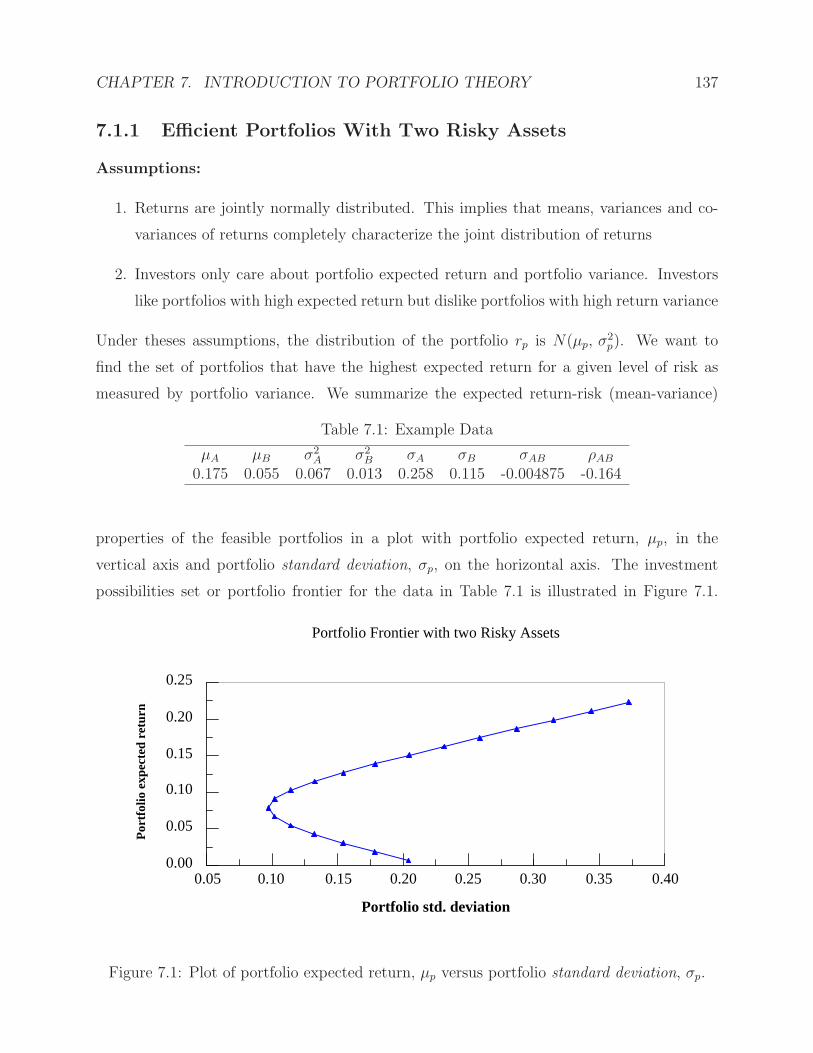

7.1.1 Efficient Portfolios With Two Risky Assets . . . . . . . . . . . . . . . 1377.1.2 Efficient Portfolios with One Risky Asset and One Risk-Free Asset . . 1387.1.3 Efficient portfolios with two risky assets and a risk-free asset . . . . . 139

7.2 Efficient Portfolios with N risky assets . . . . . . . . . . . . . . . . . . . . . 1407.3 Another Look at Mean-Variance Efficiency . . . . . . . . . . . . . . . . . . . 142

CONTENTS vi

7.4 The Black-Litterman Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 1447.4.1 Expected Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1447.4.2 The Black-Litterman Model . . . . . . . . . . . . . . . . . . . . . . . 1457.4.3 Building the Inputs . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

7.5 Estimation of Covariance Matrix . . . . . . . . . . . . . . . . . . . . . . . . 1477.5.1 Estimation Approaches . . . . . . . . . . . . . . . . . . . . . . . . . . 1487.5.2 Shrinkage estimator of the covariance matrix . . . . . . . . . . . . . . 1507.5.3 Recent Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

7.6 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1527.7 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

8 Capital Asset Pricing Model 1558.1 Review of the CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1558.2 Statistical Framework for Estimation and Testing . . . . . . . . . . . . . . . 157

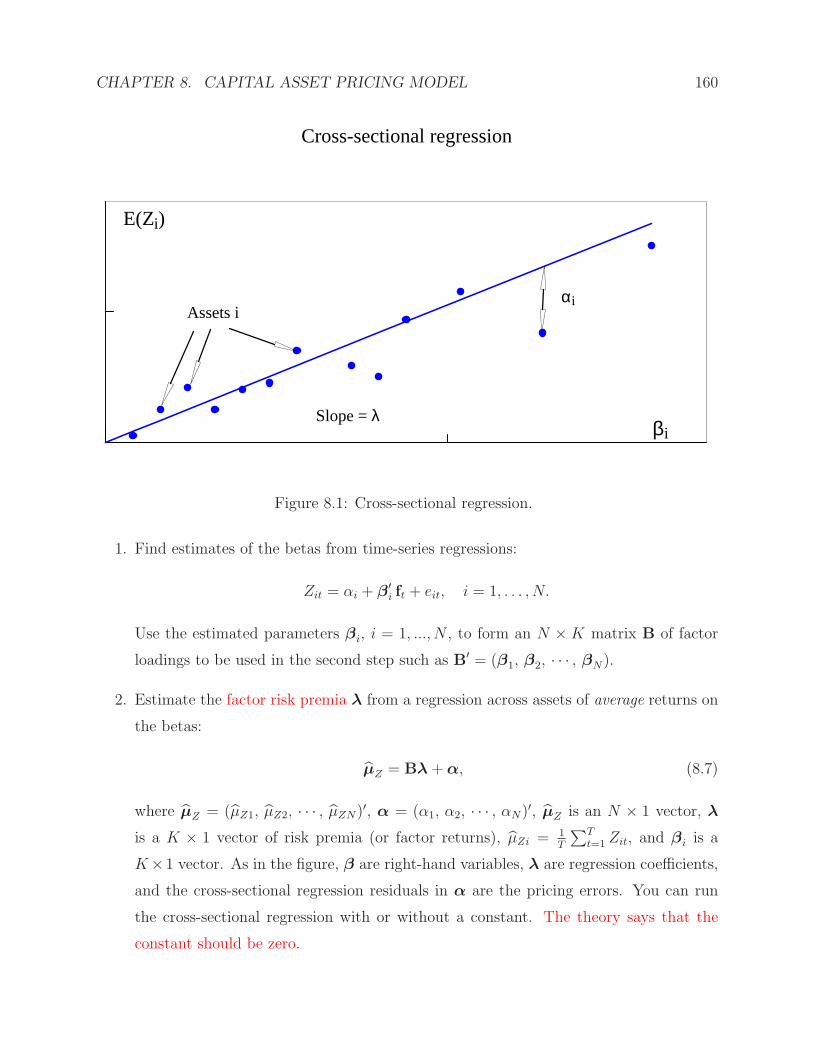

8.2.1 Time-Series Regression . . . . . . . . . . . . . . . . . . . . . . . . . . 1588.2.2 Cross-Sectional Regression . . . . . . . . . . . . . . . . . . . . . . . . 1598.2.3 Fama-MacBeth Procedure . . . . . . . . . . . . . . . . . . . . . . . . 162

8.3 Empirical Results on CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . 1638.3.1 Testing CAPM Based On Cross-Sectional Regressions . . . . . . . . . 1638.3.2 Return-Measurement Interval and Beta . . . . . . . . . . . . . . . . . 1658.3.3 Results of FF and KSS . . . . . . . . . . . . . . . . . . . . . . . . . . 165

8.4 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1668.5 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

9 Multifactor Pricing Models 1699.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

9.1.1 Why Do We Expect Multiple Factors? . . . . . . . . . . . . . . . . . 1699.1.2 The Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

9.2 Selection of Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1719.2.1 Theoretical Approaches . . . . . . . . . . . . . . . . . . . . . . . . . . 1719.2.2 Small and Value/Growth Stocks . . . . . . . . . . . . . . . . . . . . . 1719.2.3 Macroeconomic Factors . . . . . . . . . . . . . . . . . . . . . . . . . . 1729.2.4 Statistical Approaches . . . . . . . . . . . . . . . . . . . . . . . . . . 176

9.3 Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1799.4 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 180

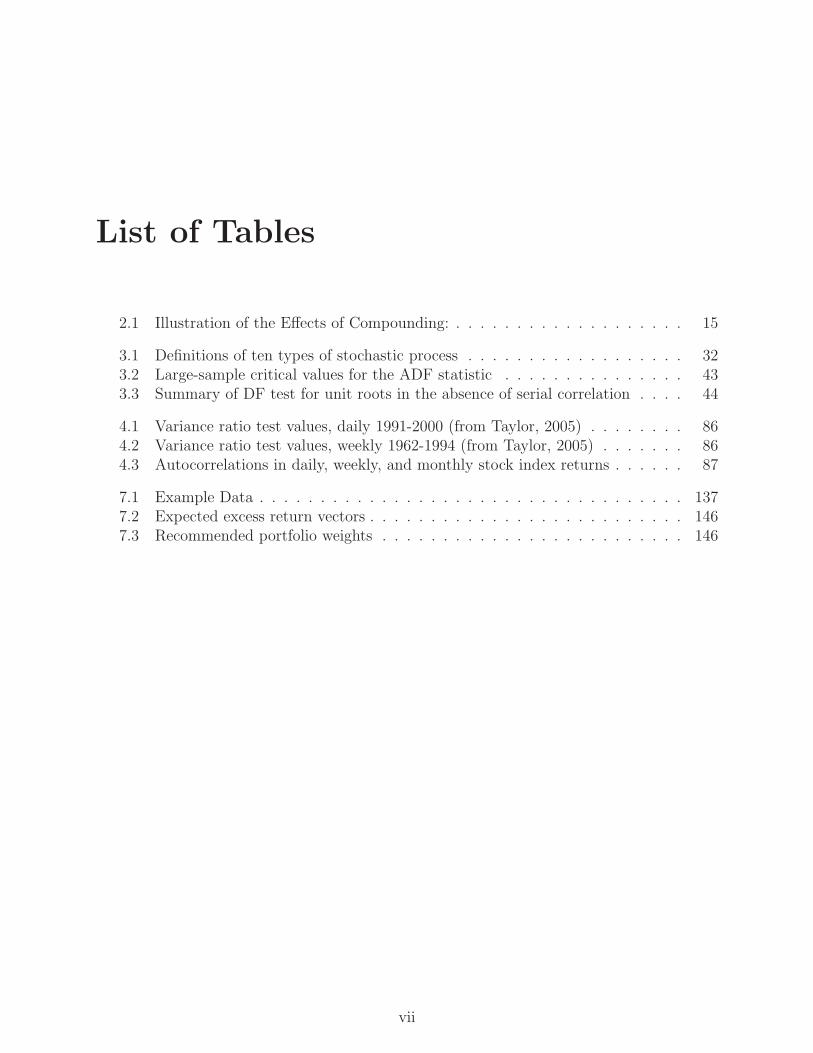

List of Tables

2.1 Illustration of the Effects of Compounding: . . . . . . . . . . . . . . . . . . . 15

3.1 Definitions of ten types of stochastic process . . . . . . . . . . . . . . . . . . 323.2 Large-sample critical values for the ADF statistic . . . . . . . . . . . . . . . 433.3 Summary of DF test for unit roots in the absence of serial correlation . . . . 44

4.1 Variance ratio test values, daily 1991-2000 (from Taylor, 2005) . . . . . . . . 864.2 Variance ratio test values, weekly 1962-1994 (from Taylor, 2005) . . . . . . . 864.3 Autocorrelations in daily, weekly, and monthly stock index returns . . . . . . 87

7.1 Example Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1377.2 Expected excess return vectors . . . . . . . . . . . . . . . . . . . . . . . . . . 1467.3 Recommended portfolio weights . . . . . . . . . . . . . . . . . . . . . . . . . 146

vii

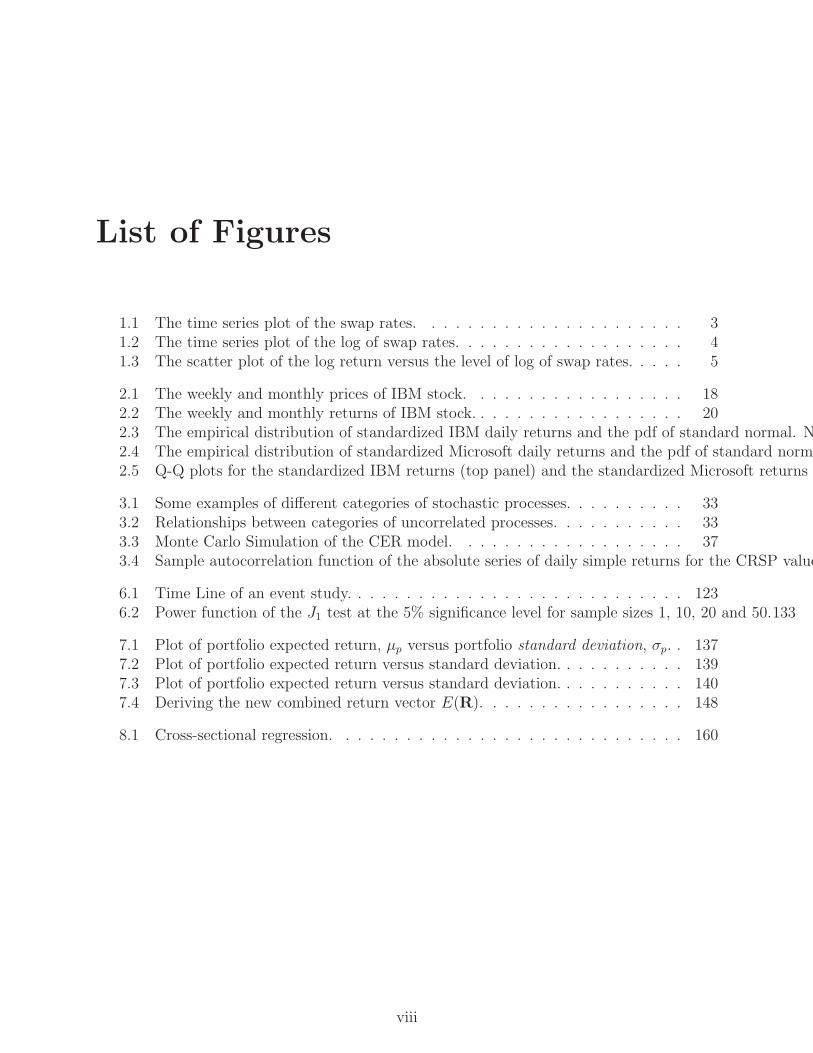

List of Figures

1.1 The time series plot of the swap rates. . . . . . . . . . . . . . . . . . . . . . 31.2 The time series plot of the log of swap rates. . . . . . . . . . . . . . . . . . . 41.3 The scatter plot of the log return versus the level of log of swap rates. . . . . 5

2.1 The weekly and monthly prices of IBM stock. . . . . . . . . . . . . . . . . . 182.2 The weekly and monthly returns of IBM stock. . . . . . . . . . . . . . . . . . 202.3 The empirical distribution of standardized IBM daily returns and the pdf of standard normal. Notice2.4 The empirical distribution of standardized Microsoft daily returns and the pdf of standard normal.2.5 Q-Q plots for the standardized IBM returns (top panel) and the standardized Microsoft returns (b

3.1 Some examples of different categories of stochastic processes. . . . . . . . . . 333.2 Relationships between categories of uncorrelated processes. . . . . . . . . . . 333.3 Monte Carlo Simulation of the CER model. . . . . . . . . . . . . . . . . . . 373.4 Sample autocorrelation function of the absolute series of daily simple returns for the CRSP value-w

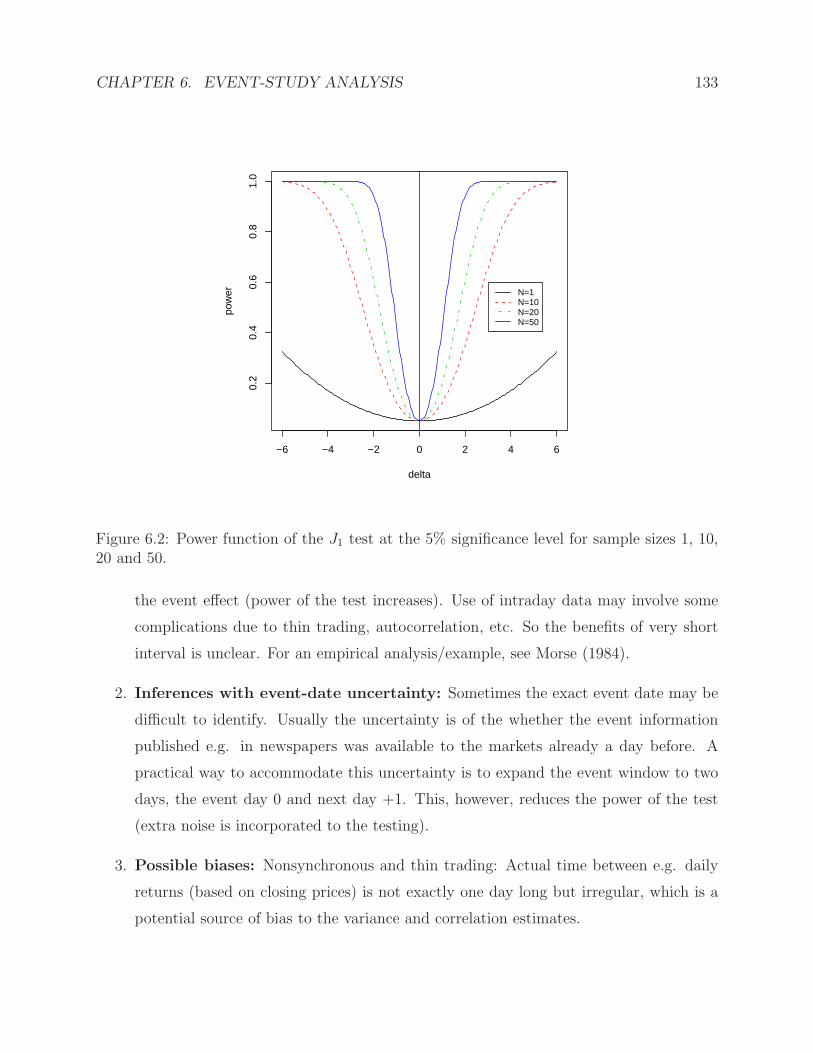

6.1 Time Line of an event study. . . . . . . . . . . . . . . . . . . . . . . . . . . . 1236.2 Power function of the J1 test at the 5% significance level for sample sizes 1, 10, 20 and 50.133

7.1 Plot of portfolio expected return, µp versus portfolio standard deviation, σp. . 1377.2 Plot of portfolio expected return versus standard deviation. . . . . . . . . . . 1397.3 Plot of portfolio expected return versus standard deviation. . . . . . . . . . . 1407.4 Deriving the new combined return vector E(R). . . . . . . . . . . . . . . . . 148

8.1 Cross-sectional regression. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

viii

Chapter 1

A Motivation Example

The purpose of this chapter is to present you, as a motivation example, a simple procedure

that can be used for proposing a reasonable jump-diffusion model for a real market data

(swap rates), calibrating parameters for the jump-diffusion model, and pricing American-

style options under the proposed jump-diffusion process. In addition, we will discuss hedging

issues for such options and sensitivity of parameters for American-style options.

1.1 Introduction

It is well known (see, e.g., Duffie (1996)) that under some regular conditions, there is

an equivalent martingale measure Q, such that for any European contingent claim on an

underlying Xt; t ≥ 0 without paying dividends with maturity T in the market, it can be

priced as follows:

P (0, T ) = EQ0

[exp

(−∫ T

0

r(s)ds

)g(XT , T )

], (1.1)

where g(·, ·) stands for the payoff function of underling for this contingent claim, P (0, T ) is

the claim’s arbitrage-free or fair price at time 0, rt is the riskless short-term interest rate,

and EQ0 [·] presents the expectation operator conditional on the information up to now.

For an American contingent claim on the same underlying with maturity T in the market,

it can be priced similarly:

P (0, T ) = supτ∈Γ

EQ0

[exp

(−∫ τ

0

r(s)ds

)g(Xτ , τ)

], (1.2)

where Γ is the collection of all stopping times less than the maturity time T . A comparison

of (1.1) with (1.2) reveals that the theory is similar but the computing for the American

option is much difficult.

1

CHAPTER 1. A MOTIVATION EXAMPLE 2

This theory provides us a “risk neutral” scheme to price any contingent claim. More

precisely, we can pretend to live a risk neutral world to modelling and calibrating parameters

using the data “lived” in the real world, then we do pricing using equation (1.1) or (1.2).

We will use this scheme throughout this paper.

In this chapter, we will present a simple procedure that can be used for proposing a

reasonable jump-diffusion model for a real market data, calibrating parameters for the jump-

diffusion model, and pricing American-style options under the proposed jump-diffusion pro-

cess. In addition, we will discuss hedging issues for such options and sensitivity of parameters

for American-style options. The remainder of the chapter is structured as follows. Section 2

presents some empirical properties of the data by graphing, mining data, and doing some pre-

liminary statistical analysis. Section 3 provides a jump-diffusion model based on the given

properties observed from Section 2, a calibration of parameters under this jump-diffusion

setting by MLE method, and a test for the existence of “jump”. Section 4 proposes a uni-

versal algorithm for American-style options with one-factor underlying model, and uses this

algorithm to price American option for the real data. Section 5 presents hedging issues for

the given American option. Section 6 concludes this chapter and discusses an extension of

our model to a more general tractable jump-diffusion setting called “affine jump-diffusion”

model proposed by Duffie, Pan and Singleton (2000).

1.2 Preliminary Statistical Analysis

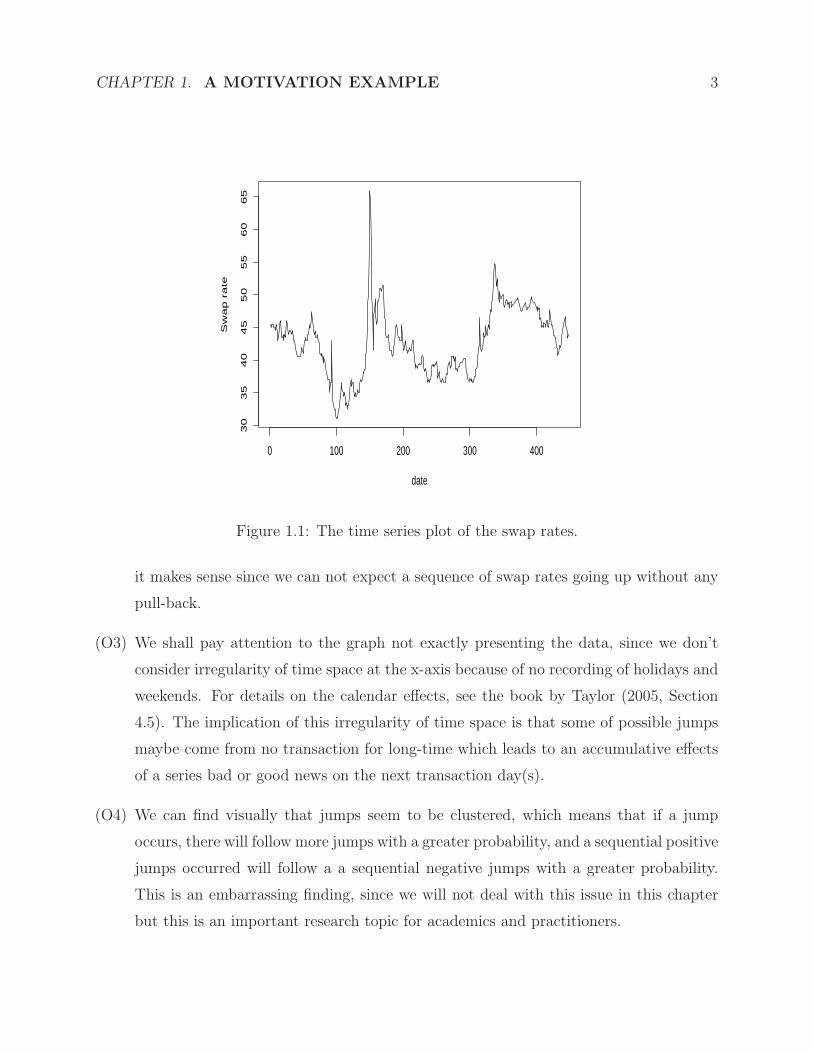

The data we will investigate is a collection of swap rates (the differences between 10 years

LIBOR rates and 10-year treasury bond’s yields) from December 19, 2002 to October 15,

2004. We can present the data graphically in Figure 1.1 by the time series plot. From the

graph, we observe the followings:

(O1) We can visually find there are some possible jumps for swap rates, and jumps seem

to have almost same frequencies for positive and negative jumps. In addition, from

economic standpoint of view, the difference of LIBOR and treasury yield should always

be positive since the former always includes some credit issues.

(O2) We can find “mean reversion” from the graph, which means a very high swap rate tends

to go lower, while a low swap rate tends to bounce back to a higher level. Economically,

CHAPTER 1. A MOTIVATION EXAMPLE 3

0 100 200 300 400

30

35

40

45

50

55

60

65

date

Sw

ap

ra

te

Figure 1.1: The time series plot of the swap rates.

it makes sense since we can not expect a sequence of swap rates going up without any

pull-back.

(O3) We shall pay attention to the graph not exactly presenting the data, since we don’t

consider irregularity of time space at the x-axis because of no recording of holidays and

weekends. For details on the calendar effects, see the book by Taylor (2005, Section

4.5). The implication of this irregularity of time space is that some of possible jumps

maybe come from no transaction for long-time which leads to an accumulative effects

of a series bad or good news on the next transaction day(s).

(O4) We can find visually that jumps seem to be clustered, which means that if a jump

occurs, there will follow more jumps with a greater probability, and a sequential positive

jumps occurred will follow a a sequential negative jumps with a greater probability.

This is an embarrassing finding, since we will not deal with this issue in this chapter

but this is an important research topic for academics and practitioners.

CHAPTER 1. A MOTIVATION EXAMPLE 4

A formal way to modelling a dynamic system for a necessary positive data is to modelling

the logarithm of the original data. The transformed data is graphed in Figure 1.2: Since our

0 100 200 300 400

3.6

3.8

4.0

4.2

date

Log

of S

wap

Rat

e

Figure 1.2: The time series plot of the log of swap rates.

objective is to modelling a dynamic mechanism of the evolution of swap rates, we propose a

general stochastic differential equation to the transformed variable (logarithm of swap rate)

which can usually be called “state” variable. Let St be the swap rate at time t, and denote

Xt as the logarithm of St, namely, Xt = log(St). The general stochastic differential equation

(SDE, or called Black-Scholes model) of Xt is as follows,

dXt = µ(Xt)dt+ σ(Xt)dWt + dJt, X0 = x0, (1.3)

where µ(·) (drift) and σ(·) (diffusion) stand for instantaneous mean function and volatility

function of the process respectively and Wt and Jt are a standard Brownian motion and a

pure jump process respectively.

The objective of modelling, in fact, is to specify the explicit forms of µ(·) and σ(·), andprobability mechanism of pure jump process Jt. In this section, we will have some idea about

the possible shape of σ(·) by a preliminary approximation of the SDE and the transformed

CHAPTER 1. A MOTIVATION EXAMPLE 5

data. First, for a very small time interval δt, the SDE can be approximated by a difference

equation (Euler approximation) as follows,

Xt+δt −Xt ≃ µ(Xt)δt+ σ(Xt)(Wt+δt −Wt) + (Jt+δt − Jt)

≃ σ(Xt)(Wt+δt −Wt) + (Jt+δt − Jt). (1.4)

The reason to omit the term µ(Xt)δt in the above equation is that this term is of the order

of o(1) while other two terms have a lower order. By (1.4), we can have a preliminary

visual sense of the form of σ(·) by looking at the graph of the transformed data with Xt as

x-coordinate and Xt+1 −Xt (log return) as y-coordinate; see Figure 1.3. The theory behind

3.6 3.8 4.0 4.2

−0

.2−

0.1

0.0

0.1

Level of log swap rate

Lo

g r

etu

rn

Figure 1.3: The scatter plot of the log return versus the level of log of swap rates.

this idea can be found in Stanton (1997) or Cai and Hong (2003). We will discuss this idea

in detail later. In the above figure, each horizontal line except x-axis represents the level of

number of standard deviations away from zero. Except some outliers which can be explained

partly by the existence of jumps in the system, most of data points fall within 3 standard

deviations away from 0. This figure intensively indicates that the variations (volatility) of

difference of Xt+1 and Xt for every level of Xt are almost same, which means it is reasonable

to assume that σ(·) is a constant function.

CHAPTER 1. A MOTIVATION EXAMPLE 6

1.3 Jump-Diffusion Modeling Procedures

By regularities observed in Section 2, we can specify our model under the so-called “equiva-

lent martingale measure” Q (see, e.g., Duffie (1996)) as follows:

(M1). We assume the volatility function σ(·) is a constant function, namely

σ(x) = σ, x ≥ 0 (1.5)

(M2). By (O2) in Section 2, we assume the instantaneous mean function µ(x) is an affine

function,

µ(x) = A(x− x), x ≥ 0, (1.6)

where x stands for long-term mean of the process, and A > 0 is the “speed” of process

back to the long-term mean x. We will explain more about these two parameters.

(M3). We assume the pure jump process Jt is a compound Poisson process independent

of continuous part of Xt and Wt; t ≥ 0 although this assumption might not be

necessary. More formally, we assume that the intensity of the Poisson process is a

constant λ and jump sizes are i.i.d with same distribution η. From (O1) in Section 2,

we can assume that η is a normal distribution, with mean 0, and standard deviation σJ

although the normality assumption on jump sizes might not be appropriate due to its

lack of fat-tail (One can assume that it follows a double exponential as in Kou (2002)

or Tsay (2002, 2005, Section 6.9)).

By assumptions (M1)-(M3) above, we can reformulate (1.3) as follows:

dXt = A(x−Xt)dt+ σdWt + dJt, X0 = x0, (1.7)

where the compensator measure of Jt, ν satisfies:

ν(de, dt) =λ√2πσ2

J

exp

(− e2

2σ2J

)dedt, (1.8)

and

EQ[dWt dJs] = 0, s, t ≥ 0. (1.9)

Using the Ito lemma for semi-martingale, we can solve the equation (1.7) explicitly. That

is, for any given times t and T (we always assume t ≤ T in the following), we have,

XT = Xte−A(T−t) + x

(1− e−A(T−t)

)+ e−A(T−t)

[σ

∫ T

t

eA(s−t)dWs +

∫ T

t

eA(s−t)dJs

].(1.10)

CHAPTER 1. A MOTIVATION EXAMPLE 7

By taking the expectation on both sides of (1.10), we obtain

EQ[XT ] = EQ[Xt]e−A(T−t) + x

(1− e−A(T−t)

). (1.11)

Since A > 0, when T − t → ∞, the first term on the right side of (1.11) will diminish to 0,

while EQ[XT ] → x with exponential rate A. These facts tell us why x is called “long-term

mean” and A is called the “speed” of process back to the long-term mean.

Suppose that the times of observations of the process are equally-spaced, namely, we

assume we observe the process at the regular times to observe data (Xt1 , Xt2 , . . . , XtN+1),

(for notational simplicity, we will denote Xn = Xtn for 1 ≤ n ≤ N + 1 ), where the equal

time interval is defined as ∆ = tn+1 − tn. Then (X1, X2, . . . , XN+1) follows an AR(1) model;

that is,

Xn+1 = a+ bXn + εn+1, 1 ≤ n ≤ N, (1.12)

where

a = x(1− e−A∆), b = e−A∆, (1.13)

and

εn ∼ σe−A∆

∫ ∆

0

eAsdWs + e−A∆

∫ ∆

0

eAsdJs i.i.d. (1.14)

Using (1.12), (1.13) and (1.14), to overcome “curse of dimensionality” for estimating pro-

cedure, we propose the so called “two-stage” estimating technique to obtain preliminary

estimate for parameters. Formally speaking, we first estimate parameters A and x by using

Weighted Least Square method, then use residuals to implement MLE estimating procedure

to estimate λ, σ and σJ . So only thing left we need to do is to find the probability density

function for εn, which is given by the following,

fεn(x) =e−λ∆

√σ2

2A(1− e−2A∆)

φ

x√

σ2

2A(1− e−2A∆)

+∞∑

k=1

e−λ∆λk

k!

∫ ∆

0

. . .

∫ ∆

0

1√σ2

2A(1− e−2A∆) +

∑kl=1 e

−2A(∆−sl)σ2J

×φ

x√

σ2

2A(1− e−2A∆) +

∑kl=1 e

−2A(∆−sl)σ2J

ds1 . . . dsk, (1.15)

where φ(x) = 1√2πe−

x2

2 , namely, the p.d.f of standard normal distribution.

CHAPTER 1. A MOTIVATION EXAMPLE 8

The two-stage estimate for parameters then can be numerically implemented. To estimate

parameters more efficiently, we shall use the whole MLE procedure using Newton-Raphson

algorithm with Two-Stage estimate as initial point of algorithm. Our Two-stage estimates

(based on daily) are as follows:

A = 0.03110101 x = 3.743758 σ = 0.01841 λ = 0.06385 σJ = 0.09299. (1.16)

Our whole MLE estimates (based on daily) are as follows:

A = 0.017124 x = 3.73213 σ = 0.018181 λ = 0.064548 σJ = 0.092432 (1.17)

Now we turn to testing whether the jump diffusion model is adequate. For testing pa-

rameters, we only do test for λ. Equivalently, it tests whether there are jumps for swap rates’

evolution. Remaining parameters’ test can be done similarly. This statistical hypothesis can

be formulated as follows:

H0 : λ = 0 versus H1 : λ > 0. (1.18)

We use the likelihood ratio method to test this hypothesis. It is well known that 2 times

the difference of two maximum log likelihoods converges asymptotically to a χ2-distribution

with degree of freedom equal to difference of dimensions of two parameter spaces. In this

hypothesis, the degree of freedom is 2 since λ = 0 makes σJ irrelevant to the process. We

find that p-value of test statistic is much less than 0.001, which means that H0 is rejected.

So a model for this dataset without jump could be inappropriate.

1.4 Pricing American-style Options Using Stratifica-

tion Simulation Method

To price an American option by using a simulation method (see, e.g., Glasserman, 2004),

it is always approximated by reducing the American option with intrinsic infinite exercise

opportunities into a “Bermudan” option with finite exercise opportunities. Suppose the ap-

proximated “Bermudan” option can be exercised only at a fixed set of exercise opportunities

t1 < t2 < . . . < tm, which are often equally spaced, and underlying process is denoted by

Xt; t ≥ 0. To reduce notation, we write Xti as Xi. Then, if Xt is a Markov process,

Xi; 0 ≤ i ≤ m is a Markov chain, where X0 denotes an initial state of the underlying. Let

hi denote the payoff function for exercise at ti, which is allowed to depend on i. Let Vi(x)

CHAPTER 1. A MOTIVATION EXAMPLE 9

denote the value of the option at ti given Xi = x. By assuming the option has not previ-

ously been exercised, we are ultimately interested in V0(X0). This value can be determined

recursively as follows:

Vm(x) = hm(x) (1.19)

and

Vi−1(x) = maxhi−1(x),E

Q[Di−1,i(Xi)Vi(Xi)|Xi−1 = x], (1.20)

where i = 1, 2, . . . ,m, and Di−1,i(Xi) stands for the discount factor from ti−1 to ti, which

could have the form as

Di−1,i(Xi) = exp

(−∫ ti

ti−1

r(u)du

). (1.21)

So for simulation, the main job will be on implementing (1.20), and main difficulty is also

at here. Actually, if the underlying state is of one dimension, for instance in our setting,

then we can efficiently implement (1.20) by stratification method. That is, we discretize not

only time-dimension but also state space. Formally speaking, for each exercise date ti, let

Ai1, . . . , Aibi be a partition of the state space of Xi into bi subsets. For the initial time 0,

take b0 = 1 and A01 = X0. Define transition probabilities

pij,k = PQ(Xi+1 ∈ Ai+1,k|Xi ∈ Aij) (1.22)

for all j = 1, . . . , bi, k = 1, . . . , bi+1, and i = 0, . . . ,m − 1. (This is taken to be 0 if

PQ(Xi ∈ Aij) = 0.) For each i = 1, . . . ,m and j = 1, . . . , bi, we also define

hi,j = EQ[hi(Xi)|Xi ∈ Aij] (1.23)

takeing this to be 0 if PQ(Xi ∈ Aij) = 0. Now we consider the backward induction

Vij = max

hij,

bi+1∑

k=1

pijkVi+1,k

(1.24)

for all j = 1, . . . , bi, k = 1, . . . , bi+1, and i = 0, . . . ,m − 1, initialized with Vmj = hmj. This

method takes the value V01 calculated through (1.24) as an approximation to V0(X0).

To implement this method, we need to do following steps:

(A1) Simulate a reasonably large number of replications of the Markov chainX0, X1, . . . , Xm.

(A2) Record N ijk, the number of paths that move from Aij to Ai+1,k, for all i = 0, . . . ,m−1,

j = 1, . . . , bi and k = 1, . . . , bi+1.

CHAPTER 1. A MOTIVATION EXAMPLE 10

(A3) Calculate the estimates

pij,k = N ij,k/(N

ij,1 + . . .+N i

j,bi) (1.25)

taking the ratio to be 0 whenever the denominator is 0. And calculate hi,j as the

average value of h(Xi) over those replications in which Xi ∈ Aij, taking it to be 0

whenever there is no path in which Xi ∈ Aij.

(A4) Set Vmj = hmj for all j = 1, . . . , bm, and recursively calculate

Vij = max

hij,

bi+1∑

k=1

pijkVi+1,k

(1.26)

for all j = 1, . . . , bi, and i = 0, . . . ,m− 1. Then V01 just be our estimate of V01.

For our example, the American-style option is defined with payoff function 1000000(exp(X)−K)+, where K = 44 bps, maturity T = 1 year, and initial price exp(X0) = 44 bps. Using

parameters presented on (1.17), we simulate 10000 paths with m = 400 exercise opportuni-

ties and decompose state-space into bi = 100 subsets. Then using the above algorithm, we

can approximate the American option price. Based on the simulation with 25 replications,

the mean value and standard deviation of approximates assuming that risk-free interest is

2.5% annually are as follows:

P = 781.762, and sP = 2.632. (1.27)

Note that the estimated value of price based on this jump model is quite close to the real

value.

1.5 Hedging Issues

In the previous implementation, we have assumed risk-free interest is 2.5% annually, and

parameters as presented in (1.17). In this Section, we consider hedging problems given these

parameters. We only discuss first order hedging for the American option. Denote P (S0)

the option price, where we have omitted all other parameters except initial swap rate in the

function of P (·). To do first hedging for the derivative is to find the value of ∂P∂S

(S0). We can

find this value numerically by using the Euler approximation, namely using first difference

ratio to approximate the partial derivative,

∂P

∂S(S0) ≃

P (S0 +∆S)− P (S0)

∆S(1.28)

CHAPTER 1. A MOTIVATION EXAMPLE 11

Then we can use simulation method to find P (S0+∆S) for sufficiently small ∆S so that we

can find an approximate “hedging ratio”. For our example, we let ∆S = ±0.25 bps. The

simulated “hedging ratio” is 0.2515. We can use similar technique to find other “Greek”s.

1.6 Conclusions

We present a whole procedure of modelling, estimating, pricing, and hedging for a real

data under a simple jump-diffusion setting. Some shortcomings are obvious in our setting,

since we don’t consider some issues which maybe important for the price of this option.

For instance, we assume interest rate is deterministic, and intensity λ of “jump event” is

constant. Most critically, we don’t deal with the issue observed on (O4) presented on Section

2. But, sometimes we need to compromise between accuracy and tractability in practice,

since calibrating a jump-diffusion model usually needs a large scale of calculating efforts. A

reasonable extension (still no touch on (O4)) to our model is to take so called “multi-factor”

models, which usually include interest rates, CPI, GDP growth rate, volatility, and other

economic variables as factors. See Duffie, Pan, Singleton (2000) for more details.

1.7 References

Cai, Z. and Y. Hong (2003). Nonparametric methods in continuous-time finance: A selectivereview. In Recent Advances and Trends in Nonparametric Statistics (M.G. Akritas andD.M. Politis, eds.), 283-302.

Duffie, D. (2001). Dynamic Asset Pricing Theory, 3th Edition. Princeton University Press,Princeton, NJ.

Duffie, D., J. Pan and K. Singleton (2000). Transform analysis and asset Pricing for affinejump-diffusion. Econometrica, 68, 1343-1376.

Glasserman, P. (2004). Monte Carlo Methods in Financial Engineering. Springer-Verlag,New York.

Kou, S.G. (2002). A jump diffusion model for option pricing. Management Science, 48,1086-1101.

Merton, R.C. (1976). Option pricing when underlying stock return are discontinuous.Journal of Financial Economics, 3, 125-144.

Stanton, R. (1997). A nonparametric model of term structure dynamics and the marketprice of interest rate risk. Journal of Finance, 52, 1973-2002.

CHAPTER 1. A MOTIVATION EXAMPLE 12

Taylor, S. (2005). Asset Price Dynamics, Volatility, And Prediction. Princeton UniversityPress, Princeton, NJ. (Chapter 4)

Tsay, R.S. (2005). Analysis of Financial Time Series, 2th Edition. John Wiley & Sons,New York.

Chapter 2

Basic Concepts of Prices and Returns

2.1 Introduction

Any empirical analysis of the dynamics of asset prices through time requires price data which

raise some of the questions:

1. The first question is where we can find the data. There are many sources of data includ-

ing web sites, commercial vendors, university research centers, and financial markets.

Here are some of them, listed below:

(a) CRSP: http://www.crsp.com (US stocks)

(b) Commodity Systems Inc: http://www.csidata.com (Futures)

(c) Datastream: http://www.datastream.com/product/has/ (Stocks, bonds, curren-

cies, etc.)

(d) IFM (Institute for Financial Markets): http://www.theifm.org (futures, US stocks)

(e) Olsen & Associates: http://www.olsen.ch (Currencies, etc.)

(f) Trades and Quotes DB: http://www.nyse.com/marketinfo (US stocks)

(g) US Federal Reserve: http://www.federalreserve.gov/releases (Currencies, etc.)

(h) Yahoo! (free): http://biz.yahoo.com/r/ (Stocks, many countries)

(i) For downloading the Chinese financial data, please see the file on my home page

http://www.math.uncc.edu/˜ zcai/finance-data.doc which is downloadable.

Further, the high frequency data (tick by tick data) can be downloaded from the

Bloomberg machine located at Room 33 of Friday Building on our campus but you

13

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 14

might ask Department of Finance for a help. Finally, you can download some data

through the web site at Wharton Research Data Services (WRDS)

http://wrds.wharton.upenn.edu/index.shtml, which our UNCC subscribes partially.

To log in WRDS, you need to have an account which can be obtained by contacting

Jon Finn through e-mail [email protected] or phone (704) 687-3156.

2. The second question is what the frequency of data is. It depends on what kind of

data you have and what kind of topics you are doing. For study of microstructure of

financial market, you need to have high frequency data. For most of studies, you might

need daily/weekly/monthly data.

3. The third one is how many periods (say, years) (the length) of data we need for analysis.

Theoretically, the larger sample size would be better but it might have structural

changes for a long sample period. In other words, the dynamics might change over

time.

4. The last one is how many prices for each period we wish to obtain and what kind of

price we need.

Answer: It depends on the purpose of your study.

2.2 Basic Definitions

First, we introduce some basic concepts, which you might be very familiar with.

2.2.1 Time Value of Money

Consider an amount $V invested for n years at a simple interest rate of r per annum (where

r is expressed as a decimal). If compounding takes place only at the end of the year, the

future value after n years is:

FVn = V × (1 + r)n.

If interest is paid m times per year then the future value after n years is:

FV mn = V × (1 +

r

m)m×n.

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 15

Table 2.1: Illustration of the Effects of Compounding:The Time Interval Is 1 Year and the Interest Rate is 10% per Annum.

Number Interest rateType of payments per period Net ValueAnnual 1 0.1 $1.10000

Semiannual 2 0.05 $1.10250Quarterly 4 0.025 $1.10381Monthly 12 0.0083 $1.10471Weekly 52 0.1/52 $1.10506Daily 365 0.1/365 $1.10516

Continuously ∞ exp(0.1) $1.10517

As m, the frequency of compounding, increases the rate becomes continuously compounded

and it can be shown that the future value becomes:

FV cn = lim

m→∞V × (1 +

r

m)m×n = V × exp(r × n), (2.1)

where exp(·) is the exponential function.

Example: Assume that the interest rate of a bank deposit is 10% per annum and the initial

deposit is $1.00. If the bank pays interest once a year, then the net value of the deposit

becomes $1(1+0.1)=$1.1 one year later. If the bank pays interest semi-annually, the 6-month

interest rate is 10%/2 = 5% and the net value is $1(1 0.1/2)2=$1.1025 after the first year.

In general, if the bank pays interest m times a year, then the interest rate for each payment

is 10%/m and the net value of the deposit becomes $1(1 0.1/m)m one year later. Table 2.1

gives the results for some commonly used time intervals on a deposit of $1.00 with interest

rate 10% per annum. In particular, the net value approaches $1.1052, which is obtained by

exp(0.1) and referred to as the result of continuous compounding.

2.2.2 Assets and Markets

Financial Assets:

1. Zero-Coupon Bond (discount bond). A zero-coupon bond with maturity date T pro-

vides a monetary unit at date T . At date t with t ≤ T , the zero-coupon bond has a

residual maturity of H = T − t and a price of B(t,H) (or B(t, T − t)), which is the

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 16

price at time t,

B(t, T ) =

(1 + r)−(T−t) pay at the end of maturity day(1 + r/m)−m(T−t) compounding with frequency mexp(−r(T − t)) continuous compounding

where r is the interest rate. In particular, B(0, T ) is the current, time 0 of the bond,

and B(T, T ) = 1 is equal to the face value, which is a certain amount of money that

the issuing institute (for example, a government, a bank or a company) promises to

exchange the bond for.

2. Coupon Bond. Bonds promising a sequence of payments are called coupon bonds. The

price pt at which the coupon bond is traded at any date t between 0 and the maturity

date T differs from the issuing price p0.

3. Stocks

4. Buying and Selling Foreign Currency

5. Options

6. More · · ·

For more details about bonds, see the book by Capinski and Zastawniak (2003).

2.2.3 Financial Theory

Basic theoretical concepts in financial theory (The best book for this aspect is the book by

Cochrane (2002)):

1. Equilibrium Models. (CAPM, CCAPM, market microstructure theory). Our focus

is only on the CAPM. Please read the paper by Cai and Kuan (2008) and the references

therein on the recent developments in the conditional CAP/APT models. Also, for the

market microstructure theory, please read Chapter 3 of Campbell, Lo and MacKinlay

(1997, CLM hereafter), or Part IV of Taylor (2005), or Chapter 5 of Tsay (2005).

2. Absence of Arbitrage Opportunity. The theory is based on the assumption that it

is impossible to achieve sure, strictly positive, gain with a zero initial endowment. This

assumption suggests imposing deterministic inequality restrictions on asses prices.

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 17

3. Actuarial Approach. This approach assumes a deterministic environment and em-

phasizes the concept of a fair price of financial asset.

Example: The price of stock at period 0 that provides future dividends d1, d2, . . . , dt at

predetermined dates 1, 2, . . . , t has to coincide with the discounted sum of future cash flows:

S0 =∞∑

t=1

dtB(0, t),

where B(0, t) is the price of the zero-coupon bond with maturity t (discount factor). The

actuarial approach is not confirmed by empirical research because it does not take into

account uncertainty.

2.3 Statistical Features

2.3.1 Prices

Prices: closing prices in stock market; currency exchange rates; option prices; more, · · ·.

2.3.2 Frequency of Observations

It depends on the data available and the questions that interest a researcher. The price

interval between prices should be sufficient to ensure that trade occurs in most intervals

and it is preferable that the volume of trade is substantial. Daily data are fine for most of

the applications. Also, it is important to distinguish the price data indexed by transaction

counts from the data indexed by time of associated transactions.

2.3.3 Definition of Returns

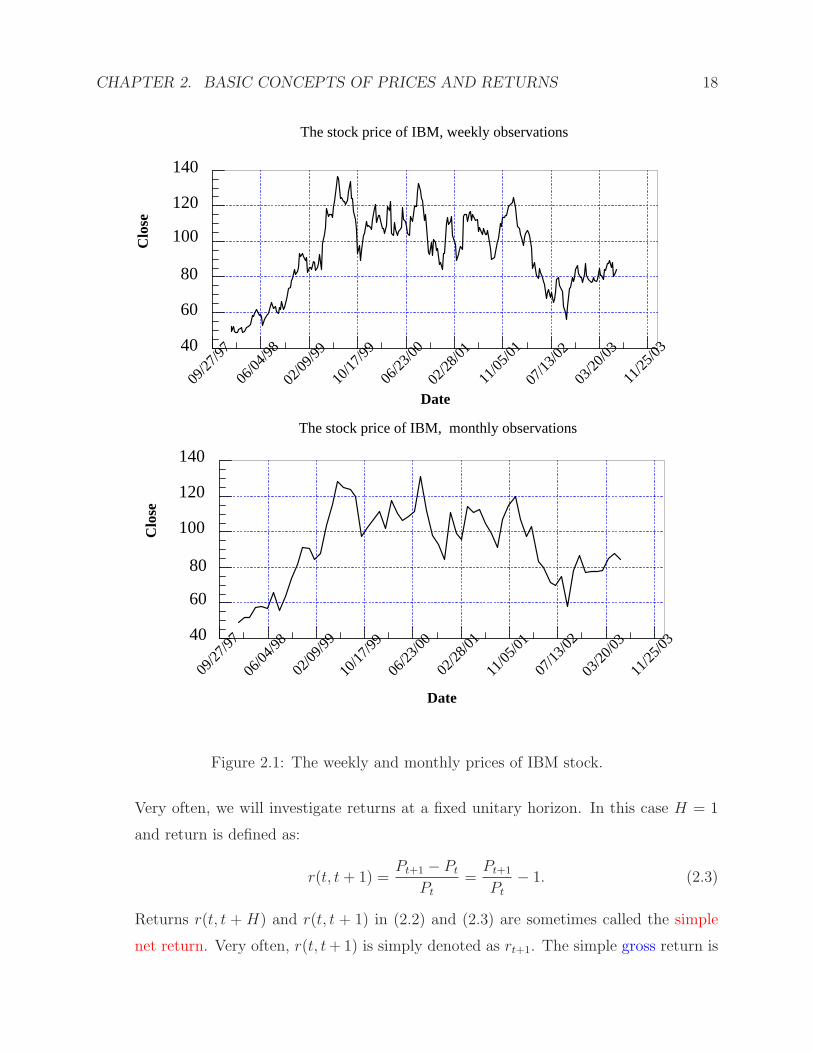

The statistical inference on asset prices is complicated because asset price might have non-

stationary behavior (upward and downward movements). One can transform asset prices

into returns, which empirically display more stationary behavior. Also, returns are scale-free

and not limited to the positiveness. You may notice the difference in the behavior of price

data and returns by looking at IBM prices and IBM returns in Figure 2.1 and Figure 2.2.

1. Return of a financial asset (stock) with price Pt at date t that produces no divi-

dends over the period (t, t+H) is defined as:

r(t, t+H) =Pt+H − Pt

Pt

(2.2)

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 18

Date

09/27

/9706

/04/98

02/09

/9910

/17/99

06/23

/0002

/28/01

11/05

/0107

/13/02

03/20

/0311

/25/03

Clo

se

40

60

80

100

120

140

The stock price of IBM, weekly observations

Date

09/27

/9706

/04/98

02/09

/9910

/17/99

06/23

/0002

/28/01

11/05

/0107

/13/02

03/20

/0311

/25/03

Clo

se

40

60

80

100

120

140

The stock price of IBM, monthly observations

Figure 2.1: The weekly and monthly prices of IBM stock.

Very often, we will investigate returns at a fixed unitary horizon. In this case H = 1

and return is defined as:

r(t, t+ 1) =Pt+1 − Pt

Pt

=Pt+1

Pt

− 1. (2.3)

Returns r(t, t + H) and r(t, t + 1) in (2.2) and (2.3) are sometimes called the simple

net return. Very often, r(t, t+1) is simply denoted as rt+1. The simple gross return is

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 19

defined as:

R(t, t+H) =Pt+H

Pt

= 1 + r(t, t+H).

Since Pt+H

Pt= Pt+H

Pt+H−1

Pt+H−1

Pt+H−2× . . . × Pt+1

Ptthe R(t, t+H) can be rewritten as:

R(t, t+H) =Pt+H

Pt+H−1

Pt+H−1

Pt+H−2

× . . . × Pt+1

Pt

= R(t+H − 1, t+H)×R(t+H − 2, t+H − 1)× . . . ×R(t, t+ 1)

=H∏

j=1

R(t+H − j, t+H + 1− j).

The simple gross return over H periods is the product of one period returns.

The formula in (2.3) is often replaced by the following approximation:

r(t, t+ 1) ≡ rt+1 ≈ ln(Pt+1)− ln(Pt) = ln

(Pt+1

Pt

)= ln(R(t, t+ 1)). (2.4)

The return in (2.4) is also known as continuously compounded return or log return. To

see why r(t, t+ 1) is called the continuously compounded return, take the exponential

of both sides of (2.4) and rearranging we get

Pt+1 = Pt exp(r(t, t+ 1)). (2.5)

By comparing (2.5) with (2.1) one can see that r(t, t + 1) is the continuously com-

pounded growth rate in prices between months t− 1 and t. Rearranging (2.4) one can

show that:

r(t, t+H) =H∑

j=1

r(t+H − j, t+H + 1− j).

2. Return of a financial asset (stock) with price Pt at date t that produces dividends

Dt+1 over the period (t, t+ 1) is defined as:

r(t, t+ 1) =Pt+1 +Dt+1 − Pt

Pt

=Pt+1 − Pt

Pt

+Dt+1

Pt

, (2.6)

where Dt+1/Pt is the ratio of dividend over price (d-p ratio), which is a very important

financial instrument for studying financial behavior.

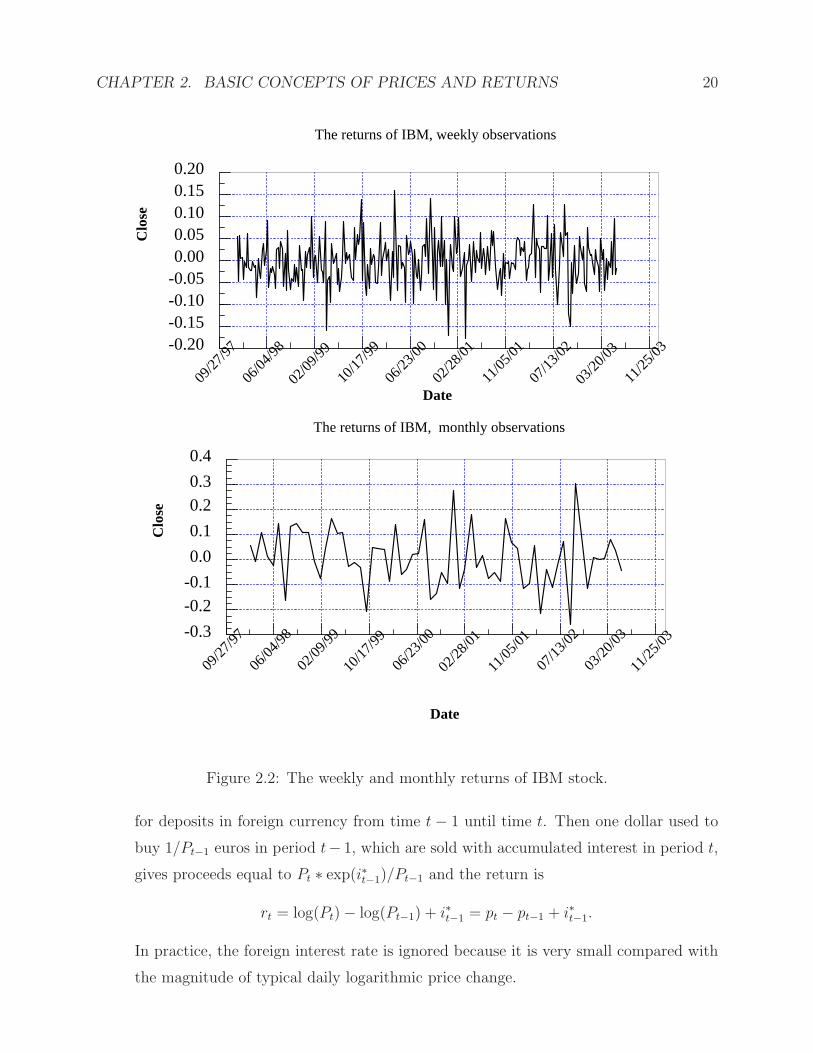

3. Spot currency returns. Suppose that Pt is the dollar price in period t for one unit

of foreign currency (say, euro). Let i∗t−1 be the continuously compounded interest rate

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 20

Date

09/27

/9706

/04/98

02/09

/9910

/17/99

06/23

/0002

/28/01

11/05

/0107

/13/02

03/20

/0311

/25/03

Clo

se

-0.20-0.15-0.10-0.050.000.050.100.150.20

The returns of IBM, weekly observations

Date

09/27

/9706

/04/98

02/09

/9910

/17/99

06/23

/0002

/28/01

11/05

/0107

/13/02

03/20

/0311

/25/03

Clo

se

-0.3

-0.2-0.1

0.0

0.1

0.20.3

0.4

The returns of IBM, monthly observations

Figure 2.2: The weekly and monthly returns of IBM stock.

for deposits in foreign currency from time t− 1 until time t. Then one dollar used to

buy 1/Pt−1 euros in period t− 1, which are sold with accumulated interest in period t,

gives proceeds equal to Pt ∗ exp(i∗t−1)/Pt−1 and the return is

rt = log(Pt)− log(Pt−1) + i∗t−1 = pt − pt−1 + i∗t−1.

In practice, the foreign interest rate is ignored because it is very small compared with

the magnitude of typical daily logarithmic price change.

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 21

4. Futures returns. Suppose Ft,T is the futures price in period t for delivery or cash set-

tlement in some later period T . As there are no dividend payouts on futures contracts,

the futures return is defined as:

rt = log(Ft,T )− log(Ft−1,T ) = ft,T − ft−1,T ,

where ft,T = log(Ft,T ).

5. Excess return is defined as the difference between the asset’s return and the return

on some reference asset. The reference asset is usually assumed to be riskless and in

practice is usually a short-term Treasury bill return. Excess return is defied as:

z(t, t+ 1) = zt+1 = r(t, t+ 1)− r0(t, t+ 1), (2.7)

where r0(t, t+ 1) is the reference return from period t to period t+ 1.

2.4 Stylized Facts for Financial Returns

When you have data, the first and very important step you need to do is to explore primarily

the data. That is; before you build models for the given data, you need to examine the data to

see what kind of key features the data have, to avoid the mis-specification, so that intuitively,

you have some basic ideas about the data and possible models for the given data. Here are

three important and common properties that are found in almost all sets of daily returns

obtained from a few years of prices:

1. The distribution of returns is not normal (do you believe this?), but it has

the following empirical properties:

• Stationarity. There are two definitions: weakly (second moment) stationary and

strictly stationary. The former is referred in most of applications. Question: How

to check stationarity?

• It is approximately symmetric. Sample estimates of skewness (µ3/σ3, where

µi is the ith central moment µi = E(rt−µ)i, µ is the mean, and σ2 is the variance)

for daily US stock returns tend to be negative for stock indices but close to zero

or positive for individual stocks.

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 22

• It has fat tails. Kurtosis (the ratio of the forth central moment over square of

the second central moment minus 3; that is, γ = µ4/µ22 − 3) for daily US stock

returns are large and positive for both indices and individual stocks which means

that returns have more probability mass in the tail areas than would be predicted

by a normal distribution (leptokurtic or γ > 0).

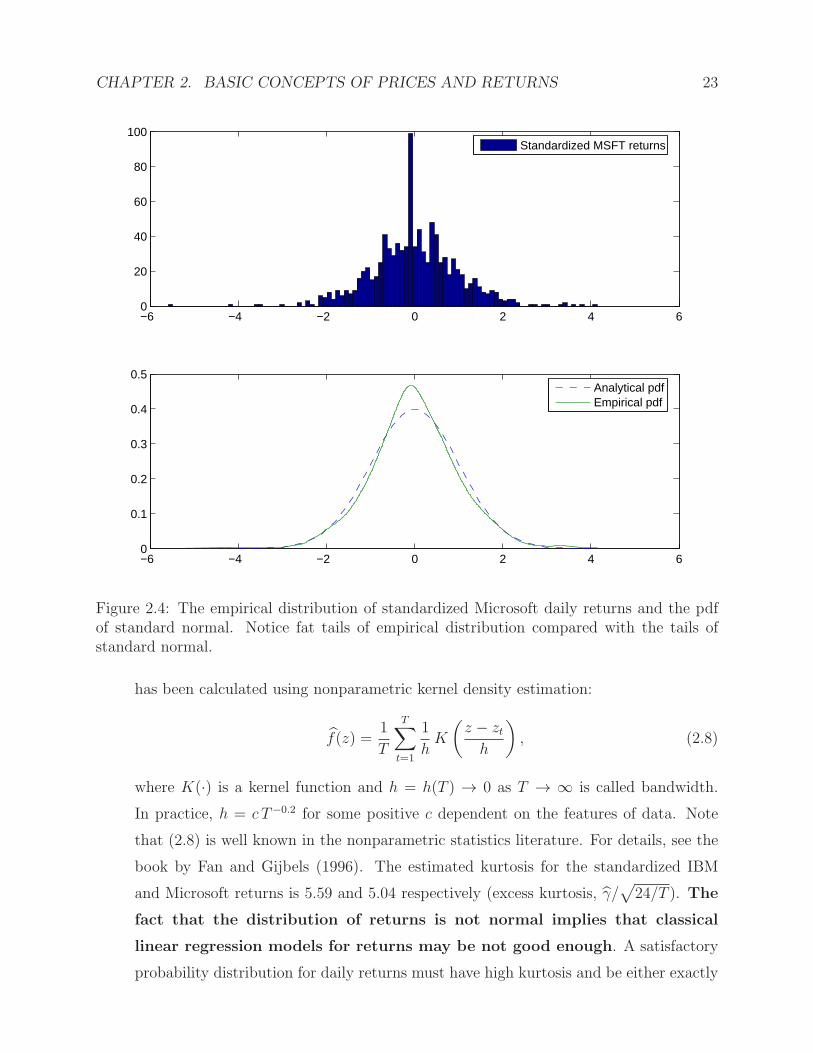

• It has a high peak. See Figure 2.3 for IMB daily returns by a comparison with

the standard norm.

Figures 2.3-2.4 compare empirical estimates of the probability distribution function

−6 −4 −2 0 2 4 60

20

40

60

80Standardized IBM returns

−6 −4 −2 0 2 4 60

0.1

0.2

0.3

0.4

0.5Analytical pdfEmpirical pdf

Figure 2.3: The empirical distribution of standardized IBM daily returns and the pdf of stan-dard normal. Notice fat tails of empirical distribution compared with the tails of standardnormal.

(pdf) of standardized IBM and Microsoft (MSFT) returns, zt = (rt − r)/σ, with the

probability density distribution of normal distribution. This empirical density estimate

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 23

−6 −4 −2 0 2 4 60

20

40

60

80

100Standardized MSFT returns

−6 −4 −2 0 2 4 60

0.1

0.2

0.3

0.4

0.5Analytical pdfEmpirical pdf

Figure 2.4: The empirical distribution of standardized Microsoft daily returns and the pdfof standard normal. Notice fat tails of empirical distribution compared with the tails ofstandard normal.

has been calculated using nonparametric kernel density estimation:

f(z) =1

T

T∑

t=1

1

hK

(z − zth

), (2.8)

where K(·) is a kernel function and h = h(T ) → 0 as T → ∞ is called bandwidth.

In practice, h = c T−0.2 for some positive c dependent on the features of data. Note

that (2.8) is well known in the nonparametric statistics literature. For details, see the

book by Fan and Gijbels (1996). The estimated kurtosis for the standardized IBM

and Microsoft returns is 5.59 and 5.04 respectively (excess kurtosis, γ/√

24/T ). The

fact that the distribution of returns is not normal implies that classical

linear regression models for returns may be not good enough. A satisfactory

probability distribution for daily returns must have high kurtosis and be either exactly

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 24

or approximately symmetric. Figure 2.5 displays the quantile-quantile (Q-Q) plots

for the standardized IBM returns (top panel) and the standardized Microsoft returns

(bottom panel). It is evident that the IBM and MSFT returns are not exactly normally

distributed. For more examples, see Table 1.2 (p. 11) and Figure 1.4 (p.19) in Tsay

(2005) or Table 4.6 and Figures 4.1 and 4.2 (pp 70-72) in Taylor (2005).

−4 −3 −2 −1 0 1 2 3 4−6

−4

−2

0

2

4

6

Standard Normal Quantiles

Qua

ntile

s of

Inpu

t Sam

ple

QQplot for standardized IBM returns

−4 −3 −2 −1 0 1 2 3 4−6

−4

−2

0

2

4

6

Standard Normal Quantiles

Qua

ntile

s of

Inpu

t Sam

ple

QQplot for standardized MSFT returns

Figure 2.5: Q-Q plots for the standardized IBM returns (top panel) and the standardizedMicrosoft returns (bottom panel).

Question 1: How to model the distribution of a return or returns? (A) Parametric

models; (B) Mixture models (see Section 4.8 in Taylor (2005) and Maheu and McCurdy

(2009)); (C) Nonparametric models.

Question 2: How do you know the distribution of a return belong to a particular family?

(A) Informative way to do a model checking using graphical methods, such as Q-Q plot;

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 25

(B) Official way is to do hypothesis testing; say Jarque-Bera test and Kolmogorov-

Smirnov tests or other advanced tests, say nonparametric versus parametric tests.

2. There is almost no correlation between returns for different days. Recall that

the correlation between returns τ periods apart is estimated from T observations by

the sample autocorrelation at lag τ :

ρτ =

∑T−τt=1 (rt − r)(rt+τ − r)∑T

t=1(rt − r)2

where r is the sample mean of all T observations. The command acf() in R is the plot

of ρτ versus τ , which is called the ACF plot.

To test H0 : ρ1 = 0, one can use the Durbin-Watson test statistic which is

DW =T∑

t=2

(rt − rt−1)2/

T∑

t=1

r2t .

Straightforward calculation shows that DW ≈ 2(1− ρ1), where ρ1 is the lag-1 ACF of

rt.

Consider testing that several autocorrelation coefficients are simultaneously zero, i.e.

H0 : ρ1 = ρ2 = . . . = ρm = 0. Under the null hypothesis, it is easy to show (see, Box

and Pierce (1970)) that

Q = T

m∑

k=1

ρ2k −→ χ2m. (2.9)

Ljung and Box (1978) provided the following finite sample correction which yields a

better fit to the χ2m for small sample sizes:

Q∗ = T (T + 2)m∑

k=1

ρ2kT − k

−→ χ2m. (2.10)

Both are called Q-test and well known in the statistics literature. Of course, they are

very useful in applications.

The function in R for the Ljung-Box test is

Box.test(x, lag = 1, type = c("Box-Pierce", "Ljung-Box"))

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 26

and the Durbin-Watson test for autocorrelation of disturbances is

dwtest(formula, order.by = NULL, alternative = c("greater","two.sided",

"less"),iterations = 15, exact = NULL, tol = 1e-10, data = list())

which is in the package lmtest.

3. The correlation between magnitudes of returns on nearby days are positive

and statistically significant. Functions of returns can have substantial autocorrela-

tions even though returns have very small autocorrelations. Usually, autocorrelations

are discussed for |rt|λ, λ = 1, 2. It is a stylized fact that there is positive dependence

between absolute returns on nearby days, and likewise for squared returns. See Section

4.10 in Taylor (2005) and Section 3.5.8.

The autocorrelations of absolute returns are always positive at a lag one day and

positive dependence continues to be found for several further lags. Squared returns

also exhibit positive positive dependence but to a lesser degree. The dependence

in absolute returns may be explained by volatility clustering or regime

switching or nonlinearity. See Section 4.9 in Taylor (2005).

4. Nonlinearity of the Returns Process. For example, Hong and Lee (2003) con-

ducted studies on exchange rates and they found that some of them are predictable

based on nonlinear time series models. There are many ongoing research activities in

this direction. See Chapter 4 in Tsay (2005) and Cai and Kuan (2008). If we have

time, we will spend some time in exploring further on this topic.

2.5 Problems

1. Download weekly (daily) price data for any two stocks, for example, IBM stock (P1t)

for 01/02/62 - 01/15/08 and for Microsoft stock (P2t) for 03/13/86 - 01/15/2008.

(a) Create a time series of continuously compounded weekly returns for IBM (r1t)

and for Microsoft (r2t).

(b) Use the constructed weekly returns to construct a series of monthly returns. You

may assume for simplicity that one month consists of four weeks.

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 27

(c) Construct a graph of stock price series (P1t, P2t) and returns series (r1t, r2t).

(d) Compute and graph the rolling estimates of the sample mean and variance for

stock prices and returns. In computation of rolling estimates, you may use the

last quarter of data (13 weeks).

NOTE: You either write code by yourself or use the build-in function in R. To use

the build-in function for the rolling analysis in R, you need to do the followings:

The first thing you need to do is to load fTrading, which is a package for RMetrics.

When you open R window, go to packages −→ local packages, and go down

to fTrading, and finally, double click it. After you load the package fTrading, the

command for the rolling analysis is

roll=rollFun(x,n,FUN=mean) # x is the series for the rolling

Or, you can use rapply or rollmean in the package zoo. To use the package zoo,

you need to load it first.

x1=zoo(x)

x2=rapply(x1,n,FUN=mean) # x is the series for the rolling

(e) What is the definition of a stationary stochastic process? Do prices look like a

stationary process? Why? Do returns look like a stationary process? Why?

(f) Compute autocorrelation coefficients ρk for 1 ≤ k ≤ 5 for prices and returns series.

To compute autocorrelation coefficients, you may use the program acf function in

R. This program is called as follows:

rho=acf(x,k, plot=F)

win.graph()

# open a graph window

plot(rho)

# make a plot

rho_value=rho$acf

# get the estimated $\rho$-values

print(rho_value)

# print the estmated $\rho$-values on screen

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 28

# where $x$ is a time-series vector (stock prices, stock returns,

# etc.), $k$ is the maximum lag considered ($5$ in this example).

(g) Based on the computed autocorrelations for IBM and MSFT stock prices and

returns, what can you say about correlation between stock prices for different

days? What can you say about correlation between stock returns for different

days?

(h) Using your stock returns for IBM and MSFT, rit, i = 1, 2, construct four more

series yit = |rit|λ, i = 1, 2 and λ = 1, 2. Compute autocorrelation coefficients

ρk for 1 ≤ k ≤ 5 for the newly constructed series. Compare the computed

correlations for |rit|λ, λ = 1, 2, and |rit|. Are results as you expected?

(i) Use the Jarque-Bera test (see Jarque and Bera (1980, 1987)) to test the assump-

tion of return normality for IBM and Microsoft stock returns.

NOTE: The Jarque-Bera test evaluates the hypothesis that X has a normal dis-

tribution with unspecified mean and variance, against the alternative that X does

not have a normal distribution. The test is based on the sample skewness and

kurtosis of X. For a true normal distribution, the sample skewness should be

near 0 and the sample kurtosis should be near 3. A test has the following general

form:

JB =T

6

(Sk +

(K − 3)2

4

)→ χ2

2,

where Sk and K are the measures of skewness and kurtosis respectively. To use

the build-in function for the Jarque-Bera test in R, you need to do the followings:

The first thing you need to do is to load tseries, which is a package for Time

Series and Computational Finance. When you open R window, go to packages

−→ local packages, and go down to tseries, and finally, double click it. After

you load the package tseries, the command for the Jarque-Bera test is

jb=jarque.bera.test(x) # x is the series for the test

print(jb)

Alternatively, you can also use the Kolmogorov-Smirnov tests as

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 29

ks.test(x, y, ..., alternative = c("two.sided", "less", "greater"),

exact = NULL)

To use Kolmogorov-Smirnov tests, you need to standardize the data first.

2. Use R program to estimate the probability density function (see (2.8)) of standardized

IBM and MSFT stock returns zit, zit = (rit − ri)/σi, where ri and σi are the sample

mean and standard deviation of ri, i = 1, 2. The program R is called as follows:

Suppose that Z is a vector of standardized stock returns,

y0=density(Z, m=100, from=-3, to=3)

# m is the number of grid points from interval (from, to)

y1=y0$y

# get estimated density vaules at m grid points

x0=seq(-3,3,length=100)

# set the vaules for m grid points

win.graph()

matplot(x0,cbind(y1,dnorm(x0)),type="l", lty=c(1,2),xlab="",ylab="")

# make a plot with two graphs

win.graph()

qqnorm(Z)

qqline(Z,col=2)

# make a Q-Q plot of Z

# where $y1$ is a vector of estimated probabilities at $m=100$

# grid points from $-3$ to $3$. Compare the empirical distribution

# with a graph of standard normal distribution.

(a) Estimate and construct a graph of the estimated probability density function for

IBM and Microsoft stock returns:

(b) On the same graph with the empirical density, construct a graph of the standard

normal density function. Comment your results.

(c) Construct QQ-plot for standardized IBM and MSFT returns. You may use the

R command for this. Comment your results.

CHAPTER 2. BASIC CONCEPTS OF PRICES AND RETURNS 30

2.6 References

Box, G. and D. Pierce (1970). Distribution of residual autocorrelations in autoregressiveintegrated moving average time series models. Journal of the American StatisticalAssociation, 65, 1509-1526.

Cai, Z. and C.-M. Kuan (2008). Time-varying betas models: A nonparametric analysis.Working paper, Department of Mathematics and Statistics, University of North Car-olina at Charlotte.

Campbell, J. Y., A.W. Lo and A.C. MacKinlay (1997). The Econometrics of FinancialMarkets. Princeton University Press, Princeton, NJ. (Chapter 1).

Capinski, M. and T. Zastawniak (2003). Mathematics for Finance. Springer-Verlag, Lon-don.

Cochrane, J.H. (2002). The Asset Pricing Theory. Princeton University Press, Princeton,NJ. (financial theory)

Hong, Y. and T.-H. Lee (2003). Inference on via generalized spectrum and nonlinear timeseries models. The Review of Economics and Statistics, 85, 1048-1062.

Gourieroux, C. and J. Jasiak (2001). Financial Econometrics: Problems, Models, andMethods. Princeton University Press, Princeton, NJ. (Chapter 1)

Fan, J. and I. Gijbels (1996). Local Polynomial Modeling and Its Applications. London:Chapman and Hall.

Jarque, C.M. and A.K. Bera (1980). Efficient tests for normality, homoscedasticity andserial independence of regression residuals. Economics Letters, 6, 255-259.

Jarque, C.M. and A.K. Bera (1987). A test for normality of observations and regressionresiduals. International Statistical Review, 55, 163-172.

Ljung, G. and G. Box (1978). On a measure of lack of fit in time series models. Biometrika,66, 67-72.

Maheu, J.M. and T.H. McCurdy (2009). How Useful are Historical Data for Forecastingthe Long-Run Equity Return Distribution? Journal of Business & Economic Statistics,27, 95-112.

Taylor, S. (2005). Asset Price Dynamics, Volatility, And Prediction. Princeton UniversityPress, Princeton, NJ. (Chapters 1-4)

Tsay, R.S. (2005). Analysis of Financial Time Series, 2th Edition. John Wiley & Sons,New York. (Chapter 1)

Zivot, E. (2002). Lecture Notes on Applied Econometric Modeling in Finance. The weblink is: http://faculty.washington.edu/ezivot/econ483/483notes.htm

Chapter 3

Linear Time Series Models and TheirApplications

In this chapter, we discuss basic theories of linear time series analysis, introduce some simple

econometric models useful for analyzing financial time series, and apply the models to asset

returns. Discussions of the concepts are brief with emphasis on those relevant to financial

applications. Understanding the simple time series models introduced here will go a long

way to better appreciate the more sophisticated financial econometric models of the later

chapters. There are many time series textbooks available. For basic concepts of linear time

series analysis, see Box, Jenkins, and Reinsel (1994, Chapters 2 and 3) and Brockwell and

Davis (1996, Chapters 1).

Treating an asset return (e.g., log return rt of a stock) as a collection of random vari-

ables over time, we have a time series rt. Linear time series analysis provides a natural

framework to study the dynamic structure of such a series. The theories of linear time series

discussed include stationarity, dynamic dependence, autocorrelation function, modeling, and

forecasting. The econometric models introduced include

(a) simple autoregressive (AR) models,

(b) simple moving-average (MA) models,

(c) mixed autoregressive moving-average (ARMA) models,

(d) a simple regression model (constant expected return model) with time series errors,

and

(f) differenced models (ARIMA).

For an asset return rt , simple models attempt to capture the linear relationship between rt

and information available prior to time t. The information may contain the historical values

31

CHAPTER 3. LINEAR TIME SERIES MODELS AND THEIR APPLICATIONS 32

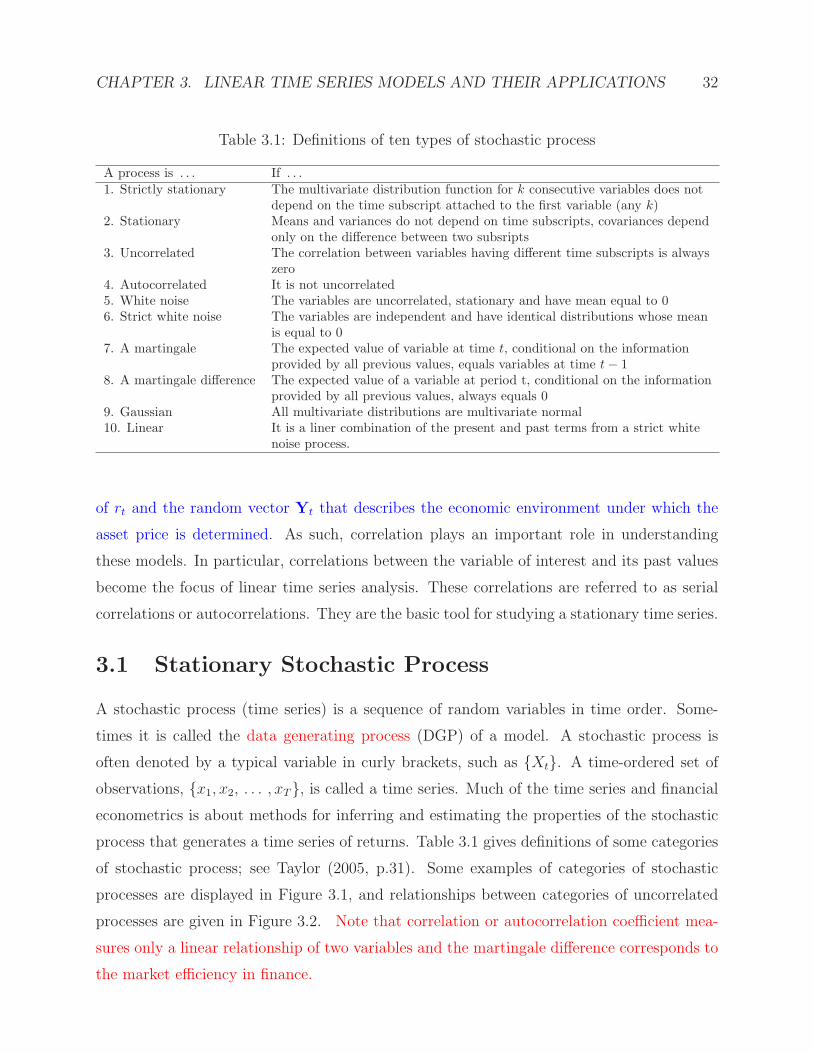

Table 3.1: Definitions of ten types of stochastic process

A process is . . . If . . .1. Strictly stationary The multivariate distribution function for k consecutive variables does not

depend on the time subscript attached to the first variable (any k)2. Stationary Means and variances do not depend on time subscripts, covariances depend

only on the difference between two subsripts3. Uncorrelated The correlation between variables having different time subscripts is always

zero4. Autocorrelated It is not uncorrelated5. White noise The variables are uncorrelated, stationary and have mean equal to 06. Strict white noise The variables are independent and have identical distributions whose mean

is equal to 07. A martingale The expected value of variable at time t, conditional on the information

provided by all previous values, equals variables at time t− 18. A martingale difference The expected value of a variable at period t, conditional on the information

provided by all previous values, always equals 09. Gaussian All multivariate distributions are multivariate normal10. Linear It is a liner combination of the present and past terms from a strict white

noise process.

of rt and the random vector Yt that describes the economic environment under which the

asset price is determined. As such, correlation plays an important role in understanding

these models. In particular, correlations between the variable of interest and its past values

become the focus of linear time series analysis. These correlations are referred to as serial

correlations or autocorrelations. They are the basic tool for studying a stationary time series.

3.1 Stationary Stochastic Process

A stochastic process (time series) is a sequence of random variables in time order. Some-

times it is called the data generating process (DGP) of a model. A stochastic process is

often denoted by a typical variable in curly brackets, such as Xt. A time-ordered set of

observations, x1, x2, . . . , xT, is called a time series. Much of the time series and financial

econometrics is about methods for inferring and estimating the properties of the stochastic

process that generates a time series of returns. Table 3.1 gives definitions of some categories

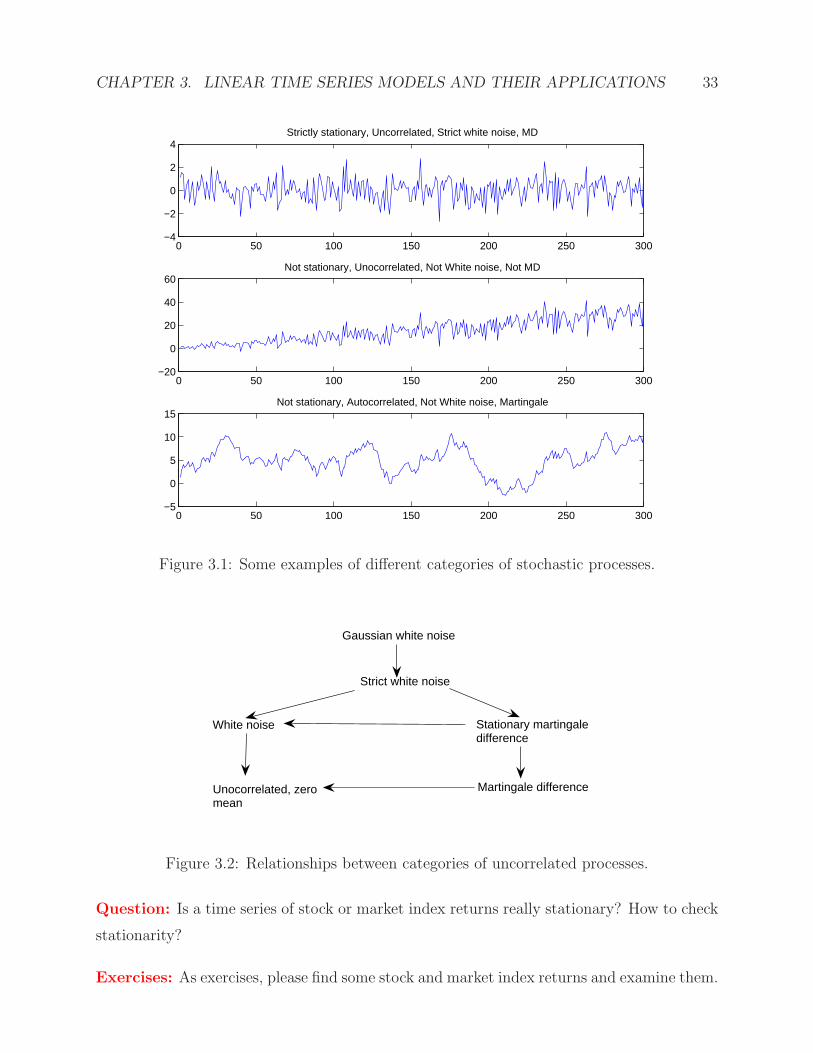

of stochastic process; see Taylor (2005, p.31). Some examples of categories of stochastic

processes are displayed in Figure 3.1, and relationships between categories of uncorrelated

processes are given in Figure 3.2. Note that correlation or autocorrelation coefficient mea-

sures only a linear relationship of two variables and the martingale difference corresponds to

the market efficiency in finance.

CHAPTER 3. LINEAR TIME SERIES MODELS AND THEIR APPLICATIONS 33

0 50 100 150 200 250 300−4

−2

0

2

4Strictly stationary, Uncorrelated, Strict white noise, MD

0 50 100 150 200 250 300−20

0

20

40

60Not stationary, Unocorrelated, Not White noise, Not MD

0 50 100 150 200 250 300−5

0

5

10

15Not stationary, Autocorrelated, Not White noise, Martingale

Figure 3.1: Some examples of different categories of stochastic processes.

Gaussian white noise

Strict white noise

Stationary martingaledifference

White noise

Unocorrelated, zeromean

Martingale difference

Figure 3.2: Relationships between categories of uncorrelated processes.

Question: Is a time series of stock or market index returns really stationary? How to check

stationarity?

Exercises: As exercises, please find some stock and market index returns and examine them.

CHAPTER 3. LINEAR TIME SERIES MODELS AND THEIR APPLICATIONS 34

Try to make conclusions by yourself to see what you can make. Also, similar to Figures 3.1

and 3.2, please simulate various time series (different types and different sample sizes) and

make the time series plot for them to make some feelings about them intuitively.

3.2 Constant Expected Return Model

Although this model is very simple and might not be appropriate for applications, it allows

us to discuss and develop important econometric topics such as estimation and hypothesis

testing. We will touch with some sophisticated and modern models later but they require

much deeper knowledge.

3.2.1 Model Assumptions

Let rit denote the continuously compounded return on an asset i at time t, rit = log(Pit)−log(Pi,t−1) = pit − pi,t−1. There are following assumptions about the probability distribution

of rit for i = 1, . . . , N assets over time horizon t = 1, . . . , T :

Assumption 1. Normality of returns: rit ∼ N(µi, σ2i ), i = 1, . . . , N and t = 1, . . . , T .

Assumption 2. Constant variances and covariances: Cov(rit, rjt) = σij, i, j = 1, . . . , N

and t = 1, . . . , T .

Assumption 3. No serial correlation across assets over time: Cov(rit, rjs) = 0, for t 6= s

and i, j = 1, . . . , N .

3.2.2 Regression Model Representation

A convenient mathematical representation or model of asset returns can be given based on

assumptions 1-3. This is the constant expected return (CER) regression model. For assets

i = 1, . . . , N and time periods t = 1, . . . , T , the CER model is represented as:

rit = µi + eit with eitiid∼ N(0, σ2

i ) and Cov(eit, ejt) = σij , (3.1)

where µi is a constant and eit is a normally distributed random variable with mean zero

and variance σ2i . Using the basic properties of expectation, variance and covariance, we can