Languages

Pages

Legal

Siddharth Rajeev, B.Tech, MBA, CFA

Anthony de Ruijter, BA

April 11, 2018

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

East Africa Metals Inc. (TSXV: EAM) - Initiating Coverage: Receives Mining License in Ethiopia

Sector/Industry: Junior Resource www.eastafricametals.com

Market Data (as of April 11, 2018)

Current Price C$0.20

Fair Value C$0.54

Rating* BUY

Risk* 5 (Highly Spec)

52 Week Range C$0.18 - C$0.37

Shares O/S 162,760,091

Market Cap C$32.55 mm

Current Yield N/A

P/E (forward) N/A

P/B N/A

YoY Return -28.6%

YoY TSXV -6.0% *see back of report for rating and risk definitions

Investment Highlights

East Africa Metals Inc. (“EAM”, “company”) is the only TSXV listed publicly traded junior resource company active in the Federal Democratic Republic of Ethiopia (“Ethiopia”).

In December 2017, the company received a Mining License for its 70% owned Terakimti oxide gold project. The company is awaiting Mining Licenses for two other projects (Da Tambuk and Mato Bula) in the same region. We believe the three mining licenses will offer EAM the potential to proceed to a district scale production scenario.

The company’s projects in Ethiopia have a total indicated resource of 0.93 Moz (million ounces), and an inferred resource of 0.87 Moz gold equivalent.

EAM’s projects are located in the Arabian-Nubian Shield (“ANS”) - one of the most under-explored prospective gold regions in the world. Targeted deposit types include precious metal enriched VMS and orogenic lode gold.

EAM also has a gold project in Tanzania, which has an indicated resource of 0.72 Moz, and an inferred resource of 0.29 Moz gold.

Institutions hold 65.49 million shares, or 40% of the total outstanding shares, implying a strong vote of confidence for EAM’s management team and its portfolio.

We are initiating coverage with a BUY rating and a fair value estimate of $0.54 per share.

Risks

The value of the company is highly dependent on commodity prices. Exploration and development risks. Political risks and changes to mining laws in Ethiopia may negatively

impact the company. There is no guarantee that the transaction related to the Tanzanian assets

will be completed. No guarantee that the financing agreement will be completed. Permitting risks. Project financing may be delayed.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Company

Overview

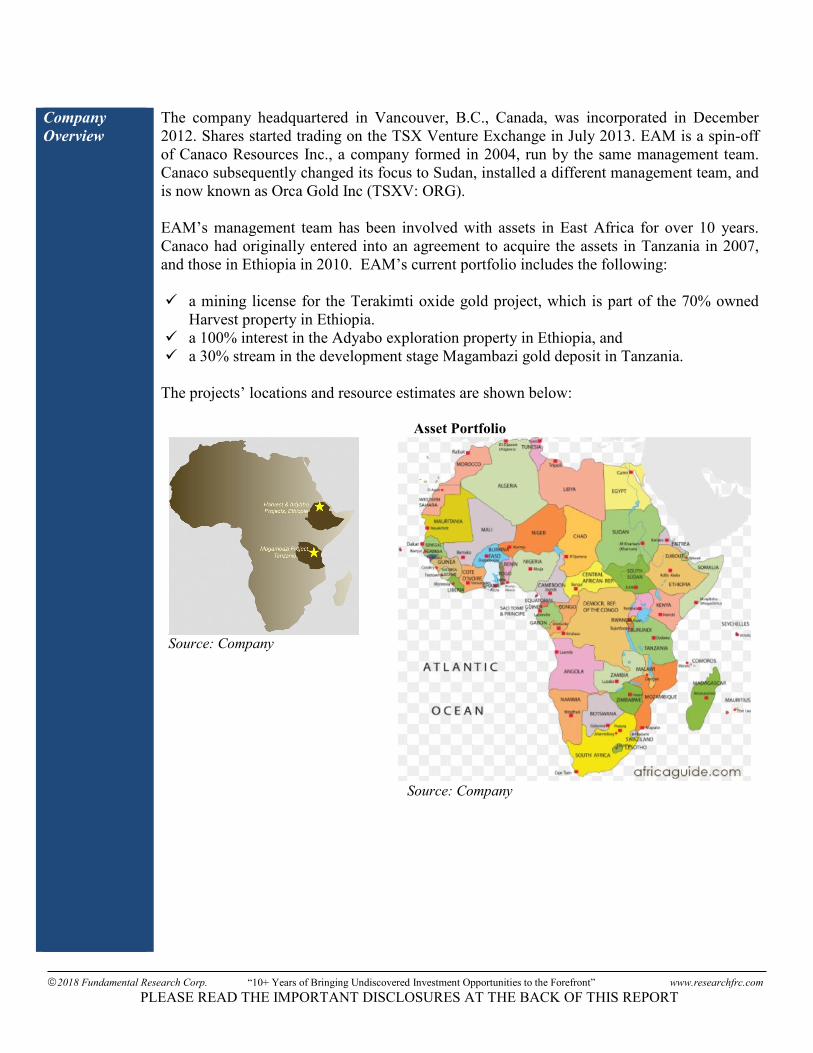

The company headquartered in Vancouver, B.C., Canada, was incorporated in December 2012. Shares started trading on the TSX Venture Exchange in July 2013. EAM is a spin-off of Canaco Resources Inc., a company formed in 2004, run by the same management team. Canaco subsequently changed its focus to Sudan, installed a different management team, and is now known as Orca Gold Inc (TSXV: ORG). EAM’s management team has been involved with assets in East Africa for over 10 years. Canaco had originally entered into an agreement to acquire the assets in Tanzania in 2007, and those in Ethiopia in 2010. EAM’s current portfolio includes the following: a mining license for the Terakimti oxide gold project, which is part of the 70% owned

Harvest property in Ethiopia. a 100% interest in the Adyabo exploration property in Ethiopia, and a 30% stream in the development stage Magambazi gold deposit in Tanzania.

The projects’ locations and resource estimates are shown below:

Asset Portfolio

Source: Company

Source: Company

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Ethiopia

Mineral Resource Summary

Source: Company

With a population of 102.4 million, and 2016 gross domestic product (“GDP”) per capita of US$706, Ethiopia ranks as one of the poorer states in the Sub-Saharan African region, according to the World Bank. The country is neighbored by Eritrea to the north, Djibouti

and Somalia to the east, Somalia and Kenya to the south, with North Sudan and South

Sudan to the west. In 2016, Ethiopia had merchandise exports of US$2.92 billion, with 0.75% of these exports being ores and metals, according to the World Bank. This is down from a peak of 3.01% in 2007. The graph below outlines the historic contribution of mining products to merchandise exports (note that the Y axis is measured in percentage terms):

Ethiopia: Metals and Ores as a % of Merchandise Exports

Source: World Bank

According to the World Bank, mineral rents made up only 0.55% of the nation’s GDP

in 2015, which was reported at US$64.47 billion. Mineral rent refers to the difference

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

between the values of produced minerals, net of costs of production. According to export.gov, a market intelligence platform managed by the U.S. Department of Commerce’s International Trade Administration, minerals found in Ethiopia include gold, platinum, nickel, copper, manganese, iron ore, gypsum, clay, potash, oil & gas, and others. Furthermore, though Ethiopia’s mining and quarrying sector does not currently contribute to GDP in a large way (5.6% in 2014/ 2015, according to export.gov), the Ethiopian Ministry

of Mines, Petroleum and Natural Gas (“MoMPNG”) established a directorate in 2014

with the goal of raising the mineral sector’s contribution to GDP to 10% or greater. Export.gov estimates that the export of gold earns Ethiopia US$300-500 million in foreign currency – making gold one of Ethiopia’s major exported metals. Significant large-scale

gold mining is almost absent, with the large majority of Ethiopian gold production

coming from artisanal mining of placer gold from alluvial deposits. The chart below outlines Ethiopia’s gold production, as reported by CEIC Data, with statistics from the U.S. Geological Survey (“USGS”):

Ethiopia’s Gold Production 2005-2015 (Kg)

Source: CEIC, USGS

Currently, there is only one significant producing gold mine in Ethiopia, the Midroc

Lega Dembi Gold Mine, owned by Saudi-owned Midroc Group. The mine, which began operations in 1998, produced 52,044.71 kg of gold and 14,670.6 kg of silver in the 16.5 years between 1998 and August 2014. Revenues from sales of produced gold at the Legadembi mine during that period amounted to US$1.25 billion, as reported by a company presentation. In addition to the Lega Dembi Gold Mine, KEFI Minerals PLC (AIM: KEFI), a London-listed junior miner with interests in Saudi Arabia and Ethiopia, is currently developing the 95% owned Tulu Kapi Gold Project. In May 2017, KEFI completed a definitive feasibility study on the project. KEFI also announced in October 2017 that it expected gold production of 144,000 oz per annum during the first three years of the mine’s life and forecasted a total of 980,000 oz over the life of the mine. Furthermore, the company estimated an all-in sustaining cost of US$800/ oz. The project’s estimated resources are given below:

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: KEFI Minerals PLC

The lack of large-scale gold mines comes despite Northern Ethiopia sitting on the Arabian-Nubian Shield (“ANS”), a prominent geological belt that is highly prospective for VMS and orogenic lode gold deposits. The ANS, which covers Egypt, Sudan, Israel, Saudi Arabia,

Eritrea, Jordan, Ethiopia, Somalia, and Yemen, is one of the most under-explored

prospective gold regions in the world.

The Arabian Nubian Shield

Source: Company

The table below outlines major gold projects in the ANS:

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Harvest and

Adyabo,

Ethiopia

Major Gold Projects on the ANS

Source: FRC, Public Disclosures

EAM’s projects are located in the Asmara mineral belt in the southern part of the ANS. Bisha (producer in Eritrea), Debarwa, and Emba Derho are well known VMS projects located along strike towards the north. The ANS also includes orogenic gold deposits including the Sukari gold mine (13 Moz in measured and indicated resource) – the only commercial gold mine in Egypt, and the Koka gold deposit in Eritrea. Ethiopia is vastly under explored for gold in modern times. Mineral exploration or production was not allowed by the private sector during the communist regime from 1974 to 1991. In 1993, the Mining Proclamation and the Mining Tax Proclamation were introduced to provide a framework to attract foreign investments, including a 5% - 8% production royalty, a 35% income tax, and a structure allowing for repatriation of profits. A new Mining

Proclamation was introduced in 2010, which showed a new income tax rate of 25%, Federal Government free carried interest of 5%, government royalties of 5% for base metals and 7% for precious stones and minerals. We believe these terms are reasonable considering the terms in other African nations. The Harvest and Adyabo projects are located in the Tigray region of northern Ethiopia, 600 km north of the capital city of Addis Ababa.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Project Location

Source: Company

Harvest’s topography is characterized by gently rolling plateaus, while Adyabo primarily consists of a steep hilly terrain. A paved highway, and high voltage powerline, pass within 7 km of the Harvest project. A water reservoir is located within 4 km.

Infrastructure

Source: Company

Geology and Resource Estimates

Targeted deposit types include precious metal enriched VMS and orogenic lode gold.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Harvest

VMS deposits are typically associated with volcanic and / or sedimentary rocks. They consist of massive and / or semi-massive accumulations of sulphide minerals, and form in flat lenslike bodies parallel to the bedding. Within VMS deposits, copper sulphides tend to form in the central parts of the deposit where the temperature is higher, while zinc sulphides form away from the center, where the temperature is lower. Gold is often present in the copper-rich zones, while silver is more commonly associated with zinc. They commonly occur in clusters (1 – 20 Mt), and the individual deposits when combined, form mining districts / camps. While depths of the smaller deposits (under 4Mt) are in the 0 to 300m range, the larger ones (10+ Mt) extend deeper to the 1,000 to 2,000 m range. The following image shows the identified deposits and prospects across both Harvest and Adyabo.

Source: Company

The Harvest Project, covering 86 sq. km, consists of three primary exploration concessions known as Terakimti, Hamlo, and Igub. Terakimti’s mining license covers 2.8 sq. km. EAM holds a 70% interest in the project, the remaining 30% is held by Ezana Mining Development, a private Ethiopian company. Ezana’s 30% interest is essentially a free carried interest until the completion of a feasibility study. EAM acquired its 70% interest from Beijing Donia Resources Co. Ltd., which had held its interest since 2007.

Harvest was subject to exploration during the 1970s by the Ministry of Mines, Energy and Water Resources. In 1996, the area was licensed to Ezana. Ezana conducted several stream sediment, soil and rock chip geochemical surveys, and an airborne EM survey (2004), which identified over ten EM anomalies, with VMS potential. The first hole was drilled in 2007. Since then, 260 holes were drilled totaling 28,884 m.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Drill Hole History - Harvest

Source: Company

As shown above, the primary focus has been on Terakimti, which was discovered in

2009. Drilling has defined a VMS system with four stacked lenses up to 25 m thick (typically 5 – 15 m) over an 800 m strike. Gold mineralization is present within oxide (near-surface), supergene and primary (sulphide) occurrences.

Terakimti Long Section

Source: Company

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

An initial NI 43-101 compliant resource estimate was announced in January 2014.

Terakimti – Initial Resource Estimate

Source: Company

The resource estimate used metal prices of US$3.50/lb copper, US$0.90/lb zinc, US$1,400/oz gold, and US$25/oz silver. Extensive metallurgical testing has confirmed

that the near-surface oxide deposit is amenable to heap leaching. Testwork also indicated supergene and primary mineralization may be processed through conventional floatation to produce copper and zinc concentrates. The following recovery rates have been achieved in testwork:

Source: Company

An updated resource estimate on the oxide portion was announced in October 2015. The updated resource showed a significant increase in tonnage, grades and contained gold equivalent oz.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Terakimti – Updated Oxide Resource Estimate

Source: Company

Mining Licence

In December 2017, the company received a mining licence for the Terakimti oxide gold project. This was a major milestone for the company as it allows the company to

establish the first commercial heap leach operation in the country. The company is now planning to advance the gold oxide deposit into production. An independent Environmental Impact and Socio-Economic Assessment (“EISA”) study has already been completed. A preliminary economic assessment (“PEA”) is current underway with completion expected by the end of April 2018. In December 2017, the company submitted Mine License applications for its Da Tambuk and Mato Bula properties. These properties are part of the Adyabo property, discussed later in this report. The three mining licenses will offer EAM the potential to proceed to a

district scale production scenario. Exploration Upside

As VMS systems occur in clusters, the project is considered to have good potential for resource expansion. The following image shows the various targets identified on Harvest.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Adyabo

Source: Company

The 2014 NI 43-101 report assigned an exploration target on the Mayshehagne prospect of 100,000 to 400,000 tonnes, with grades ranging from 0.2% to 5.0% copper, 0.2 to 2.1 g/t gold, 3 g/t to 31 g/t silver and 0.4% to 8.2% zinc. Mayshehagne is located approximately 3 km south of Terakimti. A 10 hole drill program showed best results of 20.70 m of 5.00% Cu, 1.03 g/t Au, 31 g/t Ag and 8.20% Zn from 24.0 m, including 12.8 m of 7.77% Cu, 1.62 g/t Au, 50 g/t Ag and 12.66% Zn. Another major target, VTEM09, is located 5.3 km east-northeast and along trend from Terakimti. A drill hole in 2013 intersected 10.21 m of 3.16% copper, 3.97 grams per tonne gold, 87 grams per tonne silver, and 3.82% zinc from 20.29 metres, including 2.82 metres of 5.61% copper, 7.48 grams per tonne gold, 102 grams per tonne silver, and 0.72% zinc. Subsequent drilling in 2016 intercepted 24.06 m grading 1.88% Cu, 3.08g/t Au, 66.4g/t Ag, and 2.54% Zn, from a depth of 35.84 m.

In addition to the VMS mineralization, a major zone of gold mineralization has been identified approximately 1.5 km west of Terakimti at Ruwa. The Ruwa-Ruwa Trend contains several bedrock gold prospects and abundant artisanal eluvial and alluvial working over a distance of 7 km. As shown in the image above, Ruwa, Adi Goshu, and Lihamat are classified as orogenic lode gold mineralization. None of these targets have been ever drilled.

EAM holds a 100% interest in the Adyabo project, which is subject to a 2% NSR royalty that can be purchased for $5 million. The concessions were acquired from Aberdeen International Inc. (“Aberdeen”) in 2011. The concessions were originally granted to Aberdeen in 2007.

The project consists of two exploration licences, West Shire and Adi Dairo, covering 196 sq. km. The Adi Dairo licence expired in January 2017, and the West Shire license expired in

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

October 2017. Our discussions with management indicated that they are in on-going discussions with the MoMPNG on renewing these licences. As mentioned above, the company has pending license applications on its Da Tambuk and Mato Bula properties. Similar to Harvest, Adyabo is prospective for VMS as well as orogenic gold deposits, and contains numerous alluvial, eluvial, and artisanal gold workings. Gold rich VMS mineralization is identified along the Mato Bula Trend at the Mato Bula, Mato Bula North and Da Tambuk prospects. The main prospect is Mato Bula, which is divided into six mineralized zones covering 1.3 km, namely the Silica Hill North, Silica Hill, Mato Bula, Mato Bula South, Jasper Hill, and Halima Hill. In addition, orogenic gold mineralization is identified in the 47 km long Zager gold trend.

Mata Bula Prospects

Source: Company

Historic drill holes intersected mineralization at depths of up to 450 m below surface at Mato Bula, 150 m depth at Mato Bula North, and 300 m depth at Da Tambuk. A total of 142 holes / totaling 23,412 m have been drilled on the property to date.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Historic Drilling

Source: Company

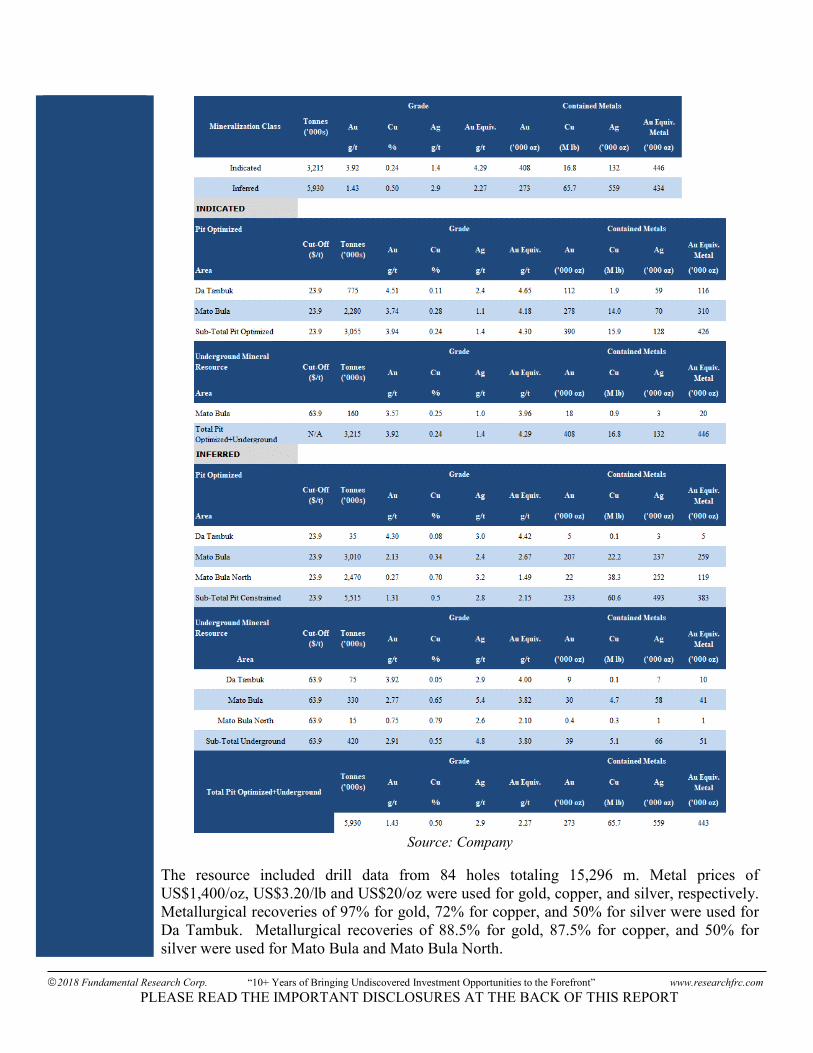

The following tables shows the NI 43-101 compliant resource announced in 2016. The resource contains an indicated resource of 3.22 Mt containing 408 koz of gold at an average grade of 3.92 g/t gold, 16.8 Mlbs copper at an average grade of 0.24% copper, and 132 koz silver at an average grade of 1.4 g/t silver. The inferred resource totaled 5.93 M containing 273 koz gold at an average grade of 1.43 g/t gold, 65.7 Mlbs copper at an average grade of 0.50%, copper, and 559 Koz silver at an average grade of 2.9 g/t silver.

Adyabo – Resource Estimate

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Company

The resource included drill data from 84 holes totaling 15,296 m. Metal prices of US$1,400/oz, US$3.20/lb and US$20/oz were used for gold, copper, and silver, respectively. Metallurgical recoveries of 97% for gold, 72% for copper, and 50% for silver were used for Da Tambuk. Metallurgical recoveries of 88.5% for gold, 87.5% for copper, and 50% for silver were used for Mato Bula and Mato Bula North.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Handeni,

Tanzania

Similar to Harvest, Adyabo also offers exploration upside through delineation of additional VMS mineralization, as well as exploration of orogenic lode gold mineralization within the Zager Trend. In 2015, EAM entered into an agreement with Tanzanian Goldfields Company Limited (a Hong Kong based company) to sell 100% of its assets in Tanzania. The agreement was subsequently updated in January 2018. The amended transaction terms are listed below: pay EAM US$2 million (US$0.75 million paid) in cash, upon achievement of certain

milestones EAM will retain a 1.6% NSR royalty capped at US$1.8 million EAM will have the option to acquire a gold stream equal to 30% of the gold produced, at

a price per oz of production cost plus 15%. offer EAM a seat on the Board of Directors, and two of the five seats on the Management

Committee of the Magambazi project. EAM will not be required to contribute any capital Should the buyer fail to produce 10,000 oz per quarter for two consecutive quarters

commencing 2020, the buyer will pay EAM a cash payment of 85% of the forecasted revenues to EAM. The remaining unpaid 15% of EAM’s revenue will be settled once the buyer reaches 10,000 oz of gold production in a quarterly period.

EAM will have a right of first refusal to re-acquire the properties if commercial production is not reached by 2020.

On April 6, 2018, the company announced it has commenced arbitration proceedings against Tanzanian Goldfields for failure to adhere to the terms of their agreement. The Handeni project is located in northeastern Tanzania, approximately 173 km northwest of Dar es Salaam. It consists of two prospecting licenses covering 83.5 sq. km, and two mining licenses covering 9.9 sq. km. Canaco had originally entered an option agreement to acquire these assets in 2007.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Company

Gold deposits on the property consist of artisanal placer deposits and orogenic vein-related mineralization. Approximately 471 diamond drill holes had been drilled for a total of 121,846 m on the Handeni property. The Handeni property package includes the Magambazi project, a gold deposit discovered in 2009. A NI 43-101 compliant resource estimate on Magambazi, calculated in 2012, based on a 0.5 gpt cut-off grade is shown below:

Source: Company

The Tanzanian government recently made certain changes to its existing legal and regulatory framework governing the natural resources sector. The changes, we believe, are likely to

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Management

impact foreign investments. Key changes are listed below: The Tanzanian Government will have the right to renegotiate existing mineral

development agreements at its discretion; The Government to receive a free-carried interest of no less than 16% in all mining

projects. We consider this to be in line with other African nations. The Government will have the right to acquire up to 50% of any mining asset equal to the

value of tax benefits provided to the owner of that asset. Increase royalties from 4% to 6% on revenues from gold, copper, silver and platinum

group metals; Foreign-owned mining groups will have to offer shares to the government and local

companies. Considering these developments, we believe there is a risk that the buyer may delay or even reneg on its agreement with EAM. Management and board members combined hold 5.08 million shares, or 3.12% of the

total outstanding shares. Institutions hold 65.49 million shares, or 40.24% of the total.

We believe the strong institutional holding is a strong vote of confidence on EAM’s management team and its portfolio.

Source: Management Circular Information, SEDI

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Brief biographies of key leadership and the board of directors, as provided by management, are given below: Andrew Lee Smith – President, Chief Executive Officer & Director

Mr. Smith is a Professional Geologist. He has over 25 years of experience successfully exploring, developing, and operating African and North American base and precious metals mining projects. He also holds Directorships and management positions with a number of other junior exploration companies. Mr. Smith holds a BSc in Earth Sciences from the University of Waterloo and is a professional geologist and a member of the Association of Professional Engineers and Geoscientists of British Columbia. He received the Mining Entrepreneur of the Year Award in 1994 from the Quebec Prospectors Association for his role in mine development with Aurizon, and was named Outstanding Alumnus of 2009 by the Science Faculty of the University of Waterloo for his contributions to mineral exploration. Jeff Heidema - Vice-President of Exploration

Mr. Heidema is a Professional Geologist with over 25 years of exploration experience with the Cominco, Teck Cominco and Teck exploration groups. Mr. Heidema's career has largely focused on exploration project management for programs ranging from grass roots to near mine exploration, and also includes EHS, agreement, and tenure management. He predominantly specializes in VMS and Archean gold exploration. Peter Granata - Chief Financial Officer

Mr. Granata is currently Chief Financial Officer of East Africa Metals and Tigray Resources Inc. Mr. Granata is a Chartered Accountant with over 10 years of accounting and financial reporting experience in Canada and Australia. Prior to joining EAM, Mr. Granata was CFO for Tigray Resources Inc., Controller for Canaco Resources Inc., and was at PricewaterhouseCoopers since 2005 specializing in statutory reporting audits, IFRS conversion projects, SOX404 projects, equity offerings and mergers and acquisitions. Whilst at PwC Mr. Granata's client portfolio comprised of mining companies including producing and exploration entities with both local and international operations, manufacturing companies and government entities including First Nations local governments. Mr. Granata is a member of the Institute of Chartered Accountants Australia and holds a Bachelor of Business from Griffith University, Australia. Nick Watters - Business Development

Mr. Watters is a co-founder of Canaco, Tigray and several other successful Mining enterprises since 1996. Mr. Watters has raised nearly $260 million in his career. Beginning in the corporate communications field, he has worked with several public and private companies in a wide variety of sectors including mining, high-tech, and the biotech industries. Mr. Watters helped create the corporate identities for a number of small start-ups as well as heading up their corporate communications departments. Mr. Watters is also serving as a Director to other Public Companies. Dr. Jingbin Wang - Chairman

Dr. Wang is currently the Chairman and General Manager of Sinotech Minerals since 2004.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

He is a leader in the non-ferrous metals industry in China as an expert in mineral exploration and mining with 30 years of experience. He has been granted the title of National Youth Expert for Outstanding Contribution in China for his great success in prospecting results and scientific research. Dr. Wang has also been President of Beijing Institute of Geology for Mineral Resources since 2002, and Vice President of China Nonferrous Metals Industry Association since 2008. Dr. Wang was a director of Goldrock until March 31, 2016, and was Executive Director of China Nonferrous Metals Resource Geological Survey until February 25, 2015. Dr. Antony Harwood - Director

Dr. Antony Harwood (Tony) is an economic geologist with over 30 years of experience in the mining industry, he graduated from the University of Wales, Cardiff, in the UK with a BSc (Hons) cum laude and a PhD degree in Economic Geology. Tony is currently President and Chief Executive Officer of Montero Mining and Exploration (TSX-V) a rare earth element focused company with its flagship property, the Wigu Hill Rare Earth Project in Tanzania. In addition, Tony is a non-executive Director of Endeavour Mining Corporation (ASX/TSX). Prior to joining East Africa Metals, Tony was President and CEO of Africo Resources, which he took to the TSX, raising $124 million during his tenure from 2006 to 2009, prior to this Tony was Vice President Global Generative Exploration for Placer Dome Inc. from 1998 to 2006. Tony was founder of Harwood International, a geological consulting company, which he operated for 10 years and prior to this he held the position of lecturer at Cardiff University, UK and Natal University, Durban, South Africa. David Parsons - Director

Mr. Parsons is retired. Until June 30, 2016 he served as Vice-President, Insurance of Goldcorp Inc. where he was responsible for corporate risk including mining operations loss control, business continuity planning and insurance. Prior to this appointment in 2010, he was Director, Corporate Services and Financial Analysis from October 2004 to 2010. He was employed by Wheaton River in 2001, serving as Controller until October 2004 and was directly involved in the acquisitions by Wheaton River and the subsequent merger with Goldcorp in 2005. He holds a Bachelor of Arts degree from the University of British Columbia and is a Chartered Professional Accountant / Certified General Accountant with over 30 years of experience in the gold mining industry, having served in the roles of Controller, Chief Financial Officer, and Director of public companies. Sean Waller - Director

Mr. Waller is a mineral processing engineer, registered as a Professional Engineer in British Columbia. Mr. Waller has over 30 years of International minerals industry experience including company and project management, evaluation, design and operation. Mr. Waller currently serves as President of Candente Copper Corp. Candente Copper is developing the large scale Cañariaco Norte copper deposit located in Northern Peru. Previous roles in Mr. Waller's career included AMEC Americas Limited Mining Division ("AMEC") in Vancouver where he held the positions of Vice President of Business Development and Senior Project Manager. At AMEC, Mr. Waller was the Study Manager for the definitive Feasibility Study of Nevsun's very successful Bisha Mine in Eritrea and the Project Manager for the Front End Engineering Design of the large scale Petaquilla Copper (Cobre de

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Panama) project in Panama (now under construction). Prior to AMEC, Mr. Waller worked with SNC-Lavalin's Mining Division in senior technical roles in mineral processing and project engineering. Mr. Waller previously worked for Freeport-McMoran as Chief Metallurgist at its world class Grasberg copper gold mine in Indonesia, as well as Chief Metallurgist at the Colomac gold mine in the sub-Arctic. Mr. Waller is a Past President of the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”).

Dr. Zhijun He - Director

Dr. Zhijun He is a professional geologist with over 20 years of experience in geological research, mineral exploration, and geological services. He holds a PhD degree in Petrology and Economic Geology from China University of Geosciences (Beijing) and is a member of AusIMM. Dr. He is Winner of the 11th Silver Hammer Prize in Geological Science awarded by Geological Society of China and has won several provincial and ministerial Technology Awards for mineral exploration and scientific research, including two First Prizes of the Prospecting Achievement Award from China Nonferrous Metals Industry Association. He currently serves as Deputy General Manager of Sinotech Minerals Exploration Co., Ltd. ("Sinotech") and holds the positions as director or supervisor for six major subsidiaries of Sinotech. Dr. He has been guiding exploration and has pioneered the market development of geological services in China, Asia, Canada, and Africa, and has led the discoveries of several large-sized multi-metallic deposits for clients of Sinotech in Africa. Yongwen Wang - Director

Mr. Yongwen Wang has been a Director and General Manager of Shandong Tyan Home Co., Ltd., a Chinese listed public company, since 2007, and Vice President of Shandong Tianye Real Estate Development Group Co., Ltd. since 1999. Mr. Wang holds a masters degree of Business Administration from Shandong University and has rich experience in enterprise management and capital operation. Our net rating on EAM’s management team is 3.8 out of 5.0 (see below).

Source: FRC

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Financials

The company’s board has seven members, of which five are independent. We believe that the Board of Directors of a company should include independent or unrelated directors who are free of any relationships or business that could materially interfere with the director’s ability to act in the best interest of the company. An unrelated/independent director can be a shareholder. The following table shows our analysis on the strength of EAM’s board.

Source: FRC

At the end of Q3-2017 (ended September 30, 2017), the company had cash of $0.63 million. We estimate the company had a burn rate (cash spent on operating and investing activities) of $783k per month in the first nine months of FY2017. The following table summarizes the company’s liquidity position:

Source: Financial Statements

Subsequent to the quarter-end, 3.78 million warrants were exercised at a price of $0.25 per share for $0.94 million. In December 2017, the company closed a $2 million financing by issuing 7.70 million units at a unit price of $0.26 per share / each unit will consist of a common share and half-warrant with an exercise price of $0.45 per share for 2 years. The company is currently in discussions with a number of parties for project financing.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Stock Options

and Warrants

Valuation and

Rating

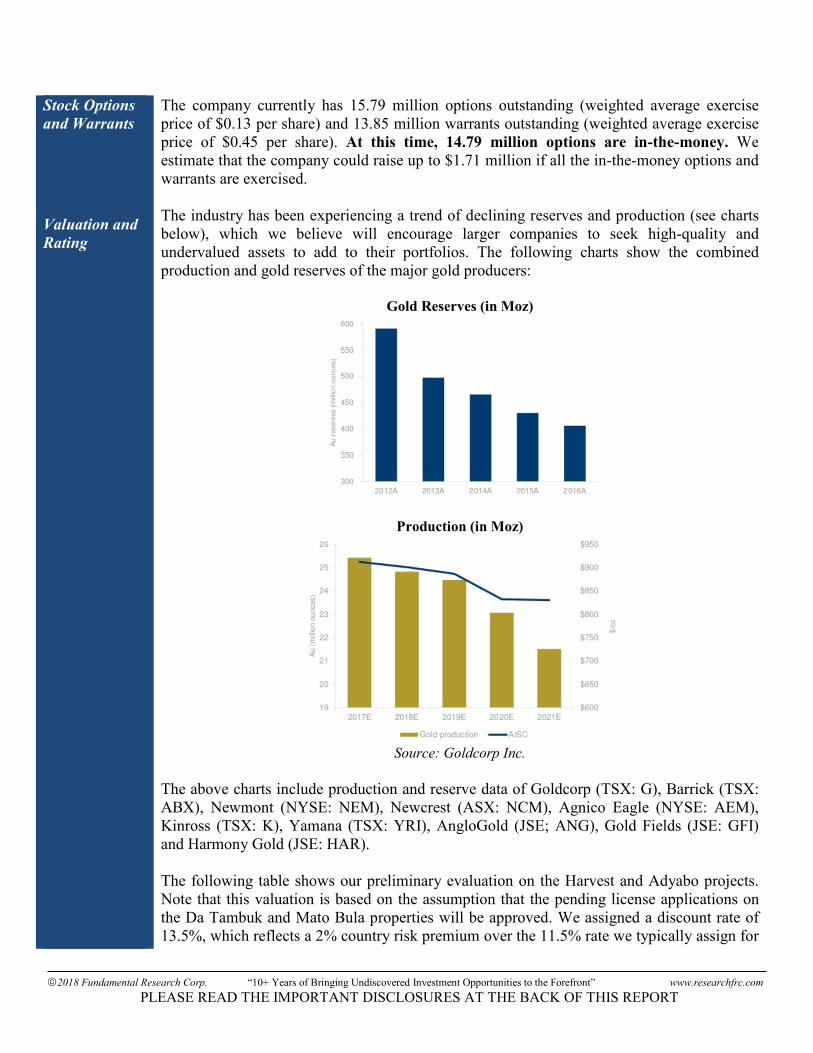

The company currently has 15.79 million options outstanding (weighted average exercise price of $0.13 per share) and 13.85 million warrants outstanding (weighted average exercise price of $0.45 per share). At this time, 14.79 million options are in-the-money. We estimate that the company could raise up to $1.71 million if all the in-the-money options and warrants are exercised. The industry has been experiencing a trend of declining reserves and production (see charts below), which we believe will encourage larger companies to seek high-quality and undervalued assets to add to their portfolios. The following charts show the combined production and gold reserves of the major gold producers:

Gold Reserves (in Moz)

Production (in Moz)

Source: Goldcorp Inc.

The above charts include production and reserve data of Goldcorp (TSX: G), Barrick (TSX: ABX), Newmont (NYSE: NEM), Newcrest (ASX: NCM), Agnico Eagle (NYSE: AEM), Kinross (TSX: K), Yamana (TSX: YRI), AngloGold (JSE; ANG), Gold Fields (JSE: GFI) and Harmony Gold (JSE: HAR). The following table shows our preliminary evaluation on the Harvest and Adyabo projects. Note that this valuation is based on the assumption that the pending license applications on the Da Tambuk and Mato Bula properties will be approved. We assigned a discount rate of 13.5%, which reflects a 2% country risk premium over the 11.5% rate we typically assign for

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

projects in North America.

Source: FRC

The following table outlines several comparable gold juniors operating in Africa. We estimate that EAM’s shares are trading at $23 per oz versus the comparables average of $31 per oz.

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: FRC, Public Disclosures

Net Resource – 100% of Measured and Indicated + 50% of Inferred Resources

The following table summarizes our valuation on EAM. We valued Handeni’s resource at the comparable average $31 per oz.

Source: FRC

The sensitivity of our valuation to key inputs is shown below:

Source: FRC

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Risks

We are initiating coverage on EAM with a BUY rating and a fair value estimate of

$0.54 per share.

We believe the company is exposed to the following key risks (not exhaustive): The value of the company is highly dependent on commodity prices. Exploration and development risks. Political risks and changes to mining laws in Ethiopia may negatively impact the

company. There is no guarantee that the transaction related to the Tanzanian assets will be

completed. Permitting risks. Access to capital and share dilution. Exchange rate. As with most junior exploration / development companies, we rate EAM’s shares a risk

of 5 (Highly Speculative).

2018 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Fundamental Research Corp. Equity Rating Scale:

Buy – Annual expected rate of return exceeds 12% or the expected return is commensurate with risk Hold – Annual expected rate of return is between 5% and 12% Sell – Annual expected rate of return is below 5% or the expected return is not commensurate with risk Suspended or Rating N/A— Coverage and ratings suspended until more information can be obtained from the company regarding recent events. Fundamental Research Corp. Risk Rating Scale:

1 (Low Risk) - The company operates in an industry where it has a strong position (for example a monopoly, high market share etc.) or operates in a regulated industry. The future outlook is stable or positive for the industry. The company generates positive free cash flow and has a history of profitability. The capital structure is conservative with little or no debt. 2 (Below Average Risk) - The company operates in an industry where the fundamentals and outlook are positive. The industry and company are relatively less sensitive to systematic risk than companies with a Risk Rating of 3. The company has a history of profitability and has demonstrated its ability to generate positive free cash flows (though current free cash flow may be negative due to capital investment). The company’s capital structure is conservative with little to modest use of debt. 3 (Average Risk) - The company operates in an industry that has average sensitivity to systematic risk. The industry may be cyclical. Profits and cash flow are sensitive to economic factors although the company has demonstrated its ability to generate positive earnings and cash flow. Debt use is in line with industry averages, and coverage ratios are sufficient. 4 (Speculative) - The company has little or no history of generating earnings or cash flow. Debt use is higher. These companies may be in start-up mode or in a turnaround situation. These companies should be considered speculative. 5 (Highly Speculative) - The company has no history of generating earnings or cash flow. They may operate in a new industry with new, and unproven products. Products may be at the development stage, testing, or seeking regulatory approval. These companies may run into liquidity issues, and may rely on external funding. These stocks are considered highly speculative.

Disclaimers and Disclosure

The opinions expressed in this report are the true opinions of the analyst about this company and industry. Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The analyst and Fundamental Research Corp. “FRC” do not own any shares of the subject company, do not make a market or offer shares for sale of the subject company, and do not have any investment banking business with the subject company. Fees were paid by EAM to FRC. The purpose of the fee is to subsidize the high costs of research and monitoring. FRC takes steps to ensure independence including setting fees in advance and utilizing analysts who must abide by CFA Institute Code of Ethics and Standards of Professional Conduct. Additionally, analysts may not trade in any security under coverage. Our full editorial control of all research, timing of release of the reports, and release of liability for negative reports are protected contractually. To further ensure independence, EAM has agreed to a minimum coverage term including an initial report and three updates. Coverage cannot be unilaterally terminated. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time. The distribution of FRC’s ratings are as follows: BUY (74%), HOLD (7%), SELL / SUSPEND (19%). To subscribe for real-time access to research, visit http://www.researchfrc.com/subscribe.php for subscription options. This report contains "forward looking" statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company's products/services in the marketplace; acceptance in the marketplace of the Company's new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company's periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. A report initiating coverage will most often be updated quarterly while a report issuing a rating may have no further or less frequent updates because the subject company is likely to be in earlier stages where nothing material may occur quarter to quarter. Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated, and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report. The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.

Top Related