Languages

Pages

Legal

1 |

Earmarking tobacco tax

revenues

Anne-Marie Perucic

Economist

Prevention of Noncommunicable Diseases

WHO

2 |

Why tax tobacco?

Public health justification:

– Tobacco tax increases that increase prices are the most-cost

effective policy for tobacco use reduction.

Economic justification:

– Correcting for negative externalities and imperfect information.

Public finance justification:

– Easy to collect (few producers),

– Demand price-inelasticity => increased taxes increase revenues.

Win-win policy: for revenues and public health

3 |

Types of consumption (indirect) taxes imposed on

tobacco products – Which is used for earmarking?

General tax on consumption: Value-Added Taxes or Sales

Taxes

general tax on consumption, applied (usually) as a single rate and on a

broad range of goods and services

Excises

selective taxes, confined to a narrow range of goods, the consumption

of which governments wish to discourage, for example, for health and

environmental reasons – "sin taxes"

Customs/import Duty

tax on a selected commodity imported in a country and destined for

domestic consumption (i.e., the goods are not in transit to another

country)

4 |

Earmarking practices around the world

Tobacco control NCDs Health

Insurance/UHC

Other/more general

health programmes

Iceland, Iran,

Switzerland,

Viet Nam

Algeria (cancer control

and other health

programmes)

Costa Rica (incl.

tobacco control), Nepal,

Panama (incl. tobacco

control)

Congo, Egypt,

Philippines

Argentina, Bangladesh,

Cape Verde, Colombia,

Comoros, Côte d'Ivoire,

El Salvador, Guatemala,

India (incl. tobacco

control), Indonesia,

Jamaica, Madagascar,

Korea, Romania,

Thailand, Macedonia,

USA

About 30 countries from all regions of the world earmark tobacco tax revenues

for health purposes

Tobacco earmarking recently terminated in Mongolia and Poland.

Source: WHO Report on the Global Tobacco Epidemic, 2015.

5 |

Revenue potential from tobacco taxes

Recent publication in the WHO Bulletin (February 2016)

shows that:

– In 2014, the total amount of excise revenue generated globally

from the sale of cigarettes was estimated to be $ 402 billion

international dollars in Purchasing Power Parity terms (or US$

328 billion).

– Raising cigarette excise by 1 international $ per pack (US$ 0.8)

in all countries would increase revenue by 47% giving an extra $

190 billion international dollars (US$ 141 billion) to governments.

Source: Goodchild M, Perucic AM, Nargis N. Modelling the impact of raising tobacco taxes on public health and

finance. Bulletin of the World Health Organization 2016;94:250–257.

Nine countries case studies

Summary analysis

(upcoming WHO publication)

7 |

Arguments for and against earmarking

Pros Cons

Population more supportive of tax increases

when they know they will be used for

targeted social programmes

Introduces rigidities in the budgetary

process, limiting availability of funds for

alternative and (sometimes) more urgent

purposes.

Help guarantee funding for under-resourced

programmes, in this case, health. Can also

lead to better health outcomes

Leads to waste of resources when not

carefully planned by recipient

institution/programme

Closer connection between tax and

expenditure: increases accountability

Pro-cyclical, susceptible to booms and busts

Closer connection between tax and

expenditure: increases efficiency of public

expenditure

Leads to fragmentation of pooling and lack of

integration of health policy in other sectors

Can educate people about the cost of a

particular program/service

Will eventually shrink as consumption of

harmful/unhealthy products goes down

Compiled in Earmarked tobacco taxes: lessons learnt from nine countries. WHO 2016.

8 |

Analysis of 9 country experience in

tobacco tax earmarking

Diverse countries with diverse backgrounds with recent

(Botswana 2014) or long history in earmarking tobacco taxes

for health (Iceland 1972).

Nine countries are: Botswana, Egypt, Iceland, Panama,

Philippines, Poland, Romania, Thailand and Viet Nam.

9 |

Fund manager and expenditure

Botswana Egypt Iceland Panama Philippines Romania Thailand Vietnam

Fund manager

Ministry of

Health

The

General

Authority

of Health

Insurance

Directorate

of Health

(DH)

Ministry of

Health

(MINSA)

Department

of Health

(DOH)

Ministry of

Health

(MOH)

Thai Health

Promotion

Foundation

(ThaiHealth)

Autonomous

fund manager

supervised by

Prime Minister.

Ministry of

Health/

VNTCF –

Tobacco

Control

Fund.

Semi-

autonomous

Intersectoral

Managmt

Board.

Expenditure Health

promotion

Students

medical insurance

Tobacco

control and

general

health

promotion activities

NCDs

and

tobacco control

UHC Health

systems

infrastructu

re, public

health programs

Health promotion

Tobacco control

10 |

Earmarked funding and magnitude of funds Country Year earmarking

tobacco tax established

Funding source Estimated annual total funds from

earmarked tax

Annual funds from

tobacco earmarked tax

as percentage of general

government expenditure

on health (2013)

General government

expenditure on

health as

percentage of GDP

(2013)

Botswana 2014 30% of production cost of tobacco

products

2014–2015: BWP 4 million (US$ 0.48

million)

NA 3.1%

Egypt 1992 10 piasters on each pack of 20

cigarettes

2013–2014: EGP 392 million (US$ 52.06

million)

Earmarked taxes only 1.8% of total taxes

on cigarettes

1.086% 2.1%

Iceland 1972 (first)

2001 (latest amendment)

0.9% of gross tobacco sales value

(2001)

2014: ISK 108.3 million (US$ 0.89 million) 0.083% 7.0%

Panama 2009 50% of selective consumption tax on

cigarettes and other tobacco products

2014: US$ 27.8 million 1.322% 5.2%

Philippines 1997 (first)

2012 (latest)

85% of incremental revenue from excise

on tobacco and alcohol products

2014: PHP 50.18 billion (US$ 1.18 billion) NA 1.4%

Poland 2000 (terminated in 2015) State budget (0.5% of the value of the

excise tax on tobacco products)

2013: PLN 1 million (US$ 0.316 million)

from general budget

0.001% 4.6%

Romania 2005 Earmarked tax on tobacco and alcohol

10 €/1000 cigarettes, 10 €/1000 cigars,

cigarillos and other tobacco products for

smoking, 13 €/kg of smoking tobacco

2014: Lei 1.1 million (US$ 0.33 million);

14.4% of total health budget

0.004% 4.2%

Thailand 2001 2% surcharge tax on tobacco and

alcohol

2014: THB 4064.74 million (US$ 125.15

million)

1.78% of Ministry of Health budget and

1.84% of National Health Security Fund

0.932% 3.7%

Viet Nam 2012 Compulsory contribution by tobacco

manufacturers and importers to Viet

Nam Tobacco Control Fund : 1% of

factory price effective from 1 May 2013,

(1.5% in 2016 and 2% in 2019)

2014: VND 299.171 billion (US$ 13.91

million)

0.5% of national health budget

0.335% 2.5%

Lessons learned

12 |

Lessons learned from earmarking tobacco tax

revenues

Common threads for success:

– Earmarked tax revenue from an additional tax (not taking away from

existing revenues/expenses),

– Seeking policy opportunity to gain political support (e.g. WHO FCTC),

– Strong partnerships and policy synergies (intersectoral, mainly MoH and

MoF, but also with civil society),

– Careful presentation of arguments in favour of earmarking and sound

proposal based on evidence and needs,

– Effective countering strong opponents (Tobacco industry, government

sectors influenced by TI).

13 |

Lessons learned from earmarking tobacco tax

revenues

Further discussion:

– Investment in prevention (incl. tobacco control) very cost effective and

cheap (cost of scaling up tobacco control 0.11$ pc*),

– Revenue potential of tobacco taxes not insignificant (and taxes should be

increased on a regular basis),

– Earmarking tobacco tax revenues augments the positive health impact of

tobacco taxes,

– Earmarking tobacco tax revenues for prevention: strong link between tax

payer, revenue and benefit,

– Earmarked amounts: relatively small amounts make a difference and do

not introduce significant rigidities,

– Autonomous/semi-autonomous fund managers: independence and

accountability.

* Source:Scaling up action against noncommunicable diseases:

How much will it cost? WHO 2011. (for 42 LMIC)

14 |

Tobacco excise tax revenues and

expenditure on tobacco control

Source: WHO Report on the Global Tobacco Epidemic, 2015

200.35

37.44

7.32 1.26 0.03 0.004

High-income Middle-income Low-income

US$

per

cap

ita

Per capita excise tax revenuefrom tobacco products

Per capita public spendingon tobacco control

Governments collect nearly US$ 270 billion in tobacco excise tax revenues each year, but

spend around US$ 1 billion combined on tobacco control

91% of this is spent by high-income countries

Specific country

experiences/success stories

16 |

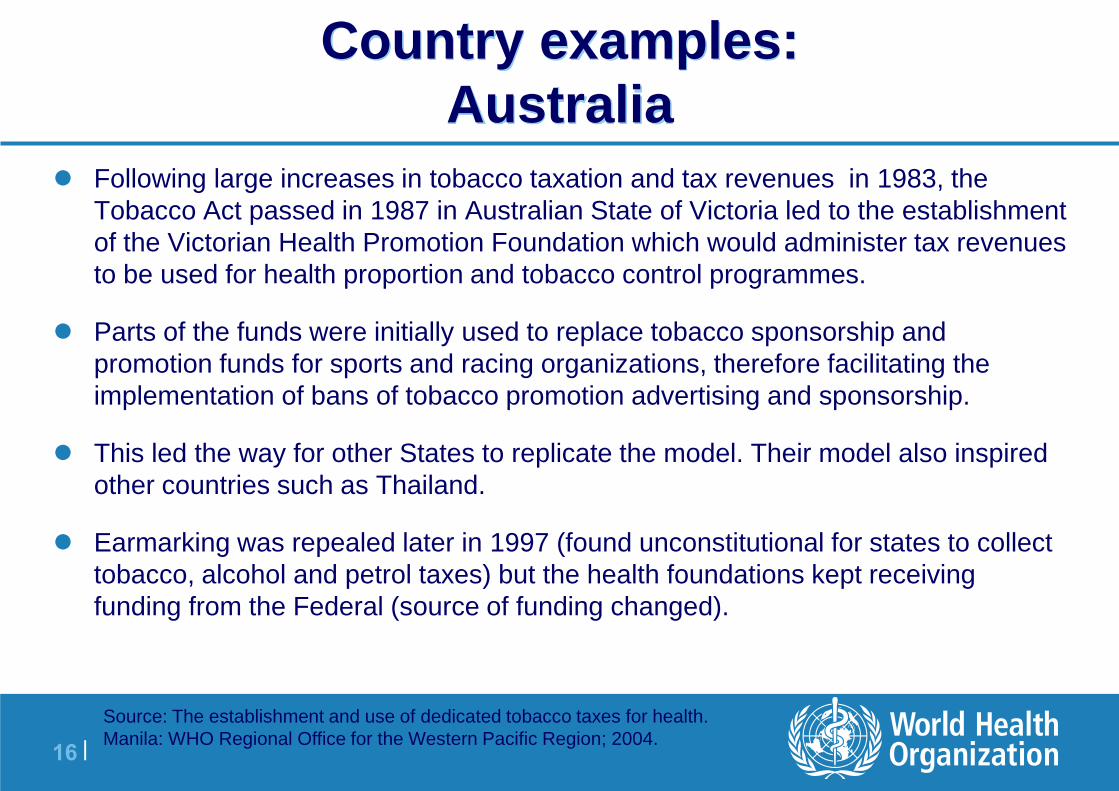

Country examples:

Australia

Following large increases in tobacco taxation and tax revenues in 1983, the

Tobacco Act passed in 1987 in Australian State of Victoria led to the establishment

of the Victorian Health Promotion Foundation which would administer tax revenues

to be used for health proportion and tobacco control programmes.

Parts of the funds were initially used to replace tobacco sponsorship and

promotion funds for sports and racing organizations, therefore facilitating the

implementation of bans of tobacco promotion advertising and sponsorship.

This led the way for other States to replicate the model. Their model also inspired

other countries such as Thailand.

Earmarking was repealed later in 1997 (found unconstitutional for states to collect

tobacco, alcohol and petrol taxes) but the health foundations kept receiving

funding from the Federal (source of funding changed).

Source: The establishment and use of dedicated tobacco taxes for health.

Manila: WHO Regional Office for the Western Pacific Region; 2004.

17 |

Country examples

Thailand

Thailand’s Health Promotion Foundation Act of 2001 established that a

2% surcharge on tobacco and alcohol excise would be earmarked to

secure funding for the Foundation (ThaiHealth)

ThaiHealth spent more than $US 100 million on health promoting

activities a year ($US 125 million in 2014) covering a wide range of

activities (including tobacco and alcohol control, traffic injury

management, promotion of physical exercise and sports for health, and

promoting healthy eating)

ThaiHealth is widely regarded as a model for ensuring that health

promotion activities receive adequate support. It has inspired models

developed in other countries such as Viet Nam.

Source: Earmarked tobacco taxes lessons learnt from nine countries.

Upcoming. WHO 2016.

18 |

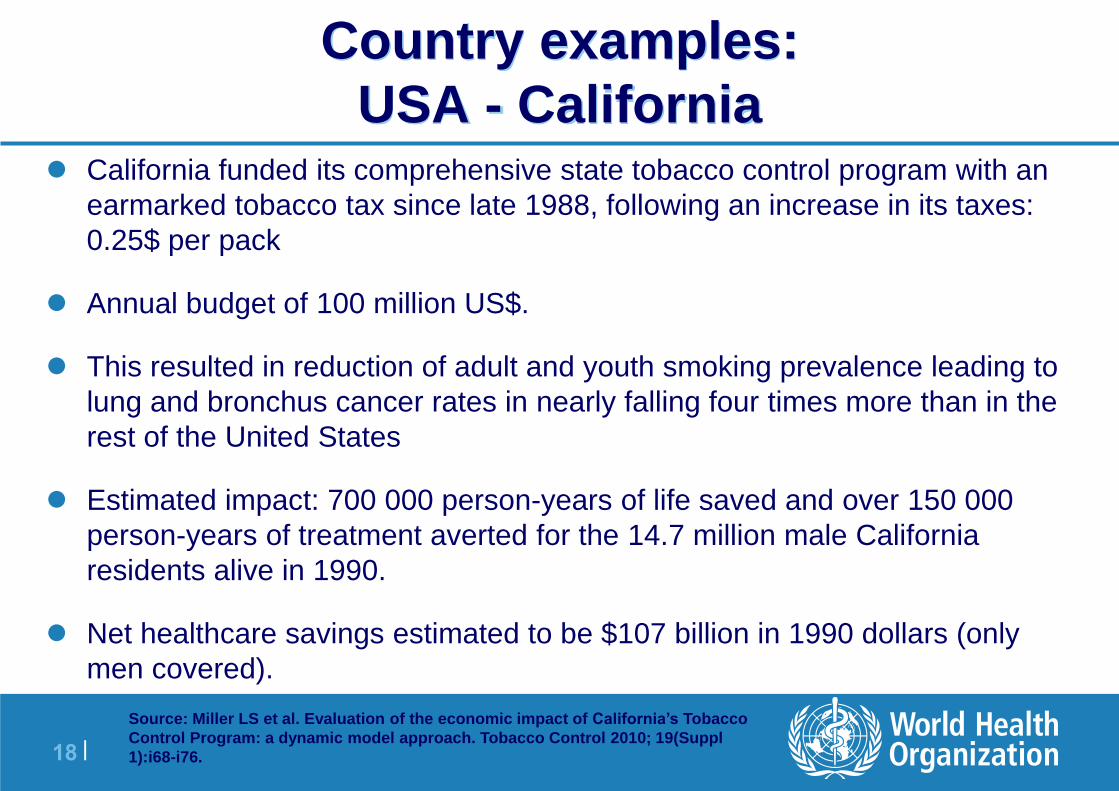

Country examples:

USA - California California funded its comprehensive state tobacco control program with an

earmarked tobacco tax since late 1988, following an increase in its taxes:

0.25$ per pack

Annual budget of 100 million US$.

This resulted in reduction of adult and youth smoking prevalence leading to

lung and bronchus cancer rates in nearly falling four times more than in the

rest of the United States

Estimated impact: 700 000 person-years of life saved and over 150 000

person-years of treatment averted for the 14.7 million male California

residents alive in 1990.

Net healthcare savings estimated to be $107 billion in 1990 dollars (only

men covered).

Source: Miller LS et al. Evaluation of the economic impact of California’s Tobacco

Control Program: a dynamic model approach. Tobacco Control 2010; 19(Suppl

1):i68-i76.

Top Related