Languages

Pages

Legal

w w w . i d a t e . o r g

The Atlas of the Digital

World11th edition

1 June 2011 - London

2

Agenda

- Steve Durbin, Chairman, DigiWorld Club UK

� DigiWorld Yearbook 2011Core telecom, Internet and media market issues- Jean-Michel Chapon, DigiWorld Programme London

- Yves Gassot, CEO, IDATE

� Other DigiWorld Initiatives 2011 - DigiWorld Summit Programme (16-17 November 2011)

- Collaborative Research programmes in UK

3

The DigiWorld Institute by IDATE …

DigiWorld Programme by IDATE

� A team of dedicated consultants specialised in the telecom, Internet and media industries

� A Digital world observatory : analysing market and business strategies, trend-tracking and forecasts

� A European forum that helps deepen interactions between enterprises, public decision-makers and academia

… the European Digital Economy Think Tank

4

DigiWorld ® Programme, an ambitious project

DigiWorldClubs

DigiWorld Events

DigiWorld Collaborative Research 2011

DigiWorldPublishing

Paris Club(monthly)

London Club(monthly)

Brussels Club(launching in 2011)

3 conferencesin Paris

TransatlanticDialogue

(Columbia University)

DigiWorld Summit 2011

Catalogue ofMarket reports

DigiWorld Economic Journal

(Communications & Strategies)

DigiWorldYearbook

OTT &Managed video

services

The future of advertising & datamining

Smart LivingSmart Cities

(launching in 2011/2012)

5

DigiWorld ® Yearbook, an original initiative

� Available in English and French, the 2011 edition will be launched in Paris and London.

6

DigiWorld ® Yearbook, an original initiative

Published with the support of DigiWorld Programme membe rs

7

DigiWorld trends by region

A market worth €2,754 billion in 2010, reporting 3% gro wth

� Market recovery in the US, but growth still on hold in Europe

� Emerging markets still the key driving forces… but not all faring the same

8

DigiWorld trends by sector

� Halting performances in hardware markets

� Very slight growth in service markets, withthe exception of TV

Recovery still tentative in most industry segments

9

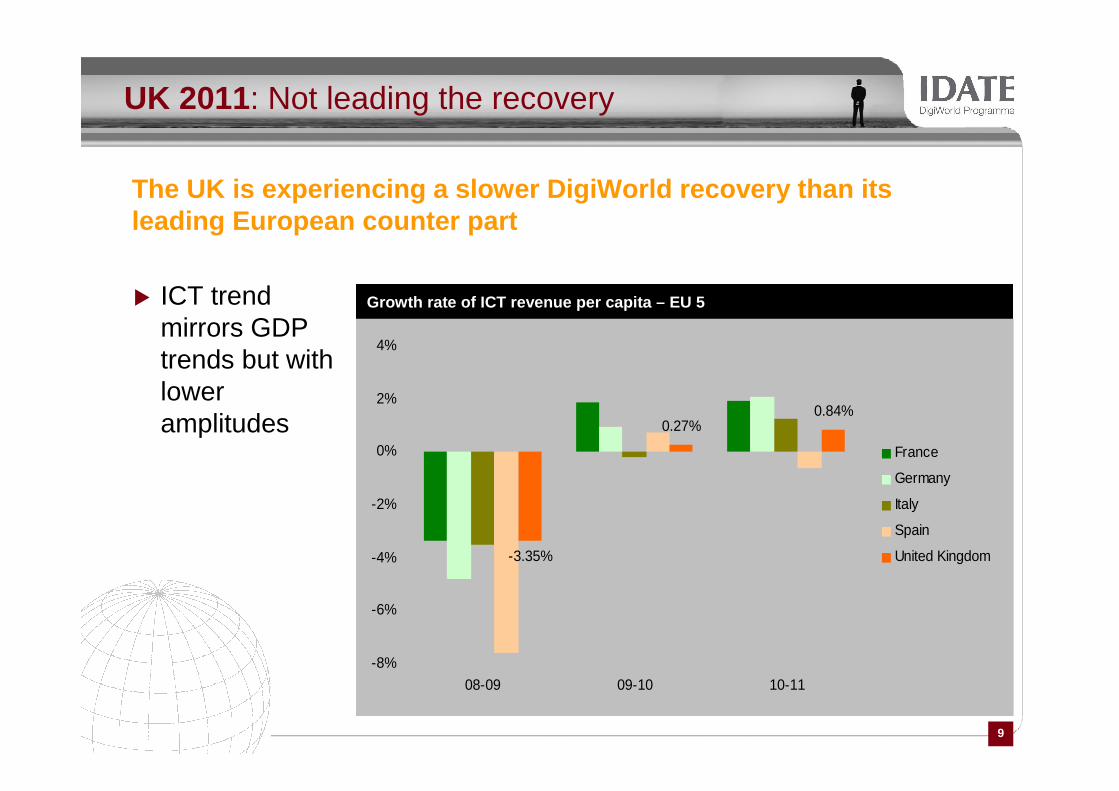

UK 2011: Not leading the recovery

Growth rate of ICT revenue per capita – EU 5

-3.35%

0.27%0.84%

-8%

-6%

-4%

-2%

0%

2%

4%

08-09 09-10 10-11

France

Germany

Italy

Spain

United Kingdom

The UK is experiencing a slower DigiWorld recovery than its leading European counter part

� ICT trend mirrors GDP trends but with lower amplitudes

10

IT in the UK : the lion share

Breakdown of DigiWorld revenue per capita in 2011

IT revenue share per capita is bigger in the UK than to the European average (at €2060 per capita)

0

500

1000

1500

2000

2500

France Germany Italy Spain UnitedKingdom

Consumer electronics

TV services

Computer hardware

Software & services

Telecom equipment

Telecom services

� IT services + IT hardware : UK = 45% EU = 38%

� Business share is pulling UK figures up

� Private consumption is lagging

11

TV services & equipment for IT & Telecom

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

France Germany Italy Spain United Kingdom

TV services

SW & services

Telecom services

Consumer electronics

Computer hardw are

Telecom equipment

2011 DigiWorld growth rate per segment – EU 5� Despite all the “buz” on new devices, most negatively impacting segment is “Consumer electronics”

UK areas for DigiWorld Growth

12

Beyond the DigiWorld’s core

IPTV

VoIP

M2MIoT

0.5 Bn€

Socialnetworking

0.5 Bn€

CloudSaas, IaaS,

PaaS5.7 Bn€

Search6 Bn€

Online gaming2 Bn€

Onlinevideo

0.7 Bn€Online advertising

0.8 Bn€

Mobileapps1 Bn€

eBook

eHealth

SmartGrid &Cities

… New Internet markets

eCommerce210 Bn€

Telecoms310 Bn€

Media125 Bn€

Software & IT265 Bn€

Note: Figures are for the EU-27 2010Source: IDATE

13

Facts and commentary : 2010 - 2011

1. Will devices be king?

2. LTE: promising first steps…

3. FTTx: hesitation and impatience

4. Net Neutrality: Act II

14

1. Will the device be king?

� Google’s Android bet likely to pay off

� Apple’s iPad bet paying off

� The Nokia-Microsoft alliance

� TV gets connected……

Will the Device be reallyKing?

In the great battle of the online ecosystems ?

15

2. LTE: Good News!

First large-scale rolloutsprogressing very differentlyfrom earlier 3G/UMTS ones …

Sizeable gap in European and American cellco’s revenue growth …

Will new pricing schemes and the huge popularity of smartphones put European carriers back on track?

16

3. FTTX : hesitation and impatience

� Underpinning telcos’ (and financial markets’) hesitations is uncertainty over ROI and, ultimately, the position of telcos vs. OTT…

Stepped up rollouts in 2011-2012? How will this affect the sector’s structure? What prices and what new services can we expect?

► FTTx: Europe lagging behind…

► The appeal of fibre needs to be bolstered by new tiered pricing schemes and attractive content …

► No single European market has emerged as a model, each one offering up a different view of the future

17

4. Net Neutrality : Act II

�Act II … as a certain degree of clarity has set inNN= non-discrimination+ justified traffic management + and segmented access (incl. for managed services) but must not affect accessibility of the open Web

�Act II … as the debate shifts, notably to the topic of how and whether the top aggregators should help finance infrastructure given the growing asymmetry in traffic at network delivery points (cf. Netflix – Level3 – Comcast affair)

31,00%

24,00% 25,00%23%

2007 2008 2009 2010

Upstream

Of which 44% for P2P and only 12% for the rest

Source: Cisco

How to generate new revenue when traffic is skyrocketing?What’s involved in making the transition to smart pipe? Are we going to see more mergers and alliances?

Upstream as a % of traffic in N-A

18

5. Also noteworthy …

Save the date! 16&17 Novembre, Montpellier

Will the Device be King?

� Smart Devices: what’s Next?

� Devices issues in digital markets: Mobile Internet, TV & Video OTT, Press

� Beyond Devices, the Cloud’ battle!

►Talking again about an Internet bubble: $25 billion for Groupon…

►Google’s troubles in China

►The role of social networking in popular uprisings in Tunisia and Egypt

►AT&T’s planned takeover of T-Mobile

►Vivendi buys Vodafone’s stake in SFR

►…

19

Thank you!