Languages

Pages

Legal

1

NILS LOMMERINOPERATIONS

EXECUTIVE VICE PRESIDENT

2

DEL MONTE OPERATIONSValue Proposition

Overall competitive cost structure

Superior supply chain performance

Sustainable cost reduction programs in place• Lean Operations

Enhancing overall competitiveness with upgraded execution abilities via transformation initiatives• Continued optimization of supply chain• Pet Manufacturing improvements

3

DEL MONTE OPERATIONSOperations footprint building block for delivering value

proposition

Distribution Center- 3rd Party

Fontana

Lathrop

Terminal Island

Jacksonville

Ft. Worth

Kankakee

Rochelle

Bloomsburg

Modesto

Kingsburg

Hanford

YakimaToppenish

Lawrence

Perham

Sleepy EyePloverMarkesanCambria

Mendota

Plymouth

Crystal City

Topeka

Atlanta

FruitTomatoVegPet Food McAllen

York

Distribution Center – DLM Operated

Decatur

Buffalo

Distribution Center- 3rd Party

Fontana

Lathrop

Terminal Island

Jacksonville

Ft. Worth

Kankakee

Rochelle

Bloomsburg

Modesto

Kingsburg

Hanford

YakimaToppenish

Lawrence

Sleepy EyePloverMarkesanCambria

Mendota

Plymouth

Crystal City

Topeka

Atlanta

FruitTomatoVegPet Food McAllen

York

Distribution Center – DLM Operated

Decatur

Buffalo

InternationalProduction Facilities

Samoa- TunaVenezuela- Veg, Tomato

Mexico- Citrus

InternationalProduction Facilities

Samoa- TunaVenezuela- Veg, Tomato

Mexico- Citrus

17 U.S. production facilities

4 International production facilities

11 Distribution Centers

U.S. and international co-packers

As of July 2007

4

SITUATIONAL ASSESSMENTGenerally speaking, we have a competitive cost structure in mostbusinesses, with initiatives in place to narrow or eliminate gaps in

areas that are dis-advantaged

Consumer Products Pet Products

FruitFruit

TomatoesTomatoes

VegetablesVegetables

TunaTuna

Advantaged

Advantaged

Dry PetDry Pet

Pet SnacksPet Snacks

Wet PetWet Pet

Dis-Advantaged

At Parity

Advantaged

At Parity

Advantaged

Note: Reflects comparable products across key SKU’s.

5

SITUATIONAL ASSESSMENTOperational costs expected to remain elevated

$150

$30

$120

$145

~$110

$0

$20

$40

$60

$80

$100

$120

$140

$160

F04

F05

F06

F07

F08E

Gross Inflationary Cost Increasesvs. Preceding Year

(Excludes Savings Initiatives)

$M

Key Operational Cost Components

Cost Bucket

Packaging

Logistics

Raw Products

Other

Total

% of Op Costs

~25%

~15%

~35%

~25%

100%

F08 Increase

~$15-20

~$0-5

~$50-60

~$35-40

~$110

F07 Increase

~$25

~$15

~$60

~$45

~$145

6

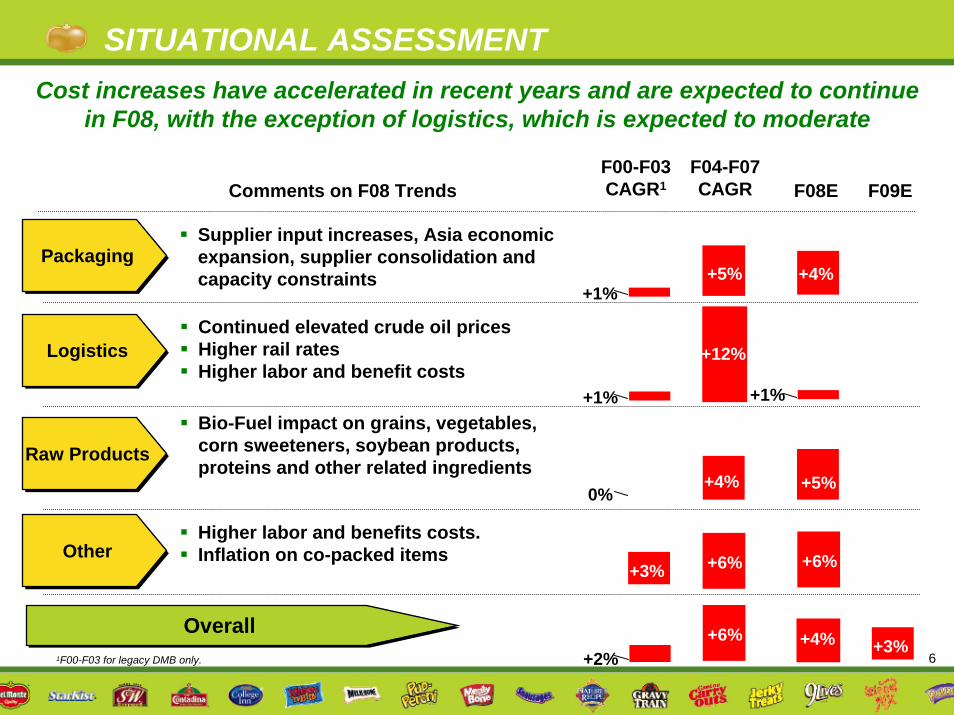

SITUATIONAL ASSESSMENTCost increases have accelerated in recent years and are expected to continue

in F08, with the exception of logistics, which is expected to moderate

PackagingPackaging

Raw ProductsRaw Products

LogisticsLogistics

OtherOther

Supplier input increases, Asia economic expansion, supplier consolidation and capacity constraints

Bio-Fuel impact on grains, vegetables, corn sweeteners, soybean products, proteins and other related ingredients

Continued elevated crude oil pricesHigher rail rates Higher labor and benefit costs

Higher labor and benefits costs.Inflation on co-packed items

F08EF04-F07CAGR

F00-F03CAGR1Comments on F08 Trends

Overall1F00-F03 for legacy DMB only.

Overall

+5% +4%

0%

+1%

+12%

+4% +5%

+6%

+6%

+6%

+4%

F09E

+2%+3%

+1%

+3%

+1%

7

SITUATIONAL ASSESSMENTSuperior supply chain value –Beyond cost competitiveness

Supply Chain excellence is driven by:Lean

• Cost competitiveness• Constant improvement focus• Managing inventory levels

On-Demand• Customer promotion execution – one chance to meet the consumer

demand• Responsiveness to satisfy dynamic customer requirements

Consistently exceed customer expectations• Match Del Monte supply delivery to specific customer strategies• High store in-stock levels

8

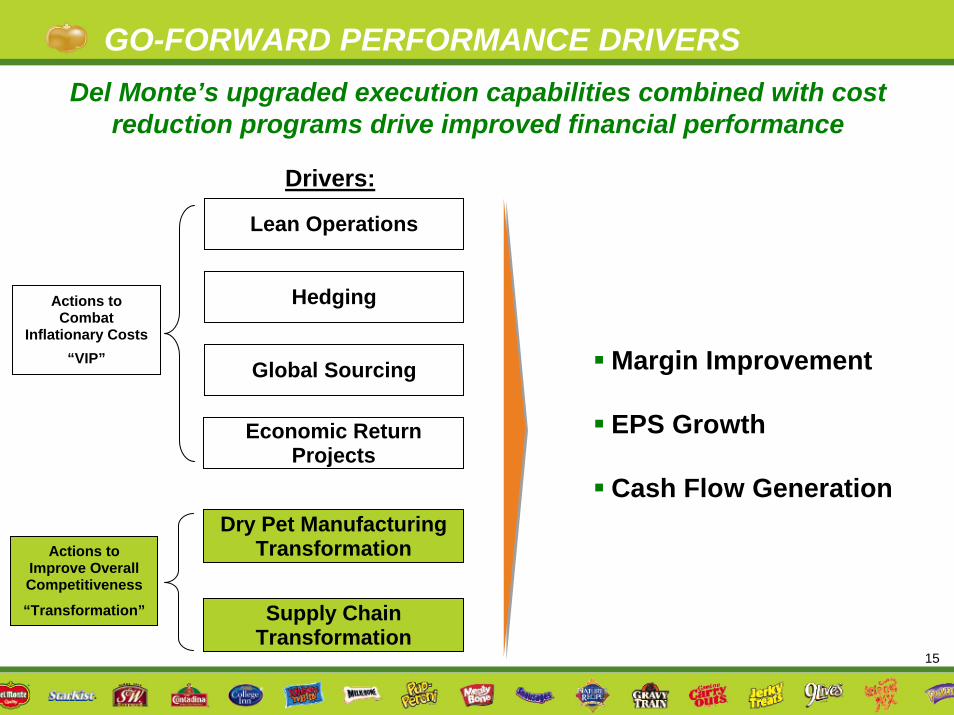

GO-FORWARD PERFORMANCE DRIVERS

Lean OperationsLean Operations

Drivers:

Del Monte’s upgraded execution capabilities combined with cost reduction programs drive improved financial performance

Dry Pet ManufacturingTransformation

HedgingHedging

Global SourcingGlobal Sourcing

Supply Chain Transformation

Actions to Improve Overall Competitiveness

“Transformation”

Actions to Combat

Inflationary Costs“VIP”

Actions to Combat

Inflationary Costs“VIP” Margin Improvement

EPS Growth

Cash Flow Generation

Economic Return Projects

Economic Return Projects

9

SUMMARY: INFLATIONARY OFFSETSVIP and Transformation Plan savings combat inflationary costs in

the short term and build the overall competitiveness of the business in the long term

100150200250300350400450500550

F05 F06 F07 F08 Cum. Gross Cost ChangeCum. Net Cost Change

Inflationary Offsets$M

VIP Cost Reduction Programs (~$60M in F08)

• Lean Operations• Hedging• Global Sourcing• Economic Return Projects

Transformation Plan Savings (~$15M in F08)

• Supply Chain Optimization• Dry Pet Food Distributed

Manufacturing

Key Drivers

$120

$270

$415

$525

$100

$205

$295$330

VIP and TransformationCost Savings

% of CostIncreases

Offsetin that year

~15% ~30% ~40% ~70%

10

GO-FORWARD PERFORMANCE DRIVERS

Lean OperationsLean Operations

Drivers:

Del Monte’s upgraded execution capabilities combined with cost reduction programs drive improved financial performance

Dry Pet ManufacturingTransformation

HedgingHedging

Global SourcingGlobal Sourcing

Supply Chain Transformation

Actions to Improve Overall Competitiveness

“Transformation”

Actions to Combat

Inflationary Costs“VIP”

Actions to Combat

Inflationary Costs“VIP” Margin Improvement

EPS Growth

Cash Flow Generation

Economic Return Projects

Economic Return Projects

11

DRIVER: LEAN OPERATIONSLean Operations is about the identification and elimination of the

seven forms of waste

INVENTORY MOTIONTRANSPORTATION WAITING

OVER PRODUCTION OVER PROCESSING DEFECTS

12

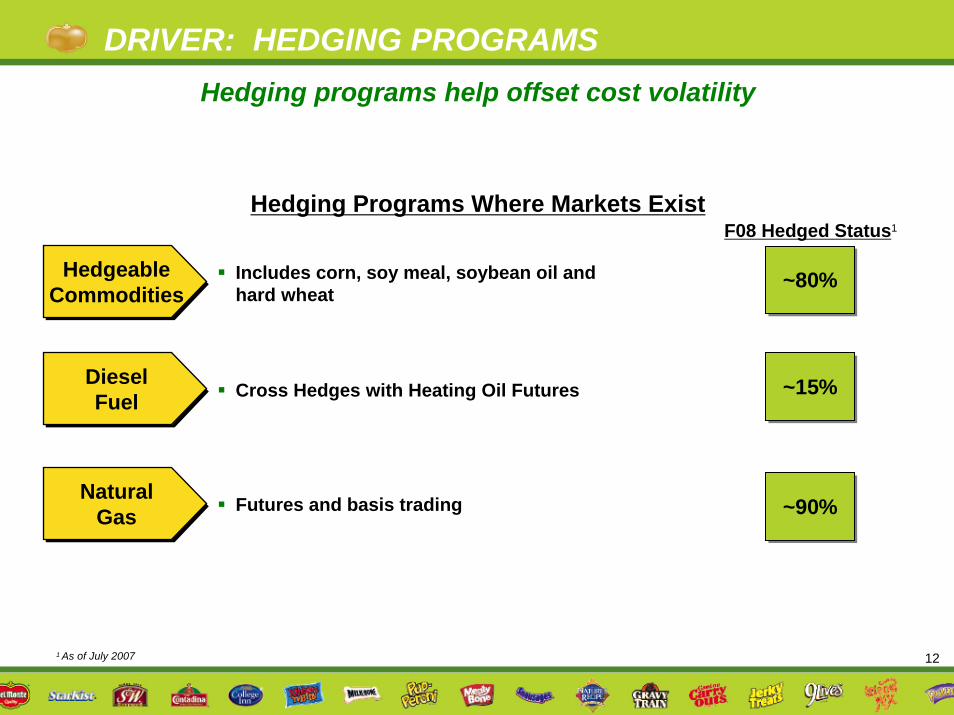

DRIVER: HEDGING PROGRAMSHedging programs help offset cost volatility

HedgeableCommoditiesHedgeable

CommoditiesIncludes corn, soy meal, soybean oil and hard wheat

Hedging Programs Where Markets Exist

~80%~80%

F08 Hedged Status1

DieselFuel

DieselFuel Cross Hedges with Heating Oil Futures ~15%~15%

NaturalGas

NaturalGas ~90%~90%Futures and basis trading

1 As of July 2007

13

DRIVER: LONG TERM RELATIONSHIPSLong-term relationships where hedging programs do not exist

PackagingPackaging Long-term contracts with Silgan (2010) and Impress (2011) Long-term relationship with Fort Dearborn (10 years)

FruitFruit Long-term relationships with ~300 growers~60% of growers are 2nd generation; 30+ years with Del Monte

VegVeg Long-term relationships with ~700 growers~85-90% growers are returning, 30% are 2nd and 3rd generation growers

TomatoTomato Long-term relationships with ~20 growers~25% of growers are 2nd generation; 30+ years with Del Monte

TunaTuna Spot and term contracts Negotiated directly with tuna vessel owners and cooperatives

14

DRIVER: GLOBAL SOURCINGInternational sourcing expertise capitalizes on global food supply

chain, with quality assurance controls in place

Asia

North America

South America

Expectations:Product ConsistencyProduct SafetyContinuous Improvement

Enhanced Measurement Tools:Vendor certification process3-Tier Audit SystemInternational QA/Tech service group

for in-country oversight

Quality Assurance

Del Monte has both the quality control and technical capabilities to expand our

current global sourcing volumes

Finished Goods Sourcing

Raw Products/ Ingredients Sourcing

Asia

North America

South America

15

GO-FORWARD PERFORMANCE DRIVERS

Lean Operations

Drivers:

Del Monte’s upgraded execution capabilities combined with cost reduction programs drive improved financial performance

Dry Pet ManufacturingTransformation

Hedging

Global Sourcing

Supply Chain Transformation

Actions to Improve Overall Competitiveness

“Transformation”

Actions to Combat

Inflationary Costs“VIP” Margin Improvement

EPS Growth

Cash Flow Generation

Economic Return Projects

16

DRIVER: DRY PET MANUFACTURING TRANSFORMATION

Redrawing the dry pet food manufacturing footprint –Reducing miles by ~5M in F07 and F08

Topeka

Decatur

Bloomsburg & Buffalo

Pet Food acquisitions have enabled a more cost effective distributed dry pet food manufacturing footprint

17

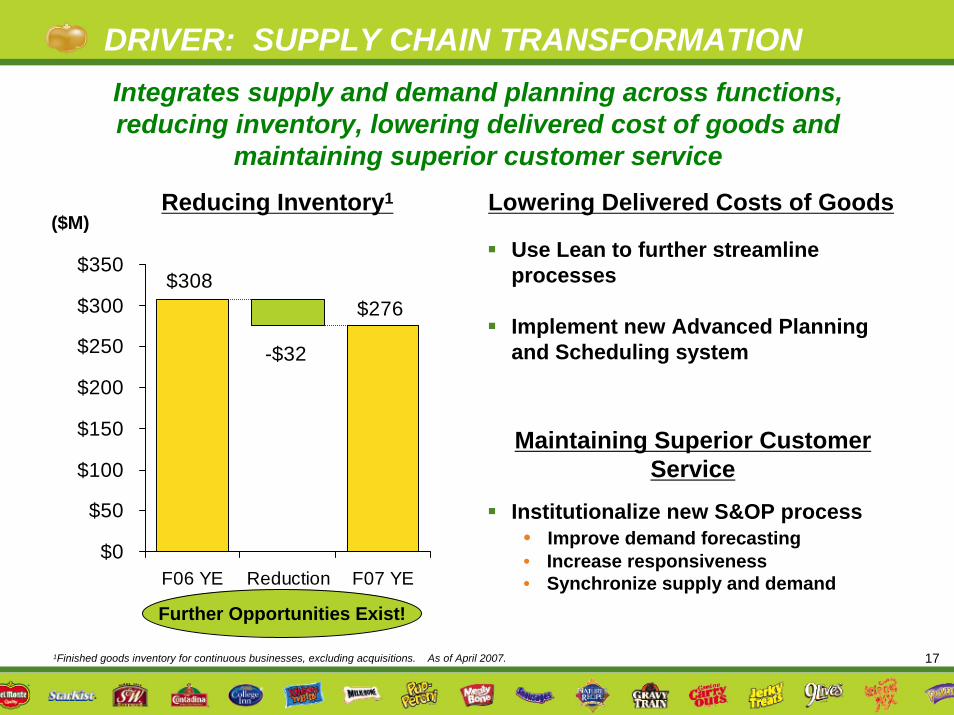

DRIVER: SUPPLY CHAIN TRANSFORMATION

$276$308

-$32

$0

$50

$100

$150

$200

$250

$300

$350

F06 YE Reduction F07 YE

Integrates supply and demand planning across functions, reducing inventory, lowering delivered cost of goods and

maintaining superior customer serviceReducing Inventory1 Lowering Delivered Costs of Goods

($M)Use Lean to further streamline processes

Implement new Advanced Planning and Scheduling system

Maintaining Superior Customer Service

Institutionalize new S&OP process• Improve demand forecasting• Increase responsiveness• Synchronize supply and demand

Further Opportunities Exist!

1Finished goods inventory for continuous businesses, excluding acquisitions. As of April 2007.

18

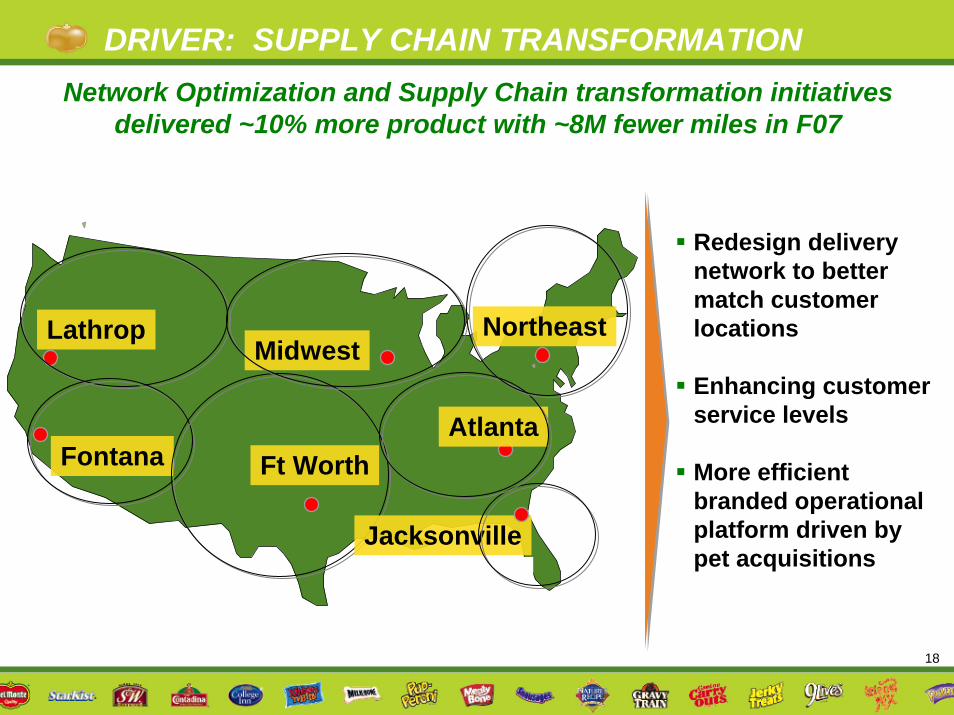

DRIVER: SUPPLY CHAIN TRANSFORMATIONNetwork Optimization and Supply Chain transformation initiatives

delivered ~10% more product with ~8M fewer miles in F07

Redesign delivery network to better match customer locations

Enhancing customer service levels

More efficient branded operational platform driven by pet acquisitions

Ft Worth

MidwestLathrop

Fontana

Jacksonville

Atlanta

Northeast

19

KEY TAKEAWAYSToday’s building blocks driving tomorrow’s earnings growth

FutureTodayOverall competitive cost structure

Effective supply chain

Continued inflationary cost pressures

Aggressive actions being taken to reduce costs

Transformation initiatives well underway

Enhanced competitive cost structure, driven by pet manufacturing improvement

Advantaged supply chain from customer’s perspective

Moderating, normalized cost pressures

Lean and other efficiency programs well embedded into organizational culture

Transformation completed and savings on-going; overall competitiveness enhanced

20

Q&A

Top Related