Languages

Pages

Legal

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 1 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Date: 20 Jul 2006

Mrs Smita Shukla

Recommended Books –

1. International Finance – PG Apte (Best book but for higher level. Students who have finance

background may opt for this. Can be referred by novices like me for Forex Arithmetic)

2. Multinational Finance – Madhu Viz (Most Recommended for all. But not the best book for

Forex Arithmetic)

3. International Finance – Jain & Others (A balanced book for theory and numericals). 4. International Finance – Levi

5. Global Finance Markets – Giddy

6. Foreign Exchange and Derivative – Jain and Others

7. International Finance – Bhalla.

Students should build their knowledge by regularly going through business journals,

magazines and newspapers.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 2 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

What is Foreign Exchange?

Foreign Exchange loosely refers to any foreign currency. In deeper sense, it is purchase and

sale of one currency against sale and purchase of another currency. Here, currency does not

necessarily mean bank notes and coins but includes Travellers Cheques, Bills of Exchange,

Letters of Credit, any drafts, etc as well. In essence any financial instrument that entitles

you to get another currency in lieu of one currency is treated as currency for this definition.

International Foreign Currency market is almost round the clock market starting in

Tokyo/Sydney in the morning and closing in West Coast of USA shortly before it is time

for opening of next day market in Tokyo (effect of changing time zones).

Indian Forex Market

Indian Forex Market is still in nascent stage of development. Prior to 1991, we had FERA

which made possession of Foreign currency a criminal offence. Exchange rate was decided

by the RBI and Forex market virtually did not exist. Post 1991, after replacement of FERA

with FEMA, and current account convertibility, Indian forex market has begun to develop.

With exports volume growing steadily at good pace, forex market is becoming important.

The Foreign Exchange Management Act (1999) popularly known as FEMA came into

force from June 01, 2000. FEMA replaced the Foreign Exchange Regulation Act of 1973

(FERA). While FERA was aimed at conserving foreign exchange by restricting

expenditure, FEMA is aimed at facilitating external trade and payments for promoting

orderly development and maintenance of foreign exchange market in India. Violations

under FEMA are considered civil offence and not criminal offence as was the case under

FERA.

In India, most of the trade happens in USD. Besides US Dollar, Euro, Great British Pound,

and Japanese Yen are other major currencies that are traded. Other currencies are also dealt

but in small volume. SBI deals in 16 currencies in all.

Exchange rates are not constant and keep changing on minute to minute basis like stocks in

stock market. Unlike “Stock Exchange”, there is no “Forex Exchange” where there is a

central intermediary available for every transaction and hence single quote for any currency

is not available. It is more like a vegetable market where there are so many shops and each

is quoting its own rate for each vegetable and willing to bargain with you. Or, in the market

language, it is Over the Counter (OTC) trade.

Foreign Currency Exchange Rate

The primary basis for exchange rate movement on day to day basis is Demand and Supply

of foreign currency. Demand can spurt due to various reasons like large companies with

considerable import requirements (like Maruti requiring import from Suzuki, Japan) stocking forex

for future requirement. Similarly, exporters may dump their forex holding if they perceive

that rupee is going to appreciate, leading to sudden excess availability of foreign currency

in the market.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 3 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Although the exchange rate is affected by market forces of demand and supply, we do not

have a fully flexible exchange rate, or as it is called Floating Exchange Rate, as yet. What

we actually have is a Managed Exchange Rate.

What it means is that exchange rate is being macro managed by the Govt through RBI. RBI

keeps a hawk eye on the forex market and keeps manipulating exchange rate by either

buying excess forex or injecting liquidity by selling forex from its own holding of 165

Billion US Dollars.

Like, SEBI is the controller of the Securities market, RBI is the controller of Forex market

in India. It authorises certain entities like banks and even other companies like Thomas

Cook to deal in Forex. It has a dealing room of its own which keeps track of exchange rate

movement in the market on continuous basis. If the exchange rate starts moving wildly in

either direction, it intervenes by either buying or selling forex in the market to control it.

Factors Affecting the Exchange Rate

(a) Balance of Payment position of the country

(b) Strength of economy

(c) Fiscal and Monetary policy

(d) Interest rates

(e) Political Factors

(f) Exchange control

(g) Central Bank Intervention

(h) Speculation

(i) Technical Factors

(j) Other factors.

Balance of Payment - Balance of Payment is the measure of demand and supply

of foreign currency. If the balance of payment is positive and high (Exports higher

than imports), it will lead to excess supply of foreign currencies and therefore local

currency will appreciate. In the reverse case, domestic currency will depreciate.

Strength of the Economy - If the economy is strong and growing, foreign

investment/capital will pour into the country, again causing excess supply of

foreign currencies leading to appreciation of local currency.

Fiscal and Monetary Policy - If fiscal policy leads to high deficit, it will result in

inflation and therefore excess supply of local currency. High inflation rate leads to

high interest rates (interest rates are mostly maintained a few percent higher than inflation rate

so that real effective interest rate is positive) leading to weakening of local currency.

Interest Rates - Higher interest rates attract foreign currency deposits provided

local currency is not depreciating faster than interest rate induced growth. Thus,

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 4 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

higher interest rates coupled with relatively stable local currency acts like a self

sustaining process. More inflow of foreign currency leads to further stability of

exchange rates.

Political Factors - If a govt is considered to be unstable, or change of govt with

socialistic inclination is expected, local currency will weaken. Currency will

strengthen if the new govt is expected to take capitalistic policy decisions.

Exchange Control - Exchange control is generally aimed at free movement of

capital flows and therefore foreign nationals will be wary of investing in the

country.

Central Bank Intervention - Already explained as to how central bank can affect

exchange rate in the short term.

Speculation - This is again a short run effect if some big players suddenly start

accumulating foreign currency or vice versa for speculative reasons. Constant

buying by big players and resultant upward movement in price leads even smaller

player to start buying aggressively and foreign currency appreciates.

Technical Factors - Technical factors work best in free market. Indian forex

market is still not as free and therefore they do not have much effect.

Other Factors - These are general factors which are hard to define. It could be

world political and economic situation, prices of major import constituent like crude

oil, etc. Fear of war with Pakistan can send the Rupee down overnight.

Reference Rate

What we have discussed above is mechanics of day to day changes in exchange rate. But

how is the basic exchange rate of one currency set against the other currency? How is it

determined that a dollar should cost approximately Rs 45 and not Rs 25?

Current mean of Rs 45 or so is called Reference Rate. This reference rate is decided using

various different methods: -

(a) Mint Parity System – Simply stated this system is based on amount of

currency printed by any country for each ounce or Kg of gold. If India prints

Rs 30,000 for each ounce of gold held with govt and US prints US$ 600 for

each ounce of gold held with USA, exchange rate between US$ and INR

would be – 30,000/600 = Rs 50 per dollar.

(b) Gold Standard System – This system started in mid 1870s and lasted till

1914 ie till start of World War I. In this system, the coins had a fixed gold

content and ratio of gold content in coins of any two countries denominated

their exchange rate. In case of paper currency, amount of gold freely

payable by Govt/Central Banks of two countries for each unit of paper

currency determined the exchange ratio. The countries were committed not

to print currency in excess of their gold holding or dilute the gold content in

coins. However, during the World War I, countries began to renege on this

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 5 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

commitment to meet the funding requirement of the war and the gold

standard collapsed.

Many countries tried to revive the Gold Standard after the war ended

in 1919 but failed. In the economic depression that followed the WW-I,

when they tried to withdraw additional money they had pumped into the

economy during the war, it led to Deflation (reverse of inflation where commodity

prices start falling due to low demand (because people do not have money to buy goods)

which deters the entrepreneurs and is therefore bad for economy). They, therefore, had

to wait for the economies to recover. But by the time they began their next

attempt a couple of decades later, World War II started in 1939 and lasted

till 1944. Thus, this standard was abandoned.

(c) Bretton Woods System – Post World War II, in 1946, the newly-created

Economic and Social Council of the United Nations called a conference at

the Bretton Woods where in the troika of post-War economic agencies ie

International Monetary Fund (IMF), World Bank and International Trade

Organisation (ITO – which later came in avatar of GATT) were born.

Countries were allowed to declare their currency value in gold or dollars and

USA promised to freely exchange an ounce of gold for US$ 35 or vice

versa. Since this system was born during Bretton Woods conference, this

standard came to be known as Bretton Woods system.

The system worked very well till 1969. However, when USA got

embroiled in the long and costly Vietnam war, its economy suffered. The

U.S. trade balance on goods and services shifted to a surprising deficit in

1971. These deficits supported speculations that the dollar was overvalued.

France realised that it was beneficial to exchange its forex holding into gold

and began to convert it. Because of massive gold outflows from the United

States, President Nixon suspended convertibility of the dollar in August

1971. This ended the Bretton Woods System.

(d) Smithsonian Agreement - IMF’s attempts in the subsequent period to revive

Bretton Woods system were unsuccessful as USA did not agree to make

dollar convertible to gold. In the following period, there was complete

chaos. In an attempt to restore order to the exchange market, 10 leading

nations met at the Smithsonian on December 16 and 17, 1971. The

“Smithsonian Agreement” was a new system of exchange-parity values.

Although this new system was still a dollar-standard exchange-rate system,

the dollar, was still not convertible to gold. Smithsonian Agreement

collapsed within 15 months and a de facto system of floating rates emerged.

(e) Now we have following systems of Exchange Rate being followed by

different countries as per their convenience:

(i) Fixed Exchange Rate Systems

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 6 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

(aa) Currency Board

(ab) Fixed Peg

(ac) Flexible Peg

(ii) Floating Exchange Rate Systems

(aa) Managed Float System

(ab) Independent Float System

Scientific Way of Deciding Exchange Rate Between Currencies

1. Purchasing Power Parity System - This theory is based on the law of one price, the

idea that, in an efficient market, identical goods must have only one price. This is

thus Real Effective Exchange Rate (REER). A basket of representative goods and

services has been identified and its cost in each country in its domestic currency is

calculated. The ratio between its costs in any two countries in their respective

domestic currencies is their exchange rate. To understand it better, let us take a case

of cost of hair cut in India and US. While the average price of a hair cut in India is

Rs 15, it costs US$ 3 in US. If this was to represent average ratio of costs for all the

goods in the basket, purchasing power parity of US$ would be 5 against INR.

The differences between PPP and market exchange rates can be significant.

For example, on plain conversion of Yuan to dollar basis, per capita GDP in China

is about USD 1,500, while on a PPP basis, it is about USD 6,200. Same is the case

of India. Per Capita GDP by PPP in 2000 = USD 2686) At the other extreme,

Japan's nominal per capita GDP is around USD 37,600, but its PPP figure is only

USD 31,400.

Exchange Rate = Price in domestic market for basket of goods = Pd

Price in foreign market for basket of goods Pf

This is called absolute version of PPP.

These special exchange rates are often used to compare the standards of living of

two or more countries. The adjustments are meant to give a better picture than

comparing gross domestic products (GDP) using market exchange rates.

2. Relative Purchasing Power Parity – This is a related theory, which predicts the

relation between the two countries' relative inflation rates and the change in the

exchange rate of their currencies. This is the economist’s definition. In business

terms, it helps in deciding Forward Rate of Forex from Spot Rate by taking inflation

into account.

Suppose, present Exchange Rate of dollar in India is Rs 47 and inflation in

India is 5% and in US 1%. Thus, cost of same product after one year in India =

PD (1+ 0.05) and in US = PF (1+ 0.01).

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 7 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Thus, exchange rate after one year = PD (1+ 0.05)

PF (1+ 0.01)

= Rs 48.86

But Inflation is not the only element that affects the long term exchange

rates. Interest rate is another element that severely affects the exchange rate (although interest rates are often a direct function of inflation, Interest rates is pegged to covered

the depreciation of money through inflation and a little as incentive. Thus, if inflation is low, interest

rates would automatically be correspondingly low).

3. Interest Parity Theory – Effect of interest on exchange rate is called Interest Parity

theory. Let us see how a smart operator can benefit by playing currency of two

countries having differential interest rates and gain from it.

Suppose, current exchange for US$ is INR 46. RBI bond interest rate is 7%

and US treasury interest rate is 2%. A smart American investor instead of investing

in US treasury bill would invest in RBI bonds. (this is what NRIs do with NRE and other

accounts). However, whole thing is not as simple as it appears. When such arbitrage

opportunity occurs, many people try to utilise the opportunity and resulting excess

supply leads to fall in exchange rate. Further, inflation in India is higher than in US.

Therefore, on maturity of deposit, reverse conversion of Rupee deposit to dollars is

going to be at higher cost than the original conversion rate Thus, losing of some

gains.

Sterilisation of Forex

While every country is bending over backwards to earn as much forex as possible, there is

limit of each economy to absorb forex inflow. Uncontrolled influx of forex can be harmful,

especially the hot money which can be withdrawn at short or nil notice, like portfolio and

stock market investment with capital account convertibility. (This is what was the prime cause of

South Asian Economic crisis of 1997). Also, influx of huge funds leads to inflation. Therefore,

there are times when forex inflows have to be checked or controlled. Technically such a

process is called Sterilisation of Forex. Recently, India adopted this approach by reducing

interest rates on NRE deposits which made parking of funds in India less attractive.

Another way of sterilisation is to liberalise Imports. Surge in imports takes away excess

supply of dollars in the market. Yet another method is to repay the old debts.

The methods we discussed above are the planned and controlled method of

Sterilisation of Forex. In addition, there could be host of uncontrollable and unpredictable

reasons leading to sterilisation, like –

(a) Threat of War

(b) Increase in oil prices

(c) Political Instability

(d) Govt Policies

(e) Social Disturbance

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 8 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Fixed Exchange Rate Systems

1. Currency Board – Currency Board arrangement is one where a country declares

value of its domestic currency against some other strong currency. In this system,

currency notes issued by the country depend upon the declared exchange rate and

the amount of foreign currency reserves. If India gets into US currency Board and

has a forex reserve of US$ 150 Billion and exchange rate is Rs 40, India can issue

150 x 40 = 6000 Billion Rupees worth of currency notes. Thereafter, Indian

currency will move in tandem (same ratio) with USD. Domestic currency is also

fully convertible into foreign currency and vice versa. However, in this case,

monetary policies have to be in consonance with other country. Thus, it kills the

economic sovereignty of the nation and therefore difficult to follow.

Examples are Argentina, Hong Kong, Estonia, and Bulgaria

2. Fixed Peg – In this system, exchange rate is declared by the country and ratified by

the IMF. Thereafter, exchange rate does not change till it is revised by the Govt.

Reluctance by the govt to revise the rate due to political or other compulsions can

lead to long term consequences. South East Asian crisis was partly result of this

system.

Reasons for South East Asian Crisis (1997)

(a) Countries had adopted complete convertibility on Current as well as Capital

account. This made flight of capital very easy. There was no way to control

outward flight of capital at the time of crisis.

(b) They adopted Fixed Peg system against dollar. There was massive influx of

foreign currency through hot investments, foreign currency loans by banks,

etc. This money was invested in assets like real estate and stocks. There was

massive rise in asset prices and an asset bubble was created.

(c) There was massive current account deficit. Imports far exceeded exports.

(d) High inflation rates due to increased money supply. Inflation was not

reflected in exchange rate; firstly, due to Fixed Peg system and secondly,

due to govts’ reluctance to revise the rate downwards which would have

affected investors’ sentiments. Speculators suddenly realized that due to

overvalued currencies, it was beneficial to convert local currency into

dollars and they went for it hammer and tongs. Due to relatively small size

of economies (a few tens of billion dollars each), and therefore small forex

reserves, in three trading sessions, Forex reserves became nil.

3. Flexible Peg System – This system provides a “Parity band” which allows limited

flexibility for movement of exchange rate on either side of the parity rate. Bands

can be very narrow or very wide. Examples are Bangladesh, China, and Egypt.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 9 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Floating Exchange Rate Systems

1. Managed Float – This is the system that we are currently following in India.

Exchange rate is free to float but under constant watch of Central Bank (RBI). It

generally intervenes only on occasions when there are wild movements. It basically

acts as stabiliser.

2. Independent Float – In this system Govt is just not bothered which way its

currency is moving. This is the system followed by rich and advanced countries like

USA, Kuwait, Saudi Arabia, etc.

India followed Fixed Peg System since independence. Indian rupee was pegged against UK

₤. In 1966, rupee was devalued. In 1975, India moved away from ₤ parity and pegged its

rupee against an unknown basket of 5 currencies. It devalued rupee once again during the

Balance of Payment Crisis in 1991. From 1993, we started following floating rate exchange

system.

Impossible Trinity (The three events that can not occur together)

(a) Having Fixed Peg system of Exchange Rate.

(b) Having complete convertibility on current and capital account.

(c) Having complete independence in deciding monetary policy.

No country to date has ever been able to achieve all the three conditions together at

any point of time. That is why it is called impossible trinity.

Why did economies of Argentina, Chile and Mexico crash?

Argentina Economic Crash – 2001

Argentina had been having a see saw economy ever since the beginning of 20th

century. It

was the 4th

largest economy in early 1915, fell down drastically in late 70s & 80s and then

again recovered to become 56th

economy in 1996. It suffered its first crash in 1929 during

American Stock Market Crash. It recovered from there to become 15th

largest economy

only to suffer yet another crash in 1970s and 1980s. In 1980, the inflation was as high as

5000%. In a matter 22 years, ie between 1970 and 1992, money got devalued by 10 billion

times. Yes! 10 billion pesos were reduced to a single peso.

Economic reforms launched in 1991 reduced inflation from 2300% in 1991 to just 1% in

next few years. However, the recovery was short lived. Some wrong currency policies of

Govt and economic crisis in countries like Mexico, Brazil and Russia, triggered another

economic crisis in 2001.

In 1991, a currency stabilization regime established a currency board, which pegged the

Argentine peso to the dollar on a 1-to-1 basis. Inflation was virtually eliminated. Foreign

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 10 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

investment returned. GDP growth was strong in the early 1990s, but unemployment

increased as a result of extensive structural reforms. Argentina finally seemed to have a

handle on its chronic economic problems. However, external events in the late 1990s

buffeted the Argentine economy:

1995: Mexico

1997: East Asia

1998: Russia

1999: Brazil

Because of its long history of economic instability, every economic crisis in the Third

World, particularly in Latin America, caused investors to pull out of Argentina, creating a

self-fulfilling prophesy. It was investors’ hair-trigger reaction to crises elsewhere that

caused Argentina’s instability, Thus, the adverse effects of these crises were greater in

Argentina than in most other new-growth economies. Another reason for this enhanced

vulnerability is that Argentina stood alone with its fixed-exchange-rate policy, whereas the

floating currencies of its neighbours depreciated. By 2001, the peso was significantly

overvalued, in no small part due to the dollar itself having become overvalued. The

devaluation of the Brazilian real had a particularly large effect. It reduced demand from

Argentina’s largest trading partner, and businesses began to move from Argentina to Brazil

in search of lower production costs. As the credibility of the peso at its pegged value

declined, and the government had to expend huge sums to support the currency, which in

turn necessitated more borrowing. Under these conditions, interest rates that were already

high rose even higher, and as both debt and interest rates rose, the ability of the government

to service its debt became increasingly doubtful. Argentina continued to keep the peso

pegged to the dollar by external borrowings.

The buzzards came home to roost in December 2001. The nation rapidly descended into an

unprecedented chaos. As economic activity shuddered to a virtual halt, governments

resigned and were hastily replaced amid sporadic rioting. The following month, when

Eduardo Duhalde (the fifth person to hold the presidency in two weeks) unpegged the peso

in January 2002, the peso crashed hard, losing more than 70% of its value and inflation

rising to 41% though it was still far far better than the expectations of four digit hyper

inflation experienced in late 80s decades. But inflation had fallen back to 3.2% by 2003.

So, we know now what agony was the country saved from by the much maligned and ever

pouting Mr PV Narsimha Rao, who displayed the rare courage to stand up against the

economically blind political class of the country (including his own party men) in

appointing Mr Man Mohan Singh as Finance Minister; and the practical economist Mr Man

Mohan Singh himself, whose economic prescriptions to cure the ills of the economy were

as effective as any measures ever were any where in the world in its modern history.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 11 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Mexican Economic Crisis

Mexican Economic trouble of 1994 was not a ‘Crash’ but a Crisis as it lasted just 10

months and the melt down was not as spectacular as in Argentina. This crisis was also

triggered by wrong currency policies of the govt. In Dec 1994, Mexican Peso fell from the

pegged rate of 3.3 peso to a dollar to 7.7 peso.

Though the crisis was triggered by; first: the devaluation of currency in December 1994

and second: floatation of currency soon after; the seeds were sown earlier.

Mexico had a fixed exchange rate of 3.3 peso to a dollar. In 1994, as the general election

drew near, the incumbent govt went into a spending blitz (politicians are same every where). As

a result, current account deficit ballooned to a record of 7%. In order to fund the spending,

the govt issued bonds repayable in dollars. High current account deficit and fixed exchange

rate led to over valuation of Peso by approximately 20%. Some investors were alarmed;

other smelled the opportunity; and together they quickly encashed the bonds in dollars.

Foreign exchange reserves fell drastically. Declining reserves necessitated devaluation of

currency. However, political compulsions did not allow this simple but hard prescription

till the incumbent govt lasted.

Next Govt which took over power in Dec 1994, devalued the currency to 4 pesos to dollar.

That did not prove adequate and within days peso was allowed full float which led to

crashing of peso to 7.2 pesos to a dollar.

Mexico’s immediate neighbour, USA, intervened immediately by first buying pesos from

open market and then arranging a loan of US$ 50 billion. The currency then stabilized first

at 6 pesos to a dollar and thereafter gradually declining over next two years to 7.7 dollars

before beginning a regular recovery. Mexico repaid all loans by 1997.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 12 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

27 Jul 2006

FOREX MARKET AND FOREX ARITHMETIC

Forex market is open almost 24 hrs a day. It starts in Tokyo and ends in West Coast of

USA. By the time it closes in USA West Coast, it is within 2.5 hrs of opening of Tokyo

market for the next day.

Total trade in the Forex market is to the tune of over US$ 5 trillion per day. The Indian

Forex Market turnover itself averages US$ 5-10 billions/day.

Communication System – Forex Market has a dedicated worldwide telecommunication

network called SWIFT (Society for Worldwide Interbank Financial Telecommunications).

Forex Dealers

There are two kinds of forex dealers in the market:

(a) Full Fledged Money Changers – Mostly designated banks and Thomas

Cook (an exception). These are the authorized dealers who are permitted to

take positions. An authorized dealer deals in millions of dollars each day.

They can go long or short (overbought or oversold positions). They are also

allowed to appoint their franchisees.

(b) Restricted Money Changers – These are the kind of money changers who

line up the streets in tourist centres. They can only buy forex. They are not

allowed to sell. They are essentially convenience centres for tourists for

currency exchange.

One peculiarity of Forex Market is that it is mostly unregulated and completely driven by

the Demand-Supply principal. There are few benchmarks. Rates fluctuate minute by

minute, dealer by dealer, and customer by customer. There is nothing fixed. Two people

doing a sell deal with the same dealer at the same time in the same place and of same

currency may end up with vastly different rates. Money changers are free to quote their

own rate for buying and selling any currency (technically called Bid and Ask rates

respectively) based on customer, size of deal, their own current positions, etc.

How to make a Quote?

All money changers are connected to Reuters through SWIFT. The Reuters screen

continuously flashes current going rate for various currencies at different centres. However,

the rates are only indicative. They are representative rates for market as a whole. Individual

rates with various dealers vary.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 13 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Exchange Rates are quoted in following format: -

USD/INR = )(

)( 9000.46/8000.46 AskRate

BidRate

Above represents amount of currency in denominator (here INR) to be paid for each unit of

currency in numerator (here USD). Quotation is always in double numbers with minor

difference between the two. First number is called the Bid Rate and second number is

called Ask Rate. Bid rate is always lower than the Ask Rate.

Bid Rate is the rate at which the money changer is willing to buy a particular currency.

Ask Rate is the rate at which the money changer is willing to sell same currency.

Spread – As stated earlier, there is always a positive difference between Ask Rate and Bid

rate. This difference is called Spread and it is the profit margin that the dealer earns by

trade.

Spread = Ask Rate – Bid Rate

Spread % = 100

BR

BRAR

Forex market behaves like any other commodity market. Here too, there is whole sale and

retail market.

Whole sale market consists of Authorised Dealers and Big Corporate Houses like TCS,

Infosys and Wipro who have high forex exposures. But spreads in whole sale market are

lower.

Retail Market is populated by money changers, ordinary citizens, small exporters and

importers and small corporates.

Positions

In any financial market, two positions can be taken

(a) Long or overbought position and

(b) Short or oversold position.

Why are positions created?

Positions are taken in anticipation of currency exchange rate movement in one direction.

If a position is taken and the trend appears to be reversing (currency depreciates against

expectation of appreciation or vice-versa), the positions are liquidated by manipulating the

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 14 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Bid and Ask rates. Example - If it is a long/overbought position, both Ask and Bid rates

will be lowered. Similarly, if there is an oversold position, both Ask rate and Bid Rate will

be hiked.

The quotations are normally in four decimal places. If a dollar is being quoted against

Rupee, it will be quoted as follows: -

46.5230/46.5250

First figure of quote is Bid Rate and second figure is Ask Rate. Third and fourth decimal

places are called PIPS. Thus, in the above case, 30 and 50 are pips.

In most cases, quotations are abbreviated to give only two or three digit pips in place of

Ask Rate. Thus, above quote could also be represented as: -

46.5230/50

Inter dealer quotes are further abbreviated to only three digit pips on both sides since base

rate of up to first decimal place is common across all dealers and therefore assumed to be

known.

Arbitrage

As in any other trade, arbitrage opportunities exist in Forex trade also. Arbitrage is

basically taking advantage of rate differential at two locations or markets or sources. For

instance, Bid (Buying) Rate of one dealer may be higher than Ask (Selling) Rate of another

dealer. A smart operator can buy from second dealer and sell to first dealer and earn some

money. This transaction is called Arbitrage. Let us see the above process in numbers.

Dealer A Dealer B

46.5030/46.5080 46.5090/46.5095

In the above case, Bid Rate of Dealer B (46.5090) is higher than Ask Rate of Dealer A

(46.5080). If a person Buys one million dollars from Dealer A and sells to Dealer B, he

earns - 0.0010 x 1,000,000 = Rs 1000

This is also called Single Point Arbitrage since there is only one Buying and Selling

operation involved. It normally happens when the deal is in single market involving two

dealers

Inverse Quote – Also called “Indirect Quote”. Normally, value of other currency is quoted

in local currency, ie, amount of local currency to be paid for each unit of foreign currency.

In India, all currencies are quoted using INR as the base, ie, value of other currency is

quoted in Indian Rupees. Similar practice is adopted by all other countries, using their local

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 15 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

currency as base and indicating number of local currency to be paid for each unit of other

currency.

Thus, a person will obtain USD/INR quote = 46.3020/46.3090 from a dealer in India and

INR/USD quote = 0.0213/0.0224 from another dealer in USA (US currency is used as base in

USA. So, the quotation will be number of USD to be paid for each INR). If the bases of quotes are

different, how do we compare the quotes? Comparison of two quotes becomes difficult.

Therefore, there is a need to INVERSE one of the quotes so that the base is common.

USD/INR = 46.3020

Inverse the quote

INR/USD = 0216.0 46.3020

1

)/(

1

INRUSD

That was a simple case when only mean rate is given. Now let us see what happens

when bid and ask rates are quoted.

USD/INR = 46.3020/46.3090

021597.046.3020

1

)/(

1

BIDASK INRUSDUSD

INR

021594.03090.46

1

)/(

1

ASKBID INRUSDUSD

INR

(Please note that for finding BID rate, we have to inverse ASK rate and for finding ASK rate we have

to inverse BID rate. What is the logic for this?

Currency trade is basically a BARTER trade. In any other trade, commodity is traded against a

currency. However, in currency trade, both sides have currencies but of different type. It is like one

side having wheat and the other side having rice and both ready to exchange their commodity for the

other’s for a negotiated exchange rate. In such a situation there is no seller and no buyer. Saying it

other way round, both are sellers and both are buyers. When one buys other’s commodity, he

simultaneously sells his commodity. So, when one trader says – I am willing to sell one dollar for

Rs 47, it can also be interpreted as - he is willing to buy Rupee for 1/47 dollar. Thus, his ASK rate

of Rs 47 for a dollar has become his BID rate for a Rupee in inverse quote at 1/47 dollar. Therefore,

when currency quotes (exchange rates) are inversed, Bid and Ask rates also have to be inversed).

Two Point Arbitrage – When two locations are involved in the dealing, it is possible to buy

a currency from one location/market and sell it in other market and earn arbitrage. For

example, some one can purchase dollars in India and sell them in US market for Rupee.

This is called Two Point Arbitrage.

Three Point Arbitrage – Some times Arbitrage opportunity is available by currency

exchange operations across two or three markets. In such an operation, first one currency is

purchased in one market and then sold in second market for a third currency. Third

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 16 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

currency is then sold in third or first market for original currency.

Suppose, there are three currencies A, B and C. Quotes are available for A/B, B/C and C/A

(C/A)BID = (B/A)BID X (C/B)BID

ASKASK

BIDCBBA

AC)/(

1

)/(

1)/(

AND

(C/A)ASK =(C/B)ASK X (B/A)ASK

BIDBID

ASKBACB

AC)/(

1

)/(

1)/(

Forward Quotes

Forward quotes are one where a dealer quotes for purchase and selling of forex at a future

date. These quotes are mainly useful for exporters and importers who commit to sell their

ware or import goods based on exchange rate prevailing on that date. However, money is

received or paid in foreign currency at a much later date. Any large adverse movement of

exchange rate in the interim can lead to heavy losses. Therefore, importers and exporters

cover their risk by utilisation of these forward quotes. Various terminologies associated

with forward quotes are as follows:

Spot Deal – Settlement on T+2 days (‘T’ refers to Transaction Date. Thus, delivery of

forex and payment of cash for a transaction done on Monday has to be completed (settled)

by Wednesday)

Spotcash Deal – Settlement on T + 0 days (Same day payment and delivery)

SpotTom Deal – Settlement on T + 1 Day (Next Day Payment)

Forward deals could be T+10, T + 30, T + 90, etc. (Add 2 working days for each settlement).

Inter Dealer Forward Quotes are not elaborate. Only differential amount to spot deal rates

are quoted. Thus, if

If GBP/INRspot = 85.8680/85.8950

Then, 30 days FP (Forward Premium) is quoted as 30/40, which means

30 days FP for GBP/INRspot = (85.8680 + 0.0030) / (85.8950 + 0.0040)

= 85.8710/85.8990

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 17 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

It is possible that Bid FP for a Forward Quote is higher than Ask FP. If such a situation

occurs, it means that local currency is expected to appreciate. If local currency appreciates,

for each unit of foreign currency, lesser amount of local currency would be paid. Thus, in

such a situation, the quoted differential amount is decreased rather than added to Spot

quotes.

In the above example, if dealer quotes were 40/30, then 30 days FP would be:

30 days FP for GBP/INRspot = 85.8680 - 0.0040 /85.8950 - 0.0030

= 85.8640/85.8920

In the Forward Deals there are more variations –

Out Right Forward Deal – A deal where there is only one transaction of sell or buy at a

future date. So, you decide to buy one million dollars after 60 days.

Spot Forward Deal – A deal where there is a Spot Deal and a covering deal on a future

date. So, you buy one million dollars today and strike a forward deal for selling one million

dollars after 60 days.

Forward Forward Deal – There is a Buy and a covering Sell deal on a future date (future

dates of buy and sell deals are different). So, you do a forward deal to buy one million

dollars after 30 days and do another forward deal to sell one million dollars after 45 days.

Broken Date/Forward Rate Calculation

Quotes are available for one month, three months or six months. There may be requirement

to calculate for a date in between these quoted dates, say for 1½ months or 3 months and 25

days. Such calculations are done by intrapolation of quotes for available dates

(extrapolation is never done for dates beyond max quote). Let us take an example for

conceptual clarity:

Spot USD/INRSpot = 46.8000/46.9000

1 month FP = 50/80

3 months FP = 100/200

6 months FP = 200/300

Find forward rates for 1 month 15 days and also for 3 months 25 days.

Ans. For 1 month 15 days =

daysdays

daysdays

1560

80200

1560

50100

(“60” because 3 months minus 1 month = 60 days)

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 18 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

= 30

13

= 46.8050 + .0013 / 46.9080 + 0.0030

= 46.8063 / 46.9110

For 3 month 25 days =

daysdays

daysdays

2590

200300

2590

100200

= 70.27

7.27

28

28

= 46.8100 + .0028 / 46.9200 + 0.0028

= 46.8128 / 46.9228

Forward Premium/Discount Computation

FP = 10012

nSR

SRFR

MR

MRMR (MR means Mid Rate which is average of Bid and Ask Rates)

If FP is (+)ve, then foreign currency is appreciating

If FP is (–)ve then forward deal is at a discount which means that local currency is

expected to appreciate.

Spot USD/INR = 46.8030/46.8500 Mid Rate = 46.8265

3M FR = 46.9030/46.9500 Mid Rate = 46.9265

n = 3 months

Forward Premium = 1003

12

46.8265

46.8265- 46.9265

= 0.8542 Thus, there is a 0.85% premium on forward quotes.

In case the result was in negative, then there was a discount, which means that foreign

currency is going to depreciate and local currency is expected to appreciate.

Factors Affecting the Forex Forward Quote

1. Inflation – The currency of the country experiencing higher inflation rate will

depreciate in value

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 19 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

2. Interest Rate – Capital will move from low interest rate country to higher interest

country. Thus, currency of country with higher interest rate will appreciate due to

higher demand.

Forward Rate =

RF

RD

I

ISpotRate

1

1

Where

IRD = Interest Rate in Domestic Market

IRF = Interest Rate in Foreign Market

Interest Arbitrage

Interest Arbitrage refers to the international flow of short term liquid capital (Fixed

Deposits denominated in Foreign Currencies or Convertible local currency) to earn a higher

interest abroad. In India, we have NRIs investing in fixed deposits to earn higher interest

rates. Interest arbitrage can be uncovered or covered.

Uncovered Interest Arbitrage

In order to be able to take benefit of higher interest opportunity in foreign country, it is

often necessary to convert the domestic currency to foreign currency while investing in

foreign country and then reconverting principal and interest earned to local currency at the

time of maturity.

In countries where interest rates are higher, inflation is also higher. (nominal interest rate is

mostly equal to real interest rate + inflation). When inflation is higher, the currency mostly

depreciates over time. Thus, there is a risk of depreciation of investment due to lower

exchange rate during the re-conversion after maturity. If such a foreign exchange risk is

covered through forward, we have covered interest arbitrage, else, we have uncovered

interest arbitrage.

Suppose, interest rate in India is 11% where as it is 5% in US. A US investor will earn 6%

extra per year or 3% every 6 months if he invests in India. However, since inflation rate is

also high in India at 5% compared to just 2% in US, INR is likely to depreciate. If INR

depreciates by 3% over one year, net return on investment by US investor falls to barely

3%. However, in case INR depreciates by more than 6%, the US investor will end up as net

loser (and we have not even considered the transaction costs in conversion and reconversion processes).

Covered Interest Arbitrage

The scenario given above is not beyond real life events. In order to insure against exchange

rate risks, investors usually go for covered interest rate arbitrage.

In this case, investor converts his investment into foreign currency at spot rate and at the

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 20 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

same time sells forward the amount of foreign currency he is investing plus the interest he

would earn to coincide with maturity date of investment. Though, he would be paying

some premium for forward cover, he is insured against depreciation of currency. His return

on investment will reduce by the amount of premium paid for forward deal compared to

uncovered interest arbitrage, but that is the price to be paid for insurance.

But such opportunities do not last long due to two reasons.

(a) As funds move out of the home country, the interest rates rise there due to

resultant paucity of funds. Vice versa, as additional funds flow in to foreign

country, excess liquidity of capital causes interest rates to soften there.

(b) As demand for forward deals on currency of other country rise, premium on

forward deals increases. Thus, the cost of transaction (conversion and

reconversion of currency) increases and eats into profits to be earned from

interest rate arbitrage.

Thus, the interest rate differential keeps reducing and forward premium keeps

increasing till it comes to a level where it is no more advantageous to invest in foreign

country.

Problem 01

Exchange rate for USD in India is

Spot: 45.0020

6 month forward: 45.9010

Interest rate (annual) in the money market is as follows:

USA: 7%

India: 12%

Work out the arbitrage opportunity.

Solution

Given Spot USD/INR = 45.0020

6 Months Forward = 45.9010

Interest Rate USA = 7% and India = 12%

Forward Rate =

RF

RD

I

ISpotRate

1

1

=

12

6

100

71

12

6

100

121

0020.45

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 21 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

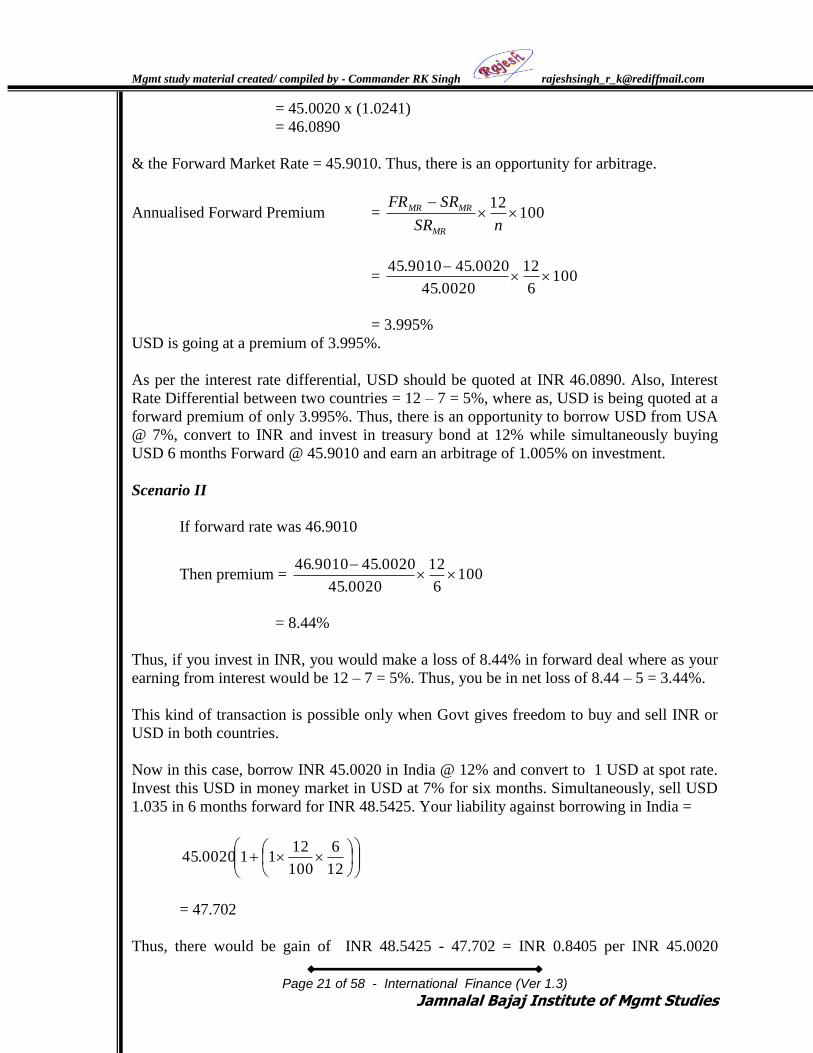

= 45.0020 x (1.0241)

= 46.0890

& the Forward Market Rate = 45.9010. Thus, there is an opportunity for arbitrage.

Annualised Forward Premium = 10012

nSR

SRFR

MR

MRMR

= 1006

12

0020.45

0020.459010.45

= 3.995%

USD is going at a premium of 3.995%.

As per the interest rate differential, USD should be quoted at INR 46.0890. Also, Interest

Rate Differential between two countries = 12 – 7 = 5%, where as, USD is being quoted at a

forward premium of only 3.995%. Thus, there is an opportunity to borrow USD from USA

@ 7%, convert to INR and invest in treasury bond at 12% while simultaneously buying

USD 6 months Forward @ 45.9010 and earn an arbitrage of 1.005% on investment.

Scenario II

If forward rate was 46.9010

Then premium = 1006

12

0020.45

0020.459010.46

= 8.44%

Thus, if you invest in INR, you would make a loss of 8.44% in forward deal where as your

earning from interest would be 12 – 7 = 5%. Thus, you be in net loss of 8.44 – 5 = 3.44%.

This kind of transaction is possible only when Govt gives freedom to buy and sell INR or

USD in both countries.

Now in this case, borrow INR 45.0020 in India @ 12% and convert to 1 USD at spot rate.

Invest this USD in money market in USD at 7% for six months. Simultaneously, sell USD

1.035 in 6 months forward for INR 48.5425. Your liability against borrowing in India =

12

6

100

12110020.45

= 47.702

Thus, there would be gain of INR 48.5425 - 47.702 = INR 0.8405 per INR 45.0020

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 22 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

invested or 3.44%.

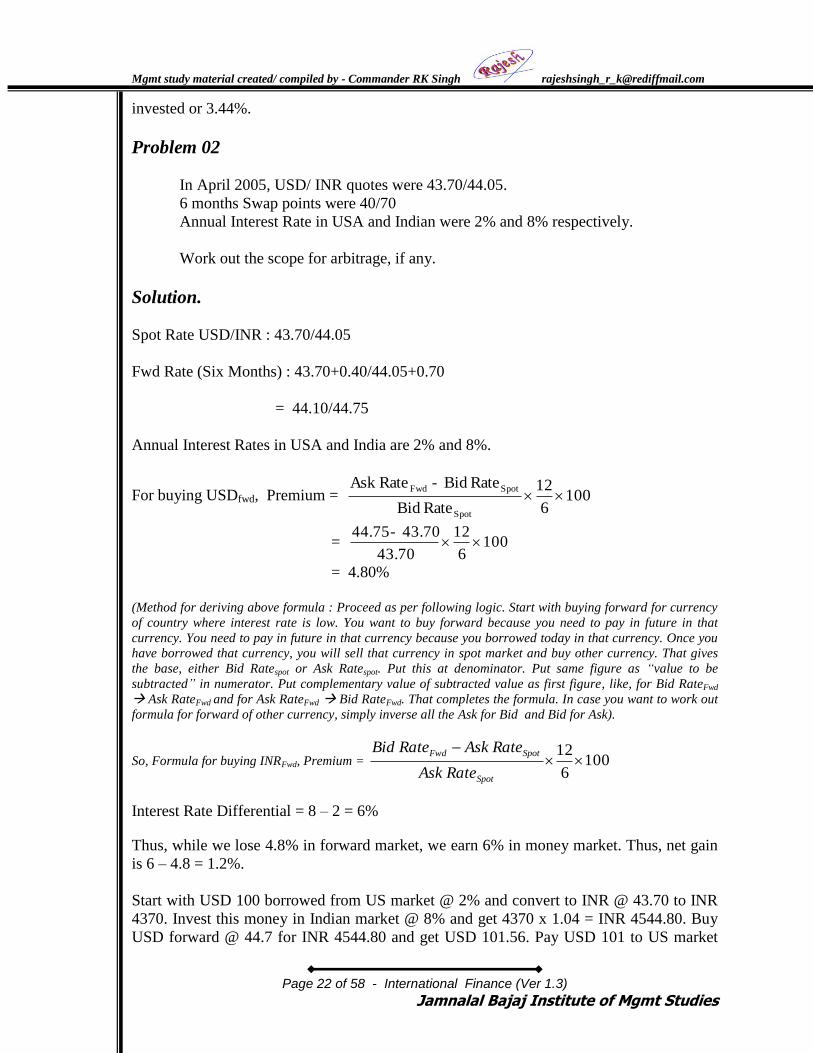

Problem 02

In April 2005, USD/ INR quotes were 43.70/44.05.

6 months Swap points were 40/70

Annual Interest Rate in USA and Indian were 2% and 8% respectively.

Work out the scope for arbitrage, if any.

Solution.

Spot Rate USD/INR : 43.70/44.05

Fwd Rate (Six Months) : 43.70+0.40/44.05+0.70

= 44.10/44.75

Annual Interest Rates in USA and India are 2% and 8%.

For buying USDfwd, Premium = 1006

12

Rate Bid

Rate Bid - RateAsk

Spot

SpotFwd

= 1006

12

43.70

43.70 - 44.75

= 4.80%

(Method for deriving above formula : Proceed as per following logic. Start with buying forward for currency

of country where interest rate is low. You want to buy forward because you need to pay in future in that

currency. You need to pay in future in that currency because you borrowed today in that currency. Once you

have borrowed that currency, you will sell that currency in spot market and buy other currency. That gives

the base, either Bid Ratespot or Ask Ratespot. Put this at denominator. Put same figure as “value to be

subtracted” in numerator. Put complementary value of subtracted value as first figure, like, for Bid RateFwd

Ask RateFwd and for Ask RateFwd Bid RateFwd. That completes the formula. In case you want to work out

formula for forward of other currency, simply inverse all the Ask for Bid and Bid for Ask).

So, Formula for buying INRFwd, Premium = 1006

12

Spot

SpotFwd

RateAsk

RateAskRateBid

Interest Rate Differential = 8 – 2 = 6%

Thus, while we lose 4.8% in forward market, we earn 6% in money market. Thus, net gain

is 6 – 4.8 = 1.2%.

Start with USD 100 borrowed from US market @ 2% and convert to INR @ 43.70 to INR

4370. Invest this money in Indian market @ 8% and get 4370 x 1.04 = INR 4544.80. Buy

USD forward @ 44.7 for INR 4544.80 and get USD 101.56. Pay USD 101 to US market

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 23 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

and keep USD 0.56 as covered interest arbitrage profit.

Interest Rate Differential, Covered Interest Arbitrage and Interest Parity Theory

3

2

Arbitrage

1

0

-1 .

.

-2

-3

-3 -2 -1 0 1 2 3 Forward Exchange Rate – Discount or premium in percent per annum

Explanation of the above figure

Arbitrage Outflow will take place

1. If (+)ve interest rate differential is > Forward Discount like at Point A, Interest Rate

Differential = 2, and Fwd Discount = 0.5

2. If Forward Premium > (–)ve Interest Rate Differential like at Point A’,

Fwd Premium = 2.2, and Interest Rate Differential = - 1.05

Arbitrage Inflow

3. If Forward Discount > (+)ve Interest Rate Differential, like at Point B,

Fwd Discount = 2.7, and (+)ve Interest Differential = 1.2

4. If (–)ve interest Rate Differential > Forward Premium, like at Point B’,

–ve Interest Rate Differential = 2.2, and Forward Premium = 0.7

Arbitrage

Outflow

Arbitrage

inflow

.A’

.B

A

Inte

rees

t D

iffe

ren

tial

in

fav

our

of

fore

ign

co

un

try

in

per

cen

t p

er a

nnu

m

Interest

Parity

B’

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 24 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Sample Practice Questions on Exch Rate (Forex Arithmetic)

Q1. The Spot Rate of two banks in US Market for GBP is as follows:

GBP/USD: Bank A: 1.4550/1.4560

Bank B: 1.4380/1.4548

Find Whether Arbitrage is possible.

Ans. Bank B 1.4380 1.4548

Bank A 1.4550 1.4560

The Ask Rate of bank B for selling a GBP is USD 1.4548 which is less than Bid Rate of

bank A at 1.4550. Thus, it is possible to buy GBP from bank B and sell to bank A and earn

an arbitrage of USD 0.0002 for each GBP traded. In the above diagram, the triple line in

green indicates the arbitrage opportunity. If the two lines, double line and solid thick line

had overlapped, then there was no arbitrage opportunity.

Q2. Rate for USD in Indian Market is as follows:

USD/INR: 46.2000/3000

Inverse the quotes.

Ans. 2000.46

1

/

1/

BID

ASKINRUSD

USDINR

= 0.021645

3000.46

1

/

1/

ASK

BIDINRUSD

USDINR

= 0.021598

Q3. In the Forex Market, following are the rates:

USD/JPY: 110.25/111.10

USD/AUD: 1.6520/1.6530

AUD/JPY: 68.30/69.00

Find Whether Arbitrage is possible in terms of AUD/JPY.

Ans. In this case, if we inverse the rate of USD/AUD and get AUD/USD, our job will

become easy.

6050.06530.1

1

/

1/

ASK

BIDAUDUSD

USDAUD

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 25 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

6053.06520.1

1

/

1/

BID

ASKAUDUSD

USDAUD

AUD/JPY = AUD/USD X USD/JPY

(AUD/JPY)BID = (AUD/USD)BID X (USD/JPY)BID

2533.6710.1116520.1

1/

6969.6625.1106530.1

1/

ASK

BID

JPYAUD

JPYAUD

By Three Point Arbitrage - AUD/JPY = 66.6969/67.2533

Forex Market Rate for AUD/JPY = 68.30/69.00

Thus, there is a difference of almost one JPY for each AUD in two situations.

So, to earn arbitrage, Sell JPY and buy USD @ 111.10.

Then sell USD and buy AUD @ 1.6520. Now sell 1.6520 AUD and buy JPY @

JPY 68.3 for AUD 1.

83.11230.686520.1

Thus, for every JPY 111.10 put into market, there is a return of JPY 112.83.

Q4. Following are the quotes in New York:

GBP/USD: 1.5275/85

USD/CHF: 1.5530/39

(a) What rate do you expect for GBP in Basle?

(b) If Basle quote is 1GBP = 2.3320/30 CHF, then find whether Arbitrage is

possible?

Ans GBP/USD: 1.5275/85, USD/CHF: 1.5530/39

CHF

GBPCHF

USDUSD

GBP

3751.2

3722.2

5539.1

5530.1

5285.1

5275.1

3751.23722.2

CHFGBP

Basle Quote = 1GBP = 2.3320/30 CHF

GBP is cheaper to buy in Basle at 2.3330 CHF. Therefore, buy one GBP in Basle

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 26 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

and sell in New York for USD 1.5275. Then sell USD 1.5275 for 2.3722 CHF and earn an

arbitrage of (2.3722 - 2.3330) = 0.0398 CHF per GBP or

2.3722 CHF = 3722.23330.2

1

= 1.0168 GBP

So, the Arbitrageur will make GBP 0.0168 for every GBP traded.

Q5. Following are the EUR/INR quotes:

Spot: 49.9525/80

1 Month Forward: 100/120

3 Month Forward: 225/255

6 Month Forward: 300/275

Find absolute forward quotes.

Ans. 1 Month Forward: 49.9625/700

3 Month Forward: 49.9750/835

6 Month Forward: 49.9225/305

Q6. A bank is quoting following rates:

EUR/USD: 1.5975/80

2 Month Forward Points :20/10

3 Month Forward Points: 25/10

Further,

AED/USD rate is 3.7550/60

2 month forwards points: 20/40

3 month Forward points: 30/50

A firm wishes to buy AED against EUR 3 month forward. Find the rate to be quoted by

the bank.

Ans. AED/USD = 3.7550/60

3 months Forward Rate = 3.7580/610

EUR/USD: 1.5975/80

3 months Forward Rate = 1.5950/70

BID

ASKUSDEUR

EURUSD/

1/

5950.1

1/ ASKEURUSD

62696.0

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 27 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

ASK

BIDUSDEUR

EURUSD/

1/

62617.0

5970.1

1/

ASKEURUSD

EUR

USD

USD

AED

EURAED

3532.2

62617.07580.3

BIDBID

BID EUR

USD

USD

AED

EURAED

3572.2

62696.07610.3

ASKASK

ASK EUR

USD

USD

AED

EURAED

So, AED/EUR = 2.3532/80

Money Market Hedging

Q1. An American Exporter will be receiving ₤ 1,000,000 three months from now. Spot

Rate for GBP/USD = 1.6 Rate of interest in USA and London Money market is

10% and 5% respectively. Suggest hedging strategies for the exporter.

Ans: Exporter should borrow ₤ 987,654 from London Money Market @ 5%, convert to

USD 1,580,247 and invest in US for 3 months @ 10%. After 3 months he will get

USD 1,580,247 + 39,506 = USD 1,619,753 and will need to pay ₤ 1,000,000 which

he can when he receives his payment 3 months later. Thus, he earns USD 19,753 as

arbitrage. There is no need to hedge the position for his borrowing with a forward

cover since he has natural hedge in terms of earning.

Q2. An American importer has to pay ₤ 1,000,000 to a party in London 3 months from

now for the denim import it has made. The Spot rate for GBP is 1.6 USD. It is

expected that USD may depreciate further in future. Rate of Interest in USA is 5%

and in UK it is 10%. Suggest hedging strategies for importer.

Ans: This is a slightly peculiar case. Normally, the currency of country where interest

rate is high, depreciates. But in this case USD is expected to depreciate despite US

interest rates being lower. But that makes the job of importer much easier.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 28 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

The American importer needs to pay 1.6 x 1,000,000 = USD 1,600,000 at

current rates. Since he needs to pay 3 months later, and USD is expected to

depreciate in the meanwhile, he can convert USD to GBP now and invest in UK @

10% per annum. He will earn 2.5% interest in 3 months. To be able to have GBP

1,000,000 three months from now, he should invest GBP 1,000,000/1.025 = GBP

975,610 now. GBP 975,610 = USD 1,560,976.

So, he should borrow USD 1,560,976 and convert to GBP and invest in UK

market @ 10%. Three months later, he will get GBP 1,000,000 (principal + interest)

and pay his liability. In US, he will have to pay only USD 1,580,488 to bank

instead of USD 1,600,000 and thus save USD19,152 as arbitrage. His position has

been also hedged simultaneously.

Interest Rate Arbitrage

Q3. A Customer obtains following quote-

EUR/USD: 1.2930/1.3270

Annual USIBBR/US IBOR: 4/5.5%

Annual LIBBR/LIBOR: 6/9%

Calculate the likely limits for the Forward Rate between the two countries.

Ans: Suppose you borrow USD 1.3270 @ 5.5% for one year. Your liability after one

year = 1.3270 + 5.5% = USD 1.4000. Convert this USD 1.3270 to EUR 1.0000 and

invest in bank @ 6%. You will earn EUR 1.0600

Sell EUR 1.0600 in Forward market. Bid Rate should be such that your money does

not fetch you more than your liability for payment (USD 1.4000 in this case)

So, 1.06 x ForwardBid ≤ 1.4000 Thus, Forward EUR/USDBid ≤ 1.3208

Now take the Reverse Arbitrage

Borrow EUR 1 @ 9% for one year. Your liability after one year = EUR1.0900

Convert (sell EUR) this EUR 1 to get USD 1.2930 and invest in bank @ 4%.

You will earn USD 1.34472. Using this USD 1.34472, buy EUR in forward market.

Forward EUR/USDAsk rates should be such that it yields you less than your liability

(EUR 1.0900 in this case).

1.34472 / FR ≤ EUR1.0900, or FR ≥ 1.34472 / 1.0900

Forward EUR/USDAsk ≥ 1.2337

Ask rate should always be higher than Bid Rate and forward spread should be more

than spot spread. Spot spread is 0.0340. If we increase the spread by another 10

points, ie, 0.0350 and add to Bid Rate. We get the range as

Forward EUR/USDAsk = 1.3208/1.3558

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 29 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

FOREX RISK MANAGEMENT THROUGH FUTURES

A future is an exchange-traded derivative which is similar to a forward. Both futures and

forwards represent agreements to buy/sell some underlying asset in the future for a

specified price. Both can be for physical settlement or cash settlement. Both offer a

convenient tool for hedging or speculation. For little or no initial cash outlay, both

instruments provide price exposure without a need to immediately pay for, hold or

warehouse the underlying asset. In this sense, both instruments are leveraged. Futures and

forwards trade on a variety of underliers: wheat, oil, live beef, Eurodollar deposits, gold,

foreign exchange, the S&P 500 stock index, etc.

The fundamental difference between futures and forwards is the fact that futures are traded

on Exchanges. Forwards trade over the counter. This has three practical implications.

1. Futures are standardized instruments. You can only trade in the specific contracts

supported by the exchange. Forwards are entirely flexible. Because they are

privately negotiated between parties, they can be for any conceivable underlier

(currency) and for any settlement date. Parties to the contract decide on the notional

amount and whether physical or cash settlement will be used. If the underlier is for

a physically settled commodity or energy, parties agree on issues such as delivery

point and quality.

2. Forwards entail both market risk and credit risk. A counterparty may fail to perform

on a forward. With futures, there is only market risk. This is because exchanges

employ a system whereby counterparties settle profits or losses on daily basis.

Through these margin payments, a futures contract's market value is effectively

reset to zero at the end of each trading day. This all but eliminates credit risk.

3. The daily cash flows associated with margining can skew futures prices, causing

them to diverge from corresponding forward prices.

A future is transacted through an authorised brokerage firm. Working through their

respective brokers, two parties will transact a trade. Legally, that trade is structured as two

trades, both with a clearinghouse owned by or closely affiliated with the exchange. For

example, suppose Party A and Party B trade. Party A is long and Party B is short. This

would be legally structured as

Party A being long on One million USD futures at Rs 47 with the

exchange's clearinghouse being the counterparty; and

The exchange's clearinghouse being long on One million USD futures at

Rs 47 with Party B being the counterparty.

Party A and B then have no legal obligation to each other. Their respective legal

obligations are to the exchange's clearinghouse. The clearinghouse never takes market risk

because it always has offsetting positions with different counterparties.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 30 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

Before you can trade a futures contract, the broker collects a deposit from you called initial

margin. This may be in the form of cash or acceptable securities. The broker holds this

deposit for you in a margin account. The amount of initial margin is determined according

to a formula set by the exchange. For a single futures contract, it will be a small fraction of

the market value of the futures' underlier. For futures spreads, or if you are using futures to

hedge a physical position in the underlier, initial margin may be even lower. Generally,

initial margin is intended to represent the maximum one-day net loss you could reasonably

be expected to incur on a position.

Through the margining process, futures settle every day. Unlike a Forward, where all

contract obligations are satisfied at maturity, obligations under the futures contract are

satisfied every day on an ongoing basis as mark-to-market profits or losses are realized.

This essentially eliminates credit risk for futures.

Maintenance Margin is some fraction - perhaps 75% - of initial margin for a position.

Should the balance in your margin account fall below the maintenance margin, your broker

will require that you deposit funds or securities sufficient to restore the balance to the initial

margin level. Such a demand is called a Margin Call. The additional deposit is called

Variation Margin. Should you fail to make a variation margin payment, your broker will

immediately liquidate some or all of your positions.

Mechanism of Futures Trading

Components of Futures Trade

1. Futures Players

(a) Hedgers – These are the importers and exporters who mitigate their risk of

unfavourable movement of exchange rate when they need to buy or sell the

foreign currency at a future date.

(b) Speculators – These are investors who buy or sell foreign currency with the

sole aim of earning money through correct anticipation of movement of

exchange rate. Even though they are essentially gamblers, they are an

important component of market as they provide the liquidity and stability in

the market.

(c) Arbitrageurs – These are people who utilise the opportunities presented by

market due to asymmetric forex exchange bid and ask rates in the same

market or in different markets

2. Clearing Houses – Futures trade is an organised trade. Futures are traded through

exchanges akin to Securities Exchanges which provide performance guarantee for

all the players. They play the role of buyer for every seller and vice versa. Thus,

every trading party in the futures market has obligation only to the clearing house.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 31 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

3. Margin Requirement – The risk of default of any player is insured by imposing the

requirement of depositing the margin money which is adequate to cover the adverse

movement of currency in the short term. Thus, margins are not uniform and vary

across markets, contracts, currencies and duration of contract. Since the currency

movement is not as wild as stocks, the margin requirement is also relatively small. (Usually in the range of 5% of contract value).

4. Daily Settlement – Notional losses or gains incurred due to fall in the value of the

currency are required to be settled between the party and the broker on daily basis

to ensure maintenance of original level of margin (security) money. This is

technically called “Mark to Market”.

5. Delivery Date – There are two types of contracts – European Contract, which are

delivered/encashed only on the last day of the contract period and American

Contracts, which can be delivered/encashed on any day during the contract period.

6. Manner of Delivery – The contract settlement, technically called “Delivery”, can be

done by either of the following three modes:

(a) Physical exchange of underlying assets ie Exchange of currencies.

(b) Cash Settlement as in the case of Stock Index Futures. There is no exchange

of currencies and only differential amount is paid.

(c) Reversing Trade - It is the process of offsetting a long position by acquiring

a short position or vice versa. The two positions square at the end of the day.

7. Types of Orders –

(a) Market Order – Order placed with broker to Buy or sell at prevailing market

price.

(b) Limit Order – Buy or sell order at a specific price or better.

(c) Fill-or-Kill Order – It instructs broker to fill an order immediately at a

specified price.

(d) All or none Order – It allows broker to fill part of the order at specified

price and remaining at other price/s.

(e) On the Open or Close Order – This represents order to trade within a few

minutes of opening or closing of the exchange.

(f) Stop Order – It triggers a reversing trade when prices hit a prescribed limit.

Functions of Futures Markets

Futures Markets function as –

1. Price Discovery Agent

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 32 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

2. Speculation Tool

3. Hedging Tool

Price Discovery

“Futures” prices are generally treated as a consensus forecast by the market of prices of

currency/commodity at the contract expiry date. Thus, for all and sundry, it is a free

forecast available to them. Empirical studies have revealed that such forecasts are not very

accurate, yet they are the best among all the alternatives available. More often than not,

they provide a reasonably good hint in case of currencies and commodities but not equally

accurately in case of stocks.

Speculation

Futures provide excellent tool for speculation since it is highly leveraged (only margin amount

of approximately 5% needs to be paid upfront). Also, the transaction costs are lower than in case of

delivery. Thus, percentage returns are higher.

Speculators are categorised based on the length of positions they hold.

(a) Scalpers – They have the shortest holding horizons, typically closing a

position within minutes of initiation.

(b) Day Traders – They hold futures positions for a few hours but never longer

than one trading session. They open and close positions within the same

day. Their net holding at the end of any day is always zero. They play on the

scheduled announcements and news related to money supply, trade deficit

etc.

(c) Position Traders – They have longer holding horizons, often a few months.

There are two types of position traders:

(i) Outright Position Holders – He takes position based on his belief

on the underlying potential. He stands to make large gains or losses.

(ii) Spread Position Holders – He does not have belief on a particular

currency or commodity, but he speculates on relative movement of

two commodities. So he holds simultaneous position in two

commodities, long in commodity which is likely to appreciate and

short in commodity which is likely to depreciate. The two

commodities could be from same basket, like wheat and rice or

could be from different baskets like wheat and Steel. If the spread

between them widens, he gains else he loses. Such positions are less

risky than Outright Positions.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 33 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

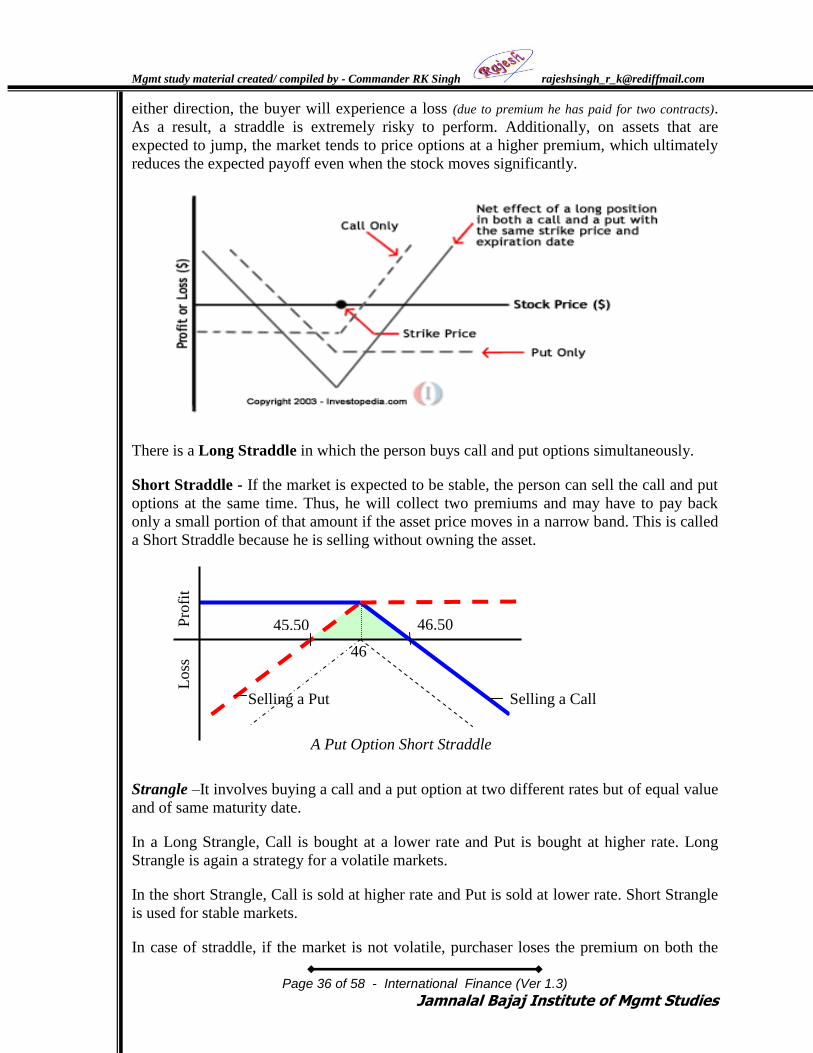

Hedging

Hedging is process of engaging in a futures or forward contract by paying a small premium

to eliminate risk associated with large unfavourable movement in exchange rate by the time

payment or receipt is due. There are three types of hedges:

(a) Long Hedge/Anticipatory Hedge – Investor does not own the asset but

wants to purchase the same in foreseeable future. He protects against

adverse price movement of the large escalation in prices of that asset by

long hedge.

(b) Short Hedge – An investor already owns an asset which he wants to sell in

future. He wants protection against steep fall in its prices. He hedges the risk

by selling its future.

(c) Cross Hedge – The act of hedging ones position by taking an offsetting

position in another good with similar price movements. Although the two

goods are not identical, they are correlated enough to create a hedged

position. A good example is cross hedging a long position in crude oil

futures contract with a short position in natural gas. Even though these two

products are not identical, their price movements are similar enough to use

for hedging purposes. In currency matters, USD and Canadian Dollars can

be used for cross hedging.

Mgmt study material created/ compiled by - Commander RK Singh [email protected]

Page 34 of 58 - International Finance (Ver 1.3)

Jamnalal Bajaj Institute of Mgmt Studies

FOREX RISK MANAGEMENT THROUGH OPTIONS

An Option is a contract which gives its buyer the right either to buy (Call Option) or to sell

(Put Option) a specified amount of a currency within/after a specified period at a

predetermined price called Strike Price. An Option that gives the right to buy is called a

Call Option and an Option that gives the right to sell is called a Put Option.

An option gives the buyer right to buy or sell but there is no obligation to do so. A buyer is

at liberty not to exercise his option. But the seller is under obligation to honour the call or

put option if the buyer decides to exercise it. And the buyer will do it only when it is

profitable to him. He will exercise his Call Option (right to buy) when market rate of that

currency is higher than the strike price. Similarly, he will exercise his put Option, only

when market price has fallen below the strike price.

Suppose, Mr Yashwant buys a Call Option from Mr Joseph @ INR 46 for USD 1,000,000

on 01 Sep 2006 with the expiry date of 30 Sep 2006. Now, Mr Yashwant can demand from

Mr Joseph to sell USD 1,000,000 on any day during this period. Mr Yashwant will want to

buy these USD from Joseph only if rate of USD in the open market is higher than strike

price of INR 46, say INR 47. In case, open market rate is lower than INR 46, say INR 45,

Mr Yashwant will be better off buying the USD from open market.