Languages

Pages

Legal

Coping with the Costly

Oversupply of Gas: Liquids

Activity Surges Ahead

Presentation to the AAPG Trustees

September 2011 • Lake Tahoe, California

Robert W. Esser,

IHS CERA (retired)

CONFIDENTIAL

© 2011, All rights reserved, IHS CERA Inc., 55 Cambridge Parkway, Cambridge, Massachusetts 02142

No portion of this presentation may be reproduced, reused or otherwise distributed in any form without prior written consent.

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

1

AAPG_09211

Terms of Use

• IHS CERA content and information, including but not limited to graphs, charts, tables,

figures, and data, are not to be disseminated outside of a client organization to any third

party, including a client’s customers, financial institutions, consultants, or the public.

• Content distributed within the client organization must display IHS CERA’s legal notices and

attributions of authorship.

The accompanying materials were prepared by IHS CERA Inc. (IHS CERA) and are not to be

redistributed or reused in any manner without prior written consent, with the exception of client internal

distribution as described below.

IHS CERA strives to be supportive of client internal distribution of IHS CERA content but requires that

Some information supplied by IHS CERA may be obtained from sources that IHS CERA believes to

be reliable but are in no way warranted by IHS CERA as to accuracy or completeness. Absent a

specific agreement to the contrary, IHS CERA has no obligation to update any content or information

provided to a client.

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

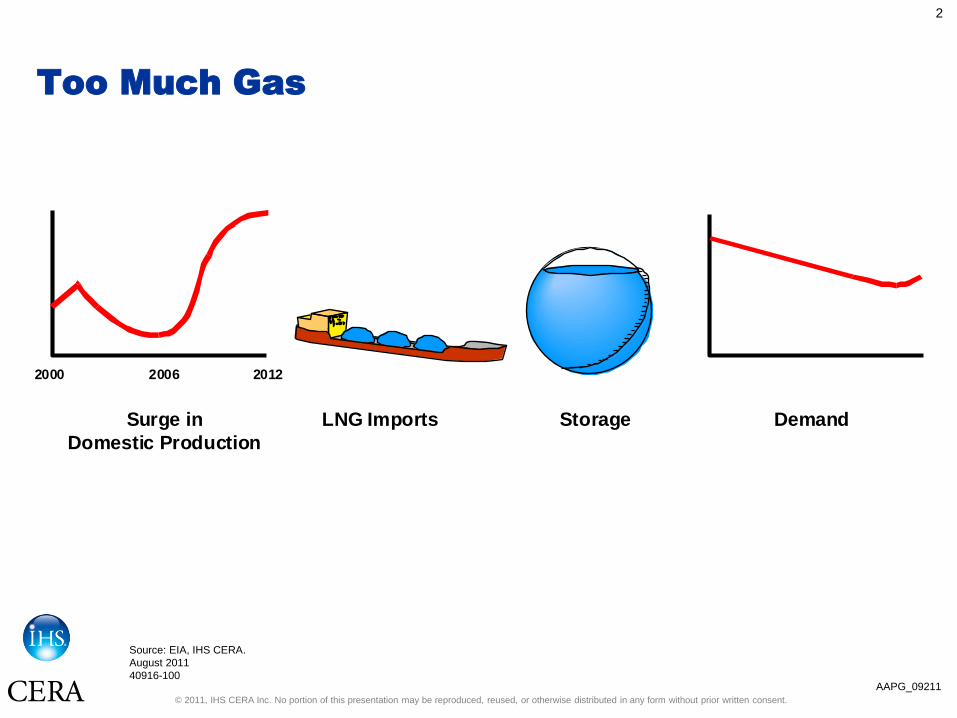

Too Much Gas

2

AAPG_09211

Surge in

Domestic Production

LNG Imports Storage Demand

2000 2006 2012

Source: EIA, IHS CERA.

August 2011

40916-100

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Recent US Lower-48 Average Annual

Dry Gas Productive Capacity Outlooks

3

AAPG_09211

Billion

Cubic Feet

per Day

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 201850

51

52

53

54

55

56

57

58

59

61

60

62

63

65

64

Sept 2006

July 2007

Oct 2008

July 2009

June 2008

March 2011

March 2010

Source: IHS CERA.

July 2011

40916-3B

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

US Gas-related Drilling

4

AAPG_09211

Gas

RigCount

Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan

250

350

450

550

650

750

850

950

1,050

1,150

0

1,250

1,350

Jan

1,450

1,650

JanJan

1,550

Jan Jan Jan

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: IHS CERA, Baker Hughes Inc.

Note: A weekly peak level of 1,606 rigs was reached in September 2008.

A secondary peak of 1,068 rigs was attained in July 2001.

Updated July 2011

40916-2

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

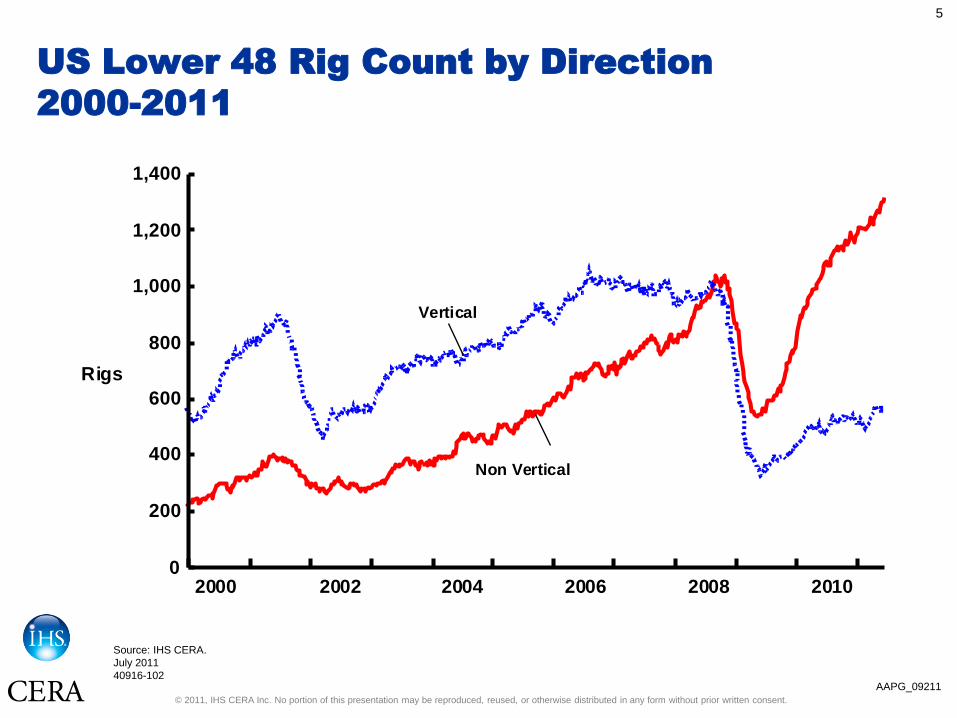

US Lower 48 Rig Count by Direction

2000-2011

5

AAPG_09211

2000 2002 2004 2006 2008 20100

200

400

600

800

1,000

1,200

1,400

Rigs

Non Vertical

Vertical

Source: IHS CERA.

July 2011

40916-102

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

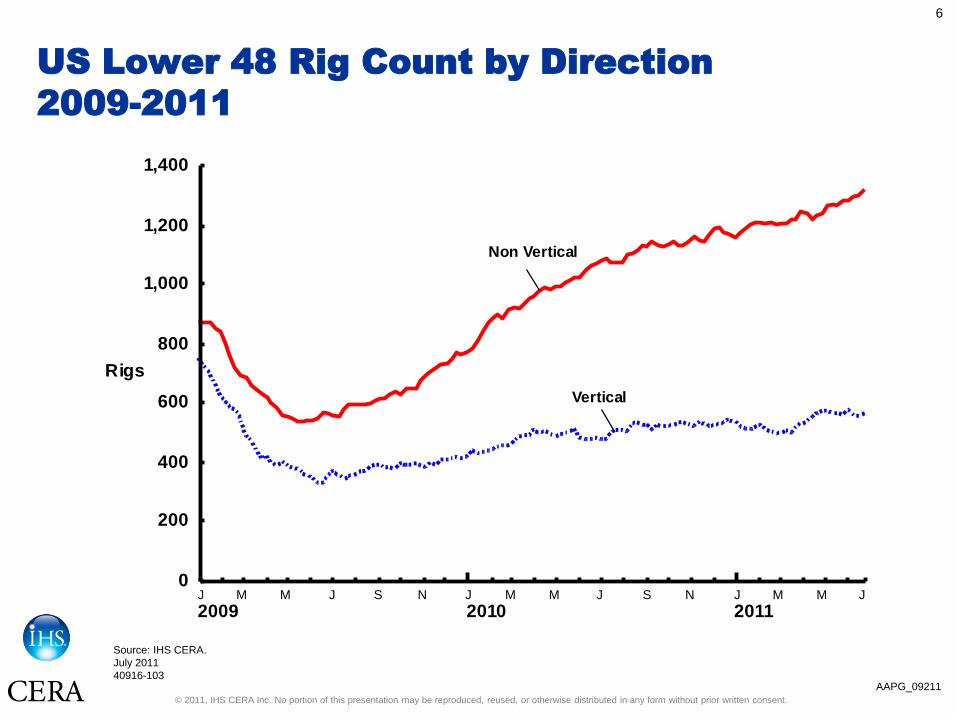

US Lower 48 Rig Count by Direction

2009-2011

6

AAPG_09211

0

200

400

600

800

1,000

1,200

1,400

Rigs

Non Vertical

Vertical

J M M J S N

2009J M M J S N

2010J M M

2011J

Source: IHS CERA.

July 2011

40916-103

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

US Lower-48 Rig Count Shifts Toward Oil

7

AAPG_09211

Gas

Oil

0

200

400

600

800

1,000

1,200

1,400

Rigs

1,600

1,800

2007 2008 2009 2010 2011 2012

Source: IHS CERA.

July 2011

40916-104

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

8

AAPG_09211

Significant Changes in Rig Counts

Source: IHS CERA.

*Rich gas.

Area Play June 2010 June 2011 Change

Oil Related

Colorado Niobrara 53 70 +17

Kansas 17 29 +12

New Mexico Bone Spring/Avalon 65 80 +15

North Dakota Bakken 115 161 +46

Oklahoma Miss Lime*, Woodford-

Cano*

125 169 +44

TX RR 1 Eagle Ford 41 106 +65

TX RR 2 Eagle Ford 28 66 +38

TX RR 7C Wolfberry 52 70 +18

TX 8 Bone Sprint/Avalon* 150 255 +105

TX 8A Wolfberry 25 37 +12

Gas Related

Arkansas Fayetteville Dry Gas 39 35 -4

North Louisiana Haynesville Dry Gas 139 100 -39

Pennsylvania Marcellus 82 111 +29

TX RR 5 Barnett 86 55 -31

TX RR 6 Haynesville Dry Gas 75 50 -25

TX 10 Granite Wash 62 78 +16

TX 3 Dry Gas 53 42 -11

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

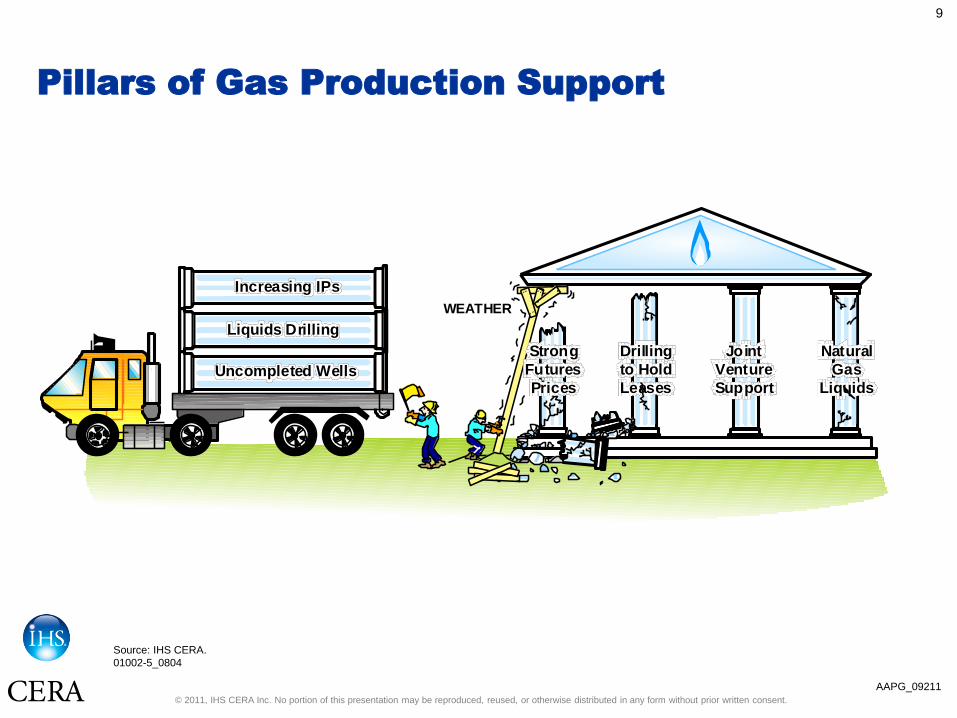

Pillars of Gas Production Support

9

AAPG_09211

Drilling

to Hold

Leases

Joint

Venture

Support

Natural

Gas

Liquids

WEATHER

Strong

Futures

PricesUncompleted Wells

Increasing IPs

Liquids Drilling

Source: IHS CERA.

01002-5_0804

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

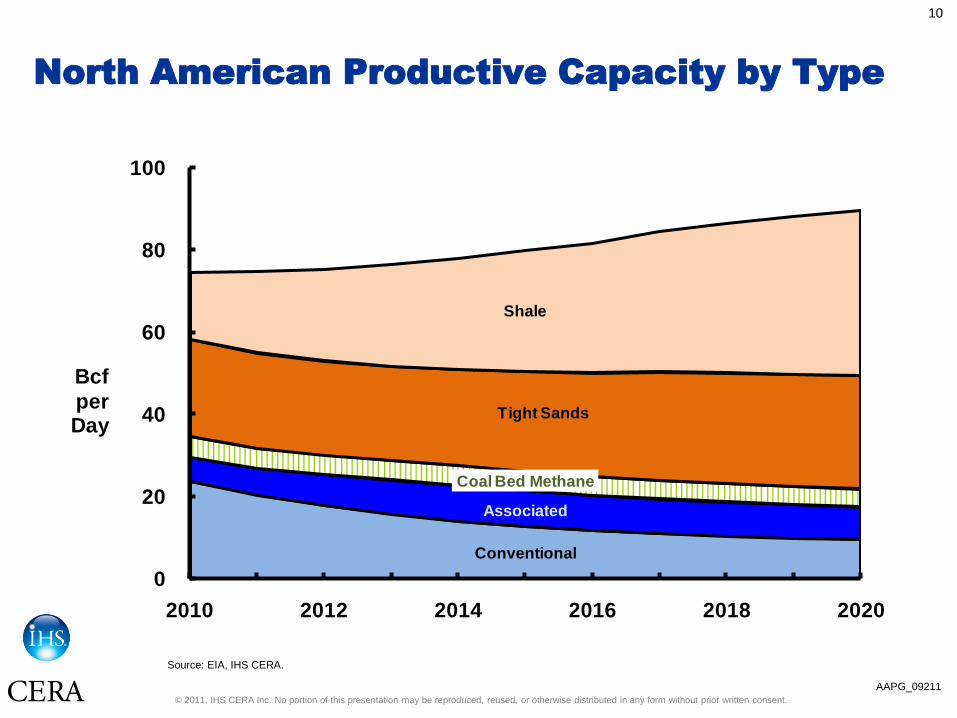

North American Productive Capacity by Type

10

Source: EIA, IHS CERA.

Conventional

Associated

Coal Bed Methane

Tight Sands

Shale

0

20

40

60

80

100

2010 2012 2014 2016 2018 2020

Bcf

perDay

AAPG_09211

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

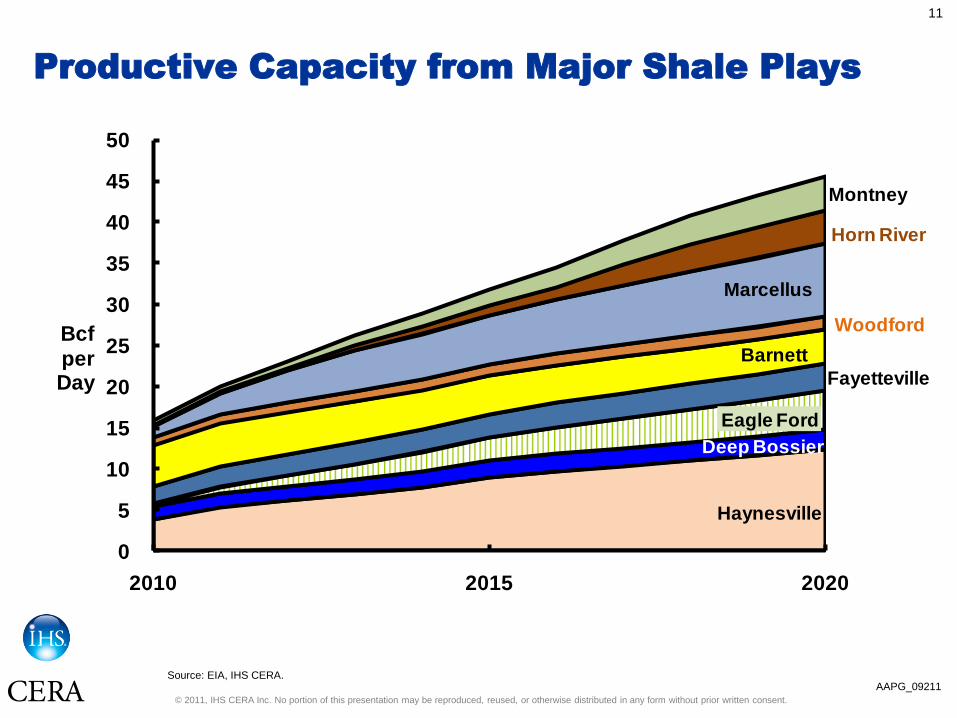

Productive Capacity from Major Shale Plays

11

Source: EIA, IHS CERA.

Haynesville

Deep Bossier

Eagle Ford

Fayetteville

Barnett

Woodford

Marcellus

Horn River

Montney

0

5

10

15

20

25

30

35

40

45

50

2010 2015 2020

Bcf

perDay

Productive Capacity, Major Shale Plays

Source: Energy Information Administration, IHS Cambridge Energy Research Associates.

AAPG_09211

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

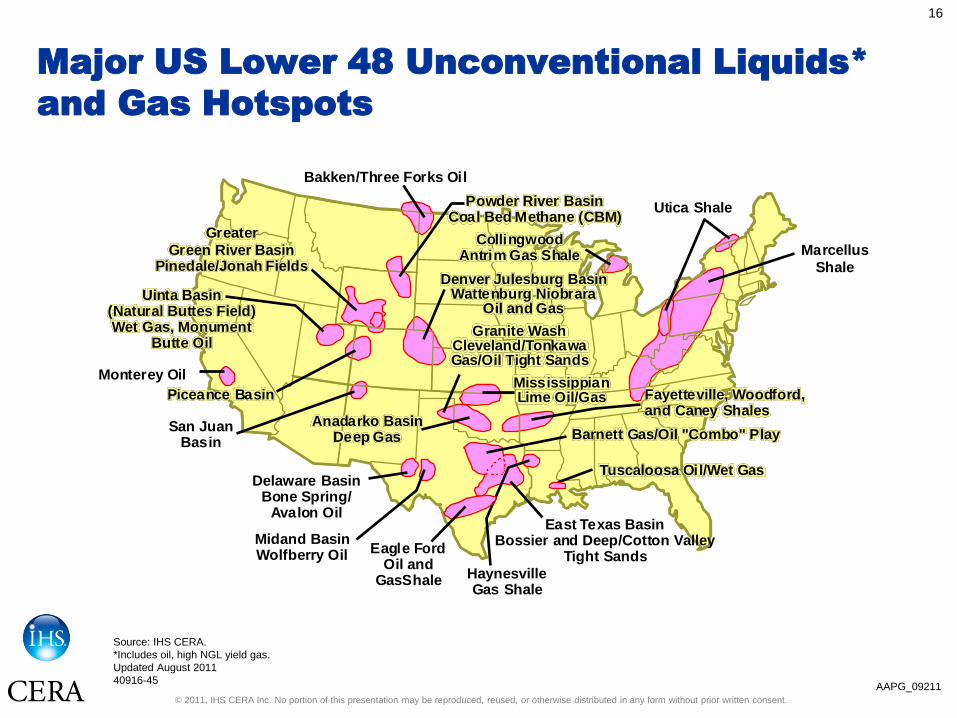

Major US Lower 48 Unconventional Liquids*

and Gas Hotspots

12

AAPG_09211

Source: IHS CERA.

*Includes oil, high NGL yield gas.

Updated August 2011

40916-45

Greater

Green River BasinPinedale/Jonah Fields

East Texas BasinBossier and Deep/Cotton Valley

Tight Sands

Anadarko BasinDeep Gas

Tuscaloosa Oil/Wet Gas

Barnett Gas/Oil "Combo" Play

Piceance Basin

Uinta Basin(Natural Buttes Field)Wet Gas, Monument

Butte Oil

San JuanBasin

Fayetteville, Woodford,and Caney Shales

Delaware BasinBone Spring/

Avalon Oil

CollingwoodAntrim Gas Shale

Denver Julesburg BasinWattenburg Niobrara

Oil and Gas

Utica Shale

Marcellus

Shale

HaynesvilleGas Shale

Eagle FordOil and

GasShale

Midand BasinWolfberry Oil

Bakken/Three Forks Oil

Powder River BasinCoal Bed Methane (CBM)

MississippianLime Oil/Gas

Granite WashCleveland/TonkawaGas/Oil Tight Sands

Monterey Oil

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

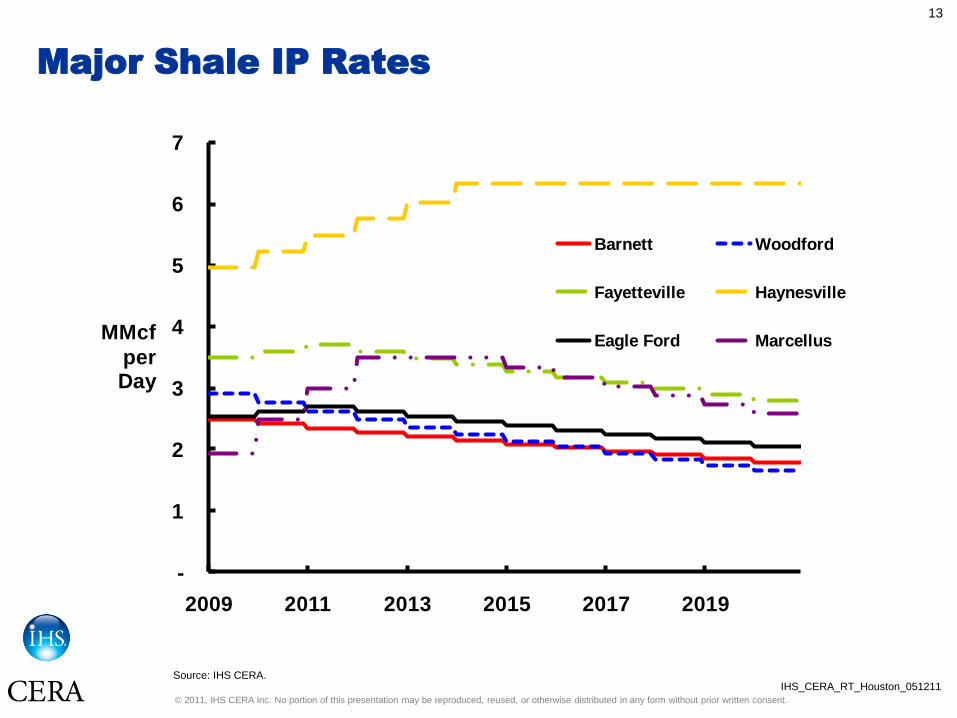

Major Shale IP Rates

13

Source: IHS CERA.

-

1

2

3

4

5

6

7

2009 2011 2013 2015 2017 2019

MMcf

perDay

Barnett Woodford

Fayetteville Haynesville

Eagle Ford Marcellus

IHS_CERA_RT_Houston_051211

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

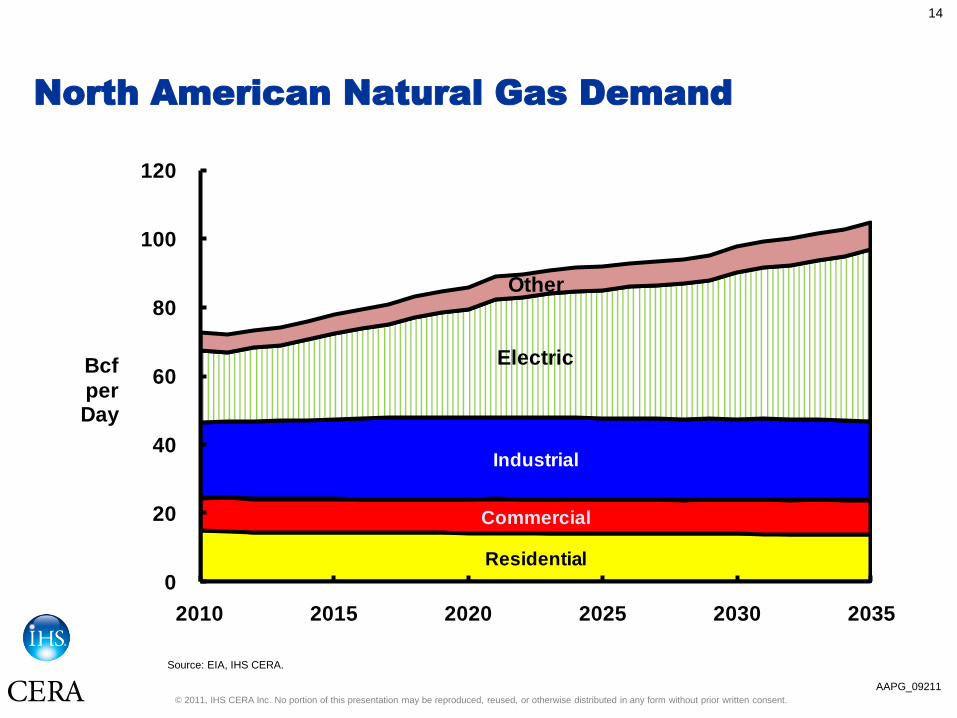

North American Natural Gas Demand

14

Source: EIA, IHS CERA.

Residential

Commercial

Industrial

Electric

Other

0

20

40

60

80

100

120

2010 2015 2020 2025 2030 2035

Bcf

perDay

North American Natural Gas Demand

Source: Energy Information Administration, IHS Cambridge Energy Research Associates. AAPG_09211

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Factors in US Gas Price Expectations

15

AAPG_09211

Source: IHS CERA.

July 2011

40916-101

GASPRICE

Uncertainty

about FutureTaxation

Unconventional gasproduction profile

US Production Increases

Rig counts

Seasonal productionshut ins

Coal price

Demand

Weather

Speed and extent ofeconomic recovery

Reduced ForwardStrip Expectations

Commodity Investment

BandwagonInflation Expectations

Value of dollar

Oil Price

Demand (global)

Equity market

LNG Imports

Storage InjectionsTiming of Total Fill

Nuclear fears

Demand (global)

OPEC and North African availability concerns

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Major US Lower 48 Unconventional Liquids*

and Gas Hotspots

16

AAPG_09211

Source: IHS CERA.

*Includes oil, high NGL yield gas.

Updated August 2011

40916-45

Greater

Green River BasinPinedale/Jonah Fields

East Texas BasinBossier and Deep/Cotton Valley

Tight Sands

Anadarko BasinDeep Gas

Tuscaloosa Oil/Wet Gas

Barnett Gas/Oil "Combo" Play

Piceance Basin

Uinta Basin(Natural Buttes Field)Wet Gas, Monument

Butte Oil

San JuanBasin

Fayetteville, Woodford,and Caney Shales

Delaware BasinBone Spring/

Avalon Oil

CollingwoodAntrim Gas Shale

Denver Julesburg BasinWattenburg Niobrara

Oil and Gas

Utica Shale

Marcellus

Shale

HaynesvilleGas Shale

Eagle FordOil and

GasShale

Midand BasinWolfberry Oil

Bakken/Three Forks Oil

Powder River BasinCoal Bed Methane (CBM)

MississippianLime Oil/Gas

Granite WashCleveland/TonkawaGas/Oil Tight Sands

Monterey Oil

© 2011, IHS CERA Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

US Lower-48 Rig Count Shifts Toward Oil

17

AAPG_09211

Gas

Oil

0

200

400

600

800

1,000

1,200

1,400

Rigs

1,600

1,800

2007 2008 2009 2010 2011 2012

Source: IHS CERA.

July 2011

40916-104

For more information about this presentation or

IHS CERA in general, please contact

Robert W. Esser +1 631 427 7086

55 Cambridge Parkway Cambridge, Massachusetts 02142, USA

IHSCERA.com

Beijing San Francisco

Washington, DC

Cambridge, MA

Calgary

Mexico City

Rio de Janeiro

Paris

Moscow

Dubai

Singapore

Houston

Denver

London

Top Related