Languages

Pages

Legal

ComplianceKeeping Customers and

Regulators Happy

Delia Rickard

Deputy Executive Director

Consumer Protection

2

ASIC

• Consumer protection regulator for the financial services sector

• Undertake surveillances of our regulated population to ensure compliance

• Also focus on unlicensed activity• Take enforcement action• Seek to educate consumers so that they

can make informed choices.

3

Our compliance role

• Helping industry understand their legal obligations & our expectations.

• Providing incentives for industry to tell us about problems early

• Monitoring compliance with the law by conducting surveillance

• Intervening in serious non-compliance.

4

The many angles of compliance

• Lots of angles to compliance

• You can focus on what customers want

• You can focus on what the law requires

• Each reinforces the other but you do need to look at it from both angles.

5

Some universal principles• Our focus today is on compliance &

financial services but the principles apply to all goods & services.

• Consumers and the law both want consumers to be safe & in a position to make confident & informed choices amongst goods & services of a reasonable standard.

• Start by asking is this the right thing to do rather than just is this legal.

6

The Regulator’s perspective

• Unrealistic to expect no breaches• They will occur from time to time• Regulators want you to have compliance

measures though that:– Prevent;– Detect;– Remedy; & if necessary– Report

• The quality of these measures will impact on how we respond to breaches.

7

Cradle to grave (life cycle) approach to compliance

UK FSA’s work on treating customers fairly translates well to a compliance philosophy re points of engagement

• Product design• Product manufacture and maintenance• Marketing practices• Sales process (including advice &

information)• Complaints handling & redress

mechanisms.

8

Where the problems are

• Breaches occur at all of life cycle stages.

• Good product design and marketing models though are likely to minimise risk

• Need Compliance’s involvement from the start.

9

Internal Tensions• We see the tensions b/n compliance & the

marketing &/or business arms all the time.• You need strategies to overcome these.• Use Data to show the business case of treating

customers well.• High level support & sign off• Use the regulator to help you here too• Don’t presume that because a competitor does

something it is OK.• Do let regulators know if competitors are doing

the wrong thing.

10

Identifying breachesSources of info include• Internal & external audits• Your complaints data, EDR complaints• Patterns of problems like defaults• Look at what EDR schemes & regulators are getting

excited about & check yourself• Your own testing & monitoring – do your own shadow

shop, market research• Talk to your customers Talk with groups like ACA –

find out what people are calling them about.• Encourage staff to self-report• Look for the patterns!

11

Reporting Systemic Issues

Reporting systemic issues

• Licensees: breach notifications to ASIC (s 912D of the Corps Act)

• Approved EDR schemes (e.g. BFSO, FICS) report systemic issues and serious misconduct to ASIC

12

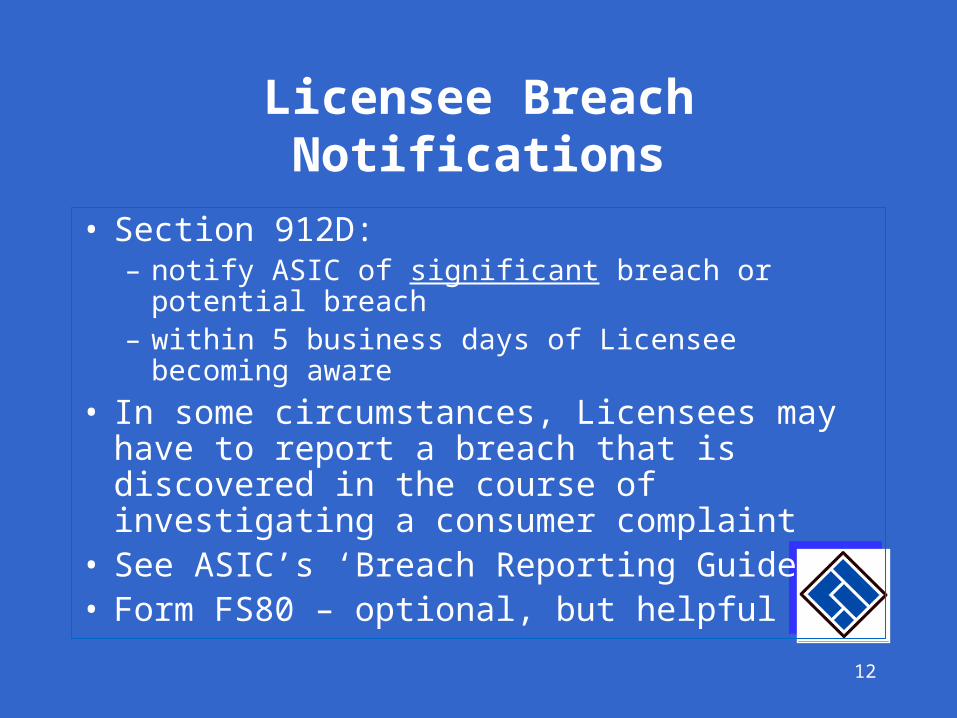

Licensee Breach Notifications

• Section 912D:– notify ASIC of significant breach or potential

breach– within 5 business days of Licensee becoming

aware

• In some circumstances, Licensees may have to report a breach that is discovered in the course of investigating a consumer complaint

• See ASIC’s ‘Breach Reporting Guide’• Form FS80 – optional, but helpful

13

Licensee Breach Notifications

What is significant?• number or frequency of similar previous

breaches • impact on the licensee’s ability to provide the

financial services• extent to which it indicates licensee’s

compliance arrangements are inadequate• the actual or potential financial loss to

clients or the licensee

14

Licensee Breach Notifications

What does ASIC do with this information ??• Receive and record (many cases)• Receive and seek more information (most

cases – use of FS80 may help avoid this)• Require remedial action• Require remedial action with report• Conduct inquiries (eg, surveillance)• Enforcement action in only 4% of

reported breaches

15

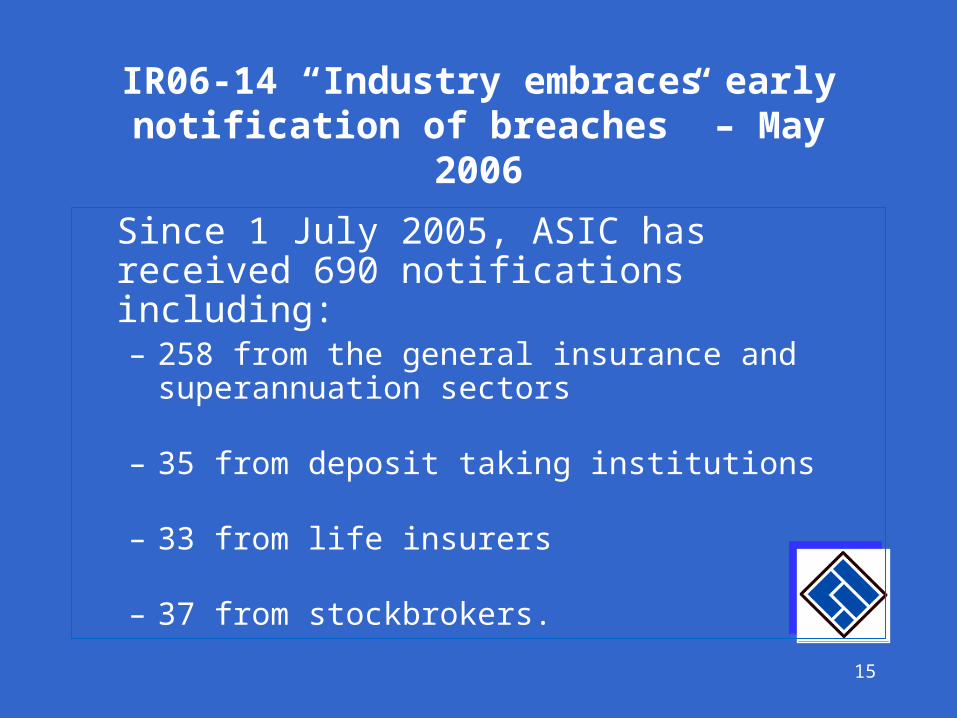

IR06-14 “Industry embraces early notification of breaches” – May 2006

Since 1 July 2005, ASIC has received 690 notifications including: – 258 from the general insurance and

superannuation sectors

– 35 from deposit taking institutions

– 33 from life insurers

– 37 from stockbrokers.

16

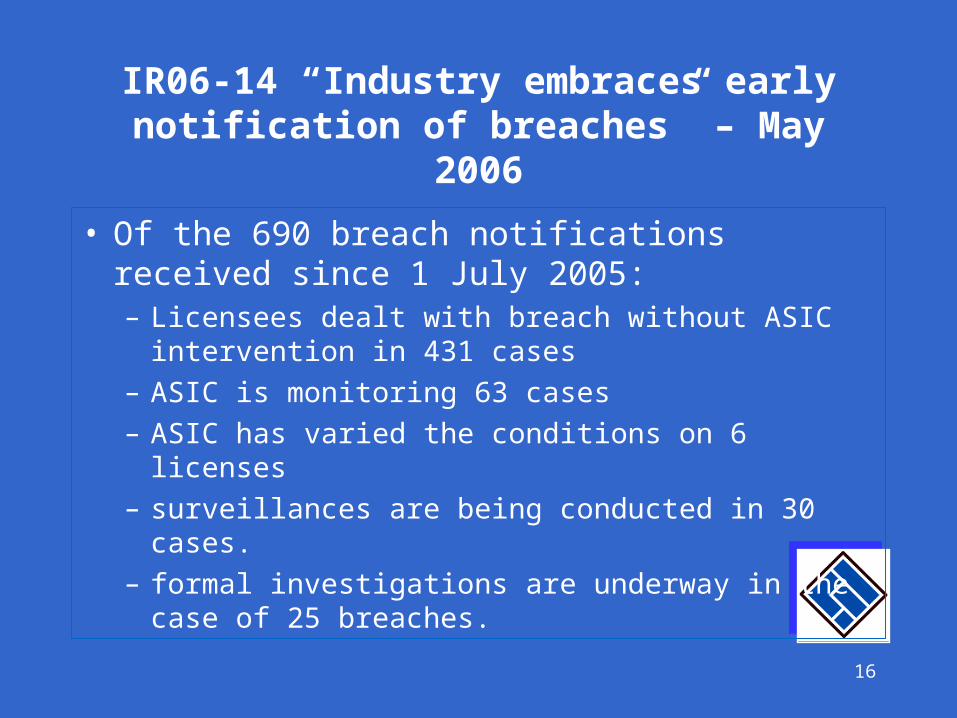

IR06-14 “Industry embraces early notification of breaches” – May 2006

• Of the 690 breach notifications received since 1 July 2005: – Licensees dealt with breach without ASIC

intervention in 431 cases – ASIC is monitoring 63 cases – ASIC has varied the conditions on 6 licenses– surveillances are being conducted in 30 cases. – formal investigations are underway in the case of

25 breaches.

17

Licensee Breach Notifications

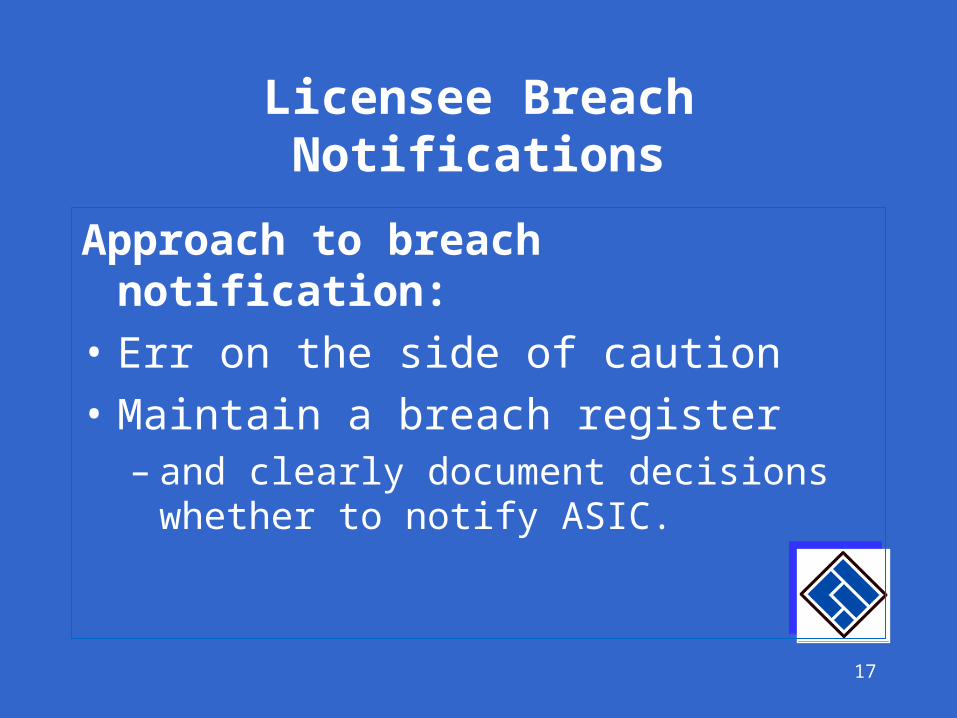

Approach to breach notification:

• Err on the side of caution

• Maintain a breach register– and clearly document decisions whether to

notify ASIC.

18

Catching the eye of the regulator

• More likely to focus on those firms or sectors with few or no breach notifications.

• Risk based approach – ie focus on impact & probability– What is the impact of the risk crystallising– What is the probability of the risk

crystallising

19

Breach notification guide updated – May 2006

New sections explain:– how ASIC handles breach notifications– what ASIC takes into account in deciding

whether to take further action– what Licensees can do to reduce the need

for ASIC to take action

20

EDR Scheme Reporting

Policy Statement 139• Approved EDR schemes must report to ASIC:

– systemic issues– serious misconduct

• Reports are lodged quarterly• Most issues are reported to us without

identifying scheme members

21

EDR Scheme Reporting

• Quarterly scheme report - used by ASIC to identify trends/emerging issues

• No enforcement action has yet been taken based on information contained in reports

• Issues referred to in reports generally addressed by schemes

22

Annual Reports• Scheme annual reports also deal with

systemic issues• Often issues not legal breaches but areas of

major customer dissatisfaction• An invaluable indicator of what should be

addressed by both firms and in self-regulatory codes.

• The ongoing appearance of an issue is likely to direct government’s mind to law reform.

23

Concurrent investigations

• Sometimes, there may be concurrent ASIC/EDR scheme investigations into systemic issues:– Licensees may receive duplicate

notices/requests to product documents– However the investigations generally have

different intended outcome– In cases of genuine duplication we talk with

the EDR scheme to work out the best approach.

24

Improving customer service –integrate the consumer into compliance

At the end of the day remember the golden rules of:

– Know your client– Help them to understand what they need to

know about your product or service– Understand their needs & wants– Design & deliver products that meet them– Continually monitor for problems & patterns– Fix things when they do go wrong– Tell the regulator if the problem is significant

Top Related