Languages

Pages

Legal

Complementary currencyFrom Wikipedia, the free encyclopedia

Jump to: navigation, search

Complementary community currency (CCC) is a hypernym (superordinate) of local currency (also referred to as community currency) and sectoral currency.

Complementary communiity currencies describe a wide group of currencies or scrips designed to be used in combination with standard currencies or other complementary currencies. They can be valued and exchanged in relationship to national currencies but also function as media of exchange on their own. Complementary currencies lie outside the nationally defined legal realm of Legal tender and are not used as such. Rate of exchange, scope of circulation and use in combination with other currencies differs greatly between complementary currency systems, as is the case with national currency systems.

Some complementary community currencies incorporate value scales based on time or the backing of real resources (gold, oil, services, etc). A Time-based currency is valued by the time required to perform a service in hours, notwithstanding the potential market value of the service.

Some complementary community currencies take advantage of demurrage fees, an intentional devaluation of the currency over time, like negative interest. This stimulates market exchanges in the devaluating currency, propagates new participation in the currency system and forces the storage of wealth (hoarding) ability usually reserved for currency into more permanent and better value holding tools like (property, improvement, education, technology, health, etc) all of which are sheltered from the currency based demurrage fees.

Other experimental complementary community currencies use high interest fees to promote heavy competition between participants, and the removal of wealth from long term wealth holding structures (natural/material wealth, property, etc) to aid in the process of rapid industriaization, mass production, automation and competitive innovation.

Monetary speculation and gambling are usually outside the design parameters of complementary currencies. Complementary currencies are often intentionally restricted in their regional spread, time of validity or sector of use and may require a membership of participating individuals or points of acceptance.

COMPLEMENTARY COMMUNITY CURRENCIES (CCC's) It is important to understand that there is evidence that, beginning in the 1960's, the first advocates of complementary community currencies (CCC's), especially in Canada, did not think of

1

CCC as working contra to our national currencies. This is why certain leaders of this movement were careful to use the term 'complementary'. They used it to emphasize the importance of working in cooperation with governments and the tax system, businesses, unions, associations, charities, the banks and all forms of democratic capitalism--as partners in the above-ground economy.

EXAMPLE OF A FULLY FUNDED CCC. For example, The Toronto Dollar system, is a system which is fully funded by Canadian dollars. In other words, the system is backed by Canadian dollars. Participating merchants are free to exchange the toronto dollars for Canadian dollars. While the system will work better when more and more of the CCC is kept in circulation, no one needs to feel trapped by the system.

In addition to being supported by any number of social activists, including philosophers, clergy, artists, etc., it is fully supported by a growing number of political leaders, past and present, including, over the years, several mayors of Toronto. For details, check out: http://www.torontodollar.com

ALTERNATIVE CURRENCY

Alternative currency is a term that refers to any currency used as an alternative to the dominant national or multinational currency systems (usually referred to as national or fiat money). Alternative currencies can be created by an individual, corporation, or organization, they can be created by national, state, or local governments, or they can arise naturally as people begin to use a certain commodity as a currency. Mutual credit is a form of alternative currency, and thus any form of lending that does not go through the banking system can be considered a form of alternative currency.

When used in combination with or when designed to work in combination with national or multinational fiat currencies they can be referred to as complementary currency. If the use of an alternative currency is limited to a certain region, it is called a local currency.

Often there are issues related to paying tax. Some alternative currencies are considered tax-exempt, but most of them are fully taxed as if they were national currency, with the caveat that the tax must be paid in the national currency. The legality and tax-status of alternative currencies varies widely from country to country; some systems in use in some countries would be illegal in others.

Examples of alternative currencies WIR Bank - One of the oldest and most successful complementary currencies,

founded in 1934, oriented towards small and mid-sized corporations, with 62,000 members.

Category:Electronic currencies , such as digital gold currency.

Digital gold currency (or DGC) is a form of electronic money denominated in gold weight. The typical unit of account for such currency is the gold gram or the troy ounce,

2

although other units such as the gold dinar are sometimes used. DGCs are backed by gold through unallocated or allocated gold storage.

Digital gold currencies are issued by a number of companies, each of which provides a system that enabled users to pay each other in units that held the same value as gold bullion. These competing providers issue independent currency, which normally carries the same name as their company. In terms of the most popular providers, e-gold has the greatest number of users and GoldMoney holds the greatest quantity of bullion (as of January 2007).

As of January 2007, DGC providers held in excess of 9.5 tonnes of gold as disclosed reserves, which is worth approximately $184 million.

Features

[edit] Asset protection

e-gold is, according to their website, "100% backed by gold"

Unlike fractional-reserve banking, DGCs (such as e-gold and GoldMoney) hold 100% of clients' funds in reserves with a store of value. Proponents of DGC systems contend that deposits are protected against inflation, devaluation and other possible economic risks inherent in fiat currencies. These risks include the monetary policy of countries or territories, which are perceived by proponents to be harmful to the value of paper currency. It is also theoretically much harder for governments and/or creditors to seize or confiscate digital gold currency from someone, as most DGC companies are incorporated in offshore financial centres.

[edit] Bullion investing

Main articles: Gold as an investment and Silver as an investment

3

Digital currencies backed by gold are the most popular, although e-gold, e-Bullion and e-dinar also provide digital currency backed by silver, while GoldMoney and Crowne Gold also provide storage in silver. Other digital silver currencies include the eLibertyDollar and Phoenix Silver. In addition to gold and silver, e-gold supplies digital currency backed by platinum and palladium. Gold, silver, platinum and palladium each have recognised international currency codes under ISO 4217.

[edit] Exchanging fiat currency

Some providers, like e-gold, do not sell DGC directly to clients. In the case of an e-gold account, currency must be bought and sold via a digital currency exchanger (DCE). According to their website the reason they do this is so there can be no debt or contingent liabilities associated with the business, making e-gold Ltd. absolutely free of any financial risk. DGCs are known as private currency as they are not issued by governments.

] Non-reversible transactions

Unlike the credit card industry, DGC issuers generally do not bundle services such as repudiation. Thus having transactions reversed, even in case of a legitimate error, unauthorized spend, or failure of a vendor to supply goods is not possible. In this respect, a DGC spend is more akin to a cash transaction while PayPal transfers, for example, could be considered more similar to credit card transactions.

Universal currency

Proponents claim that DGC offers a truly global and borderless world currency system which is independent of exchange rate variations. Gold, silver, platinum and palladium each have recognised international currency codes under ISO 4217.

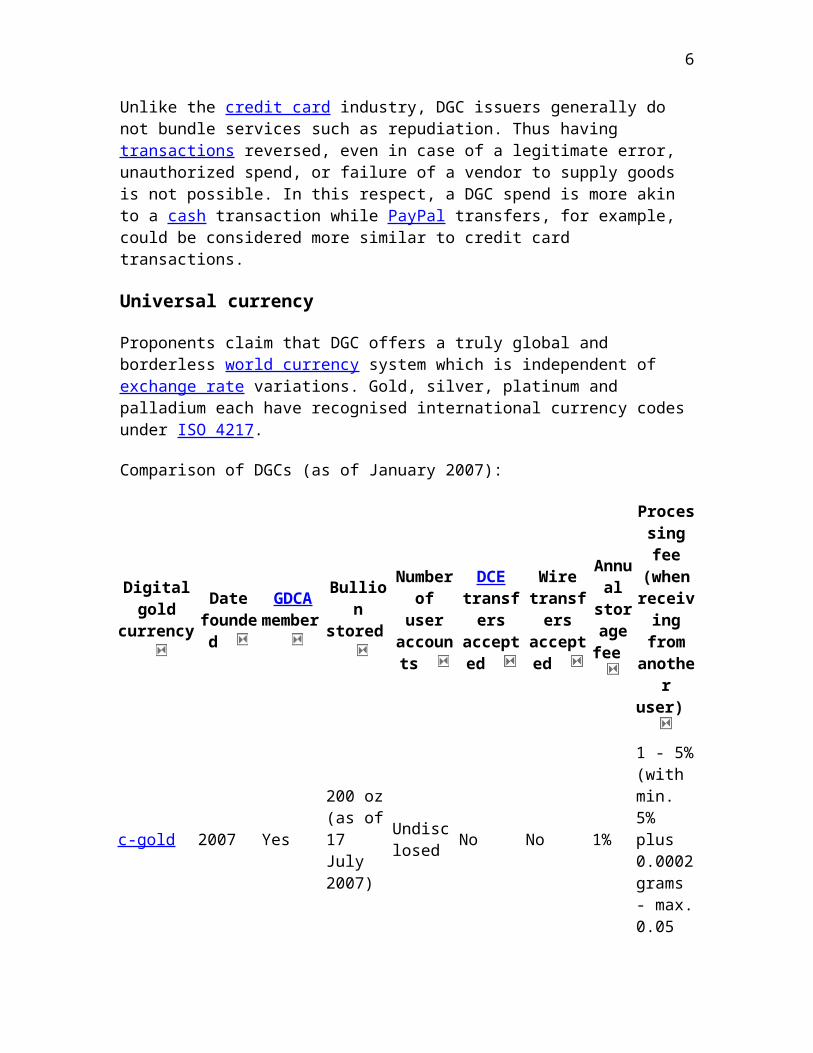

Comparison of DGCs (as of January 2007):

Digital gold

currency

Datefounded

GDCAmember

Bullionstored

Numberof user

accounts

DCE transfers accepted

Wire transfers accepted

Annual

storage

fee

Processing fee(when

receiving from another user)

c-gold 2007 Yes 200 oz (as of 17 July 2007)

Undisclosed

No No 1% 1 - 5% (with min. 5% plus 0.0002 grams - max.

4

0.05 grams)

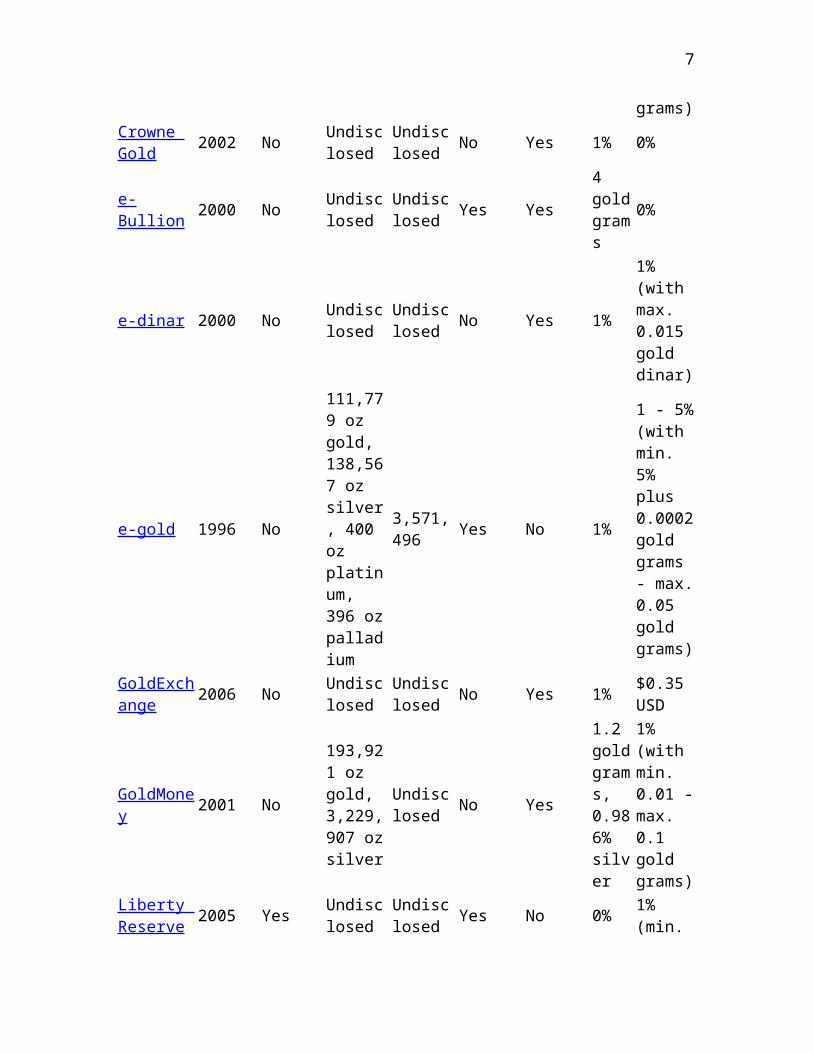

Crowne Gold

2002 NoUndisclosed

Undisclosed

No Yes 1% 0%

e-Bullion 2000 NoUndisclosed

Undisclosed

Yes Yes4 gold grams

0%

e-dinar 2000 NoUndisclosed

Undisclosed

No Yes 1%

1% (with max. 0.015 gold dinar)

e-gold 1996 No

111,779 oz gold, 138,567 oz silver, 400 oz platinum, 396 oz palladium

3,571,496 Yes No 1%

1 - 5% (with min. 5% plus 0.0002 gold grams - max. 0.05 gold grams)

GoldExchange

2006 NoUndisclosed

Undisclosed

No Yes 1%$0.35 USD

GoldMoney 2001 No

193,921 oz gold, 3,229,907 oz silver

Undisclosed

No Yes

1.2 gold grams, 0.986% silver

1% (with min. 0.01 - max. 0.1 gold grams)

Liberty Reserve

2005 YesUndisclosed

Undisclosed

Yes No 0%

1% (min. $0.01 - max. $0.25 USD)

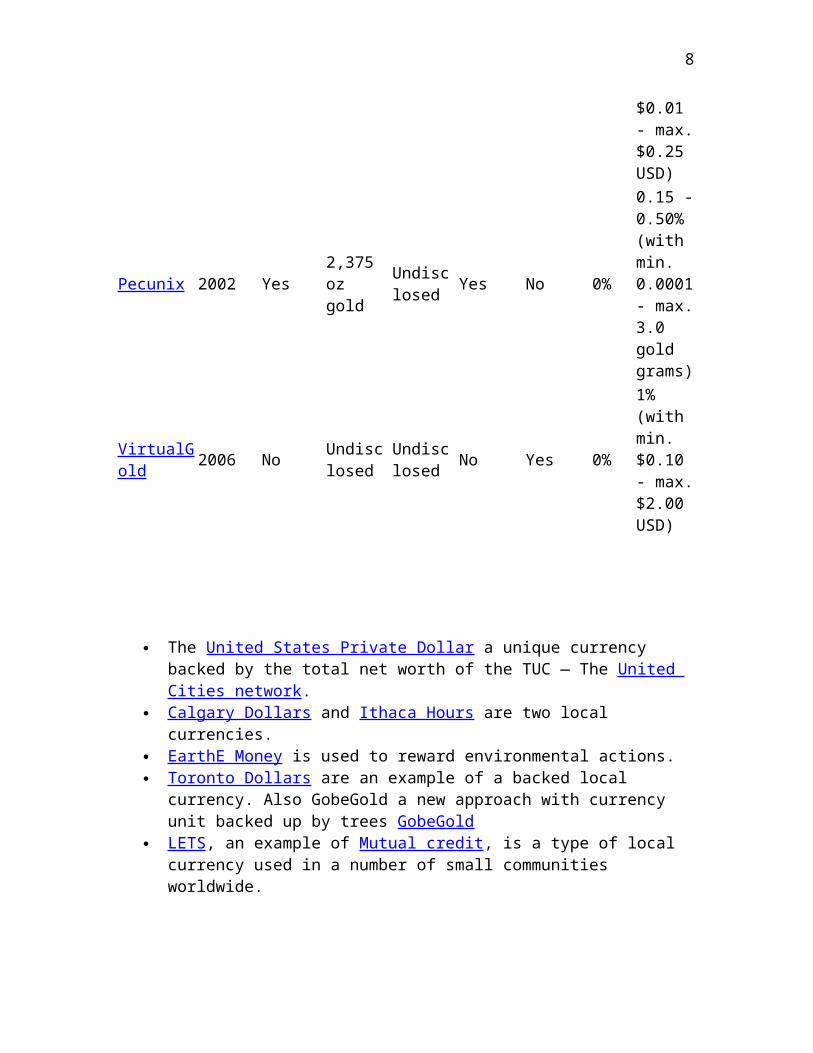

Pecunix 2002 Yes2,375 oz gold

Undisclosed

Yes No 0%

0.15 - 0.50% (with min. 0.0001 - max. 3.0 gold grams)

VirtualGold 2006 No Undisclosed

Undisclosed

No Yes 0% 1% (with min.

5

$0.10 - max. $2.00 USD)

The United States Private Dollar a unique currency backed by the total net worth of the TUC — The United Cities network.

Calgary Dollars and Ithaca Hours are two local currencies. EarthE Money is used to reward environmental actions. Toronto Dollars are an example of a backed local currency. Also GobeGold a new

approach with currency unit backed up by trees GobeGold LETS , an example of Mutual credit, is a type of local currency used in a number

of small communities worldwide.

Local Exchange Trading Systems (LETS) also known as LETSystems are local, non-profit exchange networks in which goods and services can be traded without the need for printed currency.

LETS networks use interest-free local credit so direct swaps do not need to be made. For instance, a member may earn credit by doing childcare for one person and spend it later on carpentry with another person in the same network. In LETS, unlike other local currencies, no scrip is issued, but rather transactions are recorded in a central location open to all members. As credit is issued by the network members, for the benefit of the members themselves, LETS are considered mutual credit systems.

Michael Linton originated the term "Local Exchange Trading System" in 1982 and, with his wife Shirley, for a time ran the Comox Valley LETSystems in Courtenay, British Columbia. The system he designed was intended as an adjunct to the national currency, rather than a replacement for it, although there are examples of individuals who have managed to replace their use of national currency through inventive usage of LETS.[citation

neede

Criteria

LETS are generally considered to have the following five fundamental criteria:[1]

Cost of service - from the community for the community Consent - there is no compulsion to trade Disclosure - information about balances is available to all members Equivalence to the national currency

6

No interest

Of these criteria, "equivalence" is the most controversial. According to a 1996 survey by LetsLink UK, only 13% of LETS networks actually practice equivalence, with most groups establishing alternate systems of valuation "in order to divorce [themselves] entirely from the mainstream economy."[2][3] Michael Linton has stated that such systems are "personal money" networks rather than LETS.[4]

Benefits of LETS

LETS can help revitalise and build community by allowing a wider cross-section of the community—individuals, small businesses, local services and voluntary groups—to save money and resources in cooperation with others and extend their purchasing power. Other benefits may include social contact, health care, tuition and training, support for local enterprise and new businesses. One goal of this approach is to stimulate the economies of economically depressed towns that have goods and services, but little official currency: the LETS scheme does not require outside sources of income as stimulus.

Europe

In the United Kingdom, an estimated 40,000 people are now trading in around 450 LETS networks in cities, towns and rural communities across the UK.[6] LETS currencies have their own local names

In the Great Depression, people and corporations used gift certificates as a form of currency.

The Time Dollar is a state-sponsored alternative currency in the U.S, designed to encourage the independence and productivity of welfare recipients.

Liberty Dollar is a private currency backed by silver, and is designed to be the nationwide alternative currency in the United States. In 2007 federal agents raided its offices with a warrant[1] charging money laundering, mail fraud, wire fraud, counterfeiting, and conspiracy.[2].

Millennium Dollars are a private currency backed by US Treasury bills and cash investments, designed to have a constant "real" value and hence act as a hedge against inflation or deflation.

Barter clubs or corporate barter organizations are an example of alternative currency systems.

BerkShares Fourth Corner Exchange Ripple monetary system

7

BERNARD LIETAER CALGARY DOLLARS CHIEMGAUER DIGITAL GOLD CURRENCY PRIVATE CURRENCY SILVIO GESELL TERRA WIR BANK

Private currency Sectoral currency Bearer instrument Local Exchange Trading Systems (LETS) Time-based currency Flex dollar Local currency Credit Money Money Private bank Commodity money Digital cash Electronic money

Store of valueTo act as a store of value, a commodity, a form of money, or financial capital must be able to be reliably saved, stored, and retrieved - and be predictably useful when it is so retrieved.

This is distinct from the standard of deferred payment function which requires acceptability to parties one owes a debt to, or the unit of account function which requires fungibility so accounts in any amount can be readily settled. It is also distinct from the medium of exchange function which requires durability when used in trade, and a minimum of opportunity to cheat others.

When currency is stable, money can serve all four functions. When it isn't, such as during times of hyperinflation or when complex and volatile forms of financial capital are involved, it becomes important to identify alternative stores of value, of which common ones are:

real estate - actual deeds in protectible land gold - once the basis of the gold standard

8

silver - once the basis of the silver standard precious stones , and precious metals collectibles, e.g. original art by a famous artist or antiques livestock (see African currency)

While these items may be inconvenient to trade daily or store, and may vary in value quite significantly, they rarely or never lose all value. This is the point of any store of value, to impose a natural risk management simply due to inherent stable demand for the underlying asset. It need not be a capital asset at all, merely have economic value that is not known to disappear even in the worst situation. In principle, this could be true of any industrial commodity, but gold and precious metals are generally favored because of their demand and rarity in nature, which reduces the risk of devaluation associated with increased production and supply.

Gresham's law is commonly stated: "Bad money drives out good." Or, more precisely: "When there is a legal-tender currency, bad money drives good money out of circulation." Or, more accurately: "Money overvalued by the State will drive money undervalued by the State out of circulation."

Gresham's law applies specifically when there are two forms of commodity money in circulation which are forced, by the application of legal-tender laws, to be respected as having the same face value in the marketplace.

Gresham's law is named after Sir Thomas Gresham (1519 – 1579), an English financier in Tudor times.

heory

Gresham's law says that any circulating currency consisting of both "good" and "bad" money (both forms required to be accepted at equal value under legal tender law) quickly becomes dominated by the "bad" money. This is because people spending money will hand over the "bad" coins rather than the "good" ones, keeping the "good" ones for themselves.

Consider a customer purchasing an item which costs five pence, who has in their possession several silver sixpence coins. Some of these coins are more debased, while others are less so — but legally, they are all mandated to be of equal value. The customer would prefer to retain the better coins, and so offers the shopkeeper the most debased one. In turn, the shopkeeper must give one penny in change — and has every reason to give the most debased penny. Thus, the coins that circulate in the transaction will tend to be of the most debased sort available to the parties.

If "good" coins have a face value below that of their metallic content, individuals may be motivated to melt them down and sell the metal for its higher bullion value, even if such defacement is illegal. For an example of this, consider the 1965 US Half-dollars which were made from only 40% silver. The previous year the half-dollar was 90% silver. With

9

the release of the 1965 half, which was legally required to be accepted at the same value as the previous year's 90% halves, the older 90% silver coinage of the US quickly disappeared from circulation, and the debased money was allowed to circulate in its stead. As the price of bullion silver rose above the face value of the coins, many of those old half-dollars were melted down. With the 1971 issue the government gave up on including any silver in the half dollars. A similar situation is currently (2007) occurring with the rising price of zinc and copper, and has led the U.S. government to ban the melting or mass exportation of one and five cent coins, respectively.

In addition to being melted down for its bullion value, money that is considered to be "good" tends to leave an economy through international trade. International traders are not bound by legal tender laws the way citizens of the country are, so they will offer higher value for good coins than bad ones, and thus higher value than can be obtained within the country. The good coins may leave their country of origin to become part of international trade. Thus, the good money is driven out of the country of issue, escaping that country's legal tender laws and leaving the "bad" money behind. This occurred in Britain during the period of the Gold Exchange Standard.

[edit] History of the concept

According to George Selgin in his paper "Gresham's Law":

As for Gresham himself, he observed "that good and bad coin cannot circulate together" in a letter written to Queen Elizabeth on the occasion of her accession in 1558. The statement was part of Gresham's explanation for the "unexampled state of badness" England's coinage had been left in following the "Great Debasements" of Henry VIII and Edward VI, which reduced the metallic value of English silver coins to a small fraction of what that value had been at the time of Henry VII. It was owing to these debasements, Gresham observed to the Queen, that "all your ffine goold was convayd ought of this your realm."

Gresham made his observations of good and bad money while in the service of Queen Elizabeth, with respect only to the observed poor quality of the British coinage. The previous monarchs, Henry VIII and Edward VI, had forced the people to accept debased coinage by means of their legal tender laws. Gresham also made his comparison of good and bad money where the precious metal in the money was the same. He did not compare silver to gold, or gold to paper.

An early form of Gresham's Law was described by Nicolaus Copernicus in the treatise Monetae cudendae ratio, first drawn up in the year (1519) that Thomas Gresham was born. Copernicus wrote that "bad (debased) coinage drives good (un-debased) coinage out of circulation."[1]

[edit] Origin of the name

George Selgin in his paper "Gresham's Law" offers the following comments:

10

The expression "Gresham's Law" dates back only to 1858, when British economist Henry Dunning Macleod (1858, p. 476–8) decided to name the tendency for bad money to drive good money out of circulation after Sir Thomas Gresham (1519–1579). However, references to such a tendency, sometimes accompanied by discussion of conditions promoting it, occur in various medieval writings, most notably Nicholas Oresme's (c. 1357) Treatise on money. The concept can be traced to ancient works, including Aristophanes' The Frogs, where the prevalence of bad politicians is attributed to forces similar to those favoring bad money over good.

The passage from The Frogs referred to is as follows; it is usually dated at 405 B.C.:

The course our city runs is the same towards men and money.She has true and worthy sons.She has fine new gold and ancient silver,coins untouched with alloys, gold or silver,each well minted, tested each and ringing clear.Yet we never use them!Others pass from hand to hand,sorry brass just struck last week and branded with a wretched brand.So with men we know for upright, blameless lives and noble names.These we spurn for men of brass....

[edit] The law in reverse

In an influential theoretical article, Rolnick and Weber (1986) argued that bad money would drive good money to a premium rather than driving it out of circulation. However their research did not take into account the context in which Gresham made his observation. Rolnick and Weber ignored the influence of legal tender legislation which requires people to accept both good and bad money as if they were of equal value. They also focused mainly on the interaction between different metallic moneys, comparing the relative "goodness" of silver to that of gold, which is not what Gresham was speaking of.

The experiences of dollarization in countries with weak economies and currencies (for example Israel in the 1980s, Eastern Europe and countries in the period immediately after the collapse of the Soviet bloc, or South American countries throughout the late twentieth and early twenty-first century) may be seen as Gresham's Law operating in its reverse form (Guidotti & Rodriguez, 1992), since in general the dollar has not been legal tender in such situations, and in some cases its use has been illegal.

These examples show that in the absence of legal tender laws, Gresham's law works in reverse. If given the choice of what money to accept, people will transact with money they believe to be of highest long-term value. However, if not given the choice, and required to accept all money, good and bad, they will tend to keep the money of greater perceived value in their possession, and pass on the bad money to someone else. Said in another way, in the absence of legal tender laws, the seller will not accept anything but

11

money of real worth (good money), while the existence of legal tender laws will force the seller to accept money with no commodity value (bad money). Thus, the buyer will always try to spend his bad money first, but in the absence of legal tender laws, the seller will not accept money with no real worth.

[edit] The law in other fields

The principles of Gresham's Law can sometimes be applied to different fields of study. Gresham's Law generally speaks to any circumstance in which the "true" value of something is markedly different from the value people must accept, due to factors such as lack of information or governmental decree.

In the market for second hand cars, lemon automobiles (analogous to bad currency) will drive out the good cars. The problem is one of asymmetry of information. Sellers have a strong financial incentive to pass all cars off as "good" cars, especially lemons. This makes it chancy to buy a good car at a fair price, as the buyer risks overpaying for a lemon. The result is that buyers will only pay the fair price of a lemon, so at least they won't be ripped off. High quality cars tend to be pushed out of the market, because there is no good way to establish that they really are worth more. The Market for Lemons is a work that examines this problem in more detail.

Gresham's Law poses a similar trap in education.[2] For instance, The Economist, writing on the No Child Left Behind act's effect on U.S. schools, said:

Joel Klein, the man in charge of public schools in New York City, lists other perverse incentives. States are rewarded for increasing the proportion of students who pass their exams, but not for raising a child's score from abysmal to nearly-good-enough-to-pass, or from just-passed to brilliant. So they are tempted to lavish attention on those on the cusp of passing, while neglecting both the weakest and the strongest students.[3]

Schools that respond to these incentives (and focus all their attention on those at the cusp of passing) in locations which allow easy switching of schools will tend to drive away the ignored students for whom the value of their education is not adequately captured by the Pass/Fail grade, as Gresham's Law predicts.

A case in education where Gresham's Law generally does not apply is with "diploma mills," schools that offer diplomas even to those with very low qualifications for a price. It may seem that according to Gresham's law these "bad" diplomas ought to drive out the "good" diplomas. However, unlike money, most countries have no law requiring employers to accept all diplomas as being of equal value. Each employer is free to assess the value of qualifications as they see fit. In those nations or governmental organizations where the law does require blindness, this effect does occur

Gold standard

12

From Wikipedia, the free encyclopedia

Jump to: navigation, searchFor other uses, see Gold standard (disambiguation).

The gold standard is a monetary system in which the standard economic unit of account is a fixed weight of gold. Under the gold standard, currency issuers guarantee to redeem notes, upon demand, in that amount of gold. Governments that employ such a fixed unit of account, which will redeem their notes to other governments in gold, share a fixed-currency relationship. The gold standard is not currently used by any government or central bank, having been replaced completely by fiat currency. However, private currency, backed by gold, is in use.

Contents[hide]

1 Why gold? 2 Disadvantages 3 History

o 3.1 Early coinage o 3.2 The crisis of silver currency and bank notes (1750–1870) o 3.3 Establishment of the international gold standard o 3.4 Dates of adoption of a gold standard o 3.5 Gold standard from peak to crisis (1901–1932)

3.5.1 Abandoning the standard to fund the war o 3.6 Depression and World War II

3.6.1 British hesitate to return to gold standard o 3.7 Post-war international gold standard (1946–1971)

4 Theory o 4.1 Differing definitions of gold standard

4.1.1 Perceived stability offered by gold standard 4.1.2 Mundell-Fleming model

5 Advocates and opponents of a renewed gold standard 6 Gold as a reserve today 7 See also 8 References

9 External links

[edit] Why gold?

The history of money consists of three phases: commodity money, in which actual valuable objects are bartered; then representative money, in which paper notes (often called 'certificates') are used to represent real commodities stored elsewhere; and finally fiat money, in which paper notes are backed only by the traders' "full faith and credit" in the government.

13

Commodity money is inconvenient to store and transport and is subject[citation needed] to hoarding. It also does not allow the government to control or regulate the flow of commerce within their dominion with the same ease that a standardized currency does. As such, commodity money gave way to representative money, and gold and other specie were retained as its backing.

Gold was a common form of representative money due to its rarity, durability, easy divisibility ('fungibility'), and the general ease of identification, [1] often in conjunction with silver. Silver was typically the main circulating medium, with gold as the metal of monetary reserve.

The Gold Standard variously specified how the gold backing would be implemented, including the amount of specie per currency unit. The currency itself is just paper and so has no innate value, but is accepted by traders because it can be redeemed any time for the equivalent specie. A US silver certificate, for example, could be redeemed for an actual piece of silver.

Representative money and the Gold Standard protect citizens from hyperinflation and other abuses of monetary policy, as were seen in some countries during the Great Depression. However, they were not without their problems and critics, and so were partially abandoned via the international adoption of the Bretton Woods System. That system eventually collapsed in 1971, at which time all nations had switched to full fiat money.

Former US Federal Reserve Chairman Alan Greenspan has argued that

"under the gold standard, a free banking system stands as the protector of an economy's stability and balanced growth... The abandonment of the gold standard made it possible for the welfare statists to use the banking system as a means to an unlimited expansion of credit... In the absence of the gold standard, there is no way to protect savings from confiscation through inflation."[2]

[edit] Disadvantages

Beyond the difficulty in transporting, storing, and preventing the debasement of gold, one of the main disadvantages of a gold standard is that it might artificially inflate gold's value, increasing the cost of items and industrial processes in which it is used.[3] The total amount of gold that has ever been mined is estimated at about 142,000 tonnes.[4] At a gold price of US$800 per Troy ounce, or around $26,000 per kilogram, the value of this entire planetary stock would be $3.65 trillion, which is less than the value of cash circulating. In the U.S. alone, more than $7.3 trillion is in circulation or on deposit.[5] Under a U.S. gold standard, the price of gold would be more than proportionally higher, because all the gold in the world can not be brought in to U.S. bank vaults.

Under the gold standard, gold mined at a different rate than the economy grows can produce both inflation, when deposits are discovered and extracted, and deflation when

14

they are mined to exhaustion.[6] In practice, the production of gold has usually trailed economic growth, resulting in periods of deflationary pressure, including contributing to the cause of the Great Depression [7] and events during it.[3] During the gold rushes in California and Australia, soaring gold output contributed to a 5% yearly increase in wholesale prices during the period between 1850 and 1855.[8][9]

Using a fixed commodity as a monetary standard gives central banks fewer options with which to respond to economic crises and stimulate economic growth.[10] In particular, gold-backed currencies prevent tailoring the money supply to the economy's demand for money, and are subject to speculative attacks when the government's financial position looks weak; attacks which often require punitive economic measures to counter. Such measures exacerbated the Great Depression when the U.S. raised interest rates in the middle of a recession in order to defend the credibility of its currency.[7] Finally, since commodity currency devaluations produce sharp changes in their values, rather than smooth declines, their effects are magnified.[11]

[edit] HistorySee also: History of the English penny

[edit] Early coinage

Gold coin of Alexander the Great, ca. 330 B.C.E.

The first metal used as a currency was silver more than 4,000 years ago, when silver ingots were used in trade. Gold coins first were used from 600 b.c.e. However, long before this time, gold, as per silver, was used as a store of wealth and the basis for trade contracts in Akkadia, and later in Egypt. During the heyday of the Athenian empire, the city's silver tetradrachm was the first coin to achieve "international standard" status in Mediterranean trade. Silver remained the most common monetary metal used in ordinary transactions until the 20th century.

15

Aureus minted in 193 CE by Septimius Severus.

The Persian Empire collected taxes in gold and issued its own gold coin, known in the West as the δαρεικός, dareikos in Greek, or daricus in Latin. When it was conquered by Alexander the Great, this gold became the basis for the gold coinage of Alexander's empire and those of his Diadochi. The vast gold hoard of the Persian kings was put into monetary circulation, triggering the first known "worldwide" inflation event.

Solidus of Justinian II, ca. 705 CE

The Roman Empire minted two important gold coins: the aureus, which was ~7 grams of gold alloyed with silver, and the smaller solidus, which weighed 4.4 grams, of which 4.2 was gold. These values applied only to the early Empire. Later Roman and Byzantine coins were frequently debased by being alloyed with other metals of much lower value.

The dinar and dirham were gold and silver coins, respectively, originally minted by the Persians. The Caliphates in the Islamic world adopted these coins, starting with Caliph Abd al-Malik (685–705).

Sequin (Venetian ducat), 1382 CE

In 1284 the Republic of Venice coined the ducat, its first solid gold coin. Other coins, the florin, noble, grosh, złoty, and guinea, were also introduced at this time by other European states to facilitate growing trade.

Beginning with the conquest of the Aztec and Inca Empires, Spain had access to stocks of new gold for coinage in addition to silver. The wide availability of milled and cob gold coins made it possible for the West Indies to make gold the only legal tender in 1704. The circulation of Spanish coins would create the unit of account for the United States, the "dollar", based on the Spanish silver real, and Philadelphia's currency market would trade in Spanish colonial coins.

[edit] The crisis of silver currency and bank notes (1750–1870)

16

In the late 18th century wars and trade with China, which sold many trade goods to Europe but had little use for European goods, drained silver from the economies of Western Europe and the United States. Coins were struck in smaller and smaller amounts, and there was a proliferation of bank and stock notes used as money.

In the 1790s Britain suffered a massive shortage of silver coinage and ceased to mint larger silver coins. It issued "token" silver coins and overstruck foreign coins. With the end of the Napoleonic Wars, Britain began a massive recoinage program that created standard gold sovereigns and circulating crowns, half-crowns, and eventually copper farthings in 1821. In 1833, Bank of England notes were made legal tender, and redemption by other banks was discouraged. In 1844 the Bank Charter Act established that Bank of England notes, fully backed by gold, were the legal standard. According to the strict interpretation of the gold standard, this 1844 Act marks the establishment of a full gold standard for British money.

There were 113 grains (7.32g) of gold to one pound sterling.

The U.S. adopted a silver standard based on the "Spanish milled dollar" in July 1785. This was codified in the 1792 Mint and Coinage Act. This began a long series of attempts for America to create a bimetallic standard for the US Dollar, which would continue until the 1930s. Because of the huge debt taken on by the US Federal Government to finance the Revolutionary War, silver coins struck by the government left circulation, and in 1806 President Jefferson suspended the minting of silver coins. The US Treasury was put on a strict "hard money" standard, doing business only in gold or silver coin as part of the Independent Treasury Act of 1846, which legally separated the accounts of the Federal Government from the banking system. Following Gresham's law, silver poured into the US, which traded with other silver nations, and gold moved out. In 1853, the US reduced the silver weight of coins, to keep them in circulation.

[edit] Establishment of the international gold standard

Germany was created as a unified country following the Franco-Prussian War; it established the mark. Rapidly most other nations followed suit. Gold became a transportable, universal and stable unit of valuation, and the world's dominant economy, the United Kingdom, had a longstanding commitment to the gold standard.[12] See Globalization.

[edit] Dates of adoption of a gold standard

1717: United Kingdom [13] at £1 to 113 grains (7.32g) of gold 1818: Netherlands at 1 guilder to 0.60561 g gold 1854: Portugal at 1000 réis to 1.62585 g gold 1871: Germany at 2790 Goldmarks to 1 kg gold 1873: Latin Monetary Union (Belgium, Italy, Switzerland, France) at 31 francs to

9 g gold 1873: United States de facto at 20.67 dollars to 1 troy oz

17

1875: Scandinavian monetary union: (Denmark, Norway and Sweden) at 2480 krone to 1 kg gold

1876: France internally 1876: Spain at 31 pesetas to 9 g gold 1878: Finland at 31 marks to 9 g gold 1879: Austria (see Austrian florin and Austrian crown) 1893: Russia at 31 roubles to 24 g gold 1897: Japan at 1 yen to 1.5 g gold 1898: India (see Indian rupee) 1900: United States de jure.

Throughout the decade of the 1870s deflationary and depressionary economics created periodic demands for silver currency. However, such attempts generally failed, and continued the general pressure towards a gold standard. By 1879, only gold coins were accepted through the Latin Monetary Union, composed of France, Italy, Belgium, Switzerland and later Greece, even though silver was, in theory, a circulating medium.

[edit] Gold standard from peak to crisis (1901–1932)

[edit] Abandoning the standard to fund the war

The British government ended the convertibility of Bank of England notes to gold in 1914 to fund military operations during World War I. By the end of the war Britain was on a series of fiat currency regulations, which monetized Postal Money Orders and Treasury Notes. The government later called these notes banknotes, which are different from US Treasury notes. The United States government took similar measures. After the war, Germany, losing much of its gold in reparations, could no longer coin gold "Reichsmarks," and moved to paper currency, although the Weimar Republic later introduced the "rentenmark," and later the gold-backed reichsmark in an effort to control hyperinflation.

In the UK the pound was returned to the gold standard in 1925, by a somewhat reluctant Winston Churchill. Although a higher gold price and significant inflation had followed the WWI ending of the gold standard, Churchill returned to the standard at the pre-war gold price. For five years prior to 1925 the gold price was managed downward to the pre-war level, causing deflation throughout those countries using the Pound Sterling. This deflation reached across the remnants of the British Empire everywhere the Pound Sterling was still used as the primary unit of account. The British government abandoned the standard again on September 20, 1931. Sweden abandoned the gold standard in October 1931, the U.S. in 1933, and other nations were, to one degree or another, forced off the gold standard.

[edit] Depression and World War II

[edit] British hesitate to return to gold standard

18

During the 1939–1942 period, the UK depleted much of its gold stock in purchases of munitions and weaponry on a "cash and carry" basis from the U.S. and other nations.[citation

needed] This depletion of the UK's reserve convinced Winston Churchill of the impracticality of returning to a pre-war style gold standard. John Maynard Keynes, who had argued against such a gold standard, became increasingly influential. He proposed a more wide ranging version of the "stability pact" style gold standard, later expressed in the Bretton Woods Agreement.

[edit] Post-war international gold standard (1946–1971)

Main article: Bretton Woods system

[edit] Theory

The theory of the gold standard rests on the idea that inflation is caused by an increase in the supply of money, an idea advocated by David Hume, and that uncertainty over the future purchasing power of currency depresses business confidence and leads to reduced trade and capital investment.

[edit] Differing definitions of gold standard

If the monetary authority holds sufficient gold to convert all circulating money, then this is known as a 100% reserve gold standard, or a full gold standard. In some cases it is referred to as the Gold Specie Standard to more easily separate it from the other forms of gold standard that have existed at various times. The 100% reserve standard is generally considered unworkable because the quantity of gold in the world is too small a quantity of money to sustain current worldwide economic activity and the "right" quantity of money (i.e. one that avoids either inflation or deflation) is not a fixed quantity, but varies continuously with the level of commercial activity.

In an international gold-standard system, which may exist in the absence of any internal gold standard, gold or a currency that is convertible into gold at a fixed price is used as a means of making international payments. Under such a system, when exchange rates rise above or fall below the fixed mint rate by more than the cost of shipping gold from one country to another, large inflows or outflows occur until the rates return to the official level. International gold standards often limit which entities have the right to redeem currency for gold. Under the Bretton Woods system, these were called "SDRs" for Special Drawing Rights.

[edit] Perceived stability offered by gold standard

The gold standard, in theory, limits the power of governments to inflate prices through excessive issuance of paper currency. It is also supposed to create certainty in international trade by providing a fixed pattern of exchange rates. Under the classical international gold standard, disturbances in the price level in one country would be wholly or partly offset by an automatic balance-of-payment adjustment mechanism called

19

the "price specie flow mechanism." At the time of the Bretton Woods agreement, it was believed that markets were always internally clear; Say's Law. However, in practice, wages, not capital, depreciate in price first.

.

Few lawmakers[attribution needed] today advocate a return to the gold standard, other than adherents the Austrian school and some supply-siders. However, many prominent economists have expressed sympathy with a hard currency basis, and have argued against fiat money, including former US Federal Reserve Chairman Alan Greenspan and macro-economist Robert Barro. Greenspan famously argued the case for returning to a gold standard in his 1966 paper "Gold and Economic Freedom", in which he described supporters of fiat currencies as "welfare statists" hell-bent on using monetary printing presses to finance deficit spending. He has argued that the fiat money system of today has retained the favorable properties of the gold standard because central bankers have pursued monetary policy as if a gold standard were still in place.

The current monetary system relies on the US Dollar as an “anchor currency” which major transactions, such as the price of gold itself, are measured in. Currency instabilities, inconvertibility and credit access restriction are a few reasons why the current system has been criticized. A host of alternatives have been suggested, including energy-based currencies, market baskets of currencies or commodities; gold is merely one of these alternatives.

20

Top Related