Languages

Pages

Legal

Community Participation in the Funding of Informal BusinessesFinMark Forum

21 January 2009

Contents

Introductory movieIntroductory movie

BackgroundBackground

Business ModelBusiness Model

MethodologyMethodology

Key lessons learntKey lessons learnt

ConclusionConclusion

Coenraad Jonker

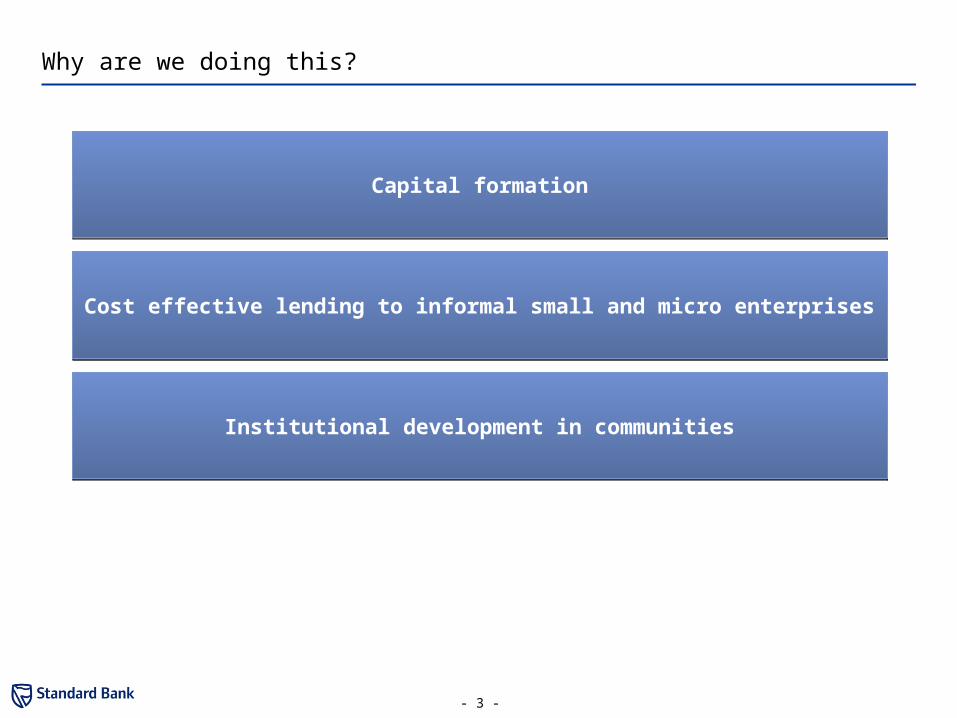

Why are we doing this?

- 3 -

Cost effective lending to informal small and micro enterprisesCost effective lending to informal small and micro enterprises

Institutional development in communitiesInstitutional development in communities

Capital formationCapital formation

Results as at end November 2008

- 4 -

The amount of money that has been lentThe amount of money that has been lent

The number of loansThe number of loans

The average size of the loansThe average size of the loans

The beneficiary gender split (female)The beneficiary gender split (female)

The default rateThe default rate

R7.1mR7.1m

630630

R11 037.61R11 037.61

79%79%

7.13%7.13%

Contents

- 5 -

Introductory movieIntroductory movie

BackgroundBackground

Business ModelBusiness Model

MethodologyMethodology

Key lessons learntKey lessons learnt

ConclusionConclusion

Coenraad Jonker

CIF 2CIF 2 CIF 3CIF 3CIF 1CIF 1

Business Model - A CIF is capitalised from a central trust and thereafter becomes a revolving source of funds

Standard Bank Community Investment Trust

Standard Bank Community Investment Trust

Donor 1Donor 1 Donor 2Donor 2 Donor 3Donor 3

Loan

The CIF uses donor funding for the purpose of

on-lending to informal micro enterprises

Community peer pressure and moral persuasion are used to ensure repayment.

No collateral required

Repayment

Donors do not accrue any profit – all returns are

reinvested into the fund

etc

All donor funds accrue to an umbrella fund which disburses

monies to the various CIF’s

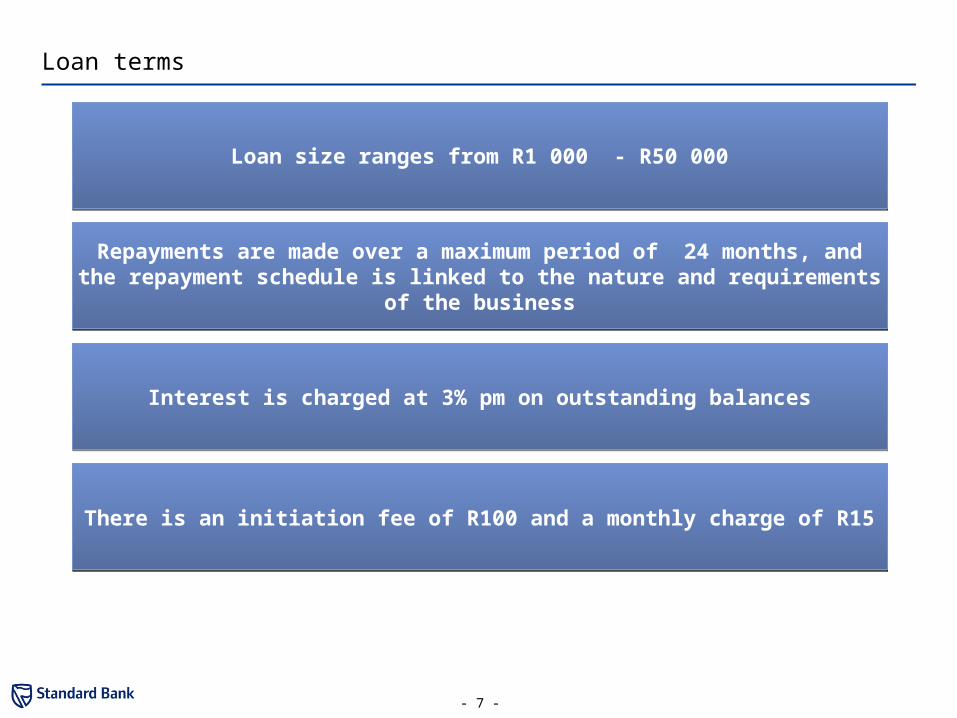

Loan terms

- 7 -

Repayments are made over a maximum period of 24 months, and the repayment schedule is linked to the nature and requirements of the business

Repayments are made over a maximum period of 24 months, and the repayment schedule is linked to the nature and requirements of the business

Interest is charged at 3% pm on outstanding balancesInterest is charged at 3% pm on outstanding balances

Loan size ranges from R1 000 - R50 000Loan size ranges from R1 000 - R50 000

There is an initiation fee of R100 and a monthly charge of R15There is an initiation fee of R100 and a monthly charge of R15

Contents

- 8 -

Introductory movieIntroductory movie

BackgroundBackground

Business ModelBusiness Model

MethodologyMethodology

Key lessons learntKey lessons learnt

ConclusionConclusion

Mike Shongwe

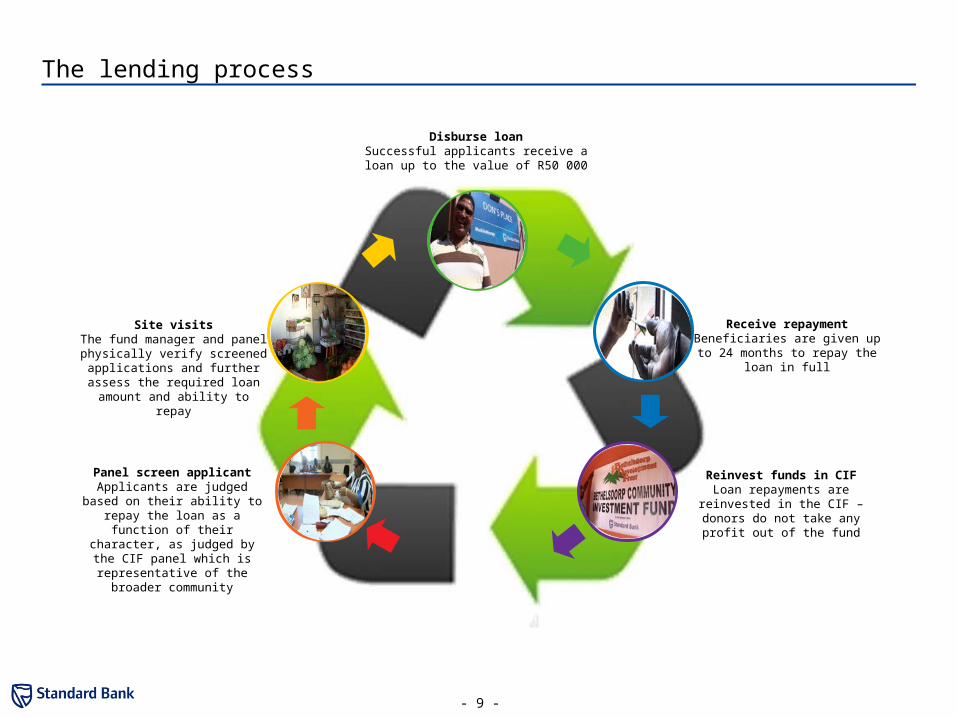

The lending process

- 9 -

Community Investment Fund

Process Flow

Launch fund

Receive Loan

application

Site visitsThe fund manager and panel

physically verify screened applications and further assess the required loan amount and ability to

repay

Panel screen applicantApplicants are judged based on

their ability to repay the loan as a function of their character, as

judged by the CIF panel which is representative of the broader

community

Receive repaymentBeneficiaries are given up to 24 months to repay the loan in full

Reinvest funds in CIFLoan repayments are reinvested in the CIF – donors do not take any

profit out of the fund

Disburse loanSuccessful applicants receive a loan up to

the value of R50 000

Contents

- 10 -

Introductory movieIntroductory movie

BackgroundBackground

Business ModelBusiness Model

MethodologyMethodology

Key lessons learntKey lessons learnt

ConclusionConclusion

Mike Shongwe

Lessons learnt

- 11 -

Community Investment Fund

Process Flow

Launch fund

Receive Loan

application

Site visits1.Decisions are taken on your feet – you do it while you are physically there2.Have to be passionate. Have to get to the level of the people 3.It is a community process, not an efficiency process (the time to listen)4.Try to avoid giving loans that will not repaid

Panel screen applicant1.Initially 50% of applications are deferred, but approvals increase as experience grows2.Experience is important in assessment

Receive repayment

Reinvest funds in CIF

Disburse loan1.Entrepreneur hand-holding by other service providers

1. The community partners must “see the opportunity”.2. Partners can take various forms and are community specific 3. Panel independence must be understood upfront and reinforced all the

time

Contents

- 12 -

Introductory movieIntroductory movie

BackgroundBackground

Business ModelBusiness Model

MethodologyMethodology

Key lessons learntKey lessons learnt

ConclusionConclusion Coenraad Jonker

Conclusions

What we don’t yet know:

– Optimal scale of funds

– Optimal operation once the funds are independent

– How to replicate lending skills and maintain performance at scale

- 13 -

Foundation Maturation Growth

What we have learnt

- 14 -

Disbursed over 630 loans to those considered uncreditworthy by conventional standards

Disbursed over 630 loans to those considered uncreditworthy by conventional standards

The structure is low cost (a single professional per fund / per two funds)

Performance of the funds is good (7.13% default rate)

The structure is low cost (a single professional per fund / per two funds)

Performance of the funds is good (7.13% default rate)

Trained 60 community members as fund panel members, providing them with skills in the areas of

character introduction and making lending recommendations

Trained 3 community members as resident CIF Managers

Trained 60 community members as fund panel members, providing them with skills in the areas of

character introduction and making lending recommendations

Trained 3 community members as resident CIF Managers

Standard Bank has become known in the CIF communities as “the bank that cares”

Standard Bank has become known in the CIF communities as “the bank that cares”

Informal businesses constitute a worthy market

Informal businesses constitute a worthy market

Institutional capacity at community level adds value and reduces risk

Institutional capacity at community level adds value and reduces risk

Building a skills base in micro-lending is an intense people orientated development

process

Building a skills base in micro-lending is an intense people orientated development

process

The involvement of communities in the lending process reconnects people and

institutions

The involvement of communities in the lending process reconnects people and

institutions

-END-

- 15 -

Background on presenters

Coenraad Jonker

Coenraad is a cum laude MBA graduate from the Gordon Institute of Business Science and currently lectures the MBA course on doing business in informal markets. He also holds B Luris and LLB degrees, both cum laude.

Coenraad is currently the Director of Community Banking at Standard Bank and has served Edward Nathan Corporate Law Advisors for 9 years of which 5 years were as Chief Executive Officer.

Mike Shongwe

Mike Shongwe is a career banker. He left conventional banking when he was the Head of National Sales and Marketing at Standard Bank Swaziland in July’ 99 following his appointment to spearhead a vision by the bank and other corporate partners, to set up the Inhlanyelo “Seed Capital” Fund; a private enterprise initiative, established to promote socio-economic development targeted at the under privileged and unbanked population across Swaziland. The Fund has since established itself as an unrivalled informal micro enterprises financier in Swaziland.

In September 2007 he joined Standard Bank of SA [SBSA] to design an implementation model for the bank’s new Community Investment Fund – a job creation and poverty reduction intervention in SA’s informal business sector.

- 16 -

Top Related