Languages

Pages

Legal

Commerzbank

Sector Conference Week

Frankfurt –

August 26, 2010

Dr. Claus Ehrenbeck, Head

of Investor Relations

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

1

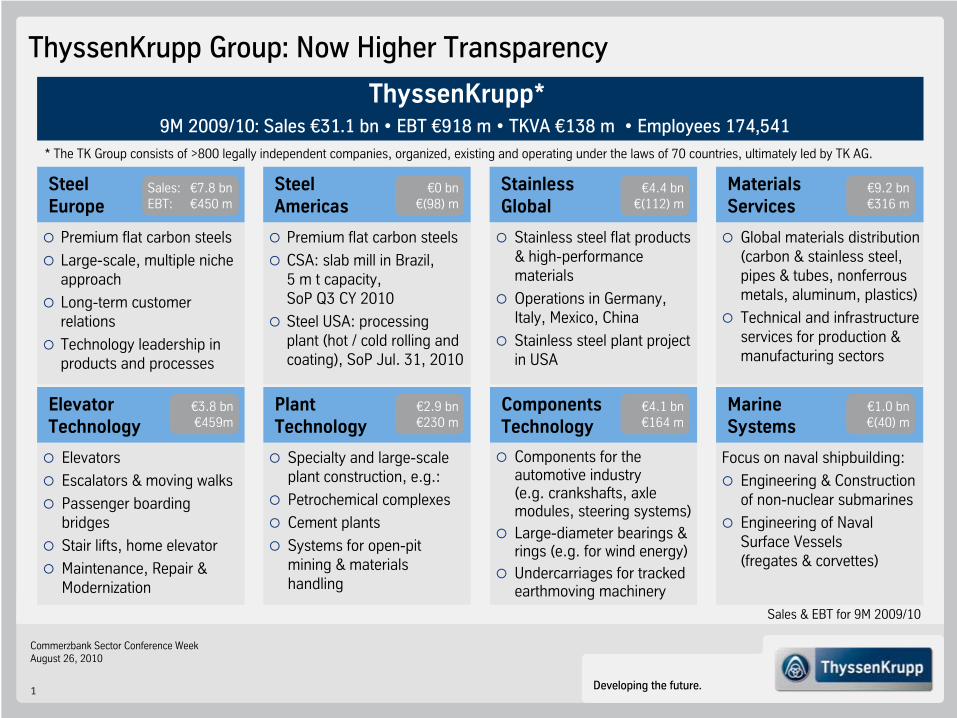

Premium flat carbon steels

Large-scale, multiple niche approach

Long-term customer relations

Technology leadership in products and processes

Premium flat carbon steels

CSA: slab mill in Brazil, 5 m t capacity,SoP Q3 CY 2010

Steel USA: processing plant (hot / cold rolling and coating), SoP Jul. 31, 2010

Stainless steel flat products & high-performance materials

Operations in Germany, Italy, Mexico, China

Stainless steel plant project in USA

Global materials distribution(carbon & stainless steel, pipes & tubes, nonferrous metals, aluminum, plastics)

Technical and infrastructureservices for production & manufacturing sectors

Elevators

Escalators & moving walks

Passenger boarding bridges

Stair lifts, home elevator

Maintenance, Repair & Modernization

Specialty and large-scale plant construction, e.g.:

Petrochemical complexes

Cement plants

Systems for open-pit mining & materials handling

Components for theautomotive industry(e.g. crankshafts, axlemodules, steering systems)Large-diameter bearings & rings (e.g. for wind energy)Undercarriages for trackedearthmoving machinery

Focus on naval

shipbuilding:

Engineering & Construction of non-nuclear submarines

Engineering of NavalSurface Vessels(fregates & corvettes)

Steel

Europe

Steel

Americas

Stainless

Global

Materials

Services

ElevatorTechnology

Plant Technology

ComponentsTechnology

MarineSystems

9M 2009/10: Sales €31.1 bn

•

EBT €918 m •

TKVA €138 m •

Employees 174,541

ThyssenKrupp*

ThyssenKrupp Group: Now

Higher

Transparency

* The TK Group consists of >800 legally independent companies, organized, existing and operating under the laws of 70 countries, ultimately led by TK AG.

Sales:

€7.8 bnEBT:

€450 m€0 bn

€(98) m

Sales & EBT for

9M 2009/10

€4.4 bn€(112) m

€9.2 bn€316 m

€2.9 bn€230 m

€4.1 bn€164 m

€1.0 bn€(40) m

€3.8 bn€459m

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

2

Group Performance and Financials

Business Area Performance

Group Outlook

Agenda

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

3

Efficiency

Management Focus

•

Realization of sustainable cost savings on track

•

Additional reduction of structural overcapacities at Components Technology

•

Cash and cost control

Reducing complexity and risk

Restoring the basis for future value creation

Projects

•

Commissioning of blast furnace and meltshop:

•

BF #1: July 12

•

1st coil: July 31

•

Intensive marketing across all US customer segments

•

Ramp-up of BF #2 earlier

now expected by end of 2010

Portfolio

Growth Structural Performance

•

Marine Systems:•

Strategic partnership with Abu Dhabi MAR (sale of Hamburg site & JV naval surface vessels) before closing

•

Best owner process for

Metal Forming business

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

4

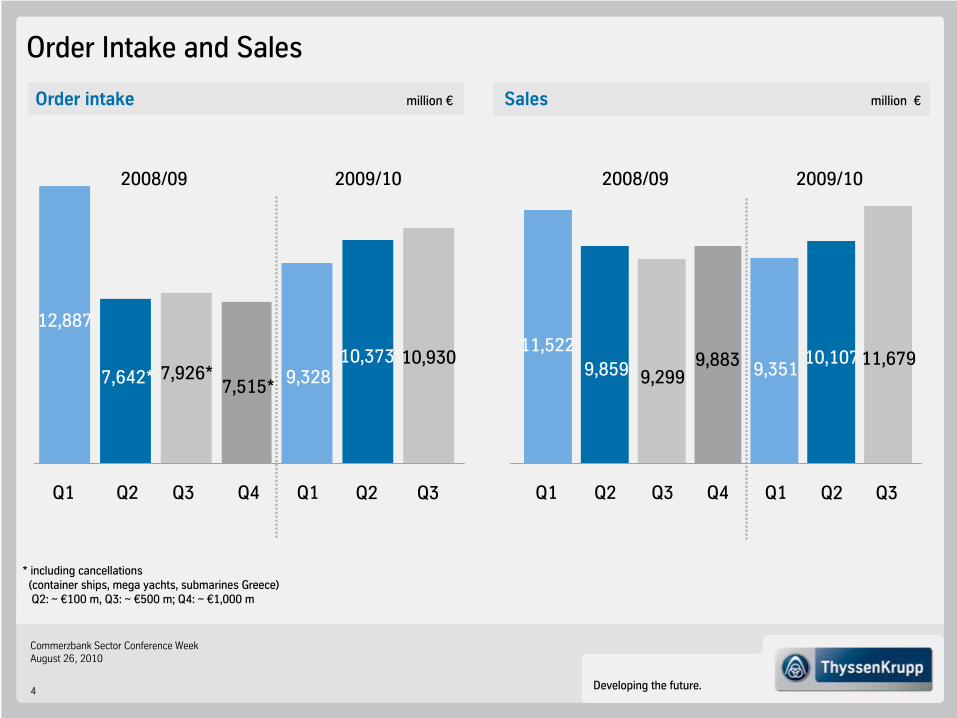

Order Intake and Sales

Order intake

million €

Q1 Q2

12,887

7,642* 7,515*7,926*

Q3 Q4

2008/09

9,328

Q1

2009/10

Sales

million €

Q1 Q2

11,5229,859 9,299

Q3 Q4

9,883 9,351

Q1

2008/09 2009/10

* including

cancellations

(container

ships, mega

yachts, submarines Greece)

Q2: ~ €100 m, Q3: ~ €500 m; Q4: ~ €1,000 m

10,373

Q2

10,107

Q2

10,930

Q3

11,679

Q3

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

5

Earnings Before Interest and Taxes and Earnings Before Taxes

Q1Q2

Q3 Q4

2008/09

Q1

2009/10

EBIT adjusted

million €

Q1Q2

407(276)

(1,197)(597)

Q3

Q4

2008/09

477

Q1

2009/10

416 (112)(289) (390)

401

EBIT

million €

EBT adjusted

million €

Q1

Q2

Q3 Q4

2008/09

Q1

2009/10

249

(291) (464) (570)

237

EBT million €

Q1Q2

240(455)

(1,377)(772)

Q3

Q4

2008/09

313

Q1

2009/10

191

Q2 Q2

206

354

Q2 Q2

369587

Q3 Q3

653

414

Q3 Q3

480

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

6

million € Q1 Q2 Q3 Q4 Q1 Q2 Q3

Steel Europe 371 131 (156) (262) 126 179 200

% 13.0 5.6 (7.3) (11.7) 5.5 6.7 6.9

Steel Americas (42) 0 9 (44) 37 7 (26)

% n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Stainless Global (228) (291) (139) (55) (41) (102) 81

% (19.4) (29.5) (13.5) (4.2) (3.4) (7.0) 4.7

Materials Services 54 (88) (106) 1 48 70 157

% 1.4 (2.8) (3.9) 0.0 1.7 2.4 4.4

Elevator Technology 157 149 168 124 154 151 150

% 11.7 11.5 12.7 9.2 12.6 12.4 11.4

Plant Technology 72 62 50 24 82 59 48

% 6.7 5.2 4.5 2.2 8.6 6.3 4.9

Components Technology 66 (7) (60) (85) 57 73 113

% 5.1 (0.6) (5.6) (7.4) 4.6 5.4 7.2

Marine Systems 32 (45) (27) (39) (1) 11 (3)

% 5.9 (12.1) (8.4) (11.0) (0.4) 3.8 (0.7)

Group 416 (112) (289) (390) 401 369 653% 3.6 (1.1) (3.1) (3.9) 4.3 3.7 5.6

2008/09 2009/10

Quarterly EBIT Adjusted and Margin

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

7

Net Income and Earnings Per Share

Net income

million €

Q1

Q2

163

(362)

(1,044)

(630)

Q3

Q4

2008/09

195

Q1

2009/10

EPS

€

Q1

Q2

0.36

(0.71)

(1.38)

Q3

Q4

(2.28)

0.35

Q1

2008/09 2009/10

234

Q2

0.45

Q2

Expected

FY 2009/10 tax rate: ~ 20%

298

Q3

0.58

Q3

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

8

Net Financial Debt

FCF: (950)Capex*

NFDMar 2010

NFDJun 2010

(3,753)

(942)

Gearing34.3%

OCF(23)

(2,652)

Gearing25.5%

15Divestments

thereof:•

Steel Europe 53• Steel Americas

622thereof:

TK CSA 310

NAFTA Steel

312

•

Stainless Global

88 thereof:

NAFTA Stainless

80• Materials Services

28• Elevator Technology 19• Plant Technology 6•

Components Technology

47

Others

Development of net financial debt in Q3

million €

* Capex

for property, plant & equipment + financial & intangible assets

(151)

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

9

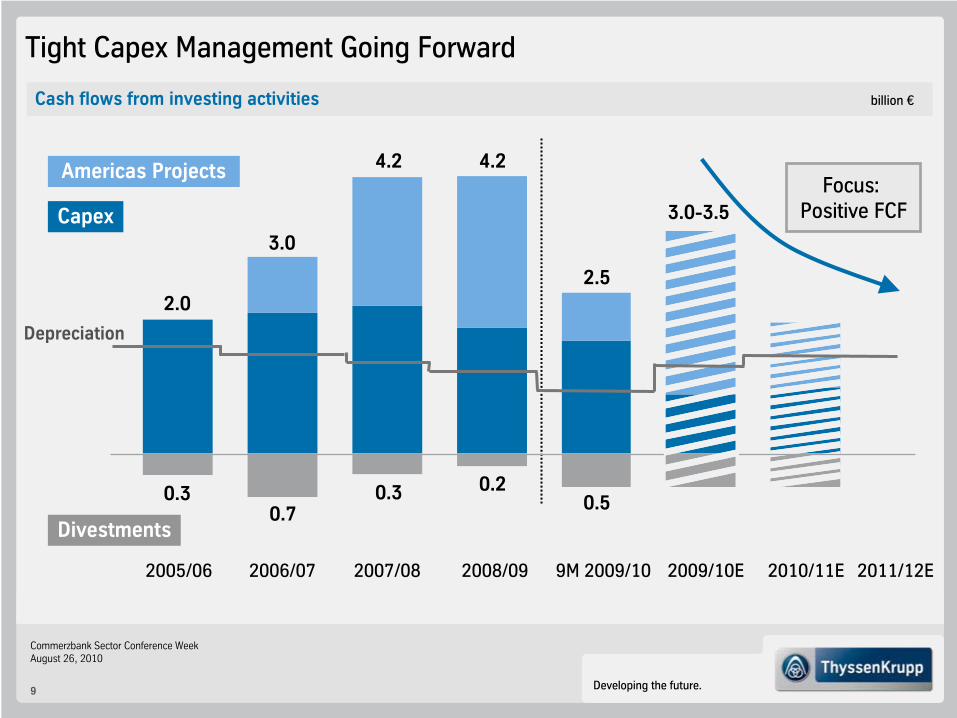

Tight Capex

Management Going Forward

2005/06 2007/082006/07 2008/09

Capex

Divestments

2009/10E 2010/11E

3.0-3.5

Americas Projects

2011/12E

4.24.2

3.0

2.0

0.30.7

0.3 0.2

Depreciation

Cash flows from investing activities

billion €

9M 2009/10

2.5

0.5

Focus: Positive FCF

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

10

Group Performance and Financials

Business Area Performance

Group Outlook

Agenda

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

11

109

Steel Europe

Q3 2009/10 Highlights

Comments Q3 (qoq)

EBT in €m

Q1 Q2 Q3 Q4 Q1

2008/09

Order intake in €m

Current trading conditions

2009/102008/09

(312)

345104

2009/10

(339)

354

Q1 Q2

Q3 Q4

Q1

EBT adjustedEBT

112(172) (273) 163

Q2

Q2

Efficiency gains, higher volumes and higher average revenues per ton compensate increasing raw material costs

Further improvement in downstream utilization; upstream capacities fully loaded

High utilization, higher average revenues per ton and significantly increased raw material costs

Robust demand from key customer groups benefiting from improved export business

Best owner process for Metal Forming business

1,866 1,4792,223 2,324 2,500 2,999

183

Q3

Q3

2,706

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

12

Average revenues per ton*, indexed

Q1 2004/2005 = 100

HKM share

724 873 837756

334265

440410

Q2

Steel Europe: Output, Shipments and Revenues per Metric Ton

3,459

Fiscal year

2005/06 2006/07

3,615

Q1

2008/09

3,194

Cold-rolledHot-rolled

122139

120100

125114

133

156

111129 136

116

153

116138

118 118133 134

115 123

150

120

Q12005/06Q2 Q3 Q4Q1

2004/05Q2 Q3 Q4 Q1

2006/07Q2 Q3 Q4

1,953

Q3

1,512

2,566

Q4

2007/08Q1 Q2 Q3 Q4

2007/08

3,553

Q1

2009/10

2,964

Crude steel output (incl. share in HKM)

1,000 t/quarter Shipments*: Hot-rolled and cold-rolled products

1,000 t/quarter

2008/09Q1 Q2 Q3 Q4

2,735 2,742 2,7162,438

1,6191,247

2,1262,554

Fiscal year

2005/06 2006/07

3,483

2007/08

1,001

2,482

3,513

1,048

2,465

3,590

1,093

2,497

Q1

2008/09

Q2 Q3 Q4

2,517

815

1,702

2,088

573

1,515

2,116

533

1,583

2,620

719

1,901

Q1

2009/10

2,533

715

1,818

2009/10Q1

* shipments and average revenues per ton until FY 2007/08 relate

to former Steel segment

3,326

2,601

726

Q2 Q2

3,167

Q2

2,199

968

3,614

2,755

859

Q3

3,216

Q3

Q3

2,165

1,051

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

13

300

400

500

600

700

800

900

1.000

Premium Product Mix Generates Above-Average Revenues

Premium Product Mix Steel Europe FY 2008/09

in % of sales

6

8

12

33

11

45

15

6

TailoredBlanks Construction

Elements

ElectricalSteel

Medium-wide Strip

Hot Strip

Tinplate

Coated Products(HDG, EG, Color)

Cold Strip

Heavy Plate

Revenues/t

€/t

*)

excl. Metal Forming

2004 200820062005 20092007

BA Steel Europe*)

majorEuropean

competitors

Multiple

Niches

Large

Scale

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

14

Demanding

Example

Applications

and Solutions Based

on Premium Flat

Carbon

Steels Made by

ThyssenKrupp

Thickhot strip

Heavy Plate

Bodies

up to 24% lighter

with

same

safety

performance

Involving

>30 innovative solutionsfor

body, chassis

and powertrain

Ratio of load

capacity

tooperating

weight

increased

to 8:1

In sour

gas resistant

gradesfor

pipelines

For extreme demands

on deep

drawing

properties

(0.07 mm)

Up to 99% efficiency

Tinplate

ElectricalSteels

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

15

Project costs in Q3 partially compensated by positive translation effect (Brazilian Real/€)

ThyssenKrupp CSA BF #1 blown in on July 12;

SoP

BF #2 currently planned for end of 2010

ThyssenKrupp Steel USA: 1st HRC on July 31

InCar project – toolbox for optimized weight/cost/safety solutions – rolled out to NAFTA customer base

Steel Americas

Q3 2009/10 Highlights

Comments

2009/102008/09

Q1 Q2 Q3 Q4 Q1

(22)

(76)

(4)

(99)

(19)

EBT in €m ThyssenKrupp CSA

Sepetiba Bay, Santa Cruz, Rio de Janeiro, BrazilCoking plant: 1.9 m t/yr of cokeSinter plant: 5.7 m t/yr of sinter2 blast furnaces: 5.3 m t/yr of hot metal Steel shop: >5 m t/yr of slabsPower plant: 490 MWCapex budget: €5.2 bnTotal cash-out: €5.9 bn1st slab: Q3 CY 2010

ThyssenKrupp Steel USASite on the Tombigbee River, Mobile Cty, AL, USAHot strip mill: >5 m t/yr

up to 74” width / 1” thickness, 7 standsTandem/cold strip line: 2.5 m t/yr4 galvanizing lines: 1.8 m t/yrCapex budget: $3.6 bnTotal cash-out: $3.8 bn1st coil: July 31, 2010

Q2

(32)

Q3

(62)

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

16

TKS USA

Mini-MillBlast Furnace

Auto Customers

Industry (Non-Auto) Customers

1) Size of Industry and Auto bubbles reflect the approximate number of customer locations in the given area.

2) Includes all steelmaking (EAF, BF) locations, excluding West Coast of U.S. and Canada.

Well Positioned in Southeastern United States with Proximity to Mexico Geographic Position of TKS USA, our Home Market and BF & EAF Competitors

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

17

ThyssenKrupp CSA:Blow in BF #1on July 12

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

18

ThyssenKruppSteel USA:

1st Coil on July 31

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

19

Stainless Global

Q3 2009/10 Highlights

Comments Q3 (qoq)

Q1 Q2 Q3 Q4 Q1

2008/09

Order intake in €m

Current trading conditions

2009/10

(367)

EBT in €m

2009/102008/09

(202)(243)

(59)(114)

Q1

Q2

Q3

Q4Q1

(156) (69)(307)

EBT adjustedEBT

(117)

Q2

Q2

Positive earnings due to higher transaction prices, ongoing high capacity utilization and positive nickel hedge effect

Continuing increase in transaction prices throughout the whole quarter

Lower order intake due to cautious ordering by service centers (decreasing nickel price by end of Q3)

Seasonally lower volumes and capacity utilization (mainly Italy), but robust demand from end customersDecreasing base prices and alloy surcharges in July and August, increase in base prices intended from SeptemberSeasonal and nickel price-related de-stocking from normal levels; pick-up in demand from September likely

967 8181,207 1,155 943

1,560

64Q3

Q3

1,317

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

20

Shipments Stainless*: Hot-rolled and cold-rolled productsCrude steel output*

1,000 t/quarter

Stainless Global: Output, Shipments and Average Transaction Price

Q1Fiscal year

2005/06

2008/09

Q2

* including carbon, forging, Ni-Alloys

Q3 Q4 Q1Fiscal year

2005/06

2008/092006/07 Q2

Hot-rolled, including slabsCold-rolled, including precision strip

567510

Q3 Q1Q4

98 9577

95

7089

122

161

118

90

123

161

82100

171

8294

123 125

177

9892

134

2007/08

Q12005/06Q2 Q3 Q4Q1

2004/05

Q2 Q3 Q4 Q1

2006/07

Q2 Q3 Q4 Q1 Q2 Q3 Q4

2006/07

2008/09

Q1 Q2 Q3

375327

450

Q1

Average transaction price per ton, indexed

Q1 2004/2005 = 100

* consolidated

531

Q4 Q1

2007/08

1,000t/quarter

516504

2007/082009/10

690630 624

465

315

525591 603 84 87

126

441 426 429

6054

99135

315 273 351 396

147

357

2009/10

2009/10

657

Q2 Q2

129

447

576

Q2

Q3

665

Q3

534

Q3

412

122

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

21

Materials Services

Q3 2009/10 Highlights

Comments Q3 (qoq)

Q1 Q2 Q3 Q4 Q1

2008/09

Order intake in €m

Current trading conditions

2009/10

EBT in €m

2009/102008/09

30

112

(91)(128)(106)Q1

Q2 Q3 Q4

Q1(19)

31

EBT adjustedEBT

60

Q2

Q2

Improvement in volumes and prices throughout all product groups

Demand strongly supported by German automotive and mechanical engineering customers

All Operating Units with improving earnings

Restructuring efforts bearing fruits

Continuing underlying demand strength and moderate seasonal impact in Europe

Cash-conscious inventory management across all customer groups

4,016

2,719 2,4692,881 2,681

3,059

144

Q3

Q3

3,695

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

22

Elevator Technology

Q3 2009/10 Highlights

Comments Q3 (qoq)

Q1 Q2 Q3 Q4 Q1

2008/09

Order intake in €m

Current trading conditions

2009/102008/09

Q1 Q2 Q3 Q4 Q1

149159 15596

166

EBT in €m

2009/10

124

EBT adjustedEBT

Q2

153

Q2

Global new installation growth is driven by Asia/China

Infrastructure projects adding additional market potential

North American and European new installation bottoming out

Strongest order intake for 6 quarters, driven by stabilizing demand and continuous expansion of maintenance business

Solid earnings performance with all Operating Units contributing positively

Strength in maintenance compensates for regional softening in new installation and modernization

1,5621,189 1,186 1,101 1,230 1,215

Q3

151

Q3

1,390

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

23

Elevator Technology: Strategic Direction

Performance Improvement Growth of Service Business

850,000

900,000

950,000

1,000,000

2007/08 2008/09

Units under maintenance

+100,000Units

Efficient and global production network

Harmonized product portfolio based on global platforms

Focus on Service & Modernization

Standardization of processes

Q1 Q2 Q3 Q4 Q1 Q2

2008/09 2009/10

14

EBIT %EBIT adj. €m

250

150

Q1 Q2 Q3 Q4

2007/08

9.1%

11.2%12.2%

50

10

6

2

Q3

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

24

Plant Technology

Q3 2009/10 Highlights

Comments Q3 (qoq)

Q1 Q2 Q3 Q4 Q1

2008/09

Order intake in €m

Current trading conditions

2009/102008/09

Q1 Q2 Q3 Q4 Q1

7499 95

(2)65

EBT in €m

2009/10

79 66

37

EBT adjustedEBT

Q2

73

Q2

1,751

517807

463

1,324824

Q3

62

Q3

800

Stable positive development of sales and order intake in all businesses, only cement plants with delays in award of several larger projects

Earnings realization lower in Q3 due to lower PoCorder execution; additionally burdened by impairments at production systems for auto industry

Order backlog of €6.5 bn (1.7x sales) supporting sales and earnings visibility

Recovery of raw materials markets leading to increased project activity in chemical, mining and minerals businesses

Cement plants subject to intensified competition with lower number of projects up for award

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

25

Plant Technology: Technology Portfolio Offering

Growth Potential

OU

Polysius

Förder-

technik

Uhde

Technologies Market Positions

Gas & Oil Refining

Biotechnology

Gasification

Coke

Plant Technologies

Electrolysis

HandlingProcessingHandlingMining

Mining and Materials

Handling

Equipment: No.1

Cement

plants:

No.3

Conversion

Technologies Customer

Products

Fertilizers, Org. Chemicals

& Polymers

Biopolymers

Electric Power; Fuel

Steel

Inorganic

& Organic

Chemicals

Raw

material preparation Clinker

production Cement

manufacturing

Fertilizers: No.1Polymers: No.2

Coke

Plant Tech.: No.1

Electrolysis: No.1

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

26

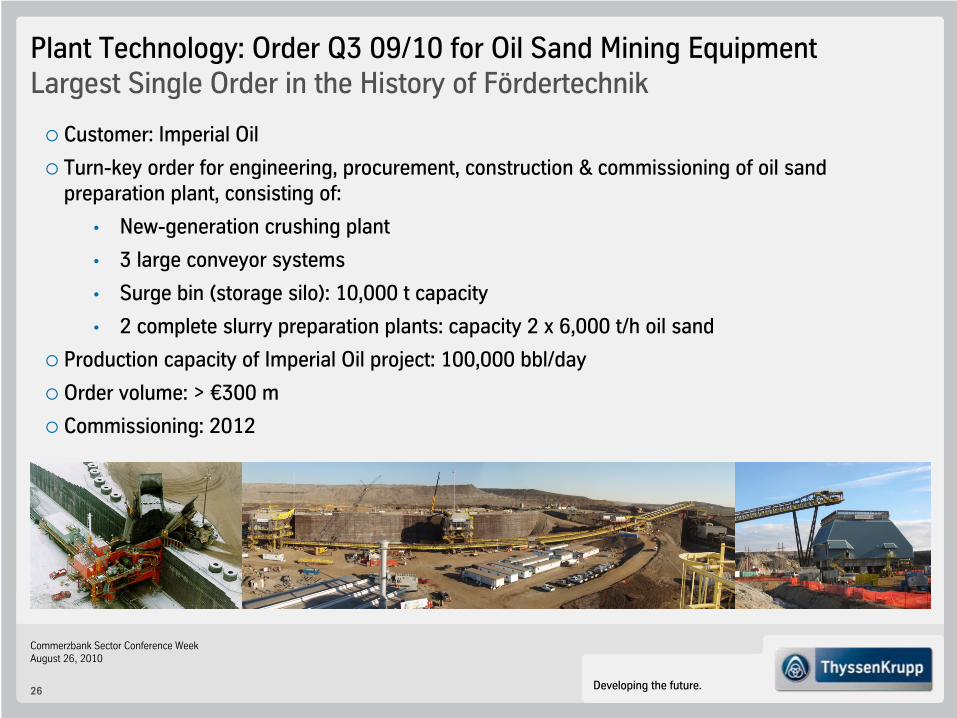

Plant Technology: Order Q3 09/10 for Oil Sand Mining Equipment Largest Single Order in the History of Fördertechnik

Customer: Imperial Oil

Turn-key order for engineering, procurement, construction & commissioning of oil sand preparation plant, consisting of:

•

New-generation crushing plant

•

3 large conveyor systems

•

Surge bin (storage silo): 10,000 t capacity

•

2 complete slurry preparation plants: capacity 2 x 6,000 t/h

oil sand

Production capacity of Imperial Oil project: 100,000 bbl/day

Order volume: > €300 m

Commissioning: 2012

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

27

Components Technology

Q3 2009/10 Highlights

Comments Q3 (qoq)

Q1 Q2 Q3 Q4 Q1

2008/09

Order intake in €m

Current trading conditions

2009/102008/09

Q1Q2

Q3

Q4

Q1

53 43

EBT in €m

2009/10

(363)

(47) (101)

(21) (76) (104)

EBT adjustedEBT

Q2

63

Q2

1,2901,016 899 972 1,169 1,337

Q3

58

Q3

1,584

105

Further increase in sales and EBT adjusted, mainly driven by demand pick-up in auto supply business and restructuring measures initiated in previous year

Construction equipment and slewing bearings business with increasing order intake for three quarters

Continued restructuring (€47 m in Q3):capacity adjustments at chassis components (Germany) and construction equipment business (Italy)

After strong growth of auto industry (mainly driven by export markets China and USA; recently also positive development also with commercial vehicles) slight slowdown expected

Continued recovery in construction equipment and slewing bearings business

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

28

Heavy

Commercial Vehicles

Automotive Components

Components Technology: Recovery of Order Intake

Passenger Cars/ Light Comm. Vehicles

COMPONENTS TECHNOLOGY

Quarterly

Order Intake

Q4Q3Q2Q1

2008/09

Q3Q2Q1

2009/10

Large-diameter

bearings & rings

Industrial & Construction Machinery

Undercarriages for

tracked/crawler equipm.

Quarterly

Order Intake

Q4Q3

2007/08

Q4Q3Q2Q1

2008/09

Q3Q2Q1

2009/10

Q4Q3

2007/08

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

29

~100

Marine Systems

Q3 2009/10 Highlights

Comments Q3 (qoq)

Q1 Q2

Q3

Q4

Q1

2008/09

Order intake in €m

1,856

193(339)

(840)

Current trading conditions

2009/10

110

2008/09

Q1

Q2 Q3

Q4

Q1

33(10)

EBT in €m

2009/10

(343)

(117) (127)~1,000

~500

Impact of cancellations

(container

ships, mega

yachts,

submarines Greece)

(47) (31) (45) (5)

EBT adjustedEBT

Q2

(7)

8

Q2

139Q3(23)

(4)

Q3

108

Implementation of new target structure (Hamburg site) before closing, corresponding regulatory approval procedures initiated and in part already completed

Negative earnings of Hellenic Shipyards (HSY) adjusted as “special items” due to non-going-concern assumption

Operating losses mainly due to underutilization in shipbuilding, partly compensated by sale of cancelled container ships

Recovery of merchant shipping market leading to pick-up of market for repairs and conversions

Q4 also burdened by underutilization in civil shipbuilding

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

30

Group Performance and Financials

Business Area Performance

Group Outlook

Agenda

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

31

Outlook FY 2009/10 –

Return to Profitability

EBT adjusted

Sales

EBIT adjusted

KPI Updated

Outlook

Mid to higher three-digit

million €

positive,

Slight improvement

> €1 billion,

incl. project costs, startup losses, depreciation and interest expenses of Americas projects (mid-range three-digit million €)

incl. project costs, startup losses and depreciation of Americas

projects

Moderate stabilization

Low three-digit

million €

positive,

High three-digit

million €

positive,

Previous

Outlook

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

32

Expectations Q4 2009/10 –

Business Areas

Steel EuropeGood capacity utilization, higher average selling prices and significantly higher raw material costs

Steel Americas

Negative EBT contribution due to startup losses for the steel and processing plants in Brazil and the USA

Stainless GlobalSlipping volumes, mainly due to seasonal factors, stable end-customer business and slow demand from distributors due to nickel price

Materials Services

Elevator TechnologyContinuing high earnings contributions thanks to high orders in hand and steady maintenance business

Plant Technology

Continuing good revenue and earnings visibility in project business due to order backlog with good earnings quality

Components

TechnologyRecovery in demand for construction equipment, mainly positive earnings from automotive suppliers and continuing positive earnings contribution from slewing bearings for the wind energy sector

Marine Systems

Continuing losses due to underutilization in civil shipbuilding until completion of consolidation of shipyard sites

Slipping volumes, mainly due to seasonal factors, higher flat steel prices and continuing strong demand from the auto and machinery sectors

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

33

The

Way Forward to Sustainable

Value Creation

Liquidity ProfitabilityValue

Creation

TKVA and FCF > 0

Operating cash flow: €3.7 bn

Capex reduction:< €4.3 bn spent

€3 bn bonds issued

Increase of Vale stake in CSA to 26.87% (from 10%) for €965 m

Divestments at Industrial Services

Strong cost control

Realization of sustainable cost savings: €1.5 - €2.0 bn targeted in FY 2010/11

Continued reduction of structural overcapacities

Increased external transparency and benchmarking

Strong cost control

Accelerated startup of Steel Americas and startup of Stainless USA with high degree of flexibility

Focus on FCF generation

Portfolio under review

FY 2009/10 FY 2010/11 et seq.FY 2008/09

Growth Structural Performance

Commerzbank

Sector Conference Week

Frankfurt –

August 26, 2010

Dr. Claus Ehrenbeck, Head

of Investor Relations

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

35

Financial Calendar –

FY 2009/10 and FY 2010/11September Roadshows

Belgium (1st), Frankfurt (8th), The Netherlands (9th), Zurich (28th)ConferencesLBBW “Engineering & Technology Investment Day”, London (2nd)Credit Suisse “Capital Goods and Aerospace Conference”, London (15th)UBS “Best of Germany Conference”, New York (15th and 16th)UniCredit “German Investment Conference”, Munich (22nd)Credit Suisse “Global Steel & Mining Conference”, London (23rd)

November Annual Report FY 2009/10Analysts’ and Investors’ Conference & Annual Press Conference (30th)

February Interim Report 1st Quarter 2010/11 (11th)

May Interim Report 2nd Quarter 2010/11 (13th)

Phone: +49 201 844-536464 E-mail: [email protected]: www.thyssenkrupp.com

New Contact Details as of June 21, 2010:ThyssenKrupp AGThyssenKrupp Allee

145143 Essen -

Germany

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

36

New Contact Details as of June 21, 2010 ThyssenKrupp Corporate Center Investor Relations

NEW phone numbers

+49 201-844-

Dr. Claus Ehrenbeck

-536464

Rainer Hecker

-538830

Head of Investor Relations

Senior IR Manager

Stefanie Bensch

-536480

Christian Schulte

-536966

Assistant

Senior IR Manager

Iris aus

der

Wieschen

-536367

Sabine Berger

-536420

Team assistant

IR Manager

Ute Kaatz

-536466

Klaudia

Kelch

-538371

Event Manager

IR Manager

Tim Lange

-536309

IR Manager

To be added to the IR mailing list, send us a brief e-mail with your details!

E-mail: [email protected]

Developing the future.

Commerzbank Sector Conference WeekAugust 26, 2010

37

Disclaimer ThyssenKrupp AG

“The information set forth and included in this presentation is not provided in connection with an offer or solicitation for the purchase or sale of a security and is intended for informational purposes

only.

This presentation contains forward-looking statements that are subject to risks and uncertainties. Statements contained herein that are not statements of historical fact may be deemed to be forward-looking information. When we use words such as “plan,”

“believe,”

“expect,”

“anticipate,”

“intend,”

“estimate,”

“may”

or similar expressions, we are making forward-looking statements. You should not rely on forward-looking statements because they are subject to a number of assumptions concerning future events, and are subject to a number of uncertainties and other factors, many of which are outside of our control, that could cause actual results to differ

materially from those indicated. These factors include, but are

not limited to, the following:(i) market risks: principally economic price and volume developments, (ii) dependence on performance of major customers and industries, (iii) our level of debt, management of interest rate risk and hedging against commodity price risks;(iv) costs associated with, and regulation relating to, our pension liabilities and healthcare measures, (v) environmental protection and remediation of real estate and associated with rising standards for real estate environmental protection, (vi) volatility of steel prices and dependence on the automotive

industry, (vii) availability of raw materials; (viii) inflation, interest rate levels and fluctuations in exchange rates; (ix) general economic, political and business conditions and existing and future governmental regulation; and (x) the effects of competition. Please note that we disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.”

Top Related