Languages

Pages

Legal

Chapter Four

AN OVERVIEW OF INDIAN CONSUMER DURABLE

INDUSTRY

[61]

CHAPTER-FOUR

AN OVERVIEW OF INDIAN CONSUMER DURABLE

INDUSTRY

The Consumer Durable industry consists of durable goods and appliances for

domestic use such as televisions, refrigerators, air conditioners and washing

machines. Instruments such as kitchen appliances (microwave ovens, grinders etc.)

are also included in this category. This industry includes all those goods which are

durable i.e. products whose life expectancy is at least 3 years. These products are

hard goods that cannot be used up at once. According to recent industry reports, the

steadily growing market for consumer durables is estimated at Rs. 300 billion.

Segmentation of Consumer Durables Industry: The consumer durables

industry can be broadly classified into 2 segments: Consumer Electronics and

Consumer Appliances. Consumer Appliances can be further categorized into Brown

Goods and White Goods. The key Product lines under each segment are as follows:

Flow Chart : 4.1: The Key Product Lines Under Each Segment

Consumer Durables

Consumer Appliances

Consumer Appliances

Others like Watches

Jwellery etc.

Brown Goods Kitchen Appliances

like Microwave Owens, Mixtures etc.

White Goods like Air conditioners,

Refrigerators etc.

Mobile Phones Televisions,

MP3 Players, DVD etc.

[62]

India‟s consumer market is riding the crest of the country‟s economic growth.

Driven by a young population with access to disposable incomes and easy finance

options, the consumer market has been throwing up staggering figures. The Indian

durable market in 2009-10, has grown by 8.6% over the previous year.

India officially classifies its population in five groups, based on annual

household income (based on year 1995-96 indices). The groups are: Lower Income;

three subgroups of Middle Income; and Higher Income. Household income in the top

20 boom cities in India is projected to grow at 10 percent annually over the next

eighth years, which is likely to increase consumer spending on durables. With the

emergence of concepts such as quick and easy loan, zero equated monthly

installment (EMI) charges, loan through credit card, loan over phone, it has become

easy for Indian consumers to afford more expensive consumer goods.

Table # 4.1: Segment-Wise Percentage Share Of Indian Durables Household

Industry

Segments Percentage

Air Conditioners 6%

Audio/Video Equipments 12%

Components 7%

Computer And Peripherals 19%

Electric Fans 1%

Industrial Electrical And Electronics 5%

Mobile Phones 20%

Other Domestic Appliances 4%

Others 3%

Refrigerators 2%

Sewing Machines 1%

Telecommunication 18%

Washing Machines 1%

Watches And Clocks 1%

As mentioned in Table 4.1 share of mobile phones segments is highest (20%) and the

lowest share of watches and clocks.

[63]

6

12

7

19

1

5

20

4

3

2

1

18

1 1

0

5

10

15

20

25

Air

Co

nd

itio

ners

Au

dio

/Vid

eo

Eq

uip

men

ts

Co

mp

on

en

ts

Co

mp

ute

r A

nd

Peri

ph

era

ls

Ele

ctr

ic F

an

s

Ind

ustr

ial

Ele

ctr

ical

An

d E

lectr

on

ics

Mo

bil

e P

ho

nes

Oth

er

Do

mesti

c

Ap

pli

an

ces

Oth

ers

Refr

igera

tors

Sew

ing

Mach

ines

Tele

co

mm

un

icati

on

Wash

ing

Mach

ines

Watc

hes A

nd

Clo

cks

Perc

en

tag

e

Figure # 4.1: Segment-Wise Percentage Share Of Indian Durables Household

Industry

CONSUMER CLASSES

Even discounting the purchase power parity factor, income classifications do

not serve as an effective indicator of ownership and consumption trends in the

economy. Accordingly, the National Council for Applied Economic Research

(NCAER), India‟s premier economic research institution, has released an alternative

classification system based on consumption indicators, which is more relevant for

ascertaining consumption patterns of various classes of goods.

There are five classes of consumer households, ranging from the destitute to

the highly affluent, which differ considerably in their consumption behaviour and

ownership patterns across various categories of goods. These classes exist in urban

as well as rural households both, and consumption trends may differ significantly

between similar income households in urban and rural areas.

[64]

The rapid economic growth is increasing and enhancing employment and

business opportunities and in turn increasing disposable income. Middle class,

defined as household with disposable incomes from Rs. 2 00 000 to 10,00,000 a year

comprises about 50 million people, roughly 5% of the population at present. By 2025

the size of middle class will increase to about 583 million people, or 41% of the

population. Extreme rural poverty has declined from 94% in 1985 to 61% in 2005

and is projected to drop to 26% by 2025.

Affluent class, defined as earning above Rs. 10,00,000 a year will increase

from 0.2% of the population at present to 2% of the population by 2025. Affluent

class‟s share of national private consumption will increase from 7% at present to

20% in 2025.

Flowchart 4.2: Porter’s Five Forces Model and Consumer Durable Industry

Buyer Power: The buyer‟s power is quite high as they have multiple brands across

different price points, hence giving them a wide variety cross both durable and non-

durable products to choose from.

Supplier Power: the suppliers‟ power is low because of the availability of the large

numbers of suppliers in the domestic market and cheap import options for

components from other suppliers and countries.

Availability of Substitutes:

Low to Medium

Supplier Power: Low

Buyer Power: High

Threat of New Entrants: Medium

Competitive Rivalry : High

[65]

Competitive Rivalry: Presence of a large number of players in the domestic

consumer durable market in each segment leads to high rivalry.

Availability of Substitutes: The threat of availability of substitutes in the Indian

Consumer Durables market is medium. Where the white goods segment (air

conditioners, refrigerators) face low threat of substitutes, the brown goods segment

and consumer electronics segment do face a threat of substitutes. As new technology

enters the market at an increasing pace, the manufacturers need to upgrade their

products accordingly. For e.g. the VCR got replaced by DVD player. On a different

note, televisions face the threat of multiplexes. Also, brown goods like pressure

cookers face the threat of microwave ovens etc.

Threat of new entrant: For any new company, to establish and build a new brand,

cope with the technological advancement and create a wide-distribution network is

difficult. One the other hand, cheaper brands from Asian countries like china and the

entry of other global brands is a concern.

OVERVIEW OF INDIA’S CONSUMER DURABLE MARKET

The Indian consumer durables segment can be segregated into 2 consumer

electronics groups:

Table 4.2(a): Segment-Wise Consumer Durables

White goods Consumer electronics

Air conditioners Televisions

Refrigerator Audio and video systems

Washing machines Electronics accessories

Sewing machines PCs

Electric fans Mobile phones

Watches and clocks Digital cameras

Cleaning equipments DVDs

Microwave ovens Camcorders

Other domestic appliances

[66]

Most of the segments in this sector are characterized by intense competition,

emergence of new companies (especially MNCs) and introduction of state-of-the-art

models, price discounts and exchange schemes. MNCs continue to dominate the

Indian consumer durable segment, which is apparent from the fact that these

companies command more than 65 percent market share in the colour television

(CTV) segment.

In consonance with the global trend, over the years, demand for consumer

durables has increased with rising income levels, double-income families,

changing lifestyles, availability of credit, increasing consumer awareness and

introduction of new models, products like air conditioners are no longer perceived

as luxury products.

Table 4.2(b): Net Profit Margin (NPM) and Compound Annual Growth Rates

Company

Name What is it into?

Net Sales (Rs. Cr.) Net Profit (Rs. Cr.) 6-yr Avg

NPM 2005 2010 CAGR 2005 2010 CAGR

Titan Watches & Jewelry 1113 4776 34% 54 253 36% 6%

Blue star White Goods 917 2525 22% 12 203 42% 5%

Whirlpool* White Goods 1476 2544 20% 13 150 126% 4%

Videocon* Consumer Electronics 7219 9163 8% 820 408 (21)% 8%

MIRC Electronics Consumer Electronics 1088 1502 7% 28 18 (8)% 2%

Bajaj electrical Brown goods 642 2229 28% 14 118 53% 4%

TTK Prestige Brown Goods 181 508 23% 3 52 74% 5%

* 6 year assessable data is not available, hence a 3-year CAGR is calculated

Titan, the market leader in watches and branded jewelry, has clocked the

highest Net Sales CAGR of 34% over the last 6 years. It has the competitive

advantage of a strong brand, which has helped it become the market leader. Titan has

successfully captured the watch and jewelry market. It has also managed to maintain

& NPM of 6%.

[67]

FACTORS AFFECTING DURABLE CONSUMER GOODS INDUSTRY

IN INDIA

The following factors are affecting Indian durable consumer goods industry

in India:

1) Rise in Disposable Income

The demand for consumer durables has been rising with the increase in

disposable income coupled with more and more consumers falling under the double

income families. Also, growing Indian middle-class plays a major role in increasing

the demand. This, along with a fall in the prices of durable goods mainly due to the

advancement of technology, easy import of components has led to an increase in the

consumption expenditure on durable goods.

2) Easy-Availability of Consumer Financing

Apart from steady growth in income of consumers, consumer financing has

become a major driver in the consumer durables industry. In the case of more

expensive consumer goods, such as refrigerators, washing machines, color

televisions and personal computers, retailers are marketing their goods more

aggressively by providing easy financing options to the consumers by partnering

with banks. The easy-availability of consumer financing is beneficial mainly for the

lower and middle income group, especially when the cost of capital and flexibility of

the scheme is in their favour.

3) Existing Potential in Rural Markets

Growth is coming in a big way from the smaller towns and rural markets and

is expected to be the next growth opportunity for the consumer durables market. In

the last year 30-35% of the total sale of consumer durable was from the rural

market. This is expected to grow by 40-45% in the near future. The rural durables

market has been growing by 30% annually, mainly due to the growing affordability

of products as well as the general buoyancy in the economy. Products like mobile

[68]

phones, televisions and music systems are the ones which have witnessed high

growth among the rural market. To further cater to this market are manufacturers

have started using local languages while offering products to the rural crowd.

Some initiatives taken by Top Consumer Durables Companies to tap

rural markets:

Videocon recently launched a mobile with basic characteristics and a long-

battery life. This was mainly done to tap the rural markets where electricity is

an issue.

Bajaj Electrical is in the process of finalizing a special team for each of its

product, specifically to tap the rural market.

4) Increasing Share of Organised Retail

Since the last couple of years there has been an increasing shift towards

organized retail (brands) from the unorganized (unbranded) products. With rising

income and purchasing power, and the younger generation preferring branded

products, the share of organized shopping is increasing. Shopping in malls is

considered more of an experience these days. According to estimates, organized

retail which constituted 4% of the total buying till 2010 is expected to grow to over

10% by 2013.

5) Entertainment and Media to Boost Growth

According to a recent report by KPMG, the Indian Media & Entertainment

(M&E) industry registered a growth of 11% over 2009 and touched Rs. 652 billion

and is expected to achieve a 13% growth in 2011. Overall the industry is expected to

register a CAGR of 14% to touch Rs. 1275 billion by 2015. Out of this, the television

industry is expected to achieve a 16% CAGR and is expected to account for almost

half of the Indian M&E industry revenues. The television segment of the consumer

durables industry is seeing high growth coming form high-end flat panel TV, LCD

[69]

TVs and Plasma TVs. All of these were expected to register a 100%+growth in the last

year. Hence, the growing importance of entertainment and media on our lifestyles is

expected to boost the demand for products like Plasma TVs, LCDs DVD players.

6) Consumer Preferences

Consumers purchase goods by looking at the brand, pricing, and discount

schemes available at the time of buying. So, for the consumer durables industry

following are important growth drivers:

Availability of new and innovative products – A company that upgrades its

technology and comes out with new and innovative products catches the

attention of consumers. Especially in the consumer electronics segment,

manufacturers have to make sure they are updated with the latest technology

that has entered the market. For the higher income groups the brand,

technology and the product features play an important role.

Pricing of the products – For the lower and middle income groups, price is

the deciding factor especially in a price-sensitive industry like consumer

durables.

Festive discount schemes – The sales of many consumer durables goods are

driven by festive discounts. For example people consider it auspicious to

purchase goods like LCDs, Televisions, Washing machines, etc during

festivals like Diwali, Gudi Padwa, etc.

1) Cheap imports form Asian Countries: The cheap imports of consumer durable

products from countries like China, Singapore etc are a major concern.

2) Increasing competition: Presence of a large number of players in each segment

leads to high rivalry. Also, the unorganized market is yet very strong in the case of

many consumer durable goods. The pie of the unorganized sector is relatively large

in most of the segments, hence increasing the competition.

[70]

3) Fluctuating raw material prices: Rising input costs of raw materials viz. copper,

steel, aluminum and plastic – the major raw materials required for this industry will

severely put pressures on margins.

4) Unfavorable duty Structure: Top players in the consumer durables industry

have been demanding a more favorable import duty on durable components imported

by them. Take the case of LCD‟s which is the fastest growing segment is right now –

the industry has been demanding a reduction in the import duty. Contrary to this is

the case of set top boxes, where 80% of the set top boxes are imported. The industry

has been recommending that the custom duty on STB should be increased by 5% to

10% in order to boost domestic manufacturing.

5) Continuously changing technology; a challenge: The consumer durable sector

faces the challenge of a continuous change in technology and the inability to cope

with it. High-end consumers prefer changing their goods along with the up-gradation

of technology and manufacturers have to make sure they cater to this requirement.

The Indian market is fast moving towards high-end products and the

importance of media and entertainment is growing among the young market. The

consumer durables industry needs to constantly focus on innovation and needs to

come out with product variations across categories to meet the different expectations

of a varied class of customers.

With easy availability of finance, fall in prices due to increased competition,

growth of media, growth in consumer base of rural sector, the consumer durables

industry is growing at a fast pace. Given these factors, a goods growth is projected in

the future too.

With the Indian Economy expected to grow at 7-8%, the existing potential in

the durables market augurs well for the consumer durables industry. Hence, we can

say that the consumer durables sector is expected to grow with a good growth rate

and have a bright future.

[71]

GROWTH OF CONSUMER ELECTRONICS PRODUCTION IN INDIA

The biggest attraction for MNCs is the growing Indian middle class. This

market is characterized with low penetration levels. MNCs hold an edge over their

Indian counterparts in terms of superior technology combined with a steady flow of

capital, while domestic companies compete on the basis of their well-

acknowledged brands, an extensive distribution network and an insight in local

market conditions.

One of the critical factors those influences durable demand is the government

spending on infrastructure, especially the rural electrification programme. Given the

government's inclination to cut back spending, rural electrification programmes have

always lagged behind schedule. This has not favoured durable companies till now.

Any incremental spending in infrastructure and electrification programmes could

spur growth of the industry.

The digital revolution is shaking up the consumer durables industry. With the

advent of MP3 music files, personal video recorders, game machines, digital

cameras, appliances with embedded devices, and a host of other media and services,

it is no longer clear who controls which part of home entertainment. This has set off

a battle for dominance, and the shakeup is spanning the entire technology spectrum.

Microsoft Corporation is spending billions on entertainment initiatives such

as its Xbox video game console. Compaq and HP sell MP3 music players that plug

into home-stereo systems. Apple Computer is positioning its new iMac as a digital-

entertainment device. Sony is building Vaio computers that focus on integrating

multimedia applications.

Philips sells stereos that hook into a high-speed Internet connection to play

music from the Web. More startups are trying to carve out profitable niches in digital

music, video, and home networking. The industry is witnessing a number of strategic

alliances, to develop a range of capabilities - electronic hardware, software, and

entertainment content.

[72]

As more consumers grow comfortable with technology, companies need to

build simpler devices that offer more entertainment and convenience. These new

machines need to work together readily, and should be as easy to set up and use as a

telephone or a television. Consumerization of technology could be a major

phenomenon over the next 5 to 10 years. This could hasten industry consolidation, as

healthy companies gain market share by buying out weaker ones at attractive prices.

Apart from steady income gains, consumer financing has become a major

driver in the consumer durables industry. In the case of more expensive consumer

goods, such as refrigerators, washing machines, color televisions and personal

computers, retailers are joining forces with banks and finance companies to market

their goods more aggressively. Among department stores, other factors that will

support rising sales include a strong emphasis on retail technology, loyalty schemes,

private labels and the subletting of floor space in larger stores to smaller retailers

selling a variety of products and services, such as music and coffee.

Figure 4.2: Consumer Electronics – Products

Rising disposable income and declining prices of durables have resulted in

increased volumes. An increase in disposable income is aided by an increase in the

number of both double-income and nuclear families. Production in the consumer

Colour TV

(CTV)

CTV is the largest contributor in this segment and the market has been estimated

at 15.15 million units in 2009-2010.

Liquid crystal

display (LCD)

LCDs are perceived as high-end products.

The LCD market has been estimated at 0.8 million units, registering a growth of

over 130 percent during 2008-09 over the previous year.

Digital video

disc (DVD)

Indian DVD market was estimated at 6.2 million units in 2009.

Direct-to-

home

(DTH)

Due to the expansion of DTH and introduction of conditional access system (CAS)

in the metros, the set top box (STB) market is growing rapidly.

Multimedia

mobile phones

Multimedia mobile phones have been growing at a fast rate, from 800,000 units in

2008-09 to 1.8 million units in 2009-2010.

[73]

8867

9436

10029

10655

11204

11795

693

789

894

1026

1178

1352

4230

4626

5048

5505

5996

6542

121

121

125

127

128

129

0

2000

4000

6000

8000

10000

12000

14000

2005 2006 2007 2008 2009 2010

'000 u

nit

s

Television Sets Personal Computers Refrigerators Video Recorders

`

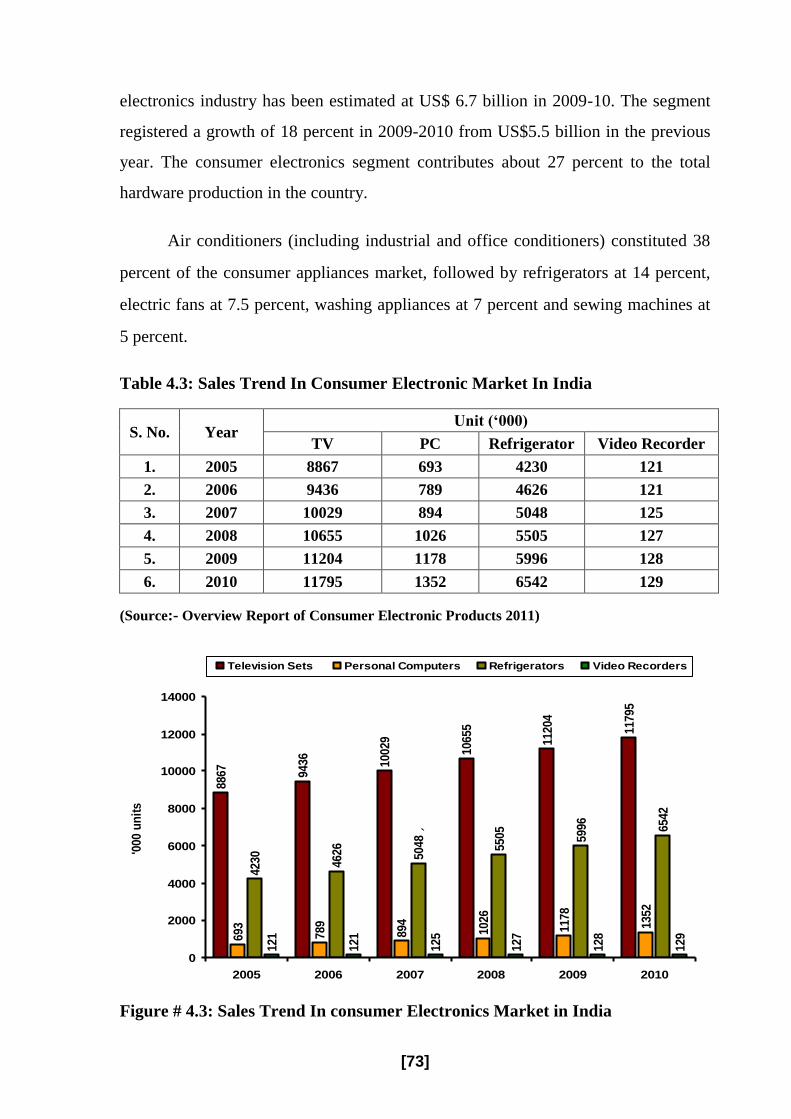

electronics industry has been estimated at US$ 6.7 billion in 2009-10. The segment

registered a growth of 18 percent in 2009-2010 from US$5.5 billion in the previous

year. The consumer electronics segment contributes about 27 percent to the total

hardware production in the country.

Air conditioners (including industrial and office conditioners) constituted 38

percent of the consumer appliances market, followed by refrigerators at 14 percent,

electric fans at 7.5 percent, washing appliances at 7 percent and sewing machines at

5 percent.

Table 4.3: Sales Trend In Consumer Electronic Market In India

S. No. Year Unit (‘000)

TV PC Refrigerator Video Recorder

1. 2005 8867 693 4230 121

2. 2006 9436 789 4626 121

3. 2007 10029 894 5048 125

4. 2008 10655 1026 5505 127

5. 2009 11204 1178 5996 128

6. 2010 11795 1352 6542 129

(Source:- Overview Report of Consumer Electronic Products 2011)

Figure # 4.3: Sales Trend In consumer Electronics Market in India

[74]

Consumer durables are expected to grow at 10-15 percent in 2007-08, driven

by the growth in CTV‟s and air conditioners. Value growth of durable is expected to

be higher than historical levels as price declines for most of the products are not

expected to be very significant. Though price declines will continue, it will cease to

be the primary demand driver. Instead the continuing strength of income

demographic will support volume growth.

Table # 4.4: Compound Annual Growth Rates (CAGR) Of Different Segment

Categories in India (2008)

S.

No. Product Name

2007-2008 Over 2005-2006

% Growth Driver

1. Air Conditioner 20-22* Decreasing Prices, changing lifestyle

2. Refrigerator 5-8 High Demand for the frost free segment together

with reduction in prices

3. Colour Televisions 5-8 Increasing disposable income and declining prices

4. Washing Machines 8-10* Reduction in prices of fully automatic machines

Source:- Computed *Significant at 5% level

Table # 4.5: Compound Annual Growth Rate (CAGR) Of Different Segment

Categories in India (2010)

S.No. Product Name 2008-2009 Over 2009-2010

% Growth Driver

1. Air Conditioner 30-40* Reduction in Prices

2. Refrigerator 24

Low penetration level in the country

and increase in demand from the

rural and semi urban areas

3. Colour Televisions 30-40 Reduction in Prices of LCD, LED

4. Washing Machines 30* New Models launched and reduction

in prices

Source:- Computed *Significant at 5% level

[75]

COMPETITION OVERVIEW

Samsung India

Samsung India commenced its operations in India in December 1995, today

enjoys a sales turnover of over US$ 1 billion in just a decade of operations in the

country. Samsung design centers are located in London, Los Angeles, San Francisco,

Tokyo, Shanghai and Rome. Samsung India has its headquartered in New Delhi and

has a network of 19 Branch Offices located all over the country.

The Samsung manufacturing complex housing manufacturing facilities for

Colour Televisions, Colour Monitors, Refrigerators, and Washing Machines is

located at Noida, near Delhi. Samsung „Made in India‟ products like Color

Televisions, Color Monitors, and Refrigerators are being exported to Middle East,

CIS, and SAARC countries from its Noida manufacturing complex. Samsung India

currently employs over 1600 employees, with around 18% of its employees working

in Research & Development.

Table 4.6: Market Share Of Major Players In Refrigerator Market

S.No. Players Turnover (Rs. Billion)

1. Godrej 12.05

2. Hair 1.85

3. LG 21.00

4. Whirlpool 15.11

5. Videocon 11.23

Source:- Consumer Electronics and Appliances Manufacturers Association (CEAMA)

[76]

12.05

1.85

21.00

15.11

11.23

0

5

10

15

20

25

Godrej Haier LG Whirlpool Videocon

Tu

rno

ver

2009-2

010 (

Rs B

illi

on

)

Figure # 4.6: Market Share Of Major Players In Refrigerator Market

Whirlpool of India

Whirlpool was established in 1911 as first commercial manufacturer of

motorized washers to the current market position of being world's number one

manufacturer and marketer of major home appliances. The parent company is

headquartered at Benton Harbor, Michigan, USA with a global presence in over 170

countries and manufacturing operation in 13 countries with 11 major brand names

such as Whirlpool, Kitchen Aid, Roper, Estate, Bauknecht, Laden, and Ignis. Today,

Whirlpool is the most recognized brand in home appliances in India and holds a

market share of over 25%. The company owns three state-of-the-art manufacturing

facilities at Faridabad, Pondicherry, and Pune.

In the year ending in March '06, the annual turnover of the company for its

Indian enterprise was Rs.13.75 billion. According to IMRB surveys Whirlpool

enjoys the status of the single largest refrigerator and second largest washing

machine brand in India.

[77]

123

318

620

17.2

340

1258 1215

2000

181

1060

13811533

2620

198.2

1400

0

500

1000

1500

2000

2500

3000

Videocon Whirlpool LG Haier Godrej

Frost-Free Direct-Cool Total

LG India

LG Electronics was established on October 1, 1958 (As a private Company)

and in 1959, LGE started manufacturing radios, operating 77 subsidiaries around the

world with over 72,000 employees worldwide it is one of the major giants in the

consumer durable domain worldwide. The company has as many as 27 R & D

centers and 5 design centers. Its global leading products include residential air

conditioners, DVD players, CDMA handsets, home theatre systems, and optical

storage systems.

Table # 4.7: Category-Wise Sales of Major Players

S.No. Players Frost Free Direct Cool Total

1. Videocon 123 1258 1381

2. Whirlpool 318 1215 1533

3. LG 620 2000 2620

4. Haier 17.20 181.00 198.20

5. Godrej 340 1060 1400

Figure # 4.7: Category Wise Sales Of Major Players

[78]

2634 33

27 26

15

14 17

16 16

17

1414

13 14

1514 13

16 16

76 5

7 6

20 15 18 21 22

0

10

20

30

40

50

60

70

80

90

100

2003-2004 2004-2005 2005-2006 2006-2007 2007-2008

Perc

en

tag

e

Others

Godrej

Whirlpool

Videocon

Samsung

LG

Table # 4.8: Market Share of Washing Machines in India

S.

No. Year

Market share

LG Samsung Videocon Whirlpool Godrej Others

1. 2003-04 26 15 17 15 7 20

2. 2004-05 34 14 14 14 6 15

3. 2005-06 33 17 14 13 5 18

4. 2006-07 27 16 13 16 7 21

5. 2007-08 26 16 14 16 6 22

(Sources : CRISIL)

Figure # 4.8: Market Share of Washing Machines In India

[79]

Godrej India

Godrej India was established in 1897, the Company was incorporated with

limited liability on March 3, 1932, under the Indian Companies Act, 1913. The

Company is one of the largest privately-held diversified industrial corporations in

India. The combined Sales during the Fiscal Year ended March 31, 2006, amounted

to about Rs. 58,000 million (US$ 1,270 million). The company has a network of 38

company-owned retail stores, more than 2,200 wholesale dealers, and more than

18,000 retail outlets. The company has representative office in Sharjah (UAE),

Nairobi (Kenya), Colombo (Sri Lanka), Riyadh (Saudi Arabia) and Guangzhou

(China_PRC).

Toshiba India

Toshiba India Private Limited (TIPL) is the wholly owned subsidiary of

Japanese Electronic giant Toshiba Corporation and was incorporated in India on

September 2001). Toshiba had a presence in India since 1985 and was represented in

India through their Liaison Office.

Sony India

Sony Corporation, Japan, established its India operations in November 1994.

In India, Sony has its distribution network comprising of over 7000 channel partners,

215 Sony World and Sony Exclusive outlets, and 21 direct branch locations. The

company also has presence across the country with 21 company owned and 172

authorized service centers.

[80]

210

230245 240

215

250

0

50

100

150

200

250

300

2000 2008 2010 2011 2012 2013

Ho

useh

old

(In

Mil

lio

n)

Table 4.9: Television Penetration Level (2013)

S. No. Year Penetration

(Household in Billion)

1. 2000 210

2. 2008 230

3. 2010 245

4. 2011 240

5. 2012 215

6. 2013 250

Figure # 4.9: Market Share of Television Penetration Level in India

[81]

Table # 4.10: Market Share of T.V. Sets in India (2007-08)

S. No. Year Market share

LG Videocon Samsung MIRC Others

1. 2003-04 26 15 17 15 20

2. 2004-05 34 14 14 14 15

3. 2005-06 33 17 14 13 18

4. 2006-07 27 16 13 16 21

5. 2007-08 26 16 14 16 22

(Note: Others = Sony, Haier, TCL, Philips, Hitachi, Sharp)

Figure # 4.10: Market Share of T.V. Sets in India (2007-08)

[82]

Sharp India Ltd

Sharp India ltd was incorporated in 1985 as Kalyani Telecommunications and

Electronics Pvt. Ltd., the company was converted into a public limited company in

the same year. The name was changed to Kalyani Sharp India in 1986. The company

was entered into a joint venture with Sharp Corporation, Japan - a leading

manufacturer of consumer electronic products to manufacture VCRs/VCPs/VTDMs.

The company manufactures consumer electronic goods such as TVs, VCRs, VCPs,

and audio products. The products were sold under the Optonica brand name. Sharp

has a production base in 26 countries with 33 plants, and its products are used in 133

countries. The company was accredited with the ISO-9001 certification in the month

of February, 2001.

Hitachi India

Hitachi India Ltd (HIL) was established in June 1998 and engaged in

marketing and sells a wide range of products ranging from Power and Industrial

Systems, Industrial Components & Equipment, Air Conditioning & Refrigeration

Equipment to International Procurement of software, materials, and components.

Some of HIL‟s product range includes Semiconductors and Display Components. It

also supports the sale of Plasma TVs, LCD TVs, LCD Projectors, Smart Boards, and

DVD Camcorders.

POLICY AND INITIATIVES

Foreign investment up to 100 per cent is possible in the Indian consumer

electronics industry to set up units exclusively for exports. It is now possible to import

duty-free all components and raw materials, manufacture products and export it.

EHTP (Electronic Hardware Technology Park) is an initiative to provide

benefits to companies that are replacing certain imports with local manufacturing.

EHTP benefits include export credits, no duties on imported components or capital

equipment, business tax incentives, and an expedited import-export process.

[83]

The government, in an attempt to encourage manufacture of electronics in

India has changed the tariff structure significantly.

Customs duty on Information Technology Agreement (ITA-1) items (217

items) has been abolished from March 2005. All goods required in the manufacture

of ITA-1 items are exempt from customs duty.

Customs duty on specified raw materials / inputs used for manufacture of

electronic components or optical fibers / cables has been removed. Customs duty on

specified capital goods used for manufacture of electronic goods has been abolished.

Excise duty on computers has been removed. Microprocessors, hard disc drives,

floppy disc drives and CD ROM drives continue to be exempt from excise duty.

INTELLECTUAL PROPERTY RIGHTS

Protection of Intellectual property rights (IPR) is a prime requisite for

development of R&D and innovation in the consumer electronics sector. The

Government of India has developed a robust IP act to facilitate innovation, growth

and development. Several amendments to the Copyright Act, creation of a new

Trademark Act, a new Designs Act and amendments to the Patents Act show India‟s

continued effort to protect IPR.

The country has already made several changes in its IP acts over the years.

Several amendments to the Copyright Act, creation of a new Trademark Act, a new

Designs Act and amendments to the Patents Act show India‟s desire to change and

adapt. New acts have also been enacted to cover semiconductors and layout designs

which will be of considerable importance to the electronic industry.

In the current WTO regime, India is a party to the “Trade Related Aspects of

the Intellectual Properties (TRIPs) Agreement” and has accordingly, amended most

of its IPR Acts and Rules to conform to the said Agreement. The Indian Copyright

Act 1957 was amended in 1999; the patent Act 1970 was amended in 1999 & 2003

[84]

and Trademarks and Merchandise Marks Act 1959 was overtaken by a new

Trademark Act 1999. The Industrial Design Act 1911 was effectively replaced by

The Design Act 2000, and the Layout Design of Semiconductor integrated Circuit

Act 2000 was enacted.

The agreement on TRIPs takes care of the intellectual property rights by

enforcing the patent rights, copy rights and related rights, and the protection of

industrial designs, trademarks, geographical indications, layout designs of integrated

circuits and undisclosed information. Accordingly, the member nations are asked to

modify their existing laws. Once these laws come into force, unauthorized use of the

patented innovations, trademarks, etc. becomes difficult. Enforcement of the TRIPs

agreement makes the production of any product possible either through internal

innovation or through formal transfer of technologies.

The consumer electronics and durables sector is expected to continue to

benefit from supportive policies and become globally competitive.

REGULATIONS

Free Trade Agreement

WTO regime which came in force in 2005, results in zero customs duty on

imports of all telecom equipment. 217 IT/electronic items were covered under the

Information Technology Agreement (ITA) of the WTO for complete customs tariff

elimination by 2005.

Out of these 217 items, several items were already at NIL customs duty. In

fact, IT/electronics was the first sector in India to face complete customs tariff

elimination. The ITA-1 would result in intensifying competition as more imported

products will be easily available at lower prices.

[85]

Foreign Investment Policy: FDI

Foreign investment up to 100 per cent is allowed in Indian electronics

industry set up exclusively for exports. The units set up under these programmes are

bonded factories eligible to import, free of duty, their entire requirements of capital

goods, raw materials and components, spares and consumables, office equipment etc.

Deemed export benefits are available to suppliers of these goods from the Domestic

Tariff Area (DTA).

A part of the production from such units is permitted to be sold in the DTA

depending upon the level of the value addition achieved. The FDI approval for electrical

equipment (including computer software and electronics) from April 2000 to January

2010 was US$ 21.24 billion, which was 2.01 per cent of the total Foreign Direct

Investment (FDI) approved. During the same period the FDI inflow for electrical

equipment (including computer software and electronics) was US$ 96.30 billion.

Procedure for Approval

Once the investment in equity has been approved, the import of capital goods,

components and raw materials or the engagement of foreign technicians for short

duration does not require any additional approvals.

Approval of Ministry of Home Affairs is not needed for hiring foreign

nationals holding valid employment visa.

Approval for setting up units in Export Processing Zones (EPZs) is given by

the Board of Approvals in the Ministry of Commerce. Approval for setting up

export-oriented units (EOUs) outside the zones is given by the Ministry of Industry.

Approvals for setting up Electronic Hardware Technology Park (EHTP) and

Software Technology Park (STP) units are cleared by the Inter Ministerial Standing

Committee (IMSC) set-up under the Chairmanship of the Secretary, Department of

Information Technology.

[86]

Proposals involving foreign direct investment not covered under the

automatic route are considered by the Foreign Investment Promotion Board (FIPB).

FDI/ Foreign Technology Collaboration Agreement

The government facilitates FDI and investment from Non- Resident Indians

(NRIs) including Overseas Corporate Bodies (OCBs), predominantly owned by

them, to complement and supplement domestic investment. Foreign technology

induction is encouraged through FDI and foreign technology collaboration

agreements. FDI and foreign technology collaborations are approved through

automatic route by the Reserve Bank of India.

CHALLENGES AND OPPORTUNITIES

Challenges

Heavy taxation in the country is one of the challenges for the players. At its

present structure the total tax incidence in India even now stands at around 25-30 per

cent, whereas the corresponding tariffs in other Asian countries are between 7 and 17

per cent.

About 65 per cent of Indian population that lives in its villages still remains

relevant for some consumer durables companies. This India, at least a large

proportion of its constituents, still buys black and white TVs and doesn't know

what flat screens are. The rural market has a considerable cost component attached

to it.

Companies not only have to set up the basic infrastructure in terms of office

space, manpower, but also spend on transportation for moving inventory. Even LG

and Samsung, which are having the largest distribution network in the country, have

a direct presence only in 15,000 to 18,000 of the around 40,000 retail outlets (for

consumer durables) in the country.

[87]

Poor infrastructure is another reason that seems to have held back the

industry. Regular power supply is imperative for any consumer electronics product.

But that remains a major hiccup in India.

Opportunities

The rising rate of growth of GDP, rising purchasing power of people with

higher propensity to consume with preference for sophisticated brands would

provide constant impetus to growth of white goods industry segment.

Penetration of consumer durables would be deeper in rural India if banks and

financial institutions come out with liberal incentive schemes for the white goods

industry segment, growth in disposable income, improving lifestyles, power

availability, low running cost, and rise in temperatures.

While the consumer durables market is facing a slowdown due to saturation in

the urban market, rural consumers should be provided with easily payable consumer

finance schemes and basic services, after sales services to suit the infrastructure and

the existing amenities like electricity, voltage etc.

Currently, rural consumers purchase their durables from the nearest towns,

leading to increased expenses due to transportation. Purchase necessarily done only

during the harvest, festive and wedding seasons – April to June and October to

November in North India and October to February in the South, believed to be

months `good for buying‟, should be converted to routine regular feature from the

seasonal character.

Rural India that accounts for nearly 70% of the total number of households,

has a 2% penetration in case of refrigerators and 0.5% for washing machines, offers

plenty of scope and opportunities for the white goods industry. The urban consumer

durable market for products including TV is growing annually by 7 to 10 % whereas

the rural market is zooming ahead at around 25 % annually. According to survey

[88]

made by industry, the rural market is growing faster than the urban India now. The

urban market is a replacement and up gradation market now.

The increasing popularity of easily available consumer loans and the

expansion of hire purchase schemes will give a moral boost to the price-sensitive

consumers. The attractive schemes of financial institutions and commercial banks

are increasingly becoming suitable for the consumer. Consumer goods companies

are themselves coming out with attractive financing schemes to consumers through

their extensive dealer network. This has a direct bearing on future demand.

The other factor for surging demand for consumer goods is the phenomenal

growth of media in India. The flurry of television channels and the rising penetration

of cinemas will continue to spread awareness of products in the remotest of markets.

The vigorous marketing efforts being made by the domestic majors will help

the industry. The Internet now used by the market functionaries that will lead to

intelligence sales of the products. It will help to sustain the demand boom witnessed

recently in this sector. The ability of imports to compete is set to rise. However, the

effective duty protection is still quite high at about 35-40 per cent. So, a flood of

imports is unlikely and would be rather need based.

Reduction in import duties may significantly lower prices of products such as

microwave ovens, whose market size is quite small in India. Otherwise, local

manufacturing will continue to stay competitive. At the same time, there will be

some positive benefits in the form of reduction in input costs. Washing machines and

refrigerators will also benefit from lower input costs.

Top Related