Languages

Pages

Legal

Copperbelt Energy Corporation Plc

H1 Results Presentationfor the period ended 30 June 2016

www.cecinvestor.com

Contents

Page

Zambia review 5Economic 6Operational & regulatory 7

Nigeria review 8Economic 9Operational 10

Health, Safety, Environment & Social 12

Financial results 13

CEC Group trend analysis 14

CEC Group profit & loss 15

Group financial position 16

Zambian financial results 17CEC Plc 18CEC Plc financial snap shot 19Telecoms 20

Nigerian Operations 21AEDC Plc and NSP 22 – 23

Financial Comparison – Zambia / Nigeria 24

Outlook & strategy 28

www.cecinvestor.com 1

Your presenters

www.cecinvestor.com 2

Owen SilavweManaging Director

Mutale MukukaChief Financial Officer

Statements in this presentation (including all other media) that are not historical facts or

information may be forward-looking statements.

These forward-looking statements are based on information available at the time the

statements are made and/or management's belief as of that time with respect to

future events and involve risks and uncertainties that could cause actual results and

outcomes to be materially different. Important factors that could cause such

differences include, but are not limited to the loss of key customers, the disruption to

operations, economic conditions, political conditions, regulatory issues and reduction in

demand.

Forward looking statements

3

CEC Group structure

www.cecinvestor.com 4

KANN Utility

SPV

Shiroro Hydro (NG)

CECA SL Generation

SPV

Abuja DiscoGeneration Project

CEC Africa

CEC Plc

Zambian Energy Corp

Ireland (ZECI)ZCCM – IH

Institutional & Retail

Investors

75%

60%

100%

50.1%

100%

100%

20%52% 28%

Nigeria Mauritius

Sierra Leone

Projects in developmentOperating assets

Key:

North South Power

20%

CEC Liquid Telecom

Hai Telecoms

Kabompo Hydro50%

100%

100%

CEC Africa Hydro

100%

Investment assets

Zambian Operations

Nigerian Operations

CEC Group

ZAMBIA

Summary Economic & Business

Overview

www.cecinvestor.com 5

Overview: Zambian operations & regulation

Operations & Operating Environment

– The business has continued to operate under the partial force majeure, accessing only 70%

of the power requirements under the Bulk Supply Agreement (BSA). Balance of supplies is

being met from supplies from SAPP

– Power supplies to the other customer categories was not materially impacted. Therefore,

domestic wheeling was on budget

– International power trading continues to be one of the key focus areas for the business,

increasing by 254% compared to the same period last year and is making up for the loss of

sales in Zambia

– Telecoms unit, CEC Liquid Telecom, has continued to be profitable on account of

increased customer acquisition, backed by more fibre build and services roll out

Environment & Regulation

– Low commodity prices for copper have led to some of the Company’s mine customers

scaling back on operations, leading to a drop in local power sales by 16%

– The new tariff of USc 10.35 kWh, passed by government, has been implemented effective 1

Jan 2016 though few customers are paying at the increased tariff

– The 2014 ERB tariff increase remains disputed and the matter is still in the courts of law

www.cecinvestor.com 7

CEC Group

NIGERIA

Summary Economic & Business

Overview

www.cecinvestor.com 8

4%

6%

8%

10%

12%

14%

20

11

20

12

20

13

20

14

20

15

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

Nigerian inflation (%)

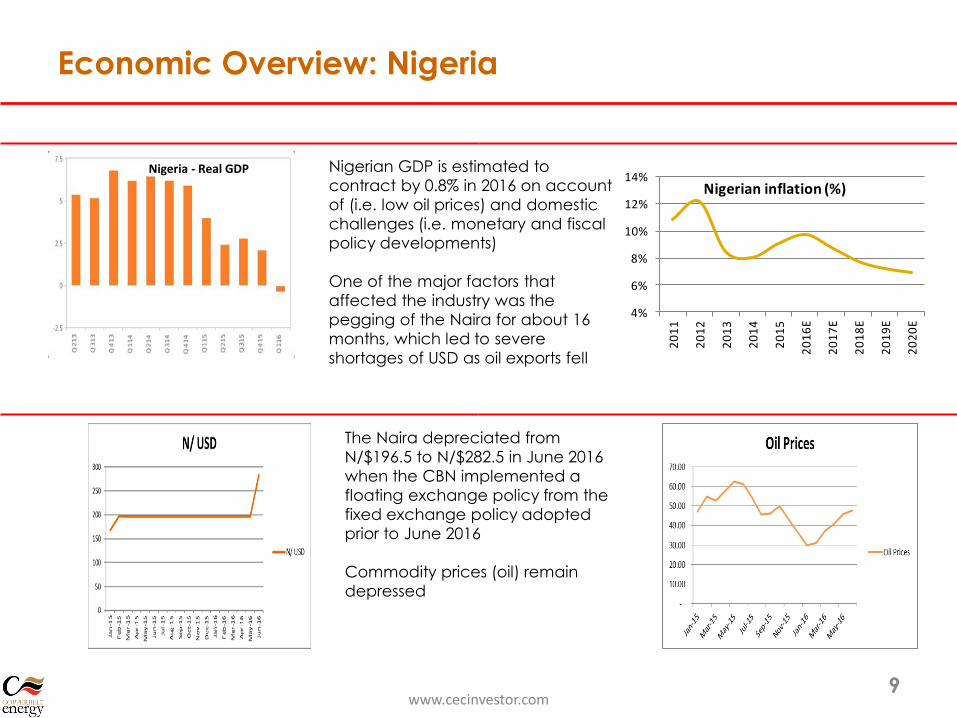

Economic Overview: Nigeria

www.cecinvestor.com9

Nigerian GDP is estimated to

contract by 0.8% in 2016 on account

of (i.e. low oil prices) and domestic

challenges (i.e. monetary and fiscal

policy developments)

One of the major factors that

affected the industry was the

pegging of the Naira for about 16

months, which led to severe

shortages of USD as oil exports fell

The Naira depreciated from

N/$196.5 to N/$282.5 in June 2016

when the CBN implemented a

floating exchange policy from the

fixed exchange policy adopted

prior to June 2016

Commodity prices (oil) remain

depressed

Nigeria - Real GDP

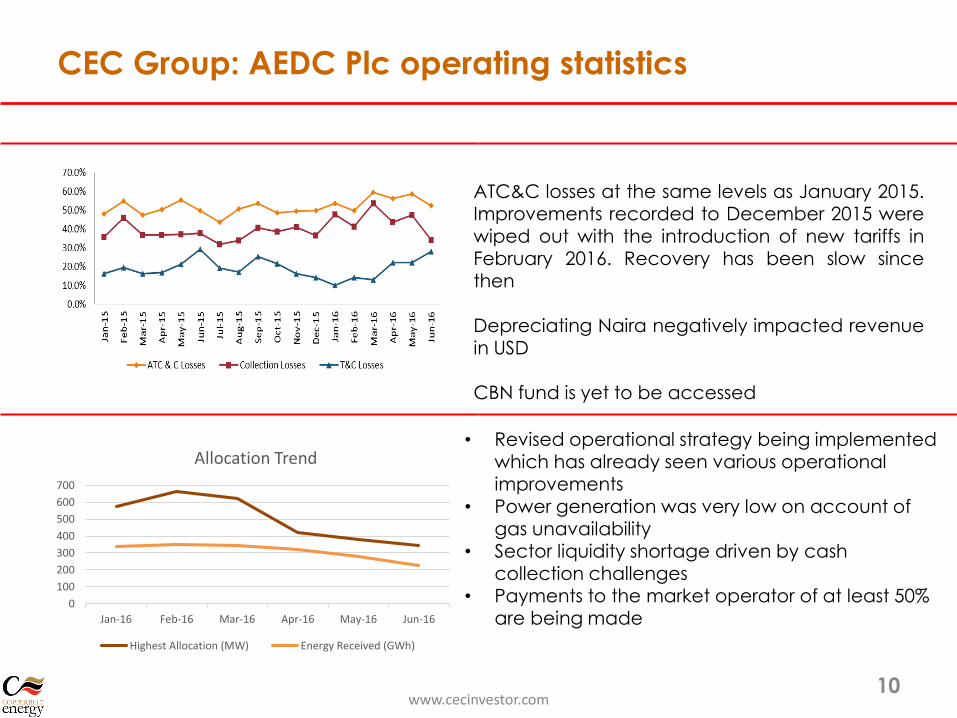

CEC Group: AEDC Plc operating statistics

www.cecinvestor.com10

ATC&C losses at the same levels as January 2015.Improvements recorded to December 2015 werewiped out with the introduction of new tariffs inFebruary 2016. Recovery has been slow sincethen

Depreciating Naira negatively impacted revenuein USD

CBN fund is yet to be accessed

0

100

200

300

400

500

600

700

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Allocation Trend

Highest Allocation (MW) Energy Received (GWh)

• Revised operational strategy being implemented which has already seen various operational improvements

• Power generation was very low on account of gas unavailability

• Sector liquidity shortage driven by cash collection challenges

• Payments to the market operator of at least 50% are being made

CEC Group

Health, Safety, Environment & Social

www.cecinvestor.com 11

Health, safety, environment and social (HSES)

Zambian Operations

– Recorded satisfactory levels of performance in HSES for the period

– Had nil fatalities and no serious environmental incidents

Nigerian Operations

– AEDC Plc:

o Poor condition and construction standards of part of the distribution

network continues to be a challenge with respect to HSES

o Working with industry regulators and all stakeholders to identify and rectify

the worst parts of the network

o Focus is on efforts aimed at reducing or eliminating network related

fatalities

– Shiroro continues with excellent performance and recorded no HSES incidents

during the period under review

Group Overall

– The Group is implementing strategies to improve HSES performance. A

programme to adopt similar practices/HSES culture across the Group is

underway

www.cecinvestor.com 12

CEC Group

Group Financial Results

www.cecinvestor.com 13

Earnings from continuing operations, USD’m, 2014-2016

Dividend, 2014-2016*

Revenue, USD’m, 2014-2016

EPS, USc, 2006-2015

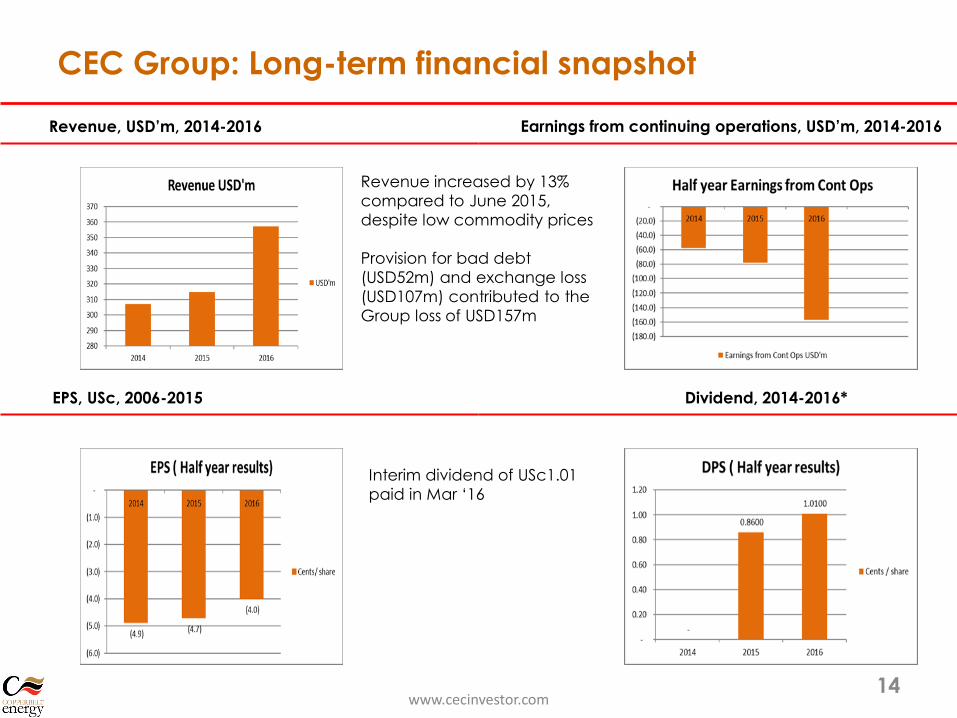

CEC Group: Long-term financial snapshot

www.cecinvestor.com14

Revenue increased by 13%

compared to June 2015,

despite low commodity prices

Provision for bad debt

(USD52m) and exchange loss

(USD107m) contributed to the

Group loss of USD157m

Interim dividend of USc1.01

paid in Mar ‘16

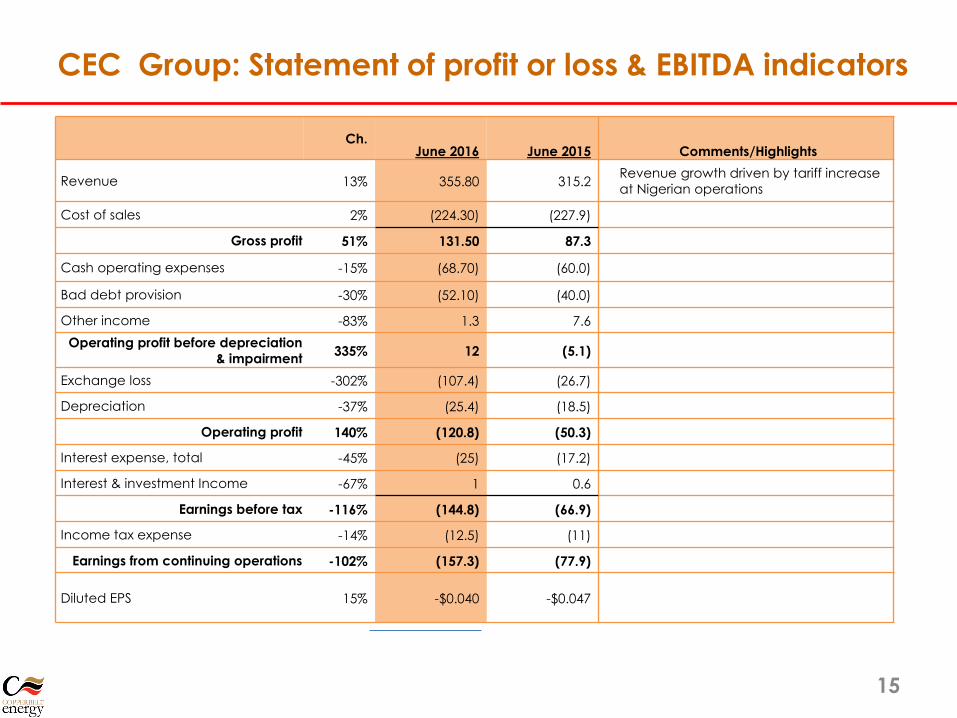

CEC Group: Statement of profit or loss & EBITDA indicators

15

Ch.June 2016 June 2015 Comments/Highlights

Revenue 13% 355.80 315.2 Revenue growth driven by tariff increase

at Nigerian operations

Cost of sales 2% (224.30) (227.9)

Gross profit 51% 131.50 87.3

Cash operating expenses -15% (68.70) (60.0)

Bad debt provision -30% (52.10) (40.0)

Other income -83% 1.3 7.6

Operating profit before depreciation

& impairment335% 12 (5.1)

Exchange loss -302% (107.4) (26.7)

Depreciation -37% (25.4) (18.5)

Operating profit 140% (120.8) (50.3)

Interest expense, total -45% (25) (17.2)

Interest & investment Income -67% 1 0.6

Earnings before tax -116% (144.8) (66.9)

Income tax expense -14% (12.5) (11)

Earnings from continuing operations -102% (157.3) (77.9)

Diluted EPS 15% -$0.040 -$0.047

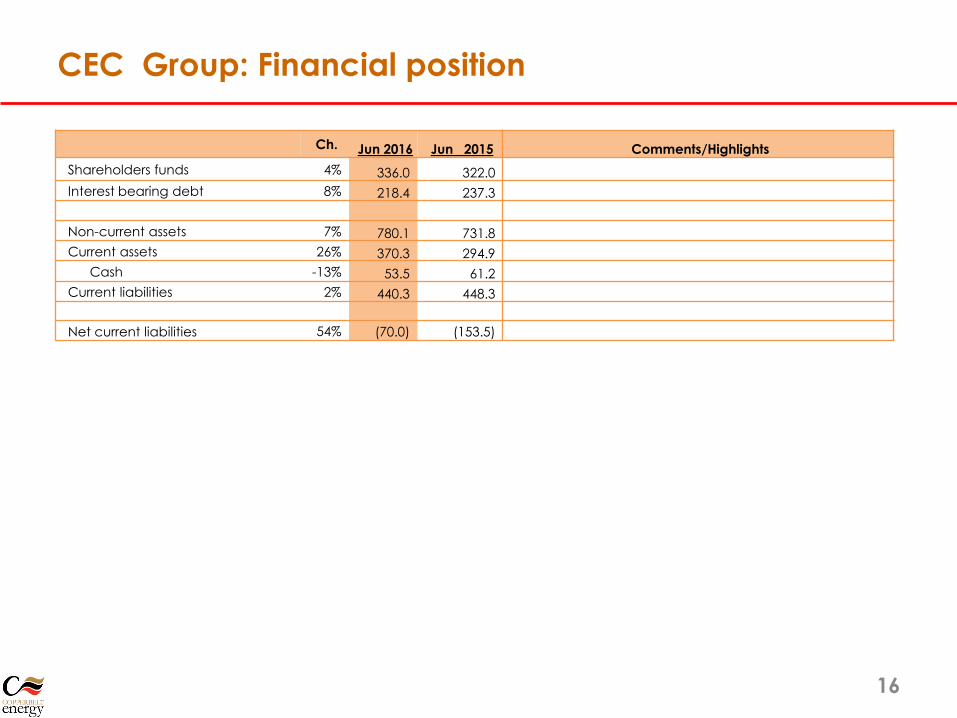

CEC Group: Financial position

16

Ch. Jun 2016 Jun 2015 Comments/Highlights

Shareholders funds 4% 336.0 322.0

Interest bearing debt 8% 218.4 237.3

Non-current assets 7% 780.1 731.8

Current assets 26% 370.3 294.9

Cash -13% 53.5 61.2

Current liabilities 2% 440.3 448.3

Net current liabilities 54% (70.0) (153.5)

CEC Group

Financial results – Zambian Operations

www.cecinvestor.com 17

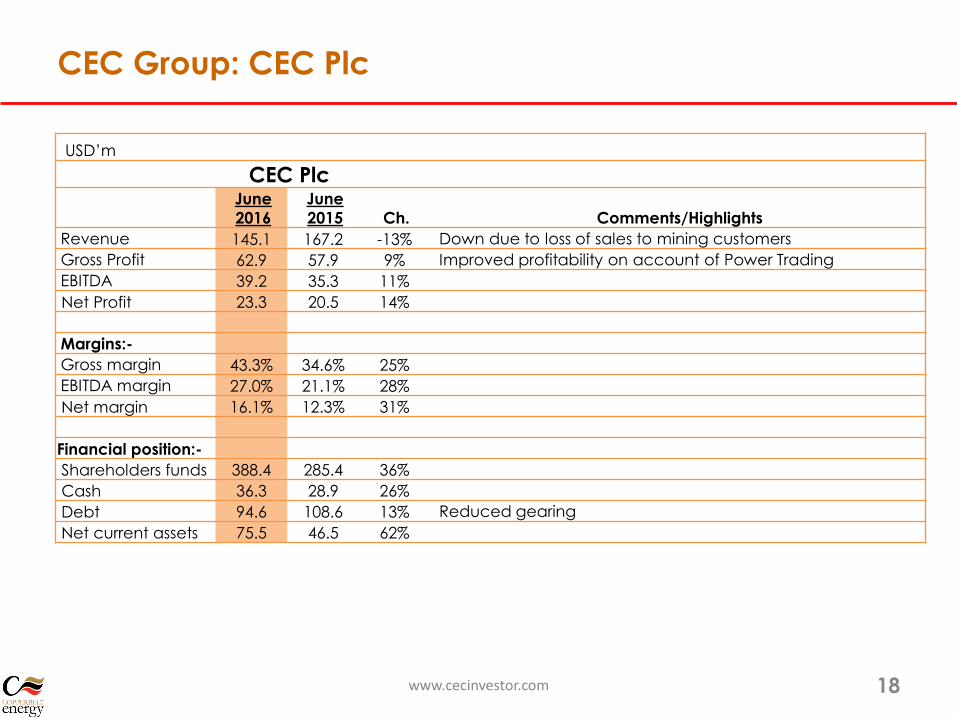

CEC Group: CEC Plc

USD’m

CEC PlcJune

2016

June

2015 Ch. Comments/Highlights

Revenue 145.1 167.2 -13% Down due to loss of sales to mining customers

Gross Profit 62.9 57.9 9% Improved profitability on account of Power Trading

EBITDA 39.2 35.3 11%

Net Profit 23.3 20.5 14%

Margins:-

Gross margin 43.3% 34.6% 25%

EBITDA margin 27.0% 21.1% 28%

Net margin 16.1% 12.3% 31%

Financial position:-

Shareholders funds 388.4 285.4 36%

Cash 36.3 28.9 26%

Debt 94.6 108.6 13% Reduced gearing

Net current assets 75.5 46.5 62%

www.cecinvestor.com 18

CEC Plc: Long-term financial snapshot

www.cecinvestor.com19

e

n/15

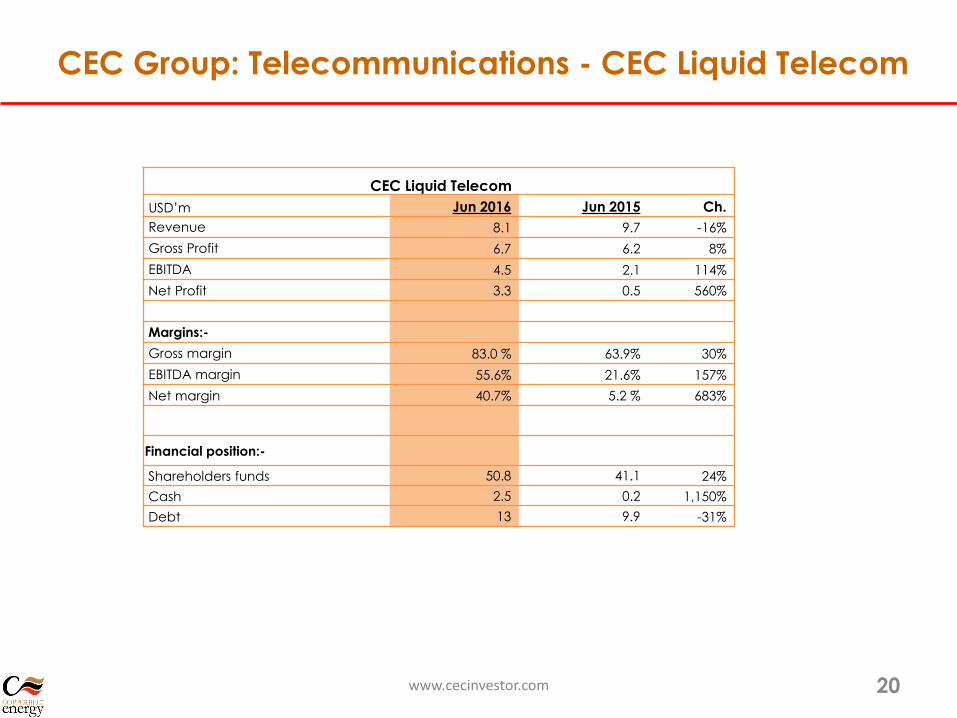

CEC Group: Telecommunications - CEC Liquid Telecom

www.cecinvestor.com 20

CEC Liquid Telecom

USD’m Jun 2016 Jun 2015 Ch.

Revenue 8.1 9.7 -16%

Gross Profit 6.7 6.2 8%

EBITDA 4.5 2.1 114%

Net Profit 3.3 0.5 560%

Margins:-

Gross margin 83.0 % 63.9% 30%

EBITDA margin 55.6% 21.6% 157%

Net margin 40.7% 5.2 % 683%

Financial position:-

Shareholders funds 50.8 41.1 24%

Cash 2.5 0.2 1,150%

Debt 13 9.9 -31%

CEC Group

Financial results – Nigerian Operation

www.cecinvestor.com 21

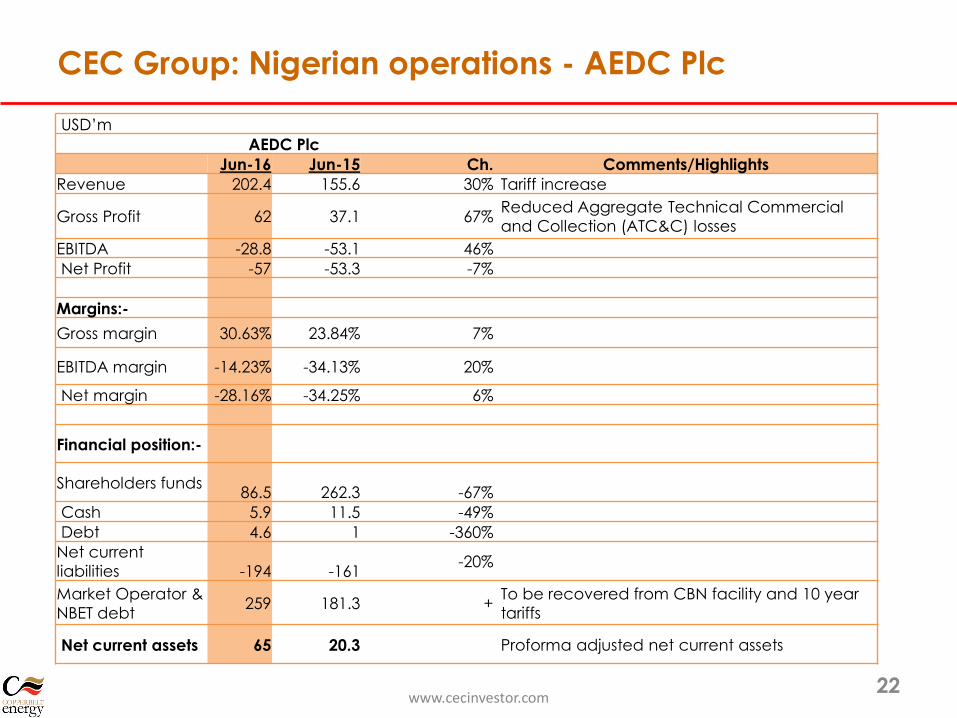

CEC Group: Nigerian operations - AEDC Plc

www.cecinvestor.com22

USD’m

AEDC Plc

Jun-16 Jun-15 Ch. Comments/Highlights

Revenue 202.4 155.6 30% Tariff increase

Gross Profit 62 37.1 67%Reduced Aggregate Technical Commercial

and Collection (ATC&C) losses

EBITDA -28.8 -53.1 46%

Net Profit -57 -53.3 -7%

Margins:-

Gross margin 30.63% 23.84% 7%

EBITDA margin -14.23% -34.13% 20%

Net margin -28.16% -34.25% 6%

Financial position:-

Shareholders funds86.5 262.3 -67%

Cash 5.9 11.5 -49%

Debt 4.6 1 -360%

Net current

liabilities -194 -161-20%

Market Operator &

NBET debt259 181.3 +

To be recovered from CBN facility and 10 year

tariffs

Net current assets 65 20.3 Proforma adjusted net current assets

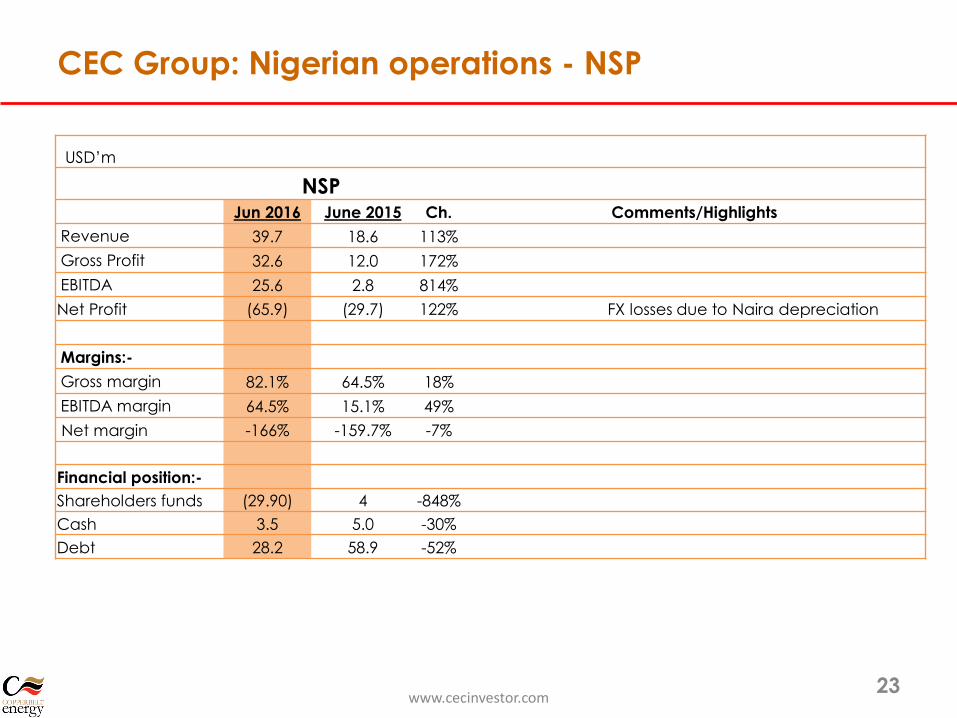

CEC Group: Nigerian operations - NSP

www.cecinvestor.com23

USD’m

NSPJun 2016 June 2015 Ch. Comments/Highlights

Revenue 39.7 18.6 113%

Gross Profit 32.6 12.0 172%

EBITDA 25.6 2.8 814%

Net Profit (65.9) (29.7) 122% FX losses due to Naira depreciation

Margins:-

Gross margin 82.1% 64.5% 18%

EBITDA margin 64.5% 15.1% 49%

Net margin -166% -159.7% -7%

Financial position:-

Shareholders funds (29.90) 4 -848%

Cash 3.5 5.0 -30%

Debt 28.2 58.9 -52%

CEC Group

Financial results –

Comparison Zambian & Nigerian Operations

www.cecinvestor.com 24

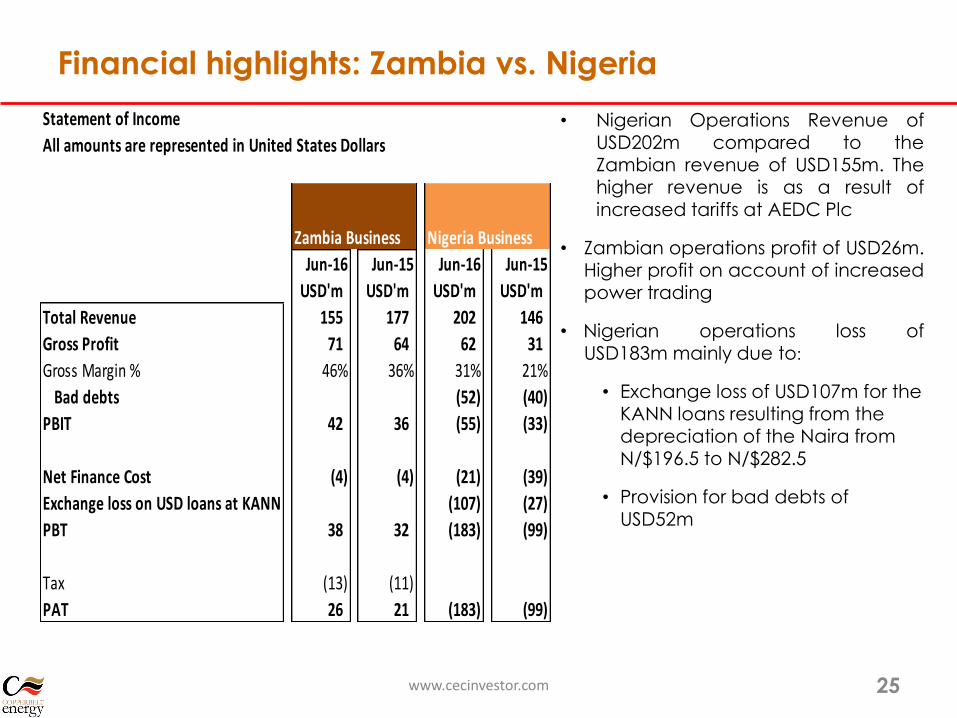

Financial highlights: Zambia vs. Nigeria

25

• Nigerian Operations Revenue ofUSD202m compared to theZambian revenue of USD155m. Thehigher revenue is as a result ofincreased tariffs at AEDC Plc

• Zambian operations profit of USD26m.Higher profit on account of increasedpower trading

• Nigerian operations loss ofUSD183m mainly due to:

• Exchange loss of USD107m for the KANN loans resulting from the depreciation of the Naira from N/$196.5 to N/$282.5

• Provision for bad debts of USD52m

www.cecinvestor.com

Statement of Income

All amounts are represented in United States Dollars

Jun-16 Jun-15 Jun-16 Jun-15

USD'm USD'm USD'm USD'm

Total Revenue 155 177 202 146

Gross Profit 71 64 62 31

Gross Margin % 46% 36% 31% 21%

Bad debts (52) (40)

PBIT 42 36 (55) (33)

Net Finance Cost (4) (4) (21) (39)

Exchange loss on USD loans at KANN (107) (27)

PBT 38 32 (183) (99)

Tax (13) (11)

PAT 26 21 (183) (99)

Zambia Business Nigeria Business

Financial highlights: Zambia vs. Nigeria

26

• Total current liabilities for the Nigerian business includes USD259m relating to the market operator’s (MO) bill

• Efforts to seek senior debt for capital expenditure underway

• Sector liquidity shortfall negatively impacting on the operation’s ability to meet the full bill to the Market Operator

• Currency mismatch between the cash-flows and UBA loan obligation remains key risk

www.cecinvestor.com

Outlook & strategy

www.cecinvestor.com 27

Strategy & Outlook

28

Business Growth Strategy Exploring opportunities that can be integrated with the core business, with a focus on

Southern Africa

Opportunities being explored include power trading growth, embedded generation, transmission reinforcement

Work with other sector players to resolve tariff issues in Zambia

Projects Underway Progress the 128MW CECA SL project to financial close

Nigerian Assets Address the currency mismatch Manage the over-leverage at KANN Restructure the facility to align the repayments to cash flows Work with Government on regulation and liquidity challenges Operational improvements

Market Cap Undervalued The Board and management believe the current market cap does not represent ‘fair

value’ for the group The Board and management appreciate that the power sector issues in Nigeria and the

limited liquidity in the stock, may be impacting valuation CEC is currently evaluating options to unlock value for shareholders (which may include

a restructuring of the group, and/or a listing on the JSE) and has appointed financial advisors to assist in this regard

Q&A

www.cecinvestor.com 29

Thank You

www.cecinvestor.com 30

Top Related