Languages

Pages

Legal

“Organization, focus and governance: How to perpetuate our history of success”

PROGRAM

8:00 Registration and breakfast

9:15 RENATO VALEOpening and welcome

9:40DYOGO OLIVEIRAMinistry of Planning, Development and Budget

11:10 Questions and Answers

11:30 to 12:00

Break

12:10 JOSÉ BRAZCCR Rodovias BR

10:25 ANTONIO LAVAREDAPolitical Scientist

12:25 ÍTALO ROPPACCR Rodovias SP

12:40 LEONARDO VIANNACCR Mobilidade

12:55 RICARDO BISORDICCR Aeroportos

13:10ARTHUR PIOTTO FILHOFinancial Strategy for the Future

13:30RENATO VALEOrganization, Focus and Governance

13:50 Debate, questions and answers

14:10 Lunch

VIDEO INSTITUCIONAL

RENATO VALEOPENING

“Organization, focusand governance”

DEFINITIONBUSINESS

To allow solutions in investments and services in infrastructure, contributing to the

social, economical and environmental development of the areas

where it engages

ACKNOWLEDGMENTS 2016 AND 2017

COMPANIES OFCCR GROUP IN 2005

URBAN MOBILITYCompany Interest

STP 34%

AIRPORTSCompany Interest

SERVICESCompany Interest

CCR Actua 100%

CCR Engelog 100%

CCR EngelogTec 100%

ROADSCompany Interest

CCR NovaDutra 100%

CCR ViaLagos 100%

CCR RodoNorte 86%

CCR AutoBAn 100%

CCR ViaOeste 100%

COMPANIES OF CCR GROUP IN 2017

Renovias 40%

CCR SPVias 100%

ViaRio 66%

CCR MSVia 100%

ViaQuatro 75%

CCR Barcas 80%

VLT Carioca 24,9%

CCR Metrô Bahia 100% SAMM 100%

Quito 50%

San Jose 48%

Curaçao 79%

BH Airport 38%

TAS 70%

QUIAMA 50%

URBAN MIBILITYCompanies Interest

AIRPORTSCompanies Interest

SERVICESCompanies Interest

CCR Actua 100%

CCR Engelog 100%

CCR EngelogTec 100%

ROADSCompanies Interest

CCR NovaDutra 100%

CCR ViaLagos 100%

CCR RodoNorte 86%

CCR AutoBAn 100%

CCR ViaOeste 100%

Communication& Sustainability

InstitutionalRelations

Compliance

CHIEF EXECUTIVE OFFICE

CCR AEROPORTOS

New Business

Functional Support

CCR USA

CCR MOBILIDADE

New Business

Functional Support

CCR RODOVIAS BR

New Business

Functional Support

CCR RODOVIAS SP

New Business

Functional Support

Corporate officer management

Institutional strategic management

Corporate management

Business development and management

Corporate Management

Business Development

Finance & Institutional Relations

Legal Department

Planning& Control

ORGANIZATION

FOCUS

ROLES ANDRESPONSIBILITIES

ESTRATEGIC

TATICS

TRANSACTIONS

• To develop and accomplish business to assure growth and

perpetuity. • Business management and

excellence.

BUSINESS DIVISIONS

• Set strategic policies and directions for the Group.

CORPORATE MANAGEMENT

• Operational excellence and efficiency

• Maximization when generating results

BUSINESS UNIT

• Perform transactions activities and processes with differentiated

solutions, maximum efficiency and added value.

CSC

SCENARIO IN BRAZIL

End of recession period – two consecutive quarters of growth (beginning in 2014 2nd Quarter)

GDP is estimated to be positive in 2017 to grow in 2018

Interest rates

Decrease in unemployment rate

Increase in production of cars in 42.2% in October (compared to the same month in the

previous year)

Increase in production and grains (agriculture) export

Inflation controled

JOSÉ BRAZCCR RODOVIAS BR

VIDEO CCR RODOVIAS BR

CCR NovaDutra

SCENARIO IN BRAZIL

End of recession period – two consecutive quarters of growth (beginning in 2014 2nd Quarter)

GDP is estimated to be positive in 2017 to grow in 2018

Interest rates

Decrease in unemployment rate

Increase in production of cars in 42.2% in October (compared to the same month in the

previous year)

Increase in production and grains (agriculture) export

Inflation controled

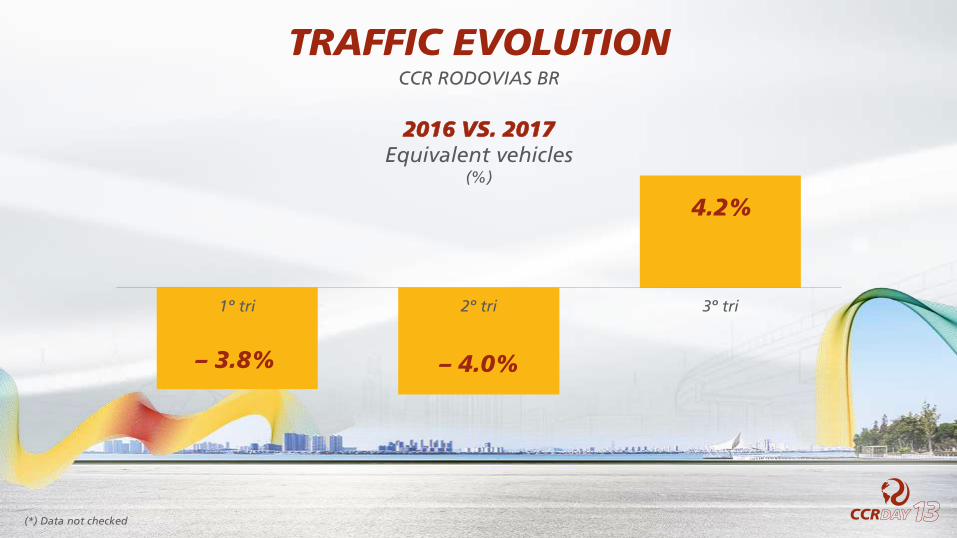

TRAFFIC EVOLUTIONCCR RODOVIAS BR

1º tri 2º tri 3º tri

– 3.8% – 4.0%

4.2%

2016 VS. 2017Equivalent vehicles

(%)

(*) Data not checked

OPPORTUNITIESANNUAL CONTRACTS

investments3 billion

priority25 worksRequest by

ANTT

in Serra das Araras1.7 billion

New investments in current contract

R$1.5BI

OPPORTUNITIESBRAZIL

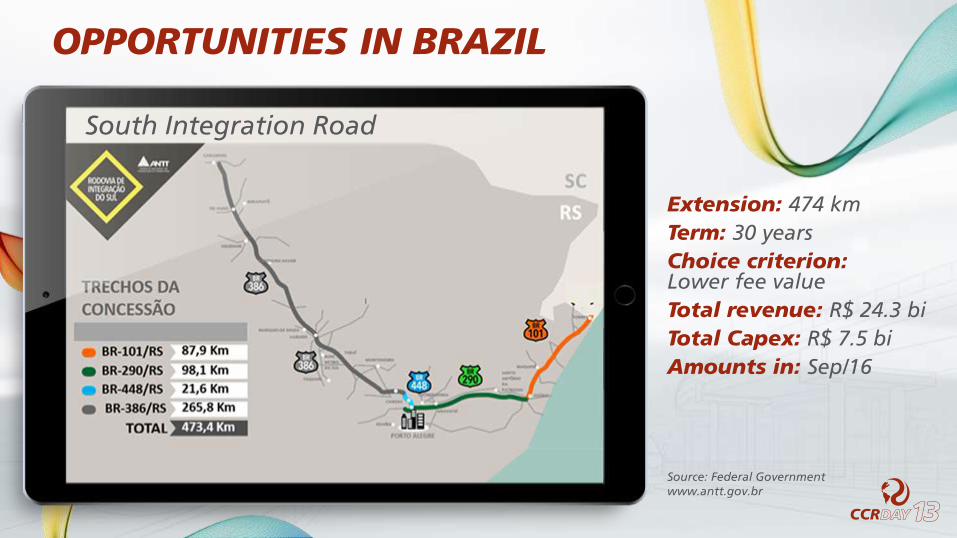

South Integration Road

Source: Federal Government www.antt.gov.br

Extension: 474 kmTerm: 30 yearsChoice criterion:Lower fee valueTotal revenue: R$ 24.3 biTotal Capex: R$ 7.5 biAmounts in: Sep/16

OPPORTUNITIES IN BRAZIL

BR101 Road (Palhoça)

Extension: 220 kmTerm: 30 yearsChoice criterion:Lower fee valueTotal Capex: R$ 4.1 biAmounts in: May/16

OPPORTUNITIES IN BRAZIL

Source: Federal Government www.antt.gov.br

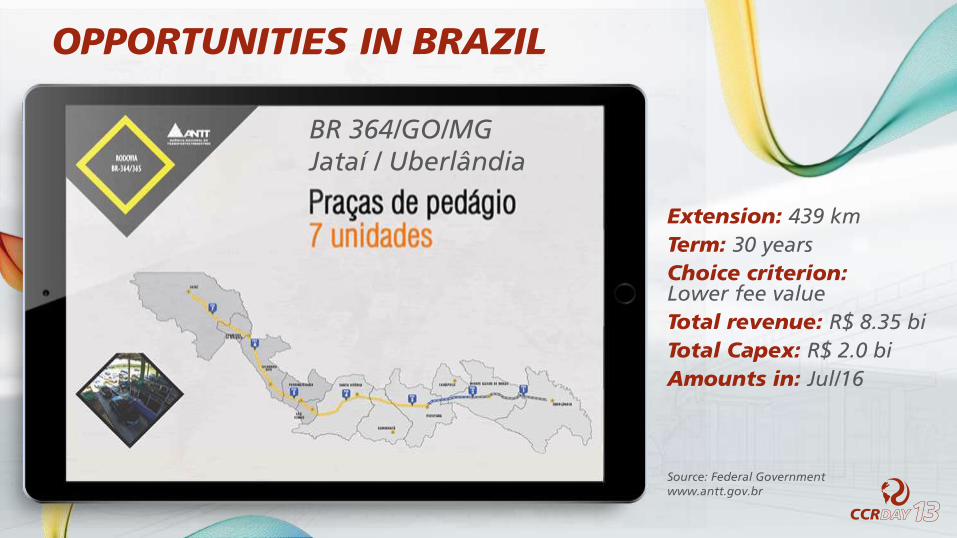

BR 364/GO/MG Jataí / Uberlândia

Extension: 439 kmTerm: 30 yearsChoice criterion:Lower fee valueTotal revenue: R$ 8.35 bi Total Capex: R$ 2.0 biAmounts in: Jul/16

OPPORTUNITIES IN BRAZIL

Source: Federal Government www.antt.gov.br

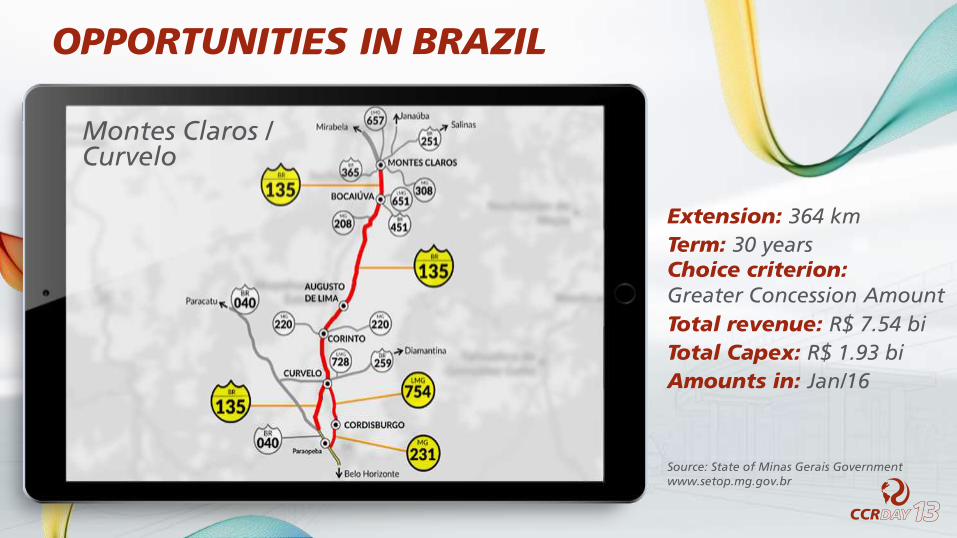

Montes Claros / Curvelo

Source: State of Minas Gerais Governmentwww.setop.mg.gov.br

Extension: 364 kmTerm: 30 yearsChoice criterion:Greater Concession Amount Total revenue: R$ 7.54 bi Total Capex: R$ 1.93 biAmounts in: Jan/16

OPPORTUNITIES IN BRAZIL

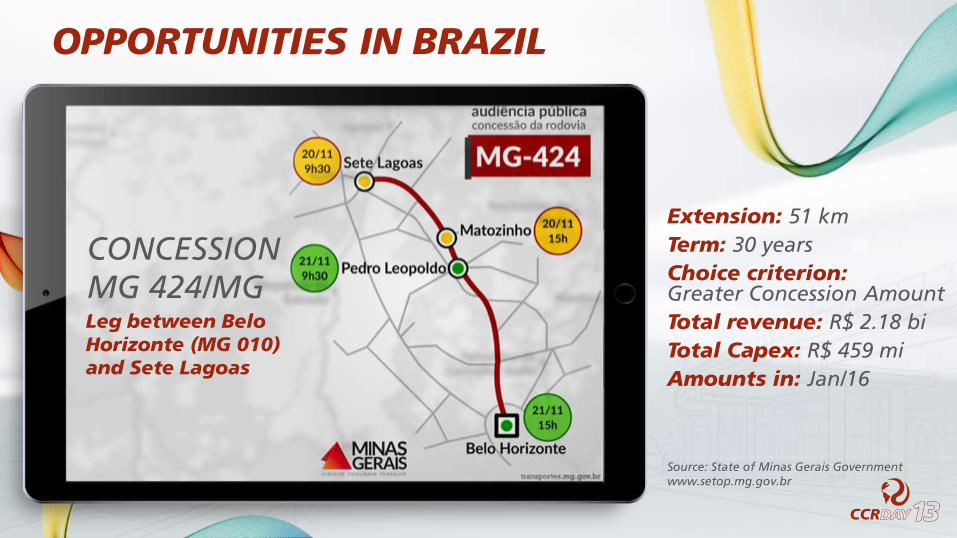

Extension: 51 kmTerm: 30 yearsChoice criterion:Greater Concession Amount Total revenue: R$ 2.18 bi Total Capex: R$ 459 miAmounts in: Jan/16

Leg between Belo Horizonte (MG 010) and Sete Lagoas

CONCESSION MG 424/MG

OPPORTUNITIES IN BRAZIL

Source: State of Minas Gerais Governmentwww.setop.mg.gov.br

DEVELOPMENT OF THE CONDITIONS IN FEDERAL NOTICES

Discounts in Fee (above 10%) fosters majoring of quota capital of the Concessionaire

Beginning of construction of duplicated lanes set by increase in demand

Works for construction of extra lanes will be adjusted

Structured planning for

highways

Objective mechanisms for

contractual adjustments

Fines resolution

DEVELOPMENT OF THE CONDITIONS IN THEFEDERAL NOTICES

CONDITIONS BEING ANALYZED BY THE FEDARL GOVERNMENT

INTERNATIONAL OPPORTUNITIES

INTERNATIONAL MARKET

Chile

Peru

Colombia

Argentina

OPPORTUNITIES IN CHILE Strong market with consolidated history of compliance to the planning

Stage Region Concession StartEnd

(estimated)Km

Bid

din

gPla

nn

ed

Pro

ject

s

SantiagoConcesión Conexión Vial Ruta 78 hasta Ruta 68

2018 2058 9

ValparaisoSegunda Concesión Ruta 66 Camino de La Fruta

2018 2053 138

SantiagoAutopista Costanera Central TramoAmérico Vespucio – Las Vizcachas

N/I N/I 12

SantiagoAutopista Costanera Central TramoIsabel Riquelme – Américo Vespucio

N/I N/I 10

Santiago Concesión Mejoramiento Ruta G|21 2018 N/I 30

LlanquihueConcesión Vial AutopistaMetropolitana de Puerto Montt

2018 2048 32

Regíon de Los LagosConcesión Vial Ruta Longitudinal Chiloé

N/I N/I 101

Atacama y Antofagasta

Ruta 5, Tramo Caldera|Antofagasta 35 years 469

Región de Coquimbo

Segunda Concesión Ruta 5 Tramo Los Vilos|La Serena

2018 N/I 245

Source: Governo do Chile Concesiones.cl/proyectos

Strong market with consolidated history of compliance to the planning

Stage Region Concession End (Estimated) Km

Co

nce

ssio

ns

du

e t

o 2

02

3

Araucanía, Los RíosConcesión Ruta 5 Tramo Temuco | Río Bueno

2023 171

Maule y Bio Bio Concesión Ruta 5 Tramo Talca | Chillán 2023 193

Regiones Metropolitana, Valparaíso y Coquimbo

Concesión Ruta 5 Tramo Santiago | Los Vilos 2023 218

Los Ríos, Los LagosConcesión Ruta 5 Tramo Río Bueno | Puerto Montt

2023 135

Bio Bio, Araucanía Concesión Ruta 5 Tramo Chillán | Collipulli 2020 161

Valparaíso y Metropolitana

Concesión Interconexión Vial Santiago |Valparaíso | Viña del Mar, Ruta 68

2023 141

Metropolitana y Valparaíso

Concesión Autopista Santiago | San Antonio, Ruta 78

2018 132

Región del Bío Bío Concesión Acceso Norte a Concepción 2023 89

Source: Governo do Chile Concesiones.cl/proyectos

OPPORTUNITIES IN CHILE

Map Lots

PPP National Route No. Extension (km)Capex 1st to 4th

year (USD M)Capex 5th to 15th

year (USD M)Stag

A 3, 226 707 984 346 I

B 5 538 989 244 I

C 7, 33 877 631 455 I

D 8 ,36, A|005, 158, 188 911 1063 298 II

E 9, 11, 34, 193, A|008, A|012 390 1342 370 I

F 9 AU Rosario Córdoba, 33 635 1114 372 I

G 12, 16 780 1039 456 II

H 34, 9, 66, 1V66 887 991 510 II

I 19, 34 664 778 427 II

SurAU Riccheri, Av. J. Newbery, AU Ezeiza | Cañuelas, 3, 205

247 975 236 I

BB 3, 33, 229, 249, 252, 1V252, 1V3 299 638 169 II

Cuyo 7, 20, 40 342 278 181 II

AU Parque AU Parque 82 500 55 III

Puente Paraná Santa Fé

Puente Paraná | Santa Fé 30 650 21 III

Puente Chaco Corrientes

Puente Chaco | Corrientes 34 700 32 III

Source: Governo da Argentina | ppp.vialida.gob.ar

OPPORTUNITIES IN ARGENTINA

ITALO ROPPACCR RODOVIAS SP

VIDEO CCR RODOVIAS SP

SCENARIO IN BRAZIL

End of recession period – two consecutive quarters of growth (beginning in 2014 2nd Quarter)

GDP is estimated to be positive in 2017 to grow in 2018

Interest rates

Decrease in unemployment rate

Increase in production of cars in 42.2% in October (compared to the same month in the

previous year)

Increase in production and grains (agriculture) export

Inflation controled

SAO PAULOMARKET

GDP: 31% of the Brazilian GDP (1)

Population: 22% of the Brazilian population (1)

Vehicles production: 45% of the Brazilian production (2)

Fleet in SP: 29% national fleet being 34% of cars (2)

Port of Santos: 28% of Brazilian imports/exports (R$) up to September 2017 (3)

Increase in Imports and Exports (t) of 10.3% compared to 2016 up to September (4)

Highway Concessions: 37%

Opportunities – Current Contracts

New bidding processes

SOURCE: ARTESP

2019 2021

End of current contracts

2022 2025 2027 2028

SOURCES: 1. Industry Portal (Portal da Indústria) / 2. ANFAVEA / 3. MDIC / 4. Port of Santos

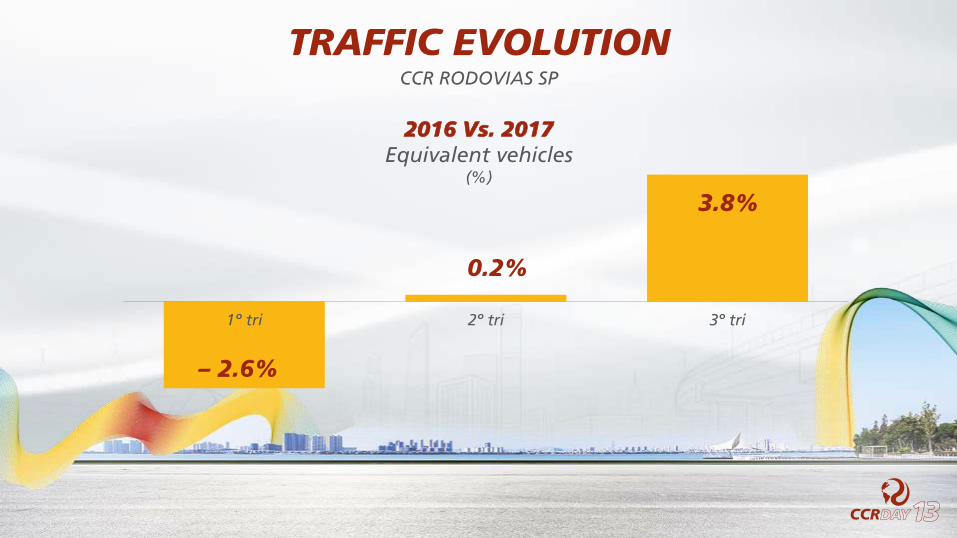

1º tri 2º tri 3º tri

– 2.6%

0.2%

3.8%

TRAFFIC EVOLUTIONCCR RODOVIAS SP

2016 Vs. 2017Equivalent vehicles

(%)

OPPORTUNITIESCURRENT CONTRACTS

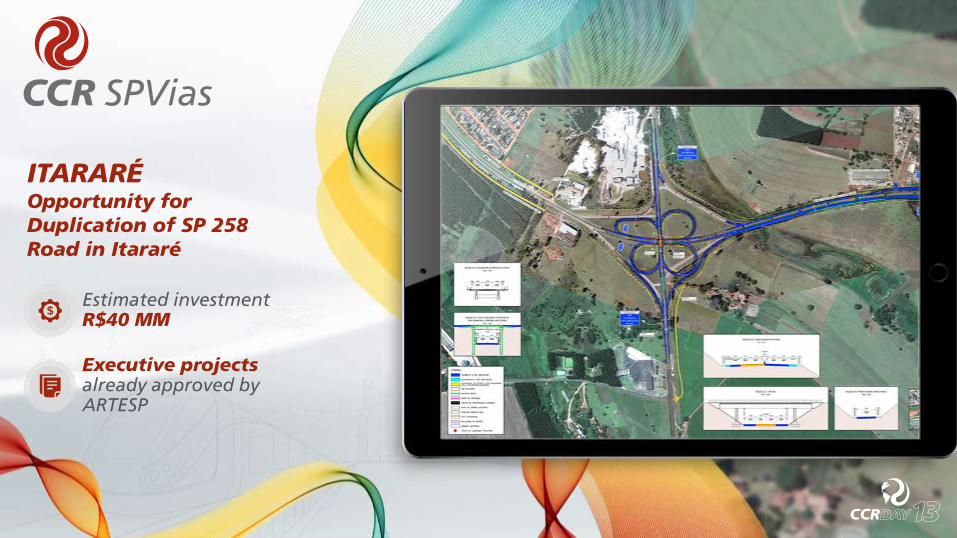

ITARARÉOpportunity for Duplication of SP 258 Road in Itararé

Estimated investment R$40 MM

Executive projects already approved by ARTESP

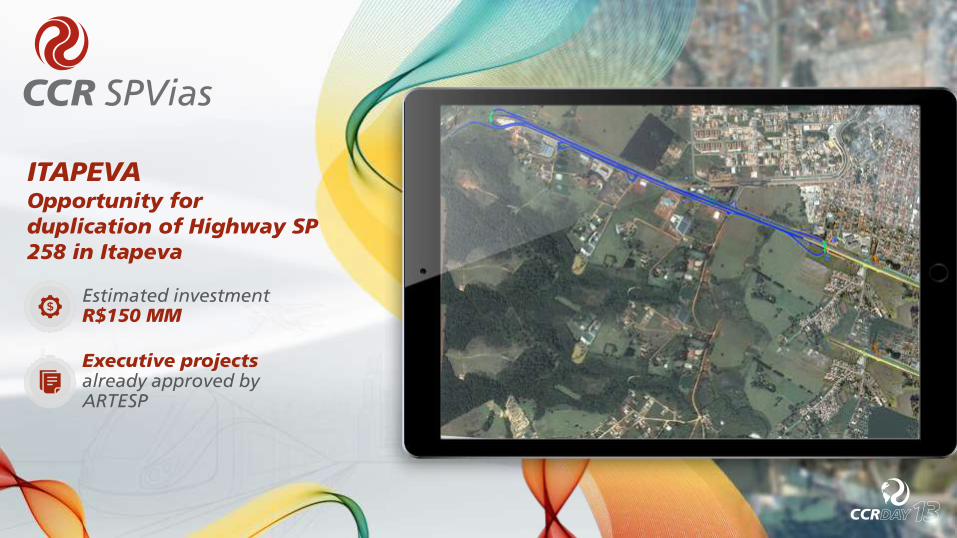

Estimated investment R$150 MM

Executive projectsalready approved by ARTESP

ITAPEVAOpportunity for duplication of Highway SP 258 in Itapeva

SP 255Opportunity for duplication of Highway SP 255 in Avaré

Estimated investment R$250 MM

Duplication of 44 km

JUNDIAÍ PROJECT Opportunity for development of 2nd Phase Implementation of flyovers and access bridges

Investments at R$ 350 MM

New crossroad implementation

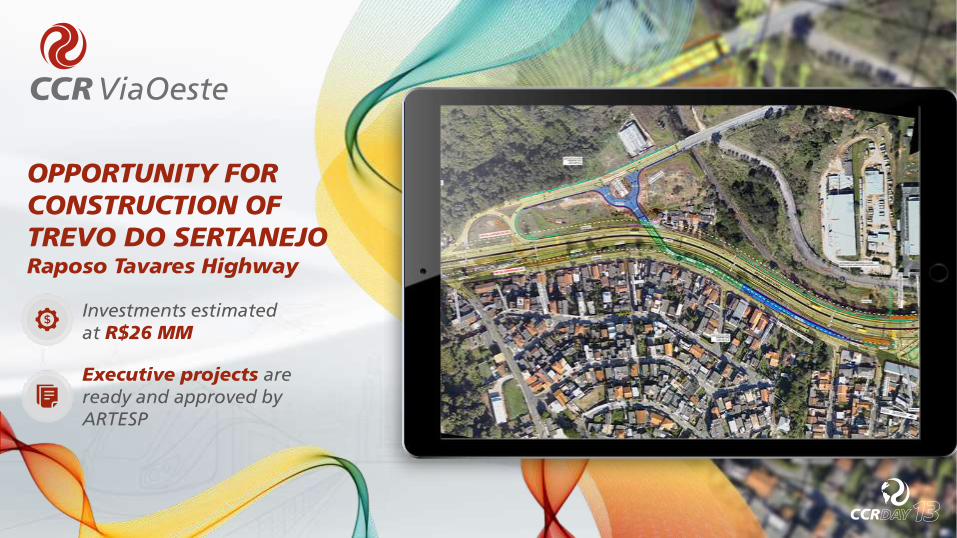

OPPORTUNITY FOR CONSTRUCTION OF TREVO DO SERTANEJORaposo Tavares Highway

Investments estimated at R$26 MM

Executive projects are ready and approved by ARTESP

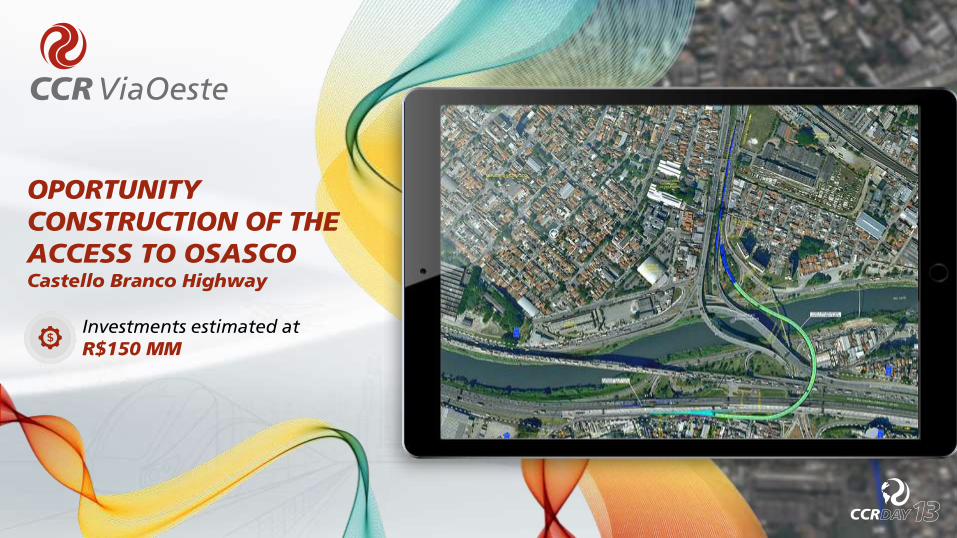

OPORTUNITY CONSTRUCTION OF THE ACCESS TO OSASCO Castello Branco Highway

Investments estimated at R$150 MM

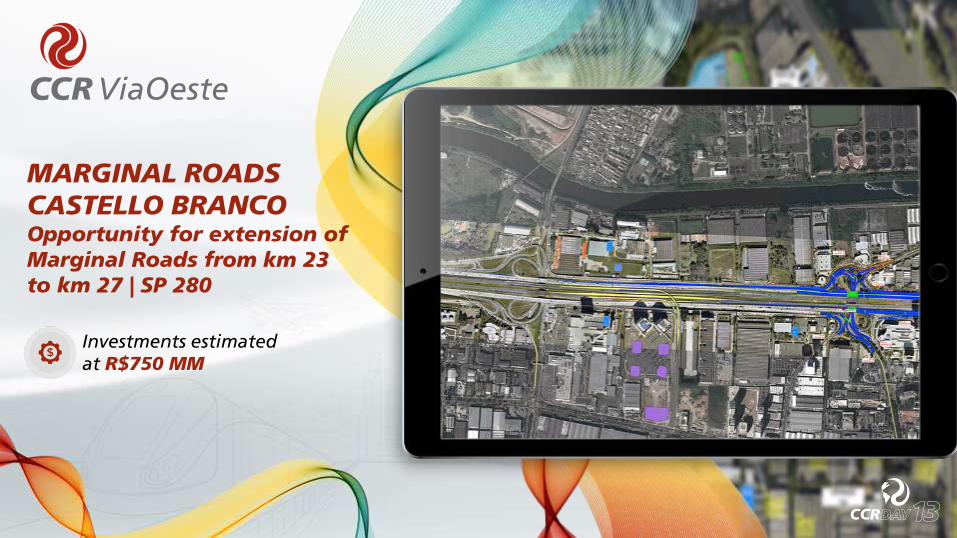

Investments estimated at R$750 MM

MARGINAL ROADSCASTELLO BRANCOOpportunity for extension of Marginal Roads from km 23 to km 27 | SP 280

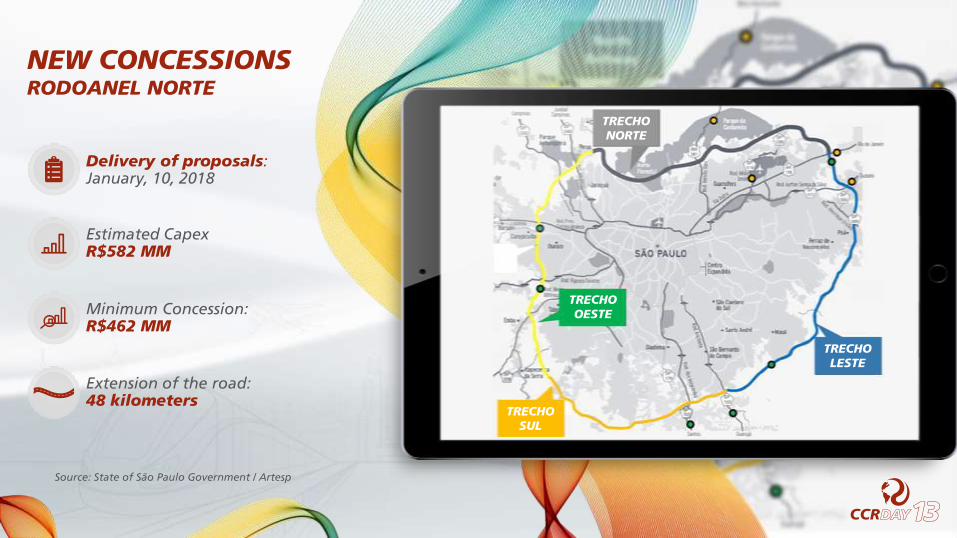

NEW CONCESSIONS RODOANEL NORTE

Estimated Capex R$582 MM

Delivery of proposals: January, 10, 2018

Minimum Concession: R$462 MM

Extension of the road:48 kilometers

Source: State of São Paulo Government / Artesp

TRECHO NORTE

TRECHO LESTE

TRECHO OESTE

TRECHO SUL

Public consultation in 2017 and bidding in 2018

Estimated investment by ARTESP: more than U$1 Bi

Source: State of São Paulo Government / Artesp

NEW CONCESSIONS RODOVIAS DO LITORAL

LEONARDO VIANNACCR MOBILIDADE

VIDEO CCR MOBILIDADE

CURRENT CONCESSIONS

Phase 2 Being implemented

Phase 1 Operating

Vila SôniaDelivery: DEC/20

São PauloMorumbi

Delivery: JUL/18Butantã

PinheirosFariaLima

FradiqueCoutinho

Oscar FreireDelivery: MAR/18

Paulista

MackenzieHigienópolis

Delivery: DEC/17

República

Luz

1º tri 2º tri 3º tri

2016 Vs. 2017PASSENGERS

(%)

Results

1.6% 1.8%

0.1%

Contractual term2043 (30 years)

Total estimated investment R$ 5 Bi (base Apr/13)

Public funds (base Oct/13):

• Total amount: R$ 2.283 Bi • Received: R$ 1,874 Bi (until 11/1/17)

Beginning of full operationSep 2017 (except Airport)

FinancingLong Term: Calculated toR$ 3,827 Bi – Loan CPand Financing LP

Employment generated5,000

Line 2 Stations

Line 1 Stations

Pecuniary counterpartR$ 173.4 MM (base Apr/13)

AcessoNorte

Lapa

Pirajá

Detran

RodoviáriaPernambués

Imbuí

CAB

Pituaçu

Flamboyant

Bairro da Paz

Tamburugy

Aeroporto

Mussurunga

LINE2LINE 1

Pituaçú (em construção)

CAB

Imbuí

Pernambués

Aeroporto

Mussurunga

Bairro da Paz

Tamburugy

Flamboyant

Rodoviária

Detran

Acesso Norte

Bonocô

Brotas

Campo da Pólvora

Lapa

Complexo de Manutenção Pirajá

Pirajá

Bom Juá

Retiro

Acesso Norte

A CHALLENGE:BUS INTEGRATION

18 20 21 21 22 29 38 45 45 49 5171 65 74 78 83 95

117 116131

174

PROGRESS IN DEMAND(AVERAGE BUSINESS DAY / THOUSAND)

BeginningBusiness Operation

Full OperationLine 1

IntegrationPirajá

IntegrationLapa

Beginning Line 2 (Access Norte – Bus Station)

Beginning Line 2 (Bus Station –Pituaçú)

Integrationfull fee

Beginning Line 2(Flamboyant –Mussurunga)

Cut of metropolitanlines

VIDEO BORA DE METRÔ

VLT | THE PROJECT AND THE CONSEQUENCES

Revitalization of port area

Expansion of number of real properties

Integration of city areas of port area and river central area

Connection between the lines that serve the river central area

28 kilometers of lines

29 stops / stations

R$ 1,188 MM* in investments

32 trains

R$ 532 MM* of public funds

R$ 5,95 MM* monthly counterparts

*Amounts with base in June 2012

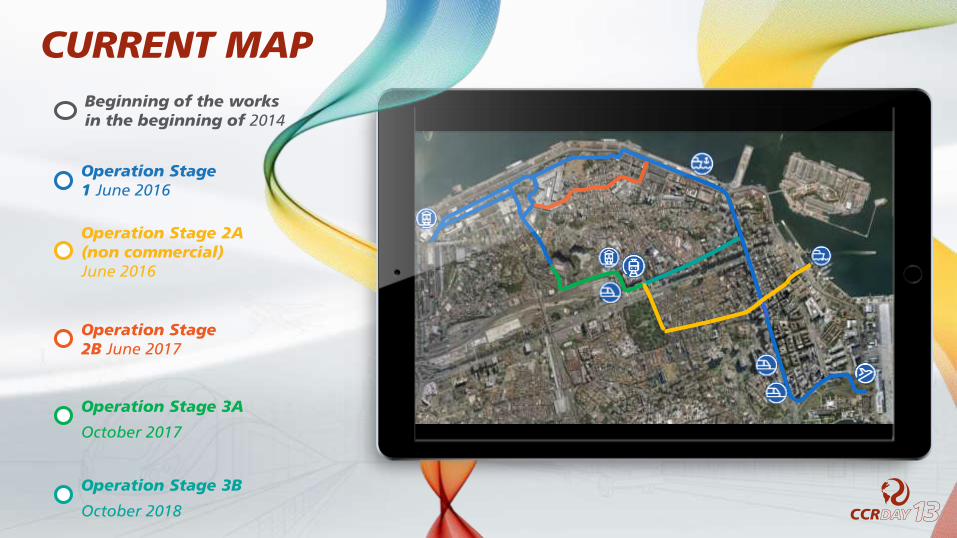

CURRENT MAPBeginning of the works in the beginning of 2014

Operation Stage 1 June 2016

Operation Stage 2A(non commercial) June 2016

Operation Stage 2B June 2017

Operation Stage 3A

October 2017

Operation Stage 3B

October 2018

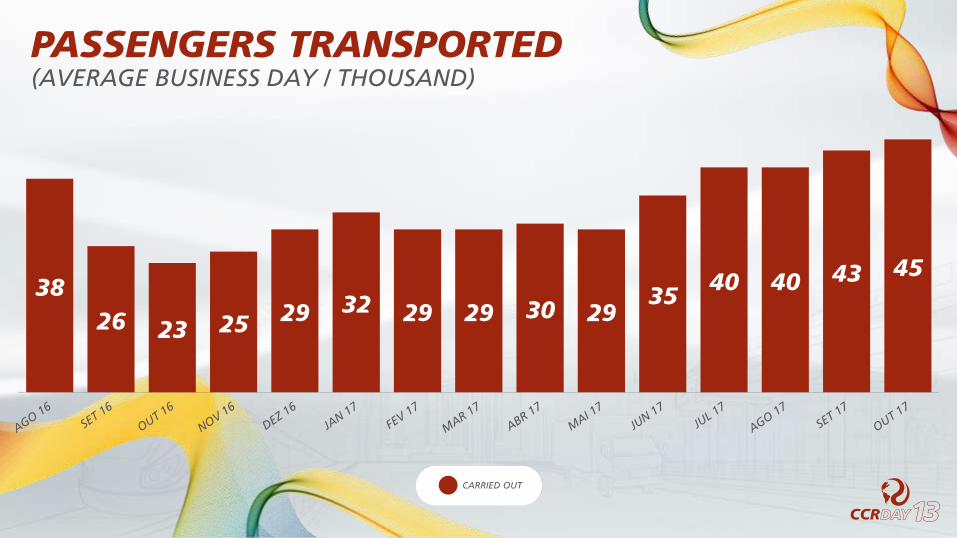

3826 23 25 29 32 29 29 30 29

3540 40 43 45

PASSENGERS TRANSPORTED(AVERAGE BUSINESS DAY / THOUSAND)

CARRIED OUT

OPPORTUNITIESCURRENT CONTRACTS

Extension5.5 Km

Under preparation basic project

Line 2 Stations

Line 1 Stations

AcessoNorte

Lapa

Pirajá

Detran

RodoviáriaPernambués

Imbuí

CAB

Pituaçu

Flamboyant

Bairro da Paz

Tamburugy

Aeroporto

Mussurunga

TRAMO 3Brasilgás

Aguas Claras / Cajazeiras

Tramo 3

2 Stations(Campinas e Águas Claras)

Predicted start of works:2018

OPPORTUNITIES BRAZIL

LINES 5 AND 17 – METRÔ SP

Common concession20 years

950 thousand passengers(reference demand)

R$ 189.6 millionMinimum Fixed Grant

Metrô Operation(Line 5) and Monorail (Line 17)

Integrationwith others subway lines and metropolitan trains

Fee: R$ 1.73 (Feb/17)

28 km extension and 25 stations

Licitação aguardando liberação pelo TCE

Source : Edital de Concessão Linhas 5 e 17

Common concession20 years

LINE15 – METRÔ SP

Daily demand 350 thousand passengers / day

InvestmentsR$ 7.0 billion – government R$ 0.2 billion – concessionaire

Monorail / Extension15.3 km

11 Stations

Public Hearing September 6, 2017

Under Public Consultation until November 24, 2017 SILVER LINE / MONORAIL

15

Source : Edital para Consulta Públicade Concessão Linha 15

Sponsored PPP – Private Public Partnership 30 years

LINES 8 and 9 l CPTM

InvestmentsR$ 1.1 billion - governmentR$ 2.7 billion - concessionaire

Integrationwith other subway lines and metropolitan trains

Current demand1.0 million passengers / day

73.1 km extensionand 43 stations

PMI delivered on September 20, 2017

Serves 6 citiesSão Paulo, Osasco, Carapicuiba, Barueri, Jandira and Itapevi

ITAPEVI

BARUERIOSASCO

JANDIRACARAPICUÍBA

LINHA 9 / ESMERALDA

Em Construção

Em Projeto

Pátio Pres. Altino

SÃO PAULO

LINHA 8 / DIAMANTE

Source: Edital de Chamamento Públicodas Linhas 8 e 9

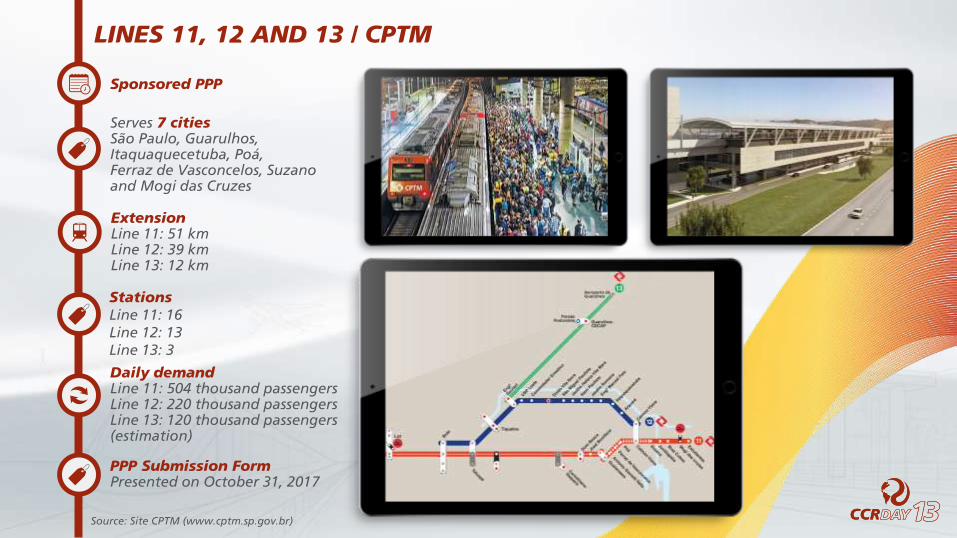

Sponsored PPP

LINES 11, 12 AND 13 / CPTM

Serves 7 citiesSão Paulo, Guarulhos, Itaquaquecetuba, Poá,Ferraz de Vasconcelos, Suzanoand Mogi das Cruzes

ExtensionLine 11: 51 kmLine 12: 39 kmLine 13: 12 km

StationsLine 11: 16Line 12: 13Line 13: 3

Daily demandLine 11: 504 thousand passengersLine 12: 220 thousand passengersLine 13: 120 thousand passengers (estimation)

PPP Submission Form Presented on October 31, 2017

Source: Site CPTM (www.cptm.sp.gov.br)

Sponsored PPP 30 years

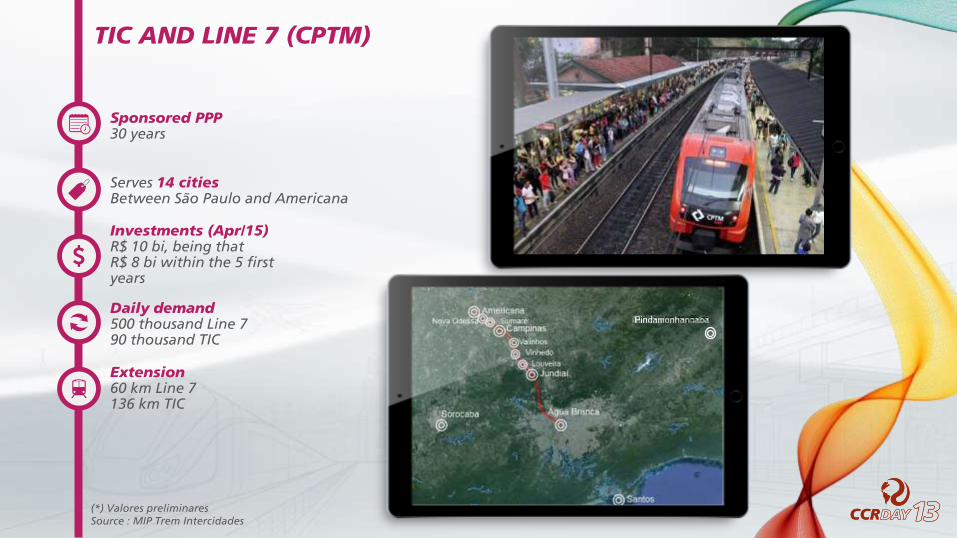

TIC AND LINE 7 (CPTM)

Investments (Apr/15)R$ 10 bi, being thatR$ 8 bi within the 5 first years

Daily demand 500 thousand Line 790 thousand TIC

Extension60 km Line 7136 km TIC

Serves 14 citiesBetween São Paulo and Americana

(*) Valores preliminaresSource : MIP Trem Intercidades

INTERNATIONALOPPORTUNITIES

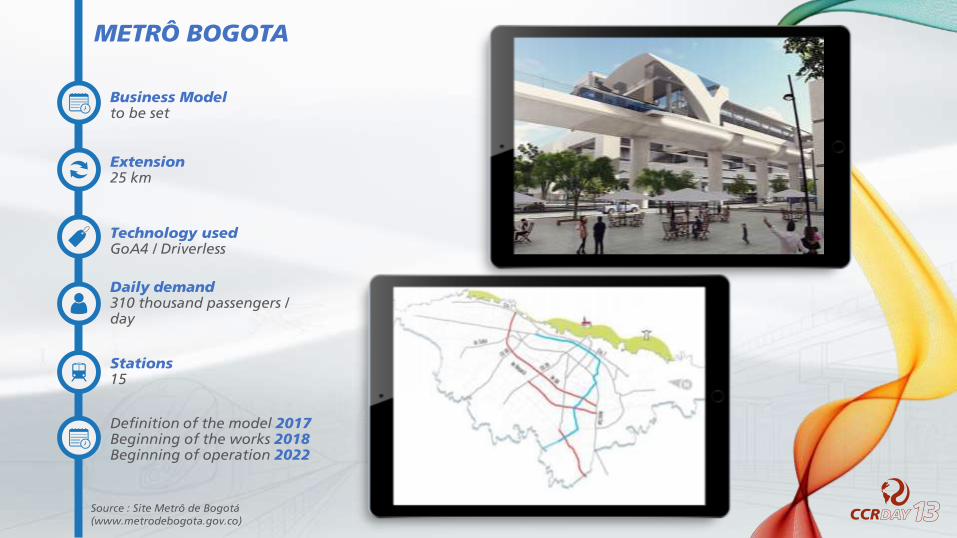

Business Modelto be set

METRÔ BOGOTA

Technology usedGoA4 / Driverless

Daily demand 310 thousand passengers / day

Stations15

Extension25 km

Definition of the model 2017Beginning of the works 2018Beginning of operation 2022

Source : Site Metrô de Bogotá (www.metrodebogota.gov.co)

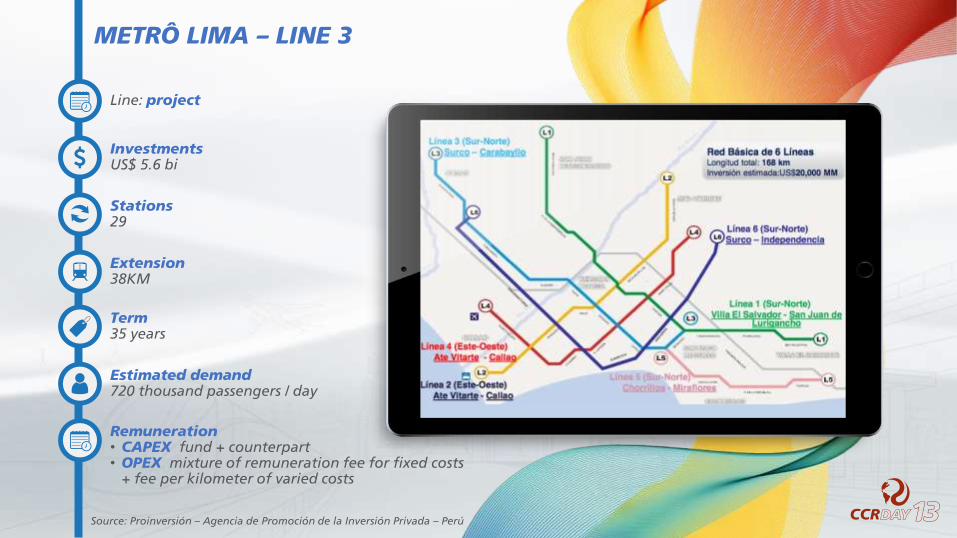

Line: project

METRÔ LIMA – LINE 3

Stations29

Extension38KM

Estimated demand 720 thousand passengers / day

Term35 years

Remuneration• CAPEX fund + counterpart• OPEX mixture of remuneration fee for fixed costs

+ fee per kilometer of varied costs

InvestmentsUS$ 5.6 bi

Source: Proinversión – Agencia de Promoción de la Inversión Privada – Perú

OTHER

OPPORTUNITIES

LINE 3Niterói

CBTUMetrô BH

Metrô Recife

METRÔ BUENOS AIRES

METRÔ BRASÍLIA

TRENSURBPORTO ALEGRE

METRÔ FORTALEZA

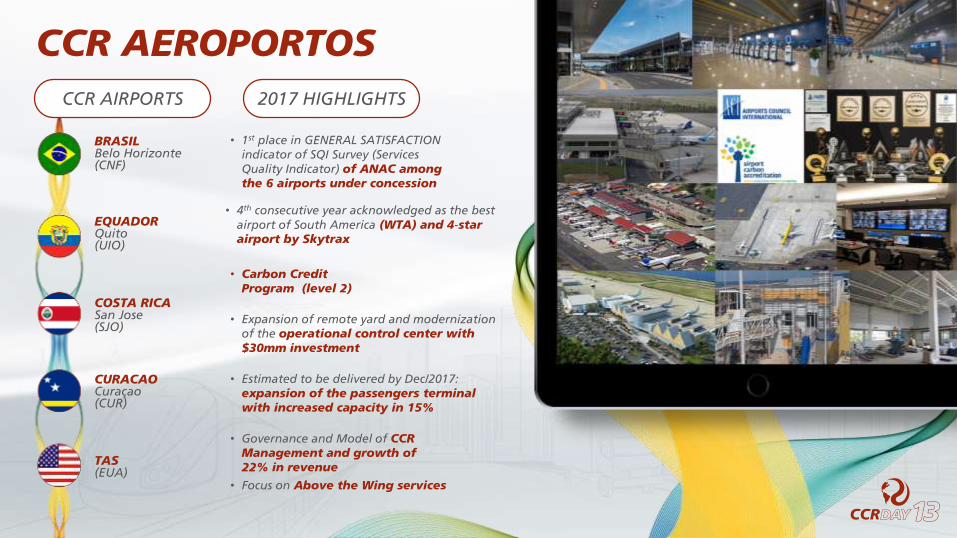

RICARDO BISORDICCR AEROPORTOS

VIDEO CCR AEROPORTOS

CCR AEROPORTOS

Strategic• To enhance qualified growth through acquisition in the primary

and secondary markets, consolidating CCR acknowledgement as a relevant player in the airports segment.

Qualifications• Sound model of Governance Management

• Multidiciplinary Teams

• Sound experience in 5 countries

• Sharing of the best practices

• Quick mobilization and access to the capital market

• Customized solutions (Service Companies)

CURRENTBUSINESS

1 2

TAS

CCR USA Airport Management Inc.Team of executives allocated in the United States

CCR Latin America and the CaribbeanTeam of executives allocated in Brazil

Total Airport Services (TAS)CCR USA holds 70% of the shares of Total Airport Services (TAS), a leading company in airport services engaged in the main airports in the United States

San José International AirportCCR: 48.75% of the shares4.3mm passengers

Curacao International AirportCCR: 79.80% of the shares1.8mm passengers

Quito International AirportCCR: 50.00% of the shares5.8mm passengers

BH AirportCCR: 38.25% of the shares10.5mm passengers

3 4

4

CCR LA & C

12

3

ORDLCK

BDL

ATL

HSV

LAX

SFO

OAK

CCR USA

CCR AEROPORTOS

BRASILBelo Horizonte (CNF)

EQUADORQuito(UIO)

COSTA RICASan Jose(SJO)

CURACAOCuraçao(CUR)

TAS(EUA)

CCR AEROPORTOSCCR AIRPORTS 2017 HIGHLIGHTS

• 1st place in GENERAL SATISFACTION indicator of SQI Survey (Services Quality Indicator) of ANAC among the 6 airports under concession

• 4th consecutive year acknowledged as the best airport of South America (WTA) and 4-star airport by Skytrax

• Carbon Credit Program (level 2)

• Expansion of remote yard and modernization of the operational control center with $30mm investment

• Estimated to be delivered by Dec/2017: expansion of the passengers terminal with increased capacity in 15%

• Governance and Model of CCR Management and growth of 22% in revenue

• Focus on Above the Wing services

GENERAL SCENARIO2017 2018Brazil• Political decisions prevailing over

technical recommendations• End of recession period

USA• Regrowth of the Market forprojects in partnership with private initiative

Costa Rica• Regrowth of the Market forprojects in partnership with private initiative

Curacao• Local operator with offer restrictions

Ecuador• Challenging political and economic scenario

Brazil• Economic indicators point out economic growth

USA• Continued infrastructure for two-party

new mayors elected• Long term operators are desired

Costa Rica• Trend for sustainable growth

Curacao• Demand constraints met by other

operators (new routes)

Ecuador• Economy permanently unaltered• Government facing difficulties to approve

new reforms

PASSENGERS

1%

7%

-15%

11%6%

Quito San José Curação BH Airport Total

Total Passengers(BOARDING ‘000)

(*) Data not checked

3rd quarter 2016 Vs. 3rd quarter 2017

OPPORTUNITIES

BRAZIL • New round of biddings: 13 airports

• Secondary market

LATIN AMERICA AND THE CARIBBEAN

• Most of airports under management of private initiative

• Secondary market

CCR AEROPORTOSDEVELOPMENT AND OPPORTUNITIES

CCR AEROPORTOSDEVELOPMENT AND OPPORTUNITIES

Strategic developer

Credibility, reputation and relationship

Public bidding and acquisitions

14 mapped opportunities

(short list)

New municipal elected representatives

UNITED STATES

Growing interest in PPP solution (P3) in infrastructure

Tax Reform may encourage P3

ARTHUR PIOTTO FILHOFINANCIAL STRATEGY

Debt of 3.0x net debt/EBITDA

Company growth will be financed thorugh leverage

Commitment to pay a minimum of 50%

of the net profitas dividend

FINANCIAL PILLARS

1.9 2.0 1.92.2 2.1 2.0 1.8 2.0 1.9 2.0 2.0

2.3 2.4 2.5 2.53.0 3.0 3.1

2.2 2.41.8 1.8

2.2

EVOLUTION OF DEBTS AND CAPACITY FOR ADDITIONAL LEVERAGE (R$ BI – PRO–FORM)

NET DEBT (R$ BI) NET DEBT / EBTDA (X)

ADDITIONAL CAPACITY

EBITDA adjusted in the last 12 months in 3Q17 does not include non-recurrent value of the acquisitions in participation in ViaQuatro and ViaRio (R$ 548.1 million). On such effects being excluded from EBITDA, the indicator Net Debt/EBITDA, in September 2017, would be of 2.4x.

5.9 6.3 6.3 7.2 7.0 6.9 6.6 7.6 7.6 7.9 8.1 9.6 9.8 10.4 10.7 12.4 13.0 13.9 13.3 14.410.8 12.0 11.8

7.0

ConsideringLaverage at 3.5x

4.6 4.73.9

4.4 4.55.1

4.3 4.6

3.7

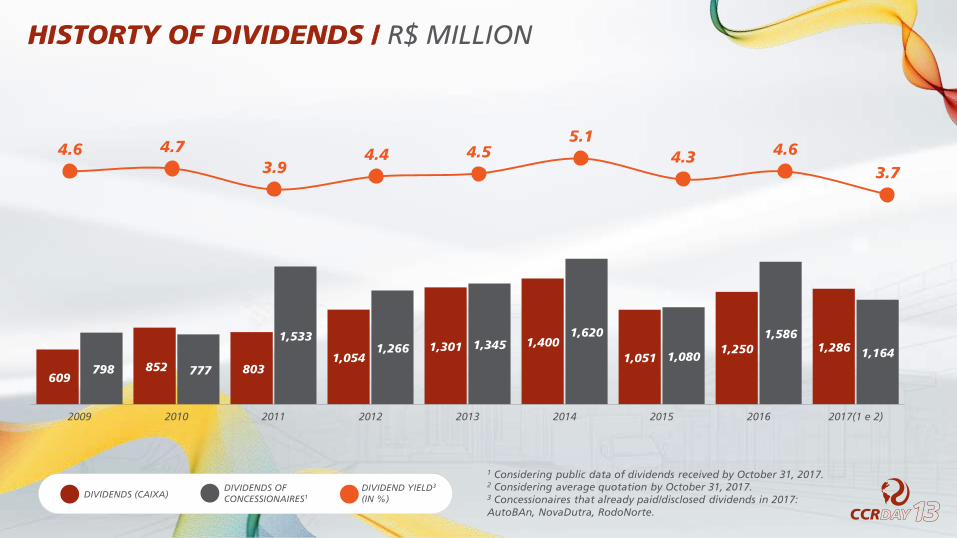

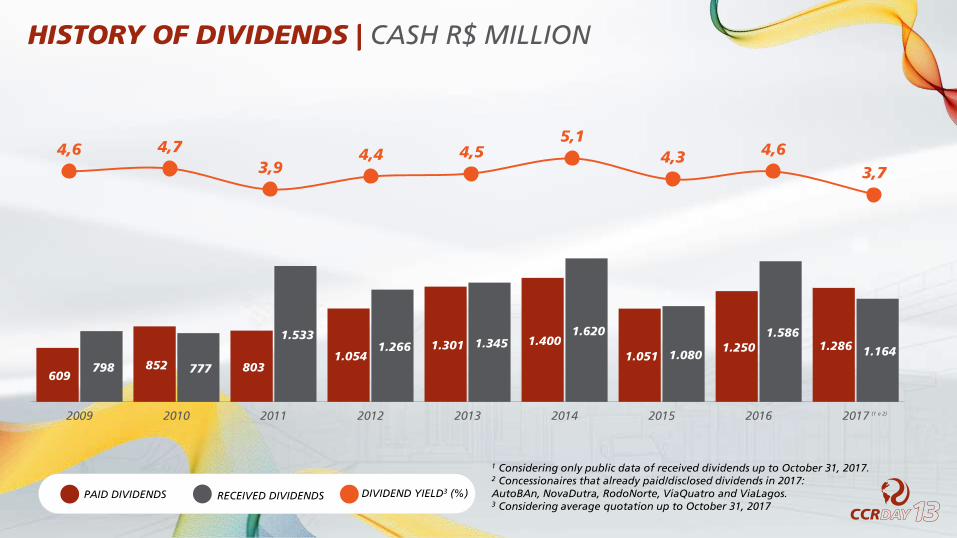

HISTORTY OF DIVIDENDS / R$ MILLION

DIVIDENDS OF CONCESSIONAIRES1

DIVIDEND YIELD3

(IN %)DIVIDENDS (CAIXA)

1 Considering public data of dividends received by October 31, 2017.2 Considering average quotation by October 31, 2017.3 Concessionaires that already paid/disclosed dividends in 2017:AutoBAn, NovaDutra, RodoNorte.

609 852 803

1,0541,301 1,400

1,0511,250 1,286

798 777

1,5331,266 1,345

1,620

1,080

1,586

1,164

2009 2010 2011 2012 2013 2014 2015 2016 2017(1 e 2)

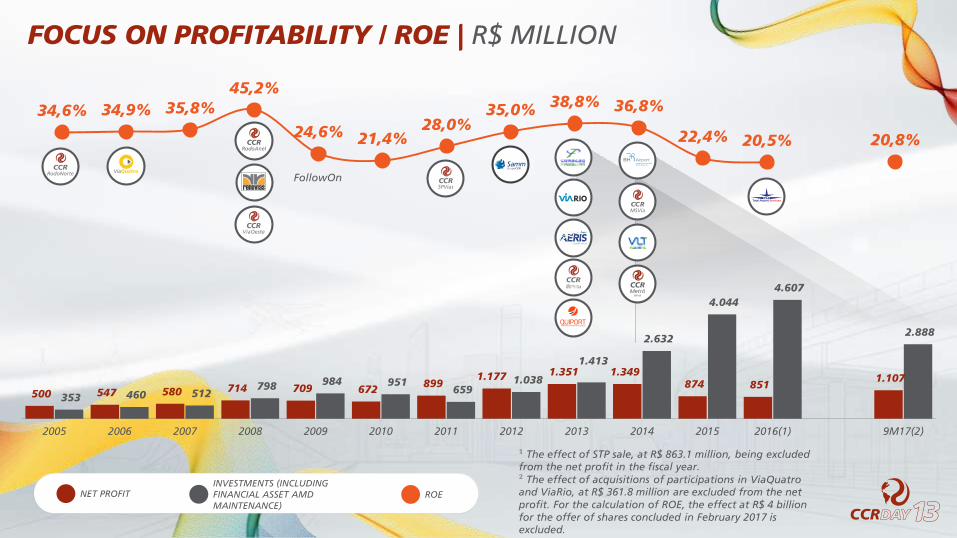

¹ The effect of STP sale, at R$ 863.1 million, being excluded from the net profit in the fiscal year. ² The effect of acquisitions of participations in ViaQuatroand ViaRio, at R$ 361.8 million are excluded from the net profit. For the calculation of ROE, the effect at R$ 4 billion for the offer of shares concluded in February 2017 is excluded.

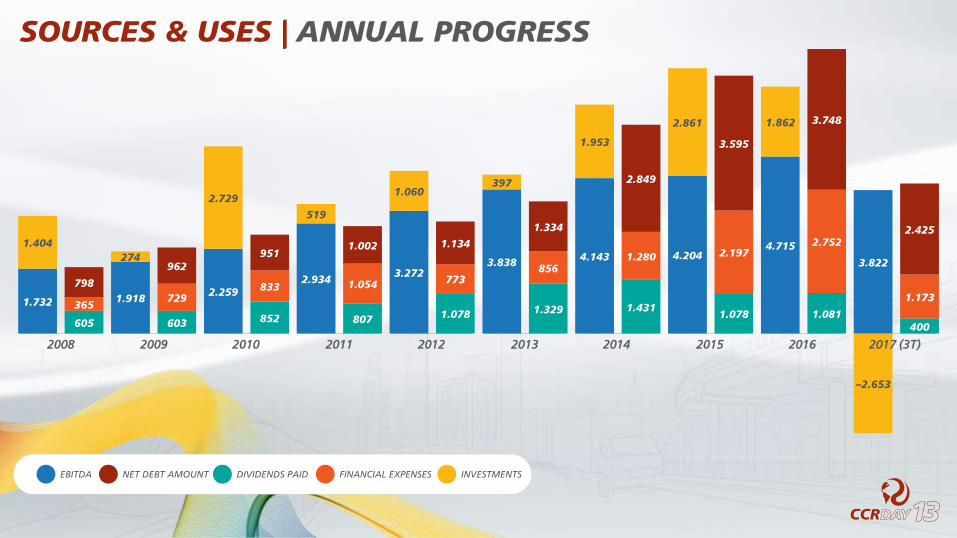

500 547 580 714 709 672 899 1.177 1.351 1.349

874 851 1.107

353 460 512 798 984 951

659 1.038

1.413

2.632

4.044 4.607

2.888

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016(1) 9M17(2)

34,6% 34,9% 35,8%45,2%

24,6% 21,4%28,0%

35,0% 38,8% 36,8%

22,4% 20,5% 20,8%

FollowOn

\

FOCUS ON PROFITABILITY / ROE | R$ MILLION

INVESTMENTS (INCLUDING FINANCIAL ASSET AMD MAINTENANCE)

ROENET PROFIT

16,5017,75 18,00

13,2511,25

13,75

8,75

10,75 11,00

7,25

10,00

11,75

14,25 13,75 13,75

7,50

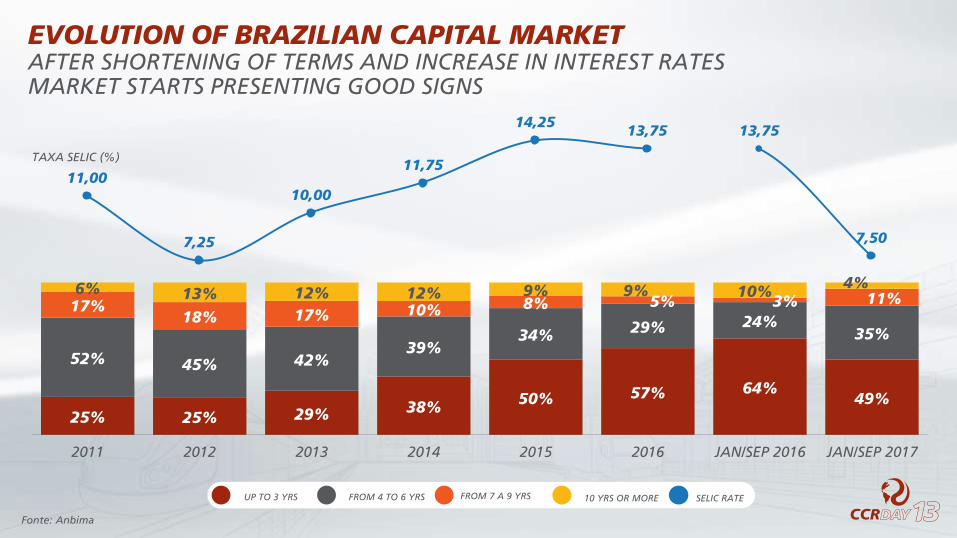

EVOLUTION OF BRAZILIAN CAPITAL MARKET TOTAL IN OFFERS IN FIXED REVENUE (R$ BI)

917 26

45 38 52 6494 101

130 117135

98 10561

86

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 9M16 9M17

Source: Anbima

SELIC RATE (%)

Fonte: Anbima

11,00

7,25

10,00

11,75

14,2513,75 13,75

7,50

UP TO 3 YRS FROM 4 TO 6 YRS FROM 7 A 9 YRS 10 YRS OR MORE SELIC RATE

25% 25% 29% 38% 50% 57% 64%49%

52% 45% 42%39%

34% 29% 24%35%

17%18% 17% 10% 8% 5% 3% 11%

6% 13% 12% 12% 9% 9% 10% 4%

2011 2012 2013 2014 2015 2016 JAN/SEP 2016 JAN/SEP 2017

TAXA SELIC (%)

EVOLUTION OF BRAZILIAN CAPITAL MARKET AFTER SHORTENING OF TERMS AND INCREASE IN INTEREST RATESMARKET STARTS PRESENTING GOOD SIGNS

Interest rateTJLP + 1.5%

+ up to 4.18%

TJLP + 1,2% + 0,4% up to

4,86%

TJLP + 1.2%+ up to 4.18%

% maximum financiable3 70% 70% 70%

Maximum term of

financing (years)

20 - 30

According to the capacity

of the project4

20

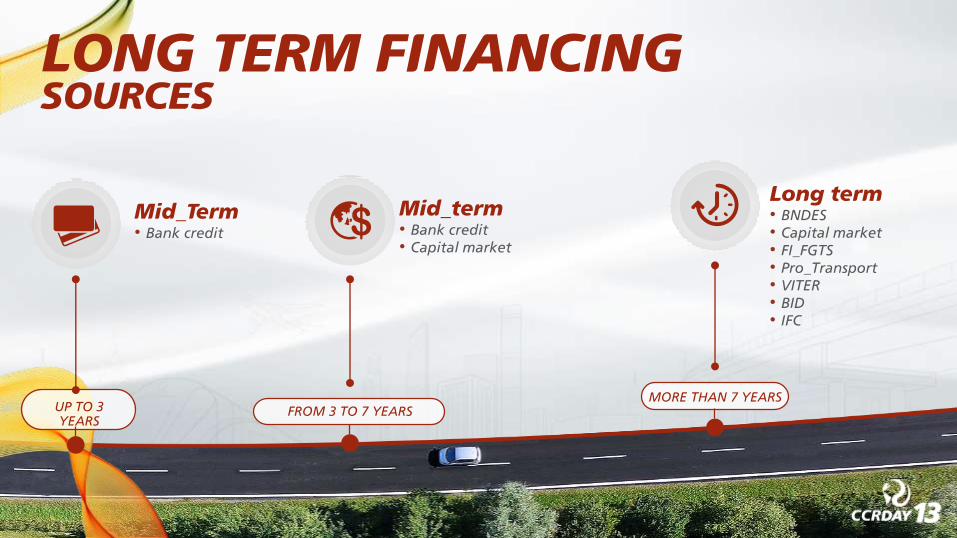

LONG TERM FINANCING

TJLP + 1.7% + + 0,4% up to

4,86%

TJLP + 1.7% + 0,4% up to

4,86%

TJLP + 1.7% + 0,4% up to

4,86%

50% 80% 40%

15 30 15

1 In the period of contracting financing of: CCR MSVia, CCR Metrô Bahia, VLT and BH Airport.2 For structural projects in public transportation of médium and high capacity. 3 For the 1st cycle of investments. 4 CCR Metrô Bahia = 30 years and VLT = 20 years.

\

PREVIOUS CONDITIONS1 TODAY

ROADS MOBILITY2 AIRPORTS ROADS MOBILITY2 AIRPORTS

UP TO 3 YEARS

FROM 3 TO 7 YEARSMORE THAN 7 YEARS

Mid_Term• Bank credit

Mid_term• Bank credit• Capital market

Long term• BNDES• Capital market• FI_FGTS• Pro_Transport• VITER • BID• IFC

LONG TERM FINANCINGSOURCES

FINAL MESSAGEAfter the cycle of relevant investments... ... and poor drecit secanrio with high interest rates,CCR kept focus:

Clear strategy

Multiple oppportunities => Selectivity

Discipline of capital

Sufficient use of balance

Concrete invetsments in new projects

WE BELIEVE THAT CCR IS READY TO A NEW CYCLEOF INVESTMENTS, WITH RELEVANT CAPACITY FOR LEVERAGEAND SOUND POSITION OF CASH AFTER FOLLOW–ON

RENATO VALECLOSING

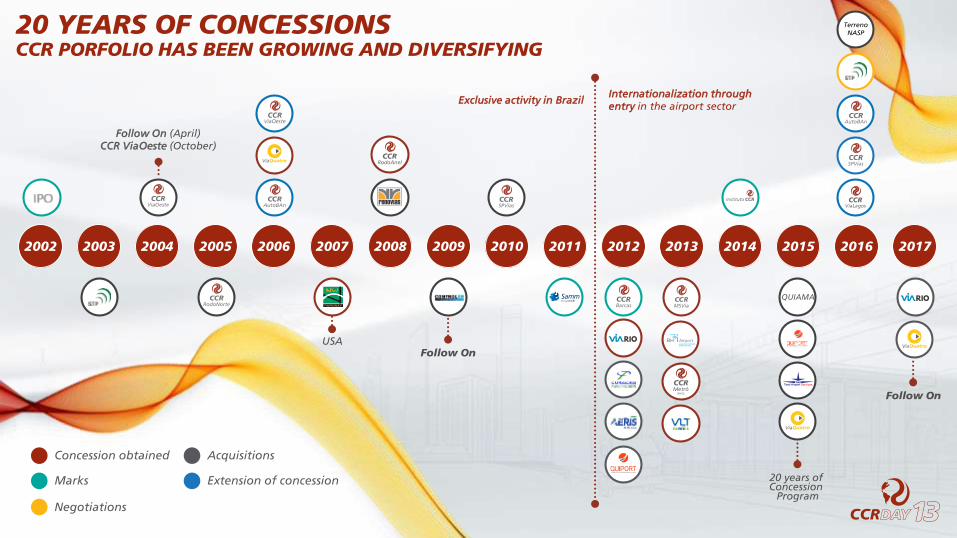

Concession obtained

Marks

Acquisitions

Extension of concession

Negotiations

20032002 2007

USA

2005 201020082006 20112004

Follow On (April)CCR ViaOeste (October)

2009

Follow On

Internationalization through entry in the airport sector

Exclusive activity in Brazil

20142013

\

2012 2015

20 years of Concession

Program

QUIAMA

2016 2017

TerrenoNASP

Follow On

20 YEARS OF CONCESSIONS CCR PORFOLIO HAS BEEN GROWING AND DIVERSIFYING

4,6 4,73,9

4,4 4,55,1

4,3 4,6

3,7

HISTORY OF DIVIDENDS | CASH R$ MILLION

RECEIVED DIVIDENDS DIVIDEND YIELD3 (%)PAID DIVIDENDS

1 Considering only public data of received dividends up to October 31, 2017. 2 Concessionaires that already paid/disclosed dividends in 2017:AutoBAn, NovaDutra, RodoNorte, ViaQuatro and ViaLagos.3 Considering average quotation up to October 31, 2017

609 852 803

1.054 1.301 1.400

1.051 1.250 1.286

798 777

1.533 1.266 1.345

1.620

1.080

1.586

1.164

2009 2010 2011 2012 2013 2014 2015 2016 2017 (1 e 2)

1.732 1.9182.259

2.9343.272

3.838 4.143 4.2044.715

3.822

1.404274

2.729

519

1.060397

1.953

2.861 1.862

–2.653

605 603 852 807 1.078 1.329 1.4311.078 1.081

400

365729

833 1.054 773856

1.280 2.1972.752

1.173798

962951

1.002 1.134

1.334

2.849

3.595

3.748

2.425

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 (3T)

SOURCES & USES | ANNUAL PROGRESS

EBITDA NET DEBT AMOUNT DIVIDENDS PAID FINANCIAL EXPENSES INVESTMENTS

Capital Discipline

Qualified Growth

Management of people Sustainability

Corporate Governance

PILLARS FOR GROWTH

Opportunities to collaborators working with creation of divisions and internal adjustments

Remuneration reserach to check competitiveness in the market

MANAGEMENT OF PEOPLE

Assessment of executives and management personnel with definition of new competences, engaging in the challenges of the company

Organizational Culture research for new initiatives on improvement and recognition of the Atmosphere and Culture

PILLARS FOR GROWTH

Qualified Growth

Management of people Sustainability

Corporate Governance

Capital Discipline

FOCUS ON ACTUATION

As key element in social investment strategy of CCR Group, the Institute currently directly engages in planning and monitoring of the initiatives supported by the Group, including those resulting from tax incentives

Health and quality of life

Education and Citizenship

Environment and road safety

Culture and Sports

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

13 years

R$ 187 million

DIRECT AND INCENTIVATED INVESTMENTS

PILLARS FOR GROWTH

Qualified Growth

Management of people Sustainability

Corporate Governance

Capital Discipline

Partners with the same objective and view

All partners are minority

Constant seek for consensual

decision

Interest in CCR above all partners interests

Participative style intense

dialogues

CCR GOVERNANCE FACTORS OF SUCESS IN

Dedicated advisors experts in the business

Balance of interests:

shareholder vs. user vs. granting authority

Business model with shared

management

Right people in the right

places

Management with market recognition

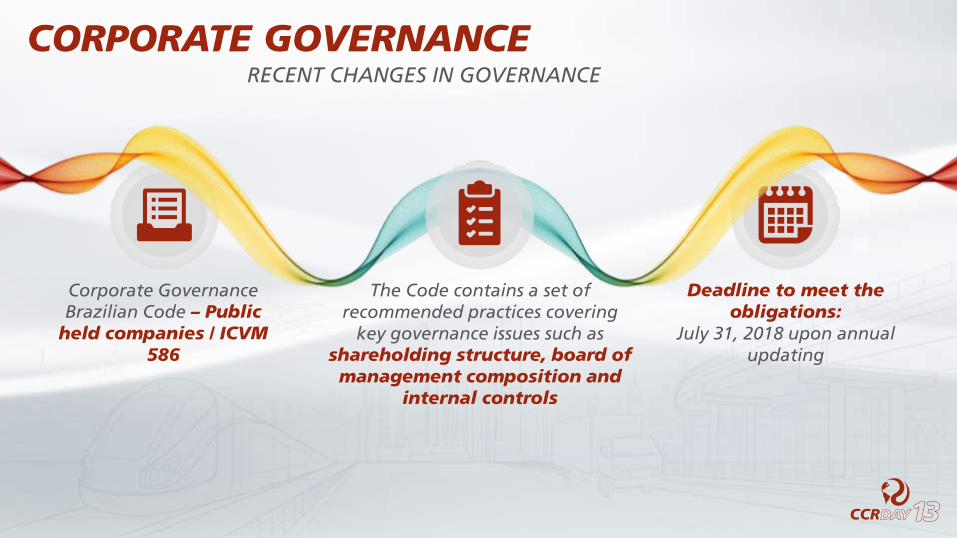

CORPORATE GOVERNANCE RECENT CHANGES IN GOVERNANCE

Corporate Governance Brazilian Code – Public

held companies / ICVM 586

The Code contains a set of recommended practices covering

key governance issues such as shareholding structure, board of management composition and

internal controls

Deadline to meet the obligations:

July 31, 2018 upon annual updating

CAD, CEO and Board of Directors assessment with disclosure of the assessment process in the Reference Form

OPA (Public Offer of Shares) for relevant participation

Compulsory disclosure of report on environmental, company and corporate governance information

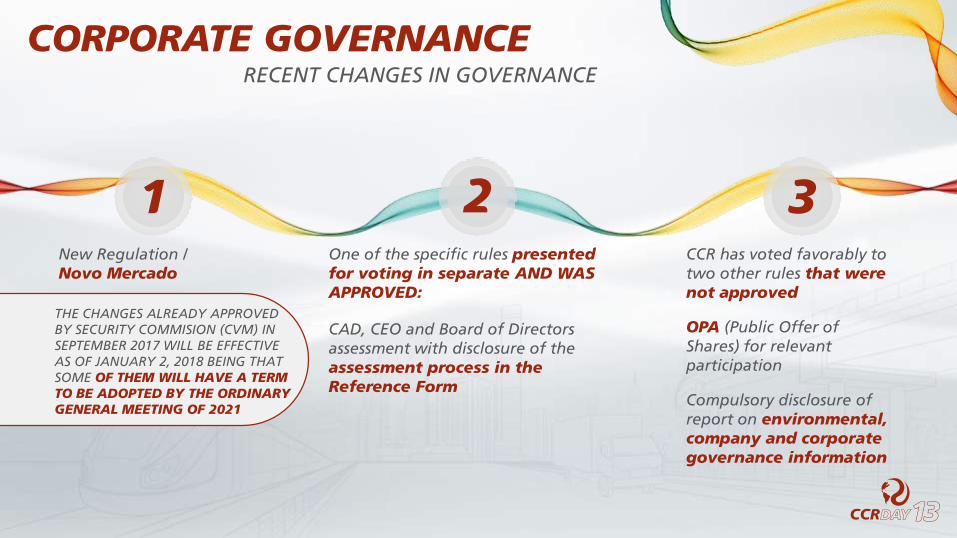

THE CHANGES ALREADY APPROVED BY SECURITY COMMISION (CVM) IN SEPTEMBER 2017 WILL BE EFFECTIVE AS OF JANUARY 2, 2018 BEING THAT SOME OF THEM WILL HAVE A TERM TO BE ADOPTED BY THE ORDINARY GENERAL MEETING OF 2021

1 2 3New Regulation /Novo Mercado

One of the specific rules presented for voting in separate AND WAS APPROVED:

CCR has voted favorably to two other rules that were not approved

CORPORATE GOVERNANCE RECENT CHANGES IN GOVERNANCE

REGULATIONS CADCOMMITTEES FISCAL BOARD

POLICIES FOR APPOINTMENT OF MEMBERS

POLICIES ON RISK MANAGEMENT

POLICIES FOR TRANSACTIONS WITH RELATED PARTIES

POLICIES FOR NEGOTIATION OF SECURITIES

CODE OF CONDUCT AND CLEAN-COMPANY POLICIES

UPDATED BYLAWS

1

2 5

6

7

8

AS OF 2021, THE CRAETION OR DISCLOSURE OF THE MATTERS AND RULES THAT FOLLOWS IS ENVISAGED

CORPORATE GOVERNANCE

REMUNERATION POLICIES3

4

NEW + DISCLOSURE

IMPROVEMENT + DISCLOSURE

IMPROVEMENT UPDATING

This is CCR keeping high governance level to which its shareholders are used

CCR has decided to promptly implement all obligations set

Brazilian Code for Corporate Governance – Public held companies

Regulation of Novo Mercado

Including all rules the deadline to be implemented is 2021

Considering that is has voted favorably to two measures that were not approved, CCR will also implement them

• OPA for relevant participation • Compulsory disclosure of report with

environmental, social and corporate governance information

CORPORATE GOVERNANCE

WHYINVEST IN CCR?

Clear, well defined and public strategy

Access to capital market

Controlling shareholders with the same objectives and view

Strong dividends policy

Qualified collaborators constantly developing

Inserted in markets with upside potential

Sound financial structure

Qualified growth and sustainable development

VIDEO 7 / INFRAESTRUTURA EM MOVIMENTO

QUESTIONS AND ANSWERS

LUNCH

Top Related