Languages

Pages

Legal

Published under the Creative Commons Licence

[Attribution, Non-Commercial, Share-Alike],

for details see www.creativecommons.org

Community Currency Implementation Framework

Version: November 2013

This Community Currency Implementation Framework has been produced by Qoin, Spice and the New Economics Foundation. It is part of the Community Currencies in Action (CCIA) partnership. The CCIA partnership leads the way in sharing knowledge and best practice on professional Community Currencies that enable vibrant and prosperous communities. It designs, develops and implements Community Currencies across North West Europe. And it provides a rigorously package of support structures to facilitate the development of Community Currencies and promote Community Currencies as a credible (policy) vehicle for achieving positive outcomes. CCIA is part funded through INTERREG IVB North West Europe (NWE), a financial instrument of the EU’s Cohesion Policy - Investing in Opportunities. For more information, see: www.communitycurrenciesinaction.eu

This framework is created by the Community Currencies in Action Project: www.ccia.eu

Compiled by:

– Qoin www.qoin.org (Edgar Kampers and Rob van Hilten)

– Spice www.justaddspice.org (Becky Booth)

– The New Economics Foundation www.neweconomics.org (Leander Bindewald)

Building on the contributions from:

– Social Trade Organisation www.socialtrade.org (Henk van Arkel)

– Arthur Brock www.lifeblooddesign.com

– John Rogers www.valueforpeople.co.uk

– Bernard Lietaer www.lietaer.com and Gwendolyn Hallsmith

– MonNetA www.monneta.org (Ludwig Schuster)

– Scott Morris www.mylocal.coop

– Community Forge www.communityforge.net (Tim Anderson)

If you change or add elements, or build your own version of this framework, we kindly request you to send your changes or suggestions to [email protected]. This allows us to add your insights to this framework.

Community Currency Implementation Framework

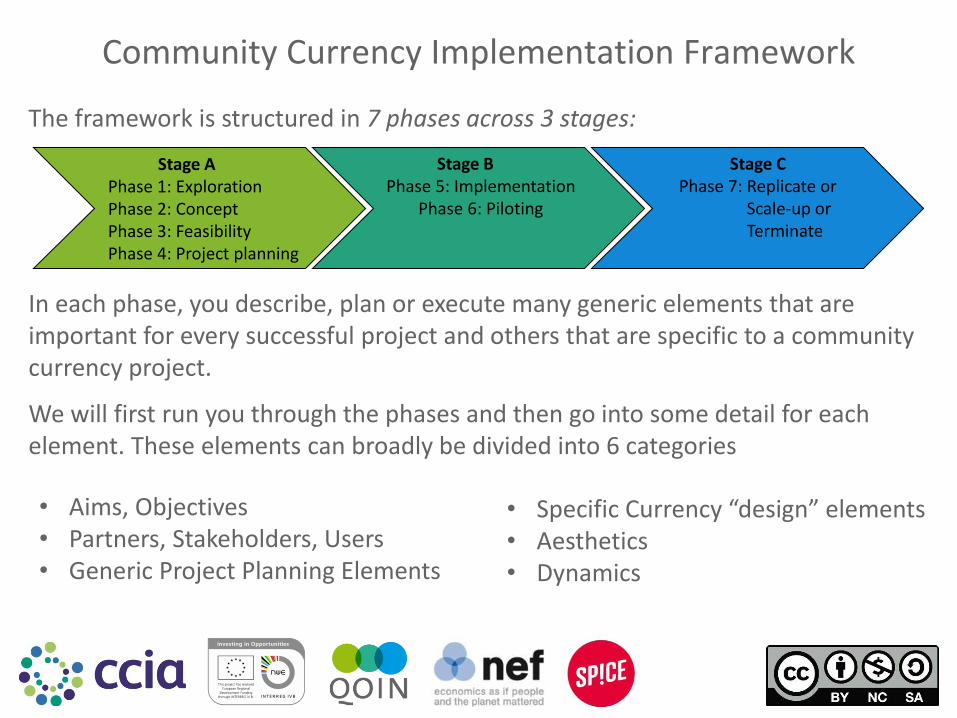

In each phase, you describe, plan or execute many generic elements that are important for every successful project and others that are specific to a community currency project.

We will first run you through the phases and then go into some detail for each element. These elements can broadly be divided into 6 categories

Stage A Phase 1: Exploration Phase 2: Concept Phase 3: Feasibility Phase 4: Project planning

Stage B Phase 5: Implementation

Phase 6: Piloting

Stage C Phase 7: Replicate or Scale-up or Terminate

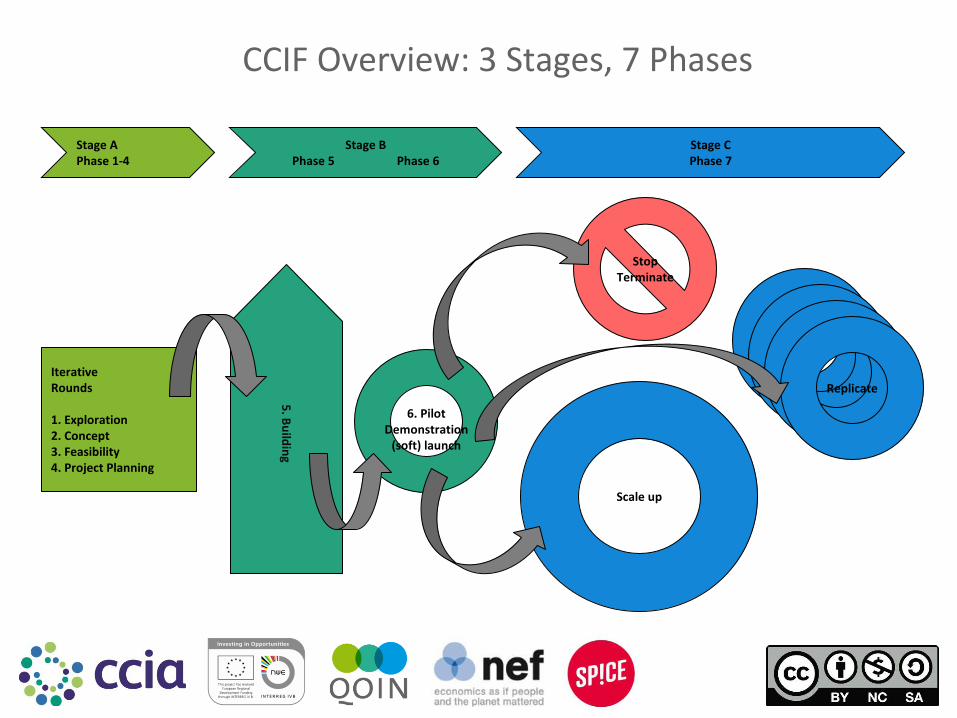

The framework is structured in 7 phases across 3 stages:

Community Currency Implementation Framework

• Specific Currency “design” elements • Aesthetics • Dynamics

• Aims, Objectives • Partners, Stakeholders, Users • Generic Project Planning Elements

5. B

uild

ing

Iterative Rounds 1. Exploration 2. Concept 3. Feasibility 4. Project Planning

Stop Terminate

6. Pilot

Demonstration (soft) launch

Replicate

Scale up

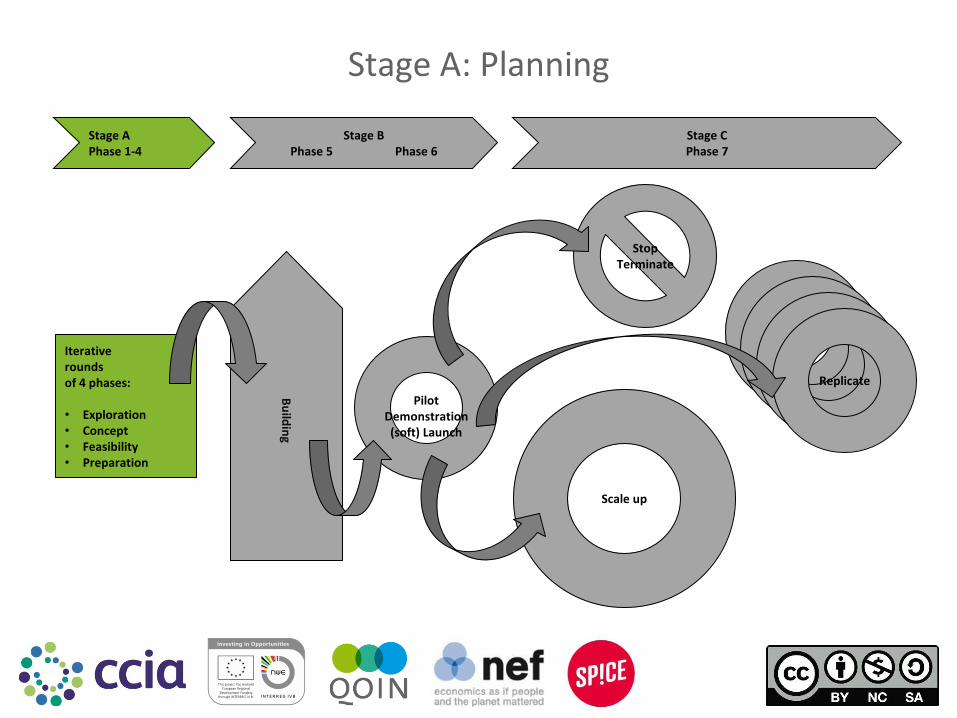

Stage A Phase 1-4

Stage B Phase 5 Phase 6

Stage C Phase 7

CCIF Overview: 3 Stages, 7 Phases

Stage A: Planning

Bu

ildin

g

Iterative rounds of 4 phases: • Exploration • Concept • Feasibility • Preparation

Stop Terminate

Pilot

Demonstration (soft) Launch

Replicate

Scale up

Stage A Phase 1-4

Stage B Phase 5 Phase 6

Stage C Phase 7

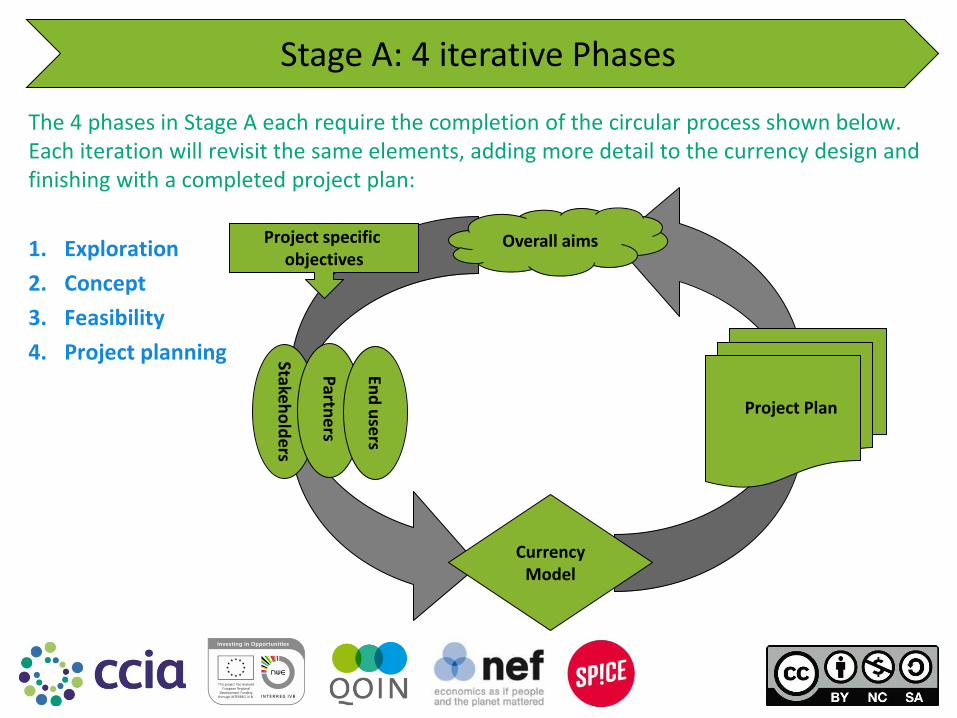

The 4 phases in Stage A each require the completion of the circular process shown below. Each iteration will revisit the same elements, adding more detail to the currency design and finishing with a completed project plan:

1. Exploration

2. Concept

3. Feasibility

4. Project planning

Stage A: 4 iterative Phases

Overall aims

Project Plan

Stakeh

old

ers

Project specific objectives

Partn

ers

End

use

rs

Currency Model

Stage A – Phase 1: Exploration

- What should we start with? – Create initial overall aims & potential objectives

– Map the potential end-users & partners

– Sketch the currency model

– Estimate the costs and prepare project plan

– Get commitment from initiator to move to the next phase

- Deliverables: – Exploration 1 pager + presentation with draft flow diagram

– Plan for Concept Phase

Stage A – Phase 2: Concept

- What will the currency project look like? – Invite end-users & partners to help with the design process

– Find common base between stakeholders. Collectively describe overall aims & SMART objectives.

– Who is missing? Detailed description of end-users & partners

– Describe the concept of the currency model and start to map specific elements

– Describe the generic project elements

– Identify feasibility issues for next phase

– Create milestone plan, funding overview, implementation brainstorm

– Get commitment for next phase

- Deliverables: – Concept 5-pager + presentation with flow diagram

– Plan for Feasibility Phase

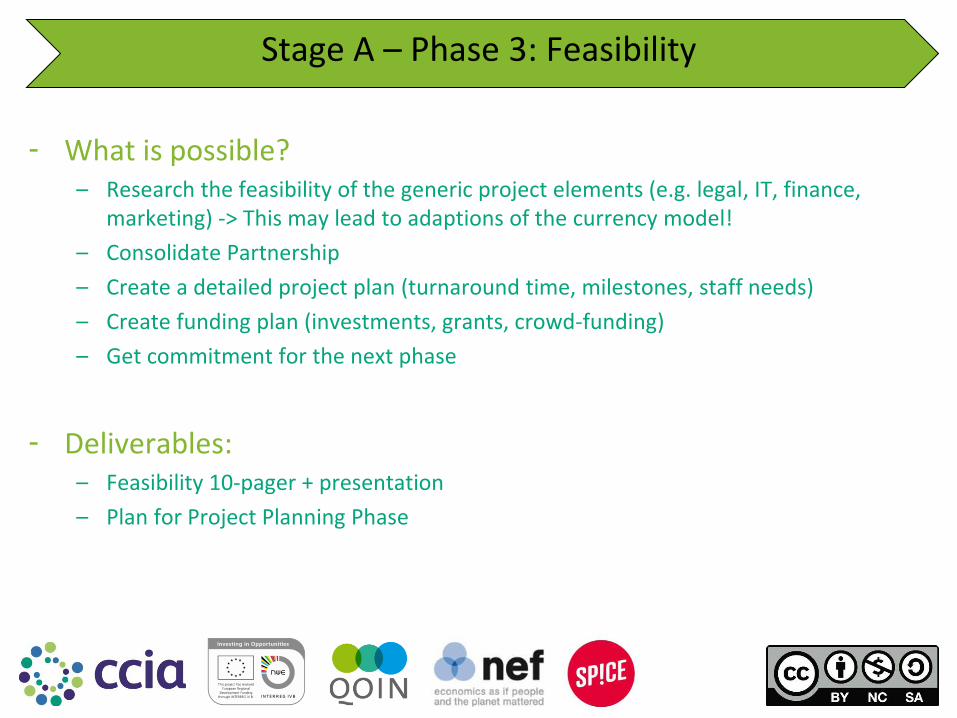

Stage A – Phase 3: Feasibility

- What is possible? – Research the feasibility of the generic project elements (e.g. legal, IT, finance,

marketing) -> This may lead to adaptions of the currency model!

– Consolidate Partnership

– Create a detailed project plan (turnaround time, milestones, staff needs)

– Create funding plan (investments, grants, crowd-funding)

– Get commitment for the next phase

- Deliverables: – Feasibility 10-pager + presentation

– Plan for Project Planning Phase

Stage A – Phase 4: Project Planning

- What is needed to start implementing? – Finalise full project implementation plan

– Realization + production + output planning

– Get the partnership agreement signed

– Recruit staff to run the operational organisation

– Create initiation pack for target area/group/market

– Secure funding

– Ensure everything is ready, and what is the contingency plan?

- Deliverables:

– Detailed project implementation plan + presentation

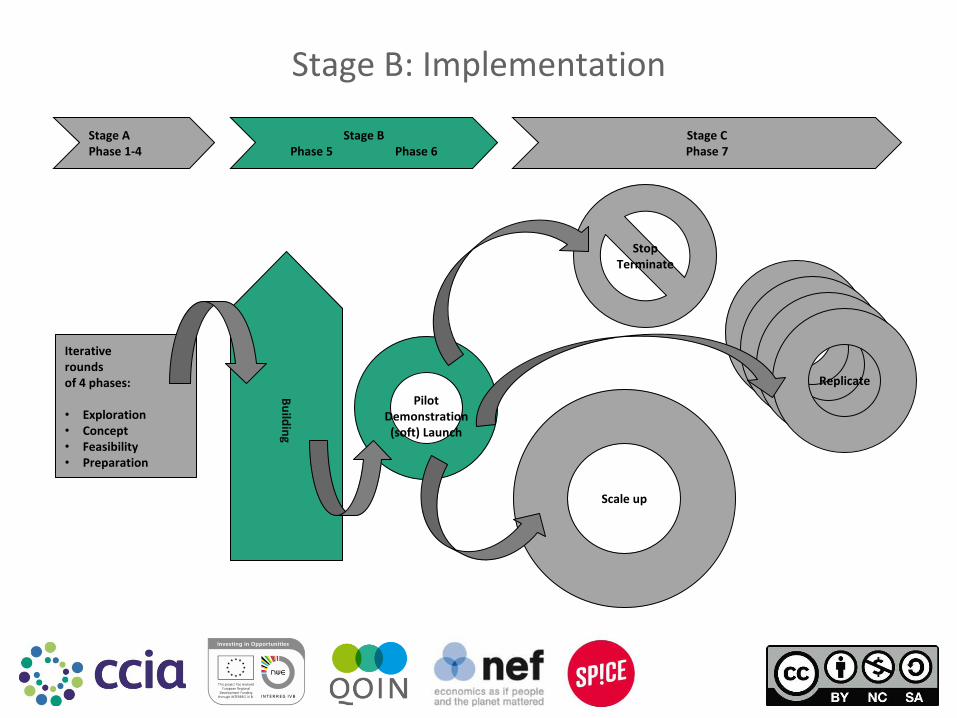

Stage B: Implementation

Bu

ildin

g

Iterative rounds of 4 phases: • Exploration • Concept • Feasibility • Preparation

Stop Terminate

Pilot

Demonstration (soft) Launch

Replicate

Scale up

Stage A Phase 1-4

Stage B Phase 5 Phase 6

Stage C Phase 7

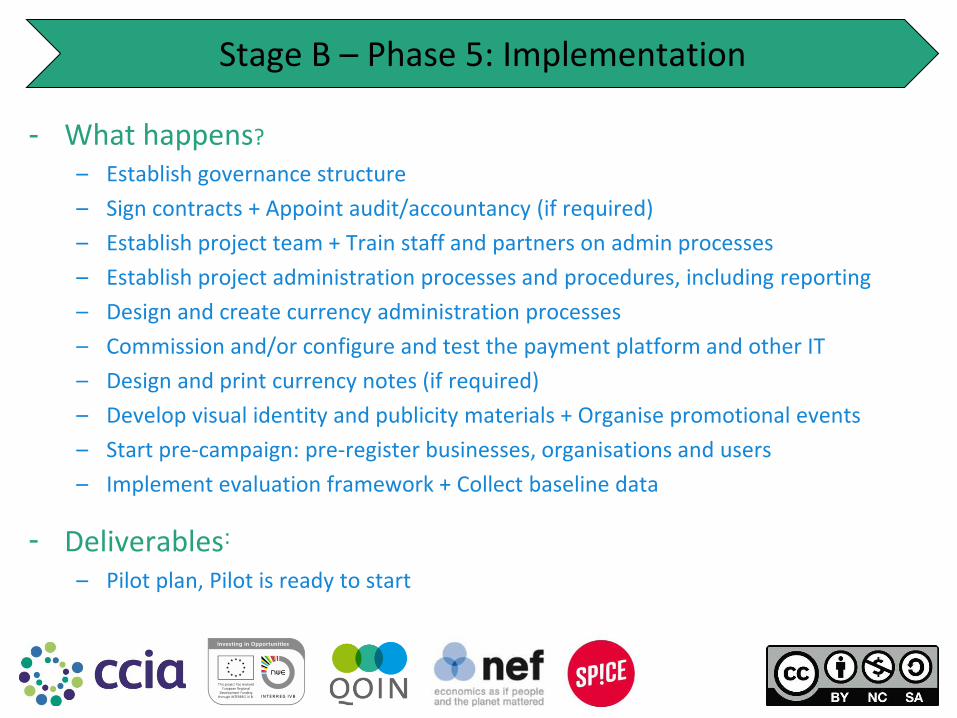

- What happens?

– Establish governance structure

– Sign contracts + Appoint audit/accountancy (if required)

– Establish project team + Train staff and partners on admin processes

– Establish project administration processes and procedures, including reporting

– Design and create currency administration processes

– Commission and/or configure and test the payment platform and other IT

– Design and print currency notes (if required)

– Develop visual identity and publicity materials + Organise promotional events

– Start pre-campaign: pre-register businesses, organisations and users

– Implement evaluation framework + Collect baseline data

- Deliverables:

– Pilot plan, Pilot is ready to start

Stage B – Phase 5: Implementation

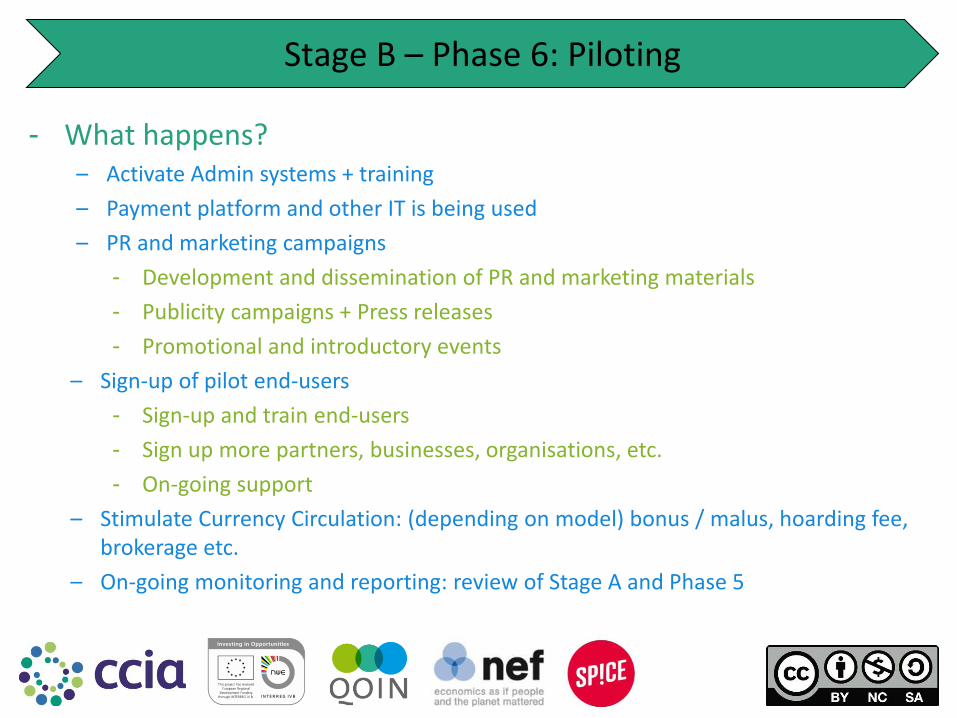

- What happens? – Activate Admin systems + training

– Payment platform and other IT is being used

– PR and marketing campaigns

- Development and dissemination of PR and marketing materials

- Publicity campaigns + Press releases

- Promotional and introductory events

– Sign-up of pilot end-users

- Sign-up and train end-users

- Sign up more partners, businesses, organisations, etc.

- On-going support

– Stimulate Currency Circulation: (depending on model) bonus / malus, hoarding fee, brokerage etc.

– On-going monitoring and reporting: review of Stage A and Phase 5

Stage B – Phase 6: Piloting

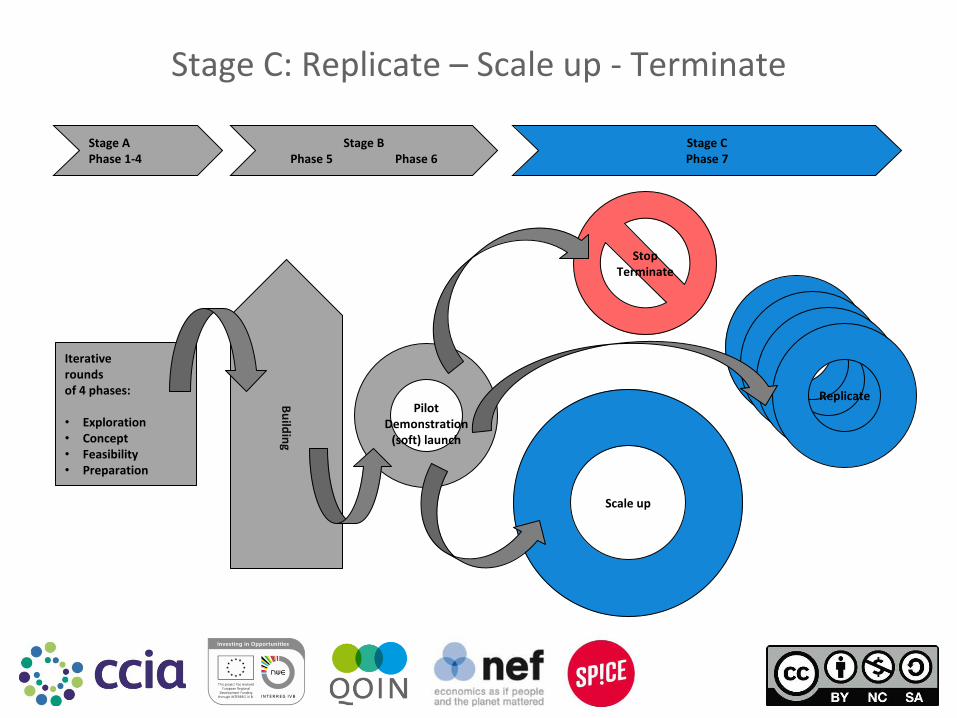

Stage C: Replicate – Scale up - Terminate

Bu

ildin

g

Iterative rounds of 4 phases: • Exploration • Concept • Feasibility • Preparation

Stop Terminate

Pilot

Demonstration (soft) launch

Replicate

Scale up

Stage A Phase 1-4

Stage B Phase 5 Phase 6

Stage C Phase 7

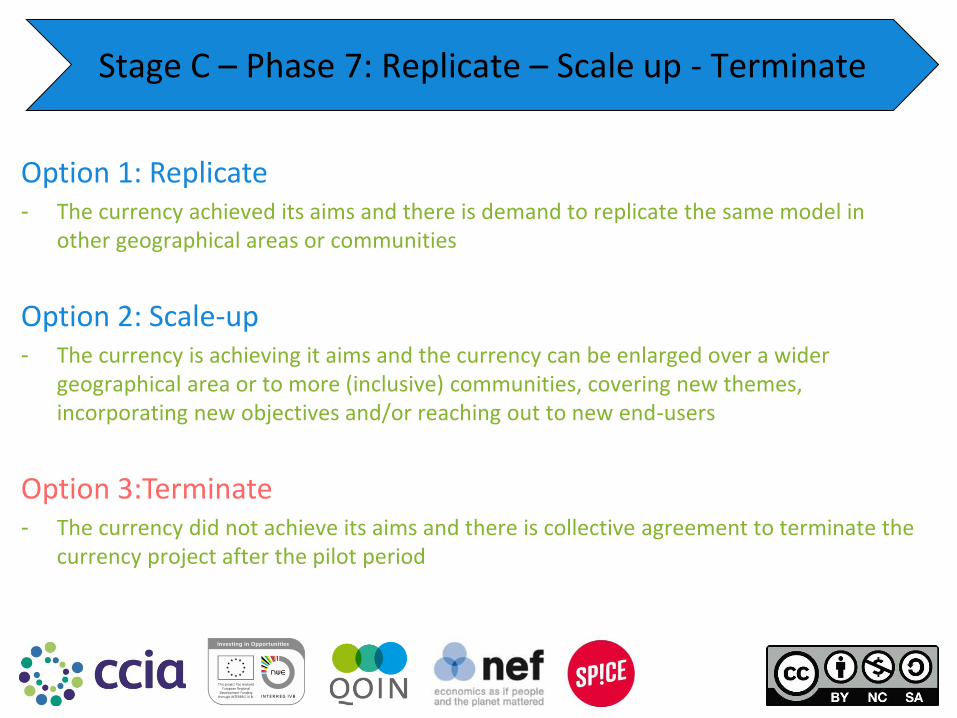

Option 1: Replicate - The currency achieved its aims and there is demand to replicate the same model in

other geographical areas or communities

Option 2: Scale-up - The currency is achieving it aims and the currency can be enlarged over a wider

geographical area or to more (inclusive) communities, covering new themes, incorporating new objectives and/or reaching out to new end-users

Option 3:Terminate - The currency did not achieve its aims and there is collective agreement to terminate the

currency project after the pilot period

Stage C – Phase 7: Replicate – Scale up - Terminate

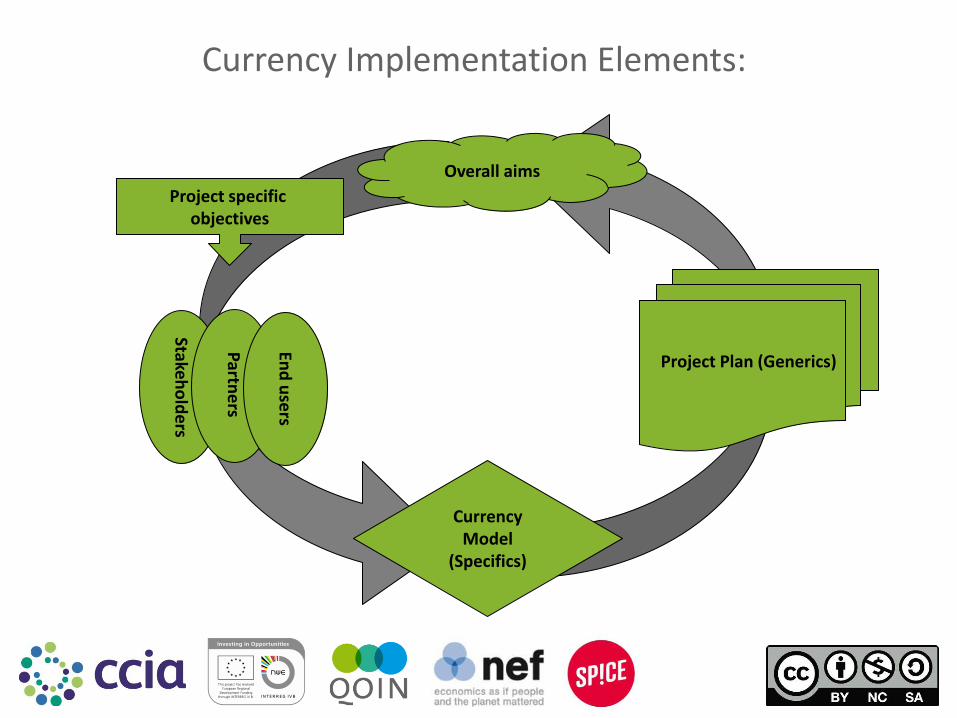

Currency Implementation Elements:

Overall aims

Project Plan (Generics)

Stakeh

old

ers

Project specific objectives

Partn

ers

End

use

rs

Currency Model

(Specifics)

Currency Implementation Elements:

Aims, Objectives – the elements describe the high level ambitions and set currency objectives

Users, Partners, Other stakeholders – the elements clarify who is involved, what they need and what they should do

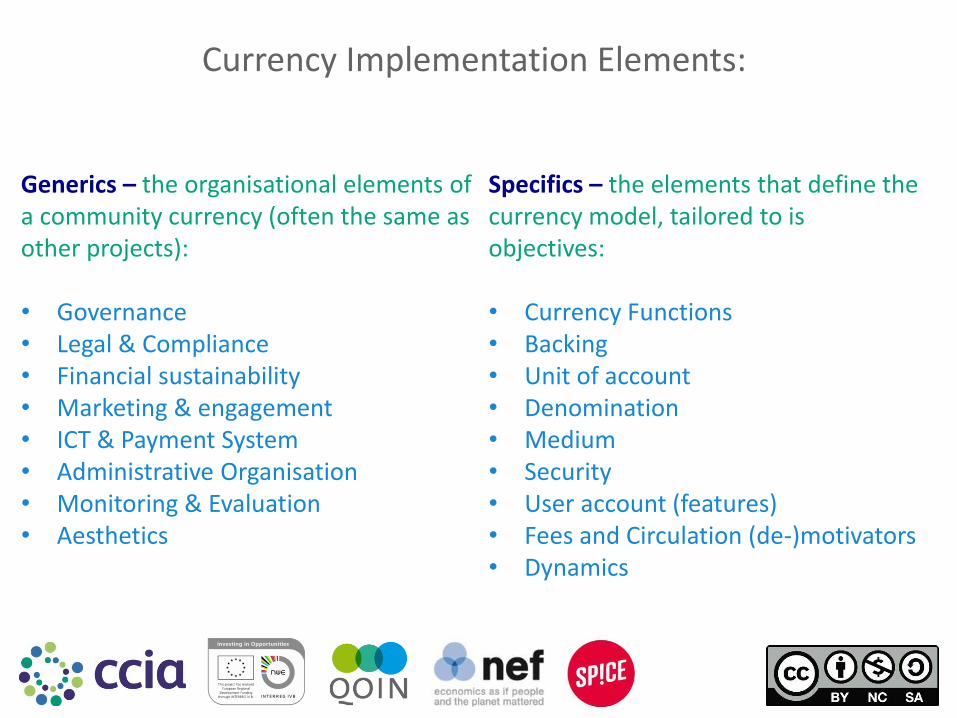

Generics – the organisational elements of a community currency (often the same as other projects)

Specifics – the elements that define the currency model, tailored to its objectives

Currency Implementation Elements:

Generics – the organisational elements of a community currency (often the same as other projects): • Governance • Legal & Compliance • Financial sustainability • Marketing & engagement • ICT & Payment System • Administrative Organisation • Monitoring & Evaluation • Aesthetics

Specifics – the elements that define the currency model, tailored to is objectives: • Currency Functions • Backing • Unit of account • Denomination • Medium • Security • User account (features) • Fees and Circulation (de-)motivators • Dynamics

Aims & Objectives: Overall Aims

“Overall aims” describe the high level ambitions: Examples: - Sustainable society and beautiful nature - Healthy people in strong communities

- Foster Innovation and strengthen regional economy

Or more granular general aims: Examples: - Support local SME + independent shops - Create regional value chains

- Social cohesion in my neighbourhood

- Local poverty alleviation

- Stimulate environmental friendly consumption - Promote green behaviour, or bio products

- Cleaner and greener transport

- Enlarge the cultural sector

- Promote sports and healthy living

Aims & Objectives : Project Specific Objectives

Concrete objectives are planned outcomes that need to be SMART: Specific, Measurable, Attainable, Relevant, and Timed

Examples:

- By 2016, we will have increased the use of local shops in locality XX by 25% as a

result of the new local currency

- At the end of the pilot period, 70% of members of our pilot currency will report

that their social networks increased as a result of participating the project

- By Q3 2016, recycling in city YY will have increased by 15% as a result of

introducing a new green points scheme

- By 2017, use of greener transport using our currency will have increased by 10%

- By April 2018, 70% of cultural venues in City Y will report a more diverse

audience base

- In two years time, 60% of participants of currency Y will report that they take part

in sport and leisure activities using currency Z

Partners, Stakeholders, Users: End Users

End users are the primary target group of the CC: The ones using the service. They can be members, citizens or customers of the implementing organisations

Examples:

– SMEs

– Innovative companies

– Unemployed

– Children

– The elderly

– Disabled people

– Cultural Creatives

– Consumers / Citizens

– Employees

Partners, Stakeholders, Users: Partners

Partners are the secondary target group. This diverse group can have different roles: part of the delivery team, funder, intermediary organisations, or ….

Examples:

– Business networks

– Employers

– Innovation stakeholders

– Municipalities

– Parents

– Governments

– Green NGOs and Business

– Insurance companies

– Services for the elderly / disabled

Partners, Stakeholders, Users: Other Stakeholders

Next to your partners, the other stakeholders are the tertiary target group. They are just as diverse. They are not directly involved as funder, delivery partner, client, etc. but they are or can be interested or connected to the CC and it outcomes

Examples:

– Authorities: Tax, social security, financial compliancy, ...

– Subcontractors: IT companies, service desks, …

– Media: web, TV, radio, print

– Academics

– NGOs with a stake

– Funders, subsidies, ...

– Competing systems and models, …

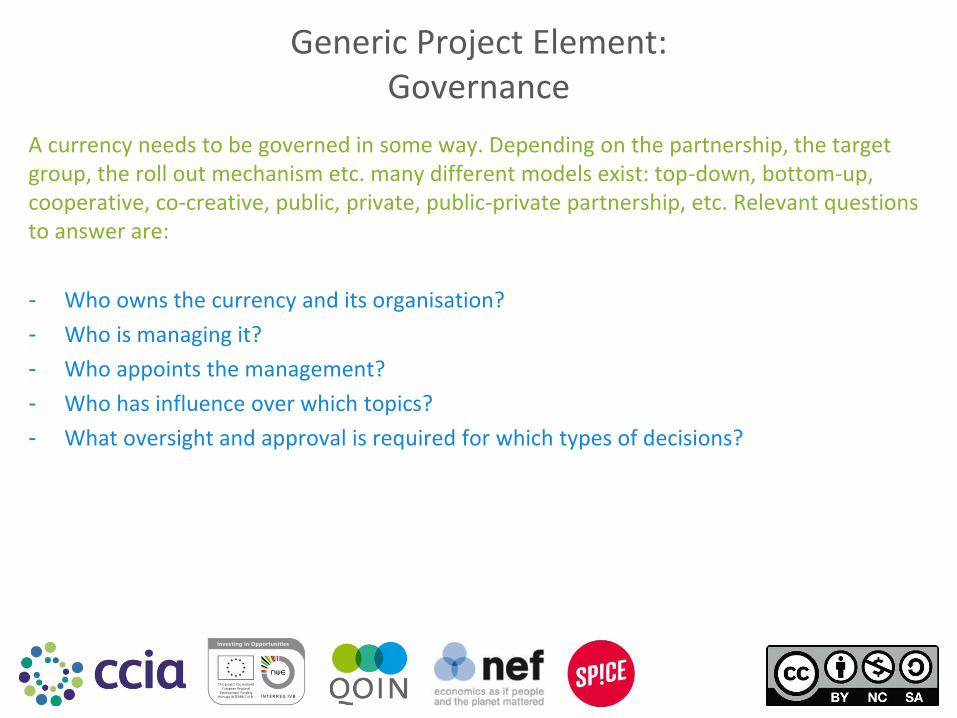

Generic Project Element: Governance

A currency needs to be governed in some way. Depending on the partnership, the target group, the roll out mechanism etc. many different models exist: top-down, bottom-up, cooperative, co-creative, public, private, public-private partnership, etc. Relevant questions to answer are:

- Who owns the currency and its organisation?

- Who is managing it?

- Who appoints the management?

- Who has influence over which topics?

- What oversight and approval is required for which types of decisions?

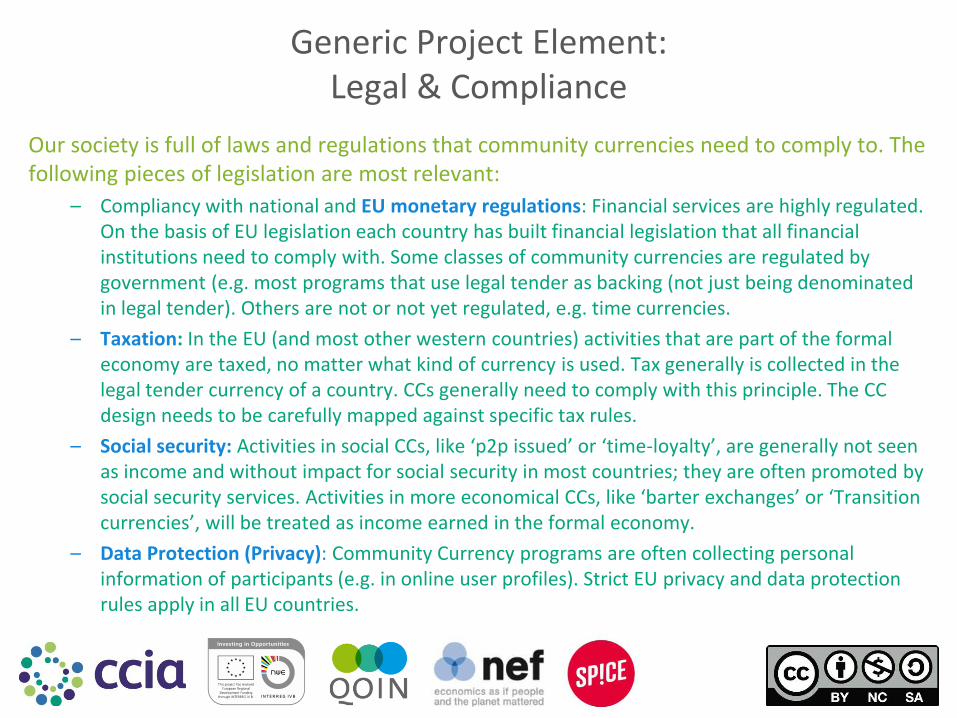

Generic Project Element: Legal & Compliance

Our society is full of laws and regulations that community currencies need to comply to. The following pieces of legislation are most relevant:

– Compliancy with national and EU monetary regulations: Financial services are highly regulated. On the basis of EU legislation each country has built financial legislation that all financial institutions need to comply with. Some classes of community currencies are regulated by government (e.g. most programs that use legal tender as backing (not just being denominated in legal tender). Others are not or not yet regulated, e.g. time currencies.

– Taxation: In the EU (and most other western countries) activities that are part of the formal economy are taxed, no matter what kind of currency is used. Tax generally is collected in the legal tender currency of a country. CCs generally need to comply with this principle. The CC design needs to be carefully mapped against specific tax rules.

– Social security: Activities in social CCs, like ‘p2p issued’ or ‘time-loyalty’, are generally not seen as income and without impact for social security in most countries; they are often promoted by social security services. Activities in more economical CCs, like ‘barter exchanges’ or ‘Transition currencies’, will be treated as income earned in the formal economy.

– Data Protection (Privacy): Community Currency programs are often collecting personal information of participants (e.g. in online user profiles). Strict EU privacy and data protection rules apply in all EU countries.

Generic Project Element: Legal (continued)

– General terms and conditions for users and partners: Community Currencies lead to all kinds of new relationships, responsibilities and obligations between users and partners. This can potentially lead to misunderstandings, complaints etc. General terms and conditions need to be tailor-made for each program.

– Insurance: Participating in a community currency can lead to changes in insurance coverage. In practice we know of 1 important example: in the Netherlands private liability insurances (e.g. which covers me as an individual if I damage somebody else’s property) does not cover activities for which any kind of reward, in this case community currency, is received. Additional insurance can therefore be required.

– Each community currency programme should further assess potential other pieces of legislation: examples are the consumers protection laws, money laundering legislation or the EU e-money directive.

– Internal constitution & by-laws need to adhere to appropriate ethical standards

– Liabilities to the organiser of the CC and legal disclaimers need to be considered

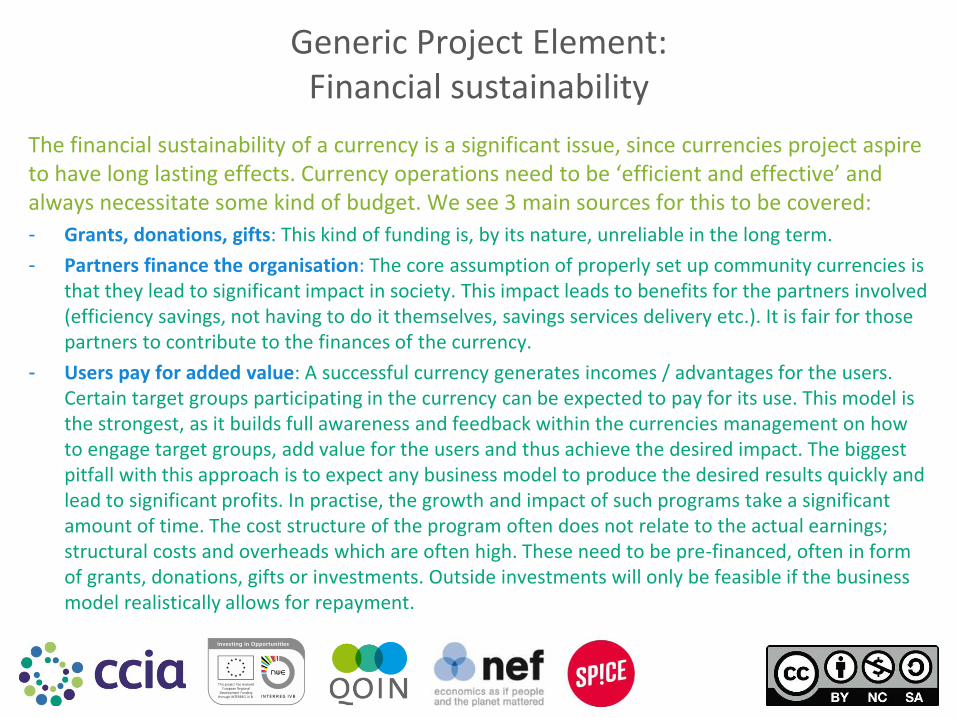

Generic Project Element: Financial sustainability

The financial sustainability of a currency is a significant issue, since currencies project aspire to have long lasting effects. Currency operations need to be ‘efficient and effective’ and always necessitate some kind of budget. We see 3 main sources for this to be covered:

- Grants, donations, gifts: This kind of funding is, by its nature, unreliable in the long term.

- Partners finance the organisation: The core assumption of properly set up community currencies is that they lead to significant impact in society. This impact leads to benefits for the partners involved (efficiency savings, not having to do it themselves, savings services delivery etc.). It is fair for those partners to contribute to the finances of the currency.

- Users pay for added value: A successful currency generates incomes / advantages for the users. Certain target groups participating in the currency can be expected to pay for its use. This model is the strongest, as it builds full awareness and feedback within the currencies management on how to engage target groups, add value for the users and thus achieve the desired impact. The biggest pitfall with this approach is to expect any business model to produce the desired results quickly and lead to significant profits. In practise, the growth and impact of such programs take a significant amount of time. The cost structure of the program often does not relate to the actual earnings; structural costs and overheads which are often high. These need to be pre-financed, often in form of grants, donations, gifts or investments. Outside investments will only be feasible if the business model realistically allows for repayment.

Generic Project Element: Financial sustainability (continued)

Most programs are a combination of the 3 options mentioned in the previous slide. Models that generate their own income are most complex. For such models additional relevant questions are:

- What services can we deliver to users/clients that actually help them on an individual basis: what's in it for them. What is our “Value Added”? These benefits need to matter to the clients themselves. More macro, philosophical, altruistic or social goals are important for individuals, too, but in practice very few are prepared to pay for them (except through collective channels like grand funding or government funding).

- What alternatives does a user/client have to get the same result. (e.g. to relax on a Saturday night I can choose to go to the cinema, the theatre, meet friends or go to a bar, all to the same effect.) Although such alternatives (like the cinema and a friend’s couch) are not direct competitors, they fulfil the same need and thus co-determine the margins that a program needs to operate in.

Generic Project Element: Marketing & Engagement

Marketing describes how the users and stakeholders will experience your organisation and what results they expect. Traditional marketing is divided by the 4-P approach:

- Product: is the product or service, how does it work, how does it come into existence, what material is it made of (paper notes, digital platform, using an app etc.)

- Price: what does it cost to use it

- Place: where does the user get it; how is it distributed

- Promotion: how is the user/consumer informed (i) that the product exists, (ii) that (s)he would want to use it, (iii) how (s)he can get it (iv) how to use it and (v) what are the benefits for him/her

A massive part of our communications is handled through digital channels. The impact is big. Web portals nowadays cannot be left out and can be realised in a simple or complex fashion.

Generic Project Element: ICT & Payment System

This is the core system of managing (most) community currencies:

- Functionality: Ability to implement the chosen mechanics on the platform

- Connectivity: Ability of the platform to connect to other ICT systems that are used

Different standard packages exist, from simple solutions to advanced bank-grade solutions. Market leader Cyclos is used by several CCIA programs. Core functions for CC platforms are:

- Highly customisable software to implement currency mechanics

- Details of currencies, accounts, transactions

- Flexible profiles, users and user groups

- Marketplace functionality to list and match offers and requests

- Advanced admin roles

- Very open connectivity, while very secure

Generic Project Element: Other ICT

Security: Full security does not exist. Security needs to be designed to avoid and discourage fraud. Depending on the kind of project (a small social program versus a large program linked to legal tender money), the systems need to be less or more secure. Security can be expensive.

Scalability: The total of the ICT components need to be resilient to handle the projected size of the program. Small programs can work with simple software that runs on one computer. Larger programs need more robust solutions, in which more advanced software programs are deployed on a range of servers. Scalability can be expensive.

Increase efficiency by automatisation: This is another important area for CC platforms which often requires customization and integration. Qoin / nef developed a set off apps to complement Cyclos and increase functionality (PayPal integration, invoice generation & reports).

Assessing the ICT requirements, in combination with associated costs & actual needs for a currency to achieve its goals is a considerable task requiring specialised knowledge. We suggest you consult a professional.

Even when ICT is used to the max in managing a currency, manual procedures are ALWAYS required to ensure the proper working and integrity of any program. Ideally these are fixed routines which are executed at a fixed time at which data is collected, processed and evaluated. In practice, it is not financially feasible to automate all processes thus manual intervention are often needed (e.g. when approving specific kinds of membership, specific administrative steps, between two not integrated software systems). Monitoring integrity and mitigating potential risks are reasons to keep specific processes manual. The design of admin processes is specialist work and need to be properly balanced with ICT. Examples of manual processes are:

- Create new members - Goal: Registering program members - Trigger: New customers fill in registration form

- Top-up balance - Goal: Transferring credits to a community currency account - Trigger: Receiving deposits in the organization's external bank account

- Top-down balance - Goal: Exchanging CC back to € - Trigger: Receiving exchange payment on the system account

- Enable local tax payment - Goal: Allowing users to pay local taxes with CC - Trigger: Receiving payments to local government account

Generic Project Element: Administrative organisation + internal control

Generic Project Element: Monitoring & Evaluation

Currencies are used to realise significant, lasting impact on society. We can only know if this is achieved, by monitoring the programs’ progress and evaluate the results.

Each currency should be accompanied with a proper monitoring and evaluation process. For the CCIA project, the New Economics Foundation will develop an evaluation framework for community currencies.

The framework will focus on steps 1-3 of any impact assessment process:

- Clarify Objective

- Determine concrete target outcomes

- Derive indicators by which to measure outcomes

- Collect Data on indicators

- Evaluate data, and discount for dead-weight, attribution and displacement factors

- Document and share results

A research data-base for quantitative information about implemented community currencies will also be developed under CCIA. See www.CCIA.eu for details and updates.

Generic Project Element: Aesthetics

The “Look and Feel” of the Currency and its user interfaces.

The physical design can have a significant impact on the adoption of a particular currency. Depending on the currency design options that are being implemented you may need to consider some of the aesthetic elements below

- Design of the physical currency

- Design of a payment card

- Design of the payment terminal

All of these can be an opportunity to highlight local people who have achieved great things and start to build community cohesion and pride.

Currency Specific Element: Currency Functions

Primary currency functions: - Unit of Account (measuring the value of goods and services)

- Medium of Exchange - purchase function (buying goods and services)

- Store of Value (saving for the future)

Secondary currency functions: - Gift (give CC to a needy person)

- Donate (to a charity)

- Incentive / loyalty bonus in CC

- Rebate / discount when paid with CC

- Investment (invest in promising business)

- Loan

- Retirement (repayment, taxing out, redemption, expiration, persistent)

- Non transferable (reputation currencies: rating, praise, reproach)

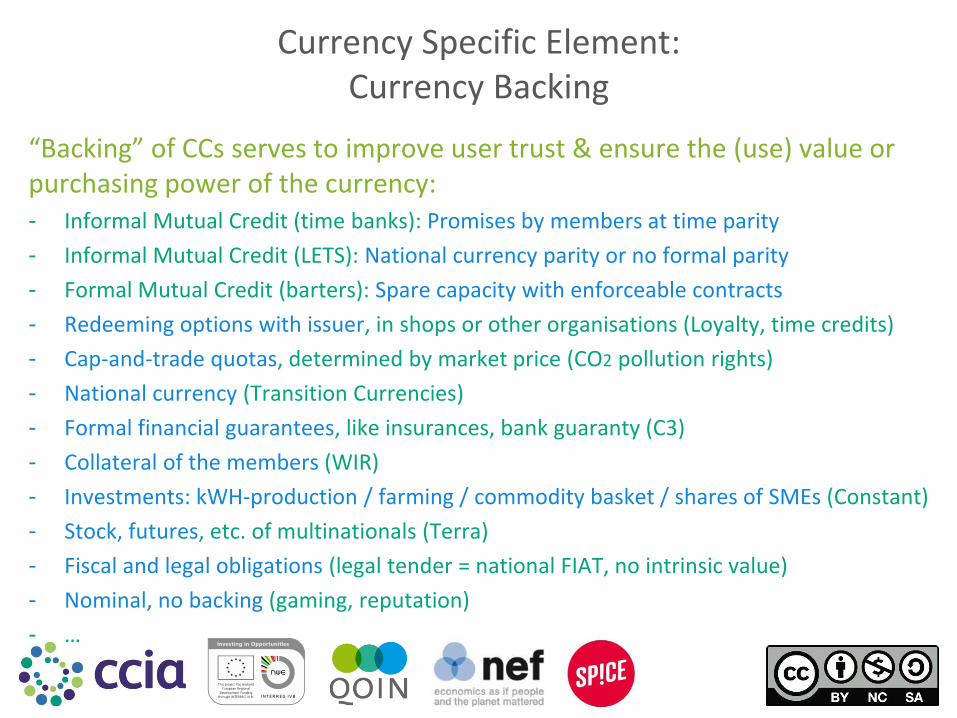

Currency Specific Element: Currency Backing

“Backing” of CCs serves to improve user trust & ensure the (use) value or purchasing power of the currency: - Informal Mutual Credit (time banks): Promises by members at time parity

- Informal Mutual Credit (LETS): National currency parity or no formal parity

- Formal Mutual Credit (barters): Spare capacity with enforceable contracts

- Redeeming options with issuer, in shops or other organisations (Loyalty, time credits)

- Cap-and-trade quotas, determined by market price (CO2 pollution rights)

- National currency (Transition Currencies)

- Formal financial guarantees, like insurances, bank guaranty (C3)

- Collateral of the members (WIR)

- Investments: kWH-production / farming / commodity basket / shares of SMEs (Constant)

- Stock, futures, etc. of multinationals (Terra)

- Fiscal and legal obligations (legal tender = national FIAT, no intrinsic value)

- Nominal, no backing (gaming, reputation)

- …

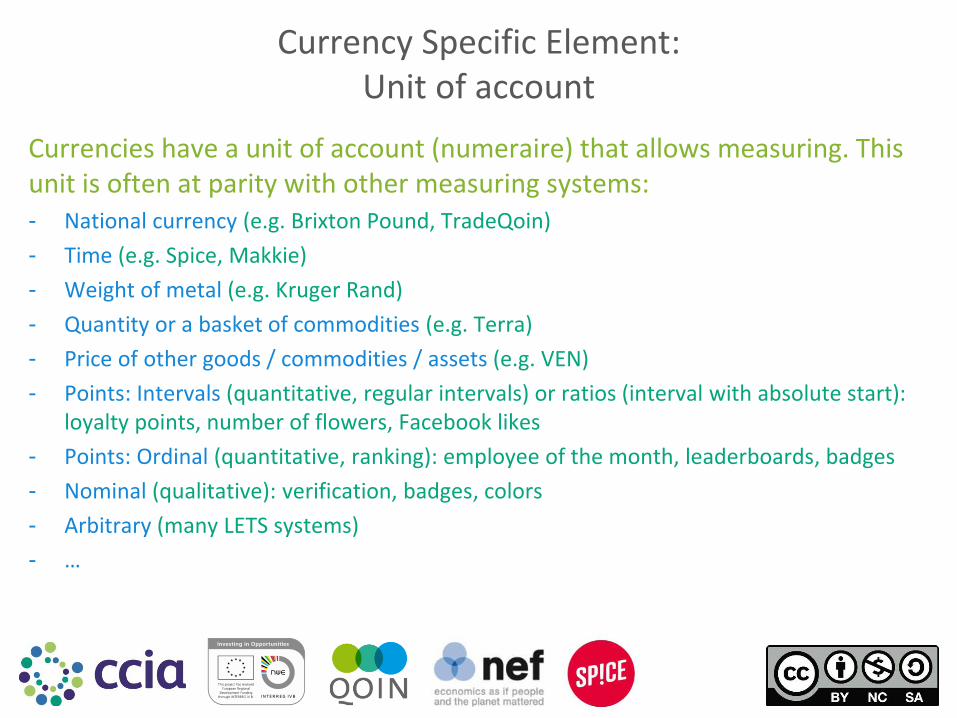

Currency Specific Element: Unit of account

Currencies have a unit of account (numeraire) that allows measuring. This unit is often at parity with other measuring systems: - National currency (e.g. Brixton Pound, TradeQoin)

- Time (e.g. Spice, Makkie)

- Weight of metal (e.g. Kruger Rand)

- Quantity or a basket of commodities (e.g. Terra)

- Price of other goods / commodities / assets (e.g. VEN)

- Points: Intervals (quantitative, regular intervals) or ratios (interval with absolute start): loyalty points, number of flowers, Facebook likes

- Points: Ordinal (quantitative, ranking): employee of the month, leaderboards, badges

- Nominal (qualitative): verification, badges, colors

- Arbitrary (many LETS systems)

- …

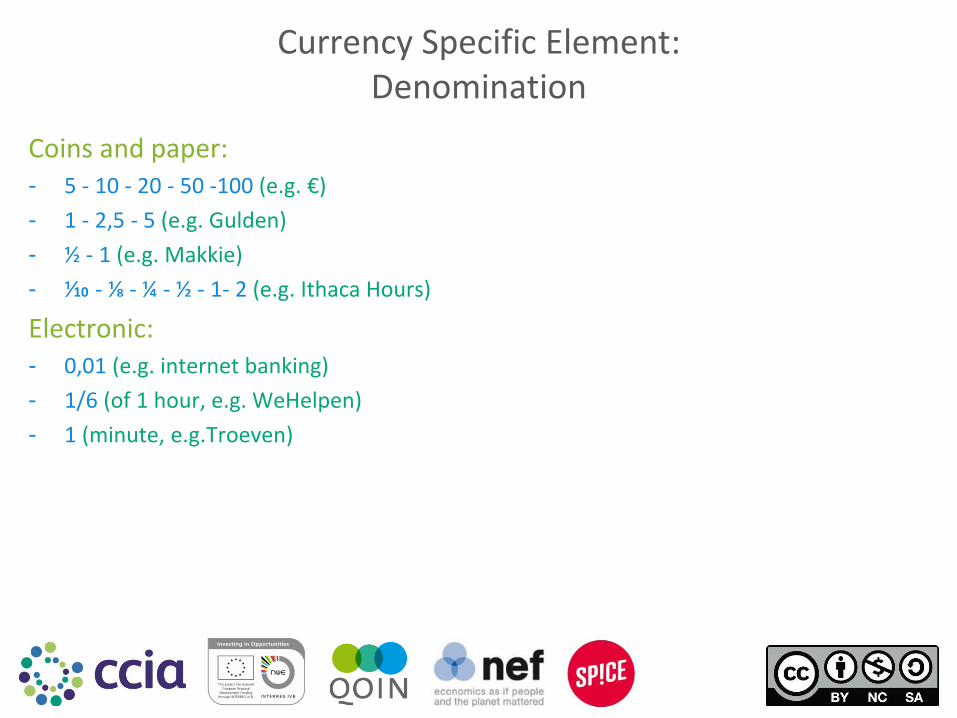

Currency Specific Element: Denomination

Coins and paper: - 5 - 10 - 20 - 50 -100 (e.g. €)

- 1 - 2,5 - 5 (e.g. Gulden)

- ½ - 1 (e.g. Makkie)

- ⅟10 - ⅛ - ¼ - ½ - 1- 2 (e.g. Ithaca Hours)

Electronic: - 0,01 (e.g. internet banking)

- 1/6 (of 1 hour, e.g. WeHelpen)

- 1 (minute, e.g.Troeven)

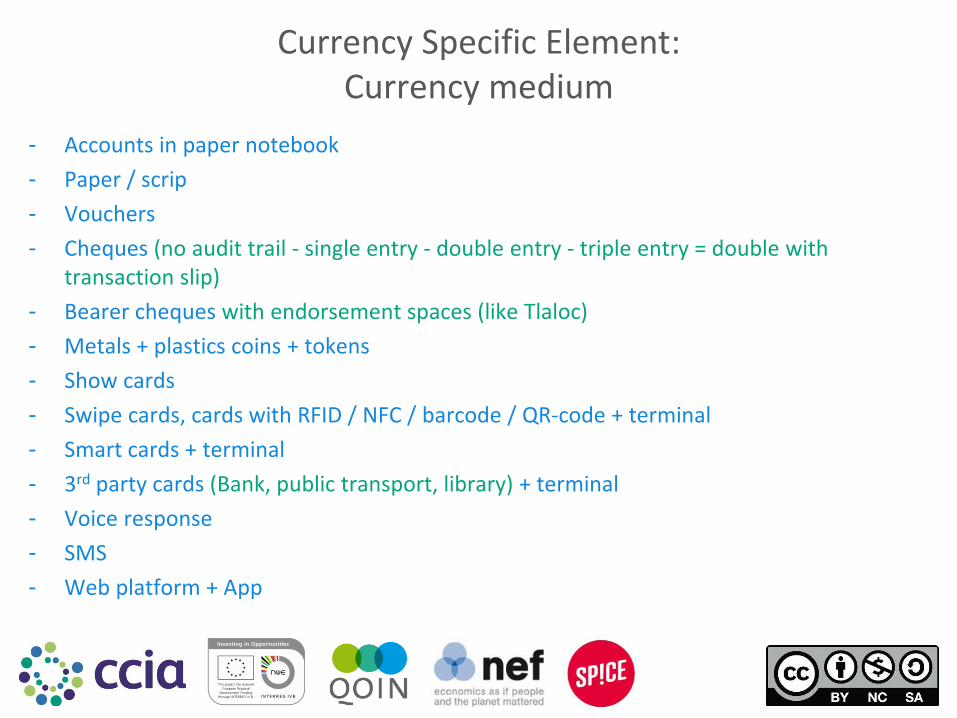

Currency Specific Element: Currency medium

- Accounts in paper notebook

- Paper / scrip

- Vouchers

- Cheques (no audit trail - single entry - double entry - triple entry = double with transaction slip)

- Bearer cheques with endorsement spaces (like Tlaloc)

- Metals + plastics coins + tokens

- Show cards

- Swipe cards, cards with RFID / NFC / barcode / QR-code + terminal

- Smart cards + terminal

- 3rd party cards (Bank, public transport, library) + terminal

- Voice response

- SMS

- Web platform + App

Currency Specific Element: Security

Choose appropriate security features according to risk and security analysis: Anti fraud, hacking & counterfeiting - Accessible trading histories as evidence of credit worthiness

- Physical safe

- Tokens are commodity (gold, etc.)

- Safe print + paper + watermarks + hologram

- Paper with unique numbering / bar code / QR-code / RFID

- Signing / double signing (on cheques)

- Authorisation by system operator (phone, electronic)

- Encryption (PGP, public-private key)

- Pin, password

- Voice recognition, face recognition, bio-metric

- Bespoke App

- …

Currency Specific Element: User account (features)

What are the necessary features and functionalities for the target group, use cases and chosen currency model? - Multiple accounts?

• Current accounts: for exchange (always needed, with options like fees, demurrage)

• Saving accounts (with options like fees, time rules, no demurrage, interest)

• Loan accounts (with options like collateral, fees, time rules, interest, credit rules)

- Credit limit: none, or fixed, based on industry, based on turnover, or adaptive

- Debit limit: none, or fixed, based on industry, based on turnover, or adaptive

- Triggered events: calendar / intervals / based or internal or external triggers

- …

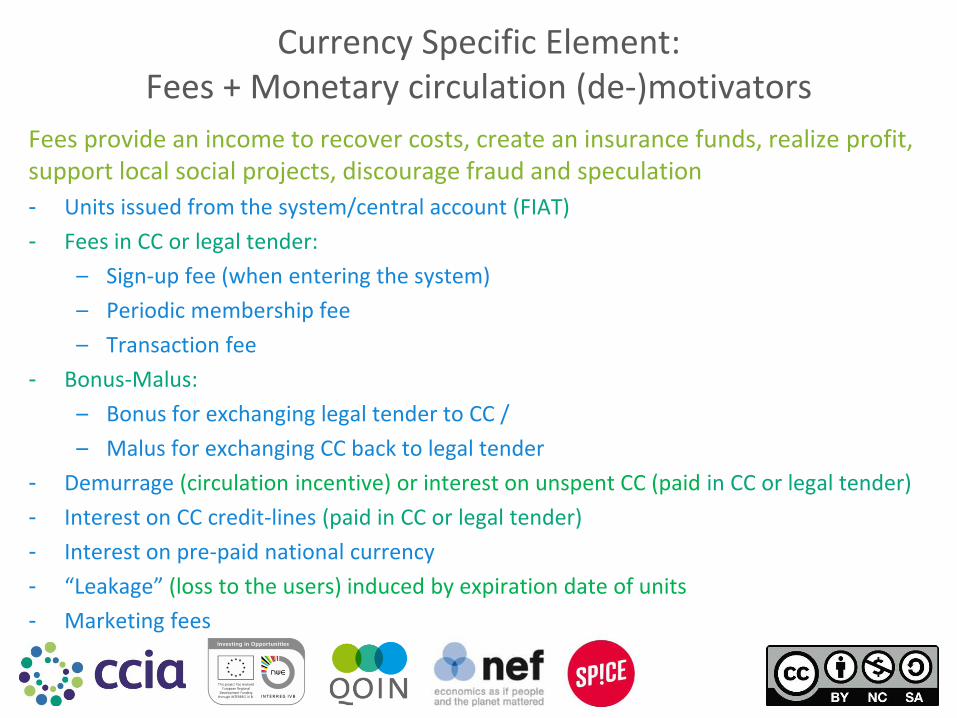

Currency Specific Element: Fees + Monetary circulation (de-)motivators

Fees provide an income to recover costs, create an insurance funds, realize profit, support local social projects, discourage fraud and speculation

- Units issued from the system/central account (FIAT)

- Fees in CC or legal tender:

– Sign-up fee (when entering the system)

– Periodic membership fee

– Transaction fee

- Bonus-Malus:

– Bonus for exchanging legal tender to CC /

– Malus for exchanging CC back to legal tender

- Demurrage (circulation incentive) or interest on unspent CC (paid in CC or legal tender)

- Interest on CC credit-lines (paid in CC or legal tender)

- Interest on pre-paid national currency

- “Leakage” (loss to the users) induced by expiration date of units

- Marketing fees

Currency Specific Element: Dynamics

Other elements that facilitate usage and circulation and determine how the users interact with and through the currency

Market

- Market place

- E-market place

- Parties and gatherings

Gaming mechanics

- Reputation, badges, likes – both on supplier and product

- Tombola, raffles, lottery

Gaming dynamics + aesthetics

- Creating a story and “meaning”

We hope this document was useful to you!

Please feel free to share this framework widely, for non-commercial purposes only, and mind the Creative Commons terms of use:

Always attribute the original authors and if you change or add elements, or build your own version of this framework, we kindly request you share your changes or suggestions with us [email protected]

Thank you and may your Community Currencies be prosperous!

Community Currency Implementation Framework

Top Related