Languages

Pages

Legal

By: Corey Leskanic, Mark Dowicz, Gabriella Grippa, DanielleTantillo

Letter to Shareholders

Corey Leskanic (CEO)

Major Accomplishments 2012

• Introduced 500-plus new products in 2012, including more than 100 low- and no-calorie choices

• Coca-Cola volume grew 3%-nearly 300 million unit cases (comparable to adding another Germany and two Russias)

• In 2012, we announced our new organizational structure of 3 operating businesses: Coca-Cola America, Coca-Cola International, and Bottle Investments Groups

• #1 Beverage company for environment, social, and governance performance by Goldman Sachs

2012 vs. 2011

Revenue 2012 vs. 2011

• decreased $222 million

Net income Growth 2012 vs. 2011

• Decreased $72 Million

Stock Performance 2012 vs. 2011

• $25.78 Dec. 30, 2011--- $31.73 Dec. 31, 2012o increase 23%

2013 Growth Opportunities

• Emphasize core brands (Coca-Cola, Coca-Cola Light, Diet Coke, Coca-Cola Zero)o Coca-Cola Light 6.5% volume growth (growth in

physical volume of sales)o Most popular, big potential growth

• Natural Sweeteners (new consumer preference)- stevia w/ Sprite & Vitamin Water

• Environment- Bottling

Business Review

Mark Dowicz (COO)

Business Review

New Products: Ayataka (Green Tea)

I Lohas (Water)

Partnership with JBF INdustries Ltd.

Zico Coconut Water

Dasani Drops

Odwalla Smoothie Refreshers

New Markets:

Business Review (continued)

Competition

• Pepsico, Inc.

• Nestle S.A.

• Dr. Pepper Snapple Group Inc.

Regulatory or Legal Issues

• Workers sue based on discrimination

• Discontinue Membership at American Legislative Exchange Council

Business Review (continued)

Risks:

• Lack of popularity of many products

• Changing health consciousness attitude

• Health issues

• Commodity costs are rising

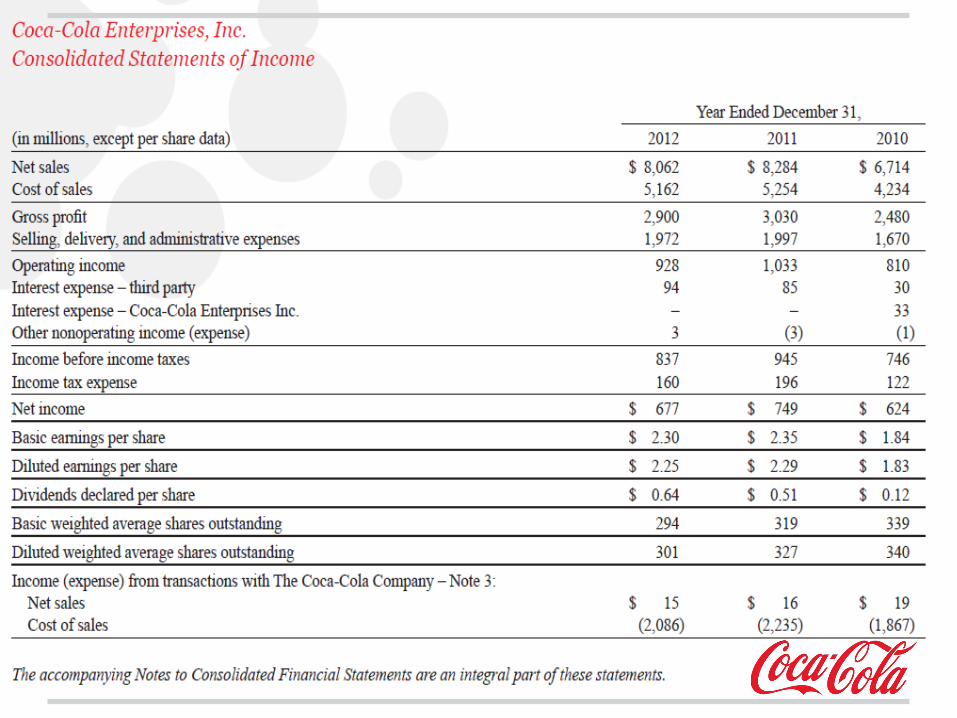

Income Statement

Gabriella Grippa (CFO)

Something to keep in mind...

• sales of products are seasonal

• 2nd and 3rd quarters account for higher unit sales

• Earn more than 60% of operating income during 2nd and 3rd quarters

Revenue (in millions)

2011 2012 Percent Decrease

$8,284 $8,062 2.68%

Why did the company's revenue go down?

• Customer marketing programso allowanceso coupon programs

Result: reduction in net sales ($1.0 billion in 2011

and 2012)

• Unfavorable currency exchange rate changes, impact of volume decline, bottle and can net pricing per case growth, challenging operating conditions, ongoing macroeconomic weakness

Cost of Revenue (in millions)

• Payments to licensors for marketing programs = reduction in cost of sales

• 2012 packaging costs per case grew due to increase cost of key raw materials like sugar.

2011 2012 Percent Decrease

$5,254 $5,162 1.75%

Gross Margin Percentage & Expenses

2011 2012 Percent Decrease

36.6% 35.9% 0.68%

GDP

2011 2012

4.1% 4.1%

Operating Expenses

Operating Income (in millions)

2011 2012 Percent Decrease

$1,033 $928 10.2%

Operating Income (continued)

Taxes (in millions)

• Increase French excise tax on beverages w/ added sweetener

• Tax rate reductions in UK and Sweden

• Tax law change in Belgium

2011 2012 Decrease

$196 $160 $36

21% 19% 2%

Net Income (in millions)

• Charges totaling $85 million related to restructuring activities

• Net mark-to-market losses totaling $4 million

• Tax benefit of $62 million from tax rate reductions in UK and Sweden, and tax law change in Belgium.

2011 2012 Percent Decrease

$749 $677 9.6%

Earnings per Share (in millions)

• 2012 paid dividends of $187 million

• February 2012, increase dividend from $0.13 to $0.16 per share

2011 2012 Percent Decrease

$2.35 $2.30 2.12%

Return on Investment (in millions)

• Became less efficient

2011 2012 Decrease

10.4% 8.8% 1.6%

Balance Statement

Danielle Tantillo (CFO)

Balance Sheet (continued)

Balance Sheet

2012 2011 Up/ Down

Current Assets 2,762 2,686 Up

Long Term Assets 6,748 6,408 Up

Current Liabilities 2,579 1,848 Up

Long Term Liabilities

4,238 4,347 Down

Shareholders Equity 2,693 2,899 Down

Retained Earnings 1,126 638 Up

Current Asset

• Cash increased (net income higher in 2011)

• Accounts Receivables (increased)

• Inventory- decreased

2012 2011

2,762 2,686

Long Term Assets

• Property, Plant, and Equipment

2012 2011

6,748 6,408

Long Term Assets(continued)

• Franchise License Intangible Assets and Goodwill

2012 2011

6,748 6,408

Current Liabilities

• Accounts Payable and Accrued Expenses

2012 2011

2,579 1,848

Current Liabilities

• Debt

2012 2011

2,579 1,848

Long Term Liabilities

• Long Term Debt

2012 2011

4,238 4,347

Shareholders Equity

• 339,064,025 shares of common stock

• Share Repurchaseso 65 million shares (no more than $1.5 billion)o 2011: $1,014 milliono 2012: $1,831 million

2012 2011

2,693 2,899

Retained Earnings

• Dividends $187 million

• Increased net income

• Bought back more common stocko 2012: 1,831 o 2011: 1,014

2012 2011

1,126 638

Key Ratios

2012 2011 better/ worse

Current Ratio 1.07 1.45 Worse

Quick Ratio .92 1.24 Worse

Debt to Asset Ratio

36.5% 33.12% Worse

Time Covered Ratio

30.85 35.65 Worse

Inventory Turnover 13.37 13.04 Worse

Days Sales Outstanding

53.29 50.23 Worse

Current Ratio

• 2012- current assets were barely larger than current liabilities o assets should be higher than liabilitieso should be greater than one= IS NOTo the ratios show that at 1.07 in 2012o Current debt increased $616 million dollars

Ratio Interpretations

Ratio Interpretations

Quick Ratio

• Ability of current assets (without inventory) to cover the current liabilities. o Shows if coca-cola has the resources necessary to

cover its current liabilities o Worse from 2011--> 1.24 to 0.92

Ratio Interpretations

Debt to Asset Ratio

• Coca-cola's financial risk increased from 33.12% to 36.5% Io Increased debt over their assetso Debt increased by $616 million dollars.

Times-Covered Ratio

• Decreased from 35.65 to 30.85 o Profits can still keep declining and they will still be

able to meet interest charges

Ratio Interpretations

Inventory Turnover

• Increased from 13.04 to 13.37 from 2011 to 2012 o cost of sales decrease from 2011 to 2012o Inventory increased from 2011 to 2012. o Took longer to get rid of all the inventory

Days Sales Outstanding

• Increased from 50.23 in 2011 to 53.29 in 2012 o Take longer to receive what customers owe