Languages

Pages

Legal

Group

Burmeister & Wain Energy A/S · Lundtoftegaardsvej 93A · DK-2800 Kgs. Lyngby · Denmark · Tel/fax +45 39 45 20 00/+45 39 45 20 05 · [email protected]

BWE – A CASE STORY

Challenges for export of

Danish biomass technology

Nicholas Kristensen

Manager, Proposals Department

Burmeister & Wain Energy – Denmark

Board member – DI Bioenergy

October 13, 2011

Bioenergy – a Driving Force for Change

Group

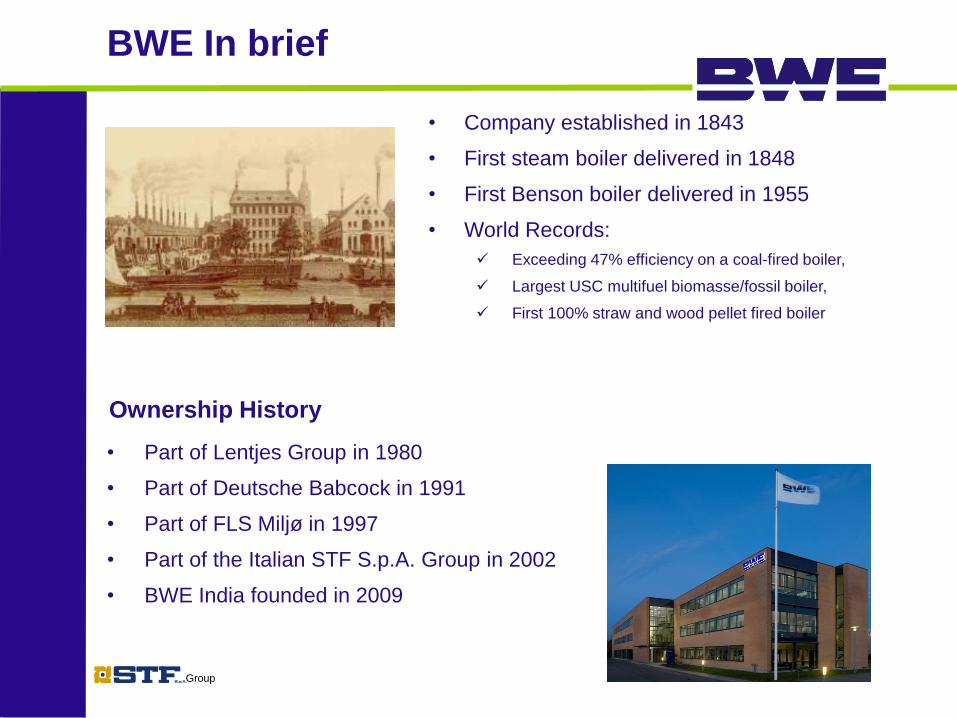

BWE In brief

• Part of Lentjes Group in 1980

• Part of Deutsche Babcock in 1991

• Part of FLS Miljø in 1997

• Part of the Italian STF S.p.A. Group in 2002

• BWE India founded in 2009

Ownership History

• Company established in 1843

• First steam boiler delivered in 1848

• First Benson boiler delivered in 1955

• World Records:

Exceeding 47% efficiency on a coal-fired boiler,

Largest USC multifuel biomasse/fossil boiler,

First 100% straw and wood pellet fired boiler

Group

• Advanced Ultra Super Critical

steam boilers for power generation

• Biomass boilers

Grate fired

Pulverized Fuel (PF) fired

• Low-NOx firing systems and multi-fuel burners

coal, gas, oil and biomass

• Upgrading of existing boilers for improved performance

• Boiler service and maintenance

BWE – Products and services

Group

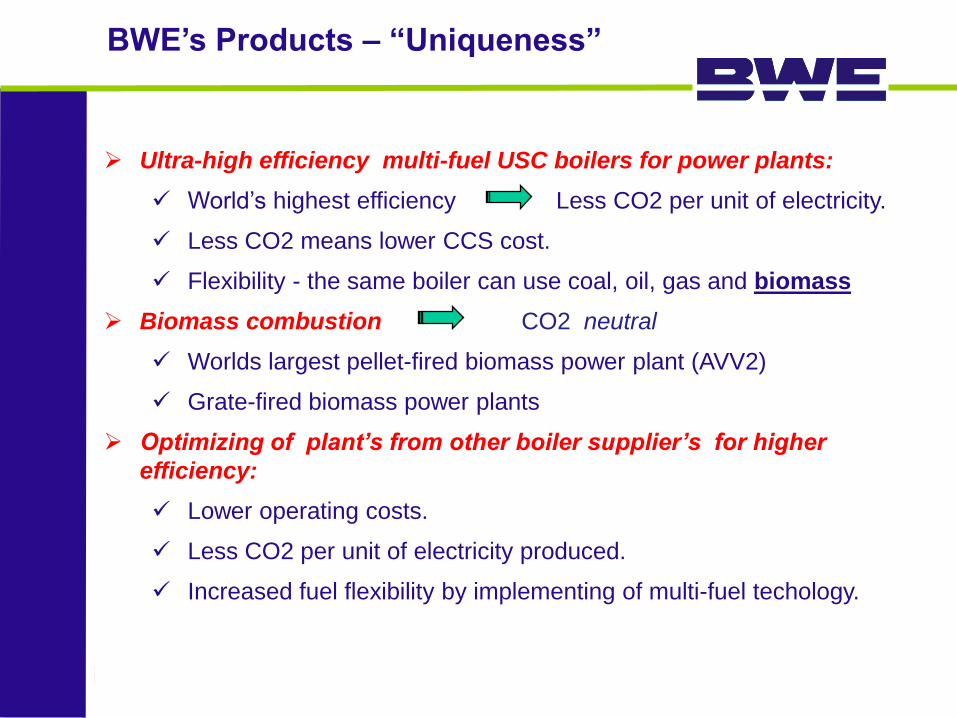

Ultra-high efficiency multi-fuel USC boilers for power plants:

World’s highest efficiency Less CO2 per unit of electricity.

Less CO2 means lower CCS cost.

Flexibility - the same boiler can use coal, oil, gas and biomass

Biomass combustion CO2 neutral

Worlds largest pellet-fired biomass power plant (AVV2)

Grate-fired biomass power plants

Optimizing of plant’s from other boiler supplier’s for higher

efficiency:

Lower operating costs.

Less CO2 per unit of electricity produced.

Increased fuel flexibility by implementing of multi-fuel techology.

BWE’s Products – “Uniqueness”

Group

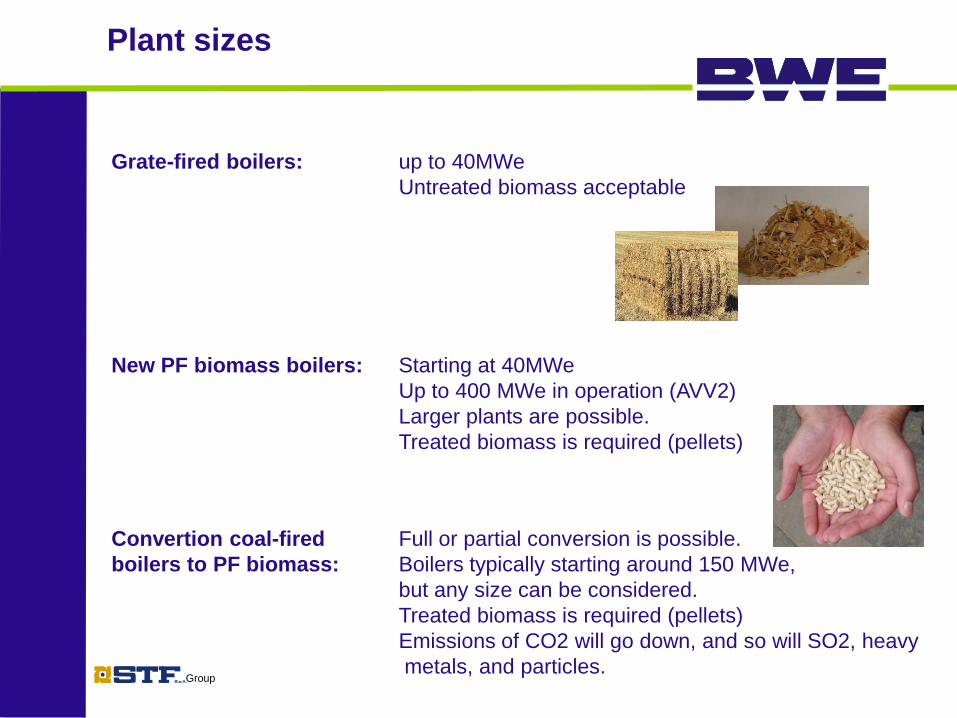

Grate-fired boilers: up to 40MWe

Untreated biomass acceptable

Plant sizes

New PF biomass boilers: Starting at 40MWe

Up to 400 MWe in operation (AVV2)

Larger plants are possible.

Treated biomass is required (pellets)

Convertion coal-fired Full or partial conversion is possible.

boilers to PF biomass: Boilers typically starting around 150 MWe,

but any size can be considered.

Treated biomass is required (pellets)

Emissions of CO2 will go down, and so will SO2, heavy

metals, and particles.

Group

•European Union

•Brazil

•Ukraine

•USA

•Canada

•China

•Australia

Biomass markets

Group

PF biomass boilers

Conversion from

fossil fuel to biomass

Generating

companies

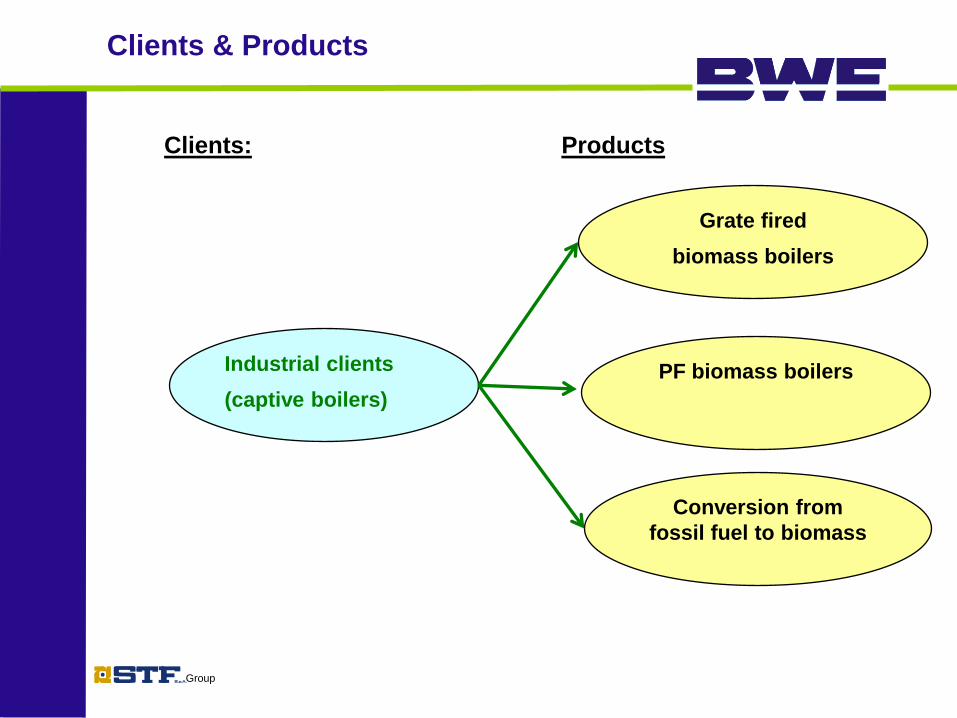

Clients: Products

Clients & Products

Group

Grate fired

biomass boilers

PF biomass boilers

Conversion from

fossil fuel to biomass

Industrial clients

(captive boilers)

Clients: Products

Clients & Products

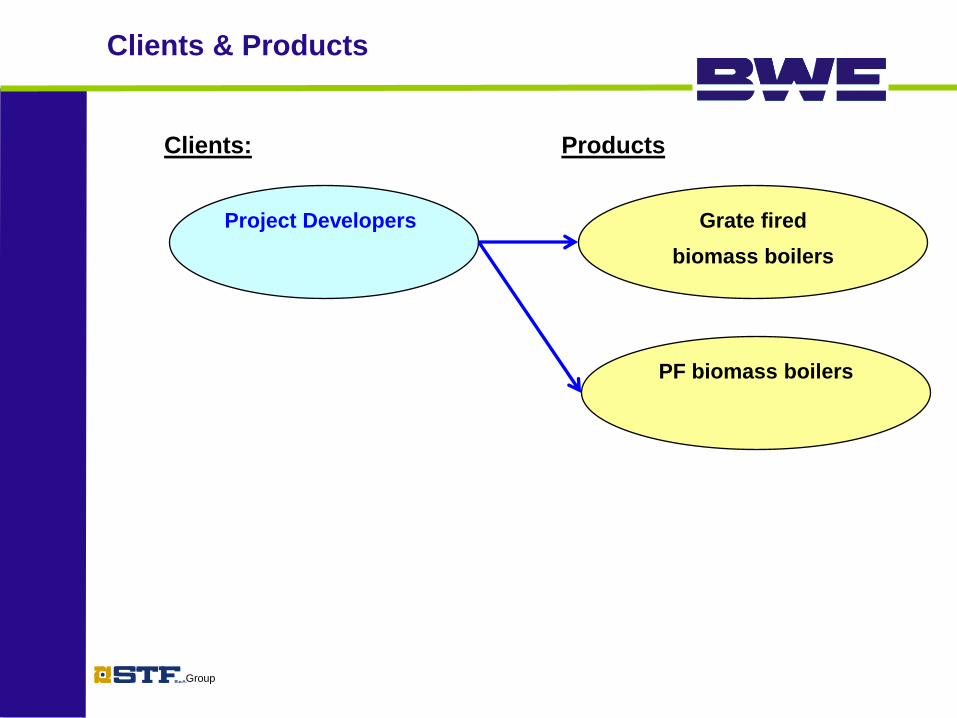

Group

Grate fired

biomass boilers

PF biomass boilers

Project Developers

Clients: Products

Clients & Products

Group

Grate fired

biomass boilers

PF biomass boilers

Conversion from

fossil fuel to biomass

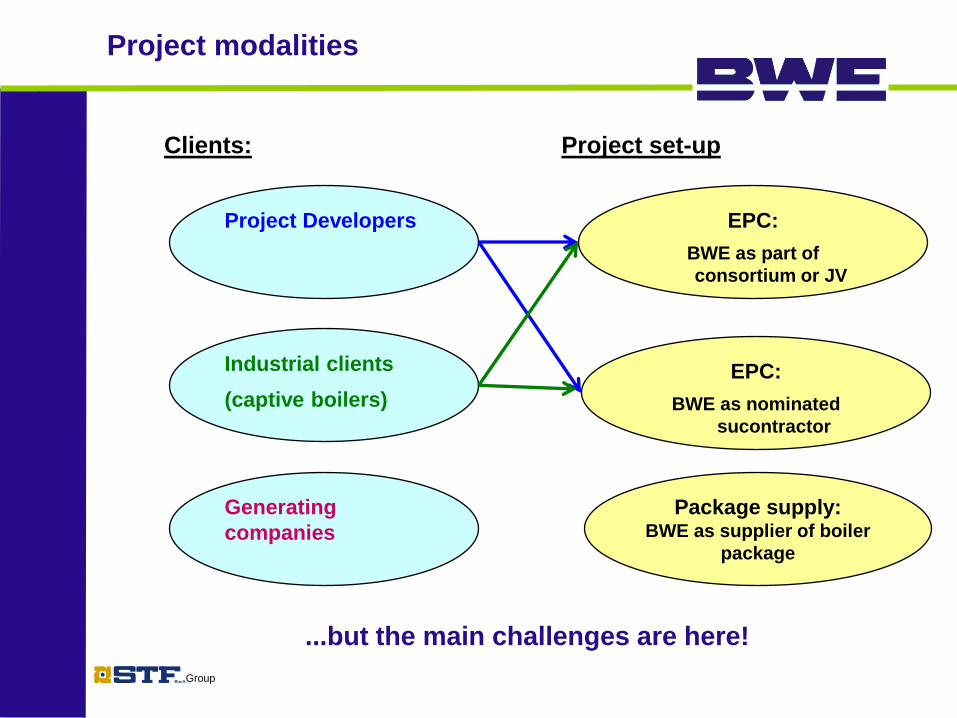

Project Developers

Industrial clients

(captive boilers)

Generating

companies

Clients: Products

Clients & Products

Group

EPC:

BWE as part of

consortium or JV

EPC:

BWE as nominated

subcontractor

Package supply: BWE as supplier of boiler

package

Project Developers

Industrial clients

(captive boilers)

Generating

companies

Clients: Project set-up

Project modalities

All combinations are possible....

Group

EPC:

BWE as part of

consortium or JV

EPC:

BWE as nominated

sucontractor

Package supply: BWE as supplier of boiler

package

Project Developers

Industrial clients

(captive boilers)

Generating

companies

Clients: Project set-up

Project modalities

...but the main challenges are here!

Group

From 2007 until today BWE has received more than 200 requests for

biomass projects, mainly from within Europe but also a few from

North America, South America, China, and Australia.

THE CHALLENGE

BWE has the technology and the experience.

So what is the challenge?

Of the more than 200 requests for biomass projects roughly:

• 25-30 has become orders

• BWE has quoted on approximately 20

• 10 of these are still undecided

• BWE has won 4

Group

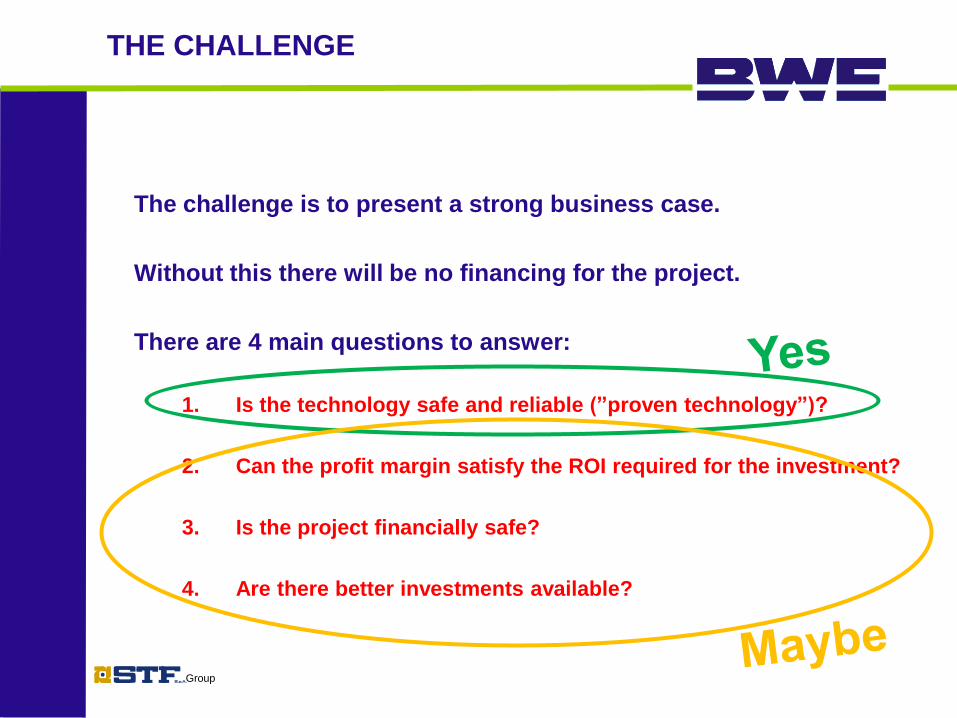

The challenge is to present a strong business case!

Without this there will be no financing for the project!

There are 4 main questions to answer:

1. Is the technology safe and reliable (”proven technology”)?

2. Can the profit margin satisfy the ROI required for the investment?

3. Is the project financially ”safe”?

4. Are there better investments available?

THE CHALLENGE

Group

The challenge is to present a strong business case.

Without this there will be no financing for the project.

There are 4 main questions to answer:

1. Is the technology safe and reliable (”proven technology”)?

2. Can the profit margin satisfy the ROI required for the investment?

3. Is the project financially safe?

4. Are there better investments available?

THE CHALLENGE

Group

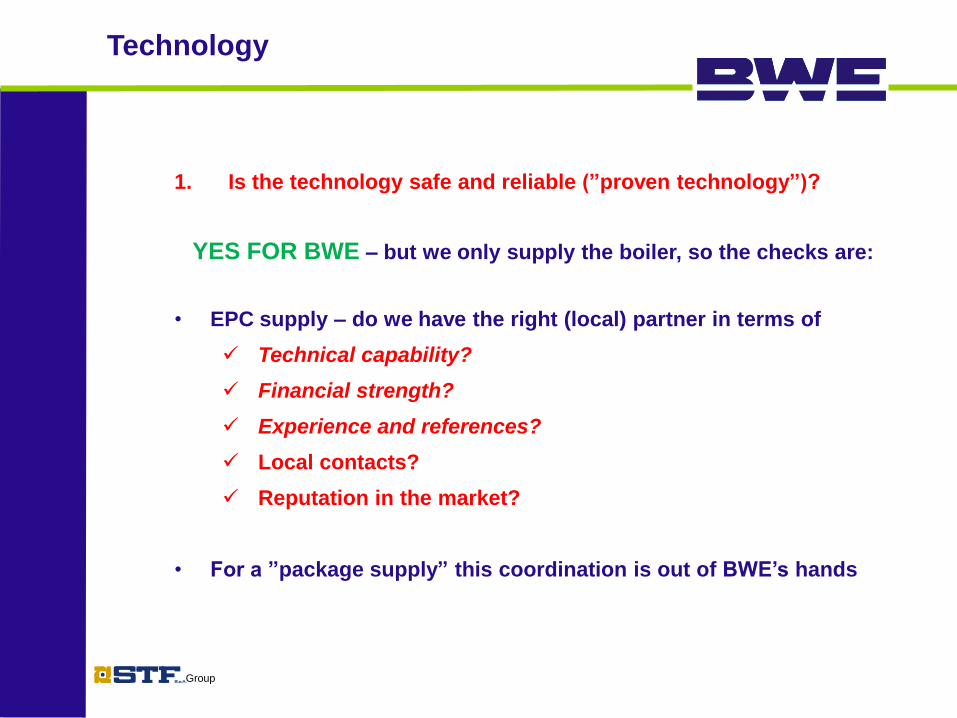

1. Is the technology safe and reliable (”proven technology”)?

YES FOR BWE – but we only supply the boiler, so the checks are:

• EPC supply – do we have the right (local) partner in terms of

Technical capability?

Financial strength?

Experience and references?

Local contacts?

Reputation in the market?

• For a ”package supply” this coordination is out of BWE’s hands

Technology

Group

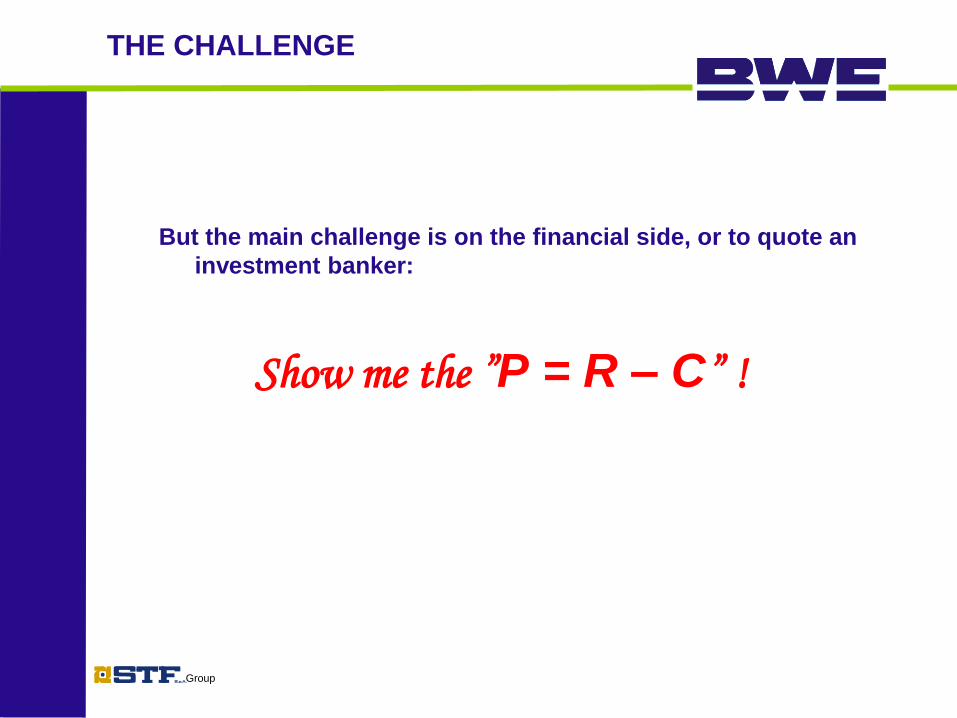

But the main challenge is on the financial side, or to quote an

investment banker:

Show me the ”P = R – C” !

THE CHALLENGE

Group

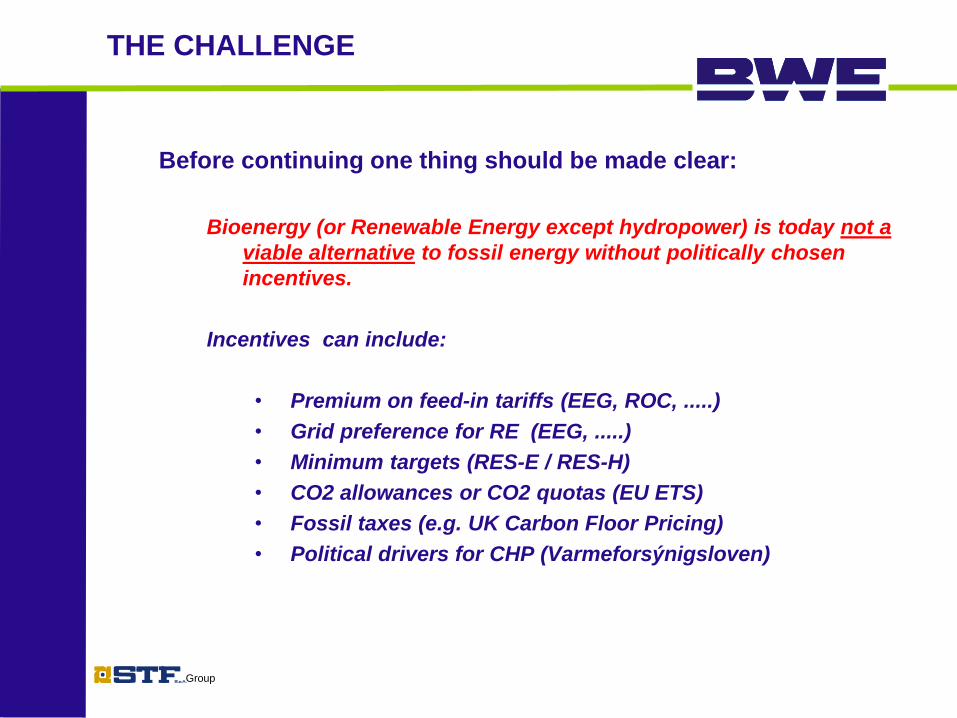

Before continuing one thing should be made clear:

Bioenergy (or Renewable Energy except hydropower) is today not a

viable alternative to fossil energy without politically chosen

incentives.

Incentives can include:

• Premium on feed-in tariffs (EEG, ROC, .....)

• Grid preference for RE (EEG, .....)

• Minimum targets (RES-E / RES-H)

• CO2 allowances or CO2 quotas (EU ETS)

• Fossil taxes (e.g. UK Carbon Floor Pricing)

• Political drivers for CHP (Varmeforsýnigsloven)

THE CHALLENGE

Group

2. Can the profit margin satisfy the ROI required for the investment?

3. Is the project financially safe?

Profit Margin

These questions can be evaluated by looking at Costs, Revenues, and

the related uncertainties.

Group

COSTS

• Construction costs

• Well-defined and handled through the supply contract.

• Maintenance costs

• Well-defined, and can be fixed with an LTSA or O&M contract.

• Fuel costs

• Fuel accounts for most of the operating costs.

• The long term supply/demand balance is unpredictable, so fuel

costs are uncertain.

• LTFS contracts required.

• Uncertainty on sustainability criteria and the coming directive

increases the uncertainty.

Profit Margin

Group

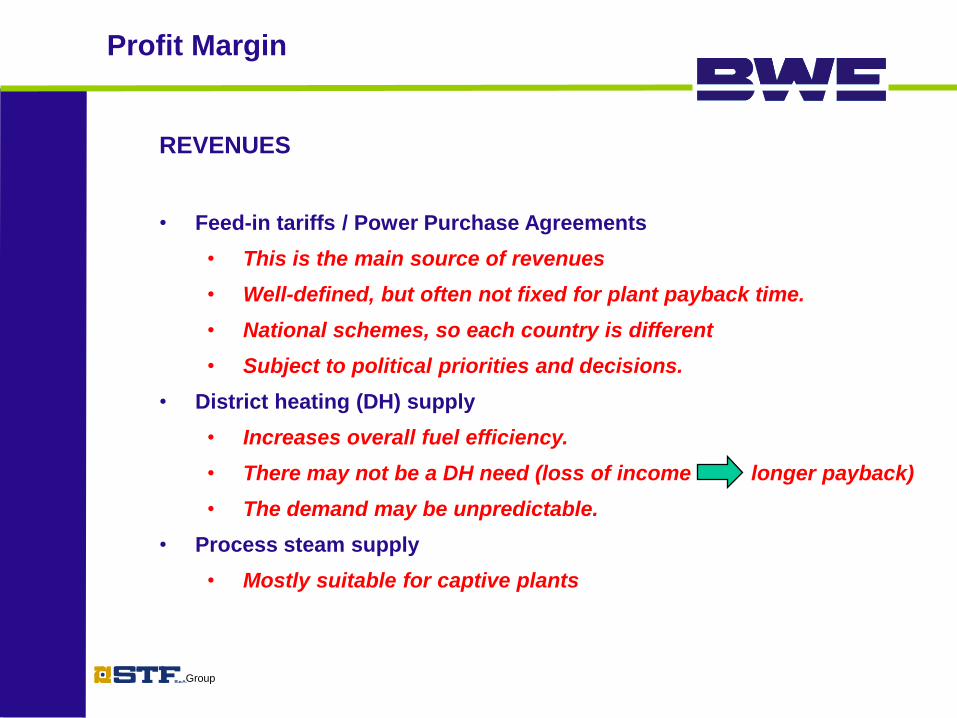

Direct revenues

REVENUES

• Feed-in tariffs / Power Purchase Agreements

• This is the main source of revenues

• Well-defined, but often not fixed for plant payback time.

• National schemes, so each country is different

• Subject to political priorities and decisions.

• District heating (DH) supply

• Increases overall fuel efficiency.

• There may not be a DH need (loss of income longer payback)

• The demand may be unpredictable.

• Process steam supply

• Mostly suitable for captive plants

Profit Margin

Group

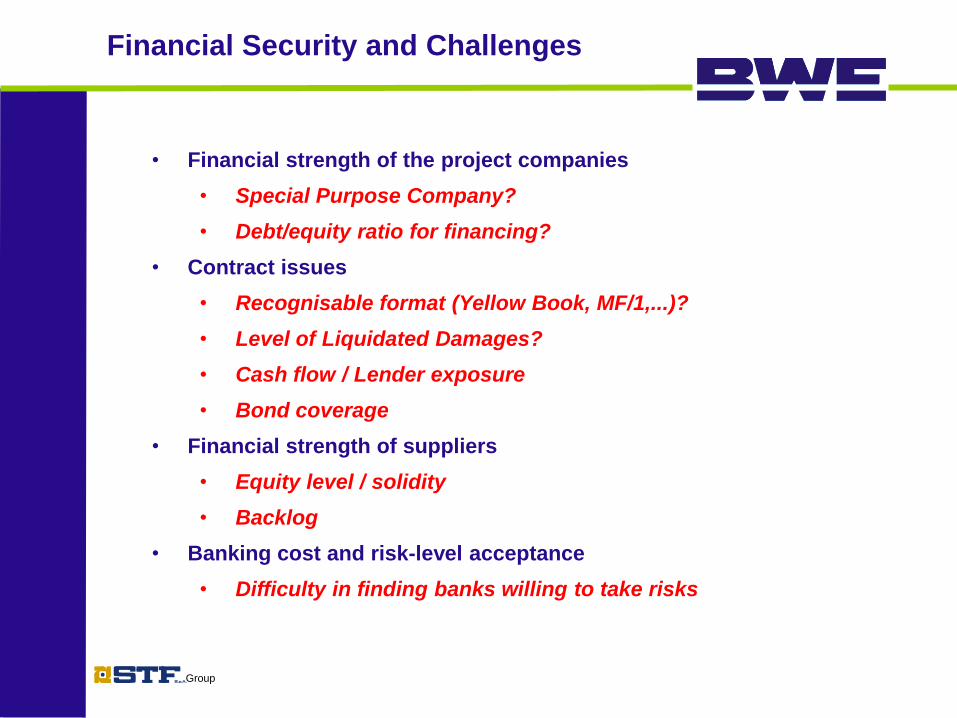

Direct revenues

• Financial strength of the project companies

• Special Purpose Company?

• Debt/equity ratio for financing?

• Contract issues

• Recognisable format (Yellow Book, MF/1,...)?

• Level of Liquidated Damages?

• Cash flow / Lender exposure

• Bond coverage

• Financial strength of suppliers

• Equity level / solidity

• Backlog

• Banking cost and risk-level acceptance

• Difficulty in finding banks willing to take risks

Financial Security and Challenges

Group

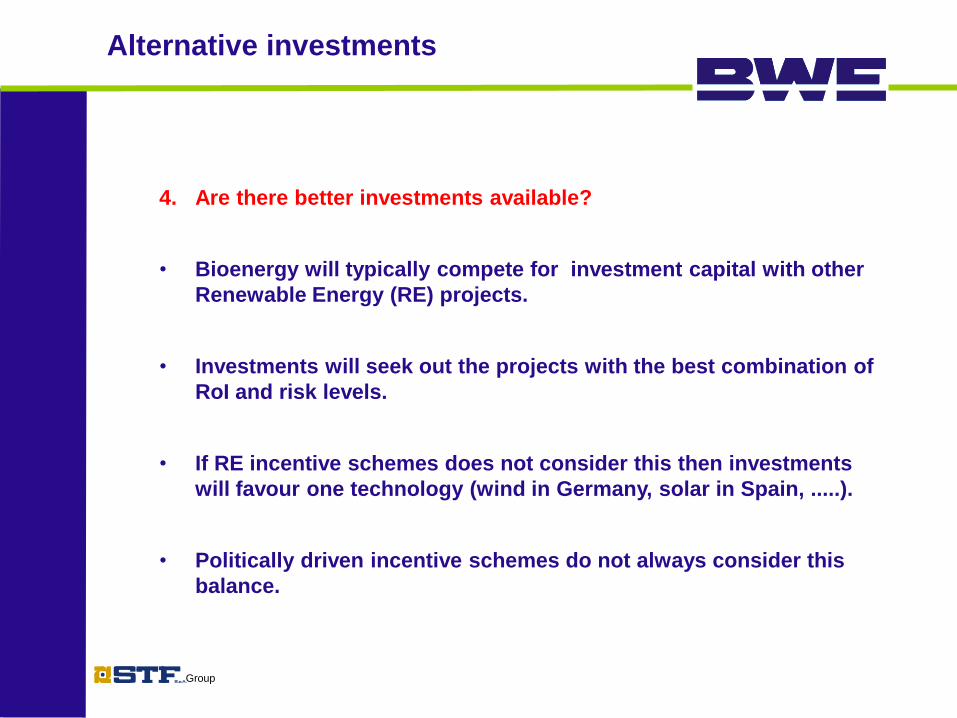

4. Are there better investments available?

• Bioenergy will typically compete for investment capital with other

Renewable Energy (RE) projects.

• Investments will seek out the projects with the best combination of

RoI and risk levels.

• If RE incentive schemes does not consider this then investments

will favour one technology (wind in Germany, solar in Spain, .....).

• Politically driven incentive schemes do not always consider this

balance.

Alternative investments

Group

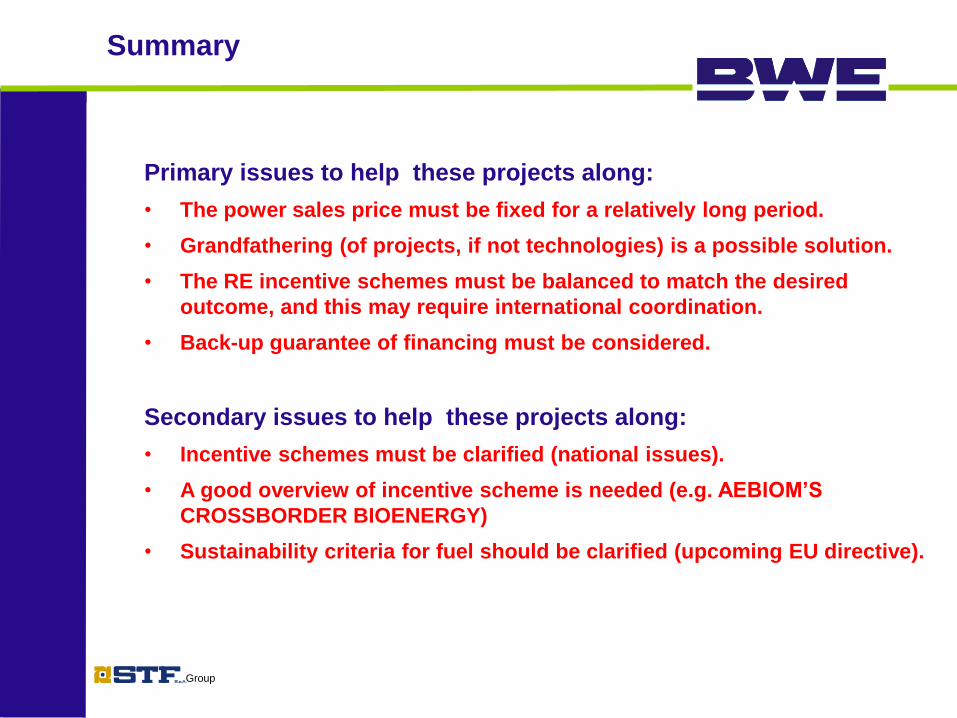

Summary

Primary issues to help these projects along:

• The power sales price must be fixed for a relatively long period.

• Grandfathering (of projects, if not technologies) is a possible solution.

• The RE incentive schemes must be balanced to match the desired

outcome, and this may require international coordination.

• Back-up guarantee of financing must be considered.

Secondary issues to help these projects along:

• Incentive schemes must be clarified (national issues).

• A good overview of incentive scheme is needed (e.g. AEBIOM’S

CROSSBORDER BIOENERGY)

• Sustainability criteria for fuel should be clarified (upcoming EU directive).

Group

Thank you for your attention!

Group

Visit us on the web – www.bwe.dk

Top Related