Languages

Pages

Legal

Budget and Finances

Kick-Off Meeting in Geneva

Kick-Off Meeting in Geneva: Budget and Finances Slide 2 22.04.2007

Budget and Finances

• Outline1. General funding principles

2. Cost structure

3. Payments and distribution of funds

Kick-Off Meeting in Geneva: Budget and Finances Slide 3 22.04.2007

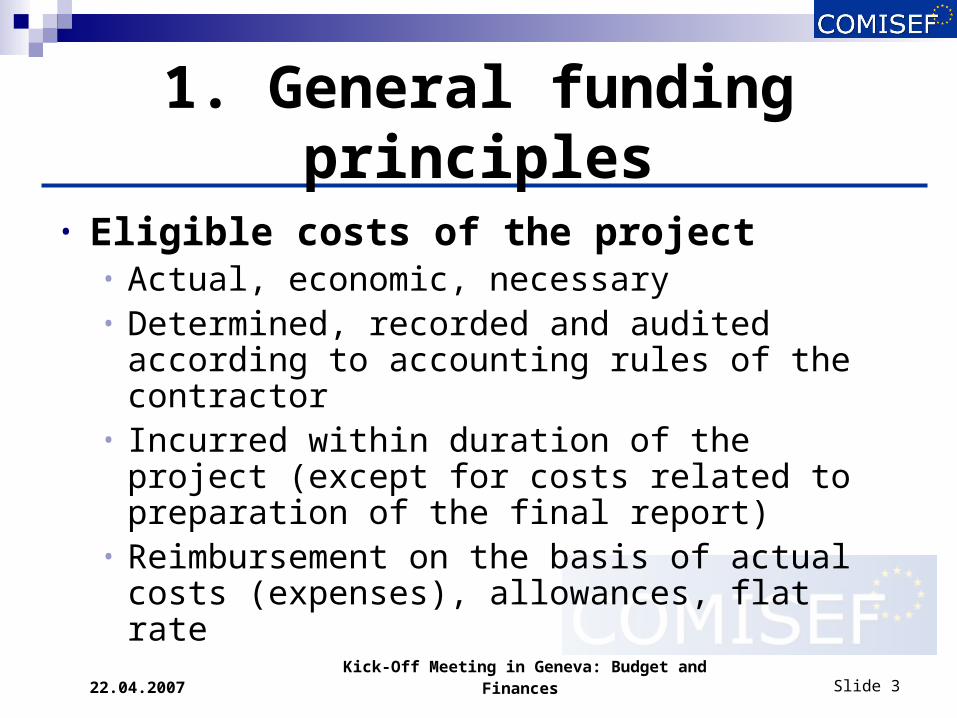

1. General funding principles

• Eligible costs of the project• Actual, economic, necessary• Determined, recorded and audited according

to accounting rules of the contractor• Incurred within duration of the project (except

for costs related to preparation of the final report)

• Reimbursement on the basis of actual costs (expenses), allowances, flat rate

Kick-Off Meeting in Geneva: Budget and Finances Slide 4 22.04.2007

1. General funding principles

• Non-eligible costs• Indirect taxes (e.g. VAT, duties)• Interest owed• Provisions for possible future losses or charges• Exchange losses• Costs related to return on capital• Debt and debt service charges• Costs declared, incurred or reimbursed in respect of

another Community project

Kick-Off Meeting in Geneva: Budget and Finances Slide 5 22.04.2007

1. General funding principles

Definition Receipts• Receipts are transfers (financial, in kind) from third

parties to the contractor• Income generated by the project• Interests yielded through Commission funding

Receipts• Community financial contribution cannot give rise to

any profit for the contractors.• (Eligible costs – receipts for the projects) ≥

Community financial contribution

Kick-Off Meeting in Geneva: Budget and Finances Slide 6 22.04.2007

Budget and Finances

• Outline1. General funding principles

2. Cost structure

3. Payments and distribution of funds

Kick-Off Meeting in Geneva: Budget and Finances Slide 7 22.04.2007

2. Cost structure

max. 10% of direct

costs

max. 7% of total eligible costs

Minimum 65% of total eligible costs

OverheadManage-ment

expenses

Research training /

Transfer of Know-

ledge(ToK)

Participation expen-

ses

Career explora

-tory allow.

Mobility allow.

Travel allow.

Monthly living

allowan-ce

Contribution to the benefit of the contractors

Contribution to the benefit of the researcher

Eligible costs of the project

Kick-Off Meeting in Geneva: Budget and Finances Slide 8 22.04.2007

2. Cost structure

• Contribution to the benefit of the researchers (fellows):• Monthly living allowance (basic salary according to

Marie Curie rates x country coefficient)• Travel allowance (paid once in 12 months according

to distance to home destination)• Mobility allowance (monthly supplement to basic

salary, 500/800€ × country coefficient)• Career exploratory allowance (one-off payment of

2,000€ if contract exceeds 12 months)

Kick-Off Meeting in Geneva: Budget and Finances Slide 9 22.04.2007

2. Cost structure

• Contribution to the benefit of the researchers (fellows) - Participation expenses

• Expenses incurred by/for the researchers• Calculated on the basis of 400€ per person-month• Administered by the host institution

(NOT directly paid to the researcher!)• Paid according to the actual cost incurred • For the purpose of training, networking, ToK

Kick-Off Meeting in Geneva: Budget and Finances Slide 10 22.04.2007

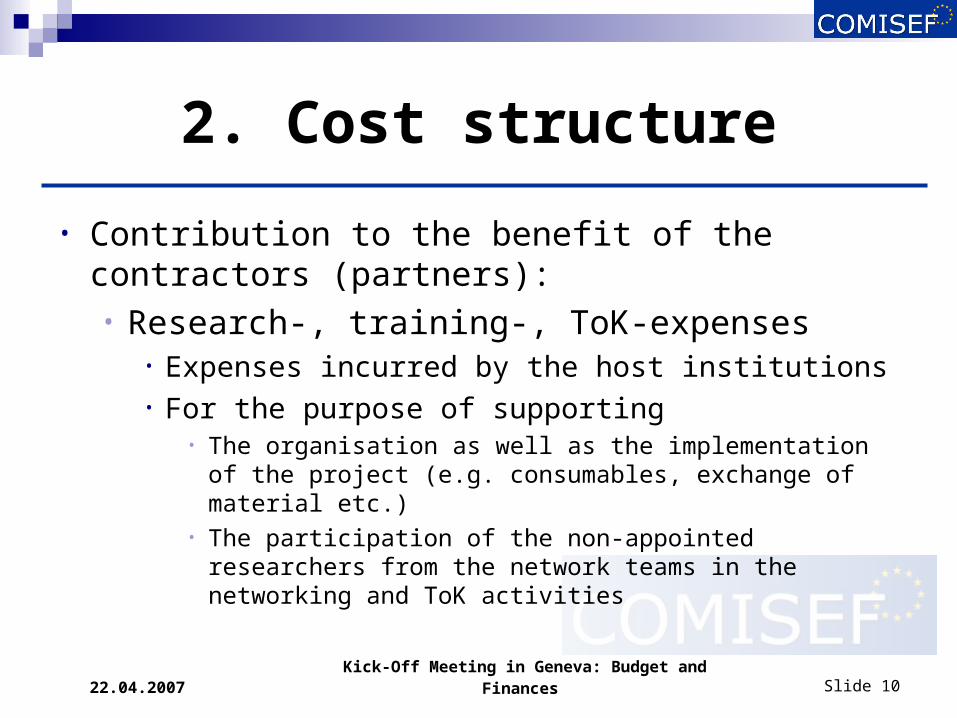

2. Cost structure

• Contribution to the benefit of the contractors (partners):• Research-, training-, ToK-expenses

• Expenses incurred by the host institutions• For the purpose of supporting

• The organisation as well as the implementation of the project (e.g. consumables, exchange of material etc.)

• The participation of the non-appointed researchers from the network teams in the networking and ToK activities

Kick-Off Meeting in Geneva: Budget and Finances Slide 11 22.04.2007

2. Cost structure

• Management expenses• Maximum of 7% of the total budget• Paid towards the management of the project and

the expenses related to the auditing of the financial reports of the RTN

Kick-Off Meeting in Geneva: Budget and Finances Slide 12 22.04.2007

2. Cost structure

• Overhead• Flat rate payment of 10% of the direct costs (i.e. costs

that can be identified by each contractor in accordance with its accounting system, can be attributed directly to the project and satisfy certain criteria) excluding costs of subcontracting

Kick-Off Meeting in Geneva: Budget and Finances Slide 13 22.04.2007

2. Cost structure

max. 10% of direct

costs

max. 7% of total eligible costs

Minimum 65% of total eligible costs

OverheadManage-ment

expenses

Research training /

ToK

Participation expen-

ses

Career explora

-tory allow.

Mobility allow.

Travel allow.

Monthly living

allowan-ce

Contribution to the benefit of the contractors

Contribution to the benefit of the researcher

Eligible costs of the project

Kick-Off Meeting in Geneva: Budget and Finances Slide 14 22.04.2007

2. Cost structure

• Expenses for ESR and ER (Example)• Assuming one single ESR from Denmark and one

married ER from Spain for the JLU in Giessen• The Correction coefficient for Germany is 103.8%

(or 1.038) for both fellows• The fixed-amount contributions for the travel

allowances based on the direct distance are 500€ (Denmark) and 750€ (Spain)

Kick-Off Meeting in Geneva: Budget and Finances Slide 15 22.04.2007

2. Cost structure

• Expenses for ESR and ER (Example) - cont’d• Expenses for the benefit of the ERS and ER

Monthly living allow.

Travel allow.

Mobility allow. Career expl. allow.

Partici-pation

expenses

Total

ESR

3 years × 30,550 € × 1.038 = 95,133 €

3 years × 500 € = 1,500 €

36 months × 500 € × 1.038 =

18,684 €

2,000€ 36 months × 400 €

= 14,400 €

129,717 €

ER 3 years × 47,000€ × 1.038 = 146,358 €

3 years × 750 € = 2,250 €

36 months × 800 € × 1.038 =

29,894 €

2,000€ 36 months × 400€

= 14,400€

194,902 €

Kick-Off Meeting in Geneva: Budget and Finances Slide 16 22.04.2007

2. Cost structure

max. 10% of direct

costs

max. 7% of total eligible costs

Minimum 65% of total eligible costs

OverheadManage-ment

expenses

Research training /

ToK

Participation expen-

ses

Career explora

-tory allow.

Mobility allow.

Travel allow.

Monthly living

allowan-ce

Contribution to the benefit of the contractors

Contribution to the benefit of the researcher

Eligible costs of the project

Kick-Off Meeting in Geneva: Budget and Finances Slide 17 22.04.2007

2. Cost structure

• Financing of a workshop (Example)

Workshop in Essex

(ESR from Klagenfurt, ESR & ER from Giessen)

Researchers

Partners (Team members)

Travelling, accommodation, conference fee

Budget Essex

Research, training,

ToK

Participation expenses

Budget Klagenfurt

Budget Giessen

Kick-Off Meeting in Geneva: Budget and Finances Slide 18 22.04.2007

2. Cost structure

• Expenses for training and ToK - Budget (Example)• Essex organizes a tutorial (T1) and a workshop (WS),

Giessen - a tutorial (T2), and Berlin - a summer school (SS)

• For each event, each organizer has to cover the costs for research, training, ToK including participation expenses for team members (not fellows)

• Participation expenses of the fellows are born by each participant (i.e. eligible researcher)

Kick-Off Meeting in Geneva: Budget and Finances Slide 19 22.04.2007

2. Cost structure

• Expenses for training and ToK - Budget (Example) – cont’d

Partici-pants

Costs per person and day

Days Travel expen-ses per person

Semi-nar

room

Invited speakers

Elig. resear-chers

Team mem-bers

Participa-tion

expenses

ToK, etc.

Total costs

T1-T2 8 150.00€ 3 500.00€

200.00€

1,500.00€ 5 3 4,750.00€ 4,550.00€

9,300.00€

WS 7 130.00€ 2 500.00€

300.00€

3,000.00€ 4 3 3,040.00€ 5,580.00€

8,620.00€

SS 5 120.00€ 4 500.00€

600.00€

750.00€ 4 1 3,920.00€ 2,330.00€

6,250.00€

Kick-Off Meeting in Geneva: Budget and Finances Slide 20 22.04.2007

Budget and Finances

• Outline1. General funding principles

2. Cost structure

3. Payments and distribution of funds

Kick-Off Meeting in Geneva: Budget and Finances Slide 21 22.04.2007

3. Payments and distribution of funds

• Distribution of funds• Community financial contribution is paid to the co-

ordinating institution (i.e. JLU Giessen)• Co-ordinator distributes the funds to partners without

unjustified delay• Distribution of funds to partners is conducted

according to CPF (Contract Preparation Forms) or other internal agreements. The Commission is to be notified and to approve any major changes to the original budget breakdown

Kick-Off Meeting in Geneva: Budget and Finances Slide 22 22.04.2007

3. Payments and distribution of funds

• Payment modalities• Pre-financing (initial as well as periodic) consists of

80% of the total budget for subsequent 18 months according to CPF budget planning or to financial planning in the periodic management report

• Initial pre-financing • Periodic payments

• Within 45 days after approval of the periodic report• Based on pre-financing for the upcoming (next) reporting

period (adjusted for amounts accepted for respective period)

Kick-Off Meeting in Geneva: Budget and Finances Slide 23 22.04.2007

3. Payments and distribution of funds

• Payment modalities• Periodic payments (Example 1)

• Initial pre-financing for reporting period 1: 1,000,000€

• Accepted costs for reporting period 1: 400,000€• 600,000 € not spent• Planned pre-financing for period 2: 1,200,000€• Effective pre-financing for period 2: 600,000€ =

1,200,000€ - 600,000€

Kick-Off Meeting in Geneva: Budget and Finances Slide 24 22.04.2007

3. Payments and distribution of funds

• Payment modalities• Periodic payments (Example 2)

• Initial pre-financing for reporting period 1: 1,000,000€

• Accepted costs for reporting period 1: 1,200,000€• 200,000 € overspent• Planned pre-financing for period 2: 1,200,000€• Effective pre-financing for period 2: 1,400,000€ =

1,200,000€ - (-200,000)€

Kick-Off Meeting in Geneva: Budget and Finances Slide 25 22.04.2007

3. Payments and distribution of funds

• Payment modalities• Periodic payments

• Total amount of pre-financing cannot exceed 80% of Community financial contribution (i.e. total budget for the respective period)

• Final payment• Within 45 days after approval of the final report

Kick-Off Meeting in Geneva: Budget and Finances Slide 26 22.04.2007

3. Payments and distribution of funds

• 70% rule• Only applies to periodic reports submitted without

audit certificates• If less than 70% of pre-financing is spent in the

reporting period, then NO pre-financing for the subsequent reporting period!

• Unless:• A complementary management report is provided once 70%

of pre-financing has been spent• or audit certificates (provided by each partner) are submitted

for the reporting period we should use the second option.

Top Related