Languages

Pages

Legal

1

Differences between Fee Structure of Mobile Money Technologies and Traditional

Banking Systems, Social Psychological Determinants and Service Uptake: A Case

Study of Uganda

Bruno L. YAWE & Tinah NASSALI

College of Business and Management Sciences

Makerere University, Kampala, UGANDA

December 07th 2011

1

2

Presentation Plan

• Research Procedures Completed to date

• Preliminary Findings

• Reflections on the Research Process [What has Worked, Successes, Pitfalls, Setbacks]

• New Questions that the Research to date has Posed

• Research Procedures still to be Conducted

• Next Steps 2

3

Research Procedures Completed to date

• Some interviews with officials from Bank of Uganda and the Uganda Communications Commission (UCC);

• Questionnaires

• Participating in public dialogues like: The operator-consumer dialogue on quality of service by UCC

3

4

Preliminary Findings

• (a) Fee Structure of the Various Mobile Money Providers in Uganda

• (b) Relate the Fees Structure of the various Mobile Money Providers to Service Uptake

• (c) Examine the Social and Psychological Determinants of Mobile Money Technology Use and Adoption in Uganda

4

5

Fee Structure of the Various Mobile Money Providers in Uganda

UTL MSENTE SUBSCRIBER TARRIFS 2011

Transaction Fee (UGX)

Amount Sending by Registered Subscriber

Sending by Non Registered Subscriber

Withdrawals by Registered Subscriber

1-500 700 N/A N/A

500-5,001 700 700 300

5,001-30,000 700 1,500 700

30,001-60,000 700 1,900 900

60,001-125,000 700 3,500 1500

125,001-250,001 700 6,800 2900

250,001-500,000 700 9,000 4900

500,001-1,000,000 700 18,000 8900

1,000,001-2,000,000 700 35,000 17000

2,000,001-4,000,000 700 N/A N/A

4,000,001-10,000,000 700 N/A N/A

6

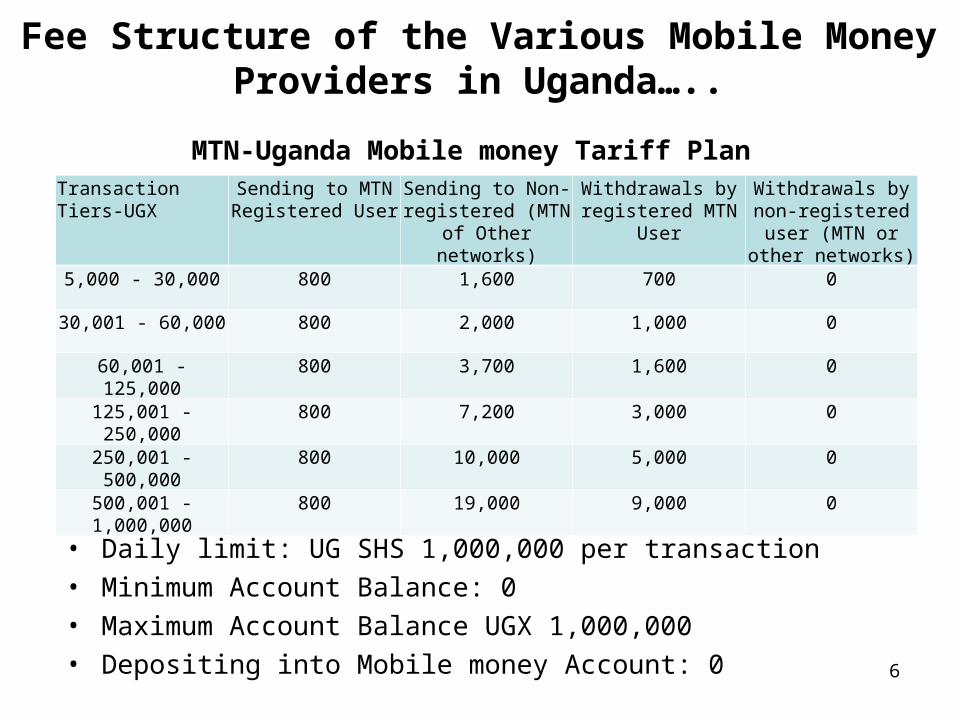

Fee Structure of the Various Mobile Money Providers in Uganda…..

MTN-Uganda Mobile money Tariff Plan

• Daily limit: UG SHS 1,000,000 per transaction• Minimum Account Balance: 0 • Maximum Account Balance UGX 1,000,000• Depositing into Mobile money Account: 0

Transaction Tiers-UGX

Sending to MTN Registered User

Sending to Non-registered (MTN of

Other networks)

Withdrawals by registered MTN

User

Withdrawals by non-registered user (MTN or other

networks)5,000 - 30,000 800 1,600 700 0

30,001 - 60,000 800 2,000 1,000 0

60,001 - 125,000 800 3,700 1,600 0

125,001 - 250,000 800 7,200 3,000 0

250,001 - 500,000 800 10,000 5,000 0

500,001 - 1,000,000 800 19,000 9,000 0

7

Fee Structure of the Various Mobile Money Providers in Uganda…

Airtel-Uganda Mobile money Tariff Plan (UGX)

• Maximum Transfer amount (per transaction): 1000000• Maximum Transactions Buy Zap/Cash-In per day: 50• Maximum Transactions Sell Zap/Cash-Out per day: 50• * Rates determined by supply and demand • All values quoted above are in Ushs and are inclusive of VAT

Amount Buy Zap (Cash-in) Sell Zap (Cash-Out)

1-5,000 250 250

5,001 - 30,000 200 1000

30,001 - 60,000 300 1200

60,001 - 125,000 400 1600

125,001 - 250,000 500 2500

250,001 - 500,000 1000 3000

500,001 - 1,000,000 2000 5000

7

8

(a) Fee Structure of the various Mobile Money Providers & Service Uptake

9

(b) Fee Structure of the various Mobile Money Providers & Service Uptake

10

Uganda; Mobile Money Services by Provider

MTN-Uganda Uganda Telecom Limited

Airtel-Uganda

Sending and Buying airtime (no charge)

Sending and Buying airtime (no charge)

Sending and Buying airtime (no charge)

(Cash-In & Cash-out) Money transfers

(Cash-In & Cash-out) Money transfers

(Cash-In & Cash-out) Money transfers

Utility bills: DSTV Water bills (NWSC)Star Times

Utility bills: DSTV Water bills (NWSC)Star Times

School fees payments School fees payments

Mobile Banking with Post Bank and Pride Microfinance

11

Correlation Matrix for Mobile Money Facilitating Conditions

Correlations

1 .231** .196* .325** .204*

. .005 .015 .000 .012

156 148 152 153 152

.231** 1 .332** .136 .472**

.005 . .000 .100 .000

148 148 146 148 145

.196* .332** 1 .350** .461**

.015 .000 . .000 .000

152 146 152 151 149

.325** .136 .350** 1 .388**

.000 .100 .000 . .000

153 148 151 153 150

.204* .472** .461** .388** 1

.012 .000 .000 .000 .

152 145 149 150 152

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

MM Network Coverage

Support from MM SvceProviders

Clear Instructions onMM usage

MM service availability

Help Desk availablefor MM

MM NetworkCoverage

Support fromMM SvceProviders

ClearInstructions

on MM usageMM serviceavailability

Help Deskavailablefor MM

Correlation is significant at the 0.01 level (2-tailed).**.

Correlation is significant at the 0.05 level (2-tailed).*.

12

Correlation Matrix for Perceived Ease of Use

Correlations

1 .772** .377** .379** .499**

. .000 .000 .000 .000

150 149 146 142 144

.772** 1 .380** .463** .604**

.000 . .000 .000 .000

149 150 146 142 144

.377** .380** 1 .484** .415**

.000 .000 . .000 .000

146 146 148 141 143

.379** .463** .484** 1 .641**

.000 .000 .000 . .000

142 142 141 143 140

.499** .604** .415** .641** 1

.000 .000 .000 .000 .

144 144 143 140 147

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

MM svces are easy tolearn to use

MM svces are easy tounderstand

information easy to getfrom MM Svce providers

Skil l Acquisition easywith MM

Using MM svces is easy

MM svcesare easy tolearn to use

MM svcesare easy tounderstand

informationeasy to get

from MM Svceproviders

Skil lAcquisition

easy with MMUsing MM

svces is easy

Correlation is significant at the 0.01 level (2-tailed).**.

13

Facilitating Conditions and Perceived Ease of Use

• The quality of MM services is dependent on amongst others the quality of mobile services and the agent-specific attributes [e.g. liquidity of agents, MM service-mix provided, security]. We delve into this on slide 14.

• Further research should investigate the rationale for consumers subscribing to all MM providers; risk exposure associated with this;

14

Operator-Consumer Dialogue on Quality of Service

Accessibility to M.M services Network coverage (no. of branches) Liquidity availability for clients at all times Possibility of inter-network transactions at reduced

cost Security of clients’ money ensured by providers Perceived Ease of Use of M.M services (flexibility &

convenience) Perceived Usefulness of M.M services (reduced time

costs)

15

Reflections on the Research ProcessWhat has Worked/Successes• Secondary data sources (from Bank of Uganda);• Questionnaire; • Focused-Group Discussions (operator-consumer dialogue);

Pitfalls• Tariff plans not easily comparable across providers;• Service uptake information from Bank of Uganda is too

aggregated and providers cannot easily release it;

Next Steps• Complete remaining research procedures;• Prepare a manuscript for submission to a journal 15

16

New Questions that the Research to date has Posed

• Who is the regulator of mobile money services? Providers; The Central Bank, Uganda Communications Commission?

• Who set the tariff plans being implemented by agents? • If a client sends money and it does not get received

where does one seek redress? BOU, UCC, National Information Technology Authority – Uganda (NITA-U) or providers?

• The tariff plans differ depending upon the provider. What are the implications of this?

16

17

Mobile Money in Rural areas

Thank You!17

Top Related