Languages

Pages

Legal

© 2009 Forrester Research, Inc. Reproduction Prohibited

Бизнес-технологии в Век Потребителя: за пределы CRM и лояльности...

Сергей Македонский

Forrester Research

Форум SAP, 06 ноября 2014 г.

• Век Потребителя и 4 императива для бизнеса

• Тенденции глобального рынка бизнес-технологий 2010-2015 гг.

• "Цифровое поведение" потребителя

• Customer Experience - ключевой тренд торговли

• Современные инструменты анализа бизнес-технологий

План презентации

Экспертная

поддержка

продукта

Возможности

самообслуживания

Систематический

«канальный»

опыт

Поддержка

по электронным

каналам

Компания

знает мою

«историю»

Проактивная

поддержка и

уведомления

«Увеличенные»

часы

обслуживания

Сегодняшний

потребитель

Ожидания и запросы потребителей постоянно растут…

Люди используют разнообразные каналы в рамках одного потребительского действия

Помощь человека

нужна для

взаимодействия. . .

. . . сложного

. . . редкого

. . . с высокой эмоцио-

нальной составляющей

Самообслуживание

предназначено для

взаимодействия. . .

. . . простого

. . . частого

. . . с низкой эмоцио-

нальной составляющей

Начало заполнения

онлайн анкеты

для приобретения

продукта/услуги

1 Звонок в колл-центр

для уточнения

специфических

деталей продукта/услуги 2

3

Завершение заполнения

анкеты и онлайн-

сравнение

с другими предложениями 4

Звонок для уточнения,

«покрывается ли страхов-

кой здание нестандарт-

ной конструкции» Покупка продукта/услуги

онлайн/офлайн

5

Source: GO-Gulf.com (http://www.go-gulf.com)

Связь

Созидание Потребление

Контроль

Блоги

IM /

чаты

SMS

Рингтоны Music

Поиск

Новости

Видео ТВ

Web-путешествия

Игры

Карты

Здоровье

Платежи Торговля

Банкинг

Билеты

Парковка

Социальные

сети

Картинки

E-mail / MMS

Organizer Голос

Формируется новая мобильная цифровая экосистема

© 2013 Forrester Research, Inc. Reproduction Prohibited 7

Мобильность - основа «цифрового разрыва»

Russia device landscape - 2017

105M

Unique mobile subscribers 142M

Total Population

55% Of unique mobile subscribers

have smartphones

49M Mobile internet users

Tablet installed base of 26.5M Source: Forrester Research World Mobile Adoption Forecast 2013-2018,

Forrester Research World Smartphone Adoption Forecast 2012-2017,

Forrester Research World Tablet Adoption Forecast 2012-2017

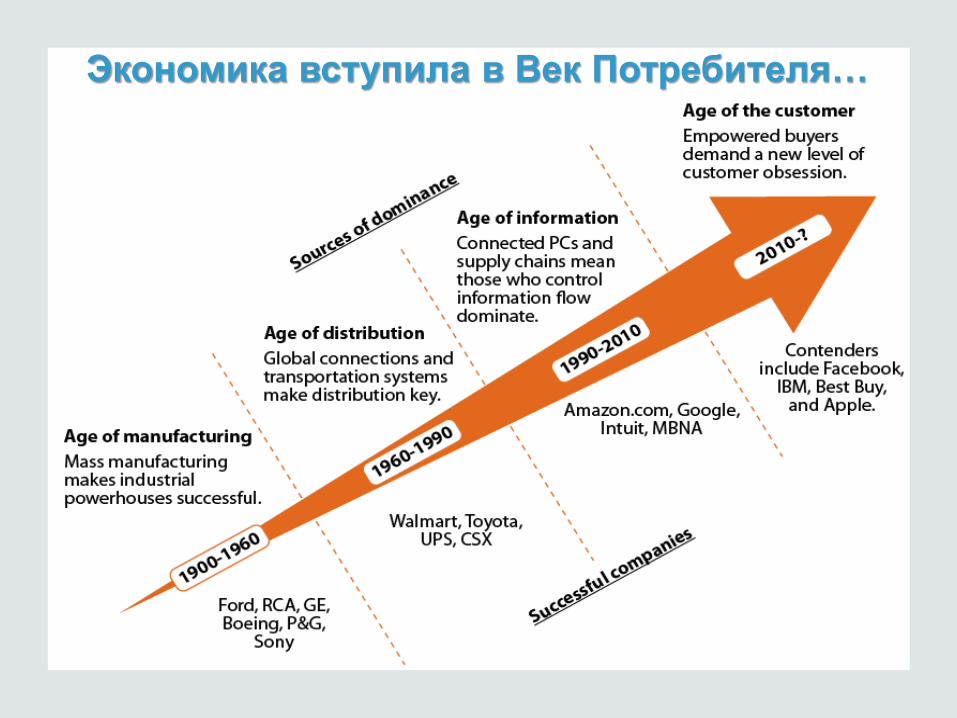

Технологии значительно усиливают возможности потребителей и сотрудников предприятий, а также

и их прямое влияние на бизнес

Экономика вступила в Век Потребителя…

© 2014 Forrester Research, Inc. Reproduction Prohibited 10

. . . с четырьмя императивами для бизнеса

Transform

the customer

experience

Embrace

the mobile

mind shift

Become

a digital

disruptor

Век

Потреби-

теля

Turn big data

into business

insights

© 2012 Forrester Research, Inc. Reproduction Prohibited

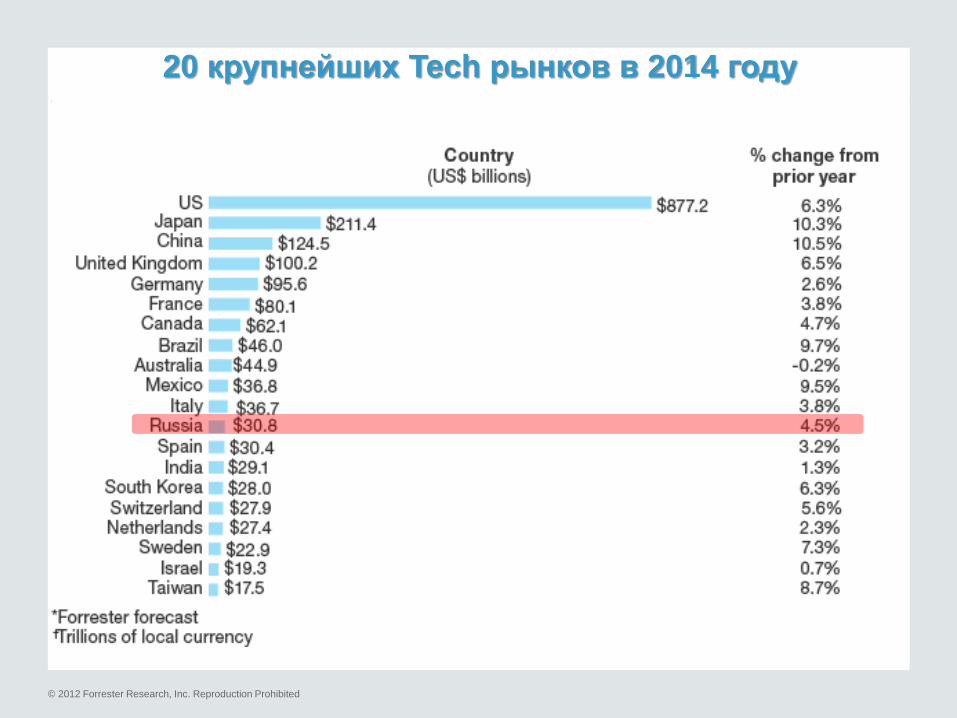

20 крупнейших Tech рынков в 2014 году

© 2012 Forrester Research, Inc. Reproduction Prohibited

20 самых быстрорастущих Tech рынков в 2014 году

The Global Tech Industry Wheel 2014

© 2012 Forrester Research, Inc. Reproduction Prohibited

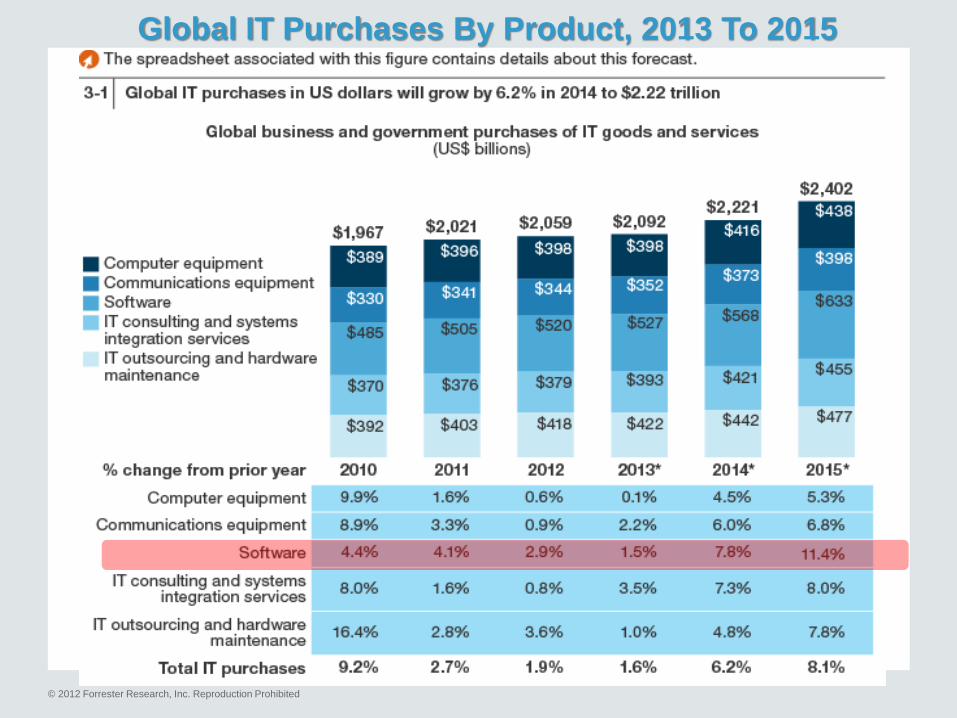

Global IT Purchases By Product, 2013 To 2015

© 2012 Forrester Research, Inc. Reproduction Prohibited

Tech Twelve Keep Pace With BRICTSAM

«Клиентские» технологии Mobile, Cloud, Smart - опережающие темпы роста

Планшеты – единственный растущий сегмент компьютерного оборудования

© 2012 Forrester Research, Inc. Reproduction Prohibited

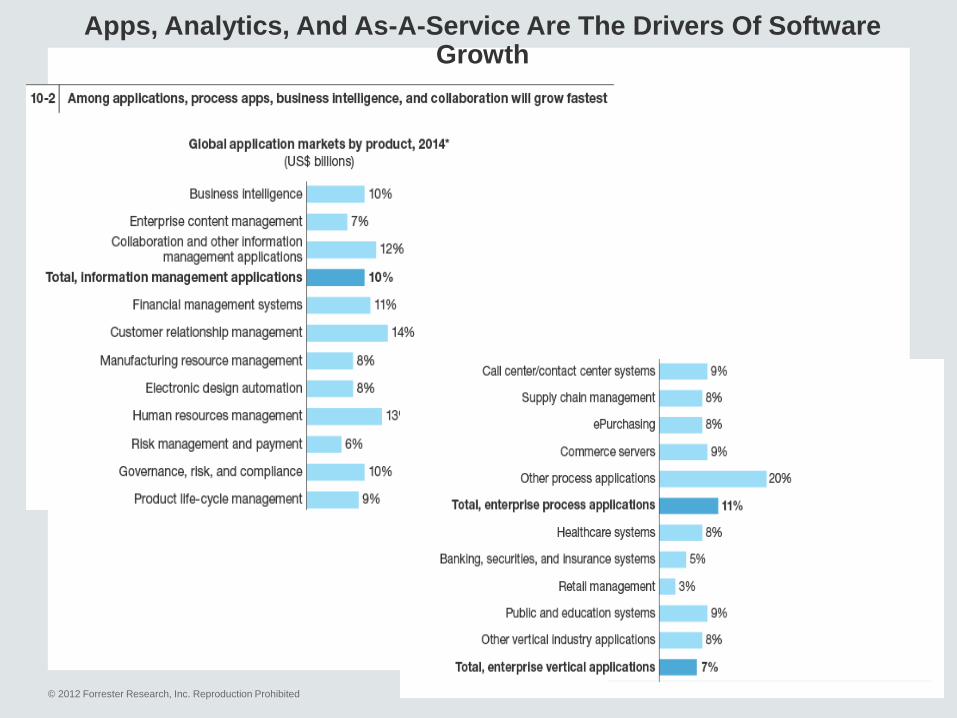

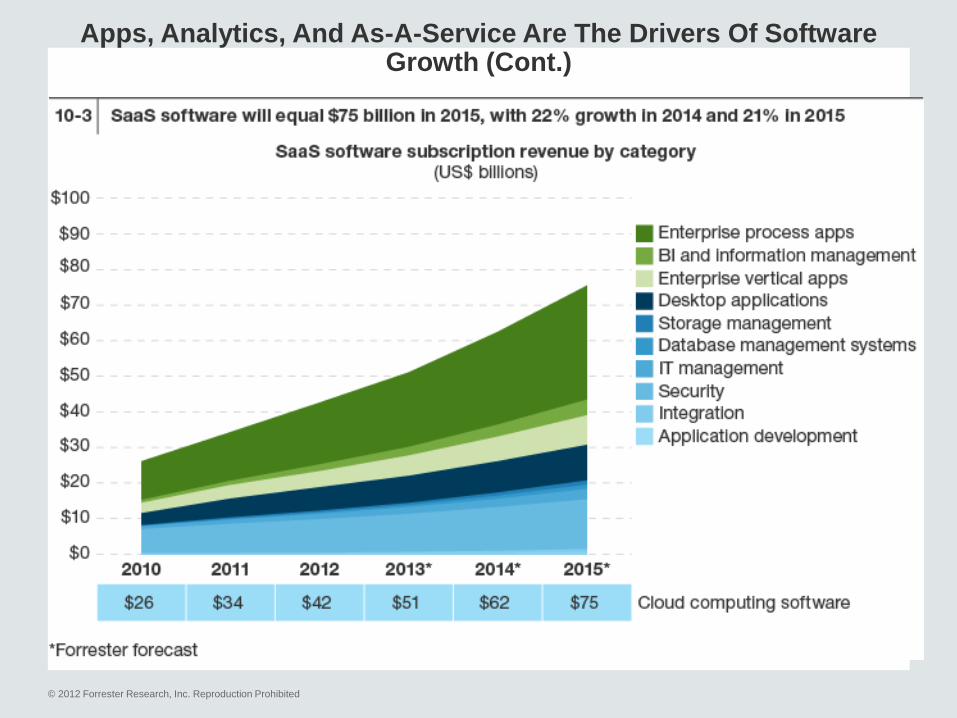

Apps, Analytics, And As-A-Service Are The Drivers Of Software Growth

© 2012 Forrester Research, Inc. Reproduction Prohibited

Apps, Analytics, And As-A-Service Are The Drivers Of Software Growth (Cont.)

© 2012 Forrester Research, Inc. Reproduction Prohibited

Smart-приложения, BI и аналитика – лидеры роста рынка ПО

20

© 2014 Forrester Research, Inc. Reproduction Prohibited

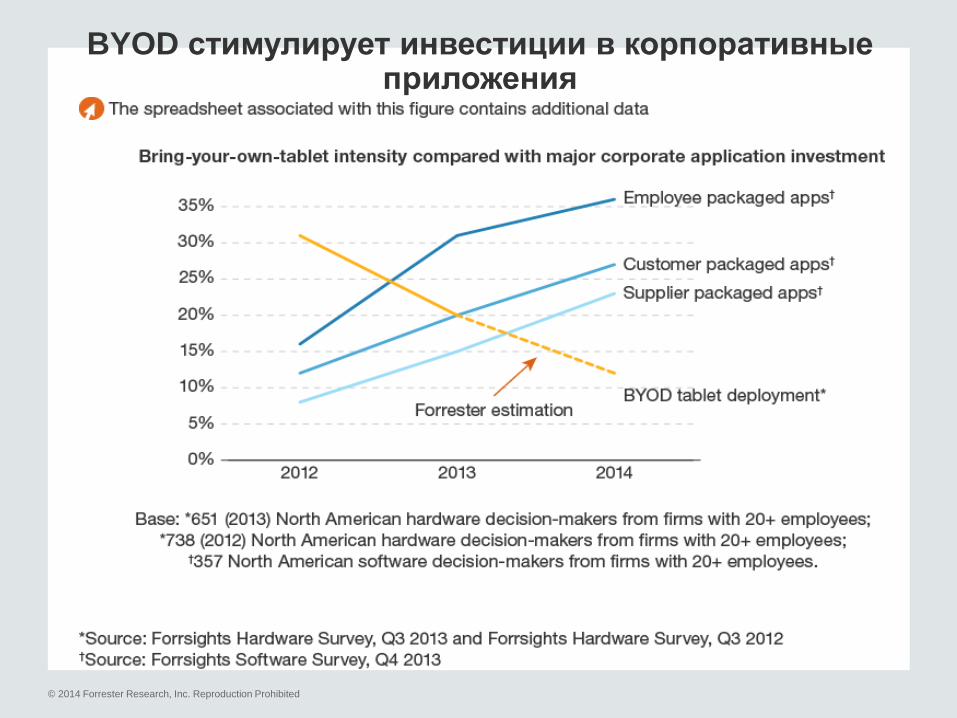

BYOD стимулирует инвестиции в корпоративные приложения

РФ: 2 января vs. 20 октября 2014 г.

-20%

Рубль/Доллар Oanda.com

-26%

Нефть марки Brent

iea.gov

-13%

Общие расходы на ИКТ

IDC

22

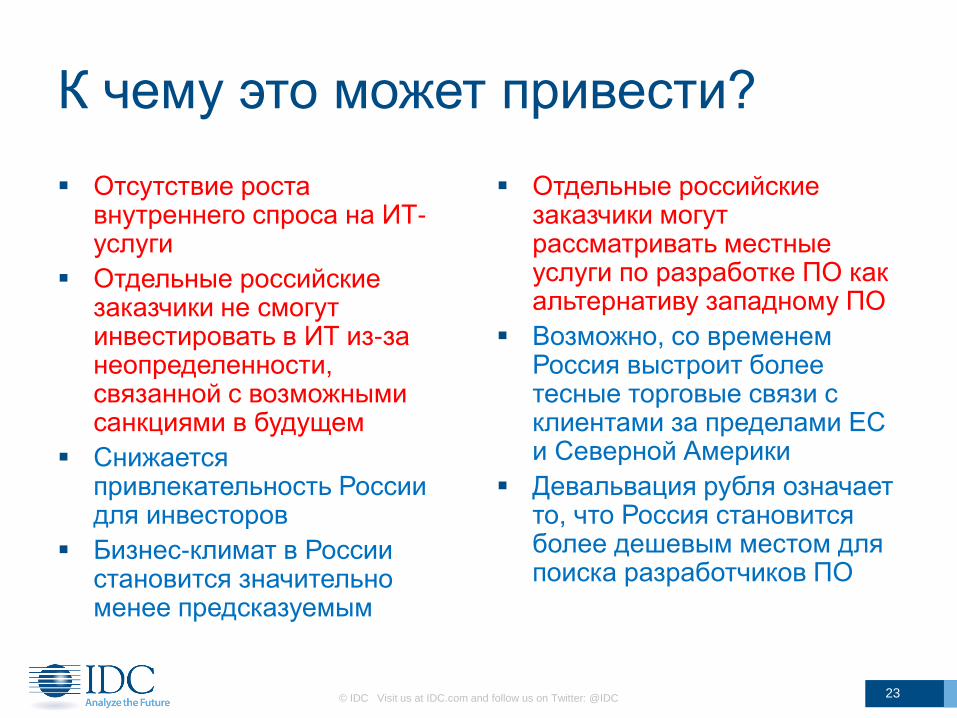

К чему это может привести?

Отсутствие роста внутреннего спроса на ИТ-услуги

Отдельные российские заказчики не смогут инвестировать в ИТ из-за неопределенности, связанной с возможными санкциями в будущем

Снижается привлекательность России для инвесторов

Бизнес-климат в России становится значительно менее предсказуемым

Отдельные российские заказчики могут рассматривать местные услуги по разработке ПО как альтернативу западному ПО

Возможно, со временем Россия выстроит более тесные торговые связи с клиентами за пределами ЕС и Северной Америки

Девальвация рубля означает то, что Россия становится более дешевым местом для поиска разработчиков ПО

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 23

Замечаете ли вы рост или

сокращение инвестиций в России

со стороны поставщиков ИТ?

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 24

0% 10% 20% 30% 40% 50% 60%

Increasing levels of investment

Reducing levels of investment

Maintaining current investment levels

Can't sayЗатрудняюсь сказать

Сохраняют текущий

уровень инвестиций

Сокращают

инвестиции

Увеличивают

инвестиции

© 2013 Forrester Research, Inc. Reproduction Prohibited 25

8%

14%

18%

47%

19%

32%

13%

8%

10%

15%

18%

39%

58%

26%

46%

16%

15%

9%

0% 20% 40% 60% 80%

Transfer money between personal accounts (Wkly‡)

Check financial accounts/statements (Wkly‡)

Mobile banking (P3M†*)

Access Internet in stores (while shopping)†

Purchase physical goods (Monthly+ **)

Research physical goods (Monthly+ **)

Finance/Banking (PM*)

Payment (e.g. PayPal) (PM*)

Shopping (e.g. Amazon) (PM*) Russia

EU7

Ownership is only part of the equation Mobile activities demonstrate levels of sophistication

Reta

il/eC

om

F

inancia

l A

pplic

ations

Source: European Technographics Online Benchmark Survey, 2013, Russian Technographics Online Benchmark Survey, 2013

Base: Various, see Appendix for details

The Mobile Mind Shift Index

• The reason we have developed this

framework is because people are now

becoming more accustomed to

accomplishing tasks and finding

information instantly and now expect

immediate, always available

convenience from every company they

interact with.

• The Mobile Mind Shift Index (MMSI)

determines how far people have

shifted.

• Based on our research we have found

that companies whose customers have

above-average MMSIs and who have

more than 35% Adapters, Immersers,

and Perpetuals must move urgently to

deliver on their customers' mobile

expectations.

More Russian adults rely on financial advisors than European adults in general

All European Adults*

All Russian Adults 16% 7% 9% 15%

18% 24% 54% 55%

Base: 26,925 European adults age 16+; 3,105 Russian adults age 16+

Financial Self-Directedness Segmentation

© 2013 Forrester Research, Inc. Reproduction Prohibited 28

Новая «нестандартная» сегментация: Ценности-Технологии (пример)

© 2013 Forrester Research, Inc. Reproduction Prohibited 29

Consumer Technographics DATA-DRIVEN INSIGHTS ACROSS A RANGE OF CONSUMER BEHAVIOR

Over 400,000 annually completed surveys across 21 countries on how

consumers:

› Shop, consume media, get services, learn, and bank

› Spend time, interact, communicate, and entertain themselves

› Are motivated by technology-driven attitudes and values

› Own and relate to over 1500 consumer brands and media

Device

Ownership

Technology

Behaviors

Technology

Attitudes

Brand

Ownership

Media

Consumption

Consumer Technographics Russia: обзор данных

© 2011 Forrester Research, Inc. Reproduction Prohibited 31

43%

7%

18%

31%

57%

63%

5%

8%

67%

43%

10%

36%

32%

63%

67%

2%

12%

33%

Other source

Radio

Newspapers

Magazines

TV

High street shops

The Internet on a mobile device

Email newsletters

The Internet on a computer

over 30

under 30

Age

31

On

line

So

urc

es

Offlin

e S

ou

rce

s

Please indicate the top 3 media sources you currently depend on the

most for obtaining information on Small domestic appliances

Base: 2283 urban Russian consumers age 16+ who used a media source for small domestic appliances

(consumers that responded none or did not answer the question were removed)

Source: European Technographics Benchmark Survey

The top 3 research sources for small domestic appliances among

urban Russian age under 30 are the internet, shops and TV

© 2011 Forrester Research, Inc. Reproduction Prohibited 32 32

0%

6%

96%

1%

7%

95%

By post/phone/catalog

Via the Internet

In a shop

over 30

under 30

Age

Where did you buy it from in the past 3 months?

16% 18% under 30

over 30

Age

Did you buy small domestic appliances

(e.g. kettle) in the past 3 months?

The majority of urban Russian small domestic appliance buyers

used a store for purchase

Base: 275 urban Russian consumers age 16+ who bought small domestic

appliances in the past 3 months

Base: 2283 urban Russian consumers age 16+

© 2011 Forrester Research, Inc. Reproduction Prohibited 33

Base: 164 urban Russian consumers age 16+ who bought consumer electronics most recently (out of a choice) - having first researched it

Source: European Technographics Benchmark Survey

Thinking of this recently researched purchase (consumer electronics.e.g. hairdryer), please

indicate which of the following sources of information you used to research it?

0%

0%

0%

0%

1%

2%

2%

2%

3%

3%

5%

6%

6%

10%

12%

14%

14%

15%

16%

29%

39%

Promotional email

Social Networking site - interaction with someone I know

Social Networking site - interaction with a company or brand

Promotional text message

A retailer’s website (e.g. Tesco, Argos)

Other website

Blogs/newsgroups

A manufacturer’s website

Online professionally-written review

Online consumer-written review

An online ad

A comparison shopping website (e.g. Kelkoo)

A search engine (e.g. Google)

Radio

Promotion sent by mail

Newspaper

Outdoor advertising (e.g. posters)

Magazine

TV

Talking with friends or family

Went into a store

76%

researched

it offline

56%

researched

it online

Offline and online research sources are used for consumer

electronics purchases in urban Russia

© 2011 Forrester Research, Inc. Reproduction Prohibited 34

Thinking of this recently researched purchase (consumer electronics e.g. hairdryer), please indicate

which of the following sources of information you used to research it?

Which one of these had the most influence on your final purchase decision?

Outdoor advertising (e.g. posters)

Magazine

TV

Online consumer-written review

An online ad

A comparison shopping website (e.g. Kelkoo)

A search engine (e.g. Google) Talking with friends or

family

Went into a store

0%

10%

20%

30%

40%

50%

60%

70%

0% 10% 20% 30% 40% 50% 60% 70%

Mo

st In

flu

en

ce

Used for research

The store is not only the research source used by most urban Russians

who purchased consumer electronics, but it also had the most influence

Base: 164 urban Russian consumers age 16+ who bought consumer electronics most recently (out of a choice) - having first researched it

Source: European Technographics Benchmark Survey

© 2011 Forrester Research, Inc. Reproduction Prohibited 35

Did you change your mind about what brand to buy as a result of researching this product?

7%

9%

21%

64%

I didn’t have a brand in mind in the first place

Don’t remember

Yes, I did change my mind

No, I didn’t change my mind

64% of urban Russian consumer electronics buyers had a

brand in mind already and didn’t change their mind

Base: 164 urban Russian consumers age 16+ who bought consumer electronics most recently (out of a choice) - having first researched it

Source: European Technographics Benchmark Survey

© 2011 Forrester Research, Inc. Reproduction Prohibited 36

How did you end up buying this product?

0% 0%

1%

16%

By mail order

On the internet using a cell phone/Smartphone

On the internet using a computer (e.g. desktop, netbook/laptop,tablet)

Base: 164 urban Russian consumers age 16+ who bought consumer electronics most recently (out of a choice) - having first researched it

Source: European Technographics Benchmark Survey

16% of urban Russian consumer electronics buyers bought

it online and 83% in store

Researched

Online

Bought

Online

Bought

Offline

Researched

Offline

Bought

Online

Bought

Offline

16% 39% 6% 70%

© 2011 Forrester Research, Inc. Reproduction Prohibited 37 © 2014 Forrester Research, Inc. Reproduction Prohibited 37

Transform the

customer

experience

and the

organization

to deliver it

Use mobile

moments to

transform

customer

perceptions

Use digital to

drive CX

innovations and

competitive

advantage

Use big data

to design and

deliver quality

experiences

Age of the

customer

. . . for customer experience (CX)

© 2011 Forrester Research, Inc. Reproduction Prohibited 38

© 2011 Forrester Research, Inc. Reproduction Prohibited 39

© 2011 Forrester Research, Inc. Reproduction Prohibited 40

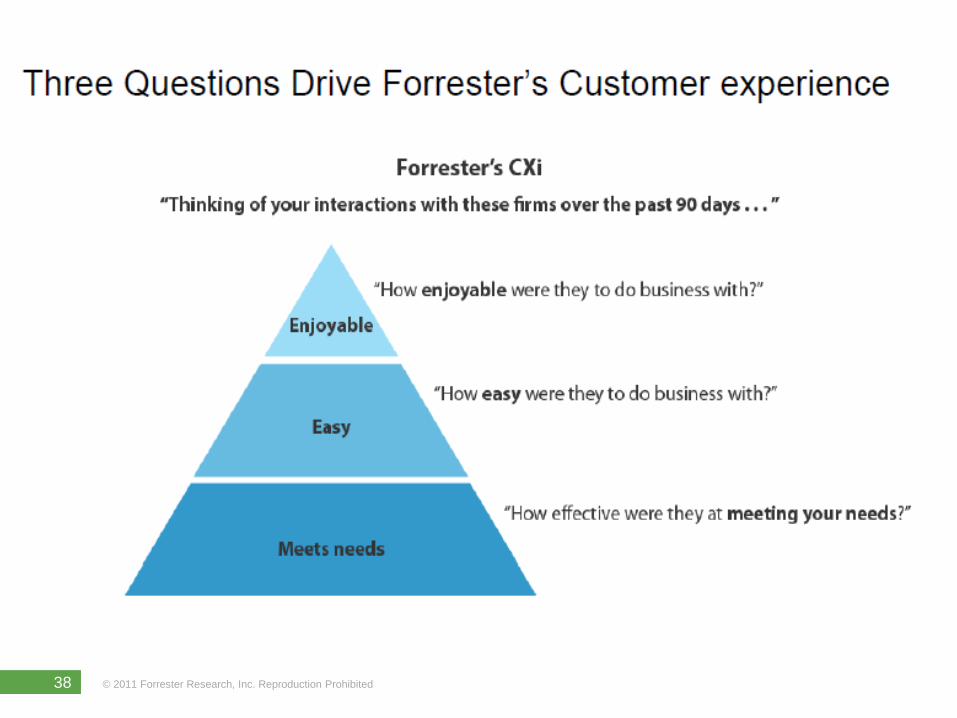

Forrester CXi - Customer Experience Index

© 2011 Forrester Research, Inc. Reproduction Prohibited 41

Свод лучших практик в сфере Customer Experience: книга Outside - In

© 2011 Forrester Research, Inc. Reproduction Prohibited 42

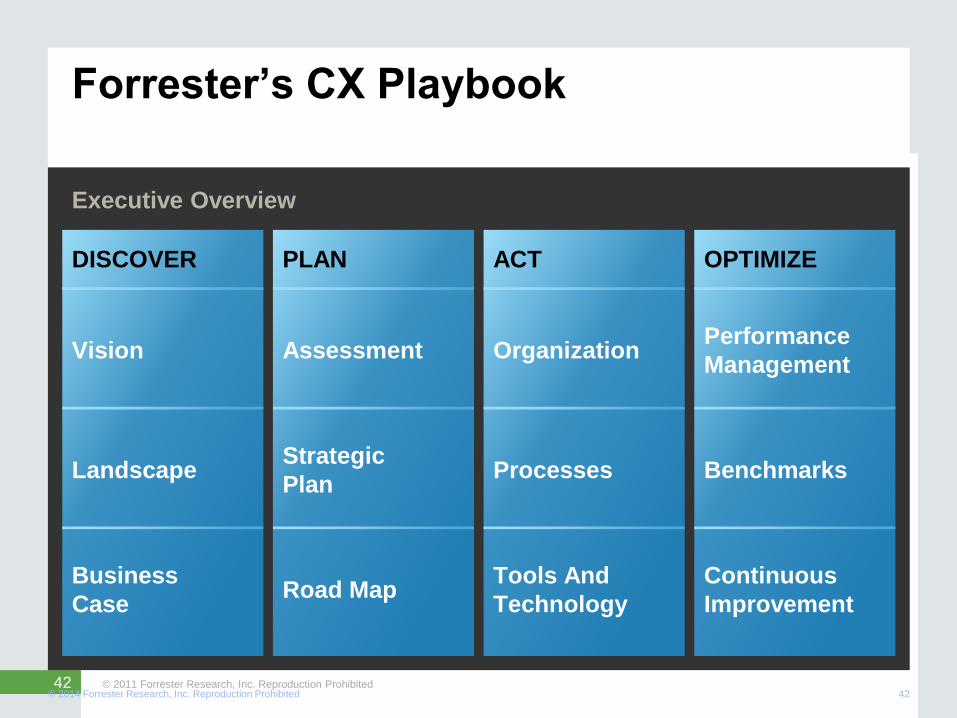

DISCOVER PLAN ACT OPTIMIZE

© 2014 Forrester Research, Inc. Reproduction Prohibited 42

Executive Overview

Forrester’s CX Playbook

Benchmarks

Continuous

Improvement

Performance

Management

Processes

Tools And

Technology

Organization

Strategic

Plan

Road Map

Assessment

Landscape

Business

Case

Vision

© 2011 Forrester Research, Inc. Reproduction Prohibited 43 © 2014 Forrester Research, Inc. Reproduction Prohibited 43

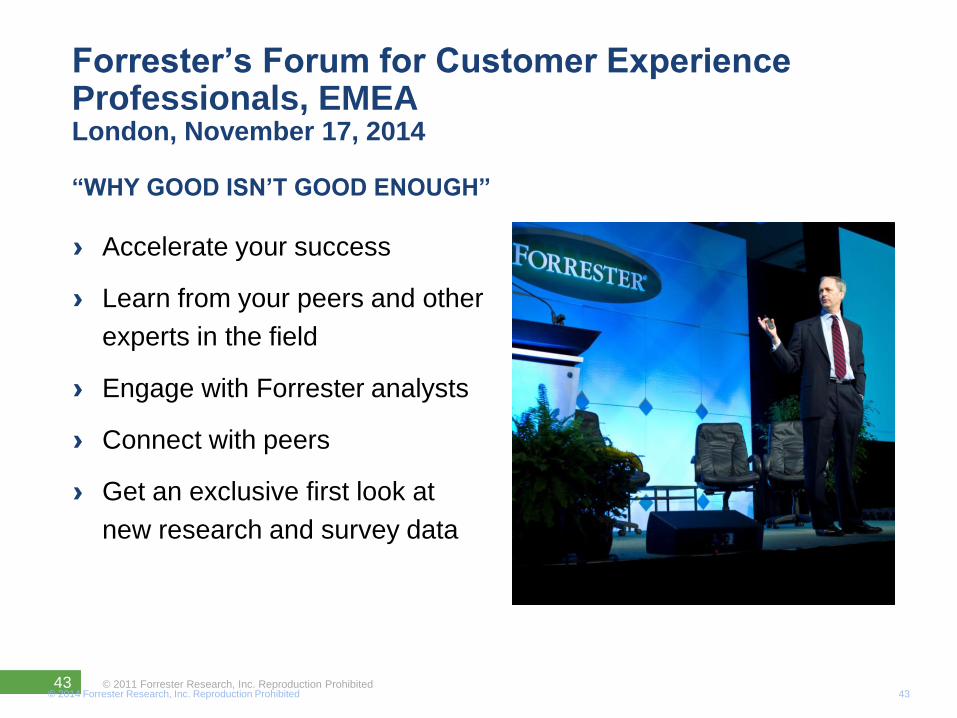

Forrester’s Forum for Customer Experience Professionals, EMEA London, November 17, 2014

“WHY GOOD ISN’T GOOD ENOUGH”

› Accelerate your success

› Learn from your peers and other

experts in the field

› Engage with Forrester analysts

› Connect with peers

› Get an exclusive first look at

new research and survey data

© 2009 Forrester Research, Inc. Reproduction Prohibited

Спасибо!

Сергей Македонский

www.forrester.com

© 2013 Forrester Research, Inc. Reproduction Prohibited 45

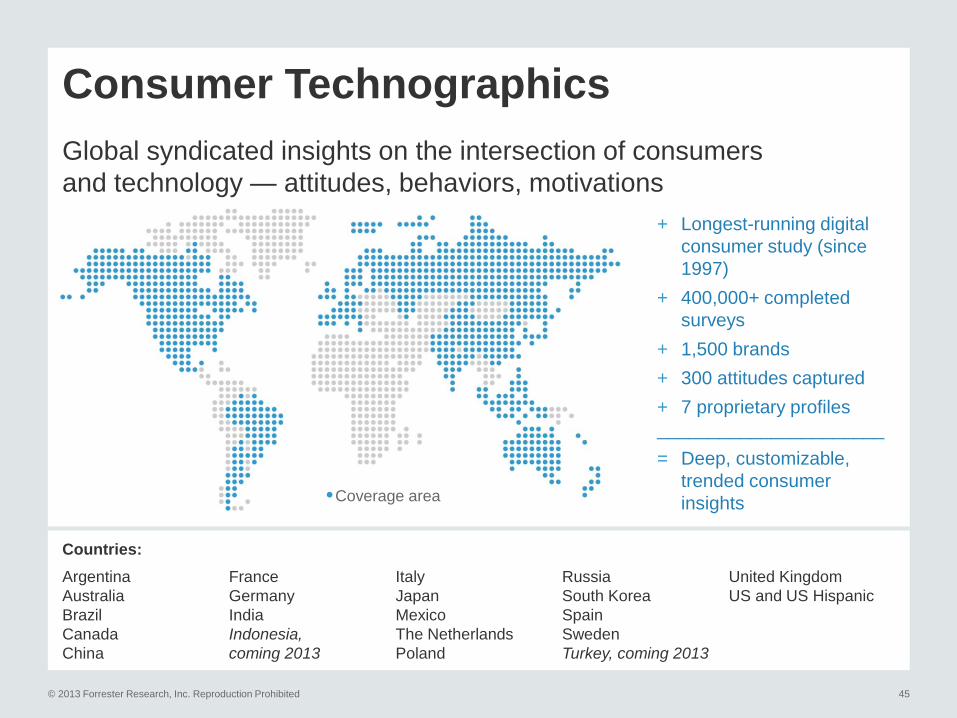

Countries:

Argentina

Australia

Brazil

Canada

China

France

Germany

India

Indonesia,

coming 2013

Italy

Japan

Mexico

The Netherlands

Poland

Russia

South Korea

Spain

Sweden

Turkey, coming 2013

United Kingdom

US and US Hispanic

Consumer Technographics Global syndicated insights on the intersection of consumers

and technology — attitudes, behaviors, motivations

+ Longest-running digital

consumer study (since

1997)

+ 400,000+ completed

surveys

+ 1,500 brands

+ 300 attitudes captured

+ 7 proprietary profiles

______________________

= Deep, customizable,

trended consumer

insights

Coverage area

© 2013 Forrester Research, Inc. Reproduction Prohibited 46

Digital consumer profiling

Understand new and changing markets.

Customer analysis Analyze your

customers, partners, and competitors.

Consumer segmentation

Target and profile the right customers.

Product and service innovation

Identify the right product features.

Marketing and advertising

Plan effective marketing

campaigns.

Marketers turn to Technographics

© 2013 Forrester Research, Inc. Reproduction Prohibited 47

Business questions answered FORRESTER CONSUMER TECHNOGRAPHICS®

› How will disruptive technologies impact my strategy?

› Does my social media strategy align with my customer’s

expectations?

› What data insight can I use to help guide my mobile strategy?

› What consumers drivers and inhibitors support my multichannel

strategy?

› What are my customer’s touch points in their purchase journey?

› What markets are best to prioritize in my globalization strategy?

› What are my customer segments attitudes towards advertising?

› How are my customers different from my competitors’ customers?

Global Digital

Profile Deck Every digital strategy starts with

the consumer. This customizable

deliverable explores the digital

lifestyle of three profile groups in

order to inform interactive

marketing, eBusiness and

product strategy decisions.

Source: Global Technographics Online Benchmark Surveys

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

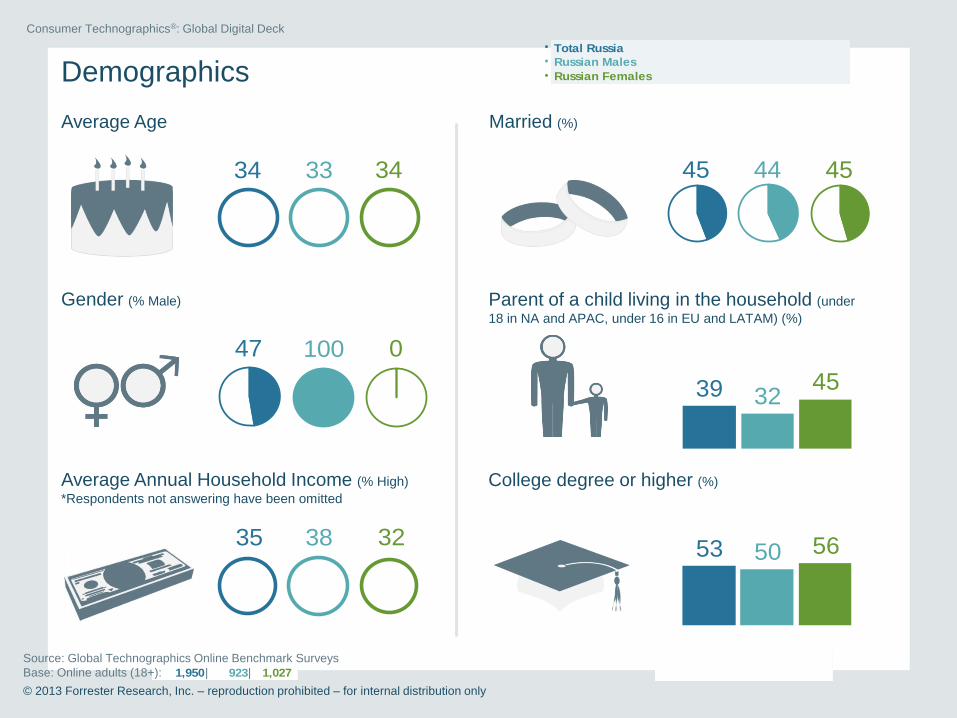

Russian online adults 18+

Russian online males adults 18+

Russian online female adults 18+

Global data should be analyzed

with caution; factors such as

sample properties and country

culture can impact the results

when comparisons are made

between countries and/or regions.

1,027 923 1,950

34 33 34 45 44 45

Demographics

Source: Global Technographics Online Benchmark Surveys

Base: Online adults (18+): | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

College degree or higher (%)

Gender (% Male)

Average Annual Household Income (% High)

*Respondents not answering have been omitted

Average Age Married (%)

Parent of a child living in the household (under

18 in NA and APAC, under 16 in EU and LATAM) (%)

39 3245

47 100 0

35 38 32

•

•

•

Total Russia

Russian Males

Russian Females

Consumer Technographics®: Global Digital Deck

53 50 56

Please us samples with <100

respondents directionally

1,027 923 1,950

53

40

61

43

87

92

3

Social Technographics® ladder (%)

52 54

38 42

63 59

47 39

83 90

92 92

4 2

•

•

•

Total Russia

Russian Males

Russian Females

Source: Global Technographics Online Benchmark Surveys

Base: Online adults (18+): | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

Consumer Technographics®: Global Digital Deck

Please us samples with <100

respondents directionally

1,027 923 1,950

58 64 53

64 65 63

38 46 31

11 8 14

5 6 4

1 2 1

Mobile Technographics® ladder (%)

•

•

•

Total Russia

Russian Males

Russian Females

Source: Global Technographics Online Benchmark Surveys

Base: Online adults (18+): | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

Consumer Technographics®: Global Digital Deck

Please us samples with <100

respondents directionally

1,027 923 1,950

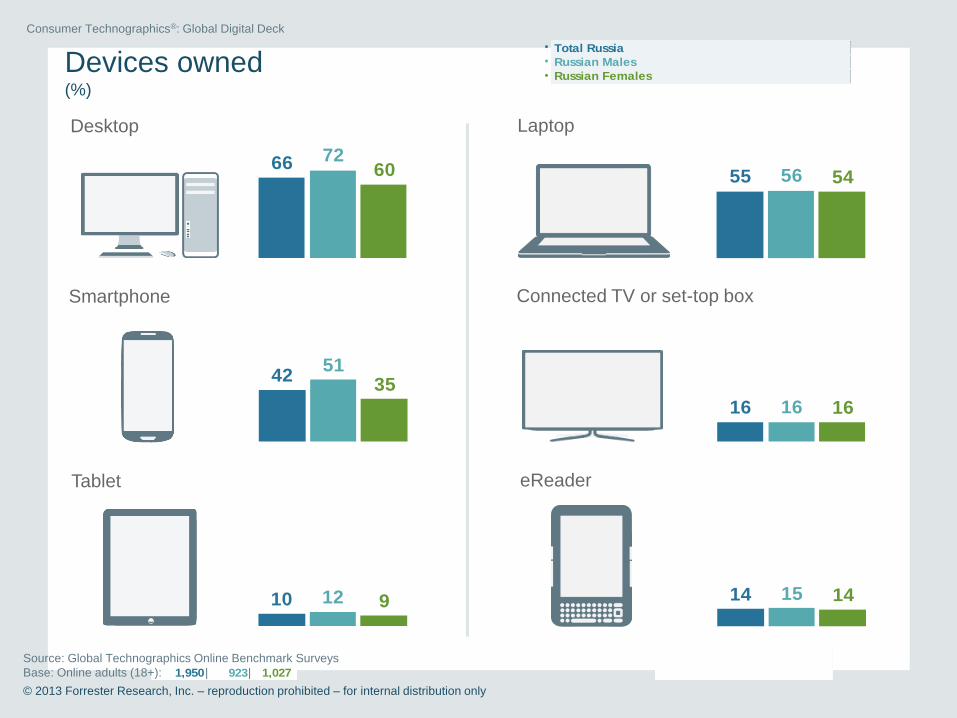

Devices owned (%)

Tablet

Smartphone

Desktop

eReader

Connected TV or set-top box

Laptop

10 12 9 14 15 14

4251

35

16 16 16

66 7260 55 56 54

•

•

•

Total Russia

Russian Males

Russian Females

Source: Global Technographics Online Benchmark Surveys

Base: Online adults (18+): | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

Consumer Technographics®: Global Digital Deck

Please us samples with <100

respondents directionally

1,027 923 1,950

Media consumption

In a typical week, how many hours do you spend:

*Breakdown of traditional media time (hours)

Using the internet

(for work or personal

purposes)

With traditional media*

Watching TV on a TV Listening to the radio Reading print newspapers Reading print magazines

23

13

1

2

24

14

1

2

22

13

1

2

1.4 1.66.9 3.4

1.5 1.66.7 3.7

7.1 3.1 1.4 1.6

•

•

•

Total Russia

Russian Males

Russian Females

Source: Global Technographics Online Benchmark Surveys

Base: Online adults (18+): | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

Consumer Technographics®: Global Digital Deck

Please us samples with <100

respondents directionally

1,020 907 1,927 1,027 923 1,950

PC and mobile activities

How frequently do you do the

following activities on a

computer or tablet?1

(% of users and doers)

Do monthly Do daily

Access social

networks

Play games

Listen to music

Watch TV / Video

Do monthly Do daily

How frequently do you do the

following activities on your

mobile phone?2

(% of users and doers)

81 80 82

67 70 65

85 85 85

74 76 72

55 51 58

40 40 41

52 52 52

33 36 31

39 43 35

47 5342

68 69 67

24 28 20

19 20 19

21 21 20

36 35 37

7 8 6

•

•

•

Total Russia

Russian Males

Russian Females

Source: Global Technographics Online Benchmark Surveys

Base: 1 Online adults (18+): | | 2 …with a mobile phone | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

Consumer Technographics®: Global Digital Deck

Please us samples with <100

respondents directionally

662 680 1,342 1,020 907 1,927

65

75

70

Mobile apps

Used any mobile apps

in the past month1

(% of those with a mobile phone)

Types of mobile apps used in past month2 (%)

40

46

34

60

63

57

44

45

44

61

59

62

25

30

20

11

15

5

12

16

8

8

8

7

18

21

14

11

16

6

•

•

•

Total Russia

Russian Males

Russian Females

Source: Global Technographics Online Benchmark Surveys,

Base: 1 Online adults (18+) with a mobile phone: | | 2 and who use apps: | |

© 2013 Forrester Research, Inc. – reproduction prohibited – for internal distribution only

Weather

Social networking

News

Finance

TV and video

Games

Music

Sports

Shopping

QR and bar codes

Consumer Technographics®: Global Digital Deck

Please us samples with <100

respondents directionally

Top Related