Languages

Pages

Legal

An Overview of theBrazilian Electricity Industry

Câmara de Comercialização de Energia Elétrica

Brazilian Market Operator

Roberto CastroAdministration Board

Agenda

1 – CCEE´s Role in the Brazilian Electricity Industry

2 – Highlights of Brazilian Economy and Electricity Industry

3 – Governance of the Brazilian Electricity Industry

4 – Brazilian Regulated Market

5 – Brazilian Free Market

6 - Conclusions

CCEE´s Role in the BrazilianElectricity Industry

CCEE´s role as Brazilan Market Operator

• Created in 1999, CCEE is a nonprofit private legal entity, regulated and supervised by ANEEL

• CCEE´s mission is to promote the electricity commercialization activities in Brazil, including ensuring the smooth market functioning and fostering discussions about the evolution of the power sector market

Accounting andsettlement

Tecnology and systems to improve market operation

Divulgation ofinformation and results

Training for agents andinstitutions

Registering of the powercontracts

Metering (generation andconsumption)

Main atributions

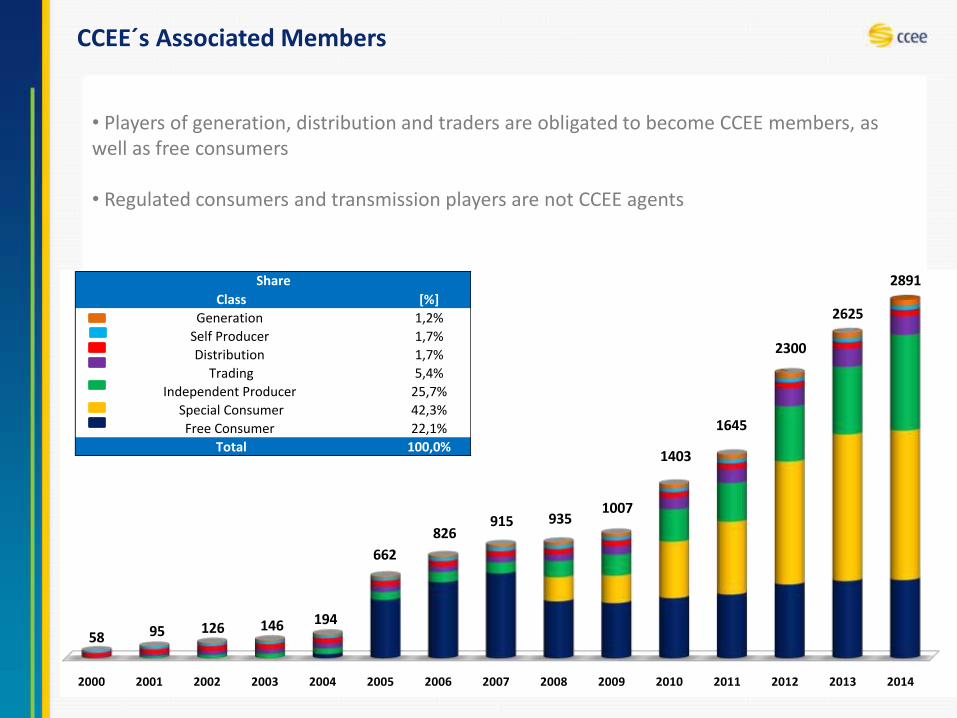

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

58 95 126 146 194

662

826915 935

1007

1403

1645

2300

2625

2891Class [%]

Generation 1,2%

Self Producer 1,7%

Distribution 1,7%

Trading 5,4%

Independent Producer 25,7%

Special Consumer 42,3%

Free Consumer 22,1%

Total 100,0%

Share

CCEE´s Associated Members

• Players of generation, distribution and traders are obligated to become CCEE members, as well as free consumers

• Regulated consumers and transmission players are not CCEE agents

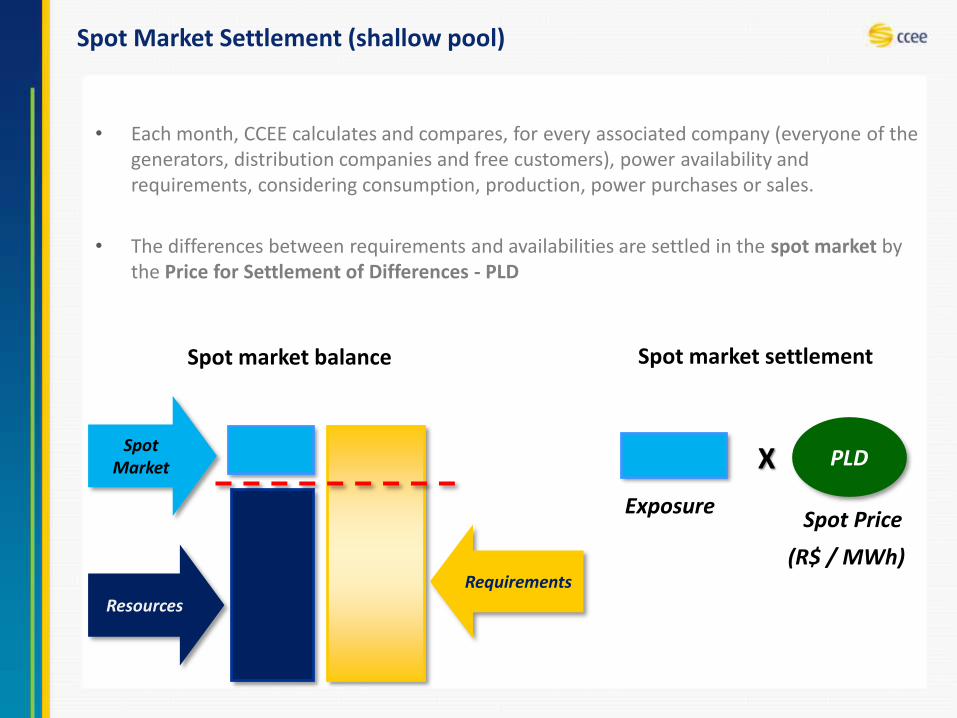

Spot Market Settlement (shallow pool)

Requirements

Resources

Spot Market

• Each month, CCEE calculates and compares, for every associated company (everyone of the generators, distribution companies and free customers), power availability and requirements, considering consumption, production, power purchases or sales.

• The differences between requirements and availabilities are settled in the spot market by the Price for Settlement of Differences - PLD

Spot market balance Spot market settlement

Exposure

X PLD

(R$ / MWh)

Spot Price

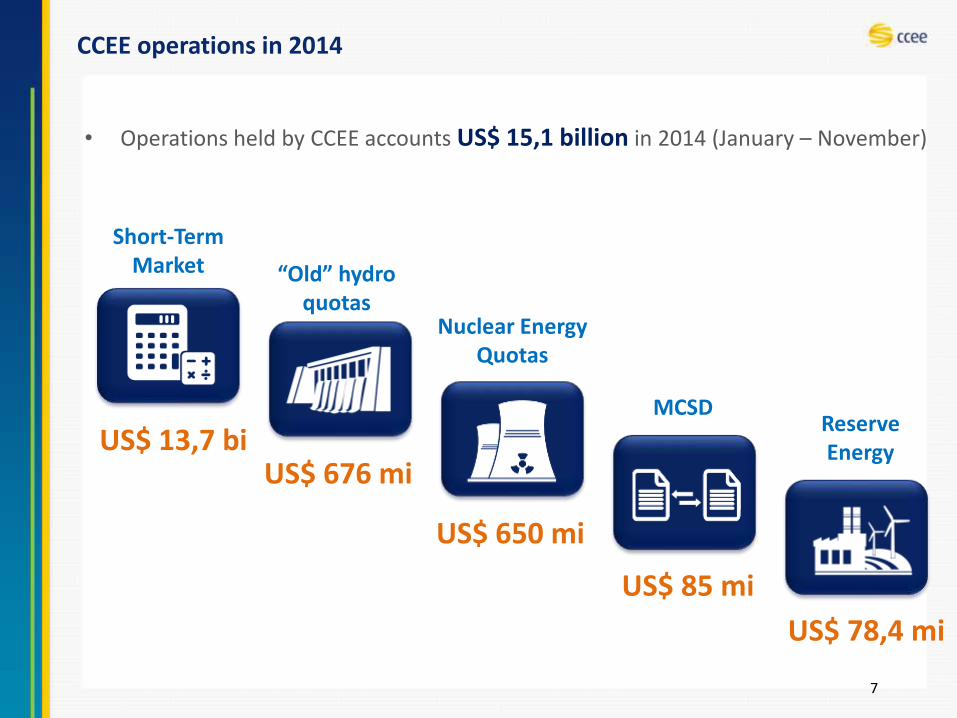

CCEE operations in 2014

7

• Operations held by CCEE accounts US$ 15,1 billion in 2014 (January – November)

US$ 13,7 biUS$ 676 mi

US$ 650 mi

US$ 78,4 mi

US$ 85 mi

Short-TermMarket “Old” hydro

quotasNuclear Energy

Quotas

MCSDReserve Energy

Highlights of Brazilian Economyand Electricity Industry

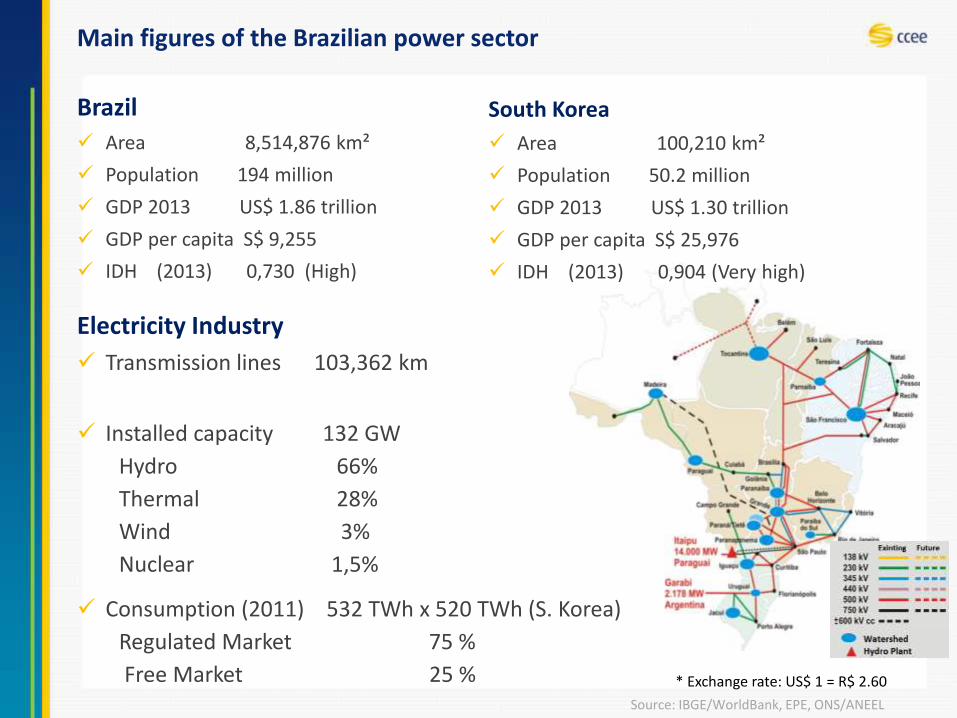

Main figures of the Brazilian power sector

Brazil

Area 8,514,876 km²

Population 194 million

GDP 2013 US$ 1.86 trillion

GDP per capita S$ 9,255

IDH (2013) 0,730 (High)

Electricity Industry

Transmission lines 103,362 km

Installed capacity 132 GW

Hydro 66%

Thermal 28%

Wind 3%

Nuclear 1,5%

Consumption (2011) 532 TWh x 520 TWh (S. Korea)

Regulated Market 75 %

Free Market 25 %Source: IBGE/WorldBank, EPE, ONS/ANEEL

* Exchange rate: US$ 1 = R$ 2.60

South Korea

Area 100,210 km²

Population 50.2 million

GDP 2013 US$ 1.30 trillion

GDP per capita S$ 25,976

IDH (2013) 0,904 (Very high)

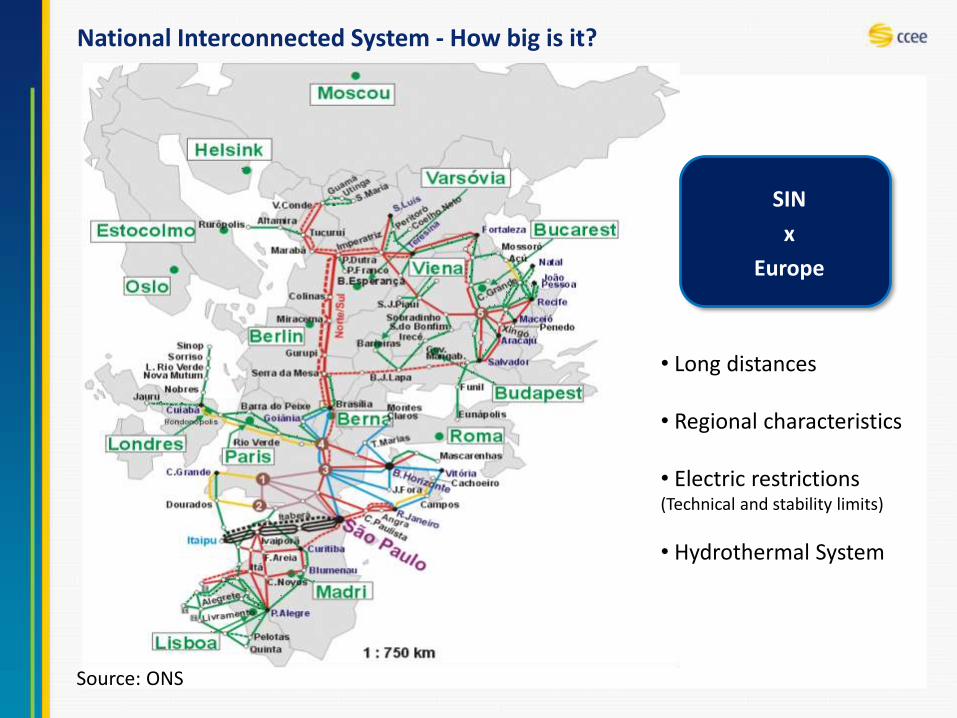

National Interconnected System - How big is it?

10

Source: ONS

SIN

x

Europe

• Long distances

• Regional characteristics

• Electric restrictions(Technical and stability limits)

• Hydrothermal System

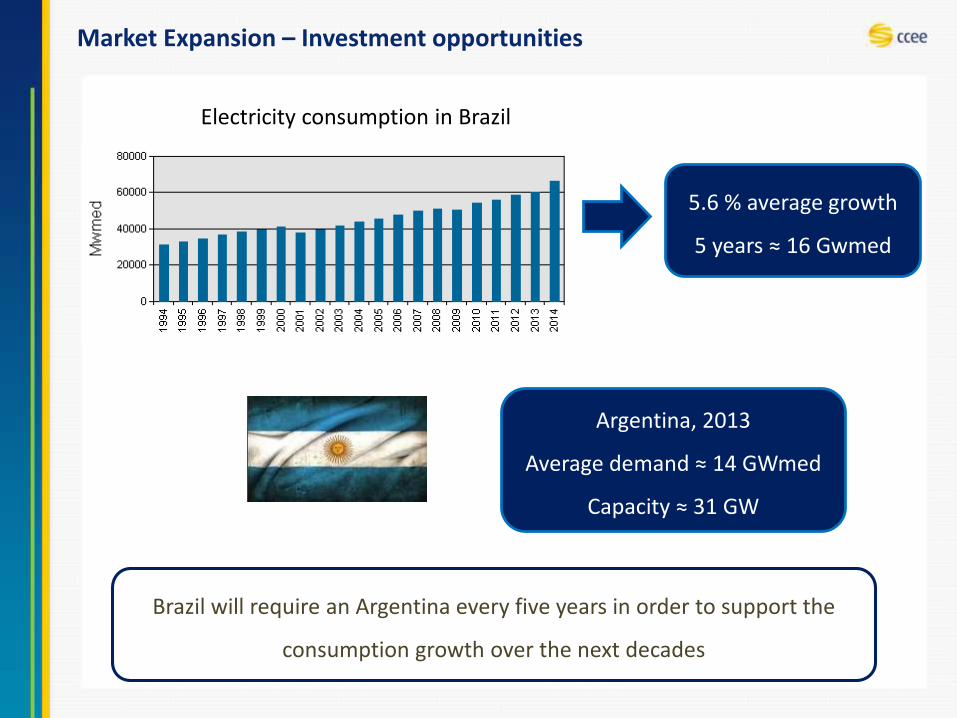

Market Expansion – Investment opportunities

Electricity consumption in Brazil

5.6 % average growth

5 years ≈ 16 Gwmed

Argentina, 2013

Average demand ≈ 14 GWmed

Capacity ≈ 31 GW

Brazil will require an Argentina every five years in order to support the

consumption growth over the next decades

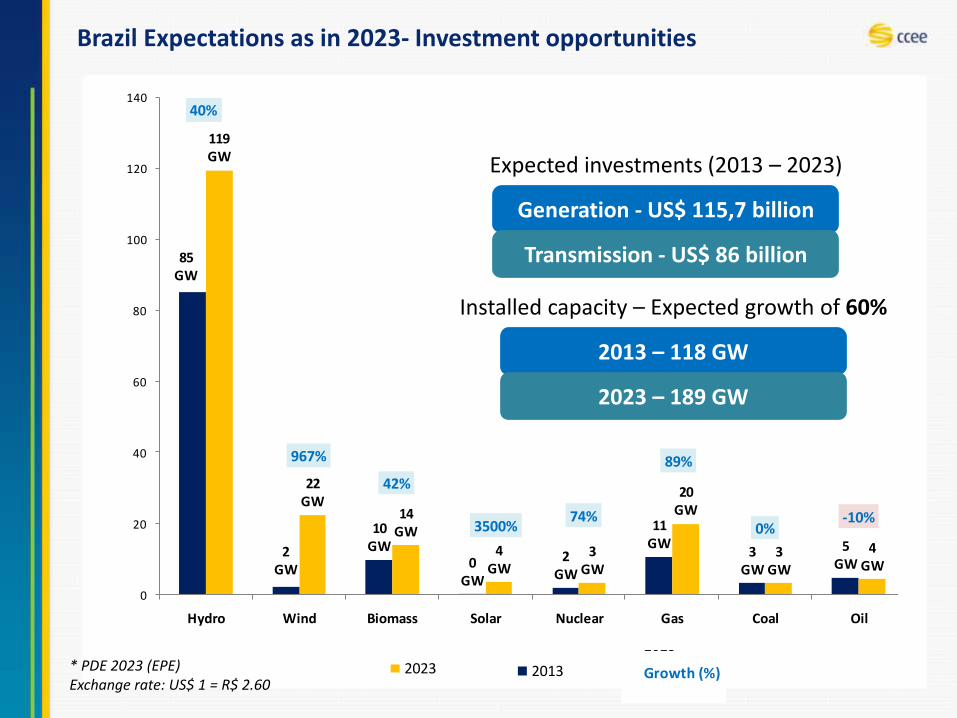

Brazil Expectations as in 2023- Investment opportunities

85 GW

2GW

10GW

0GW

2GW

11GW

3GW

5GW

119GW

22GW

14GW

4GW

3GW

20GW

3GW

4GW

40%

967%

42%

3500%74%

89%

0%-10%

-500

0

500

1000

1500

2000

2500

3000

3500

4000

0

20

40

60

80

100

120

140

Hydro Wind Biomass Solar Nuclear Gas Coal Oil

2013

2023

Growth (%)

85 GW

2GW

10GW

0GW

2GW

11GW

3GW

5GW

119GW

22GW

14GW

4GW

3GW

20GW

3GW

4GW

40%

967%

42%

3500%74%

89%

0%-10%

-500

0

500

1000

1500

2000

2500

3000

3500

4000

0

20

40

60

80

100

120

140

Hydro Wind Biomass Solar Nuclear Gas Coal Oil

2013

2023

Growth (%)

85 GW

2GW

10GW

0GW

2GW

11GW

3GW

5GW

119GW

22GW

14GW

4GW

3GW

20GW

3GW

4GW

40%

967%

42%

3500%74%

89%

0%-10%

-500

0

500

1000

1500

2000

2500

3000

3500

4000

0

20

40

60

80

100

120

140

Hydro Wind Biomass Solar Nuclear Gas Coal Oil

2013

2023

Growth (%)

85 GW

2GW

10GW

0GW

2GW

11GW

3GW

5GW

119GW

22GW

14GW

4GW

3GW

20GW

3GW

4GW

40%

967%

42%

3500%74%

89%

0%-10%

-500

0

500

1000

1500

2000

2500

3000

3500

4000

0

20

40

60

80

100

120

140

Hydro Wind Biomass Solar Nuclear Gas Coal Oil

2013

2023

Growth (%)

* PDE 2023 (EPE) Exchange rate: US$ 1 = R$ 2.60

Expected investments (2013 – 2023)

Generation - US$ 115,7 billion

Transmission - US$ 86 billion

Installed capacity – Expected growth of 60%

2013 – 118 GW

2023 – 189 GW

Governance of the BrazilianElectricity Industry

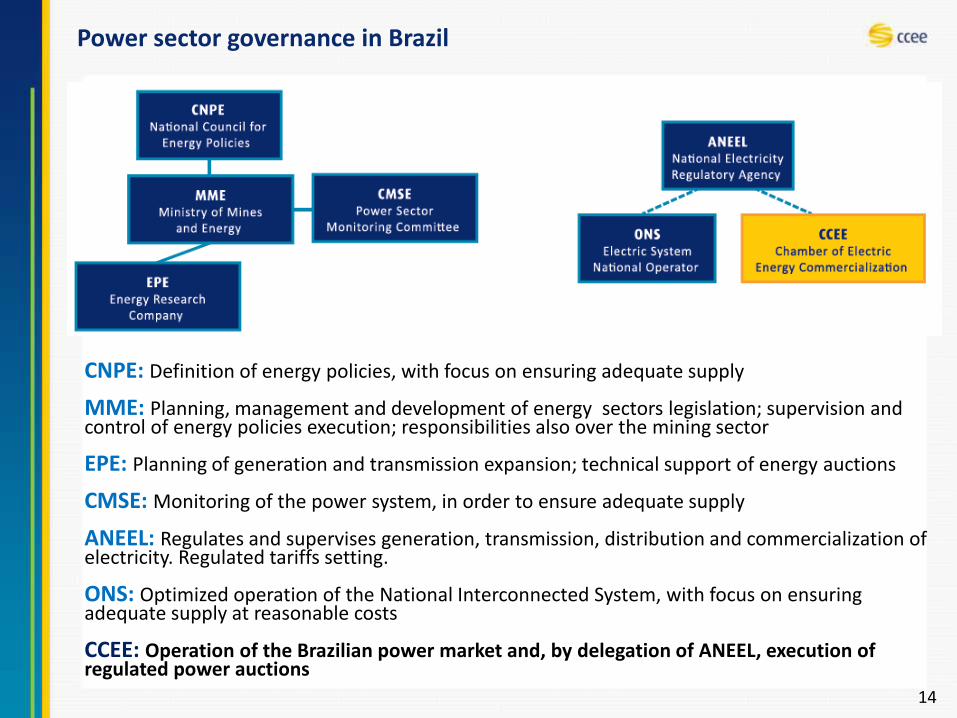

Power sector governance in Brazil

14

CNPE: Definition of energy policies, with focus on ensuring adequate supply

MME: Planning, management and development of energy sectors legislation; supervision and control of energy policies execution; responsibilities also over the mining sector

EPE: Planning of generation and transmission expansion; technical support of energy auctions

CMSE: Monitoring of the power system, in order to ensure adequate supply

ANEEL: Regulates and supervises generation, transmission, distribution and commercialization of electricity. Regulated tariffs setting.

ONS: Optimized operation of the National Interconnected System, with focus on ensuring adequate supply at reasonable costs

CCEE: Operation of the Brazilian power market and, by delegation of ANEEL, execution of regulated power auctions

Brazilian Regulated Market

Energy Auctions

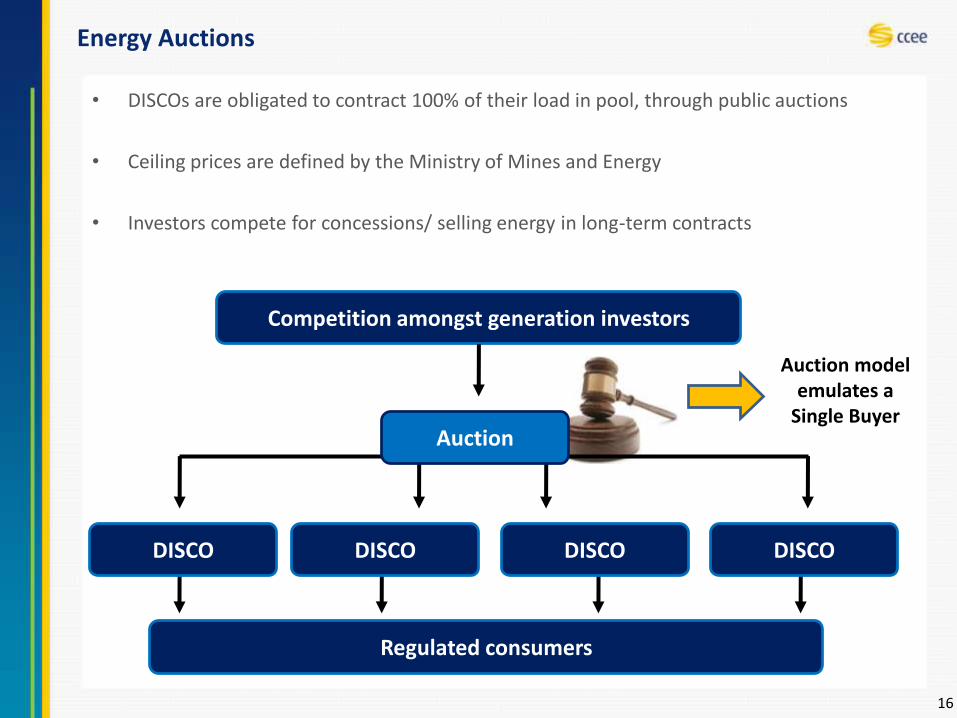

16

• DISCOs are obligated to contract 100% of their load in pool, through public auctions

• Ceiling prices are defined by the Ministry of Mines and Energy

• Investors compete for concessions/ selling energy in long-term contracts

Regulated consumers

Auction

Competition amongst generation investors

DISCO DISCO DISCO DISCO

Auction modelemulates a

Single Buyer

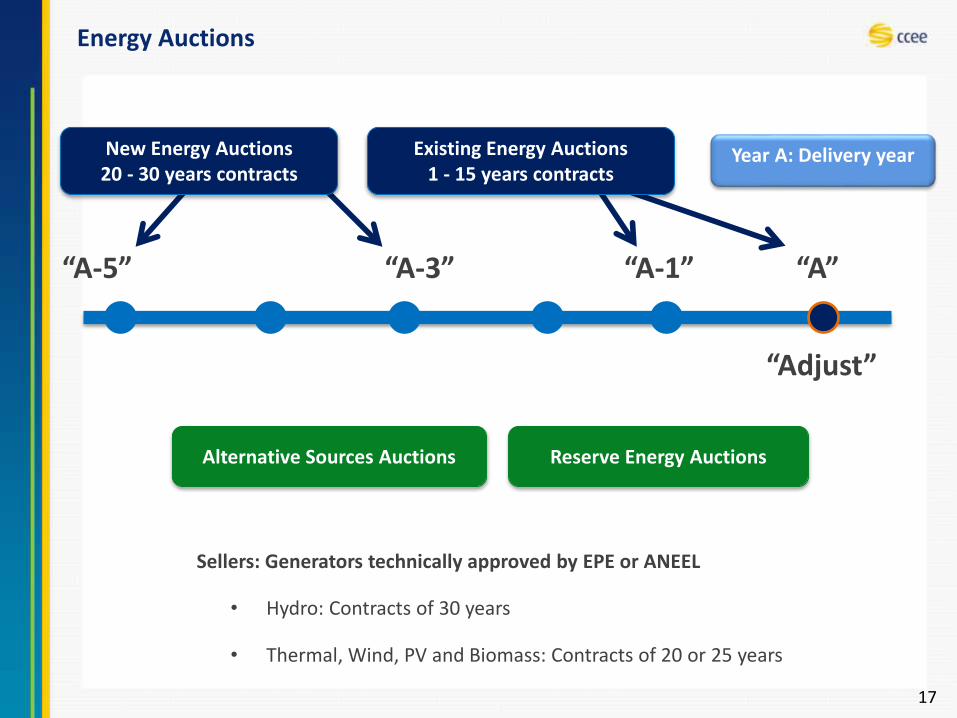

Energy Auctions

17

“A-1”“A-3”“A-5”

Existing Energy Auctions1 - 15 years contracts

New Energy Auctions20 - 30 years contracts

“A”

“Adjust”

Alternative Sources Auctions Reserve Energy Auctions

Year A: Delivery year

Sellers: Generators technically approved by EPE or ANEEL

• Hydro: Contracts of 30 years

• Thermal, Wind, PV and Biomass: Contracts of 20 or 25 years

Energy Auctions

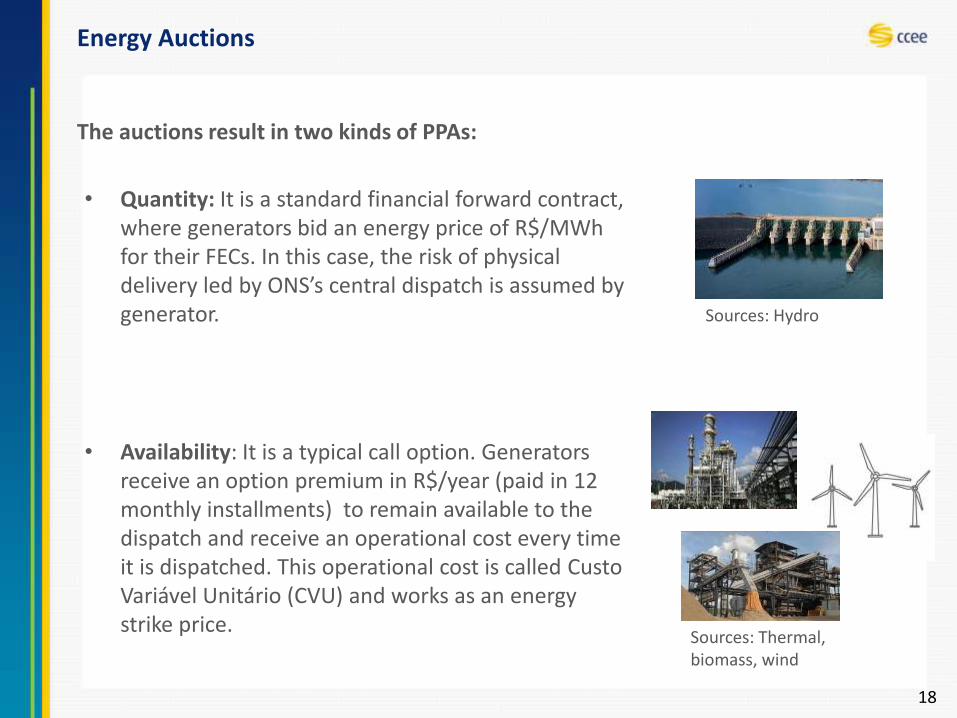

18

• Quantity: It is a standard financial forward contract, where generators bid an energy price of R$/MWhfor their FECs. In this case, the risk of physical delivery led by ONS’s central dispatch is assumed by generator.

• Availability: It is a typical call option. Generators receive an option premium in R$/year (paid in 12 monthly installments) to remain available to the dispatch and receive an operational cost every time it is dispatched. This operational cost is called CustoVariável Unitário (CVU) and works as an energy strike price.

The auctions result in two kinds of PPAs:

Sources: Hydro

Sources: Thermal, biomass, wind

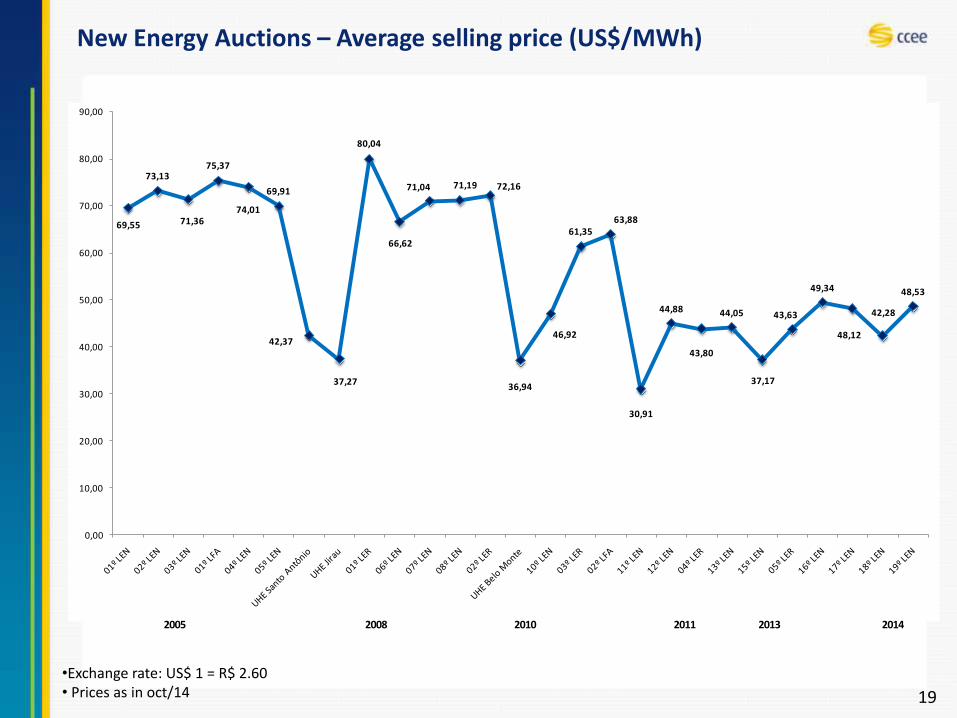

New Energy Auctions – Average selling price (US$/MWh)

19

69,55

73,13

71,36

75,37

74,01

69,91

42,37

37,27

80,04

66,62

71,04 71,19 72,16

36,94

46,92

61,3563,88

30,91

44,88

43,80

44,05

37,17

43,63

49,34

48,12

42,28

48,53

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

90,00

Preço médio por leilão (R$/MWh)

2005 2008 2010 2011 2013 2014

•Exchange rate: US$ 1 = R$ 2.60• Prices as in oct/14

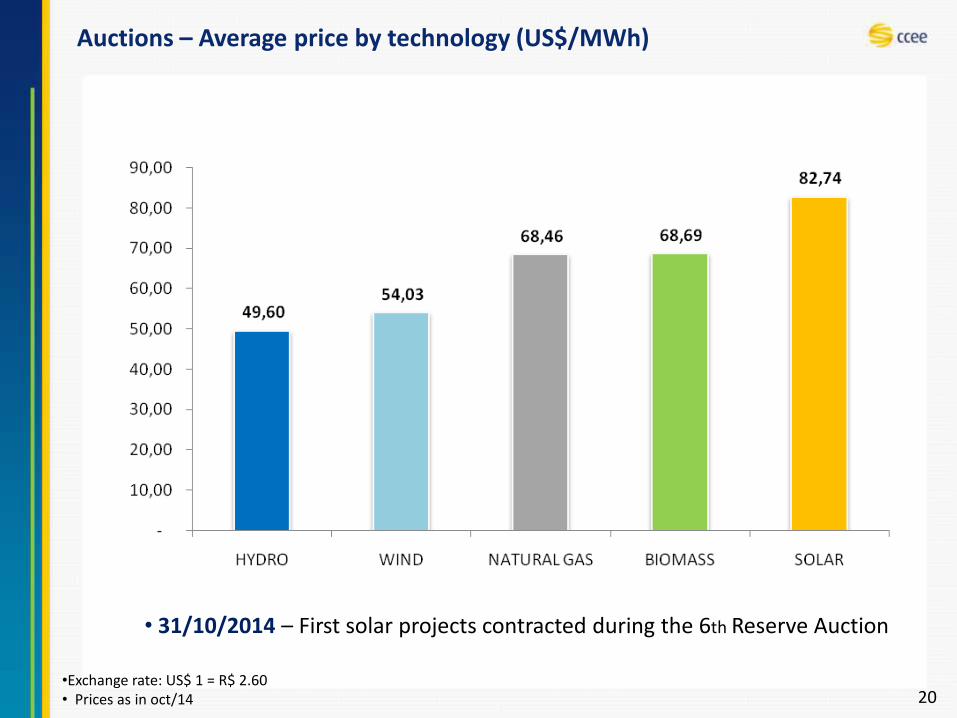

Auctions – Average price by technology (US$/MWh)

20

• 31/10/2014 – First solar projects contracted during the 6th Reserve Auction

•Exchange rate: US$ 1 = R$ 2.60• Prices as in oct/14

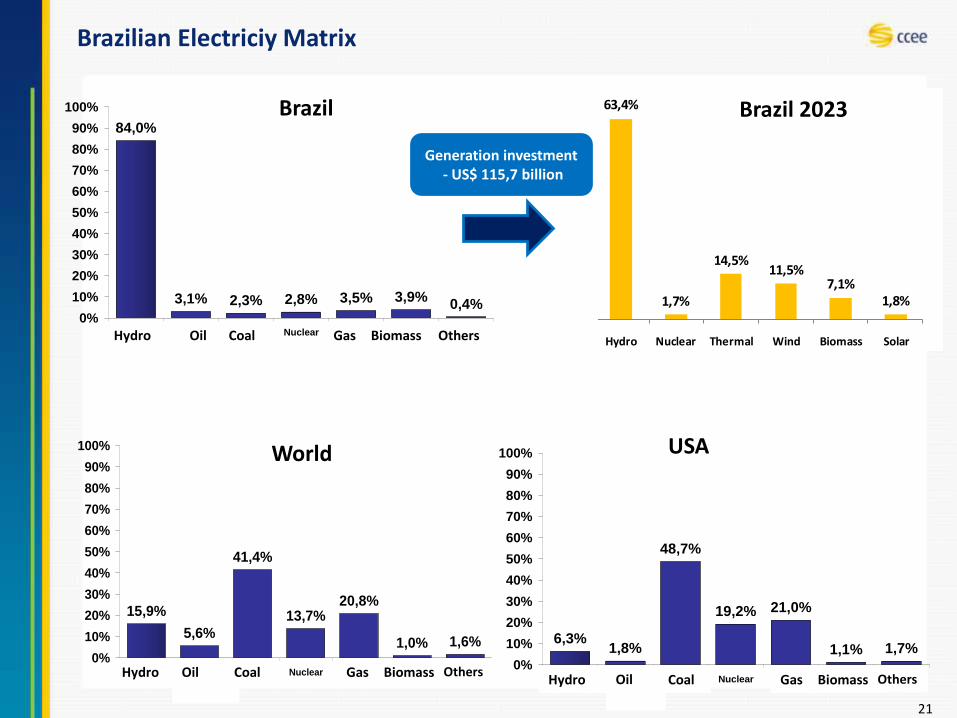

15,9%

5,6%

41,4%

13,7%20,8%

1,6%1,0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hidro Derivados

Petróleo

Carvão Nuclear Gás Biomassa Outros

84,0%

3,1% 2,3% 2,8% 3,5% 0,4%3,9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hidro Derivados

Petróleo

Carvão Nuclear Gás Biomassa Outros

Brazilian Electriciy Matrix

21

World

6,3%1,8%

48,7%

19,2% 21,0%

1,7%1,1%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hidro Derivados

Petróleo

Carvão Nuclear Gás Biomassa Outros

USA

Brazil

Hydro Oil Coal Gas Biomass Others

Hydro Oil Coal Gas Biomass OthersHydro Coal Gas Biomass OthersOil

63,4%

1,7%

14,5%11,5%

7,1%1,8%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

Hydro Nuclear Thermal Wind Biomass Solar

Série1

Brazil 2023

Generation investment- US$ 115,7 billion

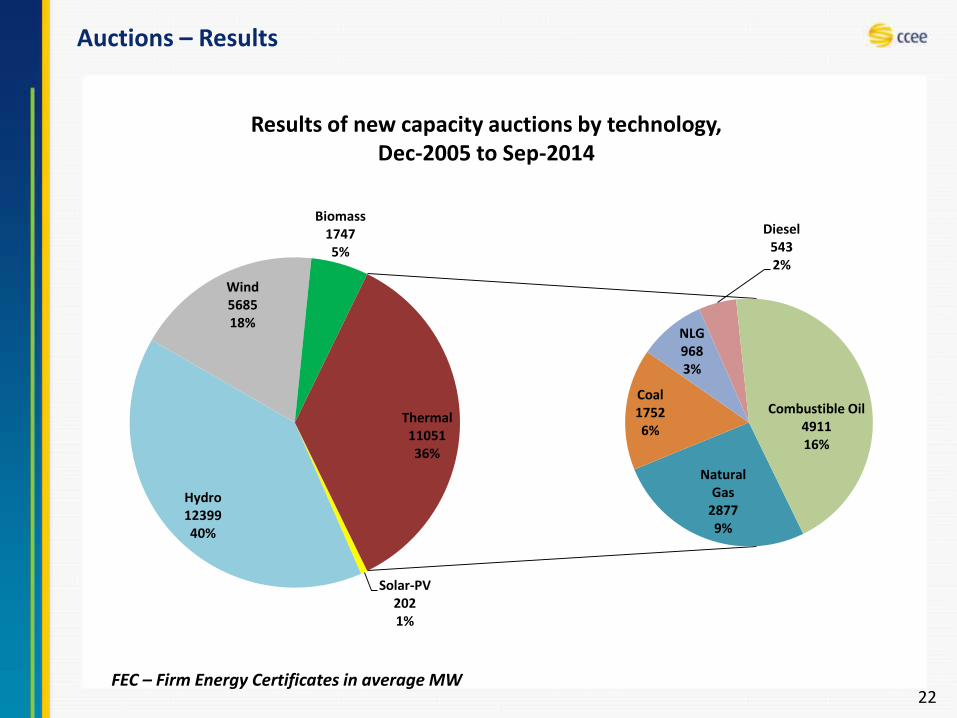

Auctions – Results

22

Results of new capacity auctions by technology, Dec-2005 to Sep-2014

Solar-PV 2021%

Hydro1239940%

Wind568518%

Biomass17475%

NaturalGas

28779%

Coal17526%

NLG9683%

Diesel5432%

Combustible Oil491116%

Thermal1105136%

FEC – Firm Energy Certificates in average MW

Brazilian Free Market

Brazilian Free Market

• The Brazilian Free Contracting Environment is an OTC Market

• Contracts are bilateral and CCEE knows only its amount and length

Generators

Self-Producers

IndependentProducers

Traders

Free Consumers

Special Consumers

Buyers

Sellers

Bilateral negotiations

Electronic Platforms

• Since June, 2014 (Portaria 185/13), Free and Special consumers are allowed to negotiateenergy ammounts with other consumers and Free Market agentes (energy cessions)

Brazilian Free Market

• All contracts and cessions need to be registered in CCEE´s platform (CliqCCEE)

• CCEE is responsible for the accounting and settlement of the differences between contracts and generation/consumption

• These settlement process includes also the regulated contracts

Settlement

Conclusions

Conclusions

• Brazilian needs of electriticy are a hugeopportunity for investors

• Auctions in the regulated marketreduce risks of investors

• The electricity industry is a low-riskenvironment in Brazil

• Brazilian power generation is changinginto a hydrothermal matrix

Thank you

Roberto CastroAdministration Board

Top Related