Languages

Pages

Legal

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 1

Running head: AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP

An Empirical Study of Audit Expectation Gap: The Case of

Lithuania

By

Vitalija Bogdanovičiūtė

Master student,

MSc in Finance and International Business

Department of Business Studies

Aarhus School of Business, University of Aarhus

Supervisor Dominyka Sakalauskaitė

May, 2011

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 2

Abstract

Associate with men of good quality if you esteem your own reputation; for it is better to be alone than in bad company. By George Washington

This study analyses the extent of an audit expectation gap among auditors and users of audited financial statements in terms of audit responsibility and reliability, objective, duties in detecting and reporting frauds and irregularities, and liability to the third parties in the Lithuanian business environment. The following four propositions are developed in order to be able to address the research question: 1) responsibility and reliability of audited financial statements differ substantially among auditors and users; 2) objective of auditing differ substantially among auditors and users; 3) auditor’s duties in detecting and reporting frauds and irregularities differ substantially among auditors and users; 4) auditor’s liability to the third parties in relations to auditors’ negligence and audit failure differs substantially among auditors and users. In order to explore the topic a survey is created based on methods used in Fadzly and Ahmad (2004), Lin and Chen (2004), Porter (1993) and Monroe and Woodcliff (1994). The results confirm that audit expectation gap exist in Lithuanian business environment, especially in the areas related to auditors reliability and responsibly, fraud detection and liability to third parties. Nevertheless, the results also show that auditors themselves have different perception regarding fraud prevention and detection, assurance and usefulness of the audited financial statements. This may be attributable to increased attention from the government and regulatory bodies regarding the role and supervision of auditors in order to regain investors trust and confidence after the corporate scandals and financial crisis.

Keywords: audit, expectation gap, attest function, fraud

Data availability: Please contact the author concerning the data availability

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 3

Table of contents

1 Introduction ..................................................................................................................... 5

2 Audit, fraud and expectation gap .................................................................................... 8

2.1 Audit function, objectives and development ........................................................... 8

2.1.1 Development of auditing practise ..................................................................... 8

2.1.2 Standards and legislation ................................................................................ 12

2.2 Fraud as audit function .......................................................................................... 15

2.2.1 Definition of fraud .......................................................................................... 16

2.2.2 Audit role in the area of fraud ........................................................................ 21

2.3 Audit expectation gap ............................................................................................ 23

2.3.1 Development of audit expectation gap ........................................................... 24

2.3.2 Audit expectation gap: Global evidence ......................................................... 26

3 Audit function and audit expectation gap in Lithuania ................................................. 32

3.1 Audit practice development in Lithuania ............................................................... 32

3.2 Role of Auditors and other institutions .................................................................. 35

4 Research of the extent of audit expectation gap in Lithuania ....................................... 39

4.1 Study propositions ................................................................................................. 39

4.2 Research methodology ........................................................................................... 41

4.2.1 Pretesting of the Questionnaire ...................................................................... 42

4.2.2 Data Analysis .................................................................................................. 43

4.3 Results .................................................................................................................... 43

4.3.1 Proposition 1 ................................................................................................... 44

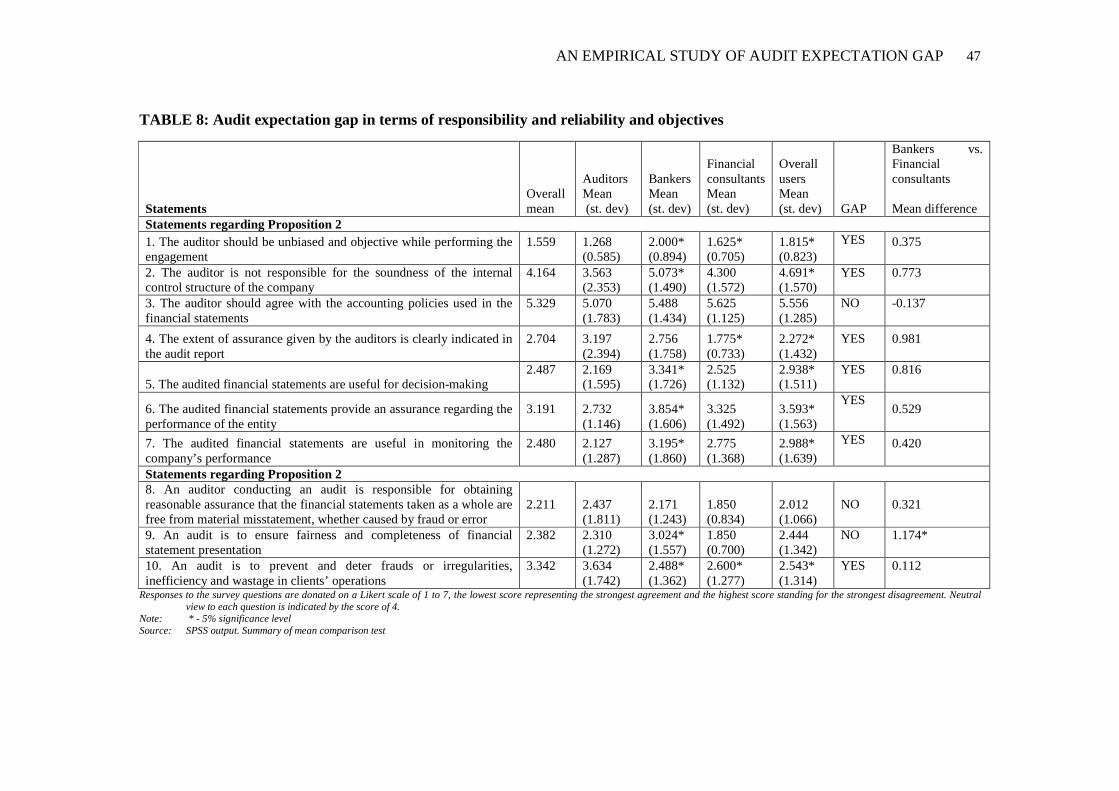

4.3.2 Proposition 2 ................................................................................................... 48

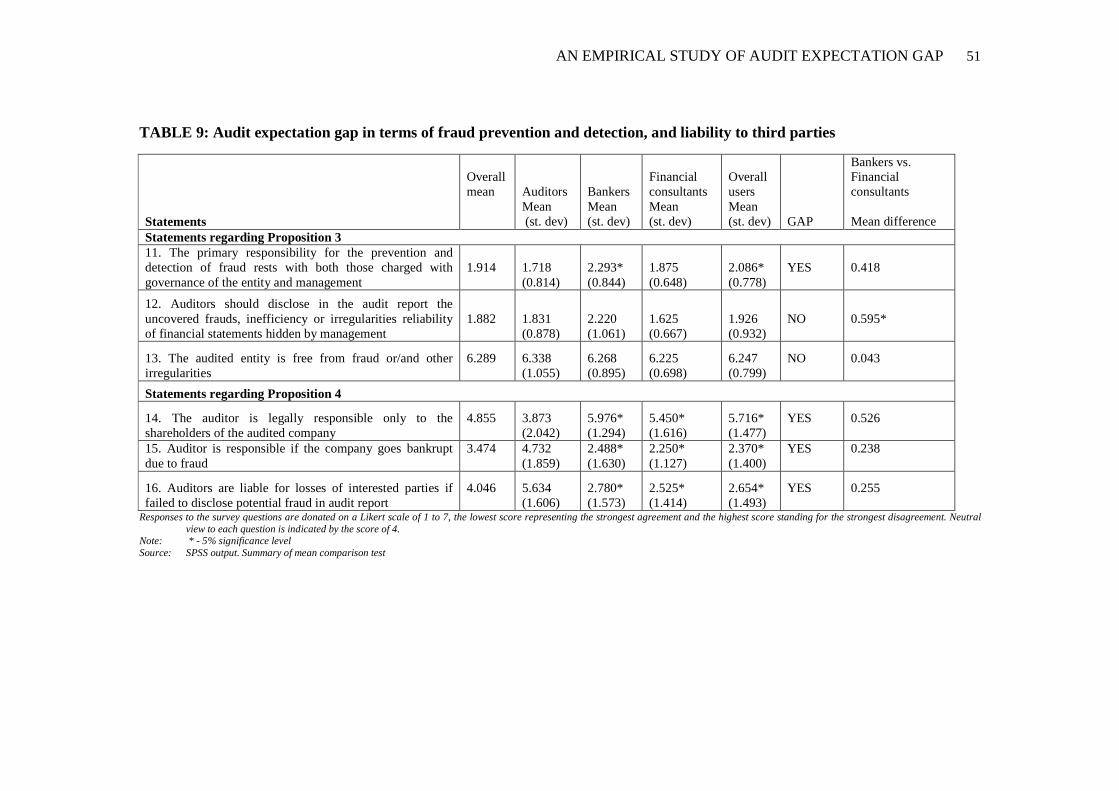

4.3.3 Proposition 3 ................................................................................................... 50

4.3.4 Proposition 4 ................................................................................................... 52

5 Discussion and conclusion ............................................................................................ 53

5.1 Limitations ............................................................................................................. 56

6 Appendices .................................................................................................................... 57

7 References ..................................................................................................................... 68

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 4

Abbreviations

ACFE - Association of Certified Fraud Examiners

EU – European Union

EUR - Euro

E&Y - Big-Four audit Firm Ernst & Young

FASB - The Financial Accounting Standards Board

FCIS - Financial Crime Investigation Service

FEE - General Assembly of European Federation of Accountants

GAAP - Generally accepted accounting principles

GDP – Gross domestic product

IASB - The International Accounting Standards Board

IFAC - International Federation of Accountants

IFRS - International Financial Reporting Standards

ISA – International Standards on Auditing

KPMG - Big-Four audit Firm KPMG

LCA - Lithuanian Chamber of Auditors

MSL - minimum subsistence level amounts

OLAF - European Anti-Fraud Office

PWC – Big-Four audit Firm PricewaterhouseCoopers

SPSS - computer program used for statistical analysis

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 5

1 Introduction

Fraud1 has been one of the most problematic and prevalent issues for business

worldwide for a long time; however, there has been much more attention and research

dedicated to the topic after the scandals such as Enron, WorldCom and others. The 5th

Global Economic Crime Survey performed by PwC (2009) reports that fraud remains a

pervasive business risk and almost every firm is subject to occupational fraud in their daily

business, leading to huge losses for business and society. Increase in occupational fraud and

number of corporate scandals had an important impact on understanding and analysing

fraud and in turn on audit and its regulation.

Prior studies on fraud investigation, detection and prevention indicate that the

deepening economic recession leads to even greater levels of fraud (PwC, 2009). The

mentioned findings and losses incurred by corporate scandals resulted in the increasing

public attention paid to auditors, who were expected to attest the accountability and

accuracy of the company’s financial statement. As mentioned in Salehi and Rostami (2009)

many users misunderstand the nature of the attest function of audit, as ‘users believe that an

unqualified opinion means that the entity has foolproof financial reporting’. Users’

expectations go beyond the responsibility required by the professional regulations and

standards, presenting subject of misconceptions especially in terms of auditors being able to

provide absolute assurance about the accuracy of financial statements and in turn create a

gap between auditors’ and users’ expectations of the audit functions. Additionally, if the

company appears to face serious financial difficulties without any warning, public usually

perceives that auditors are the ones to be made accountable for any losses experienced

(Koh&Woo, 1998). This go beyond the regulatory requirements which have been changed

over time, however currently claim that the main responsibility for fraud related items rest

with the management of the company (IFAC: IAASB, 2009a)

Fraud detection was considered the primary objective of audit process until

approximately the middle of 20th century. Later, however, the main objective changed

1 As a legal concept, fraud is broad and covers a wide range of activities. This study focuses on the category of fraud, known as occupational fraud, which is defined as “the use of one’s occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization’s resources or assets” (ACFE, 2010). ACFE identifies three primary categories of occupation fraud: 1) asset misappropriation; 2) corruption; and 3) fraudulent financial statements. This study focuses on the two categories of occupational fraud — asset misappropriation and fraudulent financial statements, as only these two types of misstatement are relevant to the auditors (ISA No. 240, paragraph 2).

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 6

from fraud detection to ‘verification of financial statements’ (Chandler, Edwards &

Anderson, 1993). Such shift in audit objectives and responsibilities created dissatisfaction

of companies’ stakeholders, including shareholders, current and potential investors,

creditors, etc.

Recently much attention paid to control issues and systems in order to narrow the

audit expectation gap, however, the actual level of fraud and financial damages has not

decreased (KPMG, 2009). The reason for this may be difficult and challenging audit

processes, as new rules and regulations require auditors to enhance the effort in terms of

fraud prevention and detection. A major issue of fraud detection is related to the difficulty

of identifying the fraud soon after it occurs. Quite often fraud is well hidden from auditors,

investors and other stakeholders and might only be discovered by chance (Plesis &

Koornhof, 2002). Besides, new rules and regulations followed by auditors when performing

audit contain terms like “reasonable”, “material”, “professional scepticism”, whose

meaning differ from auditor to auditor (Zikmund, 2008; personal communication March 3,

2011).

European Commission believes that mapping out society’s expectations of the role

and duties of auditors is crucial in taking steps to meet the expectations with auditors’

performance and fighting fraudulent activities (European Commission, 2010b). A few

studies have examined the audited expectation gap in Europe. However, to the best of my

knowledge no research has been done to examine directly the audit expectation gap in

Lithuania. In Lithuania, however, if such a gap does exist it might be presented as a result

of different situations and beliefs. Thus, the main task of this study is to investigate the

extent of an audit expectation gap among auditors and users of audited financial statements

in terms of audit responsibility and reliability, objective, duties in detecting and reporting

frauds and irregularities, and liability to the third parties in the Lithuanian business

environment. Therefore, four propositions are developed in order to be able to test the

hypothesis of existence of audit expectation gap among auditors and users.

The paper is based on the survey which presents the analysis of factors that form the

different expectations between the society and auditors and is designed and developed upon

the methods used in Fadzly and Ahmad(2004), Lin and Chen (2004), Porter (1993) and

Monroe and Woodcliff (1994). The research also highlights problems attributable to the

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 7

existing audit expectation gap and identifies possible topics for further research. Due to a

void in research in this area in Lithuania, these findings are important to stakeholders in the

financial reporting process, including auditors, the society, investors, creditors, accounting

academics, and other parties involved in audit regulation and rule making.

The paper is structured in the following way. The next part gives an historical

overview of audit process, its functions and objectives, including background on fraud

detection and audit expectation gap. The third section introduces literature review and

empirical evidence of the audit expectation gap in different parts of the world. The forth

section describes the audit and fraud detection process in Lithuania and introduces the

model used to test the extent of audit expectation gap in Lithuania. The last section

provides research implications and conclusions, including suggestions for further research.

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 8

2 Audit, fraud and expectation gap

Any enterprise worldwide relies on two very important and integral components –

accounting and auditing. The former one tracks all transactions of the firm and provides

information via financial reporting, while audit is performed to indicate the correctness of

this track and to ascertain the validity and reliability of information. The purpose of audit is

‘to enhance the degree of confidence of intended users in the financial statements <…> by

expression of an opinion on whether the financial statements are prepared, in all material

respects, in accordance with an applicable financial reporting framework’ (IAASB, 2010a).

The role of auditors in the financial statement has been and continues to be an

important issue for the auditing profession. According to Leung, Coram, Cooper, Cosserat

and Gill (2004) auditing practice has undergone various important evolution stages. During

the early 1990s, the detection of fraud was the primary purpose of external financial audit

(Rezaee&Riley, 2010). With time, Lee and Ali (2008b) claims that auditing practice

became more related to ‘enhancing role’, with special focus on integrity and credibility of

the information provided in financial statements; while Boynton, Jonson and Kell (2005)

declare that, besides enchasing credibility of financial statements, auditors nowadays are

providing other services such as reporting on irregularities, identifying business risks, and

management consulting on internal controls. In other words, auditors suppose to bridge the

communication between the managers of the company and final users of published

financial reports through authentication, reliability and correctness of financial reporting

(Salehi&Rostami, 2009).

2.1 Audit function, objectives and development

2.1.1 Development of auditing practise

External auditing plays an important role in bridging the effectiveness and efficient

functioning of business environment by adding credibility to financial statements

(Rezaee&Riley, 2010). Such assurance is needed to stakeholders of the company, usually

including not only shareholders but other parties as well (e.g. tax authorities, banks,

regulators, suppliers, customers and employees). Audits are not required by law but are

obligatory in many EU member states, as they help to decrease the costs of information

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 9

asymmetry by increasing the possibility that a material misstatement is detected by audit

procedures (European Commission, 2010b).

It is said that auditing is a social function, and the role of auditors is subject to shift

in accordance with the needs and demands of society (Porter, Simon&Hatherly, 2005). The

objective and techniques of auditors have changed significantly over time and can be

divided into several phases (Lee&Ali, 2008b).

Auditing until 1840. Auditing can be found as early as in the ancient civilisations of

China, Egypt and Greece. Lee and Ali (2008b) reports that all auditing objectives prior

1840 were similar to ancient civilisation, where a special audit officers had to make sure

that enterprises properly accounted for revenue and expenditure transactions. Interestingly

that even the name of the person hired to exanimate the transactions and prevent fraudulent

actions was derived from the Latin world “audire”, meaning to hear (Lee&Ali, 2008b). In

the period before 1840, auditors were obligated to perform detailed verification of every

transaction, where auditing procedures did not include any concept of testing or sampling.

In other words, during this period the main audit objective was to verify the honesty of

persons charged with fiscal responsibilities.

Auditing between 1840s-1920s. Industrial revolution established new grounds for

auditing practises (Chandler et al, 1993). The establishment of large factories and machine-

based production relied on the extensive amount of capital. As the market was poorly

regulated and highly speculative, investors were ‘in dire need of protection’ (Porter et al.,

2005) and this stimulated the emergence of the auditing profession and main procedures.

Some research (Brown, 1962, Queenan, 1946) states that during this period, auditors were

performing total checking of transactions with littler attention paid to internal controls.

Additionally, the concepts of materiality and sampling techniques were established as

auditors were not able anymore to verify all transactions conducted by the large

corporations and enterprises. According to Porter et al. (2005) analysis, during the years

1840-1920 the main responsibilities of the auditors were not exactly identified and their

focused on to detect fraud as well as verification of balance sheet to present the proper

company’s solvency (or insolvency). As to Chandler et al (1993) there are evidence that

auditors working with in large industries (such as banking, insurance and railway)

continued see balance sheet verification as the main objective of audit. For other

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 10

companies, which remained relatively small in that period, the objective and role of

auditors was perceived as fraud detection. Such predominant auditors’ role of fraud

detection resulted mainly because users of audited financial statements appreciated the

doubtless investment opportunity. In addition, the emphasis on fraud appeared from high

level of corporate bankruptcies experienced during the 1860s and 1870s, when ‘first hand

experienced of the causes and effects of poor or fraudulent management <…> coloured

their (auditors) attitude towards other aspects of their work’ (Chandler et al, 1993).

Above described disagreements imply the different views regarding fraud

prevention and detection as the primary auditor’s role during the engagement until

approximately middle of 20th century. However, after the McKesson & Robbins’ fraud

scandal in 1938 practitioners agreed that fraud prevention and detection should not be

considered as the primary auditor’s objective (Albrecht et al., 2001, Scott and Frye, 1997).

Different users and auditors perceptions related to fraud prevention and detection

encouraged the AICPA to issue several valuable additions to auditing standards, including

SAS No. 53 in 1988 (The Auditor’s Responsibility to Detect and Report Errors and

Irregularities), SAS No. 82 in 1997 (Considering of Fraud in a Financial Statement Audit),

and finally SAS No. 99 in 2002 (Considering Fraud in a Financial Statement Audit)

(AICPA, 1988, AICPA, 1997, AICPA, 2002). International Standards on Auditing also

included similar requirements, known as (ISA) No.240, The Auditors Responsibility to

Consider Fraud in an Audit of Financial Statements (IFAC: IAASB, 2007).

Auditing between 1920s-1960. The rapid development of the capital market and the

economic growth of the USA caused the shift in the role and objective of audit. According

to Porter et al. (2005), such development created the need to convince the participants in

the financial market about the financial statements provides true and fair picture of the

company’s financial position. Therefore, auditors were asked to provide credibility to the

financial statements prepared by company managers for their shareholders (Lee&Ali,

2008b). In other words, the auditors needed to assess the truth and fairness of the

companies’ financial statements rather than prevent and detect fraud and error (Lee&Ali,

2008b). Porter et al. (2005) states that audit focused mainly on the following

characteristics:

• Company’s internal controls

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 11

• Sampling techniques

• Audit evidence through internal and external sources

• Emphasis on the truth and fairness of financial statements.

Auditing between 1960-1990s. This period was marked with significant shifts in the

technology and economic development; however, auditors continued to play an important

role. The key role was to enhance the credibility of financial information used in the capital

market (Leung et al. 2004), leading to the fact that the role of auditors stayed similar to the

previous period. Porter et al. (2005) identifies that auditing practice continued to focus on

advanced computing auditing tools to improve audit procedures. Besides, everyone focused

audit evidence examination and usage of risk-based auditing to focus on areas most likely

to contain errors. In addition, so called one-stop shops emerged (Leung et al. 2004),

meaning that besides auditing services auditors started advising audit clients for a number

of services.

Auditing from 1990 to present. The overall audit objective remained the same over

time. The main purpose of audit is to express an opinion on whether the information

presented in the financial statements reflects the true and fair picture of the financial

position of the organisation at a given date. An audit is the independent examination of and

expression of opinion on company’s the financial statements by an appointed auditor in

compliance with any relevant statutory obligation. An auditor may express qualified

(accounts do not present a true and fair view) or unqualified (no significant concerns)

opinion (European Commission, 2010b). Statutory obligation, known as a duty imposed by

the law, is important to users of audited financial statements as they want to be sure that an

auditor has checked whether the company follows the laws and policies and keeps the

adequate records. Valuable addition to regulation and requirements has been corporate

scandals and failures, including Enron and WorldCom scandals, which has led to

discussions and debates considering the changes in the audit practice. According to Leung

et al. (2004) few dramatic implications might come into the force: it is expected that

auditors are refocusing on public interest, changing the audit relationship, ensuring the

integrity of financial reports, separating of non-audit functions and other advisory services.

In addition to this, the audit methods are expected to focus more on risk attention, fraud

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 12

awareness, objectivity and independence, in order to satisfy the needs of users of audited

financial statements (Lee&Ali, 2008b).

Currently, the market of audit practice is highly concentrated, with the leading

players been called Big-Four Audit firms2. It is estimated that the total market share of Big-

Four Audit firms account for more than 90% in terms of revenues or fees received from all

listed companies (European Commission, 2010b). Such strong concentration creates

barriers for non Big Four companies to compete in the market due to the lack of recognition

and reputational endorsement. Besides, European Commission (2010b) reports that ‘such

concentration might entail an accumulation of systematic risk and the collapse of a

‘systematic firm’’. Therefore, more attention is paid to the regulation of audit practise.

2.1.2 Standards and legislation

Quality of financial information, reliability, and transparency are the key factors of

the efficient capital markets. A collapse of big corporations such as Lehman Brothers,

WorldCom and Enron together with the extent of fraud activities resulted in concerns about

the value-adding activities of public companies' corporate ethics and governance.

Therefore, extensive reforms in various countries are directly addressed to examine the role

and responsibility of external auditor in fraud detection (Leung et al., 2004). The lack of

public trust and investor confidence in corporate world and its financial reports has

continued to adversely affect the vibrancy of the capital market forcing business leaders to

change their culture, behaviour, and attitudes to restore public confidence and trust in

business (European Commission, 2010b, European Anti-Fraud Office, 2010). To fight such

situation, large accounting firms first of all separated their consulting services from

auditing ones and announced about strict rules and measures taken to improve

independence and audit quality (European Commission, 2010b). Additionally, accounting

bodies, governments, stock exchange commissions and academics took different actions

including reforms of the legislation and standards to strengthen the audit practice (Leung et

al., 2004). One of the most important changes in auditing practice is known as The

Sarbanes-Oxley Act, which was implemented in the USA after the fall of Enron. The Act,

containing 11 sections ranging from additional corporate board responsibilities to criminal

2 Deloitte & Touche, Ernst & Young, PricewaterhouseCoopers and KPMG

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 13

penalties, includes the issues such as auditor independence, corporate governance, internal

control assessment, and enhanced financial disclosure (Sarbanes-Oxley Act of 2002).

According to the Act, there is a special Board assign to observe and check audit firms, their

procedures and the enforcement of accounting standards. There are, however, other

documents and governmental bodies which strongly regulates audit and its practise.

The International Auditing and Assurance Standards Board (IAASB) is ‘an

independent standard-setting body that develops auditing and assurance standards and

guidance for use by all professional accountants under a shared standard-setting process’

(IAASB, 2010b). The board generally meets four times a year and develops its standards

and practice statements. It is said that impact of financial crisis has been strongly felt

around the world, including auditing practise. According to IAASB, ‘the crisis has

amplified financial reporting challenges and has led to heightened attention on the role of

the audit and the broader accounting profession and <…> it [IAASB] has an important

responsibility to ensure that its work remains relevant as debates in this area evolve’

(IAASB, 2010b). As of today, IAASB has issued International Standards on Auditing

(ISAs) that deal with the independent auditor's responsibilities when conducting an audit of

financial statements.

ISAs contain objectives, requirements, application and other explanatory material,

which have to be fully understood by the auditor in order to recognize the objectives and to

apply the requirements properly. Note that IAASB completed the Clarity Project in March

2009, with the aim to promote greater understanding and consistency of application of the

ISAs (IAASB, 2010b). As a result IAASB released a set of 36 clarified ISA and the

clarified International Standard on Quality Control (ISQC) 1, which regalement functions

and standards of auditing practice. Interestingly, that even before the final release of

clarified ISAs and ISQC, there were 126 jurisdictions around the world, which had adopted

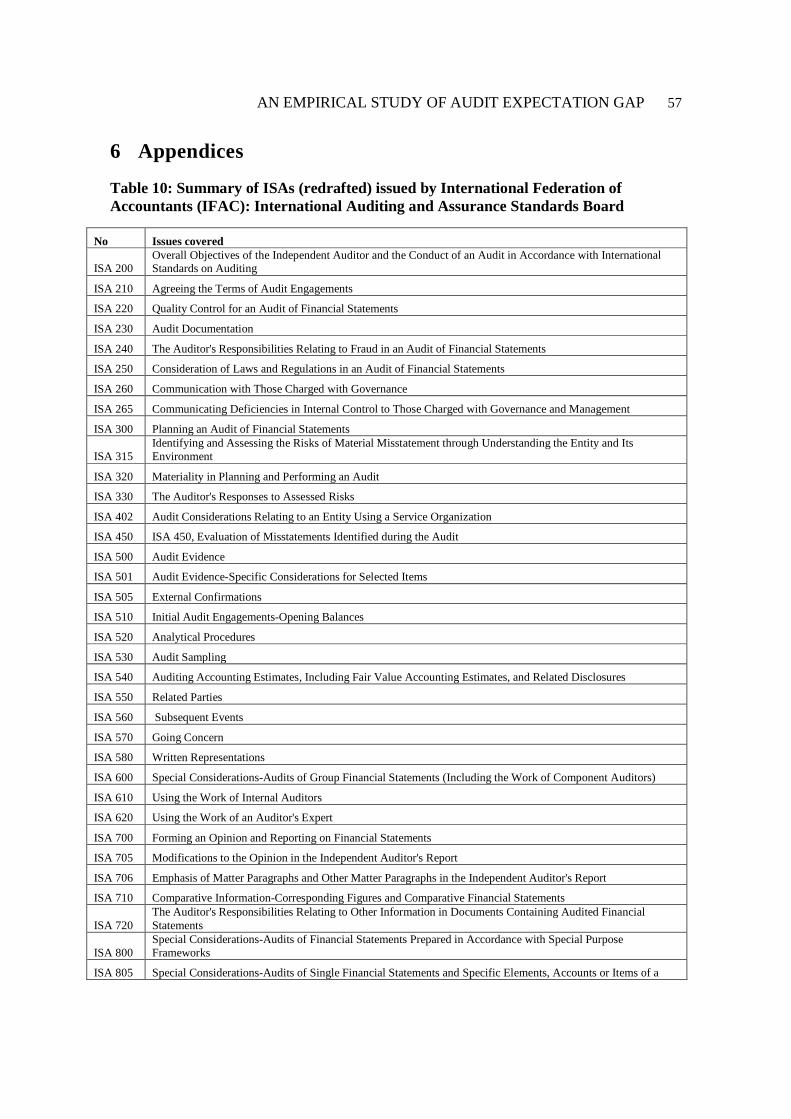

ISAs or used them as a basis for the national standards (IAASB, 2010b). ISAs covers the

independent auditor's overall responsibilities when conducting an audit of financial

statements in accordance with ISAs (ISA 200), as well as quality control (ISA 220), proper

audit documentation (ISA 230), responsibilities relating to fraud (ISA 240), materiality

(ISA320), sampling (ISA 530), related parties (ISA 550) and others (the list of ISAs is

provided in Table 10 in Appendix). Note that auditors in some countries are following

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 14

national auditing standards, yet in many cases they are based on ISA’s. For example, the

European Court of Auditors (2011) reports that auditors within the EU are obligated to

respect and follow the Court Audit Policy and Standards, ECA Audit Manuals and all audit

procedures adopted by the ECA. European Court of Auditors in turn is performing audits in

accordance with the IFAC and INTOSAI International Auditing Standards and Codes of

Ethics, which are based on ISAs (European Court of auditors, 2011).

Differently from some large countries (e.g. the US), the research among EU

stakeholders in 2009 indicated the overall support of an adoption of the clarified ISAs and

ISQCs at EU level (European Commission, 2010b, p.10). Currently, the majority of the EU

Member States have adopted or are in process of adopting ISAs. Significant support for

such action is that major international auditing firms are also applying these standards.

Such market harmonization is believed to contribute to ‘harmonised and qualitative audits

which in turn support the quality and credibility of the financial statements’ (European

Commission, 2010b, p.10). The EU governmental bodies stress the importance of the

governance and independence of the audit firms. According to the Directive on Statutory

Audit (2006/43/EC) it is important to ensure that auditors are following principles of

professional ethics and independence. These principles oversee different considerations of

auditing firms, including ‘appointment and remuneration of auditors, mandatory rotation,

non audit services, fee structure, publication of financial statements, organisational

requirements, revisiting ownership rules and the partnership model, group audits (European

Commission, 2010b).

Standards and regulation of audit also sets guidelines for accounting practice, which

is also strictly regulated and is subject to convergence of financial reporting standards.

There are different financial reporting standards, however, the latest statistics indicates that

over 120 nations and reporting jurisdictions permit or require International Financial

Reporting Standards (hereinafter IFRS) for domestic listed companies (AICPA, 2011).

Note that IFRS framework is based on ISAs and relevant ethical requirements, which

enable auditors forming the opinion on whether the financial statements are presented

fairly, in all material respects, and give a true and fair view.

A global survey conducted by the International Federation of Accountants in 2007

also highlights the importance of the convergence of financial reporting standards: a

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 15

majority of accounting leaders perceives a single set of international standards as an

important factor for the economic growth (IFAC, 2009). As a consequence, the IFRS

Foundation indicates that the number of countries that require or allow the use of IFRS for

the preparation of financial statements has been growing continuously. Some examples

includes the USA, where the growing acceptance of IFRS results from the convergence

with GAAP; Australia, New Zealand and Israel, where IFRS has been adopted as national

standards; Canada, which will adopt IFRS, in full, effective 2011 (IFAC, 2009). IAASB,

auditors and users of audited financial statements are expected to benefit from the

convergence of financial reporting standards into a single set of international standards.

Described development of audit’s roles and objectives lead to the presumption that

the primary auditors’ role has been shifting over time mainly due to the external events.

Moreover, based on current standards and legislation there are signs that public expectation

differs from auditors view especially in terms of responsibilities and obligations related to

fraud detection. Therefore, the next part presents the analysis of fraud as a function of audit.

2.2 Fraud as audit function

Fraud for a long time has been one of the key elements in the discussion regarding

the role and objective of auditors. As to the previous section, the main role of the auditors

was to detect and to prevent fraud in the company’s, however, the economic growth and

development of capital market resulted in the shift of the role of auditors. Fraud was left

aside when concept of materiality and fairness was introduced. Currently, a new trend has

been observed. ‘The reliability of auditing functions and the professionalism of the auditing

profession was, however, called into question after some spectacular and well publicised

corporations (for example Enron and WorldCom in the US) collapsed shortly after an

unqualified (in other words: “clean”) audit report had been issued’(Lee, Ali&Kandasamy,

2008c). Therefore, the society raises the question what the fraud is and whose responsibility

is to detect fraud and to prevent from it?

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 16

2.2.1 Definition of fraud

As a legal concept, fraud is a broad concept and covers a wide range of activities.

Due to the full FASB and IASB convergence effort, this study focuses on the category of

fraud, known as occupational fraud, which is defined as ‘the use of one’s occupation for

personal enrichment through the deliberate misuse or misapplication of the employing

organization’s resources or assets’ (ACFE, 2010). The definition of occupational fraud is

very wide, encompassing a number of activities covering any misconduct by employees at

every organizational level. Thus in order to understand the roots of how and when fraud can

be observed, one can rely on the simple occupational fraud and abuse classification system

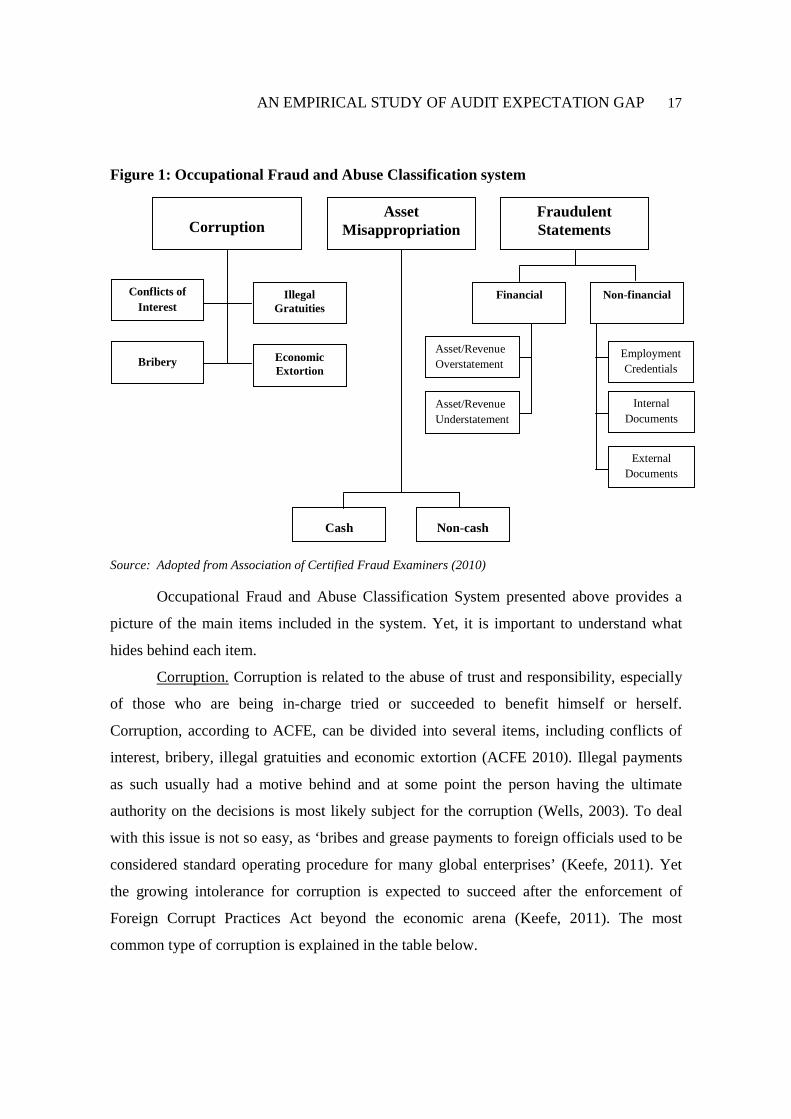

(see Figure 1 below), there fraud is be divided into three main groups (ACFE, 2010):

• Corruption - wrongful use of influence and power to achieve a benefit

contrary to their duty to their organization;

• Asset misappropriation - theft or misuse of assets;

• Fraudulent statements - Falsification of financial statements and/or other

organizational documents.

Fraud has been one of the most problematic and prevalent issues for business

worldwide for a long time; however, there has been much more attention and research

dedicated to the topic after the sandals such as Enron, WorldCom and others. The 5th

Global Economic Crime Survey performed by PwC (2009) reports that fraud remains a

pervasive business risk and almost every firm is subject to occupational fraud in their daily

business, leading to huge losses for business and society. To understand the huge risks that

exist due to economic crime it is important to look at the scale of the global financial

marketplace. It has been estimated that on each and every day around EUR 2.8 trillion is

moved across the globe. For comparison, in 2009 the Gross Domestic Product (GDP) of

Lithuania was EUR 27 billion and the GDP of Germany was EUR 2.4 trillion. This implies

that an amount moving around the world’s financial systems on a daily basis is far larger

that the GDP of Lithuania and about the same size as the Germany GDP. Report to the

Nation on Occupational Fraud and Abuse published by ACFE (2010) indicates that

constantly increasing fraudulent activities corresponded into the potential total fraud loss of

more than EUR 2.03 trillion in 2009, which equalled to around 5% total global GDP or the

GDP of the United Kingdom.

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 17

Figure 1: Occupational Fraud and Abuse Classification system

Source: Adopted from Association of Certified Fraud Examiners (2010) Occupational Fraud and Abuse Classification System presented above provides a

picture of the main items included in the system. Yet, it is important to understand what

hides behind each item.

Corruption. Corruption is related to the abuse of trust and responsibility, especially

of those who are being in-charge tried or succeeded to benefit himself or herself.

Corruption, according to ACFE, can be divided into several items, including conflicts of

interest, bribery, illegal gratuities and economic extortion (ACFE 2010). Illegal payments

as such usually had a motive behind and at some point the person having the ultimate

authority on the decisions is most likely subject for the corruption (Wells, 2003). To deal

with this issue is not so easy, as ‘bribes and grease payments to foreign officials used to be

considered standard operating procedure for many global enterprises’ (Keefe, 2011). Yet

the growing intolerance for corruption is expected to succeed after the enforcement of

Foreign Corrupt Practices Act beyond the economic arena (Keefe, 2011). The most

common type of corruption is explained in the table below.

Asset Misappropriation

Cash Non-cash

Fraudulent Statements

Non-financial Financial

Asset/Revenue Overstatement

Employment Credentials

Internal Documents

External Documents

Asset/Revenue Understatement

Corruption

Conflicts of Interest

Economic Extortion

Bribery

Illegal Gratuities

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 18

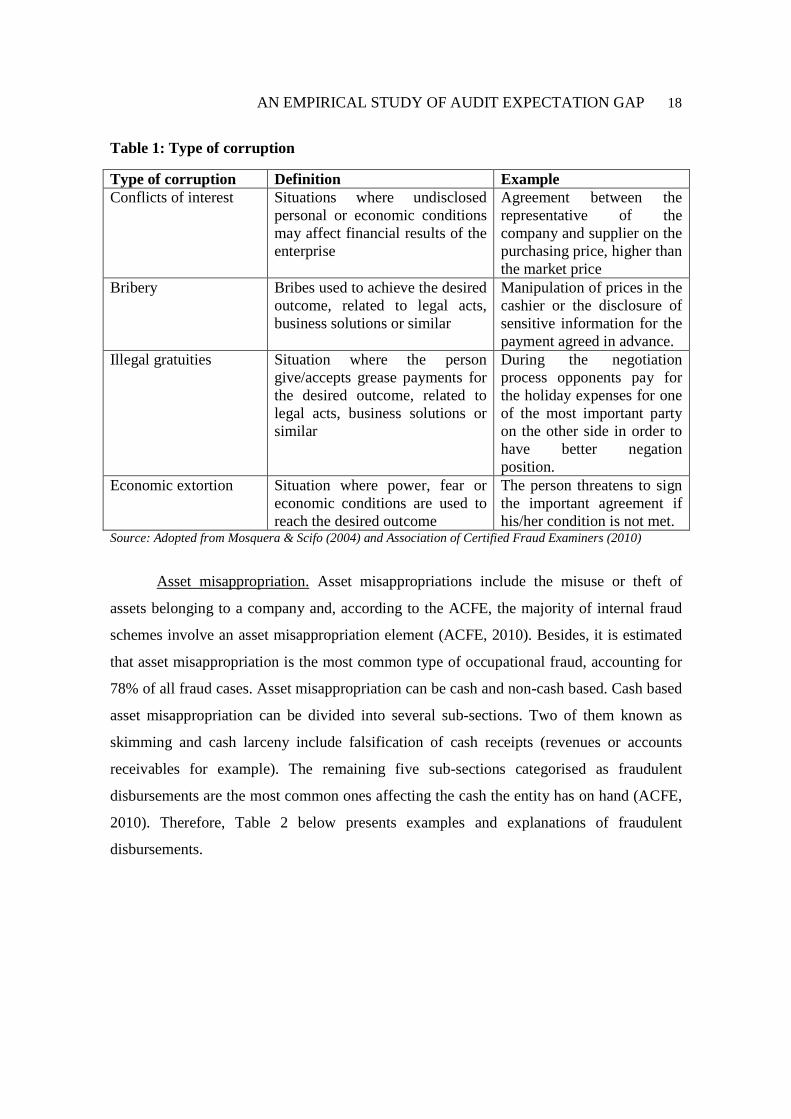

Table 1: Type of corruption

Type of corruption Definition Example Conflicts of interest Situations where undisclosed

personal or economic conditions may affect financial results of the enterprise

Agreement between the representative of the company and supplier on the purchasing price, higher than the market price

Bribery Bribes used to achieve the desired outcome, related to legal acts, business solutions or similar

Manipulation of prices in the cashier or the disclosure of sensitive information for the payment agreed in advance.

Illegal gratuities Situation where the person give/accepts grease payments for the desired outcome, related to legal acts, business solutions or similar

During the negotiation process opponents pay for the holiday expenses for one of the most important party on the other side in order to have better negation position.

Economic extortion Situation where power, fear or economic conditions are used to reach the desired outcome

The person threatens to sign the important agreement if his/her condition is not met.

Source: Adopted from Mosquera & Scifo (2004) and Association of Certified Fraud Examiners (2010)

Asset misappropriation. Asset misappropriations include the misuse or theft of

assets belonging to a company and, according to the ACFE, the majority of internal fraud

schemes involve an asset misappropriation element (ACFE, 2010). Besides, it is estimated

that asset misappropriation is the most common type of occupational fraud, accounting for

78% of all fraud cases. Asset misappropriation can be cash and non-cash based. Cash based

asset misappropriation can be divided into several sub-sections. Two of them known as

skimming and cash larceny include falsification of cash receipts (revenues or accounts

receivables for example). The remaining five sub-sections categorised as fraudulent

disbursements are the most common ones affecting the cash the entity has on hand (ACFE,

2010). Therefore, Table 2 below presents examples and explanations of fraudulent

disbursements.

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 19

Table 2: Cash based asset misappropriation (Fraudulent Disbursements)

Type Definition Example

Billing Schemes Situations may include shell company, non-accomplice vendor or personal purchases

Employee may create shell company and bill the employer for the falsificated services

Payroll Schemes Situations may include ghost employees, commission schemes, workers compensation, or falsified wages

Employee may hire unreal person as the new employee of the company or may falsified the hours worked

Expense Reimbursement Schemes

Situations may include mischaracterized expenses, overstated expenses, fictitious expenses, or multiple reimbursements

Employee may pay falsified bills from the company account

Check Tampering Situations may include forged maker, forged endorsement, altered payee, concealed checks, or authorized maker

Employee steals empty checks and fills them in afterwards in such a way receiving money in his/her bank account

Register Disbursements

Situations may include false voids or false refunds

Employee may speculate the information in the register and appropriate money into his/her account

Source: Adopted from Mosquera & Scifo (2004) and Association of Certified Fraud Examiners (2010)

Non-cash based asset misappropriations covers the theft or misuse of non-cash

assets, including items such as non-current assets, inventory, investments, intellectual

property and other, however the loss of such type of asset misappropriations are estimated

to be of smaller loss (ACFE, 2010).

Table 3: Non-cash based asset misappropriation

Type Definition Example Inventory Situations may include stealing or not

appropriate use of non-cash asset of the company, including inventory, equipment and others

Employee may steal the asset from inventory or use them for personal need

Information Situations may include stealing or disclosure of company’s confidential information or trade secrets.

Employee may sell company’s sensitive information to the competitor

Shares or obligations Situations may include stealing of companies shares, obligations or other securities

Employee may fraudulently transfer the shares of the company into a personal account

Source: Adopted from Mosquera & Scifo (2004) and Association of Certified Fraud Examiners (2010)

Fraudulent Statements. This type of fraud is related to the financial statements

which may be falsified. According to Table 4, fraudulent statements can be classified into

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 20

financial and non-financial ones. The later one is mainly related to the misuse of

employment credentials, internal and external documents. However, currently severe losses

have been created by exploiting financial types of fraudulent statements. The examples

include the bankruptcy of Enron and the fraudulent accounting of WorldCom in order to

reduce tax payables, increase revenues, share price and etc. The table below provides detail

information on types of fraudulent statements based on financial actions.

Table 4: Fraudulent statements: financial

Type Definition Example Timing Differences Situations may include false accounting

for revenues and expenses in terms of the actual period they were achieved

The company may record the revenues in the year 201X while the expenses will be included into the accounts in the year 201X+1

Fictitious Revenues Situations may include falsified sale of goods and services

The sale of inventory to the clients which do not exist or the real client invoicing while the good and services are not delivered (the sales are credited back during the next period)

Concealed Liabilities and Expenses

Situations may include false accounting for expenses and liabilities

Financial statements may exclude important expenses/liabilities or the expenses required to achieve the current level of sales are capitalized.

Improper Disclosures Situations may arise when management decides not to disclose important information

Financial statements may not include information about off-balance sheet or contingent liabilities, which may significantly affect the financial position of the company

Improper Asset Valuations

Situations may arise when the asset of the company is not values properly

The accounting may include incorrect way of depreciation of assets, inventory may be written off incorrectly or trade receivables may be falsified

Source: Adopted from Mosquera & Scifo (2004) and Association of Certified Fraud Examiners (2010)

It is important to measure the costs of occupational fraud, yet the costs can be, at

best, an estimate to present the ‘pandemic and destructive nature of white-collar crime’

(ACFE, 2010). Despite the recent attention to control issues and systems, the actual level of

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 21

fraud and financial damages has not decreased (KPMG, 2009). One reason for this trend

may be insufficient emphasis on fraud prevention and detection. Studies also show that the

deepening economic recession could lead to even greater levels of fraud (PwC, 2009). A

major issue of fraud detection is related to the difficulty of identifying the fraud soon after

it occurs. Quite often it is well hidden from auditors, investors and other stakeholders and

might only be discovered by chance (Plesis & Koornhof, 2002). Auditors, for example, find

it complicated and increasingly difficult to detect fraud with analytical procedures

requested by audit standards for at several reasons. When performing their tasks, auditors

mainly rely on management explanations not challenging or testing the explanations about

the business development (Hirst & Koonce 1996). Additionally, auditors simply lack a

sufficient understanding of certain business, thus it is difficult for them to recognized

unusual trends and ratios within the financial statements in one or another business

(Erickson et al. 2000). Even though traditional analytical procedures may lead to the

success in identifying fraud, however, this success is highly limited as financial statement

data tend to have to high rates of misclassification (Hogan et al. 2006, Erickson et al. 2000).

On the other hand, the society views such explanations in a different way. Therefore, the

auditors anyway are expected to play an important role in fraud detection and prevention.

2.2.2 Audit role in the area of fraud

European Commission (2010a) reports that the methods of detection of fraud vary

between Member States. Nevertheless, in 2009 the vast majority of cases (75%) were

detected by means of either primary national inspections or post-clearance control audits.

Primary inspections are used in particular in Denmark, Slovenia, Romania, Malta and

Greece, while the remaining Member States mostly uses ‘ex-post controls’ to detect

irregularities (European Commission, 2010a). ‘Ex-post controls’ refers to audit of the

accounts, commission inspections, inspections by anti-fraud services, inspection visits,

national post-clearance audits and tax audits.

According to Lord Justice Lopes (2004), ‘An auditor is not bound to be a detective,

or … to approach his work with suspicion, or with a foregone conclusion that there is

something wrong. He is a watchdog, not a bloodhound’. However, there are a number of

discussions regarding fraud, especially in terms of the extent of auditor responsibility for

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 22

the fraud prevention and detection. Following the development of auditing practice and

new standards to be issued, auditor responsibility for fraud detection has remained a low

priority (Jones, 2009). Following the standards defining auditing practise in terms of fraud

detection one has understand the scope and objective of ISA 240. This ISA deals with the

auditor’s responsibilities relating to fraud in an audit of financial statements, which presents

the real picture of the role of auditors in terms of fraud detection.

According to ISA 240, there are two types of intentional misstatements are relevant

to the auditor, namely misstatements resulting from fraudulent financial reporting and

misstatements resulting from misappropriation of assets (IFAC: IAASB, 2009a). Note that

the main factor which allows distinguishing between fraud and error is the underlying

action, intentional or unintentional, which finally results in a misstatement of the financial

statements (IFAC: IAASB, 2009a). Auditors following ISA guidelines are expected to deal

with the mentioned types, however, ISA 240 makes it clear that the main responsibility for

the prevention and detection of fraud rest with the management:

The primary responsibility for the prevention and detection of fraud rests with both

those charged with governance of the entity and management. It is important that

management, with the oversight of those charged with governance, place a strong

emphasis on fraud prevention, which may reduce opportunities for fraud to take

place, and fraud deterrence, which could persuade individuals not to commit fraud

because of the likelihood of detection and punishment (IFAC: IAASB, 2009a).

The auditor while conducting an audit, on the other hand, is responsible for

‘obtaining reasonable assurance that the financial statements taken as a whole are free from

material misstatement, whether caused by fraud or error’ (IFAC: IAASB, 2009a). This

implies the fact that an external audit on the financial statements does not indicate that

financial statements are entirely free from misstatements. According to the European

Commission (2010b), unqualified auditors opinion means that the financial statements give

a true and fair view in accordance with the relevant financial reporting framework. In other

words, auditors provide ‘reasonable assurance3’ about financial statements as a whole being

free from material misstatement caused by fraud or error (European Commission, 2010b).

3 Reasonable assurance means high but not absolute level of assurance

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 23

ISAs also indicate the actions of the auditors in case of risks of material

misstatements due to fraud. If significant risks of material misstatements due to fraud are

identified, the auditor shall ‘determine whether there is a responsibility to report the

occurrence or suspicion to a party outside the entity’ (IFAC: IAASB, 2009a). Note that

most of the audit engagements are confidential and the conflict between the client and

auditor may arise; however, the auditor’s legal responsibility may overcome the

professional duty to maintain client’s confidentiality (IFAC: IAASB, 2009a). According to

the European Commission (2010b), statutory audits, however, have changed their focus

from verification of revenues, costs, assets and liabilities to a ‘risk-based approach’. In

other words, auditors are more concern about the reasonable assurance in terms of

applicable financial reporting framework rather than providing true and fair view of the

financial statements.

Occupational fraud has a large impact on the audit and its reputation from the users’

perspective. The mentioned actions taken by the regulatory bodies to react to the corporate

scandals imply the significance of mapping out auditors and society’s expectations towards

role and responsibilities of auditors work. However, the number of research indicates that

this aim is hard to achieve and thus there exists rather extensive audit expectation gap in the

certain parts of the world. Therefore, the next part provides the analysis of development and

empirical evidence of audit expectation gap.

2.3 Audit expectation gap

Public expectations on deficient performance and duties of auditors sometimes go

behind the reality and legal framework (Porter, 1993; Porter & Gowthorpe, 2004; Lee,

Gloeck & Palaniappan, 2007). There are several reasons for that. Firstly, any investor,

creditor or generally speaking the public, expects that entities, where they invested money,

are held fully accountable for the use of that money. Managerial bodies of course handle

the prime responsibility for ensuring that money is used with absolute integrity and spent

wisely. Audit is a supplementary instrument to trace accountability, uncover irregularities

in financial matters, and establish public confidence that money is being properly spent.

Additionally, external auditors may have a direct and positive influence on the way

organisations and people discharge their responsibilities. From the users’ perspective

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 24

auditors working within public bodies may help to promote better management and

decision-taking, and thus a more effective use of taxpayers’ resources (Mackevicius, 2001).

However, just a few users of audited financial statements realize that the reality is different.

Representative from one of Big-Four Audit firm reveals that the audit profession has

consistently failed to explain itself properly (personal communication, March 3, 2011). The

ultimate responsibility in any case stays with management, mainly because only a

reasonable amount of testing is performed during audit procedures. Therefore, even if the

audit profession explains itself properly, the immediate next questions from the general

public would be why auditors charge money for such services and whether these services

are needed at all? These questions would arise as the society does not (or does not want to)

understand that in order to perform a wider role than it is done currently, audit companies

would need to have a permanent presence in public companies and to function as some kind

of public representative safeguarding society's interests, which would cost a lot (personal

communication, March 3, 2011). But nobody would be willing to pay for it.

In view of the contributing factors and expectations it is not surprising that that

auditors and public have different expectation of the audit function and deliverables. Those

different views create audit expectation gap, which, unless significant actions are taken to

decrease this gap, enlarges with time.

2.3.1 Development of audit expectation gap

Historically, Humphey and Tyrley (1992) claims that some hints of expectation gap

can be found back in 19th century together with the introduction of companies auditing,

while Liggio research paper The expectation gap: The Accountant Waterloo (1974) brought

the term ‘Audit expectation gap’ into the audit literature. According to Liggio (1974), the

expectation gap concept presents the difference between the expected performance “as

envisioned by the independent accountant and users of the financial statements.”

Meanwhile, the Cohen Commission (1978) in the US referred the expectation gap

introduced by Liggio (1974) as the different view between (a) what the society names as

auditors’ responsibilities and (b) what auditors believe their responsibilities are.

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 25

Porter (1993) criticized the definition of Liggio (1974) and Cohen Commission

(1978) as being too narrow. Thus she presented the more extensive way of analyzing the

gap, which included two main components: reasonableness gap and performance gap (see

the figure 2).

Figure 2: Audit expectation gap

Source: Adopted from Porter (1993)

Note: * - Duties defined by the law and professional promulgations ** - Duties which are cost beneficial for auditors to perform

The model has been extensively used to test the existence and uncover the causes of

audit expectation gap in number of countries. According to the model, performance gap

refers to the different perception between “what society can reasonably expect auditors to

accomplish and what they are perceived to achieve” (Porter, 1993, p 50). This later

component then is divided further and are presented by deficient standards (“a gap between

the duties which can reasonably be expected of auditors and auditors’ existing duties as

defined by the law and professional promulgations”) and the deficient performance (“a gap

Auditors’ Existing Duties*

Auditors’ Perceived

Performance Audit Expectation-Performance

Society’s Expectation of Auditors

Performance gap Reasonableness gap

Deficient Performance

Unreasonable Expectations

Deficient Standards

Duties Reasonably Expected of Auditors**

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 26

between the expected standard of performance of auditors’ existing duties and auditors’

perceived performance, as expected and perceived by society) (Porter, 1993, p.50).

Reasonableness gap is known as the difference between ‘what society expects

auditors to achieve and what they can reasonably be expected to accomplish’ (Porter, 1993,

p. 50). In other word, it is related to the complication and misunderstanding of nature,

purpose and capacities of an audit function as observed by the society. Humphrey (1997)

report that audit expectation gap exists mainly because of the subjective nature of terms and

concepts in auditing such as the true and fair view, reasonable, materiality, adequacy,

reliability and relevance which are not defined precisely in the Accounting and Auditing

Standards but are left for the auditors’ judgment. Lee and Ali (2008b) add that it is also

influenced by the dynamic objective of auditing and role of auditors, where contextual

factors such as socio-economic environments, critical historical events, courts or even

technological developments play an important role.

2.3.2 Audit expectation gap: Global evidence

Jedidi and Chrystelle (2009) reports that the basis for the research of audit

expectation gap in different part of the world can be found in the early works of Lee, Beck,

and Liggio, who investigated the role and responsibilities of auditors as perceived by the

users of audited financial statements. Afterwards, many others investigated the existence of

an audit expectations gap, identified its causes and made suggestions how to minimize it.

Despite a variety of research instruments used to identify audit expectation gap in different

countries, the survey or questionnaire dominated. Countries such as the US, the UK and

Canada have prevailed other countries in terms of research for audit expectation gap as this

topic was considered to an important issue for auditors especially after a number of

corporate failures (Jedidi&Chrystelle, 2009).

The financial crisis and number of collapse resulted in the new wave of questions

addressing the role and responsibilities of auditors, especially the ones to the stakeholders

of the company. Auditors have been criticized heavily on disclaiming responsibility for the

detection of fraud (Humphrey, Turley&Moizer, 1993) and interested parties (e.g. investors,

shareholders, creditors, government agency) had strong doubts about the auditors’ role in

term of audit client failure (Hassink et al, 2001). Over the period for more than 30 years up

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 27

to 2006, it became clear that mapping out the expectations is important especially in terms

of fraud detection. The users of audited financial statements expect much more from

auditors as compared to the legal acts regulating auditors work. Besides, public expects

auditors not only to provide audit opinion but also interpret the financial data of the

company in such a way that people are able to make a decision whether it is a good idea to

invest into one or another company (Salehi&Rostami, 2009).

Prior studies of the audit expectation gap presents different perceptions between

auditors’ and society’s view regarding the roles, objectives and responsibilities. In context

of the US, the research started as early as late 1970s. Auditor’s responsibilities to detect

material errors, irregularities and illegal acts are examined by Barton, Johnson, Searfoss,

and Smith (1977). The results indicate that auditors and users of financial statements had

different perceptions on the extent of auditors’ responsibilities. Such conclusions results

from miscommunications between the auditors and users, where the later devoted more

responsibility for the auditors to detect and disclose errors and irregularities. By analyzing

the extent of audit expectation gap in various dimension of the audit attest function,

McEnroe and Martens (2001) surveyed auditors and investors. The results indicate that

auditors and investors tend to agree about the meaning and importance of the specific

terminology, however, opinion differs with respect to actions to be done prior issuing

unqualified opinion. Investors expects that unqualified opinion is not issued unless 1) every

item of importance to investors and creditors has been reported or disclosed, 2) auditors

have been ‘public watchdogs’, 3) the internal controls are effective, 4) the financial

statements are free of misstatements resulting from management fraud, 5) the financial

statements are free of misstatements intended to hide employee fraud, 6) the firm has not

engaged in illegal operations (McEnroe&Martens., 2001)

The examination of the development of audit objectives in Britain during the period

1840-1940 by Chandler et al. (1993) reveals that external events tend to change public

perceptions towards auditor’s role thus creating the roots for audit expectation gap to

enlarge. Humphrey el at (1993) reports that chartered accountants, corporate finance

directors, investment analysts, bank lending officers and financial journalists possess

different view regarding the nature of audit and perceived performance of auditors. In

addition, the main contribution towards existing audit gap was mainly related to auditors’

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 28

roles and responsibilities in terms of fraud detection, liabilities to the third parties,

independence and methodology issues.

Similar findings were identified in less developed countries as well. In Malaysia for

example, Fadzly and Ahmad (2004) reports that general public opinion differs significantly

from the auditors regarding the auditors’ role and actions performed during the

engagement. Research findings were similar evidence provided by Porter (1993) who

investigate audit expectation gap in the UK and Porter and Gowthorpe (2004) who tested

the extent and development of audit expectation gap in the UK and New Zealand. Besides

the empirical evidence that audit expectation gap exist in Malaysia, analysis by Fadzly and

Ahmad (2004) also indicated that public expects more than auditors are obliged to do

unless they have proper education. The effect of education on perception of the meaning of

audit reports and responsibilities has been tested by a number of studies, most of which

concluded that expectation gap between auditors and students who have completed audit

courses exists but is of the lesser extent (Lee&Ali, 2008a). Research in China for example

was carried out by Lin and Chen (2004) who showed that the most important contributing

factors expanding audit expectation gap were different perceptions of audit objectives,

obligations regarding fraud detection and reporting as well as independence and liability.

Current research by Hassink et al (2009) also showed that, despite action taken to

narrow audit expectation gap, the business managers and bankers have higher expectations

of the duty of auditors than auditors considered their duties to be. Besides, they have

unreasonable expectations concerning auditor responsibilities to detect non-material fraud

or fraud from collusion. One may argue that audit expectation gap presents ‘diverse views

about audit function’ (Lee&Ali, 2008b). However, the majority of researchers name the

same contributing factors to the audit expectation gap, including complicated nature of an

audit function, conflicting role of auditors, hindsight evaluation of auditors’ performance,

time lag in responding to changing expectations, and self-regulation process of the audit

profession (Lee&Ali, 2008b). All this contributed to the mismatch between the expected

and actual performance, where it is said auditors ‘may fall short of the expected

performance’ (Salehi&Rostami, 2009). It is empirically tested and supported by a number

of studies in different countries. For example, the evidences of deficient performance of

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 29

auditors, or in other words underperformance, are identified in the research by Porter

(1993), Porter and Gowthorpe (2004), and Lee, et al. (2007) (see Table 5).

Table 5: Deficient performance of auditors

Porter (1993) Porter and Gowthorpe (2004) Lee, et al. (2007)

• Detect theft of corporate assets by non-managerial employees.

• Detect theft of corporate assets by company directors/senior management.

• Disclose in the audit report deliberate distortion of financial information.

• Disclose in the audit report misappropriation of company assets by company directors/senior management.

• Detect illegal acts by company officials which directly affect the company’s accounts.

• Express doubts in the audit report about the company’s continued existence.

• Disclose in the audit report illegal acts which directly affect company’s accounts

• Disclose in the audit report doubt about auditee’s continued existence.

• Detect theft of a material amount of the auditee’s assets by its directors/ senior management

• Detect theft of a material amount of the auditee’s asset by non-managerial employees.

• In the absence of regulated industry duty, report to an appropriate authority illegal acts by auditee officials.

• Detect illegal act by audit officials which directly impact on the auditee’s financial statements.

• Disclose in the audit report deliberate distortion of the auditee’s financial statements.

• In absence of a regulated industry duty, report to an appropriate authority, embezzlement of auditee’s assets by directors/senior management.

• Detect deliberate distortion of the figures in the company’s financial statements

• Report privately to a regulatory authority: • Theft has been committed by non-managerial employees. • Company directors/senior management has misappropriated company assets. • Information presented in the financial statements has been deliberately distorted. • Suspicious circumstances are encountered in the audit suggesting that theft or deliberate distortion of financial information may have occurred in the company

• Disclose in the published auditor’s report: • Company director/senior management have misappropriated company assets. • Information presented in the financial statements has been deliberately distorted.

• Illegal acts committed by the company’s management which directly impact on the company’s accounts.

Source: Adopted from Porter (1993), Porter and Gowthorpe (2004), and Lee, et al. (2007)

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 30

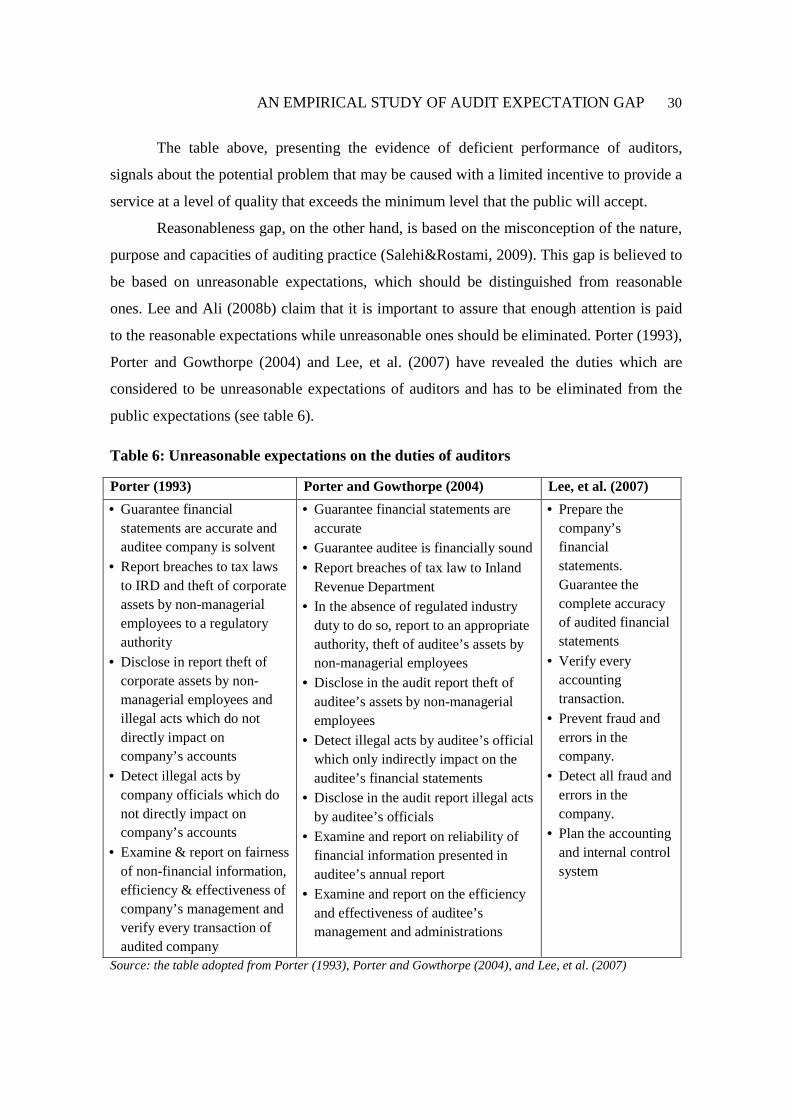

The table above, presenting the evidence of deficient performance of auditors,

signals about the potential problem that may be caused with a limited incentive to provide a

service at a level of quality that exceeds the minimum level that the public will accept.

Reasonableness gap, on the other hand, is based on the misconception of the nature,

purpose and capacities of auditing practice (Salehi&Rostami, 2009). This gap is believed to

be based on unreasonable expectations, which should be distinguished from reasonable

ones. Lee and Ali (2008b) claim that it is important to assure that enough attention is paid

to the reasonable expectations while unreasonable ones should be eliminated. Porter (1993),

Porter and Gowthorpe (2004) and Lee, et al. (2007) have revealed the duties which are

considered to be unreasonable expectations of auditors and has to be eliminated from the

public expectations (see table 6).

Table 6: Unreasonable expectations on the duties of auditors

Porter (1993) Porter and Gowthorpe (2004) Lee, et al. (2007)

• Guarantee financial statements are accurate and auditee company is solvent

• Report breaches to tax laws to IRD and theft of corporate assets by non-managerial employees to a regulatory authority

• Disclose in report theft of corporate assets by non-managerial employees and illegal acts which do not directly impact on company’s accounts

• Detect illegal acts by company officials which do not directly impact on company’s accounts

• Examine & report on fairness of non-financial information, efficiency & effectiveness of company’s management and verify every transaction of audited company

• Guarantee financial statements are accurate

• Guarantee auditee is financially sound

• Report breaches of tax law to Inland Revenue Department

• In the absence of regulated industry duty to do so, report to an appropriate authority, theft of auditee’s assets by non-managerial employees

• Disclose in the audit report theft of auditee’s assets by non-managerial employees

• Detect illegal acts by auditee’s official which only indirectly impact on the auditee’s financial statements

• Disclose in the audit report illegal acts by auditee’s officials

• Examine and report on reliability of financial information presented in auditee’s annual report

• Examine and report on the efficiency and effectiveness of auditee’s management and administrations

• Prepare the company’s financial statements. Guarantee the complete accuracy of audited financial statements

• Verify every accounting transaction.

• Prevent fraud and errors in the company.

• Detect all fraud and errors in the company.

• Plan the accounting and internal control system

Source: the table adopted from Porter (1993), Porter and Gowthorpe (2004), and Lee, et al. (2007)

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 31

Described existence and development of the audit expectation gap imply that users

of audited financial statements from different regions misunderstand the primary auditors’

role and thus possess different expectation on auditors. There are minor differences among

users in different part of the world; however, most of the users possess higher expectation

related to fraud prevention and detection as well as legal auditors’ liability from the

stakeholders’ perspective. Sometimes the gap is based on unreasonable expectations, which

should be distinguished in order to possess success when narrowing it. In Lithuania if such

gap does exists there may be different contributing factors. Thus the next section presents

the historical development of the audit function in Lithuania, which is the basis for the

analysis of the existence of audit expectation gap in Lithuania.

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 32

3 Audit function and audit expectation gap in Lithuania

3.1 Audit practice development in Lithuania

Prior to 1991 Lithuania was a part of the Soviet Union. After the regain of

independence, the lack of control and weak legislation system forced Lithuanian

government to focus on creation of own legislation system and its enforcement. Thus, the

grounds for Lithuanian audit practice are found in early 1990s, when the Association of

Lithuanian Accountants and Auditors was established (Mackevicius, 2001). This institution

was engaged in the creation of Auditing Practice Standards in Lithuania, which

unfortunately was not approved by the government.

Despite the lack of applicable legislation and legal grounds, auditing practice was

expanding in Lithuania, mainly with the entrance of the international network of audit firms

in Lithuania (Mackevicius, 2001). To mention a few, Arthur Andersen & Co as well as

KPMG, Price Waterhouse, Coopers and Lybrand were established during the period 1992-

1994. This in turn forced the creation of Lithuanian auditing firms. In addition, the growth

of private sector pushed the greater request for audit. The need for audit was fuelled by

growth of commercial enterprises, dishonest businessmen, and low qualification of

accountants working in private enterprises (Mackevicius, 2001).

Lithuanian Auditors Association established in 1997 was responsible for creating

legal grounds for auditing practice, supervise auditing standards creation projects and

recommend improvements, ensure and develop the professional auditors’ skills and

increase public recognition (LAA, 2011). It is important to note that Lithuanian auditing

system was based on the ‘bottom-up’ approach, meaning that it was created and

improvements were suggested by the public organizations engaged in audit practices with

limited governmental support. The government, however, paid an important role by issuing

the Republic of Lithuania Law on Audit in June 1999 (Lithuanian Parliament, 1999). This

document determined the establishment of the Lithuanian Chamber of Auditors (hereinafter

LCA), which in turn had to supervise of the activities of audit enterprises, issue, suspend

and terminate the auditor’s certificates, handle the register of audit enterprises and perform

other functions (Mackevicius, 2001). After the Law on Audit came into the force, it was

AN EMPIRICAL STUDY OF AUDIT EXPECTATION GAP 33

important to create the proper audit methodology, thus LCA approved 11 National Auditing

Standards (hereinafter NAS) and Auditors’ Professional Code of Ethics in June 2000.

Today, LCA as a public legal entity unifying all certified auditors of Lithuania shall

act in conformity with the Constitution of the Republic of Lithuania, Civil Code of the

Republic of Lithuania, the Law on Audit, the Law of Associations of the Republic of

Lithuania other legal acts of the Lithuania and European Union (hereinafter EU) and the

present Statute of LCA (LCA, 2010). Besides, it supervises the activities of auditors and

audit companies in Lithuania, develops the audit methodology and recommendations for

the Lithuanian auditors, translates ISAs, the Code of Ethics and other documents issued by

the International Federation of Accountants (hereinafter IFAC). According to statistics, on

1st May 2011 the LCA unified 399 certified auditors and 188 audit firms of Lithuania

(LCA, 2011). Approximately 62 % of these certified auditors worked in public practice,

providing a wide range of services to clients. Other 38 % work in various areas such as

industrial, governmental and educational institutions. Note that in 2003 LCA became an

associated member of IFAC and in 2004 the General Assembly of European Federation of

Accountants (hereinafter FEE) approved the LCA membership as a member correspondent.

In 2008 LCA became a true member of IFAC and FEE (LCA, 2010).

Mackevicius (2001) notes that there are three key elements which guarantee stable

and reliable auditing system. These elements are legal, methodological and control

frameworks. In Lithuania legal framework is based on the Law on Audit and by the

Auditors’ Professional Code of Ethics. These two documents regulates the main areas of

audit practice, defines the independence, responsibility, relations with clients. Even though

it took almost 10 years to prepare those legal documents, it is expected that properly

prepared they have to influence positively most of the areas, including audit practice,

quality, responsibility, trust, and stimulate the qualification improvement. Methodological