Languages

Pages

Legal

Adding Value to SMEs Through

Venture Capital (VC)Michael Olorunninwo

Quaking Aspens

Quaking Aspens

2

Outline

Introduction – Industry Focus

Venture Capital Advantage

Challenges Faced by VCs in the Emerging Markets

Quaking Aspens

3

• VC is a branch of Private Equity (PE) strategically

focused on providing early stage financing to start-up

and small businesses i.e. SMEs

• PE firms provide risk capital to large, established

businesses with proven markets, and growth potentials

• While VCs focus on SMEs with perceived long term

growth potentials

• Similar to mainstream PEs, VCs also bring on board

managerial and technical expertise, and have a say in

strategic decisions

• Most start-ups usually commence operations as SMEs,

requiring patient, risk capital often between $25,000

and $2 million

• Emerging markets offer great investment opportunity

for VCs, especially in Sub-Saharan West Africa

Industry Focus – Venture Capital

Introduction

Source: Financial Times, World Bank, CFED, Africa Economic Outlook

Missing Middle of SME Financing

7.8 7.9

5.9 5.3 5.6 5.8 5.56.9 6.2

6.9 6.4

0.0

2.0

4.0

6.0

8.0

10.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Western Africa - Real GDP growth (%)

Quaking Aspens

Unfriendly business environment:poor infrastructure, inconsistent government policies, inadequate economic incentives, poor legal framework, corruption

4

SMEs in the Emerging Markets…

Key Growth Drivers

Rising in income levels and the consuming class− Annual consumption to rise to $30

trillion by 2025, up by >100% from 2010

Impressive Growth in Emerging Market companies− Emerging markets to significantly

outperform developed markets− Average GDP growth of 4 to 7% p.a.

Double-digit growth of mobile phone, internet, e-commerce usage (internet penetration rising faster)

More stable politics, propelling driving economic reforms

High proportion of active population, about 40-60%

Source: CBN, Bain Insights, McKinsey Global Institute.

Increased entrepreneurial flair, huge informal sector

Poor funding: little access to flexible, risk capital, high interest rates (~23%), unreasonable collateral requirements, poor relationship with banks

Low managerial skills: dearth of skilled business managers, inadequate knowledge of business practices, poor succession and corporate governance, high cost of consulting fees

Key Challenges

Low access to modern technology: probably due to high costs (access to finance), dependence on importation, lack of training

Potential areas for VC value-add

Quaking Aspens

5

• However, SMEs presents unmatched opportunities in the emerging market due to:◊ Huge potential for growth: GDP is growing

at ~6%+, increasing consumer population, better reforms

◊ Potential for Social, Environmental & Economic Impact: crucial contributor to job creation and economic growth

◊ Lower capital requirements: i.e. investors can spread risk across investment portfolios

◊ Potential to contribute to poverty alleviation & achieve productivity gainsthrough the infusion of new technologies and business practices

◊ Access to new (underserved) or growing markets

◊ Opportunities abound in agribusiness, tech. and e-commerce, manufacturing, and retail

Reason to Invest in SMEs?

Why a targeted growth effort for SMEs?

Source: CBN, USAID, World Bank

As the world look to Emerging Markets for growth, the evident financing gap could potentially undermine global prosperity, with negative

consequences for innovation, economic growth, and global macro-economic resilience

Differences in SME contribution to GDP for low-income and high-income countries, show that growth in SMEs is likely to come from the informal sector

Quaking Aspens

6

• VC improves access to funding - a major hindrance to

emerging market SME opportunities and perform other

roles, such as:

Bringing on plans to seek new markets, innovate, train

management teams, improve business processes, make

acquisitions, strengthen financial controls and operating

systems

Hand-holding management through strategy execution

to create active value-adding partnerships, often

required by businesses

Providing managerial talent, assisting investee

businesses to produce better returns

Ensuring efficient resource (i.e. finance and

management time) allocation to opportunities with

potential for economic success and societal impact

• Interesting, in the last 5 years, PE returns have been on

the rise in the emerging markets

Venture Capital Advantage

VC Investments targeted at Emerging Markets

Deal Sourcing

Evaluation

Structuring

Investment Management

Exit Management

1

2

3

4

5

Venture Capital Value Map

О Key area with tremendous VC value-add potential

Source: Capricorn Capital Partners, Bain Insights

Quaking Aspens

7

Why VC Value Model is Essential for Growth?

Deal Sourcing

Evaluation

Structuring

Investment Management

Exit Management

1

2

3

4

5

Corporate governance:

strengthen financial controls, risk

management

Manage relationship with other

funding parties: with banks

Build management team, and

incentivise growth

Develop growth strategies and

provide implementation support

Initiate value-driven mergers

and acquisitions

Manage growth for sustainability

Provide well developed networks, in-depth sectorial knowledge, proactive targets

Play hands-on role during due diligence

Focus on strategy alignment

Grow businesses in size & profitability such that exits via, trade sale, listing, other investors, become possible

Quaking Aspens

8

Challenges Facing VCs in the Emerging Markets (SSA)1

• Investing in the emerging markets comes with various challenges. VCs must have

capabilities or strategies to overcome these challenges:

• Finding good investmentsDetermined by calibre of management team. Need for effective due diligence

• Riskier investment profilesRequire accurate understanding of local markets, regulatory environment, etc.

• Availability of limited leverageNeed for strong relationships with other funding institutions e.g. banks, etc.

• Challenges of survival and growthNeed for VCs to have strong operational capability to assist with growth

• Apathy towards equity dilutionNeed for market reputation, communicating benefits of VC

1. Sub-Saharan Africa

Appendix

Quaking Aspens

10

Total Value of Gap in SME Finance

Source: OECD, World Bank, Capricorn Capital Partners

Appendix I: Gaps in SME Finance

14.4%

5.2% 5.1%

14%

4.9% 5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Small Caps Medium Caps Large Caps

3 year 5 year

Turnover Growth (%)(world average p.a.)

Quaking Aspens

11

Appendix II: Limited Sources of Sustainable Funding for SMEs

Source: CBN, ICA

0%

10%

20%

30%

40%

50%

60%

70%

Total Small Medium Large

Difficulty of Access Cost of Debt

Percentage of SMEs reporting access to finance and cost of debt as a challenge (Nigeria)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Nigeria Brasil Indonesia S. Africa India China

Difficulty of Access Cost of Debt

Sources of Financing (selected countries) Nigeria Brazil China India Indonesia Kenya S. Africa

Retained Earnings 70% 44% 13% 47% 38% 73% 66%

Banks and Other FIs 1% 30% 27% 32% 16% 7% 17%

Credits from Suppliers & Customers 25% 15% 2% 9% 4% 17% 12%

Family & Friends 4% 5% 8% 9% 20% 3% 1%

New Equity/Debt 0% 4% 12% 2% 2% 0% 1%

Others 0% 2% 38% 1% 20% 0% 3%

Majority of emerging market SMEs reported limited access to sources of finance.

Percentage of SMEs reporting access to finance and cost of debt as a challenge

(Selected Countries)

Quaking Aspens

12

Appendix III: Access to Finance as a Major Constraint

Source: IFC, World Bank

Businesses in high income countries, regardless of size, generally have better access to finance

Location of businesses defines huge disparity in access to funding.

Quaking Aspens

13

Appendix IV: Growth in the Emerging Markets

Source: Bain Insights

Consumption in the emerging markets expected to increase by >100% in the next 15 years.

Growth in emerging market companies surpasses those of developed markets by >100%

Quaking Aspens

14

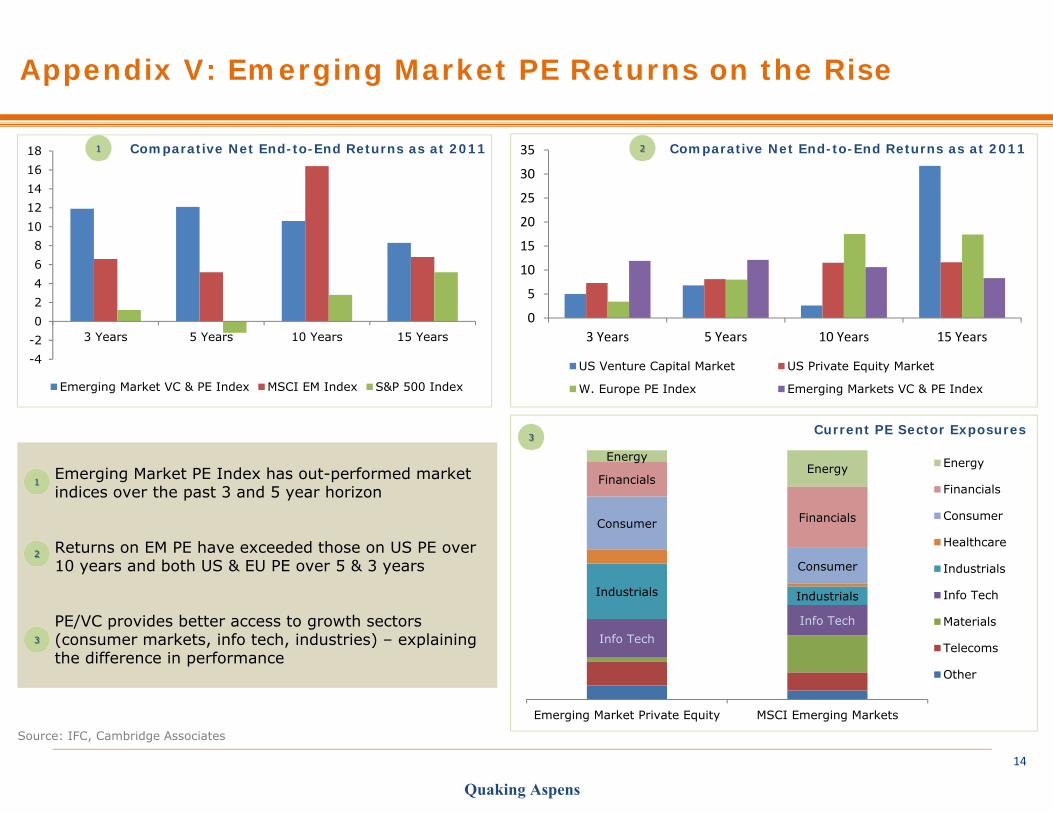

Appendix V: Emerging Market PE Returns on the Rise

Source: IFC, Cambridge Associates

Emerging Market PE Index has out-performed market indices over the past 3 and 5 year horizon

Returns on EM PE have exceeded those on US PE over 10 years and both US & EU PE over 5 & 3 years

PE/VC provides better access to growth sectors (consumer markets, info tech, industries) – explaining the difference in performance

-4-202468

1012141618

3 Years 5 Years 10 Years 15 Years

Emerging Market VC & PE Index MSCI EM Index S&P 500 Index

Comparative Net End-to-End Returns as at 2011

0

5

10

15

20

25

30

35

3 Years 5 Years 10 Years 15 Years

US Venture Capital Market US Private Equity Market

W. Europe PE Index Emerging Markets VC & PE Index

Current PE Sector Exposures

Info TechInfo Tech

Industrials Industrials

Consumer

Consumer

Financials

Financials

EnergyEnergy

Emerging Market Private Equity MSCI Emerging Markets

Energy

Financials

Consumer

Healthcare

Industrials

Info Tech

Materials

Telecoms

Other

1 Comparative Net End-to-End Returns as at 20112

3

1

2

3

Quaking Aspens

15

Appendix VI: The Opportunity keeps getting bigger

Source: IFC

Developed Markets Emerging Markets with PE OpportunityWithin the 10-year horizon from 2000 to 2010, PE has expanded to more countries in the emerging markets. West Africa represents a growing investment destination for PE, with Senegal, Cote d’Ivoire, and Ghana, now joining Nigeria, on the African PE map.

Quaking Aspens

Appendix VII: Country Overview – Nigeria

Overview● Economic growth has averaged about 7.4% annually over the past

decade and remained robust in 2011 at 6.9%, driven by the non-oil sector (i.e. telecommunications, construction, wholesale and retail trade, hotel and restaurant services, manufacturing and agriculture).

● Government is expected to reach its target inflation of under 10% in 2013. Inflation rate fell 10.2% in 2011; but climbed to 12% following removal of subsidies on petroleum products.

● The economic growth has not cut poverty nor created necessary jobs. About two thirds of the population live on less than US$1 per day and unemployment rate in 2011 was 23.9%, up from 21.1% in 2010. Unemployment in the 15-24 age group was 37.7%, and for 25-44 years, 22.4%.

● Informal economy account for a large proportion of employment.

PEST Analysis

Political Economic

● Relatively stable political climate following peaceful elections.

● Violence in the North by extremist groups is greatest source of concerns

● Corruption levels remain high, undermining recent economic reforms

● GDP growth is expected to be sustained

● Private and informal sector employs 80% of the economy

● Access to and high cost of finance remain a major constraint to growth

● Another challenge to growth is dilapidated state of infrastructure and over-dependence on oil revenue by government.

Social Technological

● Social indicators on health and education remain weak. The 2011 UN Human Development Report ranked Nigeria 156th out of 187 countries.

● Increasingly successful telecoms sector, increase in mobile telephony and internet usage

● Reforms in financial sector point towards the embrace of technology to drive growth

Selected Economic Indicators 2010 2011 2012 2013

Real GDP growth 7.8 6.7 6.9 6.6

Real GDP per capita growth 5.3 4.1 4.4 4.1

CPI inflation 13.7 10.2 10.1 8.4

Source: World Bank Database, Economist Intelligence Unit, Africa Economic Outlook

Major Sectors (contribution to GDP)Agriculture: 35%; Mining and Quarrying: 34%; Wholesale & Retail: 16%;Finance, Retail Estate & Business Services: 6.3%; Manufacturing: 2%0.0

2.04.06.08.0

10.012.0

Real GDP growth (%)

Western Africa - Real GDPgrowth (%)

Africa - Real GDP growth(%)

Quaking Aspens

Appendix VII: Country Overview – Ghana

Overview● Ghana made progress in consolidating the gains made in the

management of its macro-economy. Inflation dropped to 8.7 % and the fiscal deficit fell to 4.3 % of gross domestic product (GDP).

● Middle-income status and oil receipts have provided the country with the fiscal space to seek non-concessional sources of finance.

● Country continues to enjoy a more open society, with a vibrant media and strong public dialogue, which point to the consolidation of democratic rule.

● These have enabled Ghana to outperform most countries in West Africa and in the continent on measures of civil liberty, political rights and political stability.

PEST Analysis

Political Economic

● The organisation of district level elections came under pressure due to 2010 altering of the local Government Act.

● Smooth transition following recent death of incumbent president received global applause.

● Use of biometric registration in 2012 elections is expected to further check irregularities.

● Government has been undertaking policy and regulatory reforms for conducive enterprise development.

● Ranked twice as top 10 global reformer by World Bank's Doing Business Report.

● Private sector increasingly being considered as significant financial & deliverty partner for infrastructure.

● Oil production to boost economy.

Social Technological

● Rapid population growth rate contribute to poverty and underdevelopment

● Mobile telecoms is seeing significant growth. Currently among the top 10 projected to rule Africa’s ICT sector

Selected Economic Indicators 2010 2011 2012 2013

Real GDP growth 7.7 13.7 8.3 7.7

Real GDP per capita growth 5.4 11.3 6 5.4

CPI inflation 10.8 8.7 8.2 7.7

Source: World Bank Database, Economist Intelligence Unit, Africa Economic Outlook

Major Sectors (contribution to GDP)Agriculture: 30%; Wholesale & Retail: 12%; Transport & Communications: 12%; Finance, Retail Estate & Business Services: 10%; Manufacturing: 7%

0.02.04.06.08.0

10.012.014.016.0

Real GDP growth (%)

Western Africa - Real GDPgrowth (%)

Africa - Real GDP growth(%)

Quaking Aspens

Appendix VII: Country Overview – Senegal

Overview● GDP grew by 4% in 2011 and this rhythm is expected to continue

during the coming years, with forecasts of growth around 4.2% and 4.7% in 2012 and 2013 respectively.

● Growth is driven mainly by private consumption, which itself is sustained by transfers from emigrant Senegalese working abroad, and by the industrial and service sectors.

● The elections were a major challenge to the country's democracy, given rise to disagreements over validity of the candidacy of outgoing president. However, the positive conduct of the presidential election allayed fears of instability.

● Unemployment remains a crucial problem, especially for young adult whose employment rate is 25% below that of adults.

Source: World Bank Database, Economist Intelligence Unit, Africa Economic Outlook

PEST Analysis

Political Economic

● Relatively stable political climate following peaceful elections.

● Still underlying an threat is intermittent intensification of violence from the 30-year insurgency by separatist rebels.

● GDP growth is expected to accelerate driven by ambitious infrastructure investment funded by Eurobond.

● Country’s flourishing relations with China and gulf states is expected to boost FDI inflows.

● There is no need for rapid investment in various sectors to support growth trends

Social Technological

● 42% of the population live in urban centres, given its current urbanisation rate of 3.3%, half of the population will be reside in urban centres by 2015.

● Presence of good fixed line telephone system, although nearly two-thirds all fixed-line connections are in the capital, Dakar, where a call-center industry is emerging

Selected Economic Indicators 2010 2011 2012 2013

Real GDP growth 4.1 4 4.2 4.7

Real GDP per capita growth 1.4 1.3 1.6 2.1

CPI inflation 1.2 3 2.6 1.9

Major Sectors (contribution to GDP)Wholesale & Retail: 20%; Agriculture: 17%; Transport & Communications: 12%; Manufacturing: 14%; Finance, Real Estate & Business Services: 13%

0.01.02.03.04.05.06.07.08.09.0

Real GDP growth (%)

Western Africa - Real GDPgrowth (%)

Africa - Real GDP growth(%)

Quaking Aspens

Appendix VII: Country Overview – Cote d’Ivoire

Overview● GDP growth contracted by 5.9% in 2011, the economy was hard

hit by the negative effects of post-electoral crisis.

● Substantial growth rates forecast (8.6% and 5.5% respectively, for 2012 and 2013) depend upon peace being consolidated and productive capacities being restored.

● Need for accelerating the reforms set out in the Extended Credit Facility (ECF) 2012-14 which aim to improve governance and the business environment and boost performance in the financial, energy and coffee-cocoa sectors.

● The mismatch between training and employment and the weakness of the job prospecting system comprise obstacles to the promotion of youth employment and hampering efforts to reduce poverty.

PEST Analysis

Political Economic

● Institutional normalisation, strengthening of democratic process and progress towards reunification and reconciliation is encouraging

● Pleas for reconciliation and peace will need to be reinforced by dialogue

● Hard hit by conflict, government introduced reforms and tax breaks to help the private sector

● Country witnessed improvement on Doing Business Rankings

● Institution of public sector reforms is expected to drive economy towards normalisation

Social Technological

● Youth unemployment is a challenge, recently estimated at 40%.

● Government is now implementing a poverty reduction programme

● Technology use is drastically improving and represents a major growth sector in the economy.

Selected Economic Indicators 2010 2011 2012 2013

Real GDP growth 2.4 -5.9 8.6 5.5

Real GDP per capita growth 0.4 -8.1 6.4 5.5

CPI inflation 1.7 4.9 3.6 3.1

Source: World Bank Database, Economist Intelligence Unit, Africa Economic Outlook

Major Sectors (contribution to GDP)Agriculture: 31%; Wholesale & Retail: 14%; Manufacturing: 13%; Finance, Retail Estate & Business Services: 11%; Government Services: 9%;

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2003 2004 2005 2006 2007 2008 20092010 2011 2012 2013

Real GDP growth (%)

Western Africa - Real GDPgrowth (%)

Africa - Real GDP growth (%)

Adding Value to SMEs Through Venture Capital

Michael Olorunninwo

August 2012

Quaking Aspens is a social enterprise focused on providing business solutions to

high-potential SMEs in Africa.

Our focus is to embrace SME entrepreneurs as they aspire to attain efficiency, pursue

new markets, visible growth, and profitability.

Our teams are made up of experienced, multi-disciplinary professionals from various

fields in consulting.

Top Related