Languages

Pages

Legal

A New View of the Food ChainStefano NatellaMujtaba RanaVamil DivanCharlie Mills

Sugar

December, 2013

Sugar supply chain

September 11, 2013

1

- Manufacturers, e.g. Nestle, Coca-Cola, Pepsi, Kraft, Mondeléz

- Flavouring, e.g. DSM, Givaudan

Food & Beverage

- Agribusiness, e.g. ADM

- Processors, e.g. ABF, Tongaat

Agribusiness / Sugarproducers

- Trading, e.g. Glencore, Noble

- Refiners, e.g. Cargill, Bunge

Trading / Refining

- Agribusiness, e.g. Wilmar

- Processors, e.g. ABF, Cosan

Sweeteners

- Government

- Health Authorities

- Taxation

Regulation ?

- Bottlers, e.g. Coca-Cola FEMSA, Coca-Cola

Hellenic

Packaging

CONSUMERS

- Pharma. e.g. Novo Nordisk, Sanofi

- Managed Care. e.g. United Health

-Medical Care. e.g. Fresenius

Healthcare

Sugar and Type II Diabetes – Medical History

Etienne Lancereaux (1829-1910)French doctor who studied diabetes and pancreas

Haven Emerson (1874-1957)New York city Public Health Commissioner and Columbia Professor

Sir Frederick Banting (1891-1941)Nobel Peace Prize for medicine for insulin discovery (1923)

John Yudkin (1910-1995)British physiologist and scientist

“Fat diabetes is due to over consumption of sugar” (1877)

“Sweetness of Death” (1924)

“In the U.S. the incidence of diabetes has increased proportionally with the per capita consumption of cane sugar” (1929)

Pure, White and Deadly (1972)

September 11, 2013 2

September 11, 2013 3Source: Stephan J. Guyenet and Jeremy Landen

Medical Research: Increase in Sugar Consumption

86%

74%

85%

98%

Global

Asia

EU

US

Obesity

September 11, 2013 4

91%

86%

92%

96%

Global

Asia

EU

US

Type II Diabetes

74%

70%

73%

78%

Global

Asia

EU

US

Non-Alcoholic/Fatty Liver

Sugar Consumption is linked to the development of:

Yes / Definitely Yes

Doctor’s Opinions:

Septem

ber 11, 2013

The C

onsumer: C

aloric intake of sw

eeteners by country

0

10

0

20

0

30

0

40

0

50

0

60

0

70

0

80

0

Bangladesh

China

AFRICA

India

DEVELOPING WORLD

Indonesia

WORLD

Japan

Pakistan

Korea

Turkey

Iran

Egypt

DEVELOPED WORLD

Saudi Arabia

Thaïland

Uruguay

Algeria

EUROPE

South Africa

Russian Federation

Chile

Ukraine

Malaysia

LATIN AMERICA

Canada

Mexico

Argentina

Australia

Brazil

United States

Ca

lorie

s from

Su

ga

rC

alo

ries fro

m H

FC

S

5

September 11, 2013 6

The Consumer: Added Sugars

September 11, 2013 7

The Advertisement Battle: The Response

September 11, 2013

� Availability (New York, California, Other States)

� Labeling (Europe)

� Composition / Sugar Level (Aspartame -EU)

� Excise Tax (France, Hungary, Mexico)

� Education (EU, NY, Mexico)

8

Potential Regulatory Responses

� What do we expect to happen? - Whether consumers voluntarily move away from sugar-enriched food and beverages as they become more aware of its adverse health effects, or because tax and governmental regulation incentivizes change, we expect a shift in consumption levels downwards. More specifically:

1. Sugar demand to slow down with a potential impact on sugar prices2. Increasingly negative public opinion being followed by the real threat of regulation and

taxation3. Beverage and food manufacturers moving more aggressively towards “self-regulation”.4. Fast growth in the natural sweetener space and broadening of food and beverages’

product portfolios

� Why now? – The discussion on sugar linked to dietary concerns has been gathering momentum. The related global healthcare costs are at an all-time high (the bill is $500 billion or over 10% of global healthcare spending), as are obesity & diabetes levels.

July 2, 2013 9

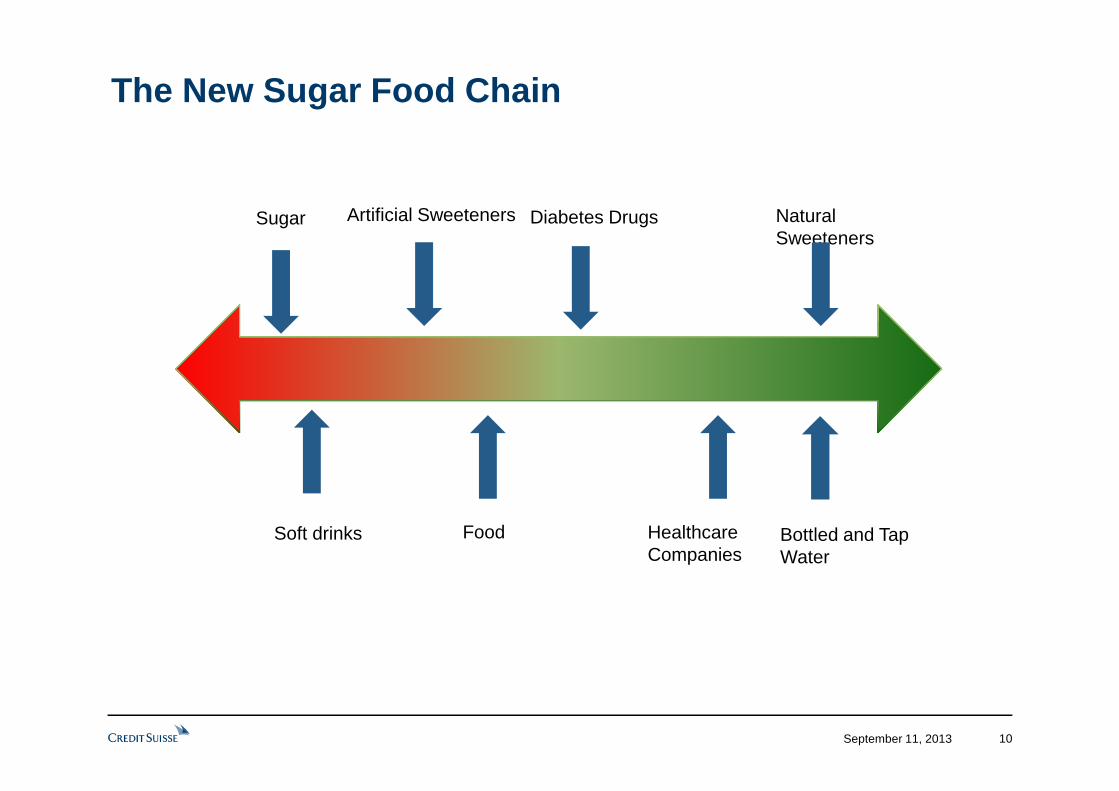

Sugar – What Can Happen?

September 11, 2013 10

Sugar Diabetes Drugs Natural Sweeteners

Soft drinks Food Healthcare Companies

Artificial Sweeteners

The New Sugar Food Chain

Bottled and Tap Water

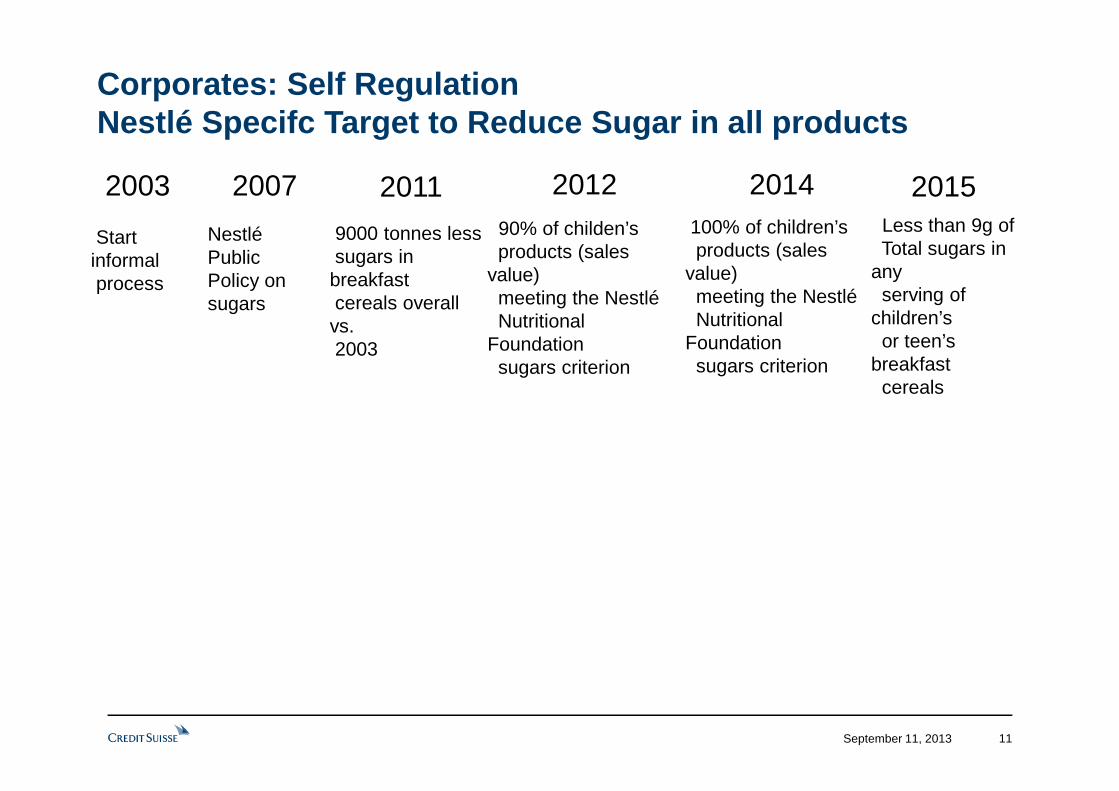

Corporates: Self RegulationNestlé Specifc Target to Reduce Sugar in all product s

September 11, 2013 11

Less than 9g ofTotal sugars in

any serving of

children’sor teen’s

breakfastcereals

9000 tonnes less sugars in breakfast cereals overall vs. 2003

100% of children’s products (sales

value) meeting the Nestlé Nutritional

Foundationsugars criterion

90% of childen’sproducts (sales

value) meeting the Nestlé Nutritional

Foundationsugars criterion

Nestlé Public Policy on sugars

2007 2011 2012 2014 20152003

Start informal process

September 11, 2013 12

The Corporates: New Launches Coca Cola Life

September 11, 2013

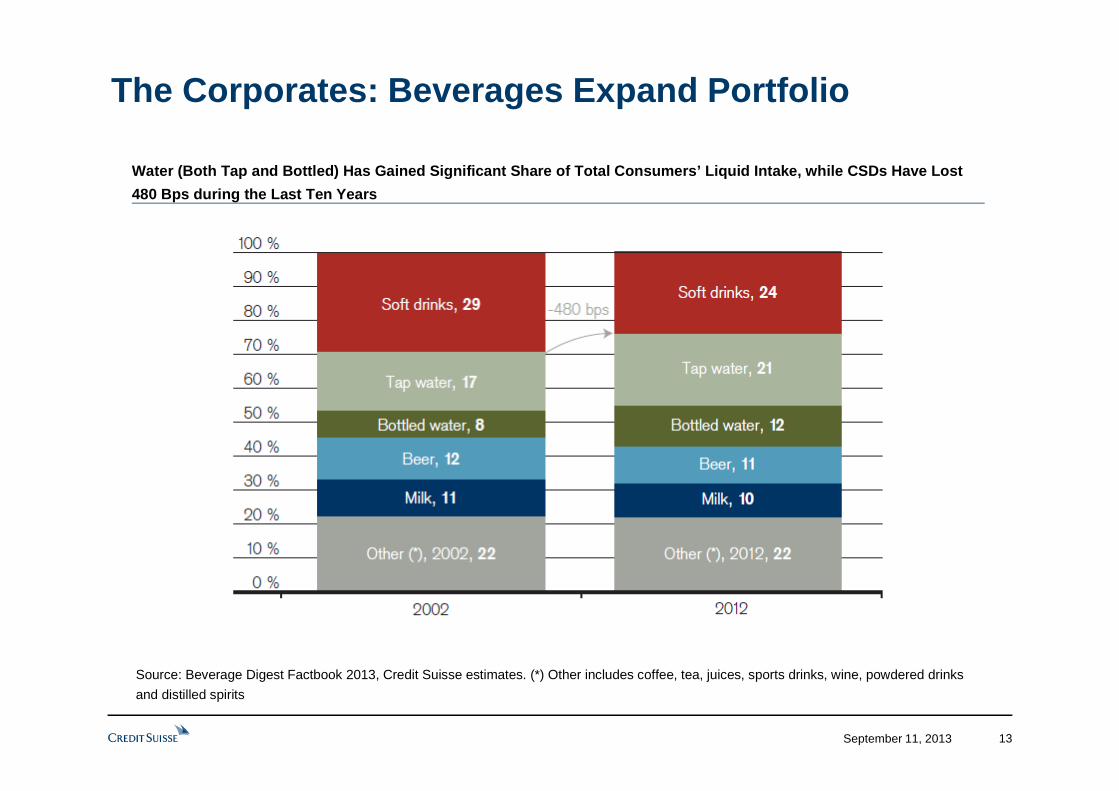

Water (Both Tap and Bottled) Has Gained Significant Share of Total Consumers’ Liquid Intake, while CSD s Have Lost

480 Bps during the Last Ten Years

13

Source: Beverage Digest Factbook 2013, Credit Suisse estimates. (*) Other includes coffee, tea, juices, sports drinks, wine, powdered drinks

and distilled spirits

The Corporates: Beverages Expand Portfolio

September 11, 2013 14

The Corporates: Natural Sweeteners

Top Related