Languages

Pages

Legal

Capital Forecasting Model

28-10-2009 1

A leading Danish financial institution

3 brands Market shares in Denmarkand volumes as at end September 2009

VolumeEURbn

Totallending

Mortgage banking(bond debt outstanding)

131 41%(bond debt outstanding)

131 41%

26%Commercial banking (loans and guarantees)

14 4%

Customers 1,128,000

Facts as at Q3/2009Asset management 9 5%

Fund administration 28 28%Staff 4,538

Equity EUR 6.9bn

Tier I ratio 15.7%

Fund administration 28 28%

Insurance(premium income)

0.38 4%

Tier I ratio 15.7%

Estate agencies(number of properties sold)

9,027 20%

28-10-2009 2

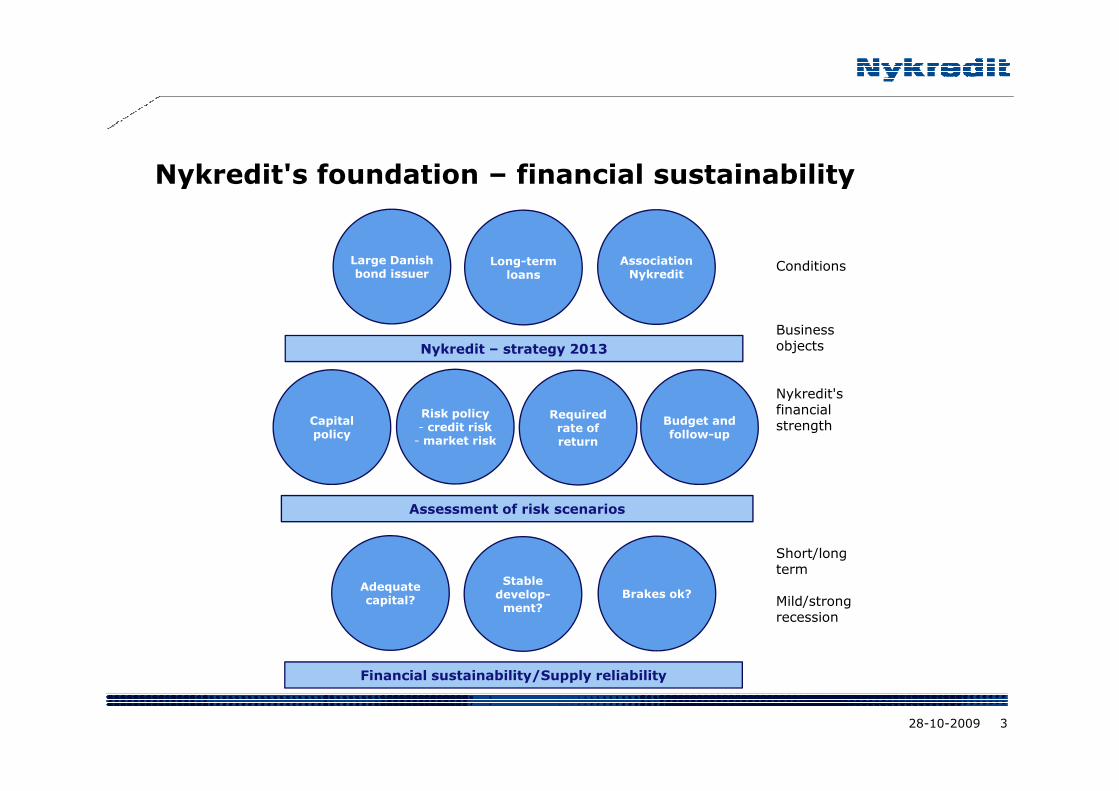

Nykredit's foundation – financial sustainability

Large Danish bond issuer

AssociationNykredit

Long-term loans

Conditions

Nykredit – strategy 2013

Business objects

Nykredit's

Risk policy - credit risk

- market risk

Budget and follow-up

Required rate of return

Capital policy

Nykredit's financial strength

Assessment of risk scenarios

Stable

Short/long term

Adequate capital?

Brakes ok?Stable develop-ment?

term

Mild/strong recession

Financial sustainability/Supply reliability

28-10-2009 3

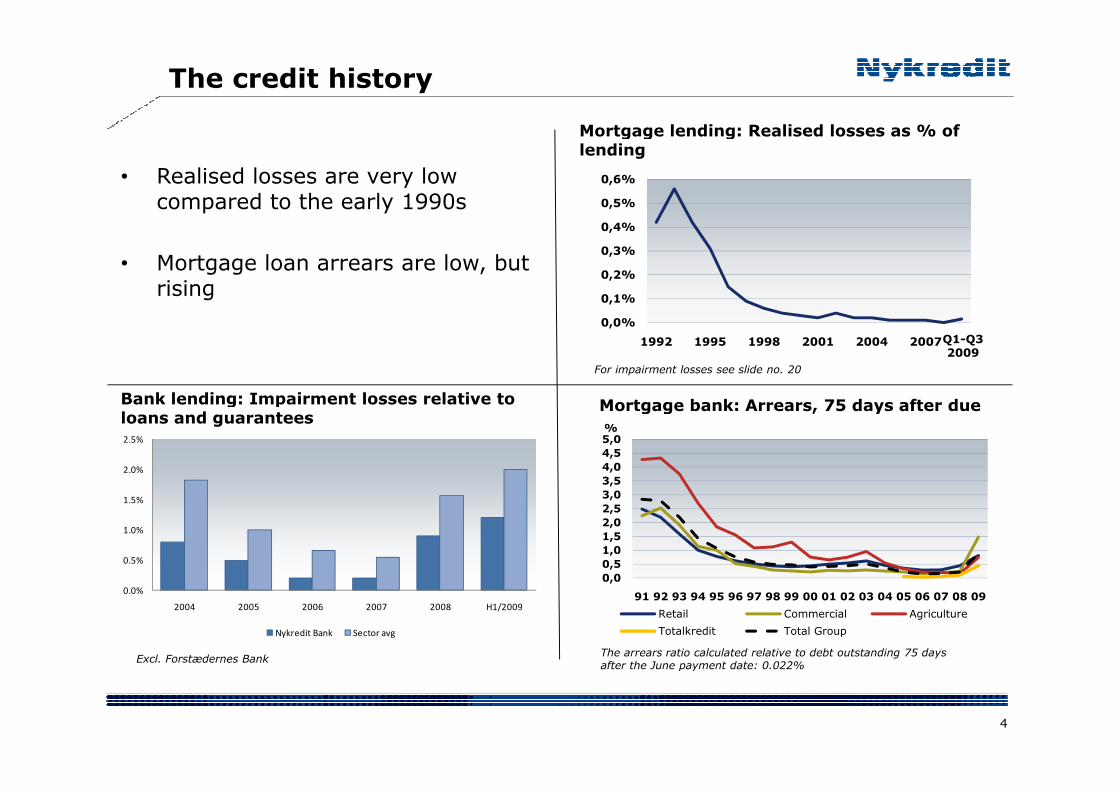

The credit history

Mortgage lending: Realised losses as % of

• Realised losses are very low compared to the early 1990s

Mortgage lending: Realised losses as % of lending

0,5%

0,6%

• Mortgage loan arrears are low, but rising

0,1%

0,2%

0,3%

0,4%

Bank lending: Impairment losses relative to

0,0%

1992 1995 1998 2001 2004 2007Q1-Q32009

Mortgage bank: Arrears, 75 days after due

For impairment losses see slide no. 20

Bank lending: Impairment losses relative to loans and guarantees

2.0%

2.5%

Mortgage bank: Arrears, 75 days after due date

3,5

4,0

4,5

5,0%

0.5%

1.0%

1.5%

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

0.0%

2004 2005 2006 2007 2008 H1/2009

Nykredit Bank Sector avg

The arrears ratio calculated relative to debt outstanding 75 days after the June payment date: 0.022%

0,0

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Retail Commercial Agriculture

Totalkredit Total Group

Excl. Forstædernes Bank

4

after the June payment date: 0.022%

Capital forecasting

The forecasting model will compare capital requirements to available financial resources under different scenarios

Current position• Basis for the analysis

– Economic capital and regulatory capital forrelevant risk types

resources under different scenarios

Available capital, driven by

relevant risk types– Portfolio segmentation– Capital measure/current capital resources

Base case

Available capital, driven by earnings, will move counter cyclically with required capital

Base case

Base case• Forecasts of earnings, capital requirements

and available capital– Earnings and volumes as input to the

Buffer

Capital

Scenario

– Earnings and volumes as input to themodel

Scenarios to model risk types• Deviations from the base case derived from

Capital

Base case

Scenario

• Deviations from the base case derived frommacroeconomic scenarios– Capital requirements given by risk drivers– Available capital driven by changes in

earnings and investments

Required capital, particularly driven by credit risk, will fluctuate over the cycle• Cyclicality of default probabilities• Cyclicality of recovery rates

earnings and investmentsTime

28-10-2009 5

Capital Forecasting Model

History

Macroeconomic variables

Nykredit Group

Macroeconomic variables

Internal losses

Risk

sensitivities- Current portfolio of assets

- Balance sheet

sensitivities Results

- Economic capital

- Balance sheet

- Projection of lending, earnings and capital Stress test Model

- P/L

- Granular credit risk projection

- Capital requirement

Macro Scenarios

- Base Case

- Stress scenarios- Stress scenarios

28-10-2009 6

Input data from Nykredit

One million exposures

are clustered into 10.000 Balancehomogenic groups Capital

structureP/L

Balance

sheet

data

Risk data

Nykredit Realkredit Nykredit Realkredit

Nykredit Bank

Totalkredit

Nykredit Insurance

Cluster

dataStress model

Nykredit Insurancedata

28-10-2009 7

Learning from historyLearning from history

Risk sensitivity models

Seven segment-specific models translating economic variables into Seven segment-specific models translating economic variables into changes in default rates and PDs

−

⋅+=

−

2

1

1

)(

ρ

ρ MCTNNDR

M

−

=21 ρ

NDRM

Nykredit Group

- Time series of losses and default rates 1990 - 2008

Macroeconomic data

- Time series of historic macroeconomic variables

Owner

Industry

Interest rate factor

Property pricesdefault rates 1990 - 2008

2,0

2,5

3,0

3,5

4,0

4,5

5,0

%

macroeconomic variables

800

1.000

1.200

1.400

1.600

1.800

Mia. kr.

Industry

Commerce

Financial

Rental

Agriculture

Bank

Property prices

Real GDP

Unemployment rate

Danish stock index

0,0

0,5

1,0

1,5

2,0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Privat Erhverv Landbrug Totalkredit Koncern i alt

0

200

400

600

800

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Scenario selection

• Risk management composes base case and stressed scenarios in collaboration with Nykredit Marketsscenarios in collaboration with Nykredit Markets

• The Risk Committee chooses two core stress scenarios from a range of different constructed scenariosfrom a range of different constructed scenarios

Three core scenarios are constructed each quarter

Stress

Base case Mild recession Severe recession

Stress

28-10-2009 9

Macroeconomic scenarios

Interest rates GDP

3,5%

4,0%

4,5%

5,0%

Interest rates

1%

2%

3%

GDP

1,5%

2,0%

2,5%

3,0%

3,5%Basis

Mild stress

Severe stress

NB: Prognosis

NB #1

-2%

-1%

0%Basis

Mild stress

Severe stress

NB: Prognosis

NB #1

0,0%

0,5%

1,0%

1,5%

2009 2010 2011

NB #1

NB #2

-5%

-4%

-3%

2009 2010 2011

NB #1

NB #2

9%

10%

Unemployment rate5%

Property prices

5%

6%

7%

8%

9%

Basis

Mild stress

Severe stress

-5%

0%

Basis

Mild stress

Severe stress

1%

2%

3%

4%

Severe stress

NB: Prognosis

NB #1

NB #2-15%

-10%

Severe stress

NB: Prognosis

NB #1

NB #2

0%

2008 2009 2010 2011

-20%

2009 2010 2011

28-10-2009 10

Capital need and economic cycles

28-10-2009 11

Macroeconomic assumptions behind Pillar IIMacroeconomic assumptions behind Pillar II"Slightly pessimistic economic climate" equal to economic experts

Full year

estimate

2009

Full year

estimate

2010

Full year

estimate

20112009 2010 2011

Slightly pessimistic climate

GDP, growth in % -2.9 0.2 0.5

Interest rate, % 3.5 4.0 4.5Interest rate, % 3.5 4.0 4.5

Property prices, growth in % -10.5 -5.0 0.0

Unemployment, % 3.8 5.4 5.5

Economic experts

GDP, growth in % -2.9 0.1 1.1

Interest rate, % 3.5 4.0 4.4

Property prices, growth in % -10.2 -8.9 0.1Property prices, growth in % -10.2 -8.9 0.1

Unemployment, % 3.4 4.9 5.7

28-10-2009 12

Business Capital (Pillar I+II)

Nykredit Realkredit Group

30 June 2009

DKKbnTotal

Pillar I

Nykredit Realkredit Group

Pillar I

- Credit risk 19.7

- Market risk 4.6

- Operational risk 1.0

- Insurance risk 0.6

- Risk relating to own properties 0.1

Pillar I total 26.1

Pillar IIPillar II

- Slightly pessimistic economic climate 3.8

- Other 0.8

- General 10% charge (uncertainty) 3.1- General 10% charge (uncertainty) 3.1

Pillar II total 7.7

Business capital (Pillars I + II) 33.8

28-10-2009 13

Assumptions behind severe recession (Pillar IV)

2009 2010 2011

Interest rate, % 3.0 3.5 4.0

Real GDP growth, % -2.9 -1.0 -0.5

Property prices, growth in % -15.0 -15.0 -10.0

Share prices, growth in % -10.0 -10.0 -5.0

Unemployment, % 6.6 8.0 7.5Unemployment, % 6.6 8.0 7.5

28-10-2009 14

Cyclical buffer (Pillar IV)

As at 30 June 2009

DKKbnTotal

Charge for severe recession – operating results 1.1

Nykredit Realkredit Group

Charge for severe recession – operating results 1.1

Charge for severe recession – credit risk 6.8

Charge for severe recession – market risk -0.2

Other risks and charges 2.5Other risks and charges 2.5

General 10% charge (uncertainty) 0.9

Cyclical buffer (Pillar IV) total 11.1

• Same calculation technique as Pillar II, cf previous

•Without inclusion of operating profit

• Given current balance of lending

28-10-2009 15

Nykredit Group Capital Policy

• Nykredit is not listed on the stock exchange

• Nykredit wants to remain an aktive lendor –also during crisis periods

• Nykredit wants to reservere capital to be able to withstand a hard recession (Pillar IV)

• Therefore Nykredit has a rather large capital base supported by the financial sustainability strategy

Equity

EUR 7.0bn

Hybrid

Tier 1

EUR 0.5bnRequired capital base

Business capital

Pillar I

EUR 3.5bn

Pillar II

EUR 1.0bn

Cyclical buffer "Pillar IV"

Equity

Strategic capital

EUR 0.3bn

Statutory capital

deductions

EUR 0.7bn Tier 1*

Strategic capitalEUR 0.5bn

EUR 0.5bnRequired capital base

*The loan of EUR 0.5bn may be prepaid at par (100) in September 2014.

EUR 3.5bn

EUR 4.5bn

EUR 1.0bn "Pillar IV"

EUR 1.5bn

Equity

Strategic capital

EUR 0.3bn

Statutory capital

deductions

EUR 0.7bn

EUR 0.5bn

28-10-2009 16

Nykredit Realkredit Group, development in own funds

50

60DKKbn

40

50

Strategic capital

Statutory capital

deduction

20

30

deduction

Cyclical buffer

Business capital

10

20

0

2001 2002 2003 2004 2005 2006 2007 2008 2009as at 30 June

1 2

1: Acquisition of Totalkredit 2: Acquisition of Forstædernes Bank

28-10-2009 17

Regulatory risks – larger capital requirements

Leverage ratio• Simple measure of gearing originating from the US

• Part of the G20 package on new financial regulations

• Basel proposal at end-2009/EU proposal in 2010

Extension of Basel I floor requirements

• Basel proposal at end-2009/EU proposal in 2010

• IRB institutions must meet 80% of the Basel I capital requirement

• Transitional rule until end-2009 likely to be extended to end-2011

• Approved by Council of Ministers – Parliament approval expected

General increase of capitalrequirement

• 8% requirement is tightened

•Measured relative to core capital or increased to eg 10%

• In preparation: Basel proposal at end-2009/EU proposal in 2010

Capital buffer in addition to capital need

Dynamic impairment

• 2% of capital need or determined by stressed PDs

• Part of G20 package on new financial regulations

• In preparation: Basel proposal at end-2009/EU proposal in 2010

• New counter-cyclical impairment against profit/loss and equityDynamic impairment

Liquidity ratio

• New counter-cyclical impairment against profit/loss and equity

• EU Directive proposal likely to be postponed from Oct '09 to '10

• Ultra liquid assets relative to funding need in 30 days

In preparation: Basel proposal at end-2009/EU proposal in 2010Liquidity ratio

• In preparation: Basel proposal at end-2009/EU proposal in 2010

28-10-2009 18

Need for capital buffers rather than capital requirementsrequirements

Capital CapitalCapitalrequirement

Capitalrequirement

Basel I

• Fixed requirement

No model uncertainty

Basel II

• Risk indicators in term of numbers

• Model uncertainty

Time Time

• No model uncertainty

• No risk indicators

• Model uncertainty

• Need for capital buffer

• Risky to aim 100% on capital

contributioncontribution

28-10-2009 19

Procyclical impairment provisions and capital buffers

Source: Danmarks Nationalbank, Source: Danmarks Nationalbank,

Financial stability, H1 2009

28-10-2009 20

Basel II – The result depends on the assumptions (1)

• Data: PD data from 1991 – todayLGD data from 1991-2003

- Or only favourable data from a favourable period

Correlations and diversification

- Within credit risk (portfolio model)Credit – Insurance – Market Risk

Confidence levels 99.9% - 99.97%

Value-at-Risk for whole year3-4 multiplication3-4 multiplication

28-10-2009 21

Basel II – The result depends on the assumptions (2)

• Pillar II: How severe a stress test?Reduction for future profits?Reduction for capital planning?Reduction for capital planning?

• Conclusion: What does your bank try to achieve?- A low capital adequacy ratio?- A realistic capital adequacy ratio?- A realistic capital adequacy ratio?- A safe capital adequacy ratio?- A wise capital adequacy ratio?

Basel II should never have been implemented withoutguidelines for the calculations.

• A rubber band regulation?

28/10/2009 22

Top Related