Languages

Pages

Legal

TPCC

Taiwan Prosperity Chemical Corporation

4Q/2013

Investors’ Conference

April 2, 2014

TPCC

Disclaimer

The forward-looking statements contained in this presentation are

subject to risks and uncertainties and actual results may differ

materially from those expressed or implied in these forward-looking

statements.

Taiwan Prosperity Chemical Corporation makes no representation or

warranty as to the accuracy or completeness of these forward-looking

statements and nor does Taiwan Prosperity Chemical Corporation

undertake any obligation to update any forward-looking statements,

whether as a result of new information or future events.

TPCC

Agenda

• Company Snapshot

• 4Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• Year 2014 Business Outlook

3

TPCC 4

Taiwan Prosperity Chemical Corp.

Established: May, 1991

Headquarter: Taipei, Taiwan

IPO in Taiwan: October, 2007

Paid in Capital: NT$ 2,920 million

Market Cap:

(as of 03/25/2014 , NTD 30.85 per share) NTD 9,008 million

(USD/NTD=30.525) ( USD 295 million )

Production facility: Lin Yuan, Kaohsiung, Taiwan

Employees: 217

(as of 12/31/2013)

TPCC

Production Facility

Kaohsiung

(TPCC)

Beijing

Shanghai

1.Cumene

(460 KTA)

2.Phenol/Acetone

(360 KTA/221 KTA)

3.Bisphenol-A

(107 KTA)

4.Anone

(150 KTA)

5.MAN

(40 KTA)

6.H2-I

(7K Nm3/hr)

H2-II

(8.1K Nm3/hr)

TPCC

Agenda

6

• Company Snapshot

• 4Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• Year 2013 Business Outlook

TPCC 7

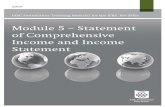

4Q/2013 Statement of Comprehensive Income

(In NT millions except otherwise noted) 4Q / 13 3Q / 13 4Q / 12 QoQ / % YoY / %

Net Sales 5,759 5,588 6,235 3 (8)

COGS 5,917 5,737 6,215 3 (5)

Gross Profit (158) (149) 20 6 (890)

Gross Margin (2.7%) (2.7%) 0.3% 0 (3)

Operating Expense 132 124 150 6 (12)

Operating Income (290) (273) (130) 6 (123)

Operating Margin (5.0%) (4.9%) (2.1%) (0.1) (2.9)

Non-operating Income/(Expense) (25) 3 (11) (986) 125

Income before Tax (315) (270) (141) 17 123

Income Tax Benefit/(Expense) 53 37 22 43 141

Net Income (262) (233) (119) 12 120

Net Margin (4.5%) (4.2%) (1.9%) (0.3) (2.6)

TPCC

4Q/2013 Statement of Comprehensive Income

(In NT millions except otherwise noted) 4Q/13 3Q/13 4Q/12 QoQ / % YoY / %

Net Income (262) (233) (119) (12) (120)

Other Comprehensive Income(Loss) 57 92 16 (38) 256

Total Comprehensive Income(Loss) (205) (141) (103) (45) (99)

Basic EPS (NT$) (0.90) (0.80) (0.40) (13) (125)

ROE (%) (4.0%) (4.6%) 0.6% 0.6 (4.6)

ROA (%) (1.4%) (2.3%) 0.8% 0.9 (2.2)

Free Cash Flow(1) 228 957 492 (76) (54)

(1) Free Cash Flow = Operating Cash Flow - CAPEX - L/T Investment

8

TPCC

Year 2013 Statement of Comprehensive Income (In NT millions except otherwise noted) 2013 2012 YoY / %

Net Sales 22,579 25,426 (11)

COGS 22,786 24,928 (9)

Gross Profit (207) 498 (142)

Gross Margin (0.9%) 2.0% (3)

Operating Expense 512 622 (18)

Operating Income (719) (124) 480

Operating Margin (3.2%) (0.5%) (2.7)

Non-operating Income/(Expense) (48) 4 (1,300)

Income before Tax (767) (120) 539

Income Tax Benefit/(Expense) 114 22 418

Net Income (653) (98) 566

Net Margin (2.9%) (0.4%) (2.5)

9

TPCC

Year 2013 Statement of Comprehensive Income

10

(In NT millions except otherwise noted) 2013 2012 YoY / %

Net Income (653) (98) 566

Other Comprehensive Income(Loss) 239 107 123

Total Comprehensive Income(Loss) (414) 10 (4,240)

Basic EPS (NT$) (2.24) (0.33) 579

ROE (%) (9.9%) (1.3%) (8.6)

ROA (%) (4.3%) (0.3%) (4.0)

Total Assets 15,078 12,443 21

Total Liabilities 8,763 5,597 57

Total Shareholders' Equity 6,315 6,846 (8)

Free Cash Flow(1) 244 2,139 (89)

(1) Free Cash Flow = Operating Cash Flow - CAPEX - L/T Investment

TPCC

Sales/ GM & PAT

3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Sales 7,416 5,474 6,238 6,464 6,489 6,235 5,310 5,922 5,588 5,759

PAT 446 -65 194 -51 -124 -118 -53 -105 -233 -262

GM 9.4% 1.4% 6.0% 1.5% 0.1% 0.3% 1.1% 0.7% -2.7% -2.7%

-5%

0%

5%

10%

15%

20%

25%

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000 NT$,M GM

11

TPCC

4Q/2013 Statement of Cash Flow

(In NT millions except otherwise noted) 4Q / 13 3Q / 13 4Q / 12

Cash Flows From Operating Activities

Income before Tax (315) (270) (140)

Adjustments to reconcile income

to net cash provided by operating activities637 1,244 748

Net cash generated from operating activities 321 974 608

Cash Flows From Investing Activities (140) 4 (100)

Cash Flows From Financing Activities (504) (79) (675)

Net Increase In Cash And Cash Equivalents (323) 899 (167)

Cash And Cash Equivalents, Begining Of Period 1,171 272 608

Cash And Cash Equivalents, End Of Period 848 1,171 441

12

TPCC

Year 2013 Statement of Cash Flow

(In NT millions except otherwise noted) 2013 2012

Cash Flows From Operating Activities

Income before Tax (768) (119)

Adjustments to reconcile income

to net cash provided by operating activities1,284 2,551

Net cash generated from operating activities 516 2,432

Cash Flows From Investing Activities (281) (265)

Cash Flows From Financing Activities 172 (2,442)

Net Increase In Cash And Cash Equivalents 407 (275)

Cash And Cash Equivalents, Begining Of Period 441 716

Cash And Cash Equivalents, End Of Period 848 441

13

TPCC

Solid Financial Structure

14

28 26 24

19 27

33

0

5

10

15

20

25

30

35

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

2.26

1.02

1.72 1.99

2.08

1.28

0.00

0.50

1.00

1.50

2.00

2.50

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

34% 43%

51% 45%

38%

52%

0%

10%

20%

30%

40%

50%

60%

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

24.8

17.1 19.5

31.1 29.8

24.1

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2007Y 2008Y 2009Y 2010Y 2011Y 1H/12

Current Ratio

Debt Ratio (L/A)

Book Value per share

1.72

1.99

2.08

1.07

1.25

0

1

2

3

2009 2010 2011 2012 2013

51% 45%

38%

45%

58%

0%

20%

40%

60%

80%

2009 2010 2011 2012 2013

19.5

31.1

29.8 23.5

21.6 10

20

30

40

2009 2010 2011 2012 2013

58.5%

-1.2%

2.5%

30.6% 30.7%

36.1%

29.6% 26.3%

25.5%

18.7%

-20%

0%

20%

40%

60%

80%

2009 2010 2011 2012 2013

Net Debt/ Equity Debt/ Asset

Leverage Ratios

(%)

TPCC

Agenda

• Company Snapshot

• 4Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• Year 2014 Business Outlook

15

TPCC

Source :TPCC

16

TPCC

Source :TPCC

17

TPCC

Worldwide Phenol Capacity & Demand Outlook

Source :TPCC

Unit:KT/YR 2012 2013 2014 2015

Phenol Capacity 10,828 11,496 12,101 12,914

Bisphenol A 4,142 4,076 4,269 4,471

Phenolic Resins 2,698 2,739 2,832 2,966

Anone 958 996 1,029 1,117

Others 1,154 1,088 1,122 1,140

Phenol Demand 8,952 8,899 9,252 9,694

Capacity - Demand 1,876 2,597 2,849 3,220

Utilization Rate, % 83% 77% 76% 75%

18

TPCC

China Phenol Capacity & Demand

Source: TPCC

Capacity Annual Growth Rate: 23.3% Demand Annual Growth Rate: 6.55%

19

TPCC

TPCC Sales Volume in Recent 5 Years (Unit : MT)

ps: Year 2013 decreased the production of BPA about 60KT.

Volume 486,148 587,477 601,101 624,090 527,039

20

TPCC

Sales Destination of 2013 vs 2012

2012 48% 14% 15% 10% 6% 4% 1% 2%

2013 54% 18% 8% 8% 4% 4% 2% 2%

21

TPCC

TPCC Business Migration

Cumene Plant Phenol/Acetone /AMS Plant

Anone Plant

BPA Plant

Propylene

Benzene

cumene

Phenol

Acetone

Anone

BPA

Acetone

Phenol

Cumene

AMS AMS

H2

Started With 4 Sites And 6 Products

22

TPCC

TPCC Business Migration

Cumene Plant Phenol/Acetone /AMS Plant

Anone Plant

BPA Plant

Propylene

Benzene

cumene

Phenol

Acetone

Anone

BPA

Acetone

Phenol

Cumene

AMS AMS

H2 Plant

H2 Plant

No 1 Steam/MAn Plant

No 2 Steam/MAn Plant

BDO Plant THF Plant

LNG

BDO

THF

GBL

MAn

LNG

nC4

nC4

Migrate to 10 Sites And 10 Products

Possessed Capacity Leased Capacity – To Be Completed By Q4 2013

23

TPCC

BDO PLANT

24

TPCC

TPCC BDO Derivatives Development Plant

C4 SPLITER

MAN PLANT

BDO PLANT

PTMEG PLANT

NMP PLANT

NHEP PLANT

POLYOL PLANT

PBT PLANT

C4

n-C4

Crude Man

GBL THF

BDO

NVP PLANT

PVP PLANT

PVP

NHEP

NVP

NMP

SPANDEX PLANT

TPU COPOLYESTER

SPANDEX FIBER

PU PLANT

PU Paint

PU Foam

PU Adhesive

PU Leather

PBT COMPOUNDING PLANT

ENGINEERING PLASTICS

The High Value-added Petrochemical

25

TPCC

MAn Series Production Capacity

2013* 2012 20XX*

80 KTA 40 KTA

BDO eq. Expansion

68 KTA 34 KTA

MAn Expansion

*: TPCC estimation

26

TPCC

Agenda

• Company Snapshot

• 4Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• Year 2014 Business Outlook

27

TPCC

Capital Expenditures NT$ M

3,065

539 539

586

30 49

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014E

28

TPCC

Agenda

• Company Snapshot

• 4Q/2013 Financial Results

• Business Overview

• Capital Expenditure

• Year 2014 Business Outlook

29

TPCC

FY/2014 Business Outlook-1

• Benzene

1. Supply from Asia will increase 2 million tons in 2nd half 2014 due to new capacity put in service.

2. Compared to year 2013, benzene price in 2014 shall be stable low.

• Propylene

1. The supply have been improved nowadays, due to CPC new cracker(No.6) and FRCC from CPC on stream from Q4/2013.

2. TPCC will reduce import quantity of propylene in 2014 compared to last year.

30

TPCC

FY/2014 Business Outlook-2

• Phenol Chain Market – U.S. and Europe economics recover, and China remained stable.Demand will be picked up gradually in 2014 compared to last year. There will be three new plants to be on stream in Q4 2014 in Asia, one existing plant will be permanent shutdown in Q3 2014, the impact for 2014 will not be so much, capacity utilization will maintain around the same level as 2013.

• Corporate strategy – To cope with threats in raw material and market trends, heavy attention will be paid to achievement of best possible margin rather than highest production. Reduce operation cost by flexible operation lines.

• Business strategy – Our strategy is to increase our sales to different countries/areas to reduce the dependence on China market. Utilized equipment leasing strategies to maintain revenue growth and acquired major new series of products (BDO/THF/GBL).

31

TPCC

Thank You

32

Top Related