Languages

Pages

Legal

22 May 2020 Results Review 4QFY20

BSE

Fighting back,cash support BSE reported inline revenue but margin performance was below estimate in

4QYF20. There was improvement in core revenue stream (transaction charges

+19.5% QoQ), but EBIT margin is still in negative territory. BSE cash market

share has declined to 6.8% in FY20 vs. 8.9% in FY19. The StAR MF platform is

witnessing strong volume growth (+60% YoY in FY20), but drop in realisation

(Rs 6.5/transaction vs. Rs 8.5) will impact growth. We have cut FY21/22E EPS

est. by 5.3/4.7%. We arrive at a SoTP based TP of Rs 480 by assigning 10x

multiple to core FY22E PAT (Rs 16/sh), Rs 67/sh for the CDSL stake and

adding net cash excluding SGF and clearing corporation liabilities (Rs 397/sh).

Maintain ADD.

Revenue was up 8.8% QoQ to Rs 1.20bn (vs. est. of Rs 1.19) led by 19.5%

growth in transaction revenue offset by 1.0% drop in annual listing fees.

StAR MF revenue stood at Rs 0.12bn (-1.7% QoQ) led by higher volumes

(+27% YoY) offset by lower realization (-23% QoQ). StAR MF was the only

initiative of BSE which was witnessing solid growth, but drop in realization

and Covid-19 will impact growth for FY21E.

BSE has managed to improve its cash market share by 53bps QoQ, but still

down 188bps YoY to 6.9%. Currency derivative market share has declined

sharply to 31.1% (-1,101bps YoY). INX is currently in investment mode

(burning ~Rs 0.23bn annually). INX ADTV stood at USD 2.6bn (+48% YoY)

and no of daily trades was 67K (+175% YoY). Hopefully, INX will start

contributing to revenue from FY22E.

Adjusted EBITDA margin improved to 3.8% vs. -1.0% in 3Q, but was below

our est. of 5.1%. For FY20, EBITDA margin was down 467bps to 1.8% due to

flat revenue and 5% increase in total cost (adjusted for one-off). OCF stood

at Rs 3.97bn vs. negative in FY19.

Valuation and view. BSE cash market share has slipped to 6.8% in FY20

witnessing third consecutive year of decline. Interoperability has offered

some respite in 4Q, but the progress is slow. BSE is trying to fight back and

build the derivative volume through LES, but it’s still early days. New

initiatives like Insurance platform, currency trading in INX sounds

promising but there is no revenue visibility in the near term and is

impacting margins. We expect revenue growth of 6.4/12.2% in FY21/22E led

by rebound in transaction revenue and increase in listing fees. We expect

operating leverage with growth (EBITDA margin of 5.3/12.8% for FY21/22E).

BSE has net cash of Rs 18bn (~91% of MCap) and a dividend yield of ~4%,

which limits downside.

Financial Summary

YE Mar (Rs mn) 4Q

FY20

4Q

FY19

YoY

(%)

3Q

FY20

QoQ

(%) FY18 FY19 FY20 FY21E FY22E

Net Revenues 1,196 1,157 3.3 1,099 8.8 5,072 4,503 4,505 4,793 5,380

EBITDA 46 24 NM -11 NM 1,302 291 81 256 687

APAT 254 557 (54.4) 288 (11.9) 2,399 2,077 1,410 1,627 2,010

Diluted EPS (Rs) 5.6 10.8 (47.5) 6.4 (11.9) 45.1 40.1 31.3 36.2 44.7

P/E (x) 9.6 10.8 13.9 12.0 9.7

EV / EBITDA (x)

-2.3 -6.2 20.7 5.6 1.7

RoE (%) 7.8 7.1 5.8 6.7 8.2

Source: Company, HSIE Research

ADD

CMP (as on 21 May 2020) Rs 434

Target Price Rs 480

NIFTY 9,106

KEY

CHANGES OLD NEW

Rating ADD ADD

Price Target Rs 410 Rs 480

EPS % FY21E FY22E

-5.3% -4.7%

KEY STOCK DATA

Bloomberg code BSE IN

No. of Shares (mn) 45

MCap (Rs bn) / ($ mn) 20/258

6m avg traded value (Rs mn) 71

52 Week high / low Rs 627/275

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) (15.9) (13.9) (28.0)

Relative (%) 9.0 9.9 (7.4)

SHAREHOLDING PATTERN (%)

Dec-19 Mar-20

Promoters 0.00 0.00

FIs & Local MFs 2.53 2.38

FPIs 17.79 16.25

Public & Others 79.68 81.37

Pledged Shares 0.00 0.00

Source : BSE

Amit Chandra [email protected] +91-22-6171-7345

Vinesh Vala [email protected] +91-22-6171-7332

Page | 2

BSE: Results Review 4QFY20

Quarterly consolidated Financial Snapshot

Particulars (Rs mn) 4QFY20 4QFY19 YoY (%) 3QFY20 QoQ (%)

Total Revenue 1,196 1,157 3.3 1,099 8.8

Employee Cost 376 355 5.8 369 1.8

Technology Expenses 294 277 6.1 294 0.1

Other Operating Expenses 480 500 -4.0 448 7.2

EBITDA 46 24 88.4 -11 NM

Depreciation 134 147 -8.9 132 1.6

EBIT -88 -123 NM -143 -38.3

Interest Cost 10 2 442.1 5 119.1

Other Income (including E/O) 95 600 -84.1 555 -82.8

PBT -3 475 NM 407 NM

Tax 82 44 85.1 15 456.5

Share of Profit Loss from JV &

Associates 66 87 -24.4 57 15.6

Minority Interest -6 0 NM -6 -6.3

RPAT -13 519 NM 456 NM

E/o gains (adj for tax) 267 39 NM -167 NM

APAT 254 557 -54.4 288 -11.9

Source: Company, HSIE Research

Margin Analysis

Particulars (% of Revenue) 4QFY20 4QFY19 YoY (bps) 3QFY20 QoQ (bps)

Employee Cost % 31.4 30.7 73 33.6 -214

Technology Expenses % 24.6 24.0 63 26.7 -213

Other Operating Exp % 40.2 43.3 -308 40.8 -58

EBITDA Margin (%) 3.8 2.1 172 -1.0 485

EBIT Margin (%) -7.4 -10.6 323 -13.0 564

Tax Rate (%) NM 9.3 NM 3.6 NM

APAT Margin (%) 21.2 48.2 -2694 26.2 -499

Source: Company, HSIE Research

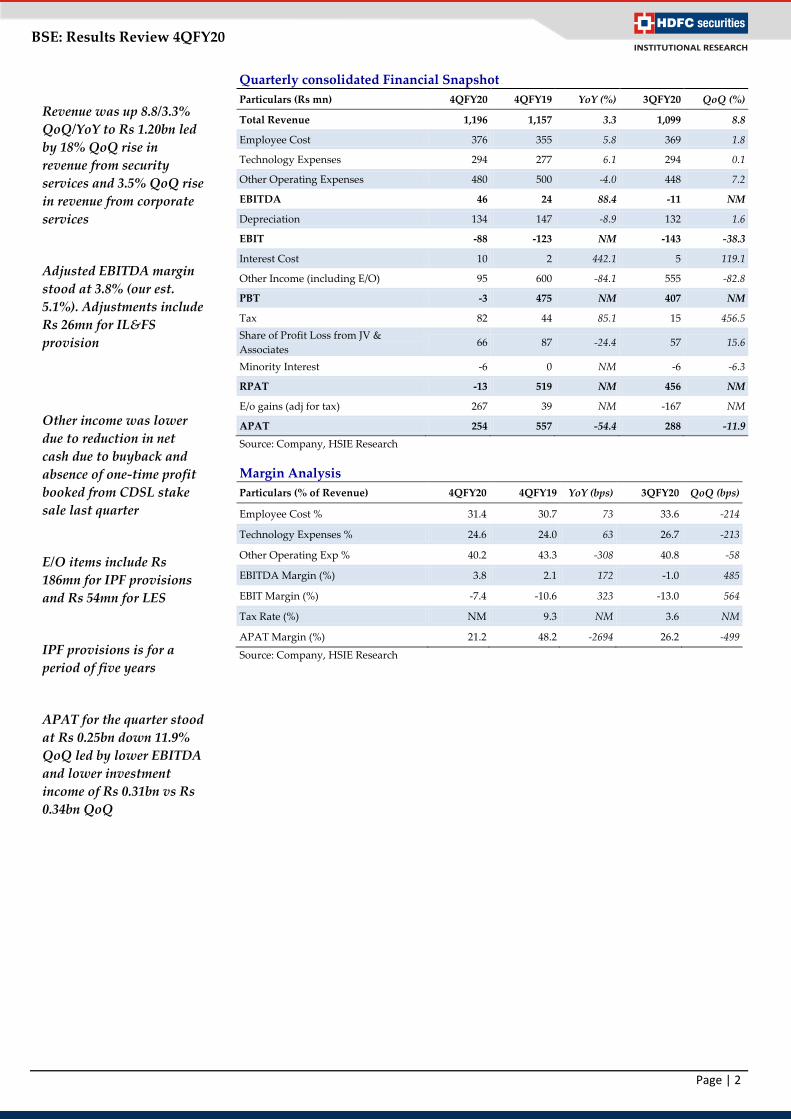

Revenue was up 8.8/3.3%

QoQ/YoY to Rs 1.20bn led

by 18% QoQ rise in

revenue from security

services and 3.5% QoQ rise

in revenue from corporate

services

Adjusted EBITDA margin

stood at 3.8% (our est.

5.1%). Adjustments include

Rs 26mn for IL&FS

provision

Other income was lower

due to reduction in net

cash due to buyback and

absence of one-time profit

booked from CDSL stake

sale last quarter

E/O items include Rs

186mn for IPF provisions

and Rs 54mn for LES

IPF provisions is for a

period of five years

APAT for the quarter stood

at Rs 0.25bn down 11.9%

QoQ led by lower EBITDA

and lower investment

income of Rs 0.31bn vs Rs

0.34bn QoQ

Page | 3

BSE: Results Review 4QFY20

Segmental Revenue Analysis

Rs mn 4QFY20 4QFY19 YoY

(%) 3QFY20 QoQ (%) FY20 FY19

YoY

(%)

Transaction Charges 313 287 9.1 262 19.5 1,193 1,139 4.7

Treasury Income 43 72 -40.4 42 2.1 215 307 -30.0

Other Income 101 98 3.0 83 21.6 296 269 10.0

Total Security

Services (A) 457 457 0.0 387 18.0 1,704 1,715 -0.7

Annual listing 493 443 11.3 498 -1.0 1,880 1,881 -0.1

Book building 60 48 24.0 31 95.1 182 149 22.1

Other Services 13 42 -69.0 18 -27.8 58 102 -43.1

Total Services to

corporate (B) 566 533 6.1 547 3.5 2,120 2,132 -0.6

Data Feed/others (C) 173 167 3.7 166 4.6 681 656 3.9

Total Revenue (A+B+C) 1,196 1,157 3.3 1,099 8.8 4,505 4,503 0.0

Source: Company, HSIE Research

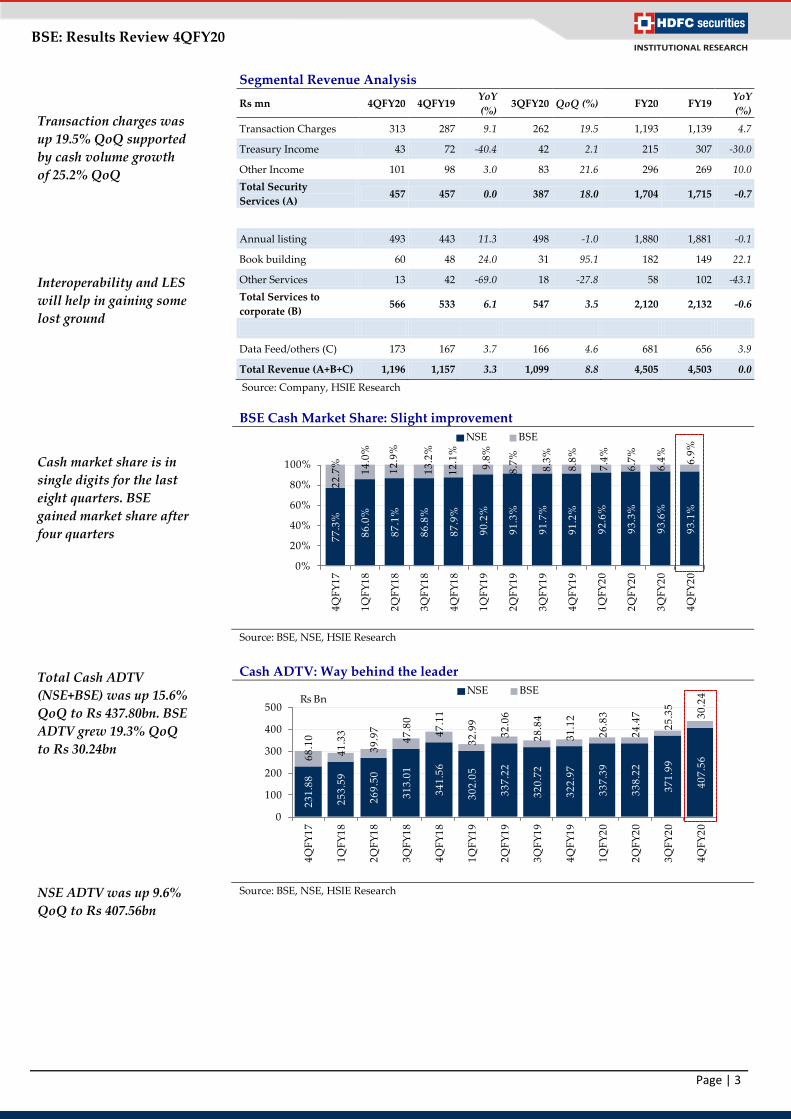

BSE Cash Market Share: Slight improvement

Source: BSE, NSE, HSIE Research

Cash ADTV: Way behind the leader

Source: BSE, NSE, HSIE Research

Transaction charges was

up 19.5% QoQ supported

by cash volume growth

of 25.2% QoQ

Interoperability and LES

will help in gaining some

lost ground

Cash market share is in

single digits for the last

eight quarters. BSE

gained market share after

four quarters

Total Cash ADTV

(NSE+BSE) was up 15.6%

QoQ to Rs 437.80bn. BSE

ADTV grew 19.3% QoQ

to Rs 30.24bn

NSE ADTV was up 9.6%

QoQ to Rs 407.56bn

77

.3%

86

.0%

87

.1%

86

.8%

87

.9%

90

.2%

91

.3%

91

.7%

91

.2%

92

.6%

93

.3%

93

.6%

93

.1%

22

.7%

14

.0%

12

.9%

13

.2%

12

.1%

9.8

%

8.7

%

8.3

%

8.8

%

7.4

%

6.7

%

6.4

%

6.9

%

0%

20%

40%

60%

80%

100%

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

NSE BSE

23

1.8

8

25

3.5

9

26

9.5

0

31

3.0

1

34

1.5

6

30

2.0

5

33

7.2

2

32

0.7

2

32

2.9

7

33

7.3

9

33

8.2

2

37

1.9

9

40

7.5

668

.10

41

.33

39

.97

47

.80

47

.11

32

.99

32

.06

28

.84

31

.12

26

.83

24

.47

25

.35

30

.24

0

100

200

300

400

500

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

NSE BSERs Bn

Page | 4

BSE: Results Review 4QFY20

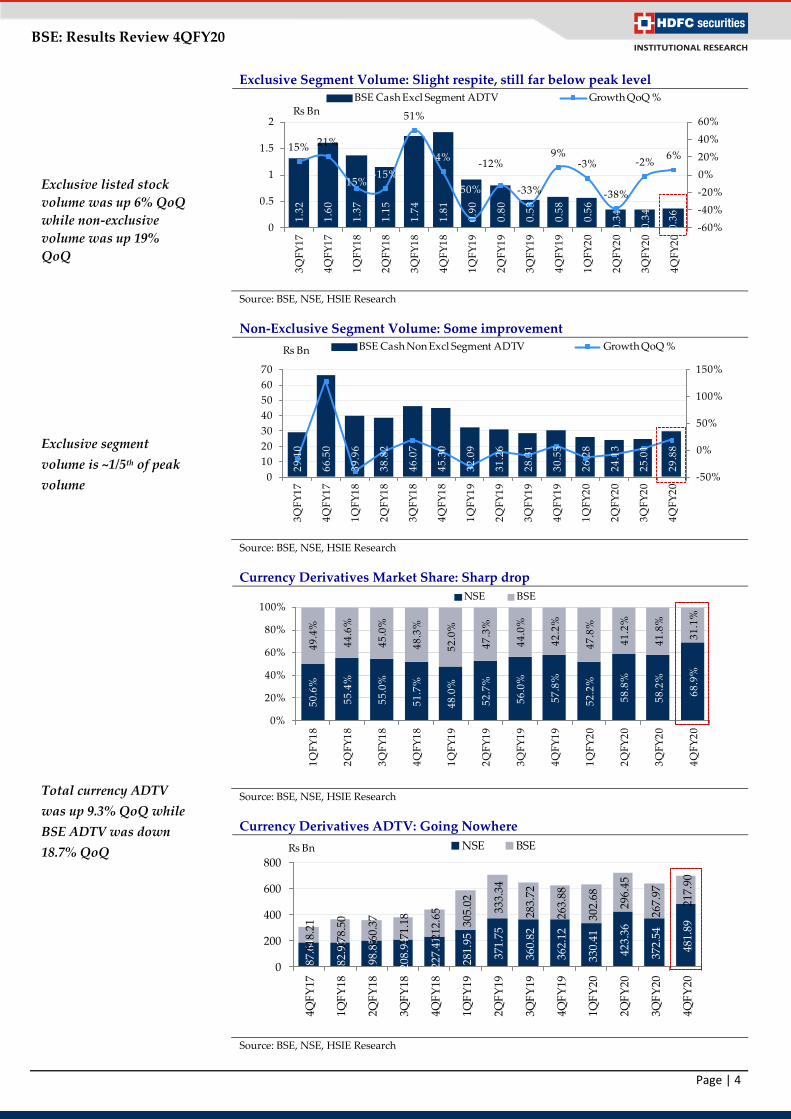

Exclusive Segment Volume: Slight respite, still far below peak level

Source: BSE, NSE, HSIE Research

Non-Exclusive Segment Volume: Some improvement

Source: BSE, NSE, HSIE Research

Currency Derivatives Market Share: Sharp drop

Source: BSE, NSE, HSIE Research

Currency Derivatives ADTV: Going Nowhere

Source: BSE, NSE, HSIE Research

Exclusive listed stock

volume was up 6% QoQ

while non-exclusive

volume was up 19%

QoQ

Exclusive segment

volume is ~1/5th of peak

volume

Total currency ADTV

was up 9.3% QoQ while

BSE ADTV was down

18.7% QoQ

1.3

2

1.6

0

1.3

7

1.1

5

1.7

4

1.8

1

0.9

0

0.8

0

0.5

3

0.5

8

0.5

6

0.3

4

0.3

4

0.3

6

15% 21%

-15%-15%

51%

4%

-50%

-12%

-33%

9%-3%

-38%

-2%6%

-60%

-40%

-20%

0%

20%

40%

60%

0

0.5

1

1.5

2

3Q

FY

17

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

BSE Cash Excl Segment ADTV Growth QoQ %

Rs Bn

29

.10

66

.50

39

.96

38

.82

46

.07

45

.30

32

.09

31

.26

28

.31

30

.55

26

.28

24

.13

25

.01

29

.88

-50%

0%

50%

100%

150%

0

10

20

30

40

50

60

70

3Q

FY

17

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

BSE Cash Non Excl Segment ADTV Growth QoQ %Rs Bn

50

.6%

55

.4%

55

.0%

51

.7%

48

.0%

52

.7%

56

.0%

57

.8%

52

.2%

58

.8%

58

.2%

68

.9%

49

.4%

44

.6%

45

.0%

48

.3%

52

.0%

47

.3%

44

.0%

42

.2%

47

.8%

41

.2%

41

.8%

31

.1%

0%

20%

40%

60%

80%

100%

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

NSE BSE

187.

64

182.

93

198.

85

208.

94

227.

41

281.

95

371.

75

360.

82

362.

12

330.

41

423.

36

372.

54

481.

89

118.

21

178.

50

160.

37

171.

18

212.

65

305.

02

333.

34

283.

72

263.

88

302.

68

296.

45

267.

97

217.

90

0

200

400

600

800

4QF

Y17

1QF

Y18

2QF

Y18

3QF

Y18

4QF

Y18

1QF

Y19

2QF

Y19

3QF

Y19

4QF

Y19

1QF

Y20

2QF

Y20

3QF

Y20

4QF

Y20

NSE BSERs Bn

Page | 5

BSE: Results Review 4QFY20

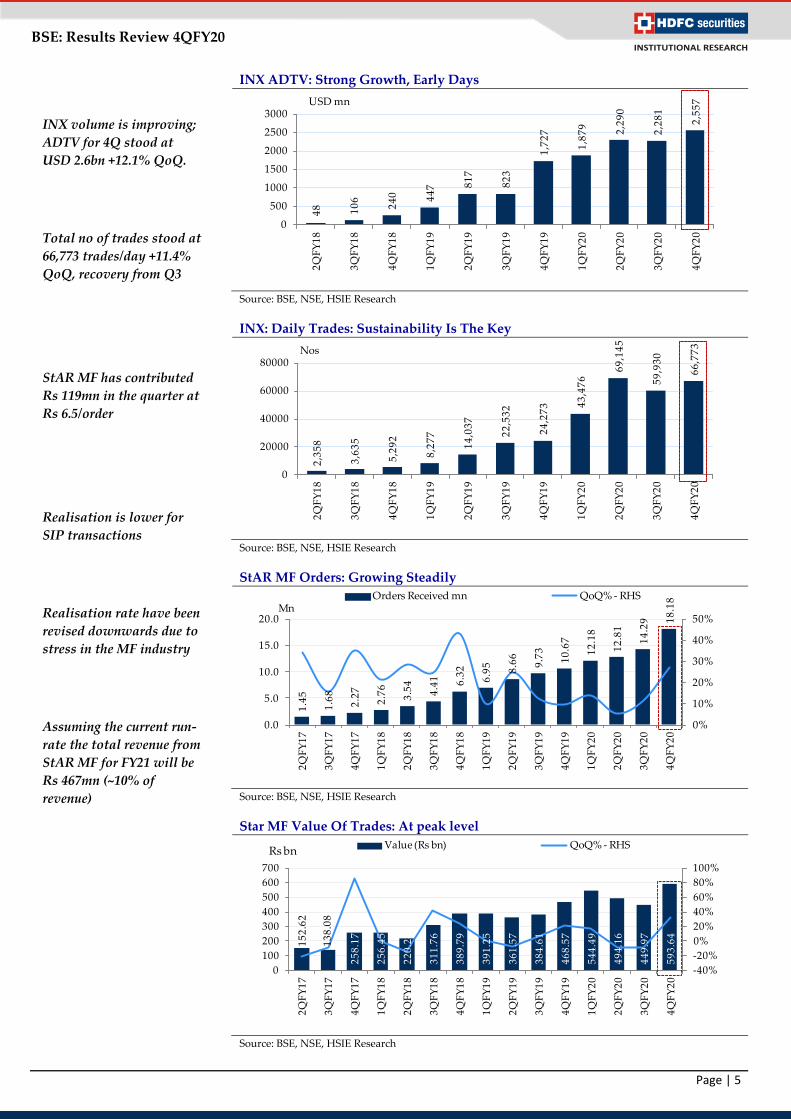

INX ADTV: Strong Growth, Early Days

Source: BSE, NSE, HSIE Research

INX: Daily Trades: Sustainability Is The Key

Source: BSE, NSE, HSIE Research

StAR MF Orders: Growing Steadily

Source: BSE, NSE, HSIE Research

Star MF Value Of Trades: At peak level

Source: BSE, NSE, HSIE Research

INX volume is improving;

ADTV for 4Q stood at

USD 2.6bn +12.1% QoQ.

Total no of trades stood at

66,773 trades/day +11.4%

QoQ, recovery from Q3

StAR MF has contributed

Rs 119mn in the quarter at

Rs 6.5/order

Realisation is lower for

SIP transactions

Realisation rate have been

revised downwards due to

stress in the MF industry

Assuming the current run-

rate the total revenue from

StAR MF for FY21 will be

Rs 467mn (~10% of

revenue)

48 10

6

24

0 44

7 81

7

82

3

1,7

27

1,8

79 2,2

90

2,2

81

2,5

57

0

500

1000

1500

2000

2500

3000

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

USD mn

2,3

58

3,6

35

5,2

92

8,2

77

14

,03

7

22

,53

2

24

,27

3 43

,47

6

69

,14

5

59

,93

0

66

,77

3

0

20000

40000

60000

80000

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

Nos

1.4

5

1.6

8

2.2

7

2.7

6

3.5

4

4.4

1 6.3

2

6.9

5

8.6

6

9.7

3

10

.67

12

.18

12

.81

14

.29 1

8.1

8

0%

10%

20%

30%

40%

50%

0.0

5.0

10.0

15.0

20.0

2Q

FY

17

3Q

FY

17

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

Orders Received mn QoQ% - RHSMn

15

2.6

2

13

8.0

8

25

8.1

7

25

6.4

5

22

0.2

4

31

1.7

6

38

9.7

9

39

1.2

5

36

1.5

7

38

4.6

1

46

8.5

7

54

4.4

9

49

4.1

6

44

9.9

7

59

3.6

4

-40%

-20%

0%

20%

40%

60%

80%

100%

0

100

200

300

400

500

600

700

2Q

FY

17

3Q

FY

17

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

Value (Rs bn) QoQ% - RHSRs bn

Page | 6

BSE: Results Review 4QFY20

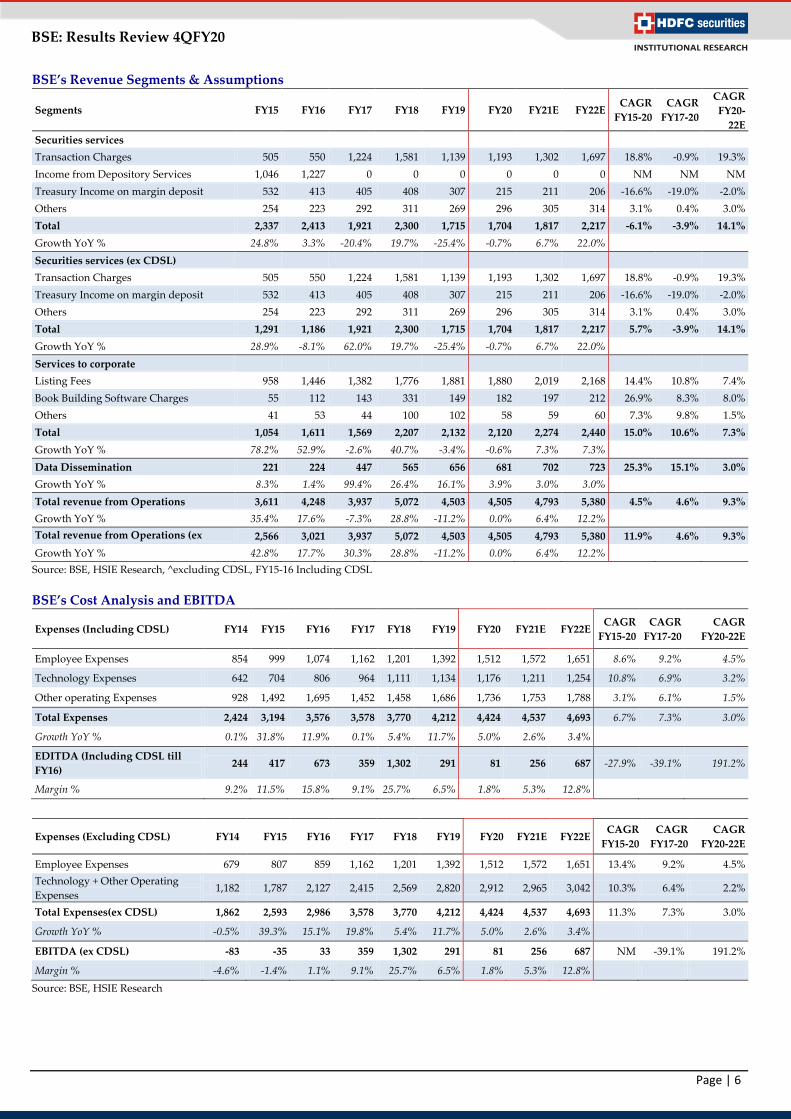

BSE’s Revenue Segments & Assumptions

Segments FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E CAGR

FY15-20

CAGR

FY17-20

CAGR

FY20-

22E

Securities services

Transaction Charges 505 550 1,224 1,581 1,139 1,193 1,302 1,697 18.8% -0.9% 19.3%

Income from Depository Services 1,046 1,227 0 0 0 0 0 0 NM NM NM

Treasury Income on margin deposit 532 413 405 408 307 215 211 206 -16.6% -19.0% -2.0%

Others 254 223 292 311 269 296 305 314 3.1% 0.4% 3.0%

Total 2,337 2,413 1,921 2,300 1,715 1,704 1,817 2,217 -6.1% -3.9% 14.1%

Growth YoY % 24.8% 3.3% -20.4% 19.7% -25.4% -0.7% 6.7% 22.0%

Securities services (ex CDSL)

Transaction Charges 505 550 1,224 1,581 1,139 1,193 1,302 1,697 18.8% -0.9% 19.3%

Treasury Income on margin deposit 532 413 405 408 307 215 211 206 -16.6% -19.0% -2.0%

Others 254 223 292 311 269 296 305 314 3.1% 0.4% 3.0%

Total 1,291 1,186 1,921 2,300 1,715 1,704 1,817 2,217 5.7% -3.9% 14.1%

Growth YoY % 28.9% -8.1% 62.0% 19.7% -25.4% -0.7% 6.7% 22.0%

Services to corporate

Listing Fees 958 1,446 1,382 1,776 1,881 1,880 2,019 2,168 14.4% 10.8% 7.4%

Book Building Software Charges 55 112 143 331 149 182 197 212 26.9% 8.3% 8.0%

Others 41 53 44 100 102 58 59 60 7.3% 9.8% 1.5%

Total 1,054 1,611 1,569 2,207 2,132 2,120 2,274 2,440 15.0% 10.6% 7.3%

Growth YoY % 78.2% 52.9% -2.6% 40.7% -3.4% -0.6% 7.3% 7.3%

Data Dissemination 221 224 447 565 656 681 702 723 25.3% 15.1% 3.0%

Growth YoY % 8.3% 1.4% 99.4% 26.4% 16.1% 3.9% 3.0% 3.0%

Total revenue from Operations 3,611 4,248 3,937 5,072 4,503 4,505 4,793 5,380 4.5% 4.6% 9.3%

Growth YoY % 35.4% 17.6% -7.3% 28.8% -11.2% 0.0% 6.4% 12.2%

Total revenue from Operations (ex

CDSL) 2,566 3,021 3,937 5,072 4,503 4,505 4,793 5,380 11.9% 4.6% 9.3%

Growth YoY % 42.8% 17.7% 30.3% 28.8% -11.2% 0.0% 6.4% 12.2%

Source: BSE, HSIE Research, ^excluding CDSL, FY15-16 Including CDSL

BSE’s Cost Analysis and EBITDA

Expenses (Including CDSL) FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E CAGR

FY15-20

CAGR

FY17-20

CAGR

FY20-22E

Employee Expenses 854 999 1,074 1,162 1,201 1,392 1,512 1,572 1,651 8.6% 9.2% 4.5%

Technology Expenses 642 704 806 964 1,111 1,134 1,176 1,211 1,254 10.8% 6.9% 3.2%

Other operating Expenses 928 1,492 1,695 1,452 1,458 1,686 1,736 1,753 1,788 3.1% 6.1% 1.5%

Total Expenses 2,424 3,194 3,576 3,578 3,770 4,212 4,424 4,537 4,693 6.7% 7.3% 3.0%

Growth YoY % 0.1% 31.8% 11.9% 0.1% 5.4% 11.7% 5.0% 2.6% 3.4%

EDITDA (Including CDSL till

FY16) 244 417 673 359 1,302 291 81 256 687 -27.9% -39.1% 191.2%

Margin % 9.2% 11.5% 15.8% 9.1% 25.7% 6.5% 1.8% 5.3% 12.8%

Expenses (Excluding CDSL) FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E CAGR

FY15-20

CAGR

FY17-20

CAGR

FY20-22E

Employee Expenses 679 807 859 1,162 1,201 1,392 1,512 1,572 1,651 13.4% 9.2% 4.5%

Technology + Other Operating

Expenses 1,182 1,787 2,127 2,415 2,569 2,820 2,912 2,965 3,042 10.3% 6.4% 2.2%

Total Expenses(ex CDSL) 1,862 2,593 2,986 3,578 3,770 4,212 4,424 4,537 4,693 11.3% 7.3% 3.0%

Growth YoY % -0.5% 39.3% 15.1% 19.8% 5.4% 11.7% 5.0% 2.6% 3.4%

EBITDA (ex CDSL) -83 -35 33 359 1,302 291 81 256 687 NM -39.1% 191.2%

Margin % -4.6% -1.4% 1.1% 9.1% 25.7% 6.5% 1.8% 5.3% 12.8%

Source: BSE, HSIE Research

Page | 7

BSE: Results Review 4QFY20

Valuation

We expect BSE’s revenue to increase at a CAGR of 9% over FY20-22E. The

EBITDA margin will expand from 1.8% in FY19 to 12.8% in FY23E due to revenue

growth and operating leverage.

RoE for the business is only 5.8%, owing to high cash levels on the books (Rs 18bn

ex-SGF and clearing and settlement cash).

BSE has been constantly innovating and investing in technology and is building

future platforms for growth. BSE has huge net cash of Rs 18bn (~Rs 397/sh, ~91%

of MCap) which is excluding SGF and the earmarked funds. The current dividend

yield of ~4% is attractive. BSE currently trades at 12.0/9.7x FY21/22E EPS (steep

discount to MCX valuations).

We have valued BSE on SOTP basis by assigning Rs 67/sh for CDSL taking 40%

holding discount. We have assigned 10x multiple to BSE’s core earnings and

adding back net-cash of Rs 17.87bn (excluding SGF and CCL funds). We maintain

ADD on BSE, with a TP of Rs 480 (11% upside from CMP), which includes the

core BSE value at Rs 16/sh, Net Cash of Rs 397/sh and CDSL stake value of Rs

67/sh.

BSE SOTP Valuation

Core PAT FY22 (Rs mn) 71

10X Core PAT (Rs mn) 706

Add: Net Cash ex SGF and CCL funds (Rs mn) 17,872

Mcap (Rs mn) 18,578

Price per Share (Rs) 413

CDSL Value/share (Rs) taking 40% holding discount 67

TP (Rs) 480

Upside (%) 11%

Source: Company, HSIE Research

CDSL Valuation

CDSL CMP (Rs) 242

CDSL Mcap (Rs mn) 25,237

Stake (%) 20%

Value of BSE Stake (Rs mn) 5,047

Taking 40% Discount (Rs mn) 3,028

Value/Share of CDSL (Rs) 67

Source: Company, HSIE Research

Change in Estimates

(Rs mn)

FY21E FY22E

Earlier New % Change Earlier New % Change

Revenue 4,830 4,793 -0.8 5,431 5,380 -0.9

EBITDA 316 256 -18.9 739 687 -7.0

EBITDA Margin (%) 6.5 5.3 -119bps 13.6% 12.8% -83bps

APAT 1,718 1,627 -5.3 2,109 2,010 -4.7

Source: HSIE Research

Peer Set Comparison

Company

M-Cap

(Rs

bn)

CMP

(Rs)

TP

(Rs) Rating

P/E (x) Dividend Yield (%) RoE (%)

FY19 FY20 FY21E FY22E FY19 FY20 FY21E FY22E FY19 FY20 FY21E FY22E

MCX 57 1,130 1,300 ADD 38.2 25.9 28.0 22.3 1.6 2.3 2.2 2.7 11.4 17.7 15.5 18.7

CDSL 25 242 325 BUY 22.2 20.1 20.9 17.9 1.7 1.9 1.8 2.1 17.0 17.3 15.3 16.2

BSE 20 434 480 ADD 10.8 13.9 12.0 9.7 8.1 3.9 6.2 7.7 7.1 5.8 6.7 8.2

Source: HSIE Research

Page | 8

BSE: Results Review 4QFY20

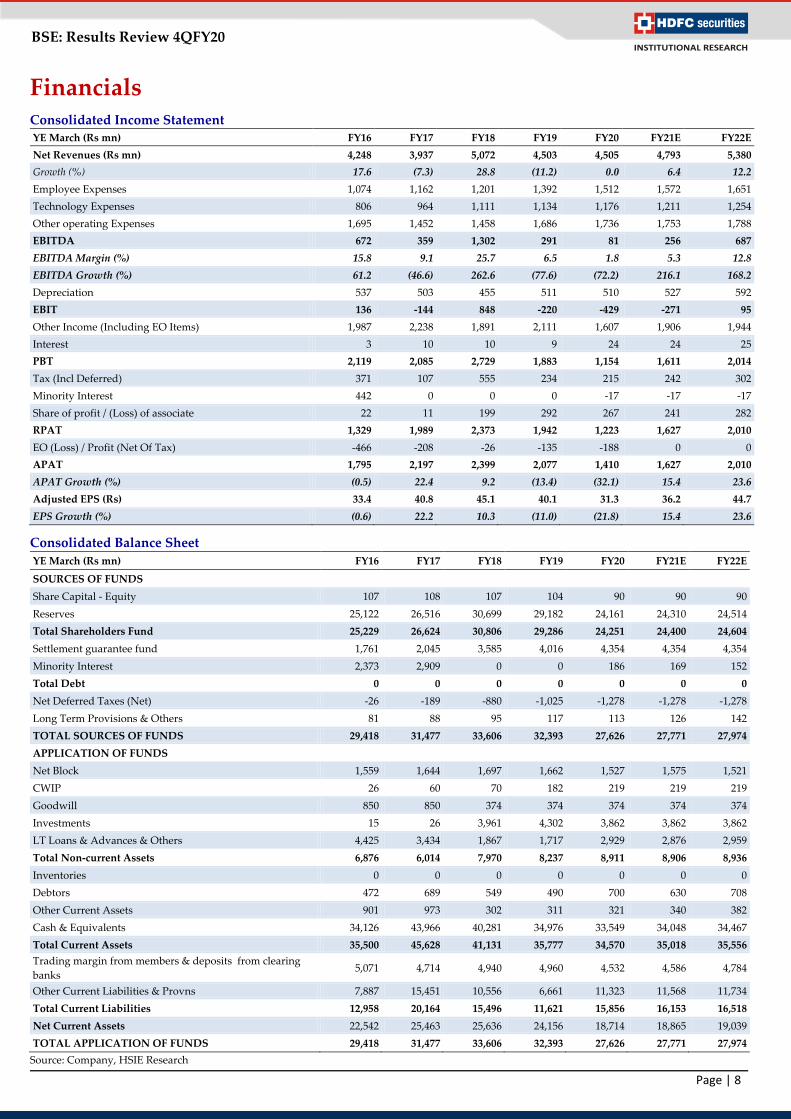

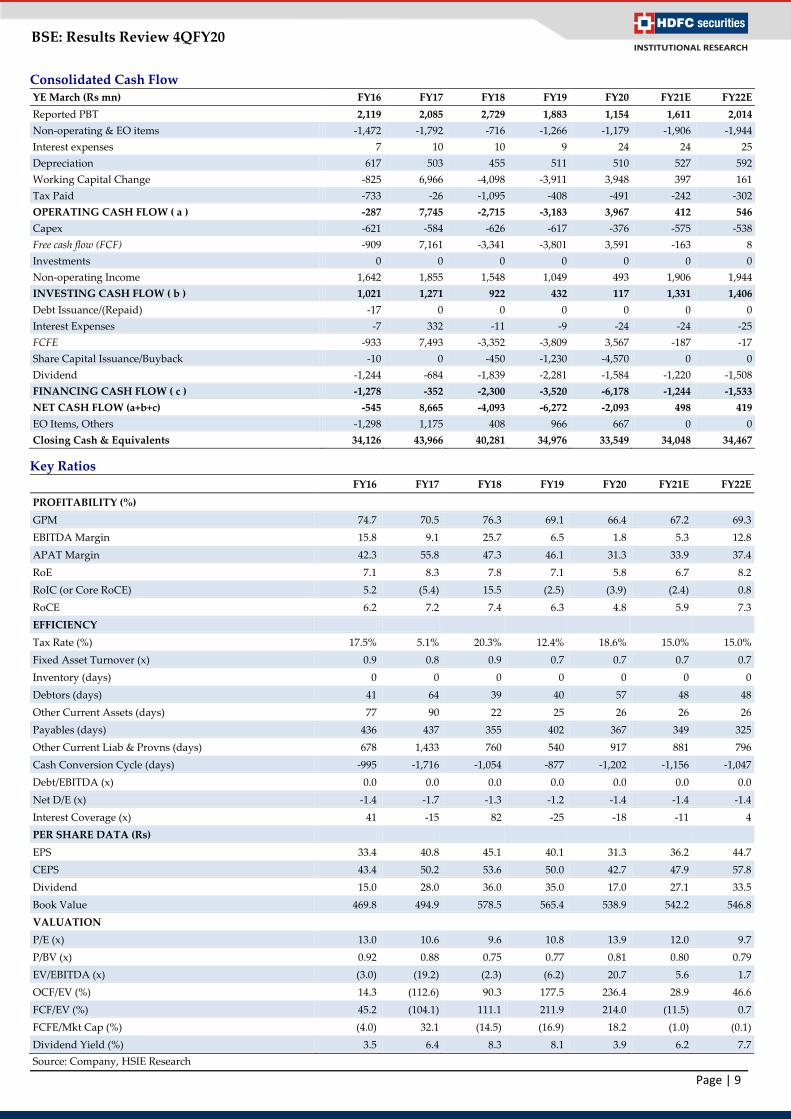

Financials Consolidated Income Statement YE March (Rs mn) FY16 FY17 FY18 FY19 FY20 FY21E FY22E

Net Revenues (Rs mn) 4,248 3,937 5,072 4,503 4,505 4,793 5,380

Growth (%) 17.6 (7.3) 28.8 (11.2) 0.0 6.4 12.2

Employee Expenses 1,074 1,162 1,201 1,392 1,512 1,572 1,651

Technology Expenses 806 964 1,111 1,134 1,176 1,211 1,254

Other operating Expenses 1,695 1,452 1,458 1,686 1,736 1,753 1,788

EBITDA 672 359 1,302 291 81 256 687

EBITDA Margin (%) 15.8 9.1 25.7 6.5 1.8 5.3 12.8

EBITDA Growth (%) 61.2 (46.6) 262.6 (77.6) (72.2) 216.1 168.2

Depreciation 537 503 455 511 510 527 592

EBIT 136 -144 848 -220 -429 -271 95

Other Income (Including EO Items) 1,987 2,238 1,891 2,111 1,607 1,906 1,944

Interest 3 10 10 9 24 24 25

PBT 2,119 2,085 2,729 1,883 1,154 1,611 2,014

Tax (Incl Deferred) 371 107 555 234 215 242 302

Minority Interest 442 0 0 0 -17 -17 -17

Share of profit / (Loss) of associate 22 11 199 292 267 241 282

RPAT 1,329 1,989 2,373 1,942 1,223 1,627 2,010

EO (Loss) / Profit (Net Of Tax) -466 -208 -26 -135 -188 0 0

APAT 1,795 2,197 2,399 2,077 1,410 1,627 2,010

APAT Growth (%) (0.5) 22.4 9.2 (13.4) (32.1) 15.4 23.6

Adjusted EPS (Rs) 33.4 40.8 45.1 40.1 31.3 36.2 44.7

EPS Growth (%) (0.6) 22.2 10.3 (11.0) (21.8) 15.4 23.6

Consolidated Balance Sheet

YE March (Rs mn) FY16 FY17 FY18 FY19 FY20 FY21E FY22E

SOURCES OF FUNDS

Share Capital - Equity 107 108 107 104 90 90 90

Reserves 25,122 26,516 30,699 29,182 24,161 24,310 24,514

Total Shareholders Fund 25,229 26,624 30,806 29,286 24,251 24,400 24,604

Settlement guarantee fund 1,761 2,045 3,585 4,016 4,354 4,354 4,354

Minority Interest 2,373 2,909 0 0 186 169 152

Total Debt 0 0 0 0 0 0 0

Net Deferred Taxes (Net) -26 -189 -880 -1,025 -1,278 -1,278 -1,278

Long Term Provisions & Others 81 88 95 117 113 126 142

TOTAL SOURCES OF FUNDS 29,418 31,477 33,606 32,393 27,626 27,771 27,974

APPLICATION OF FUNDS

Net Block 1,559 1,644 1,697 1,662 1,527 1,575 1,521

CWIP 26 60 70 182 219 219 219

Goodwill 850 850 374 374 374 374 374

Investments 15 26 3,961 4,302 3,862 3,862 3,862

LT Loans & Advances & Others 4,425 3,434 1,867 1,717 2,929 2,876 2,959

Total Non-current Assets 6,876 6,014 7,970 8,237 8,911 8,906 8,936

Inventories 0 0 0 0 0 0 0

Debtors 472 689 549 490 700 630 708

Other Current Assets 901 973 302 311 321 340 382

Cash & Equivalents 34,126 43,966 40,281 34,976 33,549 34,048 34,467

Total Current Assets 35,500 45,628 41,131 35,777 34,570 35,018 35,556

Trading margin from members & deposits from clearing

banks 5,071 4,714 4,940 4,960 4,532 4,586 4,784

Other Current Liabilities & Provns 7,887 15,451 10,556 6,661 11,323 11,568 11,734

Total Current Liabilities 12,958 20,164 15,496 11,621 15,856 16,153 16,518

Net Current Assets 22,542 25,463 25,636 24,156 18,714 18,865 19,039

TOTAL APPLICATION OF FUNDS 29,418 31,477 33,606 32,393 27,626 27,771 27,974

Source: Company, HSIE Research

Page | 9

BSE: Results Review 4QFY20

Consolidated Cash Flow YE March (Rs mn) FY16 FY17 FY18 FY19 FY20 FY21E FY22E

Reported PBT 2,119 2,085 2,729 1,883 1,154 1,611 2,014

Non-operating & EO items -1,472 -1,792 -716 -1,266 -1,179 -1,906 -1,944

Interest expenses 7 10 10 9 24 24 25

Depreciation 617 503 455 511 510 527 592

Working Capital Change -825 6,966 -4,098 -3,911 3,948 397 161

Tax Paid -733 -26 -1,095 -408 -491 -242 -302

OPERATING CASH FLOW ( a ) -287 7,745 -2,715 -3,183 3,967 412 546

Capex -621 -584 -626 -617 -376 -575 -538

Free cash flow (FCF) -909 7,161 -3,341 -3,801 3,591 -163 8

Investments 0 0 0 0 0 0 0

Non-operating Income 1,642 1,855 1,548 1,049 493 1,906 1,944

INVESTING CASH FLOW ( b ) 1,021 1,271 922 432 117 1,331 1,406

Debt Issuance/(Repaid) -17 0 0 0 0 0 0

Interest Expenses -7 332 -11 -9 -24 -24 -25

FCFE -933 7,493 -3,352 -3,809 3,567 -187 -17

Share Capital Issuance/Buyback -10 0 -450 -1,230 -4,570 0 0

Dividend -1,244 -684 -1,839 -2,281 -1,584 -1,220 -1,508

FINANCING CASH FLOW ( c ) -1,278 -352 -2,300 -3,520 -6,178 -1,244 -1,533

NET CASH FLOW (a+b+c) -545 8,665 -4,093 -6,272 -2,093 498 419

EO Items, Others -1,298 1,175 408 966 667 0 0

Closing Cash & Equivalents 34,126 43,966 40,281 34,976 33,549 34,048 34,467

Key Ratios

FY16 FY17 FY18 FY19 FY20 FY21E FY22E

PROFITABILITY (%)

GPM 74.7 70.5 76.3 69.1 66.4 67.2 69.3

EBITDA Margin 15.8 9.1 25.7 6.5 1.8 5.3 12.8

APAT Margin 42.3 55.8 47.3 46.1 31.3 33.9 37.4

RoE 7.1 8.3 7.8 7.1 5.8 6.7 8.2

RoIC (or Core RoCE) 5.2 (5.4) 15.5 (2.5) (3.9) (2.4) 0.8

RoCE 6.2 7.2 7.4 6.3 4.8 5.9 7.3

EFFICIENCY

Tax Rate (%) 17.5% 5.1% 20.3% 12.4% 18.6% 15.0% 15.0%

Fixed Asset Turnover (x) 0.9 0.8 0.9 0.7 0.7 0.7 0.7

Inventory (days) 0 0 0 0 0 0 0

Debtors (days) 41 64 39 40 57 48 48

Other Current Assets (days) 77 90 22 25 26 26 26

Payables (days) 436 437 355 402 367 349 325

Other Current Liab & Provns (days) 678 1,433 760 540 917 881 796

Cash Conversion Cycle (days) -995 -1,716 -1,054 -877 -1,202 -1,156 -1,047

Debt/EBITDA (x) 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Net D/E (x) -1.4 -1.7 -1.3 -1.2 -1.4 -1.4 -1.4

Interest Coverage (x) 41 -15 82 -25 -18 -11 4

PER SHARE DATA (Rs)

EPS 33.4 40.8 45.1 40.1 31.3 36.2 44.7

CEPS 43.4 50.2 53.6 50.0 42.7 47.9 57.8

Dividend 15.0 28.0 36.0 35.0 17.0 27.1 33.5

Book Value 469.8 494.9 578.5 565.4 538.9 542.2 546.8

VALUATION

P/E (x) 13.0 10.6 9.6 10.8 13.9 12.0 9.7

P/BV (x) 0.92 0.88 0.75 0.77 0.81 0.80 0.79

EV/EBITDA (x) (3.0) (19.2) (2.3) (6.2) 20.7 5.6 1.7

OCF/EV (%) 14.3 (112.6) 90.3 177.5 236.4 28.9 46.6

FCF/EV (%) 45.2 (104.1) 111.1 211.9 214.0 (11.5) 0.7

FCFE/Mkt Cap (%) (4.0) 32.1 (14.5) (16.9) 18.2 (1.0) (0.1)

Dividend Yield (%) 3.5 6.4 8.3 8.1 3.9 6.2 7.7

Source: Company, HSIE Research

Page | 10

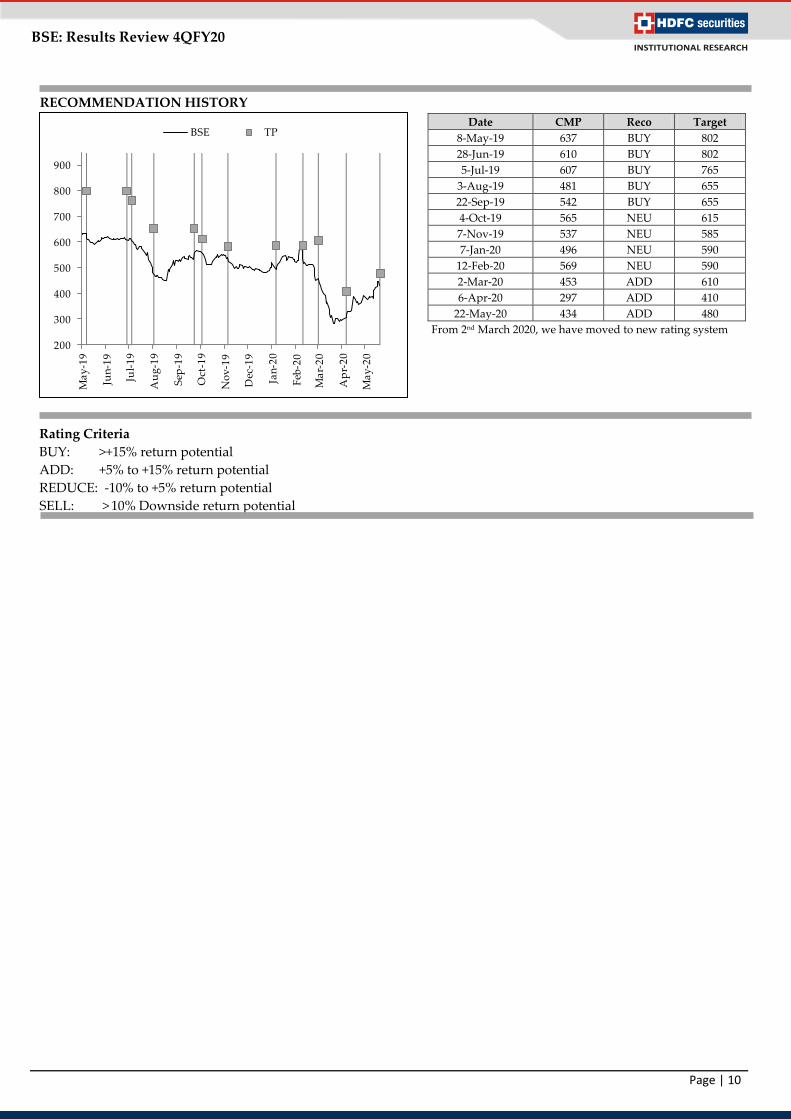

BSE: Results Review 4QFY20

Rating Criteria

BUY: >+15% return potential

ADD: +5% to +15% return potential

REDUCE: -10% to +5% return potential

SELL: > 10% Downside return potential

Date CMP Reco Target

8-May-19 637 BUY 802

28-Jun-19 610 BUY 802

5-Jul-19 607 BUY 765

3-Aug-19 481 BUY 655

22-Sep-19 542 BUY 655

4-Oct-19 565 NEU 615

7-Nov-19 537 NEU 585

7-Jan-20 496 NEU 590

12-Feb-20 569 NEU 590

2-Mar-20 453 ADD 610

6-Apr-20 297 ADD 410

22-May-20 434 ADD 480

From 2nd March 2020, we have moved to new rating system

RECOMMENDATION HISTORY

200

300

400

500

600

700

800

900

Ma

y-1

9

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Ma

r-2

0

Ap

r-2

0

Ma

y-2

0

BSE TP

Page | 11

BSE: Results Review 4QFY20

Disclosure:

We, Amit Chandra, MBA & Vinesh Vala, MBA, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research

report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this

report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this

report.

Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative

or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding

the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material

conflict of interest.

Any holding in stock –No

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is solely for information of the recipient only. The report must not be used as a singular basis of any

investment decision. The views herein are of a general nature and do not consider the risk appetite or the particular circumstances of an individual investor;

readers are requested to take professional advice before investing. Nothing in this document should be construed as investment advice. Each recipient of this

document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in securities of the companies

referred to in this document (including merits and risks) and should consult their own advisors to determine merits and risks of such investment. The

information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be

reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their

securities mentioned herein are not intended to be complete. HSL is not obliged to update this report for such changes. HSL has the right to make changes and

modifications at any time.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen

or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be

contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to

the attention of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in

any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or

price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively

assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security.

This document is not, and should not, be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report

should not be construed as an invitation or solicitation to do business with HSL. HSL may from time to time solicit from, or perform broking, or other services

for, any company mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of

the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a

market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any

other potential conflict of interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments

made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates,

diminution in the NAVs, reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt

in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations

described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject

company for any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t

hedate of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking,

brokerage services or other advisory service in a merger or specific transaction in the normal course of business.

HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with

preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this

report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may

have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of

the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg

(East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022)

3045 3600

HDFC Securities Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA

Corporate Agent License No.: CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN -

U67120MH2000PLC152193

HDFC securities

Institutional Equities

Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park,

Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Board: +91-22-6171-7330 www.hdfcsec.com

Top Related