Languages

Pages

Legal

2015 Tobacco Tax Reform in China:Results and Challenges

Rong Zheng

Director, WHO Collaborating Center for Tobacco and Economics

Professor, University of International Business and Economics (UIBE), Beijing, China

WINNING THE TAX WARS TAX COOP 2016

23-24, May, 2016

World Bank, Washington, DC

CONTENTS

1. The Tobacco Industry and Market in China

2. The 2015 Tobacco Tax Reform

3. China Tobacco Tax Structure

4.The Implementation and Impact of the 2015 Tobacco Tax Reform

5. Future Reforms and Challenges

2016/6/2 2

• 1. Tobacco industry and cigarette market in China

China is the largest producer and consumer of tobacco products in the world, where thirty percent of the world’s

cigarettes are consumed.

China’s tobacco industry is regulated by The State Tobacco Monopoly Administration (STMA), a state-owned monopoly

who is in charge of enforcing related policies for tobacco and cigarette products in China. China National Tobacco

Corporation (CNTC), a state-owned enterprise who is in charge of farming, production, distribution, sales, and marketing

of all tobacco products in China.

In 2015, STMA has 33 provincial branches while CNTC has 19 provincial branches with 94 cigarette manufacturers with

locations in 29 provinces in China except Tibet and Qinghai province.

In 2015, CNTC produces 89 cigarette family brands, within each brand there are multiple varieties differing in terms of

price, packaging and quality. As a result, the 89 family brands provide 870 different domestic cigarettes available in the

market with the price variation between 2.5RMB (0.4 USD)per pack to 100RMB(15.4USD) per pack. 2016/6/2 3

Table 1 The 2015 cigarette excise tax adjustment

Before May 10, 2015 After May 10, 2015

At Producer price level

Specific excise tax (per pack) 0.06 RMB 0.06 RMB

Ad valorem tax

>= 7 RMB 56% 56%

< 7 RMB 36% 36%

At Wholesale price level

Specific excise tax (per pack) 0 0.10 RMB

Ad valorem tax 5% 11%

Excise tax rate at the wholesale segment was increased from 5% to 11%;

An additional specific tax of 0.1RMB (0.015USD) per pack (with 20 sticks) was introduced at the

wholesale level.

STMA price announcement responding to tax adjustment: Wholesale price has increased by 6%;

STMA provincial branches can set up cigarette retail price in the province based on local market under STMA retail

price guidance and at the same time need to meet the required principle that the retailer’s profit margin shouldn’t be lower

than 10%.

Both new cigarette tax and pricing policy are effective from May 10, 2015.

2016/6/2 4

• 2. 2015 Tobacco Tax Reform

Table 2 China tobacco tax structure

Type of Tax Tax level tax base Tax Rate Revenue Beneficiary

Tobacco leaf tax agriculture value of tobacco

leaf

20% 100% local government

Value-added tax at

cigarette manufacture

(VAT)

produce,wholesal

e and retail

added value at

each level

17% 75% central government

25% local government

Specific excise tax produce 0.06

RMB/pack

100% central

government

wholesale 0.10RMB/pack

Ad valorem excise tax produce,

wholesale

allocation

price(without

VAT)

≥ 70 RMB per

carton

56%

< 70 RMB per

carton

36%

wholesale 11%

Urban maintenance and

construction tax and extra

charges of educational fee

( C&E Tax)

produce,

wholesale, retail

tax amount of

VAT and excise

tax

12% in average

100% local government2016/6/2 5

3. China Tobacco Tax Structure

• Cigarette pricing mechanism in China

2016/6/2 6

Allocation Price Wholesale Price Retail Price

A A(1+a) A(1+a) (1+b)

Figure 1:Cigarette Pricing Mechanism in China

Pr = 𝐴 × 1 + 𝑎 × 1 + 𝑏 × 1 + 𝑅𝑡𝑣𝑎𝑡 (1

4. Methodology: WHO TaXSiM model

Use 5 cigarettes as representative brands for 5 classifications of 870 different kind of cigarettes on the market with 150 brand families.

Criteria of choosing representatives: • The selected brand has a large market share in each cigarette category and, • The allocation price of the representative cigarette is the median or very close to the median allocation price in each

category• All calculations and simulations are based on the 5 representative cigarettes

Data (2001-2015)

Tobacco industry data are retrieved from China Tobacco Almanac which includes:

• cigarette output value

• cigarette output volume

• cigarette production volume for each class (Class I, Class II, Class III, Class IV, Class V)– market share of each class

• cigarette wholesale profit margin

• cigarette price data (including allocation price, wholesale price and retail price for each class of representative brand and specification) is retrieved from annual cigarette allocation plan

2016/6/2 7

• 5. Impact so far? #1 – Price

2016/6/2 8

Table 3 Impact on Prices

Class Class I

(Premium)

Class I

(Average)Class II Class III Class IV Class V Total in average

Wholesale price

(RMB/pack)

2014 36.00 20.60 11.60 8.30 4.50 2.25 10.27

2015 38.16 21.84 12.30 8.80 4.77 2.39 11.18

△ 2.16 1.24 0.70 0.50 0.27 0.14 0.92

△ % 6.00% 6.00% 6.00% 6.00% 6.00% 6.00% 8.9%

Retail price

(RMB/pack)

2014 43.00 23.00 13.00 9.50 5.00 2.50 11.61

2015 45.00 25.00 14.00 10.00 5.50 3.00 12.81

△ 2.00 2.00 1.00 0.50 0.50 0.50 1.19

△ % 4.65% 8.70% 7.69% 5.26% 10.00% 20.00% 10.3%

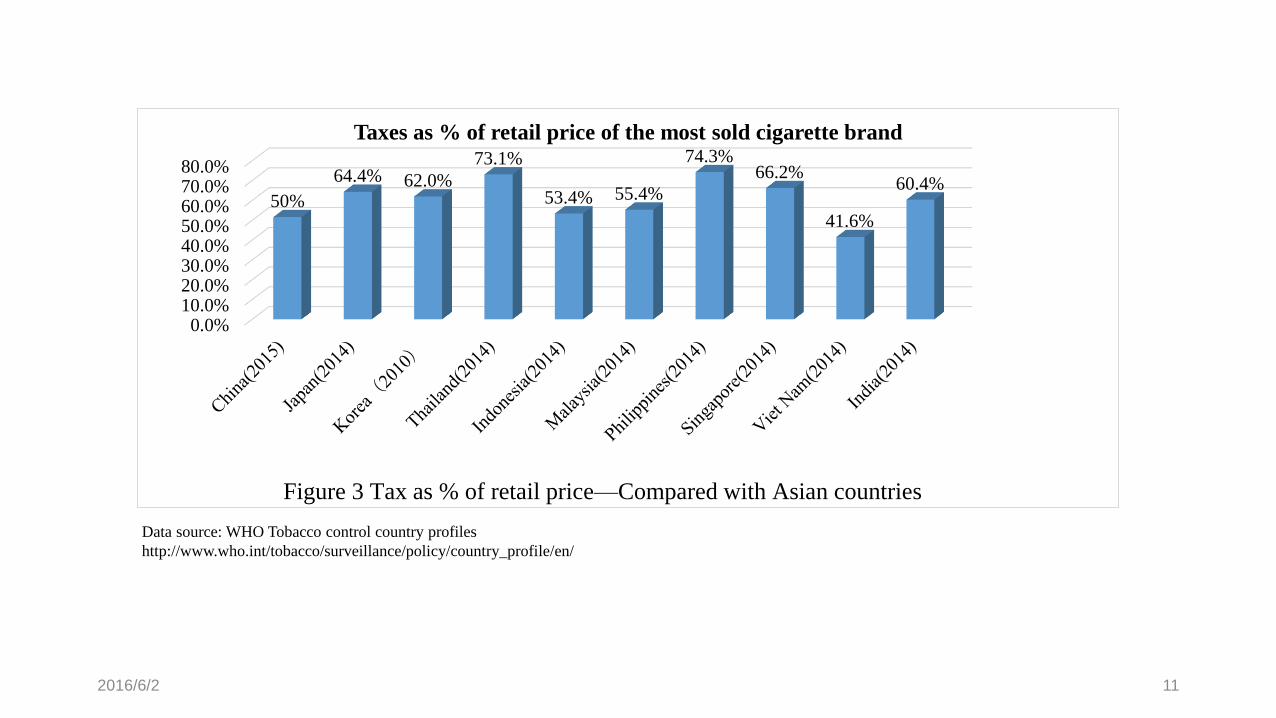

• 5. Impact so far? #2 – Tax as % of retail price (Tax incidence)

Table 4 Tax as % of retail price

Class

Class I

(Premiu

m)

Class I

(Average

)

Class II Class III Class IV Class VTotal in

average

Total tax

as% of

retail price

2014 52% 55.40% 58.50% 44.82% 47.23% 53.72% 52%

2015 55% 58.84% 61.73% 50.37% 52.22% 55.98% 56%

△3%

3.44% 3.23% 5.55% 4.99% 2.25% 4%

Total excise

as% of

retail price

2014 36% 38.68% 40.66% 27.47% 28.91% 33.37% 35%

2015 39% 42% 45% 33% 34% 36% 39%

△3%

3.48% 4.07% 5.61% 5.19% 2.95% 4%

2016/6/2 9

2016/6/2 10

55%58%

45%47%

54%52%

59%62%

50%52%

56% 56%

0%

10%

20%

30%

40%

50%

60%

70%

Class I Class II Class III Class IV Class V Total in average

2014 2015

Figure 2 Tax as % of retail price

Data source: WHO Tobacco control country profiles

http://www.who.int/tobacco/surveillance/policy/country_profile/en/

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%

50%

64.4% 62.0%

73.1%

53.4% 55.4%

74.3%66.2%

41.6%

60.4%

Taxes as % of retail price of the most sold cigarette brand

Figure 3 Tax as % of retail price—Compared with Asian countries

2016/6/2 11

• 5. Impact so far? #3 Impact on market sales

Table 5 Impact on market sales

Simulated Actual

price elasticity -0.4 -0.22

Retail price 2014 RMB/pack 11.31 11.31

Retail price 2015 RMB/pack 12.50 12.50

△(price) RMB/pack 1.19 1.19

%△(price) % 10.53% 10.53%

%△(sales volume) % -4.21% -2.36% (-3.3% 1 year )

△(sales volume) billion packs -5.37 -3.01

Sales volume 2014 billion packs 127.476 127.476

Sales volume 2015 billion packs 122.11 124.47

2016/6/2 12

• 5. Impact so far? #4 – Impact on market structure

2016/6/2 13

20.10%

10.37%

44.96%

18.20%

6.37%

21.39%

11.73%

44.02%

16.99%

5.87%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

Class I Class II Class III Class IV Class V

Figure 4 Market share change 2014-2015

2014

2015

2016/6/2 14

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Figure 5 Cigarette Market Share (2007-2015)

Class V

Class IV

Class III

Class II

Class I

Year

2016/6/2 15

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Figure 6 Market Share May 2015-March 2016

ClassⅠ

ClassⅡ

ClassⅢ

ClassⅣ

ClassⅤ

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Figure 6 Market Share May 2015-March 2016

ClassⅤ

ClassⅣ

ClassⅢ

ClassⅡ

ClassⅠ

In the first quarter of 2016, the market share of middle and up price cigarettes has been reduced, while the cheapest cigarette market share has been increased by 6%, which indicates smokers switching down.

Table 6 Impact on government’s revenue

Tobacco

tax and

profit

Tobacc

o tax

Tobacco

industry

profit

Tax and profit

contribution

to central

gov’t

Profit

before

income

tax

Corperat

e income

tax

SOE profit

contribution

rate

SOE

profit

contribut

ion

Addition

al

contribu

tion

Additional

excise

contributio

n

Billion

USD

Billion

USD

Billion

USD Billion USD

Billion

USD

Billion

USD %Billion

USD

Billion

USD

Billion

USD

2014 161.81 118.43 43.38 140.16 33.83 8.46 25% 6.34 6.92

2015 175.94 129.29 46.65 168.46 39.14 9.79 25% 7.34 13.15 8.89

△ 9% 8%

Exchange rate: 1USD=6.5CNY

2016/6/2 16

5. Impact so far? #5 Impact on government’s revenue

In the long term:

To increase tobacco tax and price persistently;

To introduce indexation management to tobacco excise tax policy with the aim to keep the affordability in a certain level

In 2016:

The central government requests additional 12.3 billion USD revenue from tobacco industry on the basis of 2015;

Cigarette production, consumption, tax revenue in the first quarter of 2016 have been decreased compared with the first quarter of 2015;

Another tax hike is expected to happen this year.

2016/6/2 17

6. Future reforms

7. Challenges

(1) The objectives of tobacco tax policy To generate revenues for the government budget.

To reduce tobacco consumption on health grounds;

Tobacco tax hike propaganda should put priority on public health to win support from general public.

(2) Earmarking plays a key role in sustainable tobacco control strategy.

(3) Governments have additional objectives, such as: Supporting the agriculture sector

Encouraging investment and employment in manufacturing and distribution activities

Concerns for the pool and low social and economic groups.

Research in these fields is fundamental to provide supporting evidence to promote tax hike.

(4) Fiscal experts should play a leading role. They have the knowledge and capacity to develop draft guidelines which frames the country’s circumstance while do not infringe tax sovereignty.

2016/6/2 18

THANK YOU!

2016/6/2 19

Top Related