Languages

Pages

Legal

Risk. Reinsurance. Human Resources.

Aon Benfield

Insurance Risk StudyGrowth, profitability, and opportunity

Ninth edition 2014

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Global Premium, Profitability, and Opportunity . . . . . . . . . . . . . .5Global P&C Gross Written Premium and Growth Rates by Product Line . 6

Growth Markets and Over / Under Performers . . . . . . . . . . . . . . . . . . . . . . 8

Looking Ahead: Growth Projections . . . . . . . . . . . . . . . . . . . . . .10

Uncovering Growth Opportunities . . . . . . . . . . . . . . . . . . . . . . .15Country Opportunity Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Insurance Trends: Risks and Opportunities . . . . . . . . . . . . . . . . .17Auto Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

U .S . Health Insurance Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

U .S . Cyber Insurance Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

China Crop Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Global Risk Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

U.S. Risk Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

U.S. Profitability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

U.S. Reserve Adequacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Global Correlation Between Lines . . . . . . . . . . . . . . . . . . . . . . . .28

Big Data and Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Sources and Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Table of Contents

Aon Benfield 3

IntroductionThe 2014 Insurance Risk Study is focused on uncovering profitable growth opportunities in the insurance

market . There are many bright spots within today’s rapidly evolving insurance marketplace . Globally, property

casualty business produced an underwriting profit in 2013 with a combined ratio of 99 .1 percent . In 21 of the

top 50 markets combined ratios were below 95 percent, and in ten the combined ratios were below 90 percent .

Furthermore, 16 countries showed five year premium growth in excess of 10 percent, led by very strong growth in

China . The first section of the Study presents the country and line of business detail to identify these opportunities

and discusses how to move from coarse statistics to targeted growth strategies . The second section provides an

update of our global risk parameters .

Premium, capital, and profitability highlights

At year end 2013, global premium stands at an all-time high of

USD4 .9 trillion, an increase of 0 .9 percent over the prior year .

Property casualty premium increased 3 .5 percent, and

life premiums shrunk by 2 .0 percent while health premiums

grew 4 .5 percent .

Global insurance premium and capital, USD trillions

Premium Capital

Property & Casualty 1 .4 1 .3

Life & Health 3 .3 2 .1

Reinsurance 0 .2 0 .5

Total 4 .9 4 .0

Global capital increased 3 .9 percent year on year to USD4 .0

trillion . Property casualty insurance capital increased 7 .1 percent .

And reinsurance capital is at an all-time high, as we discuss at

greater length in Aon Benfield’s Reinsurance Market Outlook .

Property casualty penetration is 1 .9 percent of GDP, marginally

down from 2 .0 percent last year based on the top 50 countries .

Auto insurance accounts for 46 percent of property casualty

premium, while property accounts for 33 percent and liability

for 21 percent .

Catastrophe losses have been a driver of the growth in

property premiums in many parts of the world . Impact

Forecasting, Aon Benfield’s catastrophe model development

center, estimates that during 2013 insured catastrophe losses

totaled USD45 billion . In perspective, catastrophe losses

translated into 3 .2 percent of property casualty premium and a

“global catastrophe load” of 9 .9 percent of property premium .

The combined ratio for property casualty business in the

top 50 countries in 2013 was under 99 .1 percent compared

to 101 .1 percent last year . The global average is helped by

European countries, with an average combined ratio of 96 .7

percent, compared to 101 .0 percent in the Americas and

100 .4 percent in Asia Pacific . The five year average combined

ratio continued under 100 percent too, at 99 .8 percent . The

overall global combined ratio under 100 percent, and the

variation in results by country, clearly show there are many

desirable areas for profitable growth in the market today .

Where does the insurance market go from here? We

project that global premium will grow by 18 percent over

the next five years, reaching a total of USD 1 .6 trillion by

2018 . Auto will continue to be the largest line, driven

in part by strong growth in China . Detailed projections

by line and country are shown on pages 10 to 14 .

4 Insurance Risk Study

Growth and Big Data

The Insurance Risk Study is now in its ninth edition, and

there have been many changes in the industry since we

began research for the first edition in 2005 . After seven

major (category 3+) U .S . hurricane landfalls from 2004

to 2005 there have been no major hurricane landfalls

in the last eight years . Adverse loss development has

turned into a long stream of favorable development .

Premium growth and the locus of catastrophe losses

has shifted to the East . Today the emphasis is on

making efficient use of cheaper alternative capital and

on growth in the face of an often sluggish economic

environment—challenging themes that recent editions

of the Study have addressed with increasing detail .

The market continues to embrace and adopt “Big

Data” concepts in pricing and underwriting—a subject

we explore on pages 30 to 32 . Big data for insurance

often really means Behavioral Data, with the industry

engaging in an active search for more detailed and

more predictive variables to add to underwriting

and pricing algorithms . Aon Benfield, and Aon more

broadly, are spearheading several initiatives to help

bring more predictive variables and analytic insight to

clients, in areas including health and crop insurance .

The growth imperative continues to stress many

industries, particularly in mature markets . For insurers, the

efficiency gains from Big Data often serve to redistribute

risks, but not to grow the pie—creating clear winners and

losers . The first part of the Study now covers detailed

global information about insurance capital, premium, and

profitability . We continue to be the only comprehensive

view of combined ratio by country available in the public

domain, to the best of our knowledge . We also offer some

ideas for how to grow the pie . The Study includes global

growth projections for insurance and reinsurance as well

as sections on health, auto, crop, and cyber insurance .

Using the study

Insurance risk remains core to the Study and pages 22

to 30 contain our comprehensive view of risk by line

and geography using the techniques we have been

applying consistently since 2005 . The Insurance Risk

Study continues to be the industry’s leading set of risk

parameters for modeling and benchmarking underwriting

risk and global profitability . Beyond risk modeling, we can

also provide our clients with very granular, customized

market intelligence to create business plans that are

realistic, fact-based, and achievable . With a global fact

base and broad access to local market practitioners, we

are equipped to provide insight across a spectrum of

lines, products, and geographies . Inpoint, the consulting

division of Aon Benfield, helps insurers and reinsurers

address these challenges, from sizing market opportunities

to identifying distribution channel dynamics, assessing

competitor behavior, and understanding what it takes to

compete and win . Our approach leverages Aon Benfield’s

USD130 million annual investment in analytics, data,

and modeling to help our clients grow profitably .

All of our work at Aon Benfield is motivated by client

questions . We continue to be grateful to clients who have

invited us to share in the task of helping them analyze

their most complex business problems . Dynamic and

interactive working groups always lead to innovative,

and often unexpected, solutions . If you have questions

or suggestions for items we could explore in future

editions, please contact us through your local Aon Benfield

broker or one of the contacts listed on the back page .

Aon Benfield 5

An abundance of capital is providing new lower cost alternatives to traditional equity risk financing, opening new avenues for growth . After many years of catastrophe risk management, often implemented as exposure reductions, clients are now looking more aggressively at growth opportunities to leverage this new cheaper capacity . To help guide growth decisions, Aon Benfield has worked through a mass of market data from many different sources to produce the consistent, country-level profitability statistics we introduce in this section .

Our strategic decision framework identifies accessible

markets and high-potential customer segments to formulate

growth programs tailored to an insurer’s capabilities and risk

appetite . Working with our broker network and our investment

bank, Aon Benfield Securities, we can develop and help

execute growth plans through organic growth, acquisition,

reinsurance, and joint ventures, singly or in combination .

Part of our job is to make connections and draw comparisons

that others do not see . In that spirit, we begin this section

with the map below, which overlays country names on

states with approximately equivalent premium volumes .

California is the largest U .S . state in terms of premium,

and if it were independent it would follow the U .K . as

the seventh largest insurance market in the world . Texas,

Florida, and New York would also sit among the top

10 as independent countries, having roughly the same

premium as Canada, Italy, and Australia respectively .

This section presents our unique, detailed analysis of

global capital, premium, and profitability, as well as

snapshots of trends and emerging risks that we expect to

create both risk and opportunity in the coming years .

Global P&C premium compared to U.S. state premium

U.K.

Morocco

Romania

Luxembourg

Romania Greece

Singapore

Austria

ThailandSingapore

TaiwanIreland India

DenmarkSaudi Arabia

Canada

Poland

ThailandAustria

Colombia

Mexico

Malaysia

Poland

Switzerland

Italy

Sweden

Netherlands

Portugal

South Africa

Thailand

India

Brazil Austria

Venezuela

SwitzerlandBrazil

Greece

Russia Australia

Russia

South Africa

South Africa Argentina

Morocco

Romania

Romania

Nigeria

Israel

Turkey

MoroccoPacific Region = China

Mid-Atlantic Region = China

East North Central Region = Germany

West South Central Region = U.K.

West North Central Region = Canada

Mountain Region = Australia

East South Central Region = Spain

New England Region = Spain

South Atlantic Region = Japan

Global Premium, Profitability, and Opportunity

6 Insurance Risk Study

Premium by product line

Notes: All statistics are the latest available. “Motor” includes all motor insurance coverages. “Property” includes construction, engineering, marine, aviation, and transit insurance as well as property. “Liability” includes general liability, workers’ compensation, surety, bonds, credit, and miscellaneous coverages.

U.S., 44%

U.S., 34%

Middle East & Africa

Rest of Europe

Rest of Euro AreaU.K.

GermanyFrance, 4%

Rest of APAC

South Korea

Japan

China, 10%

Rest of Americas

Canada

Motor: USD 633 billion

Property: USD 453 billion

Brazil

Middle East & Africa

Rest of Europe

Rest of Euro Area

U.K.

Germany

France, 6%

Rest of APACSouth Korea

JapanChina, 3%

Rest of AmericasCanada

Brazil

Liability: USD 296 billion

U.S., 45%

Middle East& Africa

Rest of Europe Rest of Euro Area

U.K.

Germany

France, 6%

Rest of APAC

South KoreaJapan

China, 2%Rest of Americas

CanadaBrazil

Five-year average annual growth rate

Property: 4.0% annual growth

Liability: 1.6% annual growth

Motor: 3.6% annual growth

-10

-5

0

5

10

15

20

25

30

Mid

dle Ea

st & A

frica

Rest o

f Euro

pe

Rest o

f Euro

Are

aU.K

.

Germ

any

France

Rest o

f APA

C

South

Korea

Japan

China

Rest o

f Am

erica

s

Canad

aBraz

ilU.S.

-10

-5

0

5

10

15

20

25

30

Mid

dle Ea

st & A

frica

Rest o

f Euro

pe

Rest o

f Euro

Are

aU.K

.

Germ

any

France

Rest o

f APA

C

South

Korea

Japan

China

Rest o

f Am

erica

s

Canad

aBraz

ilU.S.

-10

-5

0

5

10

15

20

25

30

Mid

dle Ea

st & A

frica

Rest o

f Euro

pe

Rest o

f Euro

Are

aU.K

.

Germ

any

France

Rest o

f APA

C

South

Korea

Japan

China

Rest o

f Am

erica

s

Canad

aBraz

ilU.S.

Global P&C gross written premium and growth rates by product line

Aon Benfield 7

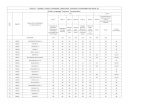

Top 50 P&C markets ranked by gross written premium by region

P&C

GW

P (U

SD M

)

Prem

ium

/ G

DP

Rati

o

Annualized Premium Growth Cumulative Net Loss Ratio Cumulative Net Expense Ratio Cumulative Net Combined Ratio

1yr 3yr 5yr 1yr 3yr 5yr 1yr 3yr 5yr 1yr 3yr 5yr

Americas

U .S . 531,838 3 .0% 5 .6% 5 .3% 2 .5% 74 .8% 75 .6% 74 .8% 27 .3% 27 .2% 27 .0% 102 .1% 102 .9% 101 .9%

Canada 42,179 2 .4% 0 .8% 7 .0% 4 .6% 65 .3% 69 .6% 70 .3% 29 .0% 28 .7% 28 .6% 94 .3% 98 .3% 99 .0%

Brazil 23,647 1 .1% -3 .1% 3 .2% 5 .9% 53 .0% 53 .6% 55 .3% 35 .3% 34 .4% 30 .4% 88 .3% 88 .1% 85 .7%

Argentina 11,835 2 .9% 13 .8% 19 .9% 16 .9% 71 .2% 68 .4% 67 .5% 36 .4% 37 .3% 37 .3% 107 .6% 105 .7% 104 .8%

Mexico 10,415 0 .8% 11 .9% 10 .7% 6 .2% 61 .7% 64 .0% 65 .9% 30 .4% 30 .2% 31 .0% 92 .2% 94 .2% 96 .9%

Venezuela 6,732 2 .0% 27 .2% 1 .6% 12 .2% 58 .8% 61 .5% 63 .7% 37 .7% 35 .2% 33 .1% 96 .5% 96 .7% 96 .9%

Colombia 4,425 1 .1% 0 .5% 11 .2% 11 .2% 63 .5% 61 .4% 61 .4% 48 .7% 48 .0% 47 .6% 112 .2% 109 .4% 108 .9%

Chile 3,708 1 .4% -0 .3% 11 .8% 10 .2% 50 .4% 51 .4% 51 .6% 45 .0% 43 .0% 44 .0% 95 .4% 94 .4% 95 .6%

Ecuador 1,547 1 .5% 16 .5% 16 .3% 14 .0% 53 .0% 52 .3% 53 .2% 35 .8% 34 .3% 33 .7% 88 .8% 86 .6% 86 .9%

Subtotal 636,325 2.6% 5.3% 5.6% 3.1% 72.7% 73.8% 73.4% 28.3% 28.2% 27.7% 101.0% 101.9% 101.1%

Europe, Middle East & Africa

Germany 71,432 1 .8% 3 .1% 2 .3% 0 .5% 73 .3% 74 .6% 73 .9% 25 .3% 25 .7% 25 .2% 98 .6% 100 .3% 99 .0%

U .K . 65,538 2 .3% 1 .3% 3 .5% -3 .0% 65 .2% 67 .1% 66 .9% 34 .3% 33 .9% 34 .3% 99 .5% 101 .0% 101 .2%

France 66,918 2 .3% -6 .5% -1 .8% -0 .3% 73 .5% 74 .5% 74 .3% 24 .2% 24 .5% 24 .6% 97 .7% 99 .0% 98 .9%

Italy 37,397 1 .7% -2 .4% -2 .2% -4 .2% 71 .5% 74 .2% 75 .2% 23 .7% 23 .6% 23 .6% 95 .2% 97 .7% 98 .8%

Spain 28,826 2 .0% 0 .0% -1 .7% -4 .9% 71 .2% 71 .6% 71 .5% 21 .4% 21 .0% 21 .1% 92 .6% 92 .6% 92 .5%

Russia 19,199 0 .9% 8 .2% 14 .7% 5 .9% 63 .0% 64 .7% 65 .8% 28 .6% 24 .5% 22 .9% 91 .6% 89 .3% 88 .7%

Netherlands 13,366 1 .6% -7 .9% -3 .5% -1 .0% 88 .8% 88 .6% 88 .0% 12 .0% 12 .7% 13 .0% 100 .9% 101 .3% 101 .0%

Switzerland 14,682 2 .1% 2 .4% 5 .3% 5 .1% 68 .6% 70 .0% 70 .9% 26 .6% 26 .1% 26 .2% 95 .2% 96 .1% 97 .1%

Belgium 10,880 2 .0% -4 .2% 0 .9% 1 .7% 67 .2% 70 .1% 71 .3% 28 .1% 28 .0% 27 .7% 95 .2% 98 .1% 99 .0%

Norway 9,454 1 .8% 9 .5% 7 .9% 5 .7% 71 .4% 73 .5% 73 .8% 14 .2% 15 .1% 15 .7% 85 .7% 88 .7% 89 .6%

Austria 9,767 2 .2% 5 .9% 3 .3% 0 .4% 70 .2% 70 .8% 70 .6% 28 .3% 28 .7% 28 .5% 98 .5% 99 .5% 99 .0%

Sweden 7,669 1 .3% -1 .3% 5 .2% 0 .8% 74 .1% 73 .9% 73 .4% 18 .4% 17 .7% 17 .8% 92 .4% 91 .6% 91 .1%

Denmark 8,473 2 .4% 2 .7% 1 .8% -0 .1% 71 .4% 76 .3% 76 .2% 17 .2% 17 .2% 17 .3% 88 .6% 93 .5% 93 .5%

Turkey 7,770 1 .0% 14 .2% 13 .0% 5 .3% 79 .0% 77 .7% 78 .2% 26 .7% 27 .8% 26 .9% 105 .7% 105 .5% 105 .1%

Poland 7,439 1 .4% 3 .5% 3 .4% -0 .2% 60 .8% 65 .9% 64 .1% 30 .6% 30 .7% 31 .7% 91 .4% 96 .7% 95 .8%

South Africa 9,968 2 .8% -3 .0% 9 .2% 11 .7% 61 .0% 61 .3% 63 .3% 24 .9% 25 .0% 24 .2% 86 .0% 86 .4% 87 .6%

Finland 5,107 1 .9% 15 .6% 7 .6% 3 .2% 78 .2% 81 .7% 80 .1% 20 .5% 20 .7% 20 .6% 98 .7% 102 .4% 100 .6%

Ireland 3,548 1 .5% -9 .2% -6 .2% -6 .1% 73 .2% 72 .1% 72 .6% 29 .3% 29 .2% 28 .4% 102 .5% 101 .3% 101 .0%

Israel 4,326 1 .4% 13 .3% 6 .2% 4 .0% 74 .3% 76 .2% 77 .2% 32 .2% 32 .2% 31 .5% 106 .5% 108 .4% 108 .7%

Czech Republic 3,935 2 .0% 4 .1% -0 .7% -2 .5% 62 .5% 63 .0% 63 .1% 29 .9% 29 .3% 27 .9% 92 .4% 92 .3% 91 .0%

U .A .E . 3,424 0 .8% -8 .9% -1 .2% 0 .1% 70 .4% 71 .5% 70 .5% 22 .0% 19 .9% 17 .6% 92 .4% 91 .4% 88 .1%

Portugal 4,165 1 .8% -8 .6% -4 .4% -5 .0% 71 .7% 71 .2% 70 .0% 23 .3% 22 .8% 22 .7% 95 .1% 94 .0% 92 .7%

Greece 2,840 1 .1% -4 .9% -2 .2% 0 .4% 56 .4% 58 .3% 62 .1% 40 .5% 38 .8% 38 .6% 96 .9% 97 .1% 100 .7%

Saudi Arabia 3,067 0 .4% 27 .8% 19 .6% 15 .8% 79 .1% 74 .2% 73 .4% 15 .0% 18 .3% 18 .1% 94 .1% 92 .5% 91 .5%

Romania 1,929 1 .0% 9 .2% -2 .0% -6 .9% 72 .1% 72 .7% 75 .0% 42 .5% 40 .5% 36 .8% 114 .6% 113 .2% 111 .8%

Morocco 1,638 1 .4% 11 .5% 5 .9% 10 .8% 57 .9% 61 .2% 64 .5% 33 .2% 33 .8% 33 .2% 91 .1% 95 .1% 97 .8%

Nigeria 1,136 0 .4% 8 .5% 2 .1% 17 .2% 51 .0% 49 .3% 48 .6% 31 .4% 31 .2% 31 .7% 82 .5% 80 .5% 80 .2%

Luxembourg 951 1 .5% -3 .2% 2 .2% -13 .0% 66 .0% 65 .3% 64 .7% 37 .2% 37 .5% 37 .2% 103 .2% 102 .8% 101 .9%

Bulgaria 917 1 .7% 7 .6% 0 .3% -3 .9% 54 .6% 55 .0% 54 .8% 34 .8% 35 .8% 35 .5% 89 .5% 90 .8% 90 .3%

Subtotal 425,763 1.8% 0.4% 1.8% -0.5% 72.0% 73.2% 73.3% 24.8% 24.6% 24.6% 96.7% 97.8% 97.9%

Asia Pacific

Japan 94,825 2 .0% 2 .7% 7 .3% 7 .8% 69 .1% 71 .0% 69 .1% 33 .2% 33 .9% 34 .4% 102 .3% 105 .0% 103 .5%

China 84,431 0 .8% 18 .1% 26 .1% 26 .3% 64 .4% 64 .6% 66 .8% 34 .5% 33 .3% 31 .9% 98 .9% 97 .9% 98 .7%

Australia 34,097 2 .4% 0 .1% 11 .6% 11 .0% 64 .1% 69 .8% 71 .6% 27 .7% 27 .8% 28 .1% 91 .8% 97 .6% 99 .7%

S . Korea 13,298 1 .0% -12 .5% -0 .7% 0 .0% 78 .5% 77 .8% 77 .9% 23 .6% 23 .1% 23 .1% 102 .1% 100 .9% 101 .1%

India 9,200 0 .5% 9 .3% 12 .1% 10 .2% 82 .8% 87 .7% 87 .4% 28 .7% 30 .1% 31 .1% 111 .6% 117 .9% 118 .5%

Thailand 5,651 1 .5% 14 .7% 18 .4% 14 .6% 75 .6% 69 .6% 64 .6% 34 .4% 35 .5% 36 .4% 110 .0% 105 .1% 101 .0%

Malaysia 4,442 1 .3% 4 .5% 8 .3% 8 .4% 59 .0% 61 .9% 62 .3% 30 .6% 28 .5% 28 .4% 89 .7% 90 .4% 90 .7%

Taiwan 3,917 0 .8% 2 .7% 7 .5% 3 .1% 59 .6% 58 .9% 56 .8% 37 .3% 37 .7% 40 .5% 96 .9% 96 .6% 97 .2%

New Zealand 3,886 2 .0% 10 .6% 16 .1% 12 .1% 59 .5% 90 .7% 84 .4% 36 .6% 35 .3% 36 .1% 96 .1% 126 .1% 120 .5%

Indonesia 3,404 0 .4% 3 .5% 15 .4% 11 .6% 53 .3% 54 .3% 55 .0% 33 .0% 33 .3% 33 .2% 86 .3% 87 .6% 88 .2%

Hong Kong 3,187 1 .1% 29 .6% 15 .7% 11 .6% 61 .1% 59 .9% 59 .5% 45 .8% 38 .9% 39 .1% 106 .8% 98 .8% 98 .6%

Singapore 2,501 0 .8% 2 .1% 6 .8% 7 .5% 53 .8% 55 .0% 55 .7% 32 .8% 33 .2% 33 .1% 86 .6% 88 .3% 88 .9%

Subtotal 262,839 1.2% 6.5% 12.9% 12.2% 69.4% 70.8% 70.7% 31.0% 30.9% 31.0% 100.4% 101.8% 101.7%

Top 50 1,324,927 1 .9% 3 .9% 5 .6% 3 .3% 71 .6% 72 .8% 72 .8% 27 .4% 27 .3% 27 .0% 99 .1% 100 .1% 99 .8%

8 Insurance Risk Study

Growth markets and over or under performersAon Benfield examined premium growth and loss ratio

performance by country across motor, property, and liability

lines of business as well as premium growth and combined ratio

performance by country for all lines . The quadrant plots below

summarize the results of that analysis and identify countries as

either low growth or high growth and as loss ratio (by line) or

combined ratio (total) out performers or under performers .

To measure performance, the first three quadrant plots use loss

ratio for each line of business while the right-most plot shows

combined ratio for all lines of business . Each plot also provides

the gross written premium size, in USD millions, of each country .

For all quadrant plots, growth is determined based on five

year annualized premium growth . Countries with values

greater than 7 .5 percent are classified as high growth .

Loss ratio and combined ratio performance is determined

based on five year average loss ratio and five year average

combined ratio, respectively . Each country’s loss ratio

performance is compared against its income level peers,

using a USD30,000 GDP per capita split between high income

and low income companies . Combined ratio performance

is compared against the global combined ratio . Countries

with five year loss ratios lower than the average of their

income peers, or combined ratios below the global

combined ratio, are classified as out performers .

Property

Loss ratio performance

Motor

Loss ratio performance

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Australia 11,644Brazil* 1,692Chile* 742China* 7,007Colombia* 1,078Ecuador* 337Hong Kong* 1,425India* 1,764Indonesia* 487New Zealand* 421Russia* 2,231Saudi Arabia 251Singapore* 784South Africa 1,144Turkey* 595Venezuela* 1,166

Austria 2,313Bulgaria 33Canada 6,607Czech Republic 1,182France 9,945Greece* 356Japan 17,034Malaysia* 480Mexico 1,591Netherlands 2,941Nigeria 294Poland 1,209Romania 192Spain 6,322Switzerland* 3,330Taiwan 397Thailand 294U.A.E.* 1,137

Belgium 3,151Denmark 1,026Finland 1,375Germany 16,331Ireland 812Israel 622Italy 5,392Luxembourg 193Portugal 1,047S. Korea 1,797U.K. 16,617U.S. 133,766

Argentina 4,830Morocco 408Norway 1,594Sweden 203

China* 13,902Colombia* 1,365Ecuador* 616Indonesia* 1,721Mexico 3,631Morocco* 307Nigeria* 548Russia* 5,860Saudi Arabia* 1,121South Africa 4,289

Brazil* 7,745Bulgaria 210Greece 730Hong Kong 745India 2,223Luxembourg 277Malaysia 1,573Romania 456Singapore 744Spain 10,216Switzerland* 5,165Taiwan 1,266Turkey* 2,700U.A.E.* 1,106U.K. 25,132U.S. 191,255Venezuela* 1,059

Austria 3,455Belgium 3,307Canada 15,803Czech Republic 1,141Denmark 4,544Finland 1,682France 25,672Germany 23,030Ireland 1,216Israel 1,181Italy 7,206Japan 20,501Netherlands 4,943Norway 4,916Poland 1,868Portugal 978S. Korea 2,605Sweden 4,179

Argentina* 1,844Australia 11,598Chile 1,784New Zealand 2,287Thailand 1,503

China* 63,522Colombia* 1,982Ecuador* 593Indonesia* 1,196Nigeria* 294Singapore 974South Africa 4,535Thailand* 3,854Venezuela* 4,506

Austria 3,999Bulgaria 673Czech Republic 1,829Denmark 2,903Hong Kong 481Japan 57,290New Zealand 1,179Norway* 3,369Switzerland 6,449U.S. 206,817

Belgium 4,422Brazil* 14,209Canada 19,768Finland 2,051France 24,785Germany 30,671Greece 2,006Ireland 1,520Israel 2,401Italy 24,799Luxembourg 481Mexico 5,193Netherlands 5,483Poland 4,361Portugal 1,739Romania 1,281Russia 11,127S. Korea 8,896Spain 12,717Sweden 3,287Taiwan 2,254Turkey 4,475U.A.E.* 1,227U.K. 23,789

Argentina 5,160Australia 12,854Chile 1,181India 5,213Malaysia 2,388Morocco 931Saudi Arabia 1,695

Australia 34,097Chile* 3,708China 84,431Ecuador* 1,547Hong Kong 3,187Indonesia* 3,404Malaysia* 4,442Morocco 1,638Nigeria* 1,136Saudi Arabia* 3,067Singapore* 2,501South Africa 9,968Venezuela* 672

Austria 9,767Belgium 10,880Brazil* 23,647Bulgaria 917Canada 42,179Czech Republic 3,935Denmark 8,473France 66,918Germany 71,432Italy 37,397Mexico 10,415Norway 9,454Poland 7,439Portugal 4,165Russia* 19,199Spain 28,826Sweden 7,669Switzerland 14,682Taiwan 3,917 U.A.E.* 3,424

Finland 5,107Greece 2,840Ireland 3,548Israel 4,326Luxembourg 951Netherlands 13,366Romania 1,929S. Korea 13,298Turkey 7,770U.K. 65,538U.S. 531,838

Argentina 11,835Colombia 4,425India 9,200Japan 94,825New Zealand 3,886Thailand* 5,651

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Australia 11,644Brazil* 1,692Chile* 742China* 7,007Colombia* 1,078Ecuador* 337Hong Kong* 1,425India* 1,764Indonesia* 487New Zealand* 421Russia* 2,231Saudi Arabia 251Singapore* 784South Africa 1,144Turkey* 595Venezuela* 1,166

Austria 2,313Bulgaria 33Canada 6,607Czech Republic 1,182France 9,945Greece* 356Japan 17,034Malaysia* 480Mexico 1,591Netherlands 2,941Nigeria 294Poland 1,209Romania 192Spain 6,322Switzerland* 3,330Taiwan 397Thailand 294U.A.E.* 1,137

Belgium 3,151Denmark 1,026Finland 1,375Germany 16,331Ireland 812Israel 622Italy 5,392Luxembourg 193Portugal 1,047S. Korea 1,797U.K. 16,617U.S. 133,766

Argentina 4,830Morocco 408Norway 1,594Sweden 203

China* 13,902Colombia* 1,365Ecuador* 616Indonesia* 1,721Mexico 3,631Morocco* 307Nigeria* 548Russia* 5,860Saudi Arabia* 1,121South Africa 4,289

Brazil* 7,745Bulgaria 210Greece 730Hong Kong 745India 2,223Luxembourg 277Malaysia 1,573Romania 456Singapore 744Spain 10,216Switzerland* 5,165Taiwan 1,266Turkey* 2,700U.A.E.* 1,106U.K. 25,132U.S. 191,255Venezuela* 1,059

Austria 3,455Belgium 3,307Canada 15,803Czech Republic 1,141Denmark 4,544Finland 1,682France 25,672Germany 23,030Ireland 1,216Israel 1,181Italy 7,206Japan 20,501Netherlands 4,943Norway 4,916Poland 1,868Portugal 978S. Korea 2,605Sweden 4,179

Argentina* 1,844Australia 11,598Chile 1,784New Zealand 2,287Thailand 1,503

China* 63,522Colombia* 1,982Ecuador* 593Indonesia* 1,196Nigeria* 294Singapore 974South Africa 4,535Thailand* 3,854Venezuela* 4,506

Austria 3,999Bulgaria 673Czech Republic 1,829Denmark 2,903Hong Kong 481Japan 57,290New Zealand 1,179Norway* 3,369Switzerland 6,449U.S. 206,817

Belgium 4,422Brazil* 14,209Canada 19,768Finland 2,051France 24,785Germany 30,671Greece 2,006Ireland 1,520Israel 2,401Italy 24,799Luxembourg 481Mexico 5,193Netherlands 5,483Poland 4,361Portugal 1,739Romania 1,281Russia 11,127S. Korea 8,896Spain 12,717Sweden 3,287Taiwan 2,254Turkey 4,475U.A.E.* 1,227U.K. 23,789

Argentina 5,160Australia 12,854Chile 1,181India 5,213Malaysia 2,388Morocco 931Saudi Arabia 1,695

Australia 34,097Chile* 3,708China 84,431Ecuador* 1,547Hong Kong 3,187Indonesia* 3,404Malaysia* 4,442Morocco 1,638Nigeria* 1,136Saudi Arabia* 3,067Singapore* 2,501South Africa 9,968Venezuela* 672

Austria 9,767Belgium 10,880Brazil* 23,647Bulgaria 917Canada 42,179Czech Republic 3,935Denmark 8,473France 66,918Germany 71,432Italy 37,397Mexico 10,415Norway 9,454Poland 7,439Portugal 4,165Russia* 19,199Spain 28,826Sweden 7,669Switzerland 14,682Taiwan 3,917 U.A.E.* 3,424

Finland 5,107Greece 2,840Ireland 3,548Israel 4,326Luxembourg 951Netherlands 13,366Romania 1,929S. Korea 13,298Turkey 7,770U.K. 65,538U.S. 531,838

Argentina 11,835Colombia 4,425India 9,200Japan 94,825New Zealand 3,886Thailand* 5,651

* Indicates country was a high growth out performer in 2013 Insurance Risk Study Bold indicates country outperforms in all four quadrant plots.

Aon Benfield 9

Twenty countries are high growth, loss ratio outperformers

in at least one line of business . Of these twenty countries,

five appear in each of the lines of business analyzed

as high growth out performers: China, Colombia,

Ecuador, Indonesia, and South Africa . All but China and

South Africa were similarly distinguished last year .

If we compare these countries on the basis of overall combined

ratio, four of the five are outperformers globally . The exception

is Colombia, which underperforms its peers with a five year

net combined ratio of 108 .9 percent, driven by a higher than

average expense ratio . In addition to the four outperforming

countries mentioned above, nine additional countries

outperform the global averages for both growth

and profitability . Singapore, as an example, outperforms for

both motor and liability insurance, and with an all lines five year

combined ratio of 88 .9 percent, it has been a significantly

more profitable market than its overall Asia Pacific peer group .

(See the Top 50 P&C Markets table, page 7 for more details .)

Using combined ratio in addition to loss history allows us

to further analyze and target high growth opportunities .

Liability

Loss ratio performance

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Australia 11,644Brazil* 1,692Chile* 742China* 7,007Colombia* 1,078Ecuador* 337Hong Kong* 1,425India* 1,764Indonesia* 487New Zealand* 421Russia* 2,231Saudi Arabia 251Singapore* 784South Africa 1,144Turkey* 595Venezuela* 1,166

Austria 2,313Bulgaria 33Canada 6,607Czech Republic 1,182France 9,945Greece* 356Japan 17,034Malaysia* 480Mexico 1,591Netherlands 2,941Nigeria 294Poland 1,209Romania 192Spain 6,322Switzerland* 3,330Taiwan 397Thailand 294U.A.E.* 1,137

Belgium 3,151Denmark 1,026Finland 1,375Germany 16,331Ireland 812Israel 622Italy 5,392Luxembourg 193Portugal 1,047S. Korea 1,797U.K. 16,617U.S. 133,766

Argentina 4,830Morocco 408Norway 1,594Sweden 203

China* 13,902Colombia* 1,365Ecuador* 616Indonesia* 1,721Mexico 3,631Morocco* 307Nigeria* 548Russia* 5,860Saudi Arabia* 1,121South Africa 4,289

Brazil* 7,745Bulgaria 210Greece 730Hong Kong 745India 2,223Luxembourg 277Malaysia 1,573Romania 456Singapore 744Spain 10,216Switzerland* 5,165Taiwan 1,266Turkey* 2,700U.A.E.* 1,106U.K. 25,132U.S. 191,255Venezuela* 1,059

Austria 3,455Belgium 3,307Canada 15,803Czech Republic 1,141Denmark 4,544Finland 1,682France 25,672Germany 23,030Ireland 1,216Israel 1,181Italy 7,206Japan 20,501Netherlands 4,943Norway 4,916Poland 1,868Portugal 978S. Korea 2,605Sweden 4,179

Argentina* 1,844Australia 11,598Chile 1,784New Zealand 2,287Thailand 1,503

China* 63,522Colombia* 1,982Ecuador* 593Indonesia* 1,196Nigeria* 294Singapore 974South Africa 4,535Thailand* 3,854Venezuela* 4,506

Austria 3,999Bulgaria 673Czech Republic 1,829Denmark 2,903Hong Kong 481Japan 57,290New Zealand 1,179Norway* 3,369Switzerland 6,449U.S. 206,817

Belgium 4,422Brazil* 14,209Canada 19,768Finland 2,051France 24,785Germany 30,671Greece 2,006Ireland 1,520Israel 2,401Italy 24,799Luxembourg 481Mexico 5,193Netherlands 5,483Poland 4,361Portugal 1,739Romania 1,281Russia 11,127S. Korea 8,896Spain 12,717Sweden 3,287Taiwan 2,254Turkey 4,475U.A.E.* 1,227U.K. 23,789

Argentina 5,160Australia 12,854Chile 1,181India 5,213Malaysia 2,388Morocco 931Saudi Arabia 1,695

Australia 34,097Chile* 3,708China 84,431Ecuador* 1,547Hong Kong 3,187Indonesia* 3,404Malaysia* 4,442Morocco 1,638Nigeria* 1,136Saudi Arabia* 3,067Singapore* 2,501South Africa 9,968Venezuela* 672

Austria 9,767Belgium 10,880Brazil* 23,647Bulgaria 917Canada 42,179Czech Republic 3,935Denmark 8,473France 66,918Germany 71,432Italy 37,397Mexico 10,415Norway 9,454Poland 7,439Portugal 4,165Russia* 19,199Spain 28,826Sweden 7,669Switzerland 14,682Taiwan 3,917 U.A.E.* 3,424

Finland 5,107Greece 2,840Ireland 3,548Israel 4,326Luxembourg 951Netherlands 13,366Romania 1,929S. Korea 13,298Turkey 7,770U.K. 65,538U.S. 531,838

Argentina 11,835Colombia 4,425India 9,200Japan 94,825New Zealand 3,886Thailand* 5,651

All Lines

Combined ratio performance

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Lowgrowth

Highgrowth

Out performers

Under performers

Australia 11,644Brazil* 1,692Chile* 742China* 7,007Colombia* 1,078Ecuador* 337Hong Kong* 1,425India* 1,764Indonesia* 487New Zealand* 421Russia* 2,231Saudi Arabia 251Singapore* 784South Africa 1,144Turkey* 595Venezuela* 1,166

Austria 2,313Bulgaria 33Canada 6,607Czech Republic 1,182France 9,945Greece* 356Japan 17,034Malaysia* 480Mexico 1,591Netherlands 2,941Nigeria 294Poland 1,209Romania 192Spain 6,322Switzerland* 3,330Taiwan 397Thailand 294U.A.E.* 1,137

Belgium 3,151Denmark 1,026Finland 1,375Germany 16,331Ireland 812Israel 622Italy 5,392Luxembourg 193Portugal 1,047S. Korea 1,797U.K. 16,617U.S. 133,766

Argentina 4,830Morocco 408Norway 1,594Sweden 203

China* 13,902Colombia* 1,365Ecuador* 616Indonesia* 1,721Mexico 3,631Morocco* 307Nigeria* 548Russia* 5,860Saudi Arabia* 1,121South Africa 4,289

Brazil* 7,745Bulgaria 210Greece 730Hong Kong 745India 2,223Luxembourg 277Malaysia 1,573Romania 456Singapore 744Spain 10,216Switzerland* 5,165Taiwan 1,266Turkey* 2,700U.A.E.* 1,106U.K. 25,132U.S. 191,255Venezuela* 1,059

Austria 3,455Belgium 3,307Canada 15,803Czech Republic 1,141Denmark 4,544Finland 1,682France 25,672Germany 23,030Ireland 1,216Israel 1,181Italy 7,206Japan 20,501Netherlands 4,943Norway 4,916Poland 1,868Portugal 978S. Korea 2,605Sweden 4,179

Argentina* 1,844Australia 11,598Chile 1,784New Zealand 2,287Thailand 1,503

China* 63,522Colombia* 1,982Ecuador* 593Indonesia* 1,196Nigeria* 294Singapore 974South Africa 4,535Thailand* 3,854Venezuela* 4,506

Austria 3,999Bulgaria 673Czech Republic 1,829Denmark 2,903Hong Kong 481Japan 57,290New Zealand 1,179Norway* 3,369Switzerland 6,449U.S. 206,817

Belgium 4,422Brazil* 14,209Canada 19,768Finland 2,051France 24,785Germany 30,671Greece 2,006Ireland 1,520Israel 2,401Italy 24,799Luxembourg 481Mexico 5,193Netherlands 5,483Poland 4,361Portugal 1,739Romania 1,281Russia 11,127S. Korea 8,896Spain 12,717Sweden 3,287Taiwan 2,254Turkey 4,475U.A.E.* 1,227U.K. 23,789

Argentina 5,160Australia 12,854Chile 1,181India 5,213Malaysia 2,388Morocco 931Saudi Arabia 1,695

Australia 34,097Chile* 3,708China 84,431Ecuador* 1,547Hong Kong 3,187Indonesia* 3,404Malaysia* 4,442Morocco 1,638Nigeria* 1,136Saudi Arabia* 3,067Singapore* 2,501South Africa 9,968Venezuela* 672

Austria 9,767Belgium 10,880Brazil* 23,647Bulgaria 917Canada 42,179Czech Republic 3,935Denmark 8,473France 66,918Germany 71,432Italy 37,397Mexico 10,415Norway 9,454Poland 7,439Portugal 4,165Russia* 19,199Spain 28,826Sweden 7,669Switzerland 14,682Taiwan 3,917 U.A.E.* 3,424

Finland 5,107Greece 2,840Ireland 3,548Israel 4,326Luxembourg 951Netherlands 13,366Romania 1,929S. Korea 13,298Turkey 7,770U.K. 65,538U.S. 531,838

Argentina 11,835Colombia 4,425India 9,200Japan 94,825New Zealand 3,886Thailand* 5,651

10 Insurance Risk Study

For the growth-seeking insurance enterprise, an analysis of historical growth trends and relative profitability will provide a good indication of where to initially target opportunities . However, the key is to be able to understand what is driving the trends and how they might change over the near term, and what these changes may mean for an evolving global insurance marketplace .

We have projected global property casualty insurance premium

growth for the next five years, for the overall insurance market,

and for motor, property, and liability . These projections

are based on a weighting of historic premium growth rates

with projected country GDP and population estimates .

By 2018, we expect the global insurance market to grow by

18 percent to a total direct written premium of USD1 .6 trillion .

Motor insurance will remain the largest property casualty

segment, accounting for 47 percent of total direct written

premium, followed by property (33 percent) and liability

(21 percent) .

The United States will remain the largest property casualty

insurance market, representing an estimated 37 percent

of global premium . China will surpass Japan to become

the second largest market, with an expected 9 percent of

premium . But note that the U .S . projected annual growth

rate is 2 .7 percent while China’s is over 11 percent .

Digging deeper into each line reveals similar trends . In each

line the U .S . will remain the largest property casualty insurance

market, but with relatively limited growth prospects .

Global 2018 premium projections

2013 2018 Projected Projected annual growth %

Country Rank DWP (USD B) Rank DWP (USD B)

United States 1 531 .8 1 607 .8 2 .7%

China* 3 84 .5 2 143 .7 11 .2%

Japan* 2 92 .4 3 108 .8 2 .8%

Germany 4 73 .7 4 81 .9 2 .1%

France 5 69 .3 5 74 .8 1 .5%

China will become the second largest insurance market in the world by 2018 and account for over 10% of global DWP *2013 DWP unavailable; 2012 used as proxy

Motor47%

2018 projected premium mixProjected direct written premium by line

Total DWP: $1,627 Total Growth: 18%

Liability21%

Property33%

0

100

200

300

400

500

600

700

800

MotorLiabilityProperty

453

17%

529

296341

633

757

2013 2018 2013 2018 2013 2018

20%

15%

Looking Ahead: Growth Projections

Aon Benfield 11

Motor Motor, which accounts for USD633 billion of global premium

today, will experience continued rapid growth with a

20 percent five year rate increasing to USD757 billion of direct

written premium . Such projections are easy to understand,

given that we expect continued strong population growth,

particularly in developing markets—and an early sign of middle

class life is owning a car, usually with auto insurance as a

compulsory addition .

China is already the second largest auto market, and will almost

certainly retain this position given its projected 11 .3 percent

annual growth . Yet we must also express a note of caution: the

widely expected partial de-tariffing of China motor business

later this year has the potential to shake-up the world’s fastest

growing insurance market . Companies are struggling with

the data and modeling implications of the change, as well

as the potential market reaction to new pricing flexibility . An

extremely competitive market reaction could lower the growth

rate through an adjustment period . Long term growth that is

driven by economic fundamentals is, however, unlikely to be

significantly impacted .

We project no change in rank amongst the top five global motor

markets . Despite more limited population growth, wealth

generation continues in these countries at a rapid pace, with

more families owning multiple cars, supporting continued

steady growth; developing countries have a long way to go to

catch up with motor penetration in these top markets .

Later in the Study we discuss the changing dynamics of the

U .S . motor insurance market . We do anticipate similar changes

globally, but further off in the future; the technologies gaining

momentum in the U .S . will be slower to make their way into the

developing markets . As such, despite slow projected growth in

the U .S ., global growth will remain strong .

Motor 2018 premium projections

2013 2018 Projected Projected annual growth %

Country Rank DWP (USD B) Rank DWP (UD B)

United States 1 206 .8 1 234 .0 2 .5

China* 2 63 .5 2 108 .4 11 .3

Japan* 3 57 .3 3 66 .3 3 .0

Germany 4 30 .7 4 33 .8 2 .0

France 5 26 .3 5 28 .8 1 .9

*2013 DWP unavailable; 2012 used as proxy

0%

2%

4%

6%

8%

10%

12%

Argentin

a

ColombiaChile

Indonesia

Thail

and

Ecuad

or

Malaysi

aIndia

Saudi A

rabia

China

108.4 2.3 5.40.83.47.5 1.7 1.6 6.72.6 796

U.S.

2018 est. premiumfor country

Middle East & Africa

Rest of Europe

Rest of Euro AreaU.K.

GermanyFrance

Rest of APAC

South Korea

Japan

China

Rest of Americas

CanadaBrazil

2018 projected premium: USD757 billionProjected direct written premium by country

12 Insurance Risk Study

PropertyChina is by far the largest of the rapidly growing property

markets in the world with an 8 percent expected growth rate,

representing nearly USD20 .5 billion of direct written premium,

which will tie China with Japan for the fifth largest property

market in five years .

Many other countries with high expected premium growth

currently have a relatively small premium base . Thailand, for

instance, has nearly 9 percent executed annual growth but

only USD2 .3 billion of projected property premium . When

determining where and how to grow, companies must balance

the growth opportunity against the total market opportunity .

Catastrophe risk potential is another important consideration

for property lines . Economic growth and urbanization are

creating greater risk concentrations, often in catastrophe

exposed areas . Property premium growth is driven, in part,

by catastrophe losses—both actual and potential . Aon Benfield

can use its understanding of global catastrophe risk to produce

an optimal blending of target growth and acceptable risk .

Property 2018 premium projections

2013 2018 Projected Projected annual growth %

Country Rank DWP (USD B) Rank DWP (USD B)

United States 1 191 .3 1 223 .8 3 .2

Germany 2 26 .7 2 30 .3 2 .5

United Kingdom 3 25 .1 3 27 .9 2 .1

France 4 24 .8 4 26 .4 1 .2

Japan* 5 20 .5 5 23 .4 2 .6

*2013 DWP unavailable; 2012 used as proxy

0%

2%

4%

6%

8%

10%

2018 projected premium: USD529 billion Projected growth rate by country

2.3 0.9 2.13.31.920.5 1.5 2.9 0.74.7 796

U.S.

Middle East & Africa

Rest of Europe

Rest of Euro Area

U.K.

Germany

France

Rest of APACSouth Korea

JapanChina

Rest of AmericasCanada

Brazil

Nigeria

Mexico

India

Saudi A

rabia

Malaysi

a

New Zeal

and

Hong KongChina

Ecuad

or

Thail

and

2018 est. premiumfor country

Aon Benfield 13

LiabilityLiability insurance is the smallest of the global property

casualty segments, at approximately half the size of the global

motor insurance market . The U .S . will remain the largest

market by a wide margin, and with Japan, will grow faster than

other top five markets .

China is the fastest growing market for liability

with 16 percent projected annual growth—though

this will not yet make it a top five market .

Liability 2018 premium projections

2013 2018 Projected Projected annual growth %

Country Rank DWP (USD B) Rank DWP (USD B)

United States 1 133 .8 1 150 .0 2 .3

France 2 18 .1 2 19 .6 1 .6

Japan* 3 17 .0 3 19 .1 2 .3

United Kingdom 4 16 .6 4 18 .2 1 .9

Germany 5 16 .3 5 17 .7 1 .7

*2013 DWP unavailable; 2012 used as proxy

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2018 projected premium: USD341 billionProjected growth rate by country

14.8 0.71.60.57.3 2.5 2.0 0.60.30.7 796

U.S.

Middle East& Africa

Rest of Europe Rest of Euro Area

U.K.

Germany

France

Rest of APAC

South Korea

Japan

China

Rest of AmericasCanada

Brazil

New Zeal

and

Saudi A

rabia

Malaysi

a

Hong KongIndia

Indonesia

Colombia

Ecuad

or

Argentin

aChina

2018 est. premiumfor country

14 Insurance Risk Study

ReinsuranceGlobal reinsurance premium by year (USD billions)

Our analysis so far has focused on primary insurance

direct written premium growth without considering the

impact of reinsurance . This approach is largely due to

data availability: reinsurance data is much more limited

and often distorted by the reporting of intercompany

reinsurance within global insurance conglomerates .

Aon Benfield has worked through the available data to

estimate the size of the property casualty global reinsurance

market and project it five years forward . As of year end

2013, we believe total global ceded written premium is

approximately USD170 billion, excluding intercompany

reinsurance and other mandatory pools . This amount

represents the total opportunity for reinsurers .

We do not expect the reinsurance market to grow as rapidly

as the primary market . Excess capital in the insurance market

will allow companies to retain much of their expected

growth, and excess capital in the reinsurance market will

pressure rates so ceded premium will not necessarily

reflect growth in exposures . The influx of alternative capital

could have a positive or a negative impact on reinsurance

premium growth depending on price elasticity . Hedge fund

reinsurers are bringing new capacity to reinsurance markets,

often pricing to a break-even underwriting profit while

expecting to make significant returns on assets . Whether such

changes will serve to stimulate new reinsurance demand,

or merely to further depress prices, remains to be seen .

Aon Benfield projects five year growth of approximately

2 .1 percent per year for the global reinsurance market .

By country, reinsurance growth estimates vary from 5 percent

annual growth in South Korea to negative growth in Japan .

On average, we expect the mature reinsurance markets to

grow about 2 percent per year while developing markets will

grow 5 to 7 percent per year . In China, the impact of the new

C-ROSS capital standards could have a negative impact on

ceded premium in the medium term . The new standards lower

the capital requirements for writing motor business, and at the

same time, decrease the capital efficiency of certain cessions .

The new standards are expected to run in parallel with the

current approach in 2015 and to be fully adopted in 2016 .

Given these dynamics, reinsurance companies are seeking

out new growth opportunities, as growth certainly will not

follow from continued rate reductions . The key to future

growth will be innovation coupled with hard data . While

capital remains plentiful, primary insurers’ growth will

not broadly translate into reinsurance growth . Reinsurers

must develop value propositions and seek partnership

opportunities to help primary insurers grow into new markets

and in new ways that they could not do by themselves .

0

45

90

135

180

20132012201120102009200820072006200520042003

147 142 142 142153

137 140 145155

165170

Aon Benfield 15

Last year Aon Benfield introduced to the Study a detailed screening process that we employ to identify potential markets worth exploring for realistic growth opportunities .

Our analysis entails an evaluation of basic insurance economics,

such as country market scale and insurance penetration, country

profitability and loss ratio volatility, and overall out or under

performance relative to other opportunities . We couple those

basics with an understanding of the larger macroeconomic

environment including population changes, GDP measures,

and an understanding of the legal and regulatory systems .

Finally by combining this fact based information with qualitative

feedback from Aon’s local teams we can identify attractive

opportunities in each country . Our process reveals specific

opportunities from which to form executable growth strategies .

Aon Benfield has expanded the analysis this year by introducing

five year projected insurance premiums in each country,

which we have added to the Country Opportunity Index

on the next page . We have selected and analyzed several

specific trends that we are seeing in the market, including

auto, health, crop, and cyber insurance . Based on our

experience with carriers, reinsurers, agents, brokers, and other

insurance service providers, we highlight some of the key

trends and emerging insurance opportunities in each area .

Profitability

Scale

Growth

Demographics

Political Stability

Regulation

Broker Surveys

Contender Geographies Deep dive on strategy, organic growth and M&A opportunities

Uncovering Growth Opportunities

16 Insurance Risk Study

Country opportunity indexTo summarize and sort between the various countries

outlined in this section, we have updated our

Country Opportunity Index . The index identifies

countries with a desirable mix of profitability,

growth potential and a relatively stable political

environment . For growth potential we used the

projections shown on pages 10 to 14 of the Study .

The table displays the top 50 P&C markets ranked

by the Index and divided into quartiles .

Ten of the thirteen countries in Quartile 1 were also

in the top quartile last year . Singapore fell from the

top spot last year to the number three position, as

we estimated its projected premium growth to be

less than its recent history . Saudi Arabia is now the

top country according to our Index, with a recent

combined ratio of 91 .5 percent, strong projected

growth of 8 .1 percent, and only modest political risk .

The new entrants to the top quartile are all in

Asia Pacific: Hong Kong, China, and Australia .

China showed the biggest overall increase on the

Index, driven by a combined ratio improvement

from 101 .7 percent down to 98 .7 percent .

Geography is one factor when considering a growth

strategy . Another is opportunities created by

advances in insurance products . The next section of

the Study will delve into several insurance markets

where we see significant changes at work—and

with them, significant opportunity for insurers to

differentiate and create value for their clients .

Aon Benfield country opportunity index

5yr Cumulative Net Combined

Ratio

5yr Annualized Projected

Growth RatePolitical Risk Assessment

Quartile 1

Saudi Arabia* 91.5% 8.1% Medium Low

Ecuador* 86.9% 7.8% High

Singapore* 88.9% 4.6% Low

Hong Kong 98.6% 7.0% Low

Malaysia* 90.7% 6.8% Medium

Indonesia* 88.2% 5.7% Medium

Nigeria* 80.2% 4.4% Medium High

China 98.7% 11.2% Medium

Chile* 95.6% 5.5% Medium Low

South Africa* 87.6% 4.4% Medium

Norway* 89.6% 2.9% Low

Brazil* 85.7% 3.7% Medium

Australia 99.7% 4.4% Low

Quartile 2

Switzerland* 97.1% 3.2% Low

United Arab Emirates* 88.1% 2.5% Medium Low

Thailand 101.0% 7.3% Medium

Sweden* 91.1% 2.4% Low

Taiwan 97.2% 3.3% Medium Low

Mexico 96.9% 4.2% Medium

New Zealand 120.5% 6.7% Low

Morocco 97.8% 4.4% Medium High

Canada 99.0% 2.9% Low

India 118.5% 7.0% Medium

Denmark 93.5% 1.6% Low

Argentina 104.8% 6.4% High

Quartile 3

Poland 95.8% 2.2% Medium Low

South Korea 101.1% 3.7% Medium Low

Russia 88.7% 1.7% Medium

Finland 100.6% 2.8% Low

Colombia 108.9% 6.1% Medium

Israel 108.7% 3.9% Medium Low

Luxembourg 101.9% 2.8% Low

Germany 99.0% 2.1% Low

Austria 99.0% 1.8% Low

United States 101.9% 2.7% Low

Bulgaria 90.3% 0.9% Medium

Japan 103.5% 2.8% Medium Low

Quartile 4

Czech Republic 91.0% 0.2% Medium Low

France 98.9% 1.5% Medium Low

Turkey 105.1% 3.1% Medium

United Kingdom 101.2% 2.3% Medium Low

Belgium 99.0% 1.6% Medium Low

Portugal 92.7% 0.6% Medium

Venezuela* 96.9% 1.3% High

Spain 92.5% -0.1% Medium

Netherlands 101.0% 0.8% Low

Italy 98.8% 0.4% Medium

Greece 100.7% 0.9% High

Ireland 101.0% 0.5% Medium

Romania 111.8% 1.1% Medium High

*Indicates top quartile performer in 2013. Index defined in Sources and Notes.

Aon Benfield 17

The insurance industry is evolving rapidly . We are witnessing long term shifts that are changing the risks that property casualty companies insure . Cars are becoming safer . Employers face rapidly rising health care costs . Hardly a week goes without news of a new cyber attack . Advances in modeling are facilitating the growth of the international crop insurance market . And technology is posing new opportunities and risks for individuals and businesses . As the world is becoming more connected, it is also becoming riskier . These shifts present challenges, but also opportunities for insurers .

Auto trendsPersonal auto insurance, which for many years has been the

stable cash flow product of the property casualty universe,

is currently undergoing a revolution due to advances in

technology .

Cars today are significantly safer than those that our parents

drove . The Economist reports that 90 percent of car crashes

are caused by human error . As a result, recent innovations

in vehicle safety have focused on mitigating the effects of

human error or negligence . The results speak for themselves:

the U .S . has seen a 15 percent reduction in crashes for cars

with an automatic braking system for example . Between

2000 and 2011, driver deaths due to rollover crashes have

fallen more than 50 percent for passenger cars . And for

SUVs, the death rate has fallen roughly 90 percent .

People in large metropolitan areas are changing the way

they get around, from drive share programs to semi-

private car services such as Uber and Lyft . This is forcing

the auto insurance industry to think about how to create

and better price policies for uberX and Lyft drivers, who

need a commercial policy when they have passengers and

personal policies when they do not . Recent incidents have

posed questions about how these policies overlap .

Telematics and usage-based insurance (UBI) are becoming

widespread across the industry, with many of the largest U .S .

and U .K . auto insurers now having some form of UBI . Insurers

believe UBI will allow them to better segment price and risks

accordingly . Good drivers should benefit, as in theory drivers

who opt for UBI will pay less while other drivers’ rates will

increase . While the potential discount varies by carrier and

driver, the average quoted is 30 percent . Smaller insurers are

struggling to enter the UBI market, as they lack the scale to

offset the up-front investment in telematics infrastructure .

Companies are seeking ways to better leverage the data they

have accumulated from UBI . Two commonly cited applications

are teen driving and commercial trucking monitoring . And the

data accumulated from UBI may not only help to sell additional

insurance products, but may also be monetized by companies

outside the insurance industry . While vast amounts of data exist,

companies are only beginning to understand its full value .

The insurers that have been successful in growing are doing

so with data . Through market segmentation and targeted

advertising, auto specialist insurers in the U .S . have expanded

their market shares—growing at an average annual rate of 7

percent—while traditional personal lines insurers’ premium

has on average been static over the past five years .

Looking further ahead, driverless cars have the potential to

radically change the business model for auto insurers . Personal

auto insurance is 45 percent of global premium, and it has

long provided ballast and stability for multiline insurers . An

insurance world without this ballast would have very different

risk dynamics . For example, we estimate that without personal

auto, loss ratio volatility for the U .S . market would have been

nearly 40 percent higher for the period 1995 to 2013 .

Such changes, while not on the immediate horizon, could

increase industry capital intensity and lower premium to

surplus ratios by more than 30 percentage points, from

0 .84x to 0 .50x . We estimate that surplus needed in the

U .S . to support personal auto is USD100 to 125 billion .

The changing dynamics of the auto industry do not

foreshadow the death of the auto insurance industry but

do represent a clear emerging risk . Insurers need to keep

pace with the changes and innovate accordingly .

Insurance Trends: Risks and Opportunities

18 Insurance Risk Study

U.S. health insurance marketIn 2014, the individual mandate of the Affordable Care Act—

aka “Obamacare”—came into effect . With the ACA, state-run

public health care exchanges have become operational, and

as of May 2014 approximately 20 million Americans have

purchased insurance through these public exchanges . At

the same time, and with much less controversy, a revolution

has been taking place in the private health care insurance

market—the advent of corporate health care exchanges .

Aon Hewitt has been a pioneer in this market, with 330,000

employees enrolled in its Corporate Health Exchange for 2014 .

Currently, about 60 percent of U .S . workers who receive

health insurance through their employers are covered under

self-insured plans . For companies with over 5,000 employees

this number is even higher—by some estimates as many as

94 percent of larger employers run self-insured health plans .

In these cases, the role of the health insurer is simply to

process payments and bill claims back to the employer—hence

these plans are called Administrative Services Only plans .

But over the past several years, several significant

developments in the industry have begun to change how

people buy health insurance and increase the flow of

insurance premiums into the market . These changes are a

real and material opportunity for the insurance industry .

Health care costs have risen at a 7 percent annual rate during

the 10 years to 2012, with long term trends estimated at

8 to 9 percent per year . At most companies, revenue growth

has not kept pace with this expansion in costs . Given these

trends, companies are seeking ways to manage costs while

continuing to provide essential benefits to their employees .

One such way is to rethink the traditional model of a self-

insured health plan . This trend has led to the creation of private

health care exchanges . Under this model, companies enroll

in a private exchange, which allows insurance companies

to compete for their employees’ health care insurance

business . Insurers bear the risk from these policies .

The private exchange market is still small; analysts at JP Morgan

estimate that less than 1 percent of active employees will be

enrolled in private exchanges in 2014 . Yet interest is high,

with an average of 40 percent of employers in recent surveys

saying they are considering a switch to a private exchange .

The implications for growth in the private health care insurance

market are significant . We estimate that if 20 percent of U .S .

employers move to private exchanges, then an additional

USD350 billion in premium will flow into the private health

insurance market . Twenty percent is the minimum level

of interest quoted in recent surveys . The median is 33

percent—if one in three U .S . employers move to a private

exchange, this will generate an additional USD500 billion

of premium flow into the market . As a reference point, this

number is roughly the size of the entire U .S . property casualty

insurance market, as shown in the statistics on page seven .

While the potential premium growth can seem staggering,

insurers must also consider the capital required to support

this growth . We estimate that the U .S . health insurance

industry’s capital adequacy, as defined by A .M . Best’s BCAR

model, is currently 225 percent—roughly in line with the

U .S . property casualty industry’s 230 percent . Depending

on how much premium flows into private exchanges,

we estimate that health insurers’ capital adequacy could

fall between 107 and 128 percent if capital levels remain

constant . To maintain a 225 percent capital adequacy level,

insurers will need to raise a significant new level of capital:

USD105 billion at the minimum, and USD150 billion at the

median . The table below summarizes these estimates .

Impact of private exchanges on health insurers

% of Employers Moving to Corporate Exchanges

New health insurance premium

(USD billions)

Additional required capital to maintain BCAR

(USD billions)

20% (minimum) 350 105

33% (median) 500 150

A capital demand of USD105 billion to USD150 billion is a

significant opportunity not only for investors but also for

property casualty insurers that are currently sitting on record

levels of capital and actively seeking new opportunities in

which to deploy it . For traditional property casualty insurers,

it is an opportunity to diversify into new lines of (potentially

uncorrelated) business . For reinsurers it is an opportunity as

well . Reinsurance can provide a substitute to traditional capital

and help health insurers lower their capital requirements by

sharing risk with the reinsurers . The U .S . group health insurance

market has only three insurers who are truly national in scope,

so a significant amount of the “new” commercial premium could

fall to regional carriers who are bigger users of reinsurance .

Aon Benfield 19

Earlier, we mentioned the potential market changes that could

take place if driverless cars cause the personal auto insurance

market to shrink . Perhaps health insurance will become the

new “ballast” to property casualty commercial lines volatility

in the future .

U.S. cyber insurance marketIn the past year, cyber risk has come into the mainstream as a

significant threat to businesses of all sizes . The data breach at

Target affected as many as one-third of all U .S . consumers, and the

Heartbleed bug exposed weaknesses in 17 percent (500,000) of

the internet’s secure web servers . Both the frequency and severity

of cyber attacks are on the rise . Attitudes are changing; businesses

now see a data breach as inevitable: not if but when .

Different sources count data breaches differently but all agree

there is an increasing trend . Symantec released a study counting

253 breaches, a 62 percent increase over 2012 . The Identity

Theft Resource Center counted 614 data breaches last year,

rising at an annual trend rate of 11 percent, as shown below .

Number of U.S. data breaches by year

All studies suggest that 2013 was a banner year, of sorts, for data

breaches . Notably, 2013 saw eight mega breaches, each more

than 10 million records; the previous high was the five breaches

in 2011, according to Symantec . In total, 552 million identities

were exposed—roughly 7 .8 percent of the world population .

And while breaches are increasing, the cost of a breach is

increasing as well . Data from the Ponemon Institute suggest

that the cost of the average breach is now USD5 .9 million—and

this number excludes breaches of more than 100,000 records .

The Ponemon study also indicates that customers are fleeing

from breached companies more than in the past: lost business

following a breach rose 15 percent last year .

Finally, the Ponemon study included a shocking statistic: that

roughly 19 percent of businesses are expected to have a data

breach in the next 24 months . These percentages vary by

industry, but every company in today’s economy is vulnerable to

the risks of a cyber attack .

Average total cost of a data breach (USD millions)

Excludes breaches with more than 100,000 records

From its beginnings 15 years ago, cyber insurance has

now become a standard product offered by many large

commercial insurers . Common coverage includes third-

party liability protection as well as first-party indemnity

protection for breach response expenses, business

interruption, forensics, and cyber extortion . Although

statistics on the business are difficult to come by, cyber

insurance has generally been seen as profitable . That said,

a growing number of entrants are offering the coverage,

and prices are beginning to fall as competition expands .

Takeup of cyber insurance is increasing, and the U .S . cyber

market is now estimated at roughly USD1 .5 billion in gross

written premium . Aon Risk Solutions has seen cyber premium

rise at a compound annual growth rate of 38 percent over the

last five years, according to data from the Aon GRIP platform .

Nearly one-third of companies buy some kind of cyber policy .

Main Street businesses have been slower to adapt than large

corporations . This presents a significant market opportunity for

enterprising insurers, given that small and medium enterprises

are often the most vulnerable to a cyber attack . A study by

Verizon found that 71 percent of cyber attacks are targeted

at companies with fewer than 100 employees . Moreover,

attacks against small businesses shot up by 91 percent in

2013 . Small businesses often lack the time and resources to

develop sophisticated cyber risk management strategies .

0

200

400

600

800

201320122011201020092008200720062005

0

2

4

6

8

201420132012201120102009200820072006

+11% trend

+3% trend

20 Insurance Risk Study

Many smaller businesses are responding to such limitations by

outsourcing their network security to managed security service

providers (MSSPs) . While MSSPs can provide valuable services

to help companies protect themselves, they are not insurers .

Insurers have a vital role to play, by providing indemnity

protection as well as sharing their security expertise in this area .

Current cyber insurance policies only provide basic protection .

Cyber insurance for large companies has focused primarily

on first party indemnity protection . This is not surprising,

given that since 2004 companies have been required to

notify customers in the event their personal information is

compromised—and the costs of doing so can be considerable .

Yet the potential for other kinds of expense is significant .

Increasingly, lawyers are pursuing directors and officers in the

event that a company fails to protect its data . Target’s data

breach has generated at least 40 lawsuits against the retailer .

Moreover, the current cyber insurance policies focus solely on

the direct costs and ramifications of a data breach . They do not

contemplate the risk a cyber attack can cause other kinds of

damage . Most property and general liability policies exclude

cyber risk . The first cyber difference-in-conditions policy to fill

such coverage gaps was just made available earlier this year .

For Main Street, the coverage options can be confusing,

and risk leaving the buyer exposed should an actual event

occur . Many insurers will include data breach coverage in

their business owners policies but subject to a USD10,000 or

USD25,000 limit . Given the size of the potential costs discussed

previously, such coverage limits are very low, and may create

a false sense of security that businesses are “covered .”

Cyber coverage must evolve in order to meet the needs of

buyers, and underwriting practices will need to evolve with it .

Cyber underwriting is currently focused more on compliance

with industry standard practices than on actual risk assessment .

And cyber risk still has an image challenge to overcome: often, it

is seen by companies merely as an IT problem, not tied into the

larger ERM framework . This suggests a failure by corporate risk

managers to translate cyber exposure into a potential bottom-

line impact that executives can understand and manage .

China crop insuranceGlobal population growth and emerging middle classes are

driving a rising demand for agricultural products including

those used for animal feed .

China is the second largest crop insurance market globally,

with USD3 billion premium of a global USD22 billion market .

The U .S . market is much larger, and fairly mature . The China

market, in contrast, is primed for growth . China’s population

is expected to grow by 4 percent by 2017 totaling nearly 1 .4

billion people . Even more impressive, GDP is expected to grow

by 50 percent by 2018 . These significant expectations, coupled

with the Chinese government’s focus on providing government

support to the agricultural industry and rural population,

warrant attention when considering growth opportunities .

Global crop insurance premium (USD billions)

0

2

4

6

8

10

12

14

Latin AmericaIndiaCanadaEuropeChinaUSA

Aon Benfield 21

Since 2004, China crop premium has quadrupled, from

RMB5 billion in 2007 to RMB20 billion in 2012 . The business

has also been relatively profitable, with an average 63 percent

loss ratio over these years . Considering China’s trajectory, we

expect the crop insurance market to continue growing quickly .

The size of the crop insurance opportunity and the number

of players in the market are simultaneously increasing . In the

last ten years, four new specialized agricultural insurance

companies were established in China that now collectively

write more than a quarter of the market . This growth has

not come without resistance: the largest crop insurers in

the market have been active for almost 30 years, and have

worked to limit competition and protect their market share .

For carriers seeking to enter this market, Aon Benfield can

provide detailed and data-driven support to help navigate the

vast and dynamic China agricultural landscape . The Aon Crop

Reinsurance System (ACReS) is built on 30+ years of county-level

yield data at the crop level, 60 years of city and provincial level

data and weather data from 160 weather stations . It is the only

model in the market built at this level of granularity . The ACReS

model provides PMLs per province for an insurer’s major crop

portfolio . It also incorporates correlation coefficients between

provinces so that we can model multi-province portfolios .

China premium and claims performance

Additionally, ACReS is a tool to help insurers grow

strategically in China, because it identifies the varying risk

by region and allows insurers to select those provinces

with an acceptable risk level for future growth . The model

demonstrates the effect of changes in policy terms or exposure

levels on underwriting results as well as the efficiency

and adequacy of various reinsurance arrangements .

Prem

ium

/cla

ims

(RM

B b

illio

ns)

Loss ratio

ClaimsLoss ratio Premium

0

5

10

15

20

201120102009200820072006200540%

50%

60%

70%

80%

22 Insurance Risk Study

The first part of the Study focused on insurance premium, profitability, and growth opportunities . Once insurers have set a strategy and identified opportunities for growth, they must address the tactical matters of operations: underwriting, claims and risk management . Insurance is a tradeoff between risk and potential return, and we now turn to the “risk” side of the equation . Measuring the volatility and correlation of risk has always been the core of the Study .

The 2014 edition of the Study quantifies the systemic risk by

line for 49 countries worldwide . By systemic risk, or volatility,

we mean the coefficient of variation of loss ratio for a large

book of business . Coefficient of variation (CV) is a commonly

used normalized measure of risk defined as the standard

deviation divided by the mean . Systemic risk typically comes

from non-diversifiable risk sources such as changing market rate

adequacy, unknown prospective frequency and severity trends,

weather-related losses, legal reforms and court decisions, the

level of economic activity, and other macroeconomic factors . It

also includes the risk to smaller and specialty lines of business

caused by a lack of credible data . For many lines of business

systemic risk is the major component of underwriting volatility .

The systemic risk factors for major lines by region appear

on the facing page . Detailed charts comparing motor

and property risk by country appear below . The factors

measure the volatility of gross loss ratios . If gross loss

ratios are not available the net loss ratio is used .

Global Risk Parameters

Coefficient of variation of gross loss ratio by country

ThailandSingapore

MexicoPeru

PhilippinesGreece

Hong KongBrazil

IndonesiaTaiwan

Dominican RepublicPakistanVietnamRomania

NicaraguaPanamaSlovakia

ArgentinaU.S.

South KoreaHondurasColombia

UruguayEl Salvador

TurkeyPoland

HungaryEcuador

IndiaChile

MalaysiaJapanChina

FranceSwitzerland

SpainCanada

U.K.IsraelItaly

AustriaBolivia

AustraliaGermany

South AfricaNetherlands

DenmarkVenezuela

PhilippinesGreece

Hong KongRomania

NicaraguaPanama

South AfricaSlovakia

IndonesiaDenmarkEcuador

VenezuelaSingapore

TurkeyColombia

ChinaU.S.

CanadaHonduras

PakistanPoland

ArgentinaDominican Republic

U.K.BrazilPeru

VietnamIndiaItaly

UruguayMexico

ChileMalaysia

NetherlandsEl Salvador

Czech RepublicGermany

AustriaBolivia

AustraliaSpain

HungarySwitzerland

FranceJapanIsrael

South KoreaTaiwan

Thailand12%

10%

12%14%15%16%

18%18%18%

21%22%22%23%25%

27%33%33%33%33%33%34%34%35%35%

40%40%

36%39%

42%42%

52%53%54%55%57%57%58%

61%66%

68%68%69%

77%83%85%

99%

124%

3%5%5%5%6%6%7%8%8%8%8%8%9%9%9%9%10%10%11%11%12%12%13%13%13%13%13%14%14%14%15%15%16%16%16%17%18%18%

21%

19%19%

22%22%

43%

22%34%

37%

50%70%

Americas

Asia Pacific

Europe, Middle East & Africa

110%

Motor Property