![€¦ · Web viewBACKGROUND. T. riple fixed-dose combinations (inhaled . glucocorticoid [ICS]/ long-acting mus. carinic antagonist [LAMA]/ long-acting β. 2-agonist [LABA]) for](https://static.fdocuments.us/doc/165x107/60b248cbf19f060b930e921f/web-view-background-t-riple-fixed-dose-combinations-inhaled-glucocorticoid.jpg)

Languages

Pages

Legal

An Expert Drug Delivery Company Skyepharma PLC Peter Grant, CEO

An Expert Drug Delivery Company

2 June 2014

The contents of this presentation and the information which you are given at the time of the presentation have not been approved by an authorised person within the meaning of

the Financial Services and Markets Act 2000 (the “Act”). Reliance on this presentation for the purpose of engaging in investment activity may expose an individual to a

significant risk of losing all of the property or other assets invested. This presentation does not constitute or form part of any offer for sale or subscription or solicitation of any

offer to buy or subscribe for any securities in Skyepharma PLC (the “Company”) nor shall it form the basis of or be relied on in connection with any contract or commitment

whatsoever. No reliance may be placed for any purpose whatsoever on the information contained in this presentation and/or opinions therein. This presentation is exempt from

the general restriction (in section 21 of the Act) on the communication of invitations or inducements to engage in investment activity on the grounds that it is made to:- (a) persons

who have professional experience in matters relating to investments who fall within Article 19(1) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005

(the “Order”); or (b) high net worth entities and other persons to whom it may otherwise lawfully be communicated, falling within Article 49(1) of the Order (all such persons

together being referred to as “relevant persons”). Any person (whether relevant persons or otherwise) are recommended to seek their own independent financial advice from a

person authorised for the purposes of the Act before engaging in any investment activity involving the Company’s securities.

This presentation does not constitute or form part of any offer or invitation or inducement to sell, issue, purchase or subscribe for (or any solicitation of any offer to purchase or

subscribe for) the Company’s securities in the UK, US or any other jurisdiction and its distribution, does not form the basis of, and should not be relied on in connection with, any

contract or investment decision in relation thereto nor does it constitute a recommendation regarding the Company’s securities by the Company or its advisers and agents.

Nothing in the presentation shall form the basis of any contract or commitment whatsoever. The distribution of this presentation outside the UK may be restricted by law and

therefore persons outside the UK into whose possession this Presentation comes should inform themselves about and observe any such restrictions as to the distribution of this

presentation.

This presentation contains "forward-looking" statements, beliefs or opinions, including statements with respect to the business, financial condition, results of operations and plans

of the Company. These forward-looking statements involve known and unknown risks and uncertainties, many of which are beyond the Company’s control and all of which are

based on the current beliefs and expectations of the directors of the Company about future events. Recipients should note that past performance is not necessarily an indication

of future performance. Forward-looking statements are sometimes identified by the use of forward-looking terminology such as "believes", "expects", "may", "will", "could",

"should", "shall", "risk", "intends", "estimates", "aims", "plans", "predicts", "continues", "assumes", "positioned" or "anticipates" or the negative thereof, other variations thereon or

comparable terminology or by discussions of strategy, plans, objectives, goals, future events or intentions. These forward-looking statements may and often do differ materially

from actual results. The significant risks related to the Company’s business which could cause the Company’s actual results and developments to differ materially from those

forward-looking statements are discussed in the Company’s Annual Report and other filings. They appear in a number of places throughout this presentation and include

statements regarding the intentions, beliefs or current expectations of the directors of the Company with respect to future events and are subject to risks relating to future events

and other risks, uncertainties and assumptions relating to the Company's business, concerning, amongst other things, the results of operations, financial condition, prospects,

growth and strategies of the Company and the industry in which it operates. The Company will not publicly update or revise any forward-looking statements, either as a result of

new information, future events or otherwise.

In considering the performance information contained herein, recipients should bear in mind that past performance is not necessarily indicative of future results, and there can be

no assurance unrealised return projections will be met. Certain of the past performance information presented herein may not be representative of all transactions of a given type.

Actual events could differ materially from those projected herein and depend on a number of factors, including the success of the Company’s development strategies, the

successful and timely completion of clinical studies, securing satisfactory licensing agreements for products, the ability of the Company to obtain additional financing for its

operations and the market conditions affecting the availability and terms of such finances.

The Company reports under IFRS. Where foreign currency equivalents have been provided for convenience in this presentation, the exchange rates applied are those used in

the relevant financial statements from which the figures have been extracted.

2

Disclaimer

3

Business summary

• Proven scientific expertise + validated proprietary technologies

• Track record of diverse and complex inhalation and oral pharmaceutical product development

• Independent partner for companies worldwide

Drug delivery experts

with global reach

• Long-term royalty and supply agreements

• Include 16 approved products

• Momentum from multiple recent product approvals

Recurring revenues and strong growth

potential

• flutiform® - up to €45m+ of further* milestones and royalties from Europe, Japan, RoW, plus product supply

• GSK’s Relvar®/Breo®, Anoro® - royalties up to £9m a year

• Pacira’s EXPAREL® - up to $52m of further milestones plus 3% share of relevant net sales

New revenue streams

Listed on LSE (SKP.L), HQ: London, UK, R&D: Muttenz, Switzerland * Post 31 December 2013

• 2013 revenues and operating profits ahead of market expectations

• Substantial progress with flutiform®, now approved in 29 countries

• Significant revenue-generating potential from other recent approvals

• Strong share price momentum – market cap ~ $437m*

4

Operating highlights

* As at 29 May 2014

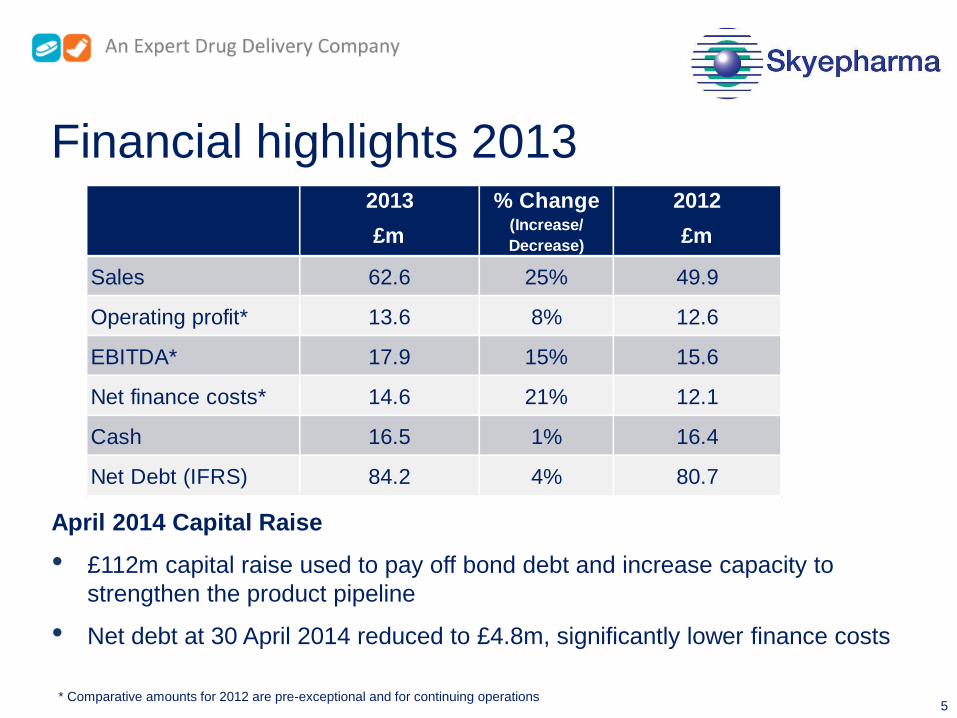

April 2014 Capital Raise

• £112m capital raise used to pay off bond debt and increase capacity to

strengthen the product pipeline

• Net debt at 30 April 2014 reduced to £4.8m, significantly lower finance costs

5

Financial highlights 2013

* Comparative amounts for 2012 are pre-exceptional and for continuing operations

2013 % Change 2012

£m(Increase/

Decrease)£m

Sales 62.6 25% 49.9

Operating profit* 13.6 8% 12.6

EBITDA* 17.9 15% 15.6

Net finance costs* 14.6 21% 12.1

Cash 16.5 1% 16.4

Net Debt (IFRS) 84.2 4% 80.7

Long-term agreements – recurring revenues

2013: 72% recurring

revenues from long-

term agreements

6

Global potential from 8 recent product approvals

flutiform®

23 European Countries

RAYOS®

U.S.

EXPAREL®

U.S.

Breo® Ellipta®

U.S.

flutiform®

Australia

flutiform®

RoW - Israel, HK, S Korea

flutiform®

Japan

Paxil CR™

Japan

Requip® Once-a-day

Japan

Relvar® Ellipta®

Japan

Relvar® Ellipta®

Europe

Anoro™ Ellipta ®

U.S.

NASDAQ:PCRX NASDAQ:HZNP LSE:GSK TOKYO:4569

7

Incruse®

Europe

Incruse® Ellipta™

U.S.

Anoro® Ellipta®

Europe

flutiform®

Argentina

Key

Inhalation

Oral

Other

Inhalation Product Primary Indication Licensee / Partner

flutiform® – EU & other / Japan Asthma Mundipharma / Kyorin

†Relvar® / Breo® Ellipta® COPD (U.S.)/Asthma (Japan)/COPD & Asthma (Europe) GlaxoSmithKline

†Anoro™ Ellipta® - U.S., Europe COPD (U.S., Canada, Europe) GlaxoSmithKline

†Incruse® - U.S., Europe COPD (U.S.,Canada & Europe) GlaxoSmithKline

Revenues from 16 approved products

Oral Product Primary Indication Licensee / Partner

Xatral® OD / Uroxatral® BPH (urinary symptoms) Sanofi

Requip® Once-a-day Parkinson’s disease GlaxoSmithKline

Paxil CR™ Depression GlaxoSmithKline

Sular® Hypertension Shionogi

ZYFLO CR® Asthma Cornerstone Therapeutics

Coruno® Angina Therabel

Lodotra® / RAYOS® RA pain & stiffness Horizon Pharma

Triglide® Lipid disorders Shionogi

Madopar DR® Parkinson’s disease Roche

Diclofenac-ratiopharm® uno Pain / inflammation Teva

Other Products Primary Indication Licensee / Partner

Solaraze® Actinic keratosis Sandoz / Almirall

*EXPAREL® Pain management Pacira Pharmaceuticals

8

† Technology license, product not developed by Skyepharma *A product of Skyepharma’s former Injectable Business now Pacira Pharmaceuticals

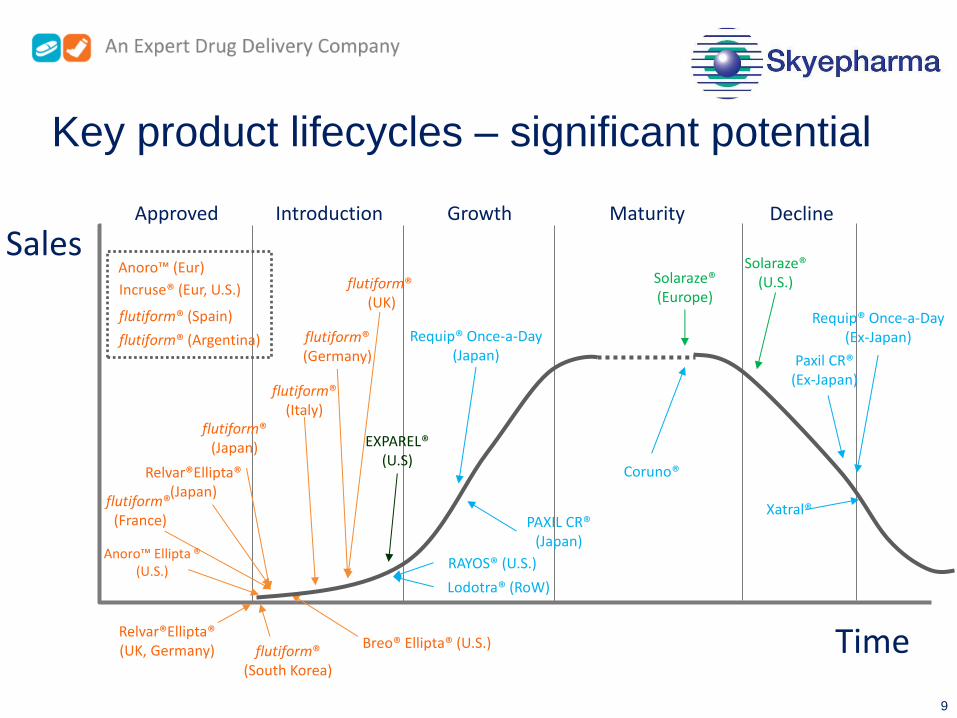

Key product lifecycles – significant potential

Sales

Time

Approved Introduction Growth Maturity Decline

Anoro™ (Eur)

Incruse® (Eur, U.S.)

flutiform® (Spain)

flutiform® (France)

Relvar®Ellipta® (Japan)

flutiform® (Japan)

flutiform® (Italy)

flutiform® (Germany)

flutiform® (UK)

EXPAREL® (U.S)

RAYOS® (U.S.)

PAXIL CR® (Japan)

Requip® Once-a-Day (Japan)

Solaraze® (Europe)

Solaraze® (U.S.)

Xatral®

Paxil CR® (Ex-Japan)

Requip® Once-a-Day (Ex-Japan)

Breo® Ellipta® (U.S.)

Coruno®

9

Lodotra® (RoW)

Anoro™ Ellipta ® (U.S.)

flutiform® (South Korea)

Relvar®Ellipta® (UK, Germany)

flutiform® (Argentina)

Proven oral platform

Oral drug delivery solutions and technologies used in 10 marketed products

Oral products incorporating Skyepharma technology achieved in-market sales of

approx. U.S.$3bn in past 5 years

Developing new drug delivery technologies to serve unmet needs

Technology Delivery solution Product examples

Geomatrix™ Family of 8 controlled release

mechanisms

Paxil CR, Requip® Once-a-day, ZYFLO CR,

Coruno, Sular®,

Diclofenac-ratiopharm-uno, Madopar DR

Geoclock™ Customised drug delivery with

pre-determined release delay LODOTRA® / RAYOS®, SKP-1041, SKP-1052

Gastroretention “Parachute” technology Xatral® OD / Uroxatral®

Improved

bioavailability

Several particle engineering

technologies Triglide®

11

Inhalation platform covering pMDI and DPI

• Global Asthma and COPD market U.S.$29.4bn*

• Broad range of R&D and clinical regulatory capabilities from pre-clinical

development through to post-approval supply and product support

• Proven formulation and device expertise

− Pressurised Metered Dose Inhaler (“pMDI”) approvals in more than 50

countries

− Dry Powder Inhaler (“DPI”) approvals in 31 countries including the U.S.

• pMDI flutiform®, conceived and developed by Skyepharma, already

approved in 29 countries

• DPI formulation, analytical and process development of new classes of

molecules for COPD and severe asthma for Janssen Biotech

(RespiVert)

* 2012 Market Source: Company analysis: i) Datamonitor COPD report, DMKC0047510, Publication Date: 19/08/2013 ii) Datamonitor Asthma report, DMKC0082148, Publication Date: 07/09/2012 iii) Extrapolation of main market sales to global numbers with a factor of 25% 12

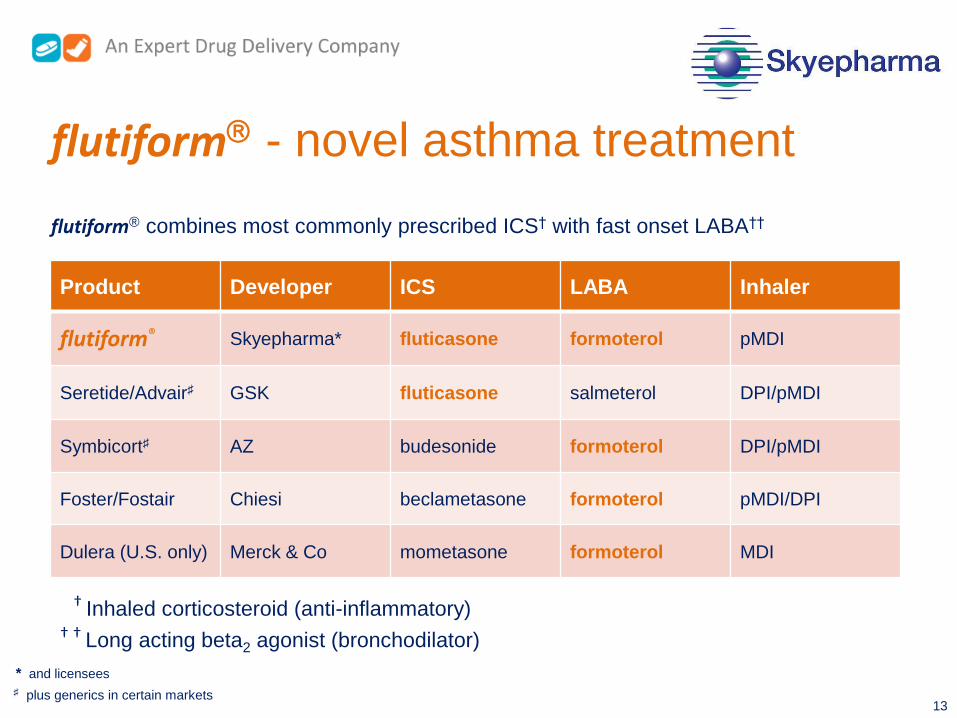

flutiform - novel asthma treatment

flutiform® combines most commonly prescribed ICS† with fast onset LABA††

Product Developer ICS LABA Inhaler

flutiform® Skyepharma* fluticasone formoterol pMDI

Seretide/Advair♯ GSK fluticasone salmeterol DPI/pMDI

Symbicort♯ AZ budesonide formoterol DPI/pMDI

Foster/Fostair Chiesi beclametasone formoterol pMDI/DPI

Dulera (U.S. only) Merck & Co mometasone formoterol MDI

* and licensees

† Inhaled corticosteroid (anti-inflammatory) † † Long acting beta2 agonist (bronchodilator)

♯ plus generics in certain markets 13

As needed rapid-acting β2 agonist

Treatment guidelines for asthma

Source: Global Strategy for Asthma Management and Prevention (updated 2013) – www.ginasthma.org http://www.ginasthma.org/uploads/users/files/GINA_Pocket2013_May15.pdf

Controller options

Low-dose inhaled ICS

Leukotriene

modifier

Low-dose ICS plus LABA

Medium-or high

dose ICS

Low-dose ICS plus leukotriene modifier

Low-dose ICS plus sustained release

theophylline

Medium-or high dose ICS plus LABA

Leukotriene modifier

Sustained release theophylline

Oral glucocorticosteroid

(lowest dose)

Anti-IgE treatment

Step 1

Select one Select one To Step 3 treatment select one or more

To Step 4 treatment add either

Step 2 Step 3 Step 4 Step 5

flutiform ® market

14

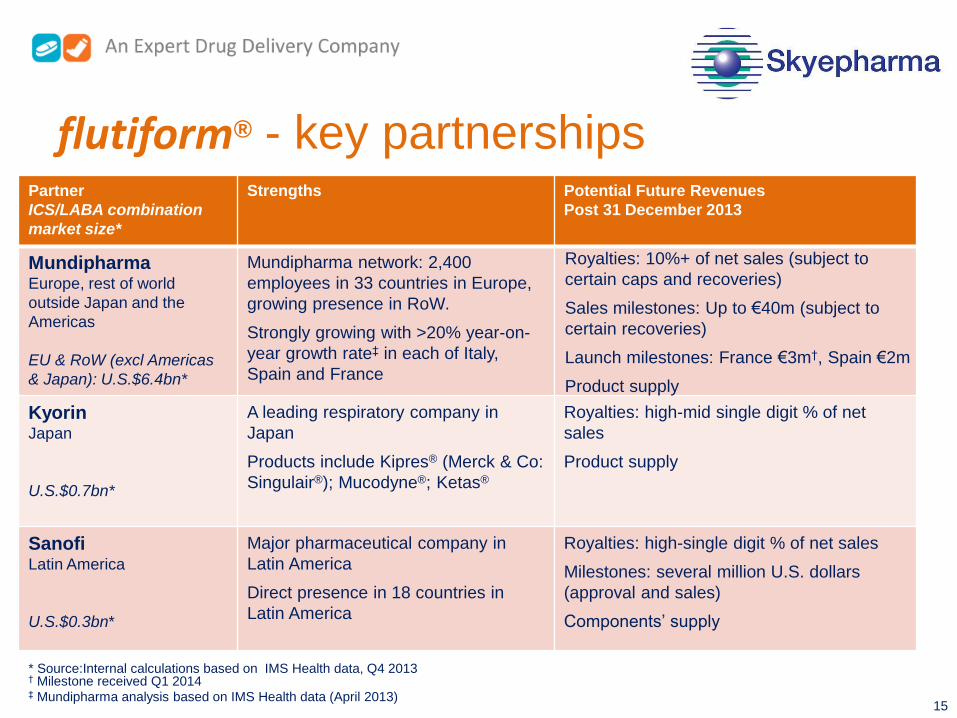

flutiform® - key partnerships Partner

ICS/LABA combination

market size*

Strengths Potential Future Revenues

Post 31 December 2013

Mundipharma Europe, rest of world

outside Japan and the

Americas

EU & RoW (excl Americas

& Japan): U.S.$6.4bn*

Mundipharma network: 2,400

employees in 33 countries in Europe,

growing presence in RoW.

Strongly growing with >20% year-on-

year growth rate‡ in each of Italy,

Spain and France

Royalties: 10%+ of net sales (subject to

certain caps and recoveries)

Sales milestones: Up to €40m (subject to

certain recoveries)

Launch milestones: France €3m†, Spain €2m

Product supply

Kyorin Japan

U.S.$0.7bn*

A leading respiratory company in

Japan

Products include Kipres® (Merck & Co:

Singulair®); Mucodyne®; Ketas®

Royalties: high-mid single digit % of net

sales

Product supply

Sanofi Latin America

U.S.$0.3bn*

Major pharmaceutical company in

Latin America

Direct presence in 18 countries in

Latin America

Royalties: high-single digit % of net sales

Milestones: several million U.S. dollars

(approval and sales)

Components’ supply

* Source:Internal calculations based on IMS Health data, Q4 2013 † Milestone received Q1 2014

15 ‡ Mundipharma analysis based on IMS Health data (April 2013)

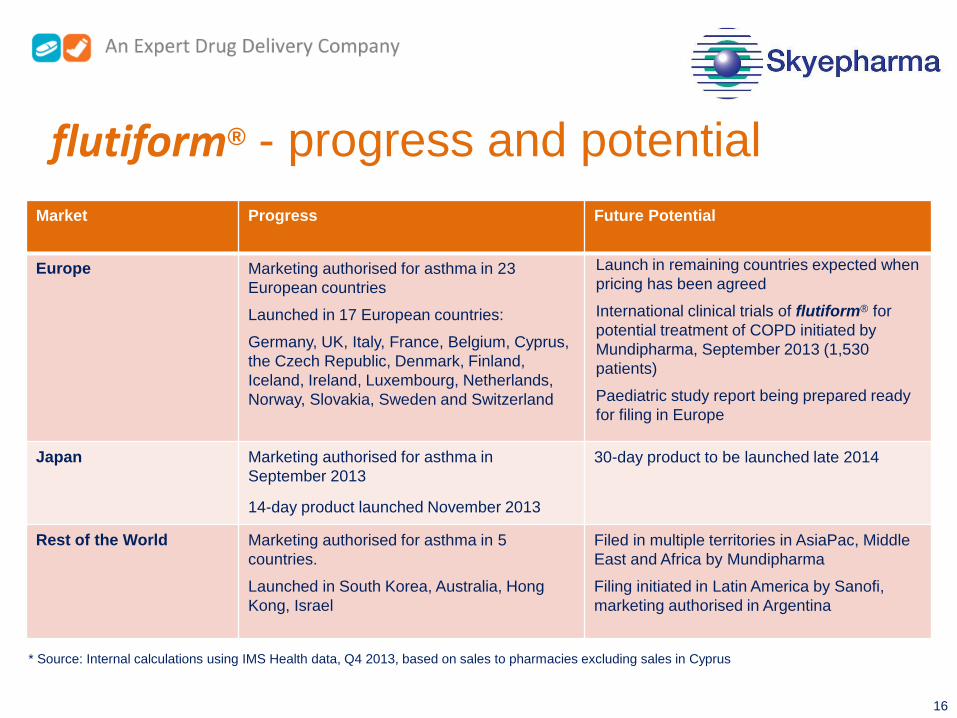

flutiform® - progress and potential

Market Progress Future Potential

Europe Marketing authorised for asthma in 23

European countries

Launched in 17 European countries:

Germany, UK, Italy, France, Belgium, Cyprus,

the Czech Republic, Denmark, Finland,

Iceland, Ireland, Luxembourg, Netherlands,

Norway, Slovakia, Sweden and Switzerland

Launch in remaining countries expected when

pricing has been agreed

International clinical trials of flutiform® for

potential treatment of COPD initiated by

Mundipharma, September 2013 (1,530

patients)

Paediatric study report being prepared ready

for filing in Europe

Japan

Marketing authorised for asthma in

September 2013

14-day product launched November 2013

30-day product to be launched late 2014

Rest of the World

Marketing authorised for asthma in 5

countries.

Launched in South Korea, Australia, Hong

Kong, Israel

Filed in multiple territories in AsiaPac, Middle

East and Africa by Mundipharma

Filing initiated in Latin America by Sanofi,

marketing authorised in Argentina

* Source: Internal calculations using IMS Health data, Q4 2013, based on sales to pharmacies excluding sales in Cyprus

16

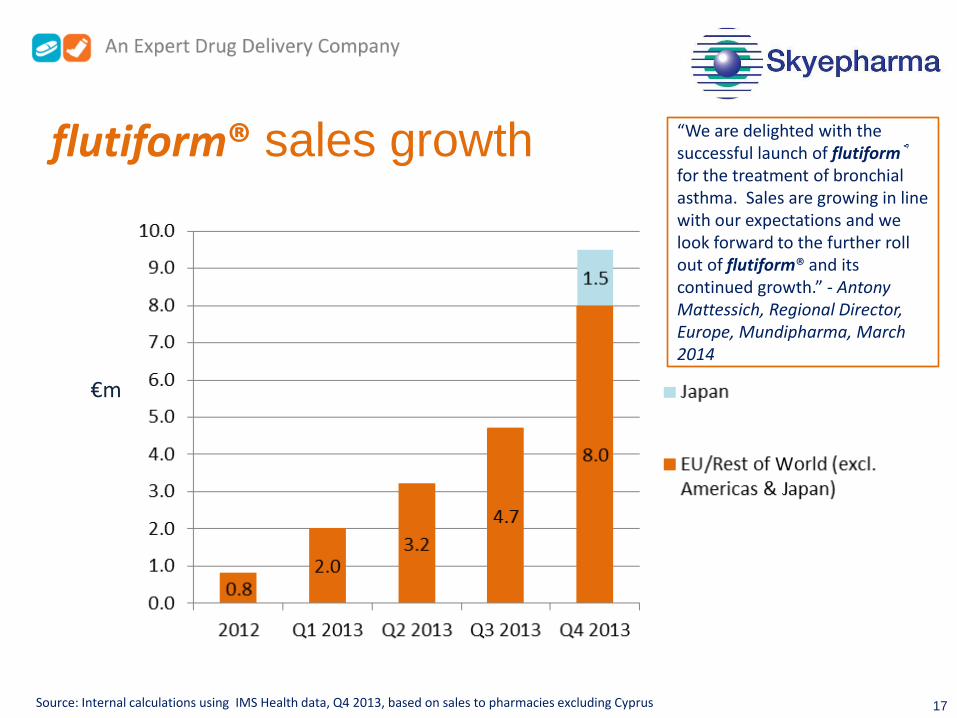

flutiform® sales growth

17

€m

Source: Internal calculations using IMS Health data, Q4 2013, based on sales to pharmacies excluding Cyprus

“We are delighted with the successful launch of flutiform® for the treatment of bronchial asthma. Sales are growing in line with our expectations and we look forward to the further roll out of flutiform® and its continued growth.” - Antony Mattessich, Regional Director, Europe, Mundipharma, March 2014

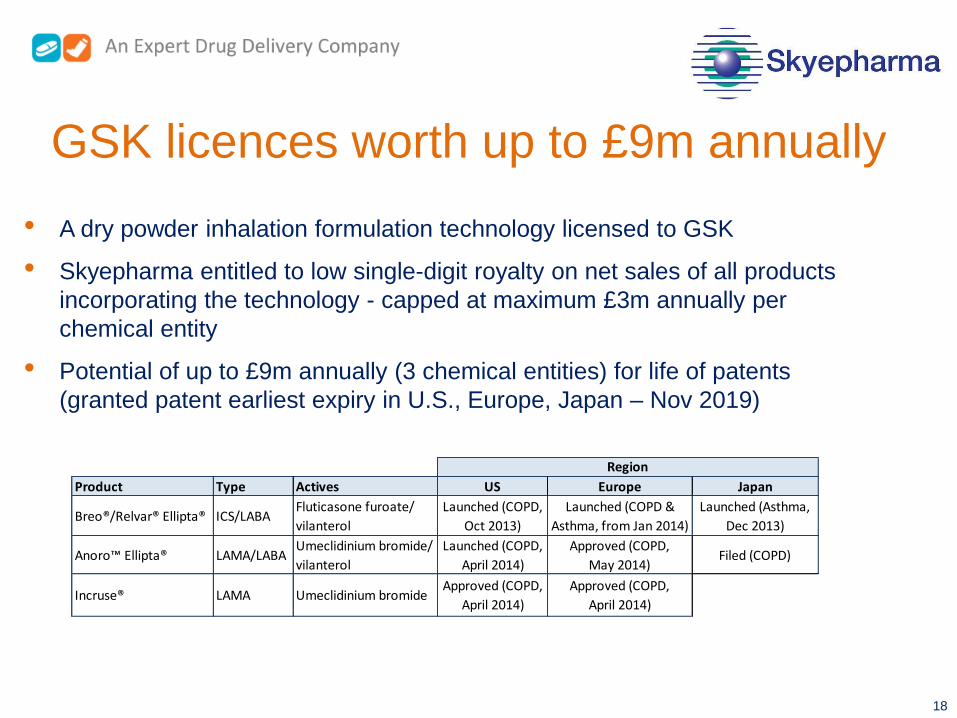

GSK licences worth up to £9m annually

• A dry powder inhalation formulation technology licensed to GSK

• Skyepharma entitled to low single-digit royalty on net sales of all products

incorporating the technology - capped at maximum £3m annually per

chemical entity

• Potential of up to £9m annually (3 chemical entities) for life of patents

(granted patent earliest expiry in U.S., Europe, Japan – Nov 2019)

18

Product Type Actives US Europe Japan

Breo®/Relvar® Ellipta® ICS/LABAFluticasone furoate/

vilanterol

Launched (COPD,

Oct 2013)

Launched (COPD &

Asthma, from Jan 2014)

Launched (Asthma,

Dec 2013)

Anoro™ Ellipta® LAMA/LABAUmeclidinium bromide/

vilanterol

Launched (COPD,

April 2014)

Approved (COPD,

May 2014)Filed (COPD)

Incruse® LAMA Umeclidinium bromideApproved (COPD,

April 2014)

Approved (COPD,

April 2014)

Region

• EXPAREL® developed by Skyepharma’s former Injectable Business,

now Pacira Pharmaceuticals†

− Long-acting bupivacaine for post-surgical pain management

− Studies show analgesia delivered for up to 72 hours post-surgery

− sNDA filed for nerve block indication in May 2014

EXPAREL® - milestones plus 3% share of net sales

* On a cash-received basis † NASDAQ:PCRX Market Cap $2.8bn at 29 May 2014

• Launched in U.S. April 2012; 2013 sales

$76.2m; Q1 2014 $34.4m

• Skyepharma eligible for 3% of net sales* in

U.S., Japan and major European countries

until patents expire (anticipated Nov 2018)

• Further contingent milestones of up to $52m

• $8m when annual net sales reach $100m

• $8m when annual net sales reach $250m

• $32m when annual net sales reach $500m

• $4m on launch in major EU country

19

0

5

10

15

20

25

30

35

40

Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14

Quarterly Sales, $ Millions

Pipeline product candidates (disclosed)

Oral Product Primary Indication Feasibility Phase

I

Phase

II

Phase

III Filed Licensee / Partner

SKP-1041 Sleep

maintenance Somnus

SKP-1052 Nocturnal

hypoglycaemia Available

Inhalation Product Primary Indication Feasibility Phase

I

Phase

II

Phase

III Filed Licensee / Partner

flutiform (ROW) Asthma o o Mundipharma

flutiform (LATAM) Asthma o Sanofi

flutiform (Europe) COPD Mundipharma

Anoro (Japan) COPD GlaxoSmithKline

flutiform (U.S.) Asthma † Available

flutiform (Canada) Asthma Available

Various Asthma/COPD o o Janssen Biotech

(RespiVert)

Mundipharma has filed marketing authorisation applications in some Rest of World markets

† Complete response letter received January 2010 and additional studies are required

o Partial 20

• Growing momentum from recent launches and approvals

• Transactions significantly reduce debt and enhance future earnings

• Increased capacity to invest in product and technology development and

corporate opportunities

• Strategy is to:

− Maximise revenue from approved products and pipeline product candidates

− Strengthen product pipeline by developing new products and technologies

− The development opportunities may be from own development, collaborations

with partners, targeted in-licensing or acquisition

21

Summary

Peter Grant

Chief Executive Officer

Andrew Derodra

Chief Financial Officer

Contact information

Head Office:

Skyepharma PLC

46-48 Grosvenor Gardens, London, SW1W 0EB, United Kingdom

Tel: (+44) 20 7881 0524

LSE:SKP

www.skyepharma.com 22

An Expert Drug Delivery Company

Financials Andrew Derodra, CFO

An Expert Drug Delivery Company

2 June 2014

Capital Raise

• Raised c. £112.1m at 191 pence per share (10-day mid-market average to 25 March 2014)

Use of Proceeds

• Repaid Bonds in full for £95.6m, at £25.2m discount

• c. £8.4m of additional funding for general corporate purposes

Rationale

• Significantly reduced gearing and cost of debt

• Eliminated £120.8m of future payments to bondholders (net saving £25.2m)

• Increased capacity to invest in product and technology development and corporate

opportunities

24

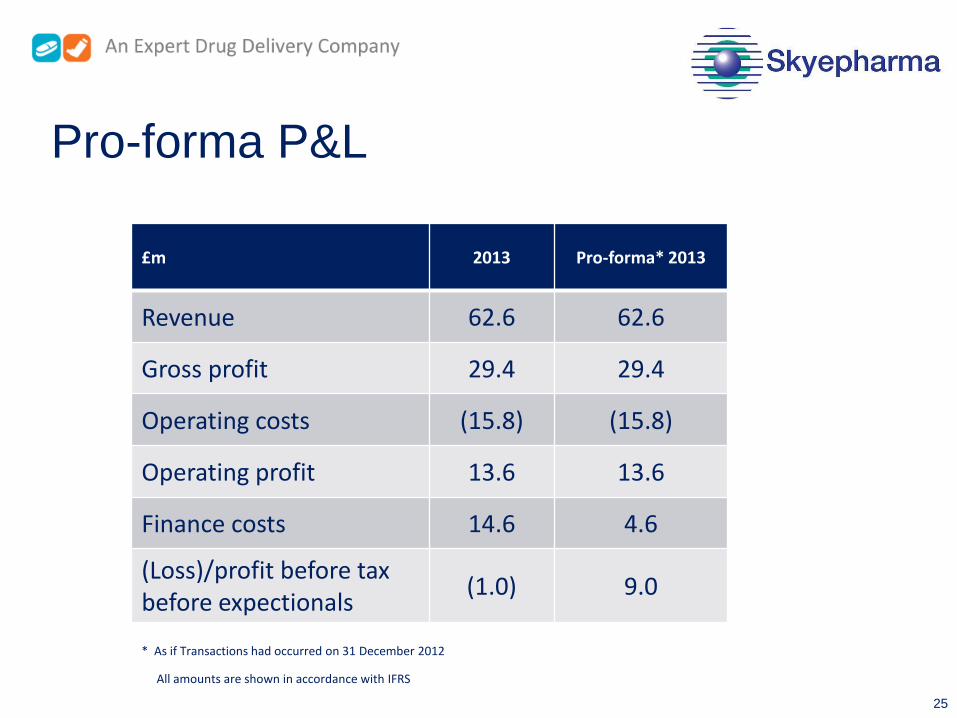

April 2014 Capital Transactions

£m 2013 Pro-forma* 2013

Revenue 62.6 62.6

Gross profit 29.4 29.4

Operating costs (15.8) (15.8)

Operating profit 13.6 13.6

Finance costs 14.6 4.6

(Loss)/profit before tax before expectionals

(1.0) 9.0

Pro-forma P&L

All amounts are shown in accordance with IFRS

25

* As if Transactions had occurred on 31 December 2012

£m As at 31 Dec 2013

Firm Placing, Placing and Open

Offer

Repayment of bonds

Pro forma as at 31 Dec 2013

2024 bonds 66.8 - (66.8) -

Property Mortgage 7.3 - 7.3

CRC Finance 24.5 - 24.5

Other Borrowings 2.1 - 2.1

Total Debt 100.7 - (66.8) 33.9

Less cash and cash equivalents

(16.5) (104.4)† 96.0* (24.9)

Net Debt 84.2 (104.4) † 29.2 9.0

Pro-forma net debt

All amounts are shown in accordance with IFRS

26

† This figure assumes a Capital Raise of £112m less transaction costs of £7.6m

* This figure includes bond repayment of £95.6m plus related costs of £0.4m

• Revenues up 25%

• Gross profit up 5%

• Operating profit* up 8%

• EBITDA up 15%

2013 results

† Re-stated * Pre-exceptional

27

2013

£m

2012†

£m

Continuing operations

Revenue 62.6 49.9

Cost of sales (33.2) (21.9)

Gross profit 29.4 28.0

Selling, marketing and distribution (1.5) (1.5)

Research and development (10.8) (11.9)

Corporate costs (2.7) (2.0)

Amortisation (0.9) (0.7)

Share-based payment charge (0.3)

Other income 0.4 0.7

Operating profit* 13.6 12.6

EBITDA* 17.9 15.6

Profit/ (loss) for the period 0.8 (4.4)

EPS (pence) 1.8 (14.9)

Diluted EPS (pence) 1.7 (14.9)

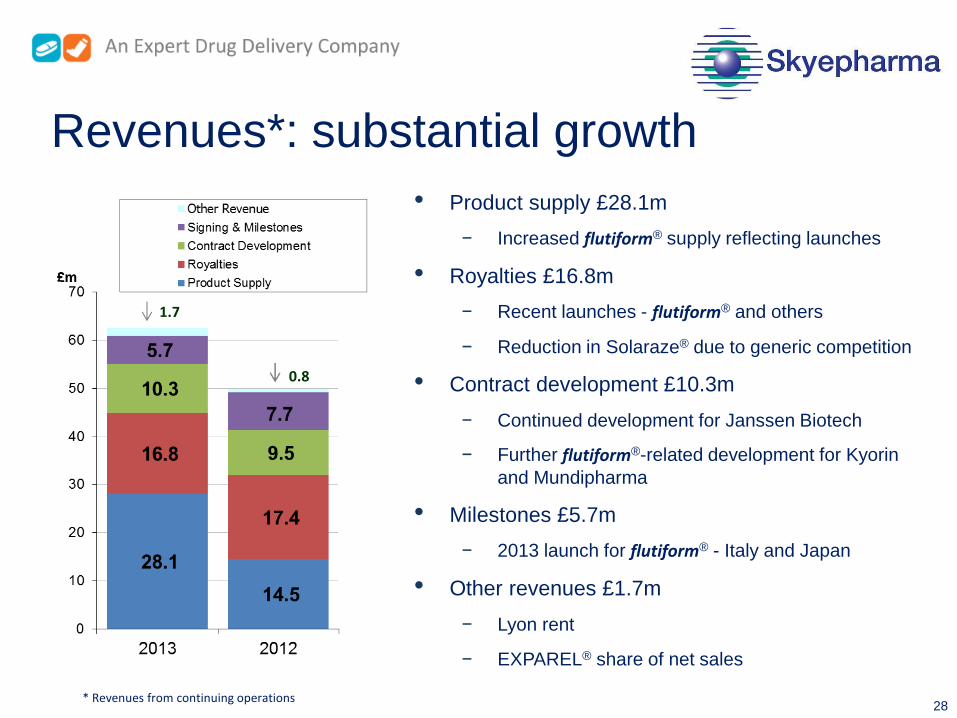

Revenues*: substantial growth

• Product supply £28.1m

− Increased flutiform® supply reflecting launches

• Royalties £16.8m

− Recent launches - flutiform® and others

− Reduction in Solaraze® due to generic competition

• Contract development £10.3m

− Continued development for Janssen Biotech

− Further flutiform®-related development for Kyorin

and Mundipharma

• Milestones £5.7m

− 2013 launch for flutiform® - Italy and Japan

• Other revenues £1.7m

− Lyon rent

− EXPAREL® share of net sales

0.8

1.7

28 * Revenues from continuing operations

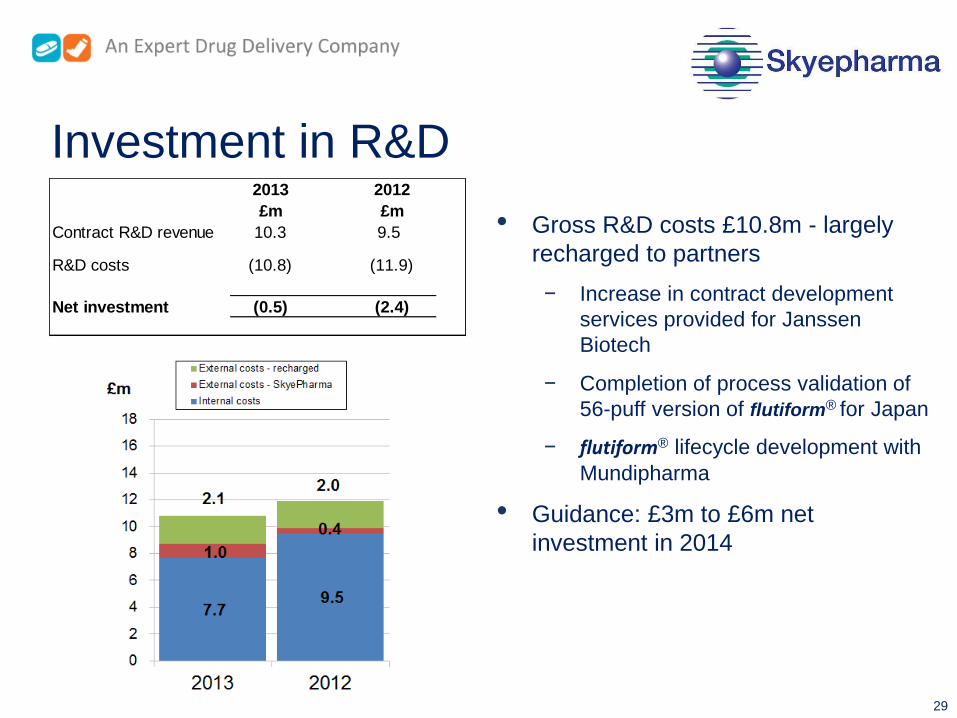

• Gross R&D costs £10.8m - largely

recharged to partners

− Increase in contract development

services provided for Janssen

Biotech

− Completion of process validation of

56-puff version of flutiform® for Japan

− flutiform® lifecycle development with

Mundipharma

• Guidance: £3m to £6m net

investment in 2014

Investment in R&D 2013 2012

£m £m

Contract R&D revenue 10.3 9.5

R&D costs (10.8) (11.9)

Net investment (0.5) (2.4)

29

• As expected, progression towards positive gross profit driven by:

− Increased volumes

− Supplier price breaks

• Substantial growth anticipated as in-market sales increase

• Supply chain is anticipated to move into positive gross profit during 2014

flutiform® supply chain – substantial growth

30

2013 2012

£m £m

Supply revenue 20.6 4.8

Cost of sales (23.4) (10.4)

Gross profit/(loss) (2.8) (5.6)

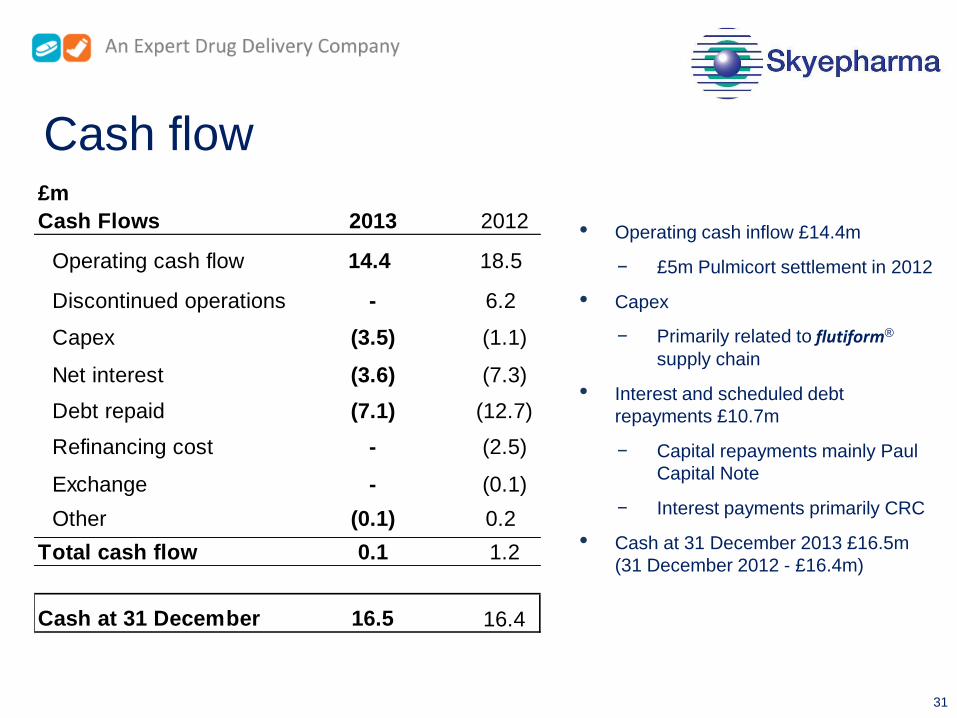

• Operating cash inflow £14.4m

− £5m Pulmicort settlement in 2012

• Capex

− Primarily related to flutiform®

supply chain

• Interest and scheduled debt

repayments £10.7m

− Capital repayments mainly Paul

Capital Note

− Interest payments primarily CRC

• Cash at 31 December 2013 £16.5m

(31 December 2012 - £16.4m)

Cash flow £m

Cash Flows 2013 2012

Operating cash flow 14.4 18.5

Discontinued operations - 6.2

Capex (3.5) (1.1)

Net interest (3.6) (7.3)

Debt repaid (7.1) (12.7)

Refinancing cost - (2.5)

Exchange - (0.1)

Other (0.1) 0.2

Total cash flow 0.1 1.2

Cash at 31 December 16.5 16.4

31

• Board expects further substantial growth in revenues in 2014:

− €3m (£2.5m) received on launch of flutiform® in France plus potential milestone U.S.$8m

(£4.9m) related to sales of EXPAREL®

− Growth of royalties from recently launched products likely to offset decline in royalties from

products which are off patent or facing generic competition

− Full years’ rental income for Lyon Facility and growing EXPAREL® sales

− Product supply growing to support increasing market penetration of flutiform® - anticipate

moving into positive gross profit during 2014

− Increased demand for contract development work (recruitment in progress)

• Operating costs to increase to support the customer-funded work and the Group’s

own expenditure on developing technologies and products

• Guidance: net expenditure in 2014 on R&D between £3m and £6m. Board will

consider uplifting this in future years as the Group’s net income rises, subject to

suitable opportunities being available

• Exceptional charge related to paying off the bonds estimated at £25.5m*

Outlook (31 March 2014)

32 * Being the difference between the expected book value of the Bonds at 30 April 2014 and cost of redemption

An Expert Drug Delivery Company

Appendices

33

Skyepharma’s business model

Expertise

Track record Resources Networks

Capabilities Technologies

Patents

Know-how

Products

Partner-initiated Skyepharma-initiated

Licence

fees

Royalties

Milestones

Contract research &

development revenues

Supply income

Revenues

34

Recent launches

2012 2013 2014 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

flu

tifo

rm®

O

the

rs

UK Germany

Netherlands Cyprus

Sweden Norway

Denmark Iceland Italy

Finland

Ireland Japan

Belgium Slovakia

Australia Hong Kong

Czech Rep.

S Korea

PAXIL CR® (Japan)

Requip® Once-a-Day (Japan)

EXPAREL® (U.S.)

Breo® Ellipta® (U.S.)

Relvar®Ellipta® (Japan)

RAYOS® (U.S.)

35

France

Israel

Anoro™ Ellipta® (U.S.)

Relvar®Ellipta® (UK, Germany)

Locations

R&D Muttenz, Switzerland

Leased to Aenova: Manufacturing

Lyon, France

Corporate Headquarters London, UK

FTEs: 69* (Aenova FTEs: approx. 100) FTEs: 11*

* as at 31 December 2013 36

• Pharmaceutical manufacturing site (22,000m² operational buildings), which

makes a number of the Group’s oral products

− Plant approved according to FDA (U.S.); EMA (EU); ANVISA (Brazil) and KFDA

(South Korea)

− Approximately 100 employees

• Entire operation was leased to Aenova in July 2011 for up to 5 years

− Aenova bears operating risks and profits and losses during lease period

− Aenova sought to terminate in July 2013, but expert determination resolved in

Skyepharma’s favour

− Lease renewed December 2013 at a rent of €2m per annum to June 2016

− On expiry in June 2016 the operations come back to Skyepharma

• Process underway to see if there is a third party interested in taking over the

facility

Lyon manufacturing facility

37

The Board Frank Condella Non-Executive Chairman

• Joined 2006

• CEO 2006 - 2008

• President/CEO Columbia Labs

• NED: Prosonix

• Previous Exec: IVAX; Faulding; Roche;

Lederle

Jean-Charles Tschudin Non-Executive Director

Senior Independent Director

Chairman Nomination Committee

• Joined 2007

• Non-Exec Director Sinclair IS Pharma

• Previous Exec: Astellas; Cardinal

Health; J&J; Schering-Plough

Thomas Werner Non-Executive Director

Chairman Remuneration Committee

• Joined 2009

• NED: Chairman 4SC; Board member:

Basilea; Blackfield; BSN; SuppreMol

• Previous Exec: GSK; BMS

Peter Grant Chief Executive Officer

• Joined 2006 as CFO

• Appointed CEO 2012

• Previous Exec: Voice Commerce;

Eurodis Electron; WorldPay;

Molins; General Electric; KPMG

John Murphy General Counsel,

Company Secretary

• Joined 2006

• Previous Exec: Medeva;

Celltech; Pharmagene

Andrew Derodra Chief Financial Officer

• Joined November 2013

• Previous Exec: Tate & Lyle;

SABMiller; Diageo; British Airways;

Reed Elsevier

No

n-E

xecu

tive

Ex

ecu

tive

C

o. S

ec

John Biles Non-Executive Director

Chairman Audit Committee

• Joined March 2014

• NED: Bodycote; HellermannTyton;

Sutton & E Surrey Water

• Previous Exec: FKI; Chubb Security;

Racal Electronics; PwC

38

Top Related