Languages

Pages

Legal

1

Chapter 14Entity Operations and

Distributions-2010 Howard Godfrey, Ph.D., CPA

UNC CharlotteCopyright © 2010, Dr. Howard Godfrey

Edited October 30, 2010. T10-Chp-14-1-Entity-Choice-Operations-and-Dist-2010

2

Proprietorship S CorporationPartnership Separate items

Income reporting RecaptureNet operating Loss No div. received deductionTransaction w/ ptshp Net operating LossBasis Considerations Basis Considerations

Corporation Entity DistributionsCapital gains & losses ProprietorshipDiv. received deduction PartnershipCharitable Contributions CorporationNet operating Loss S CorporationTax Credits Tax PlanningBasis Considerations Income Splitting

Children-EmployeesFamily Entities

14. Entity - Operations and Distributions

3

Partnerships Income reporting

Net operating Loss

Transaction w/ partnership

Basis Considerations

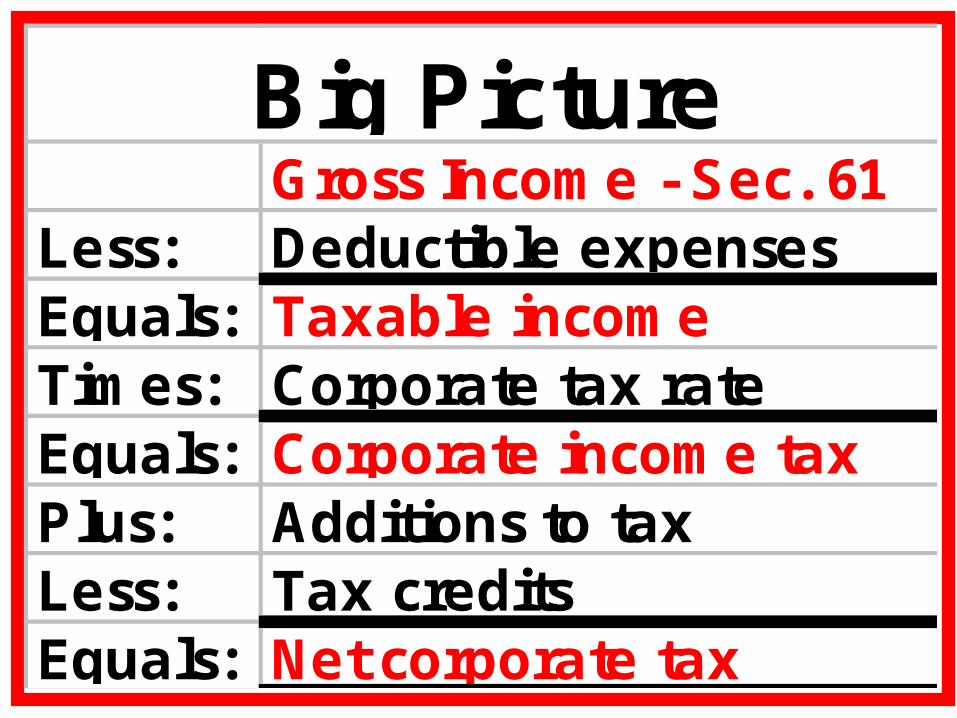

Taxation of OperationsThe general formula for computing

income tax is:

Gross Incomeless: Deductions

Taxable Incometimes: Tax rate (for entity)

Income taxless: Tax prepayments and Tax credits

Tax (refund) due with return

Let’s concentrate on the exceptions to the general formula

common to each entity.

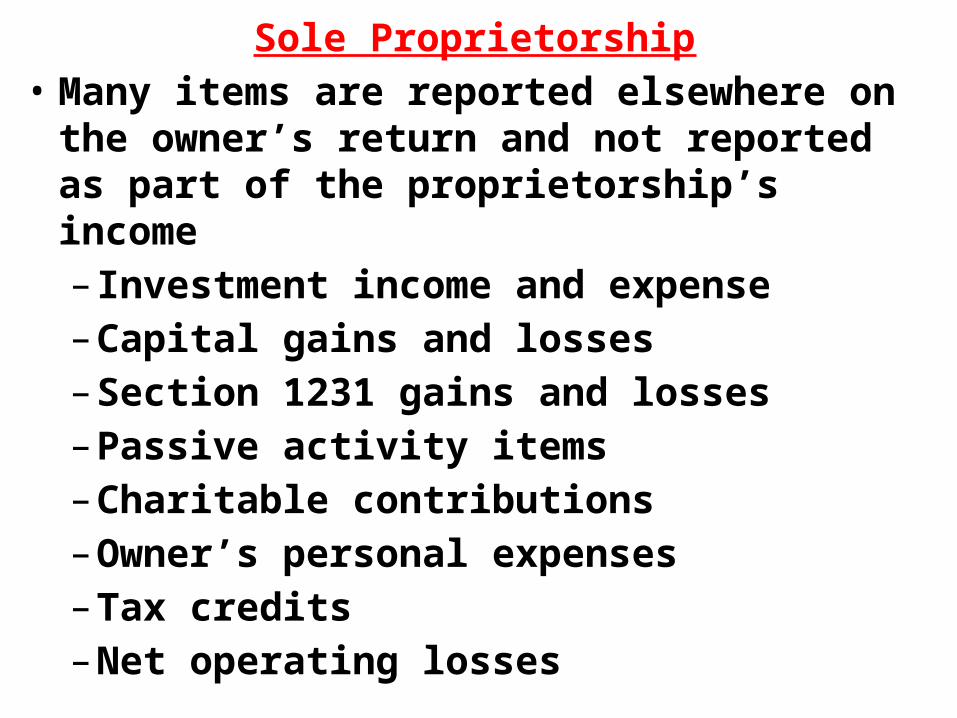

Sole Proprietorship• Many items are reported elsewhere on the

owner’s return and not reported as part of the proprietorship’s income– Investment income and expense– Capital gains and losses– Section 1231 gains and losses– Passive activity items– Charitable contributions– Owner’s personal expenses– Tax credits– Net operating losses

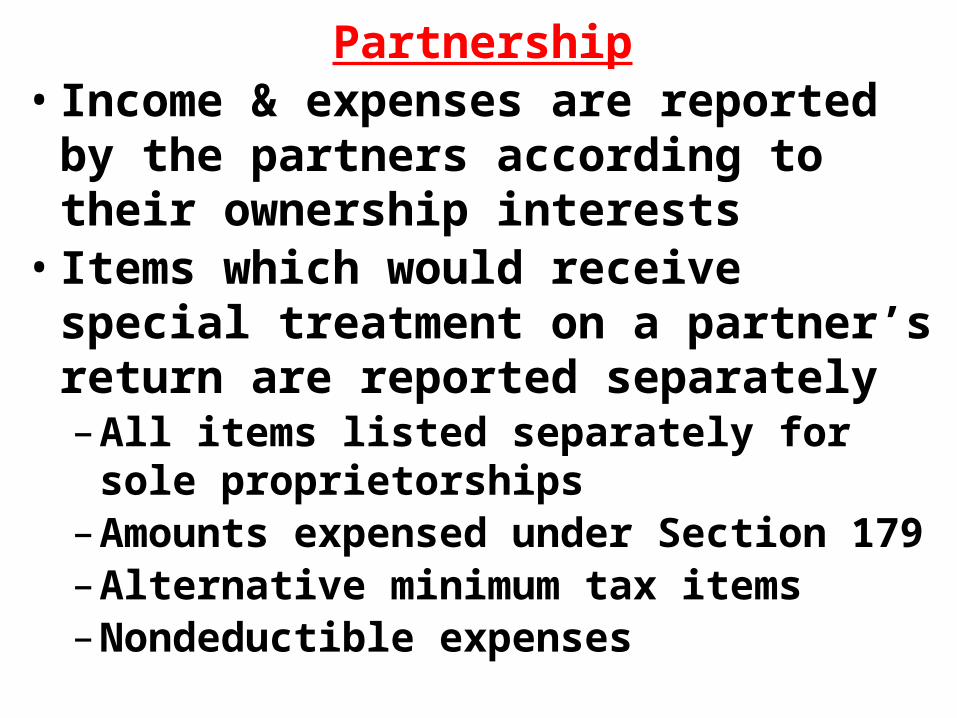

Partnership• Income & expenses are reported by the

partners according to their ownership interests

• Items which would receive special treatment on a partner’s return are reported separately– All items listed separately for sole

proprietorships– Amounts expensed under Section 179– Alternative minimum tax items– Nondeductible expenses

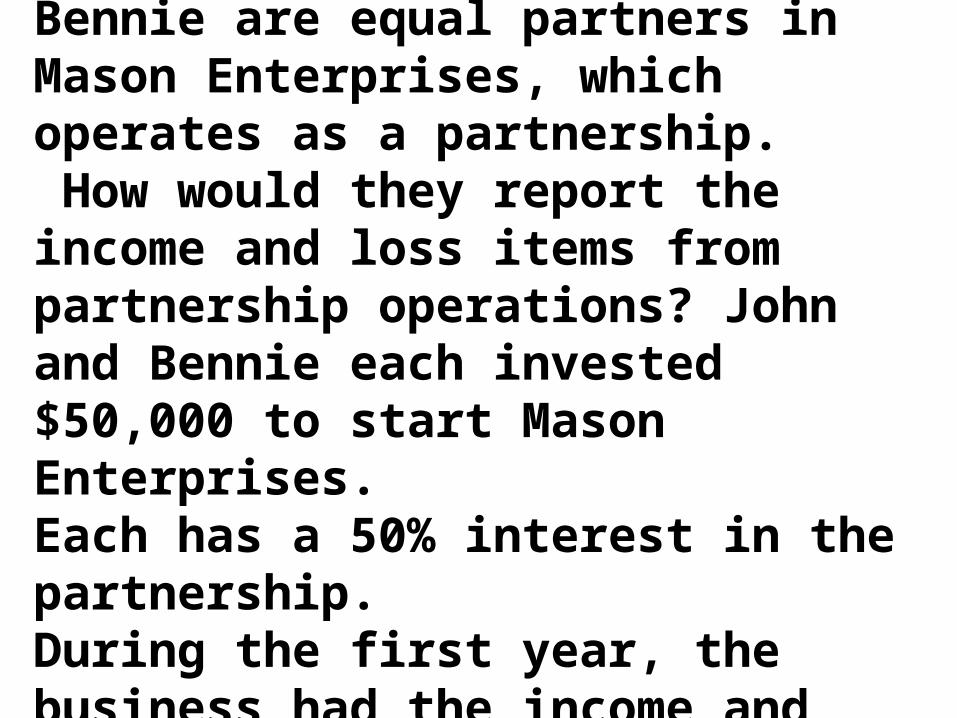

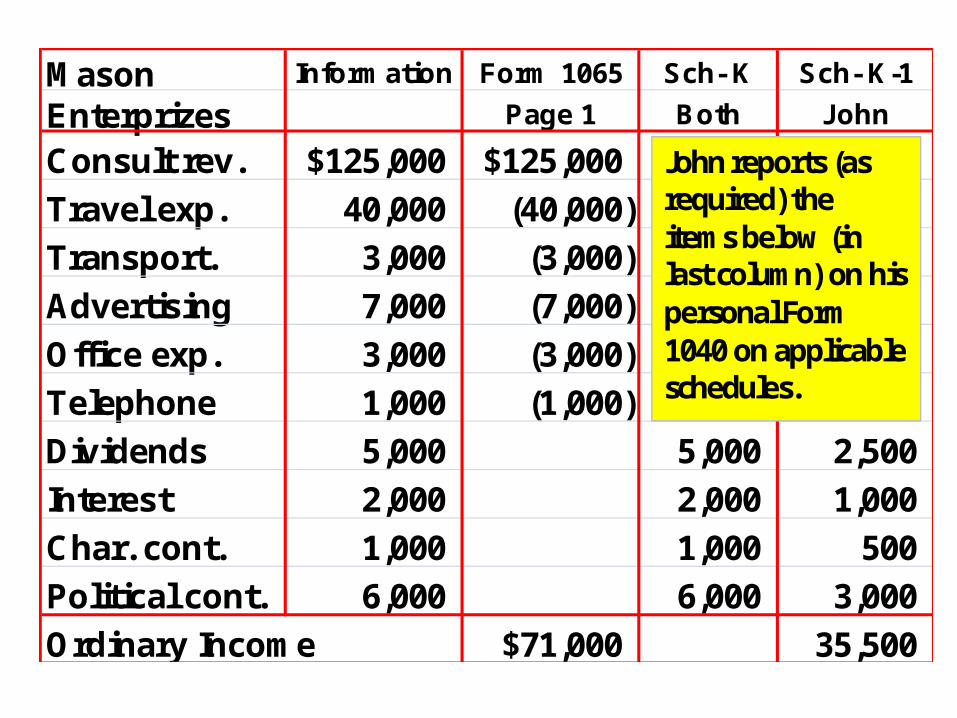

Partnership Income-1John Mason and his brother Bennie are equal partners in Mason Enterprises, which operates as a partnership. How would they report the income and loss items from partnership operations? John and Bennie each invested $50,000 to start Mason Enterprises. Each has a 50% interest in the partnership.During the first year, the business had the income and expenses from operations shown on the next slide:

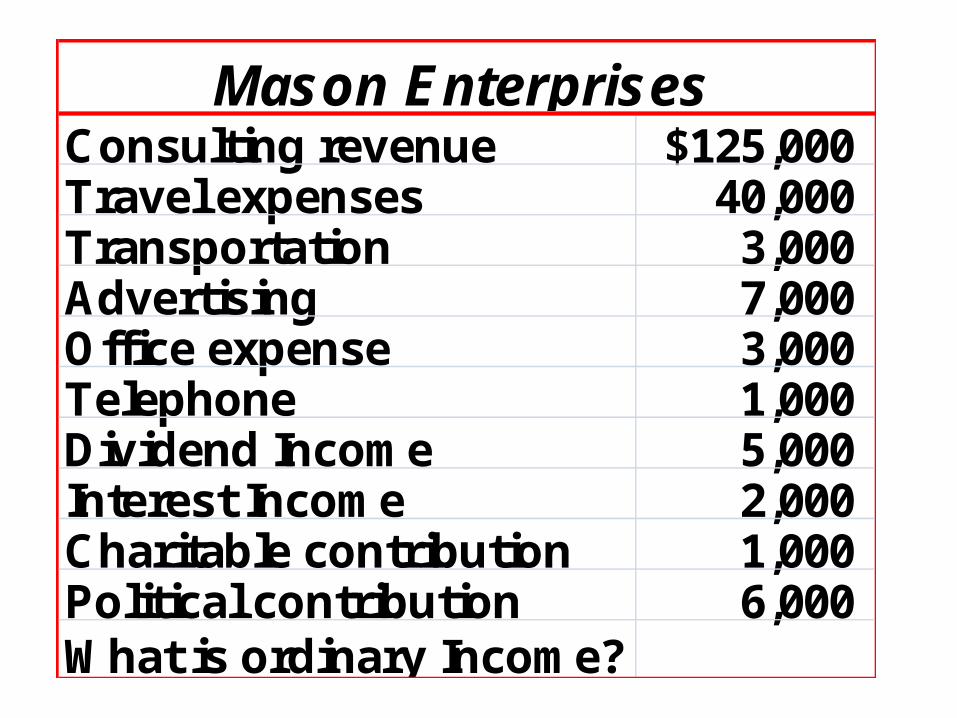

Consulting revenue $125,000Travel expenses 40,000 Transportation 3,000 Advertising 7,000 Office expense 3,000 Telephone 1,000 Dividend Income 5,000 Interest Income 2,000 Charitable contribution 1,000 Political contribution 6,000 What is ordinary Income?

Mason Enterprises

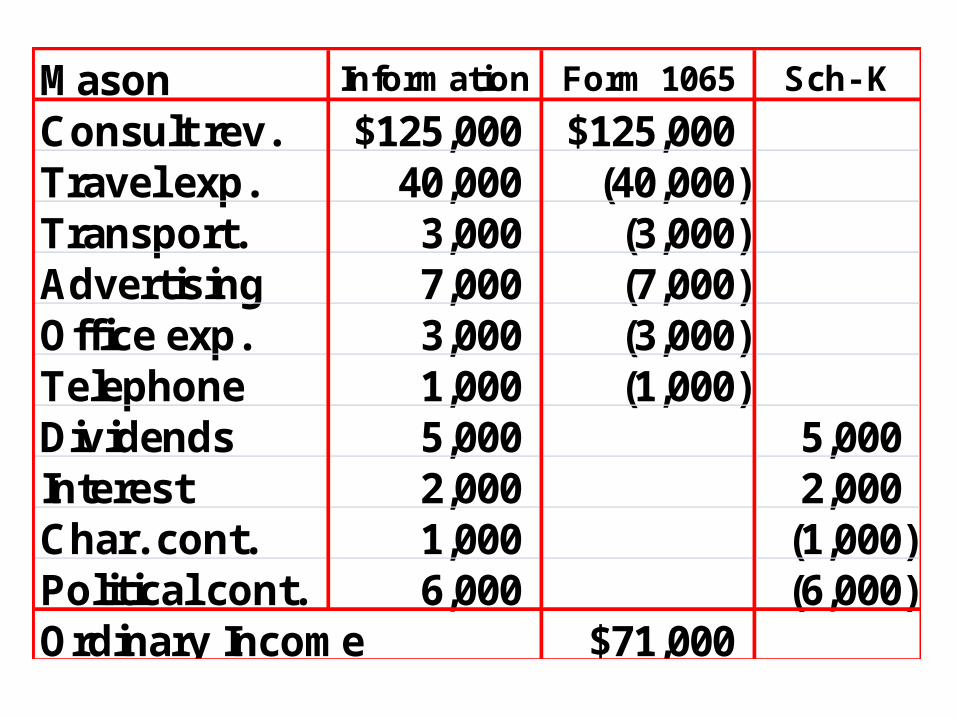

OrdinaryConsulting rev. $125,000 $125,000Travel expenses 40,000 (40,000) Transportation 3,000 (3,000) Advertising 7,000 (7,000) Office expense 3,000 (3,000) Telephone 1,000 (1,000) Dividend Income 5,000 Interest Income 2,000 Charitable cont. 1,000 Political cont. 6,000 Ordinary Income $71,000

Mason Enterprizes

Mason Information Form 1065 Sch- K

Consult rev. $125,000 $125,000Travel exp. 40,000 (40,000) Transport. 3,000 (3,000) Advertising 7,000 (7,000) Office exp. 3,000 (3,000) Telephone 1,000 (1,000) Dividends 5,000 5,000 Interest 2,000 2,000 Char. cont. 1,000 (1,000) Political cont. 6,000 (6,000) Ordinary Income $71,000

Mason Information Form 1065 Sch- K Sch- K-1

Enterprizes Page 1 Both John

Consult rev. $125,000 $125,000

Travel exp. 40,000 (40,000)

Transport. 3,000 (3,000)

Advertising 7,000 (7,000)

Office exp. 3,000 (3,000)

Telephone 1,000 (1,000)

Dividends 5,000 5,000 2,500

Interest 2,000 2,000 1,000

Char. cont. 1,000 1,000 500

Political cont. 6,000 6,000 3,000

Ordinary Income $71,000 35,500

John reports (as required) the items below (in last column) on his personal Form 1040 on applicable schedules.

Partnership• Losses are deductible subject to

three limitations–Limited to the amount of a partner’s

basis (capital recovery concept)–Limited to the partner’s at-risk

amount–Limited by passive activity rules

Partnership• Partner’s basis is adjusted to

reflect partnership income and losses reported–Increased for income or gains

• Designed to prevent double taxation

–Decreased for losses• Designed to prevent double benefit

and reflect capital recovery

Problem.In computing the ordinary business income of a partnership, a deduction is allowed for:a. Net operating loss deduction.b. Depreciation Expensec. Short-term capital losses.d. Gifts to qualified charities.

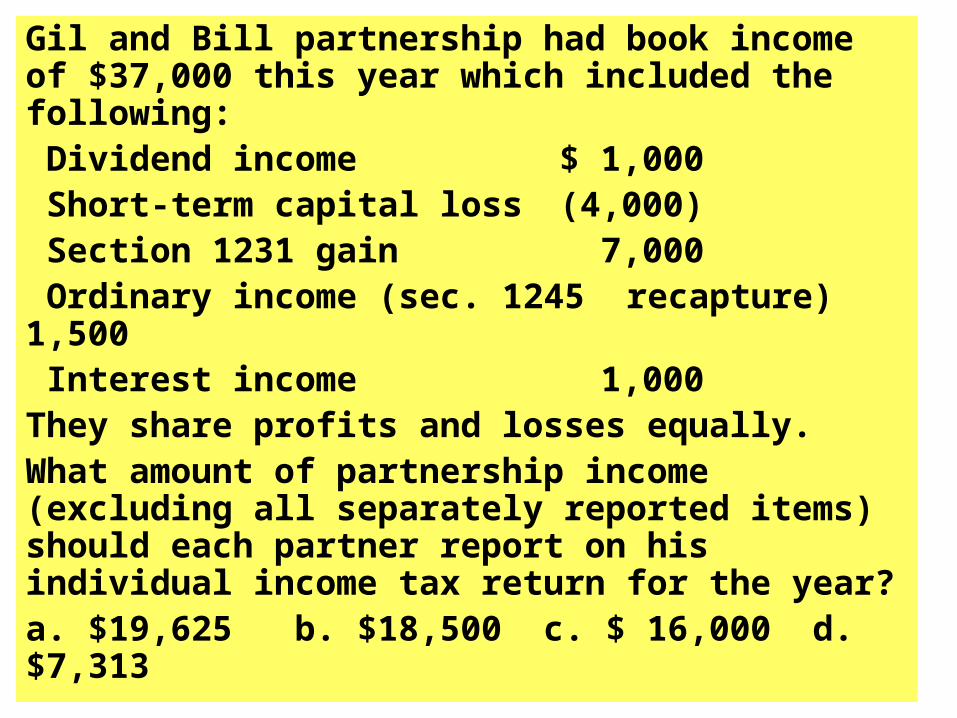

Gil and Bill partnership had book income of $37,000 this year which included the following: Dividend income $ 1,000 Short term capital loss‑ (4,000) Section 1231 gain 7,000 Ordinary income (sec. 1245 recapture) 1,500 Interest income 1,000They share profits and losses equally. What amount of partnership income (excluding all separately reported items) should each partner report on his individual income tax return for the year? a. $19,625 b. $18,500 c. $ 16,000 d. $7,313

Gil & Bill partnership had booknet income of $37,000 including:

Ordinary Book income $37,000Dividend income $1,000ST capital loss (4,000) Section 1231 gain 7,000 Ordinary income(sec. 1245 recapture) 1,500 Interest income 1,000 Ordinary IncomeThey share profits and losses equally.What is partnership ordinary income

Gil & Bill partnership had book incomeof $37,000 which included:

Ordinary Book income $37,000Dividend income $1,000 ($1,000)ST capital loss (4,000) 4,000 Section 1231 gain 7,000 (7,000) Ordinary income(sec. 1245 recapture) 1,500 Interest income 1,000 (1,000) Ordinary Income $32,000They share profits and losses equally.What is partnership ordinary income

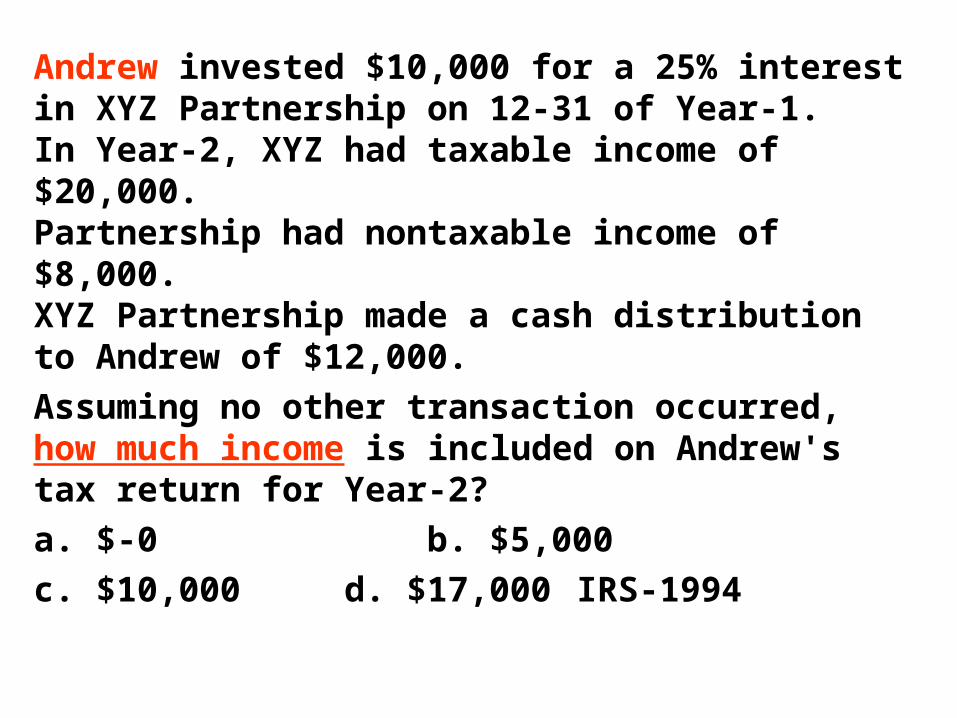

Andrew invested $10,000 for a 25% interest in XYZ Partnership on 12-31 of Year-1. In Year-2, XYZ had taxable income of $20,000. Partnership had nontaxable income of $8,000. XYZ Partnership made a cash distribution to Andrew of $12,000. Assuming no other transaction occurred, how much income is included on Andrew's tax return for Year-2?a. $-0 b. $5,000 c. $10,000 d. $17,000 IRS-1994

Andrew invested $10,000 for a 25% interest in XYZ Partnership on 12-31 of Year-1. In Year-2, XYZ had taxable income of $20,000. It also had nontaxable income of $8,000. XYZ Partnership made a cash distribution to Andrew of $12,000. Assuming no other transactions occurred, what is Andrew's basis in the partnership at the end of Year-2?a. $-0 b. $5,000 c. $10,000 d. $17,000 IRS-1994

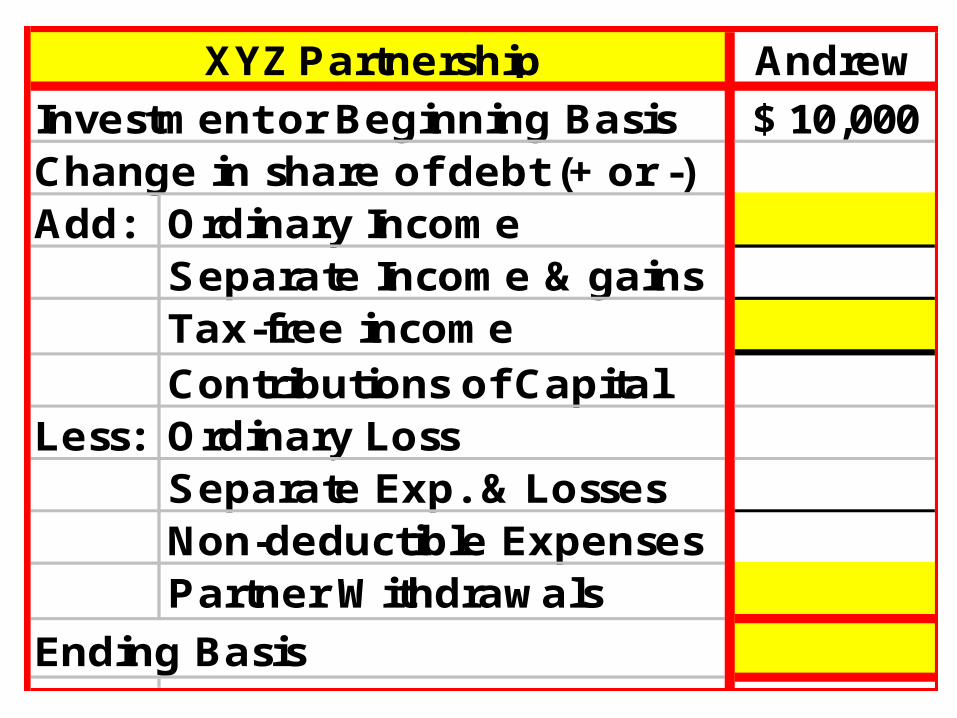

Andrew

Investment or Beginning Basis 10,000$ Change in share of debt (+ or -)Add: Ordinary Income

Separate Income & gainsTax-free incomeContributions of Capital

Less: Ordinary LossSeparate Exp. & LossesNon-deductible ExpensesPartner Withdrawals

Ending Basis

XYZ Partnership

Andrew

Investment or Beginning Basis 10,000$ Change in share of debt (+ or -)Add: Ordinary Income 5,000

Separate Income & gainsTax-free income 2,000 Contributions of Capital

Less: Ordinary LossSeparate Exp. & LossesNon-deductible ExpensesPartner Withdrawals (12,000)

Ending Basis 5,000$

XYZ Partnership

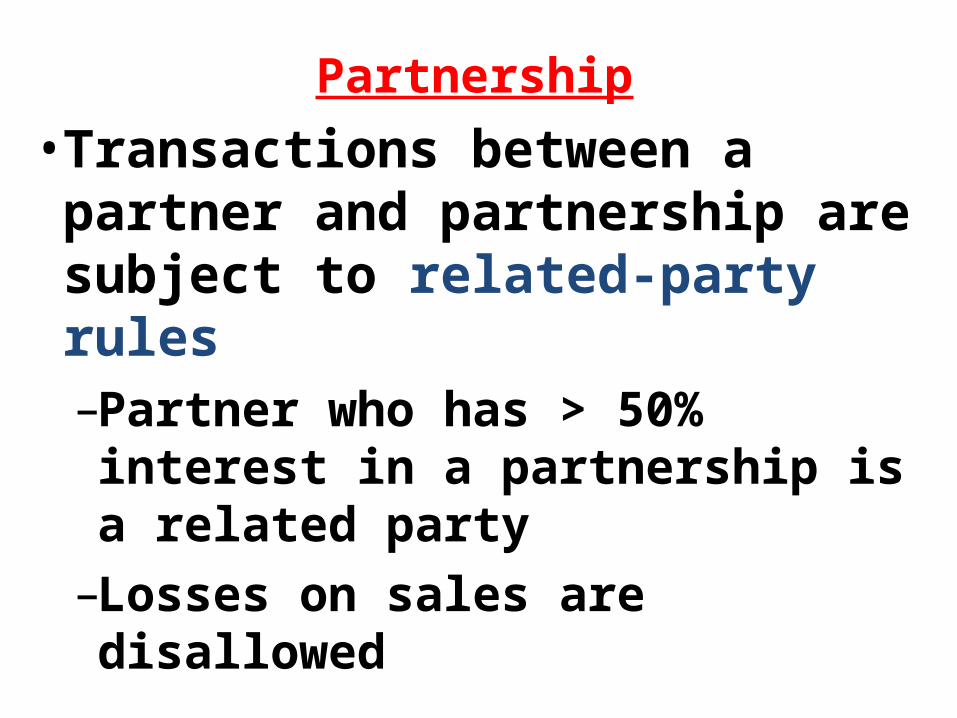

Partnership• Transactions between a partner

and partnership are subject to related-party rules–Partner who has > 50% interest

in a partnership is a related party

–Losses on sales are disallowed

24

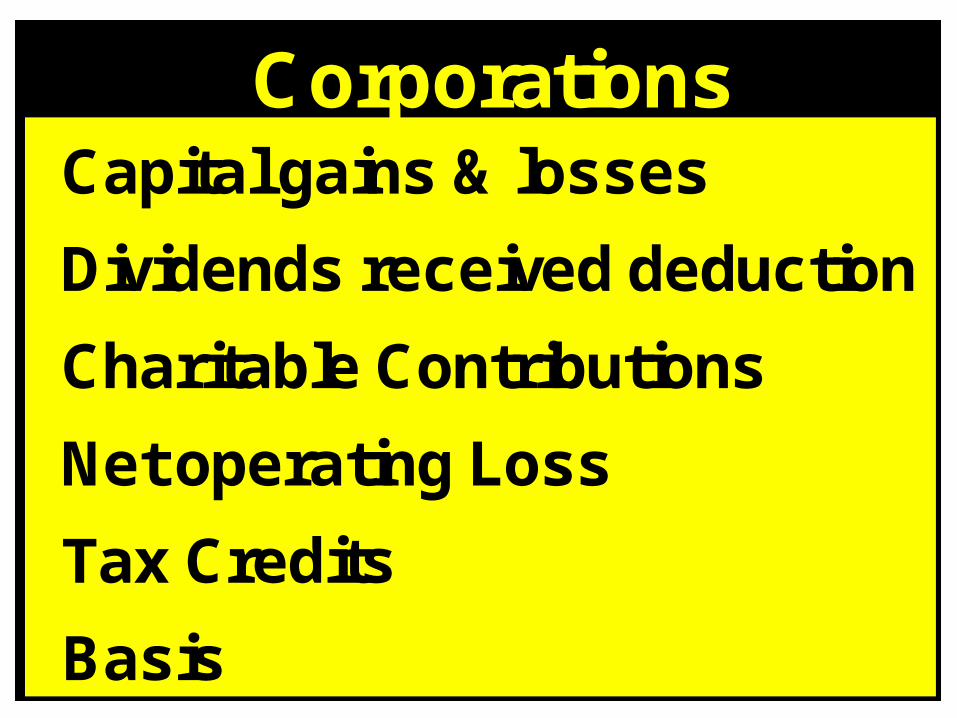

Corporations Capital gains & losses

Dividends received deduction

Charitable Contributions

Net operating Loss

Tax Credits

Basis

Gross Income - Sec. 61Less: Deductible expenses Equals: Taxable income Times: Corporate tax rate Equals: Corporate income tax Plus: Additions to tax Less: Tax credits Equals: Net corporate tax

Big Picture

26

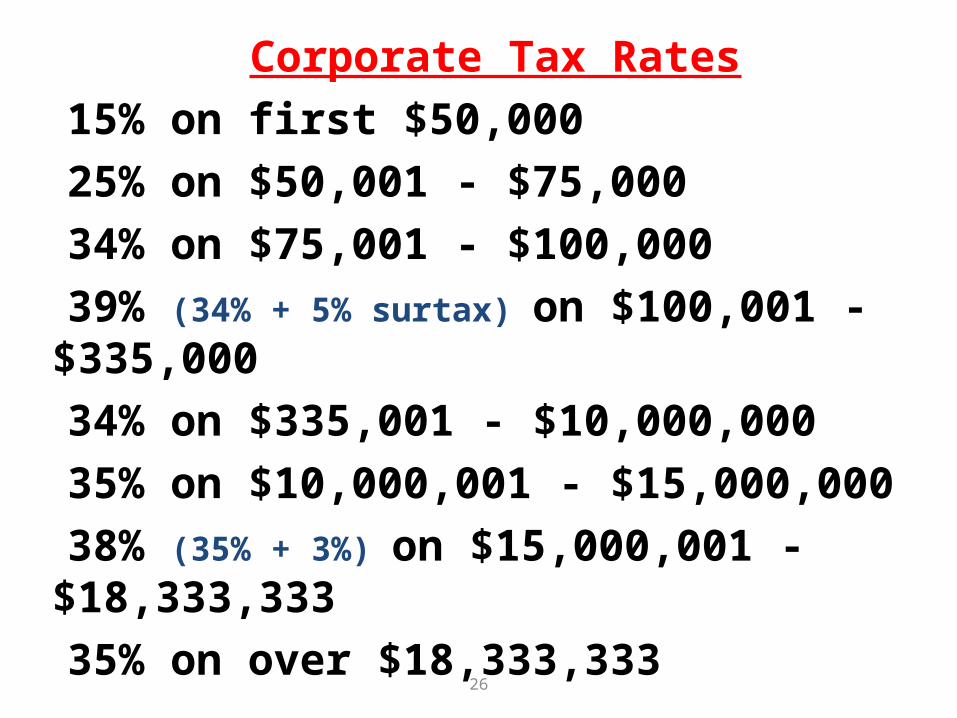

Corporate Tax Rates15% on first $50,00025% on $50,001 - $75,00034% on $75,001 - $100,00039% (34% + 5% surtax) on $100,001 - $335,00034% on $335,001 - $10,000,00035% on $10,000,001 - $15,000,00038% (35% + 3%) on $15,000,001 - $18,333,33335% on over $18,333,333

27

PSC• Personal service corporation is a corporation

– that provides service in the fields of accounting, actuarial science, architecture, consulting, engineering, health, law, or performing arts and

– is substantially owned by its employees• A flat 35% tax rate applies to its entire taxable

income• The PSC provisions encourage owner-

employees to take earnings out as salary

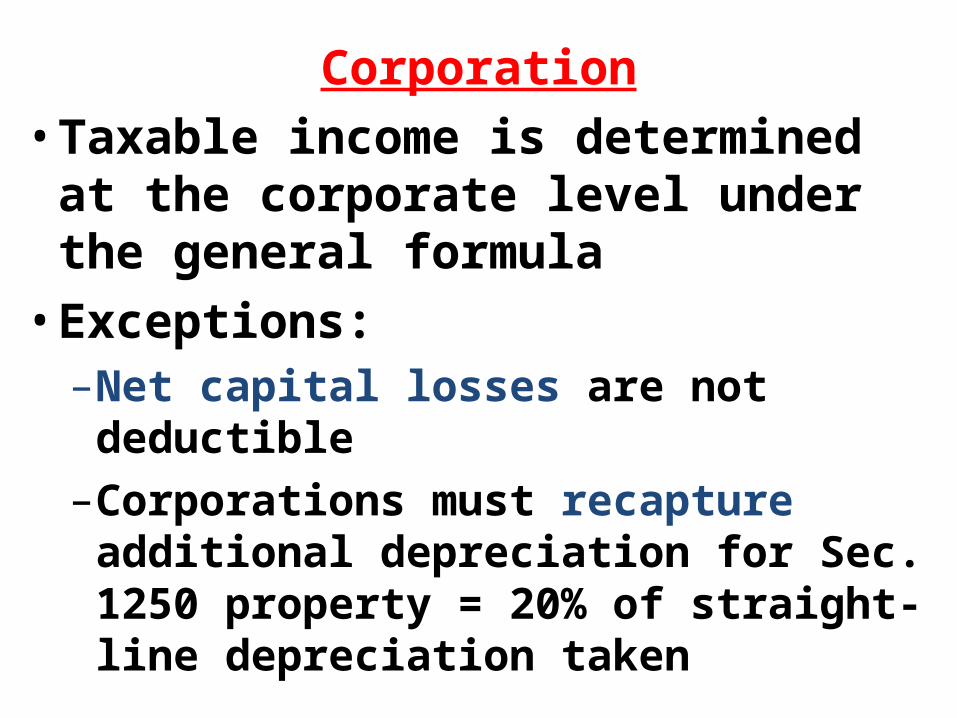

Corporation• Taxable income is determined at the

corporate level under the general formula

• Exceptions:–Net capital losses are not deductible–Corporations must recapture additional

depreciation for Sec. 1250 property = 20% of straight-line depreciation taken

Corporation–Passive activity losses• Corporations are not subject to the passive activity

rules–Personal service corporations must follow them–Closely-held corporations may use passive losses to offset

active income but not portfolio income

–Charitable contributions are limited to 10% of taxable income• Before dividend-received deductions and any

carryovers• Excess contributions may be carried forward 5 years

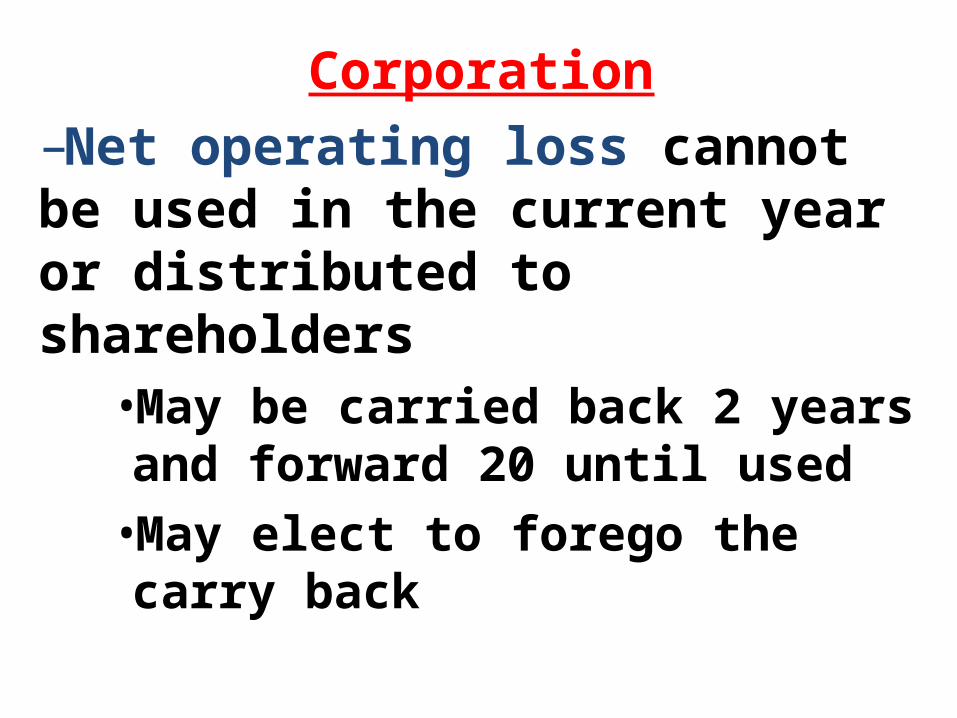

Corporation–Net operating loss cannot be used in the current year or distributed to shareholders

•May be carried back 2 years and forward 20 until used

•May elect to forego the carry back

31

Gross incomeLess: Deductions: Except charity, Div. Rec.,

NOL & C-Loss Carryback

Equals Taxable Income- For Charity Limit

Less: Charitable Cont. < = 10% of T.I. Above

Equals Taxable Income- Before Div. Rec'd Ded.

Less: Div. Rec. Deduct.

Equals Taxable Income- Before carrybacks

Less: NOL and/or Capital Loss carrybacks

Equals Taxable Income

32

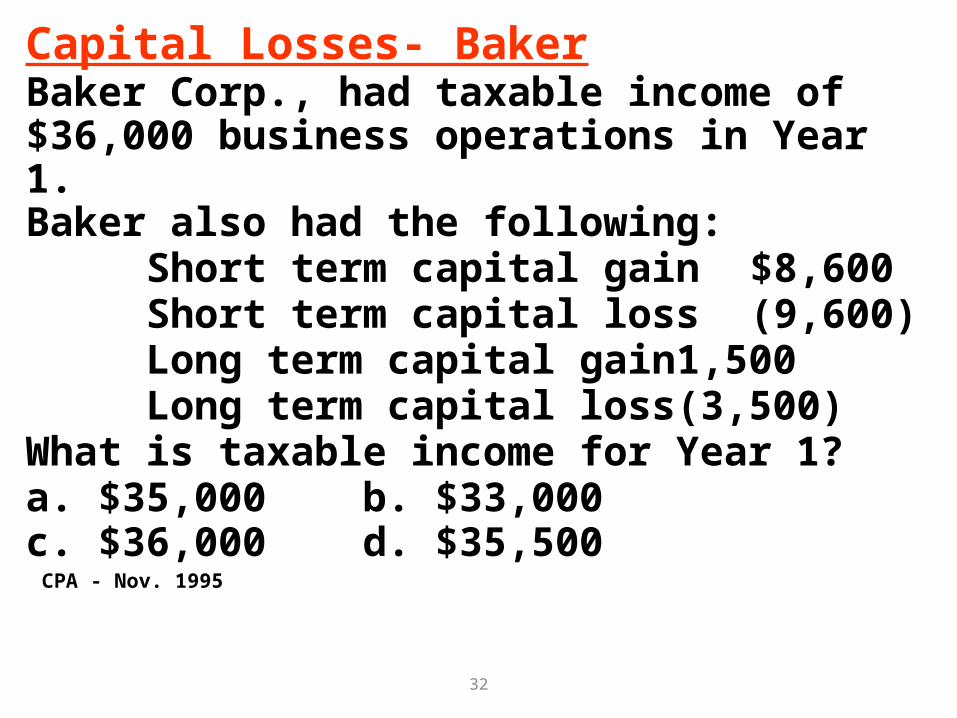

Capital Losses- BakerBaker Corp., had taxable income of $36,000 business operations in Year 1. Baker also had the following: Short term capital gain $8,600 Short term capital loss (9,600) Long term capital gain 1,500 Long term capital loss (3,500)What is taxable income for Year 1? a. $35,000 b. $33,000 c. $36,000 d. $35,500 CPA - Nov. 1995

33

Capital Losses-Baker Baker Corp., had taxable income of $36,000 business operations in Year-1. Baker also had the following: Short term capital gain $8,600 Short term capital loss (9,600) Long term capital gain 1,500 Long term capital loss (3,500)What is taxable income for Year-1?

$36,000

34

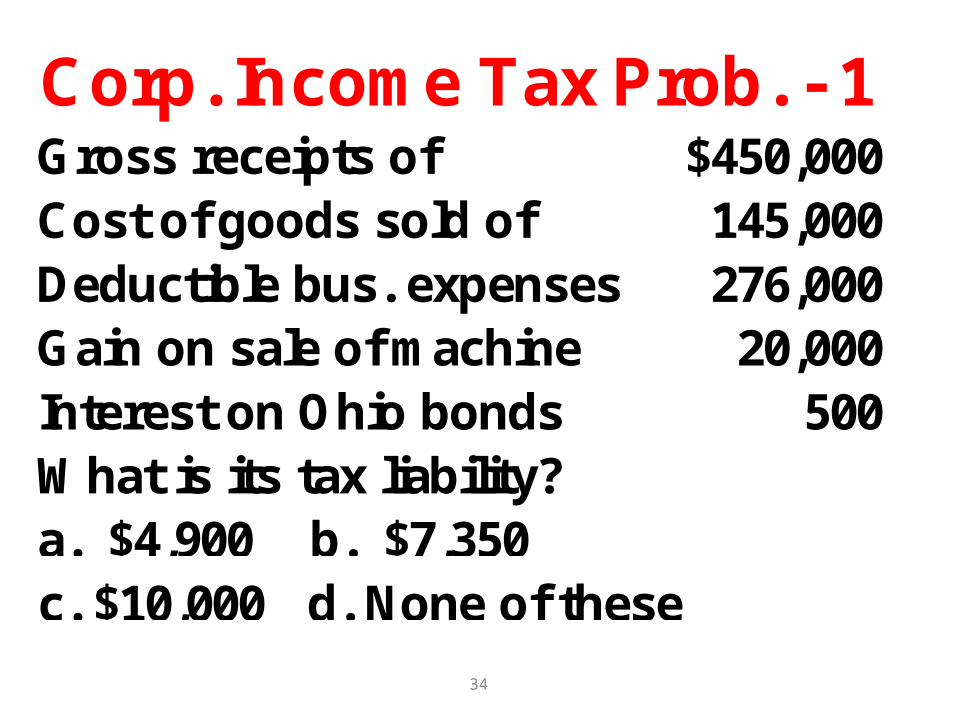

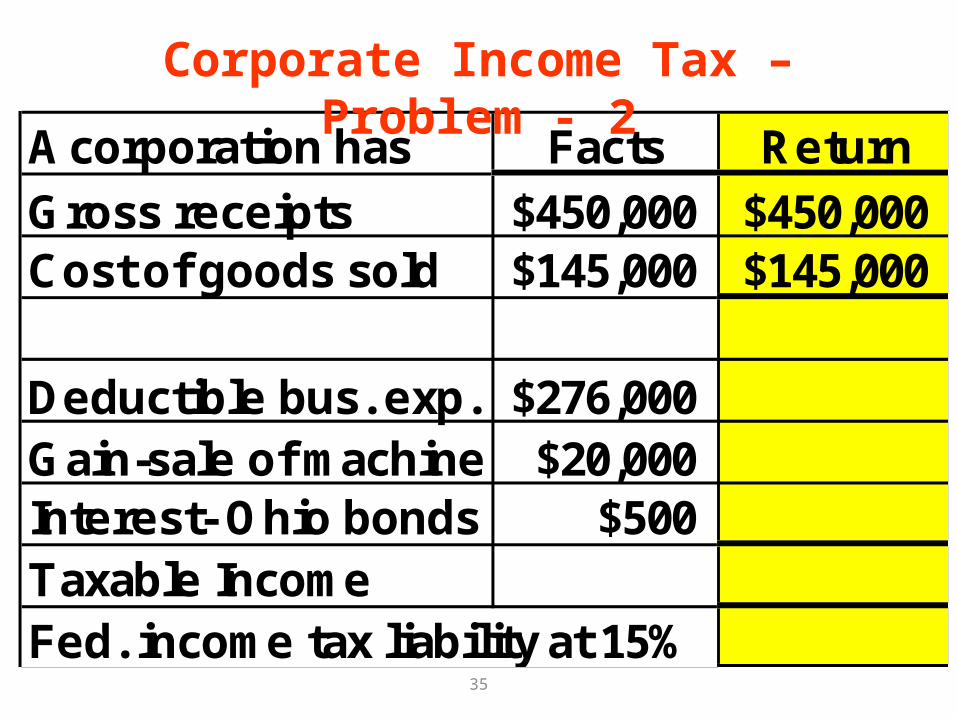

Corp. Income Tax Prob. - 1 Gross receipts of $450,000Cost of goods sold of 145,000 Deductible bus. expenses 276,000 Gain on sale of machine 20,000 Interest on Ohio bonds 500 What is its tax liability? a. $4,900 b. $7,350 c. $10,000 d. None of these

35

A corporation has Facts Return

Gross receipts $450,000 $450,000Cost of goods sold $145,000 $145,000

Deductible bus. exp. $276,000Gain-sale of machine $20,000Interest- Ohio bonds $500Taxable IncomeFed. income tax liability at 15%

Corporate Income Tax – Problem - 2

36

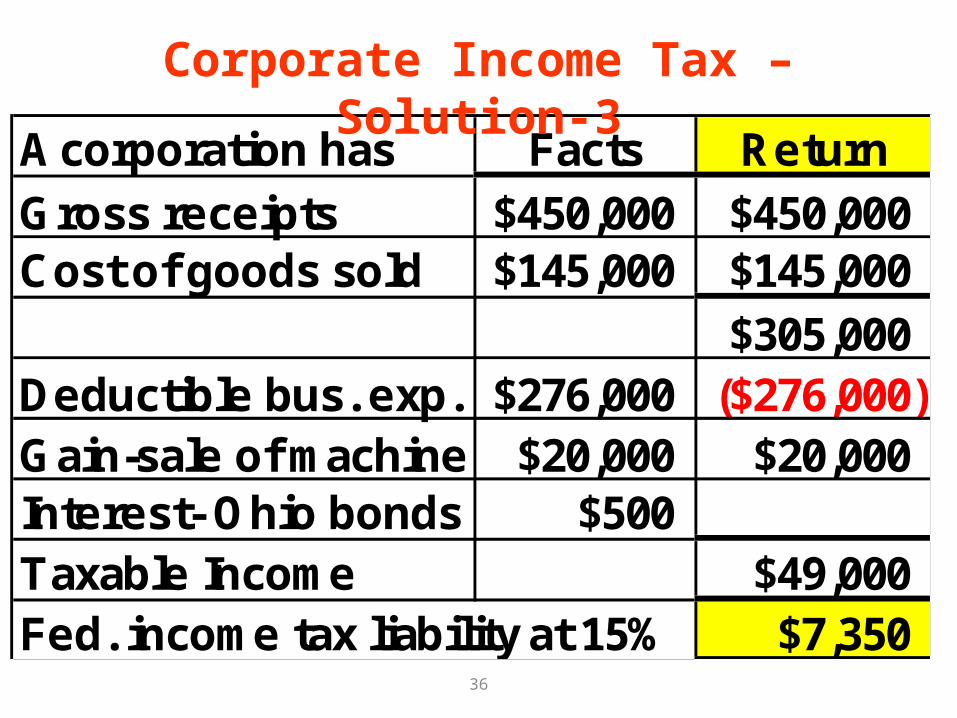

A corporation has Facts Return

Gross receipts $450,000 $450,000Cost of goods sold $145,000 $145,000

$305,000Deductible bus. exp. $276,000 ($276,000)Gain-sale of machine $20,000 $20,000Interest- Ohio bonds $500Taxable Income $49,000Fed. income tax liability at 15% $7,350

Corporate Income Tax – Solution-3

37

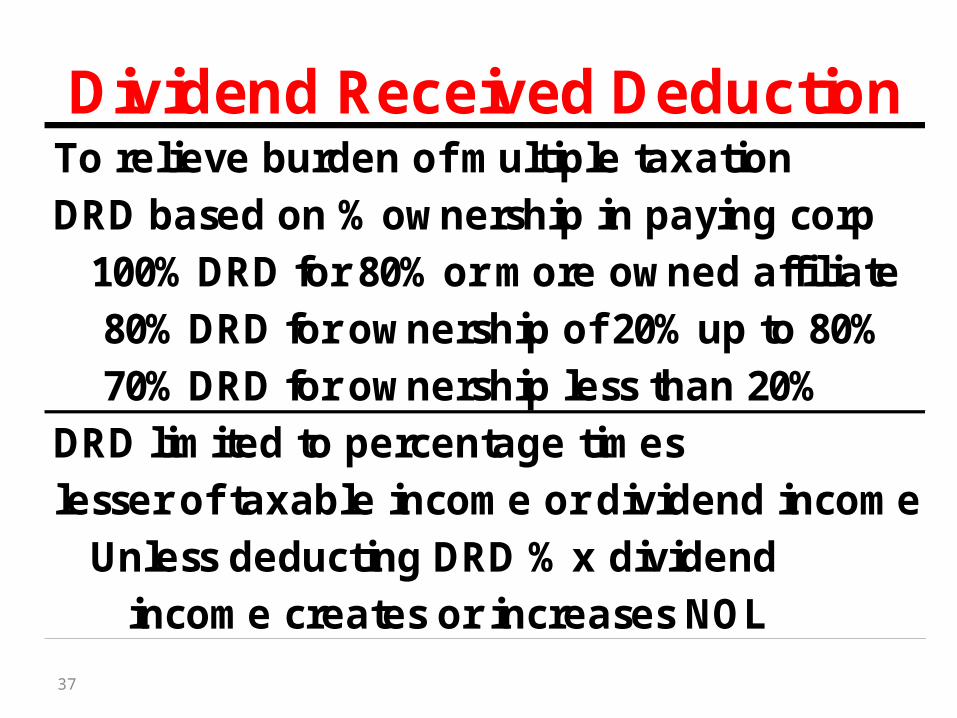

Dividend Received DeductionTo relieve burden of multiple taxationDRD based on % ownership in paying corp

100% DRD for 80% or more owned affiliate 80% DRD for ownership of 20% up to 80% 70% DRD for ownership less than 20%

DRD limited to percentage timeslesser of taxable income or dividend income

Unless deducting DRD % x dividendincome creates or increases NOL

38

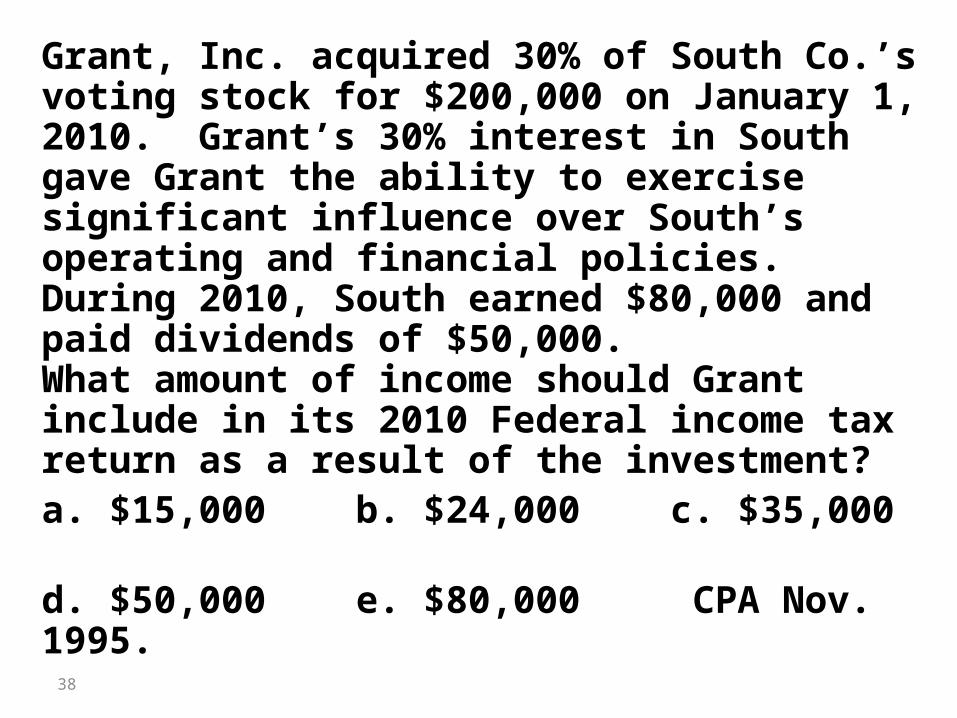

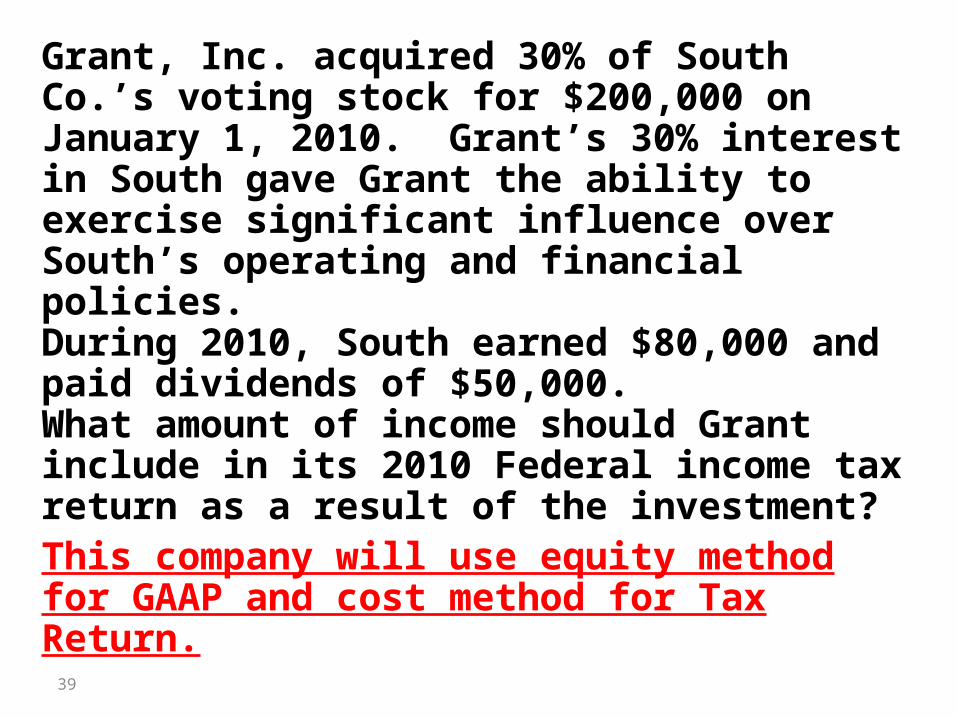

Grant, Inc. acquired 30% of South Co.’s voting stock for $200,000 on January 1, 2010. Grant’s 30% interest in South gave Grant the ability to exercise significant influence over South’s operating and financial policies. During 2010, South earned $80,000 and paid dividends of $50,000. What amount of income should Grant include in its 2010 Federal income tax return as a result of the investment?a. $15,000 b. $24,000 c. $35,000 d. $50,000 e. $80,000 CPA Nov. 1995.

39

Grant, Inc. acquired 30% of South Co.’s voting stock for $200,000 on January 1, 2010. Grant’s 30% interest in South gave Grant the ability to exercise significant influence over South’s operating and financial policies. During 2010, South earned $80,000 and paid dividends of $50,000. What amount of income should Grant include in its 2010 Federal income tax return as a result of the investment?This company will use equity method for GAAP and cost method for Tax Return.

40

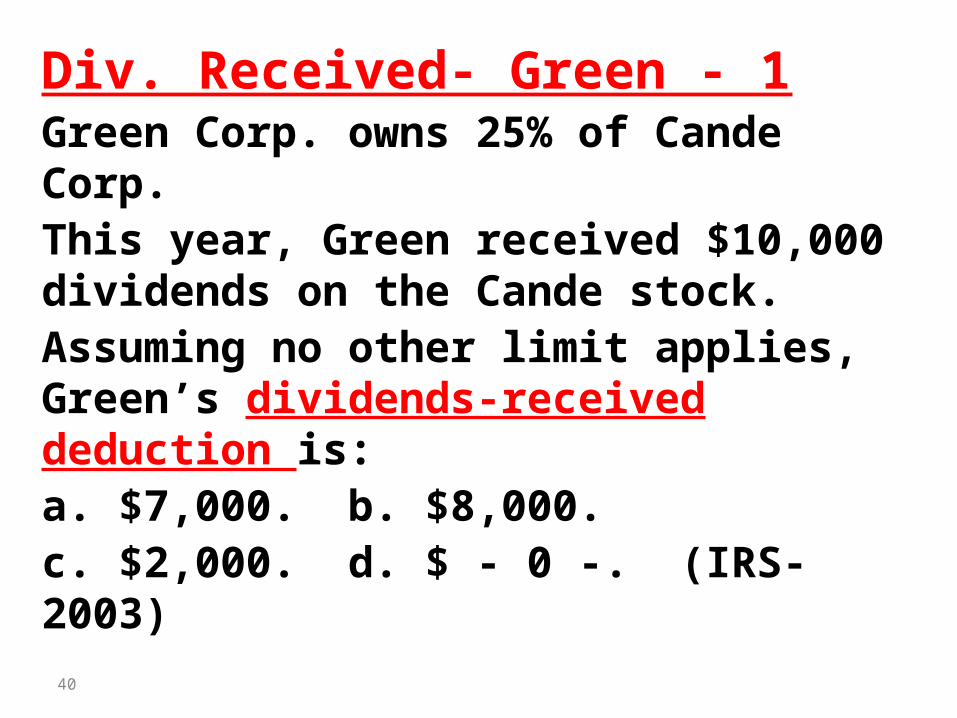

Div. Received- Green - 1Green Corp. owns 25% of Cande Corp. This year, Green received $10,000 dividends on the Cande stock. Assuming no other limit applies, Green’s dividends-received deduction is: a. $7,000. b. $8,000. c. $2,000. d. $ - 0 -. (IRS-2003)

41

Div. Received- Green – 12Green Corp. owns 25% of Cande Corp. This year, Green received $10,000 dividends on the Cande stock. Assuming no other limit applies, Green’s dividends-received deduction is: a. $7,000. b. $8,000. c. $2,000. d. $ - 0 -. (IRS-2003)

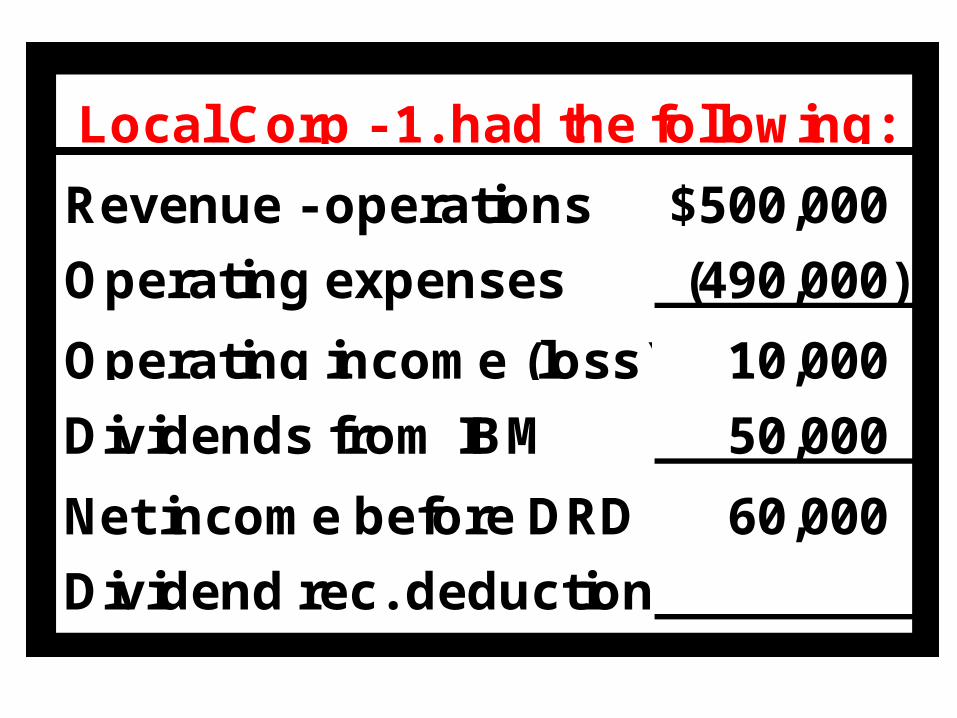

Revenue - operations $500,000

Operating expenses (490,000)

Operating income (loss) 10,000

Dividends from IBM 50,000

Net income before DRD 60,000

Dividend rec. deduction

Local Corp - 1. had the following:

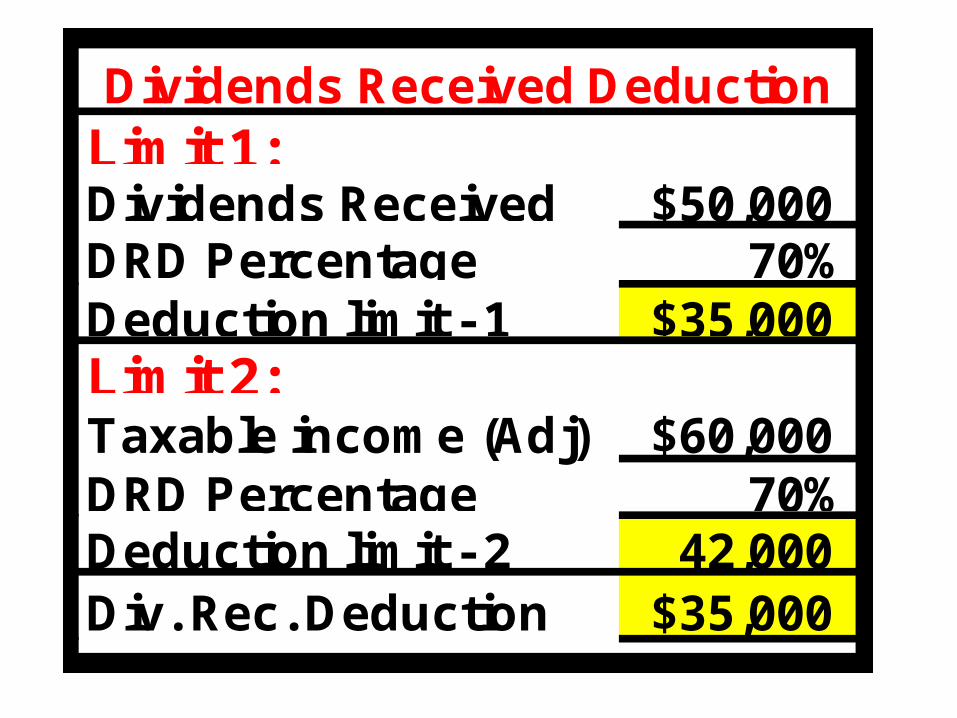

Limit 1:Dividends Received $50,000DRD Percentage 70%Deduction limit - 1 $35,000Limit 2:Taxable income (Adj) $60,000DRD Percentage 70%Deduction limit - 2 42,000 Div. Rec. Deduction $35,000

Dividends Received Deduction

Revenue - operations 500,000$

Operating expenses (510,000)

Operating income (loss) (10,000)

Dividends from IBM 50,000

Net income before DRD 40,000

Dividend rec. deduction

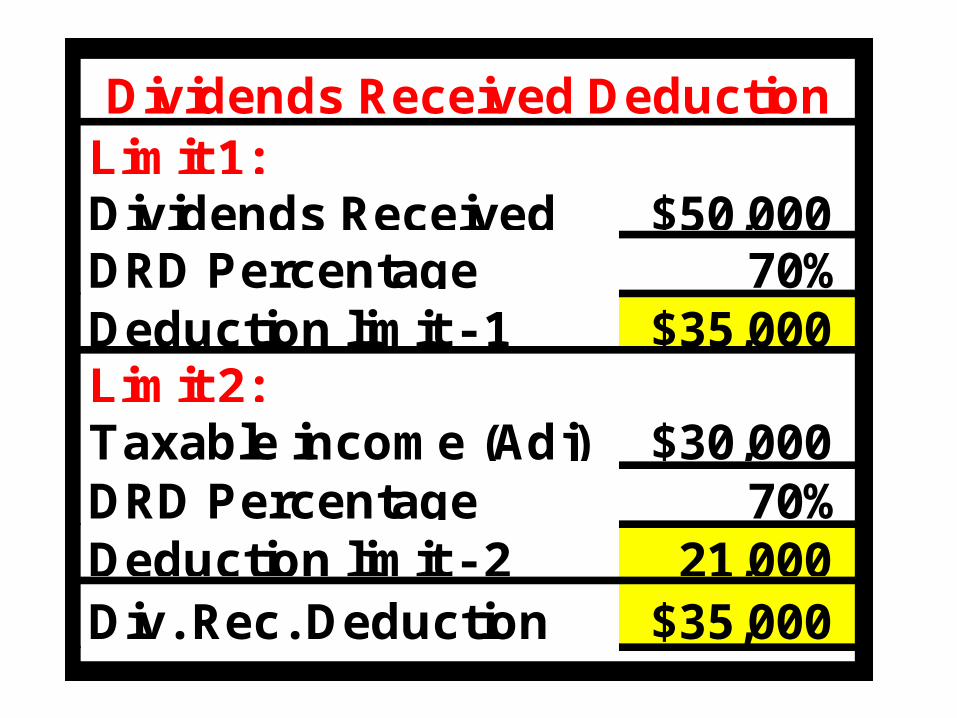

Local Corp - 2. had the following:

Limit 1:Dividends Received $50,000DRD PercentageDeduction limit - 1Limit 2:Taxable income (Adj) $40,000DRD PercentageDeduction limit - 2Div. Rec. Deduction

Dividends Received Deduction

Limit 1:Dividends Received $50,000DRD Percentage 70%Deduction limit - 1 $35,000Limit 2:Taxable income (Adj) $40,000DRD Percentage 70%Deduction limit - 2 28,000 Div. Rec. Deduction $28,000

Dividends Received Deduction

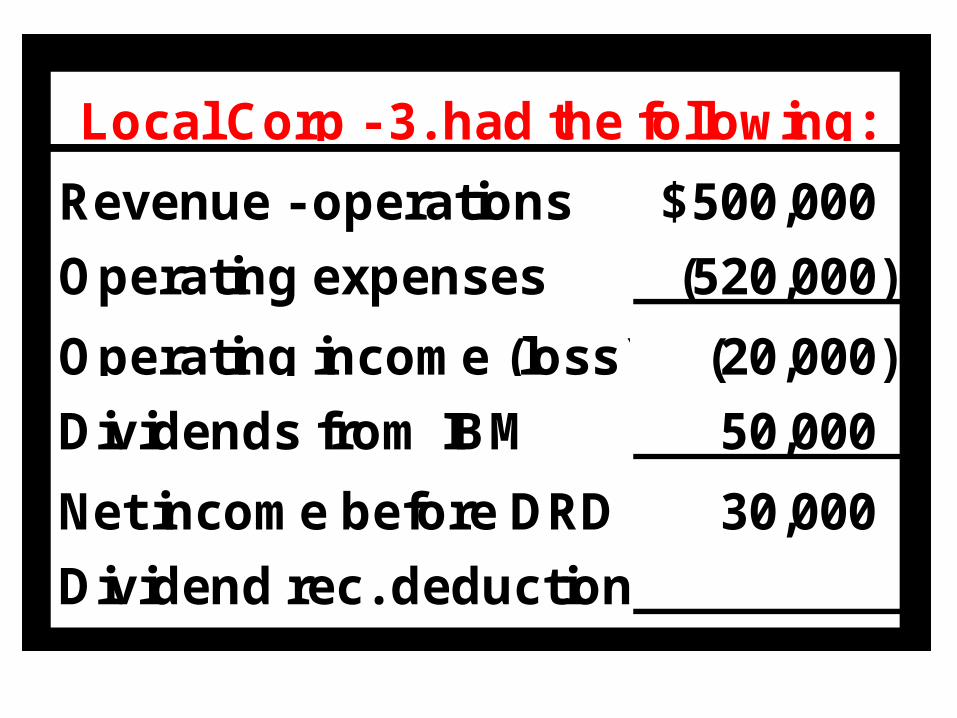

Revenue - operations 500,000$

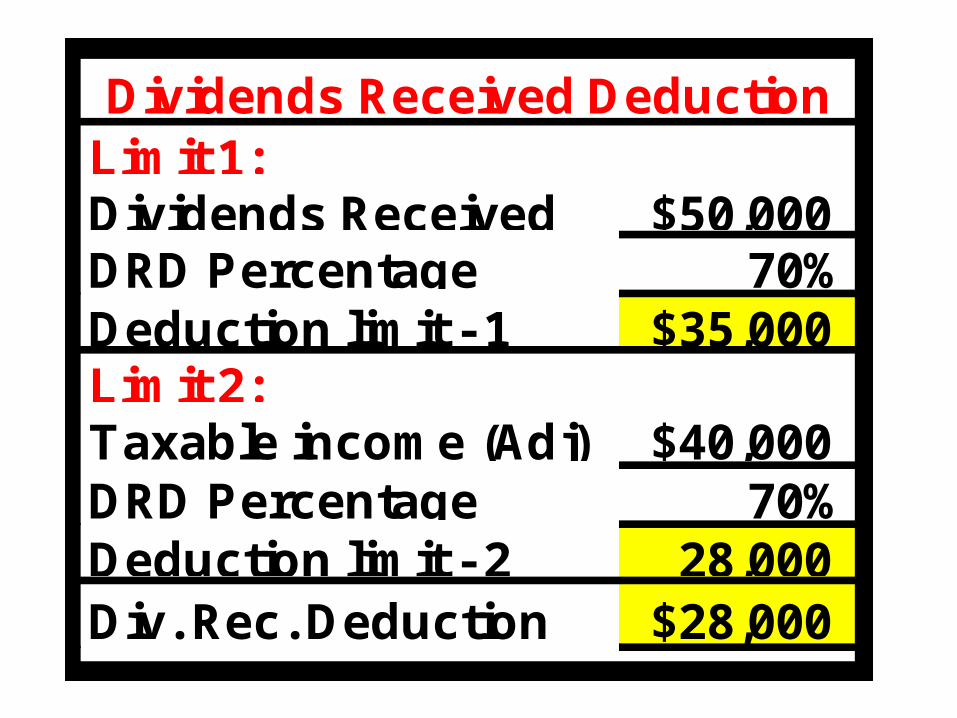

Operating expenses (520,000)

Operating income (loss) (20,000)

Dividends from IBM 50,000

Net income before DRD 30,000

Dividend rec. deduction

Local Corp - 3. had the following:

Limit 1:Dividends Received $50,000DRD Percentage 70%Deduction limit - 1 $35,000Limit 2:Taxable income (Adj) $30,000DRD Percentage 70%Deduction limit - 2 21,000 Div. Rec. Deduction $35,000

Dividends Received Deduction

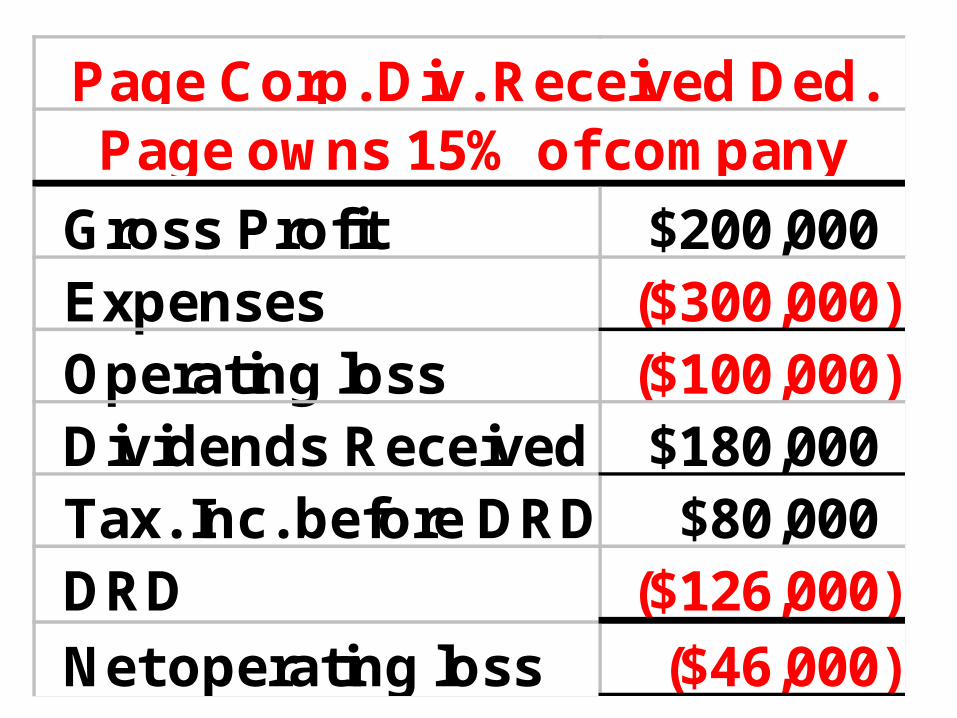

Gross Profit $200,000Expenses ($300,000)Operating loss ($100,000)Dividends Received $180,000Tax. Inc. before DRDDRDNet operating loss

Page Corp. Div. Received Ded.Page owns 15% of company

Gross Profit $200,000Expenses ($300,000)Operating loss ($100,000)Dividends Received $180,000Tax. Inc. before DRD $80,000DRD ($126,000)Net operating loss ($46,000)

Page Corp. Div. Received Ded.Page owns 15% of company

51

Spring Corp’s has income from business of $500,000 & expenses of $750,000. Spring also received dividends from the Acme Corp. of $100,000. Spring owns 25% Acme. What is Spring’s NOL for the year? a. ($150,000) b. ($0). c. ($220,000) d. ($230,000). (IRS Exam 2003)

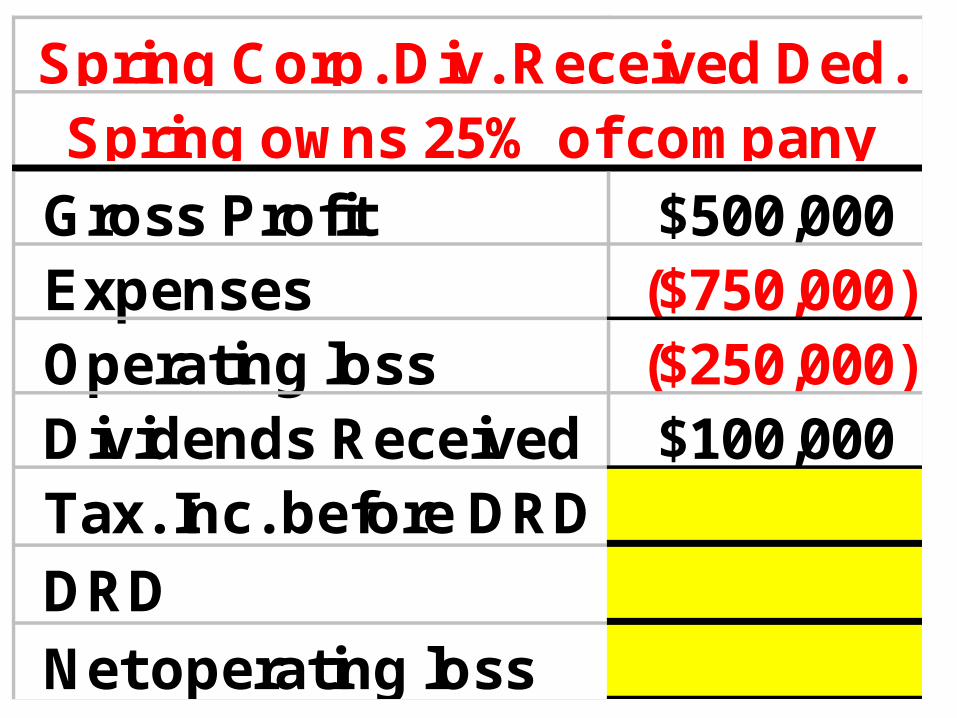

Gross Profit $500,000Expenses ($750,000)Operating loss ($250,000)Dividends Received $100,000Tax. Inc. before DRDDRDNet operating loss

Spring Corp. Div. Received Ded.Spring owns 25% of company

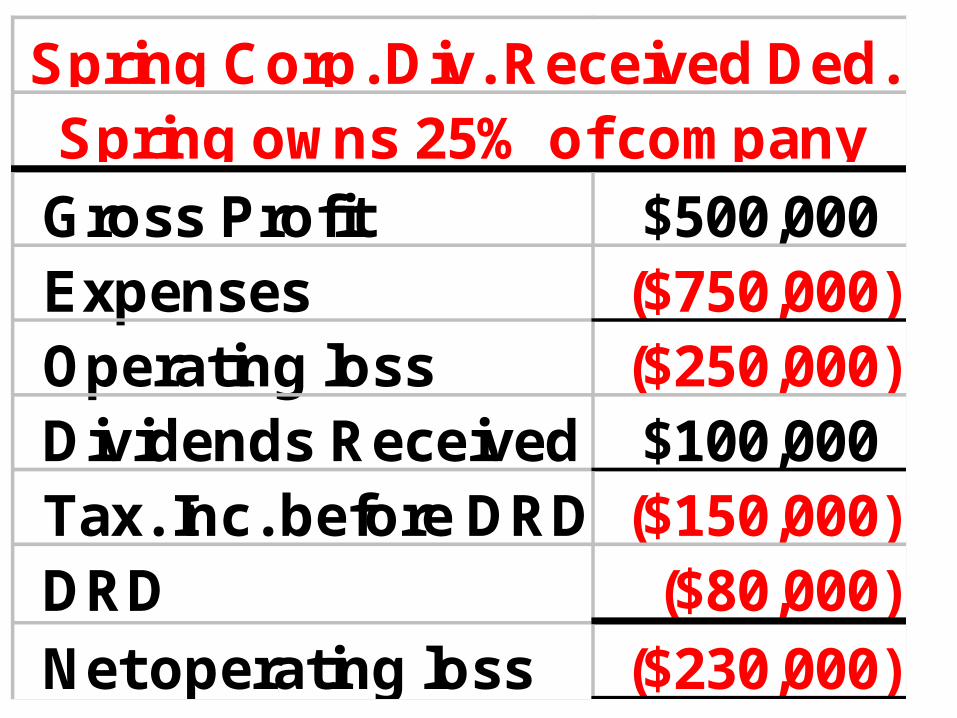

Gross Profit $500,000Expenses ($750,000)Operating loss ($250,000)Dividends Received $100,000Tax. Inc. before DRD ($150,000)DRD ($80,000)Net operating loss ($230,000)

Spring Corp. Div. Received Ded.Spring owns 25% of company

54

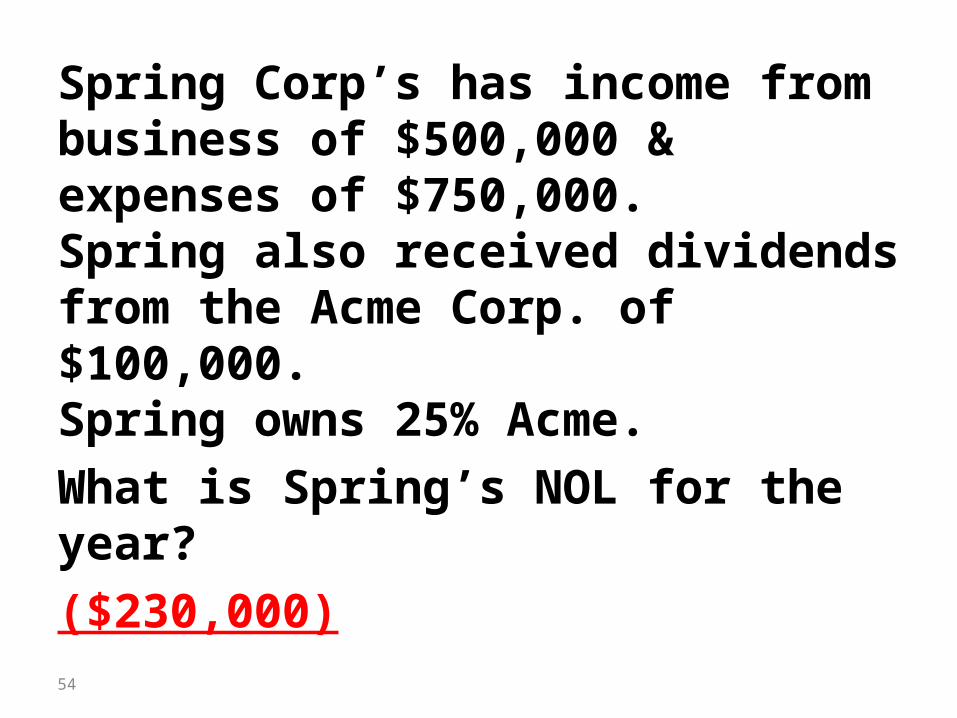

Spring Corp’s has income from business of $500,000 & expenses of $750,000. Spring also received dividends from the Acme Corp. of $100,000. Spring owns 25% Acme. What is Spring’s NOL for the year? ($230,000)

55

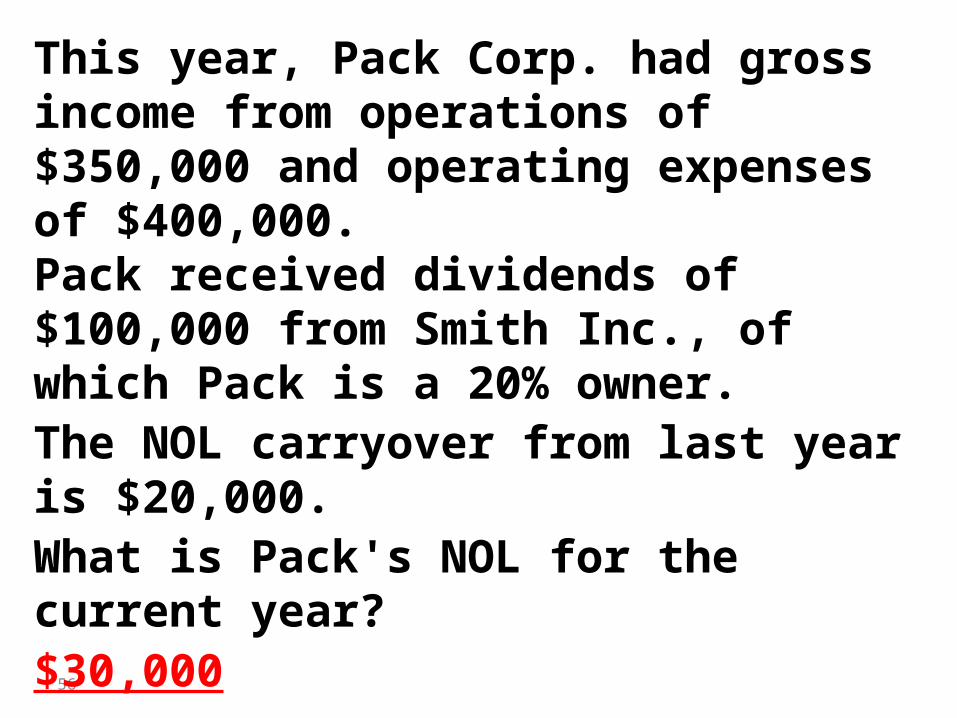

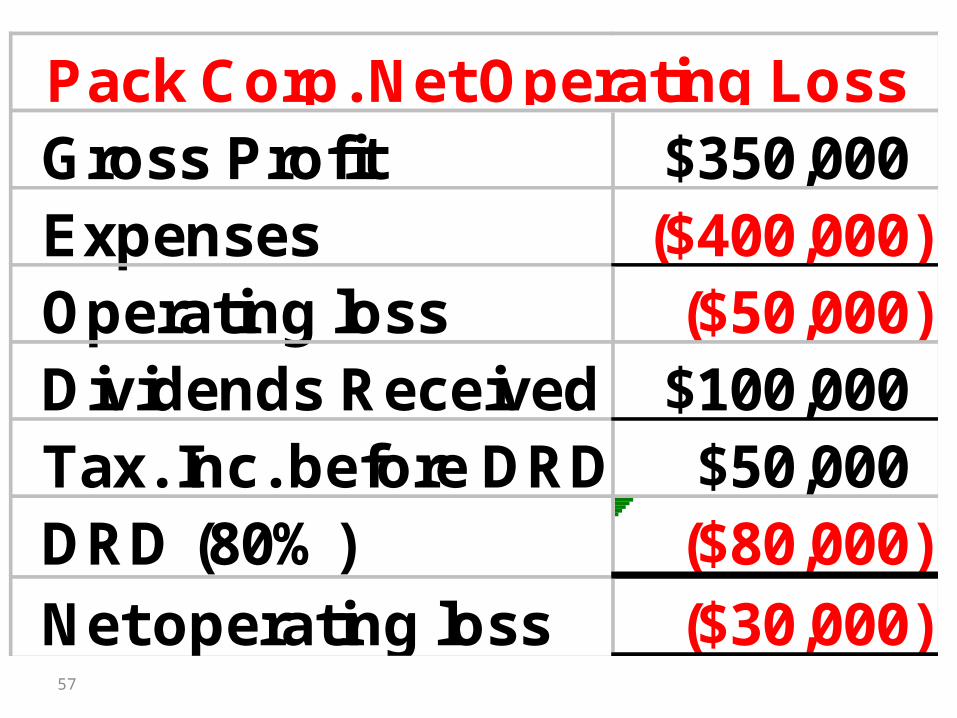

This year, Pack Corp. had gross income from operations of $350,000 and operating expenses of $400,000. Pack received dividends of $100,000 from Smith Inc., of which Pack is a 20% owner. The NOL carryover from last year is $20,000. What is Pack's NOL for the current year?a. $50,000 b. $30,000 c. $20,000 d. $10,000 IRS-1995

56

This year, Pack Corp. had gross income from operations of $350,000 and operating expenses of $400,000. Pack received dividends of $100,000 from Smith Inc., of which Pack is a 20% owner. The NOL carryover from last year is $20,000. What is Pack's NOL for the current year?$30,000

57

Gross Profit $350,000Expenses ($400,000)Operating loss ($50,000)Dividends Received $100,000Tax. Inc. before DRD $50,000DRD (80%) ($80,000)Net operating loss ($30,000)

Pack Corp. Net Operating Loss

58

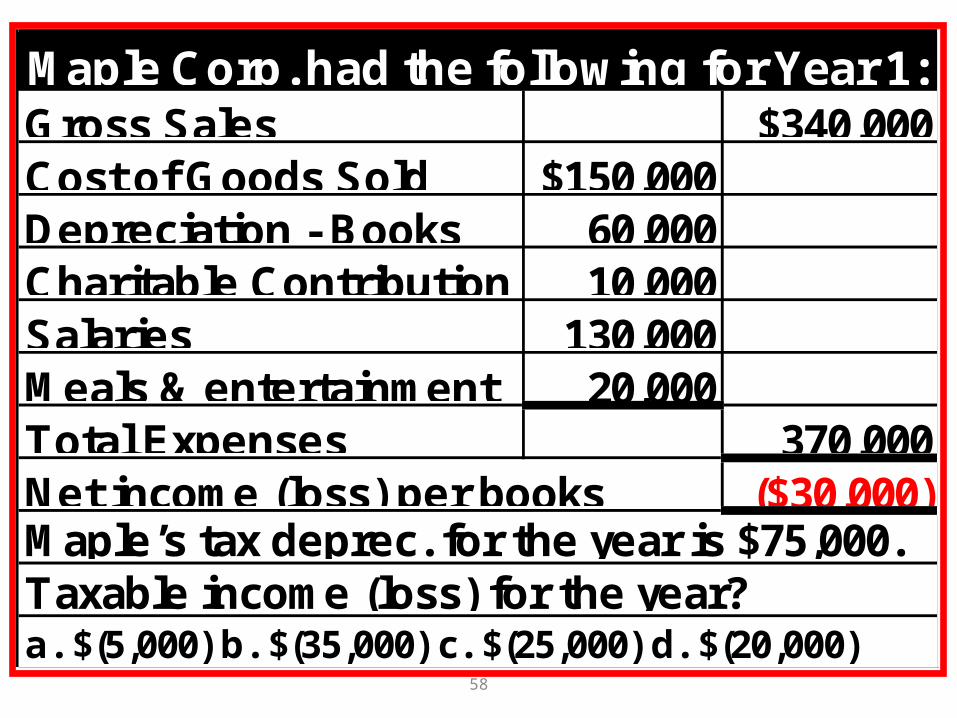

Gross Sales $340,000 Cost of Goods Sold $150,000Depreciation - Books 60,000Charitable Contribution 10,000Salaries 130,000Meals & entertainment 20,000Total Expenses 370,000

($30,000)

Maple Corp. had the following for Year 1:

a. $(5,000) b. $(35,000) c. $(25,000) d. $(20,000)

Net income (loss) per books

Taxable income (loss) for the year?Maple’s tax deprec. for the year is $75,000.

59

Maple Corporation Facts Return

Gross Sales $340,000

Cost of Goods Sold 150,000

Depreciation - Books 60,000 Depreciation - TaxCharitable Contribution 10,000

Salaries 130,000 Meals & entertainment 20,000

Total Expenses 370,000

Net income (loss)-books ($30,000)Taxable income?

60

Maple Corporation Facts Return

Gross Sales $340,000 $340,000

Cost of Goods Sold 150,000 150,000

Depreciation - Books 60,000 Depreciation - Tax 75,000 Charitable Contribution 10,000 -

Salaries 130,000 130,000 Meals & entertainment 20,000 10,000

Total Expenses 370,000 365,000

Net income (loss)-books ($30,000)

($25,000)Taxable income?

61

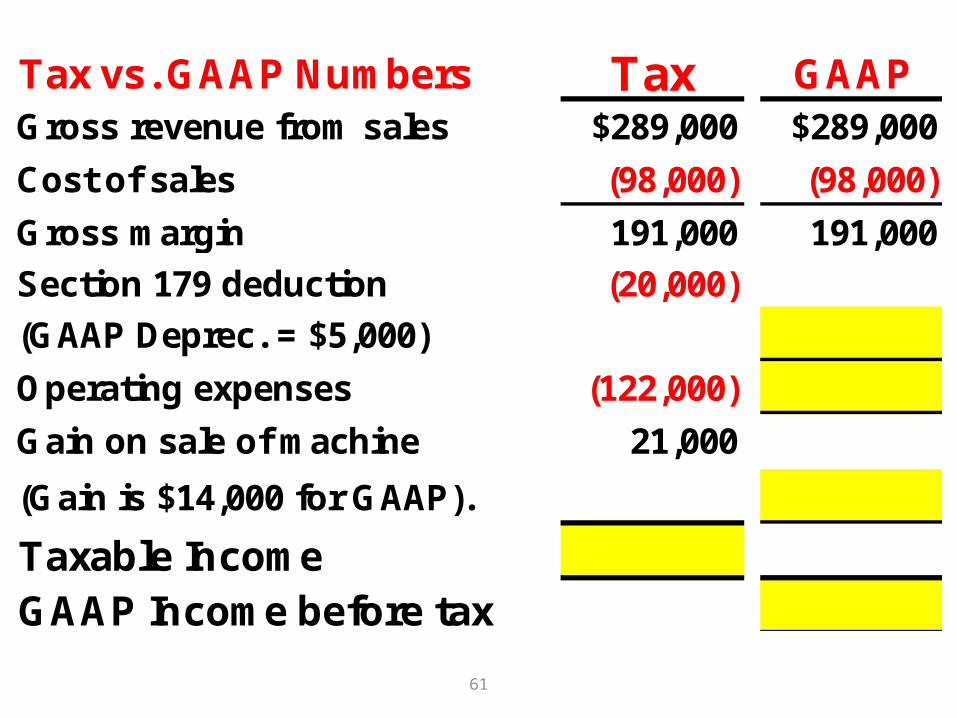

Tax vs. GAAP Numbers Tax GAAPGross revenue from sales $289,000 $289,000

Cost of sales (98,000) (98,000)

Gross margin 191,000 191,000

Section 179 deduction (20,000)

(GAAP Deprec. = $5,000)

Operating expenses (122,000)

Gain on sale of machine 21,000

(Gain is $14,000 for GAAP).

Taxable IncomeGAAP Income before tax

62

Tax vs. GAAP Numbers Tax GAAPGross revenue from sales $289,000 $289,000

Cost of sales (98,000) (98,000)

Gross margin 191,000 191,000

Section 179 deduction (20,000)

(GAAP Deprec. = $5,000) (5,000)

Operating expenses (122,000) (122,000)

Gain on sale of machine 21,000

(Gain is $14,000 for GAAP). 14,000

Taxable Income $70,000

GAAP Income before tax $78,000Impact on def. tax account (40% tax rate)?

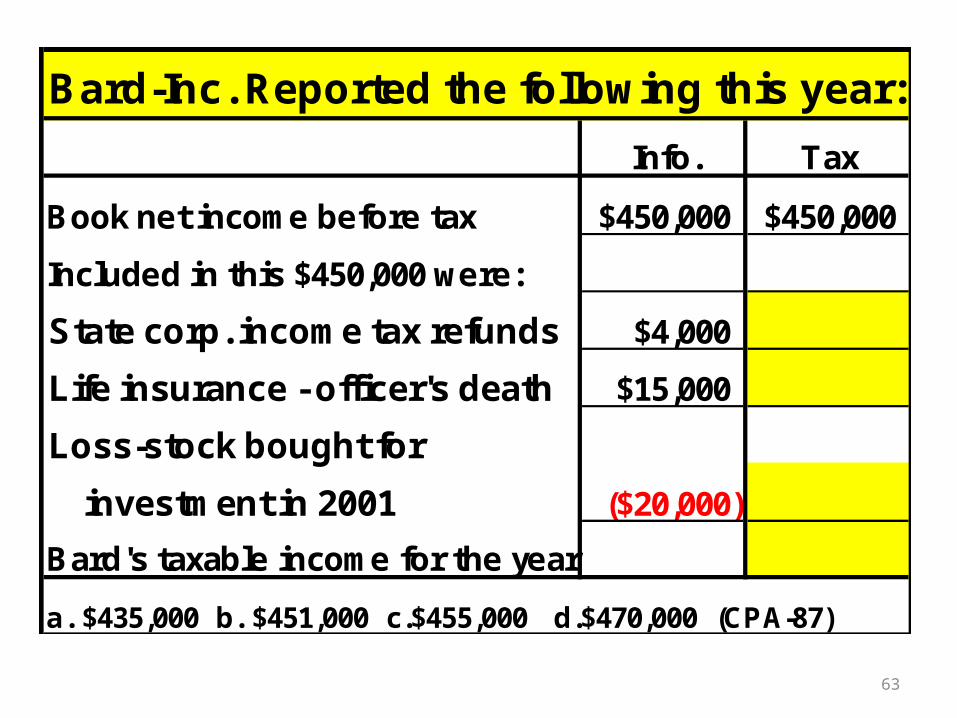

63

Info. Tax

Book net income before tax $450,000 $450,000

Included in this $450,000 were:

State corp. income tax refunds $4,000

Life insurance - officer's death $15,000

Loss-stock bought for

investment in 2001 ($20,000)

Bard's taxable income for the year

a. $435,000 b. $451,000 c.$455,000 d.$470,000 (CPA-87)

Bard-Inc. Reported the following this year:

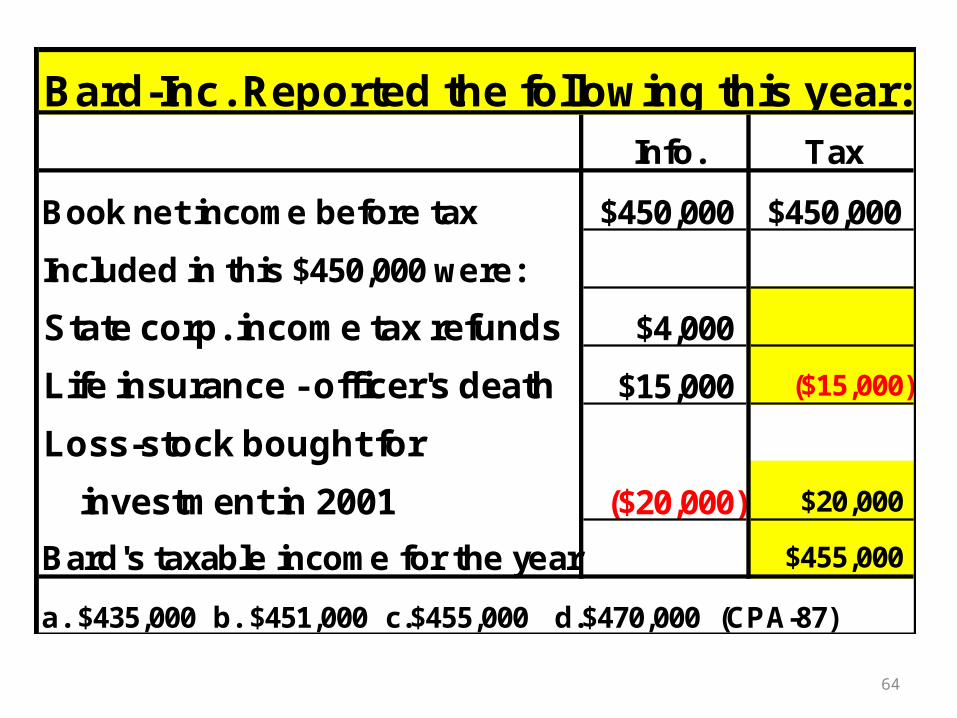

64

Info. Tax

Book net income before tax $450,000 $450,000

Included in this $450,000 were:

State corp. income tax refunds $4,000

Life insurance - officer's death $15,000 ($15,000)

Loss-stock bought for

investment in 2001 ($20,000) $20,000

Bard's taxable income for the year $455,000

a. $435,000 b. $451,000 c.$455,000 d.$470,000 (CPA-87)

Bard-Inc. Reported the following this year:

65

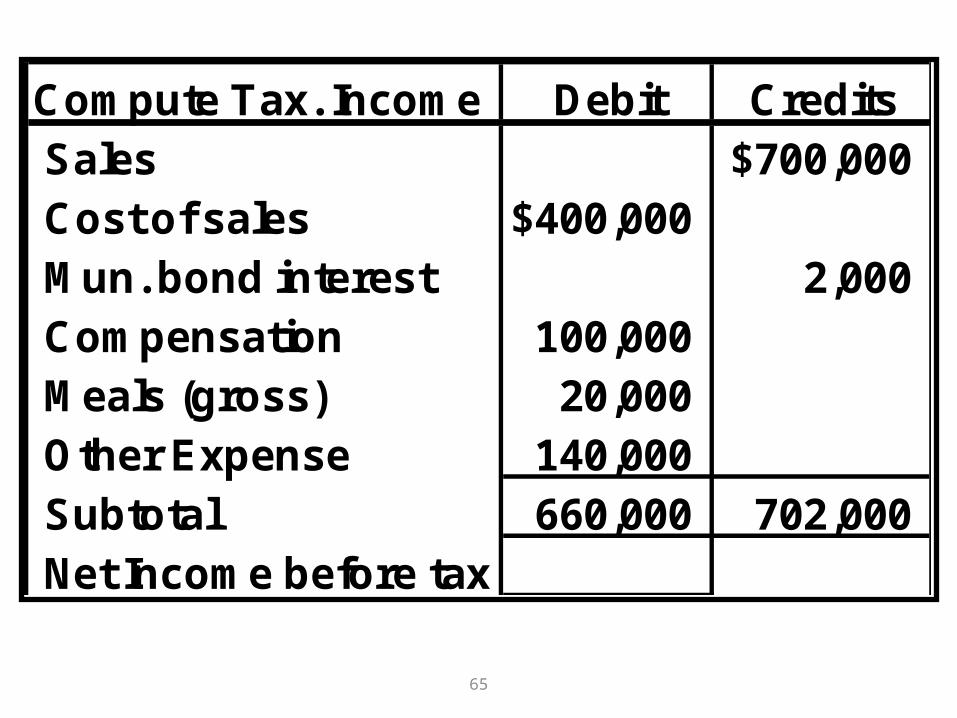

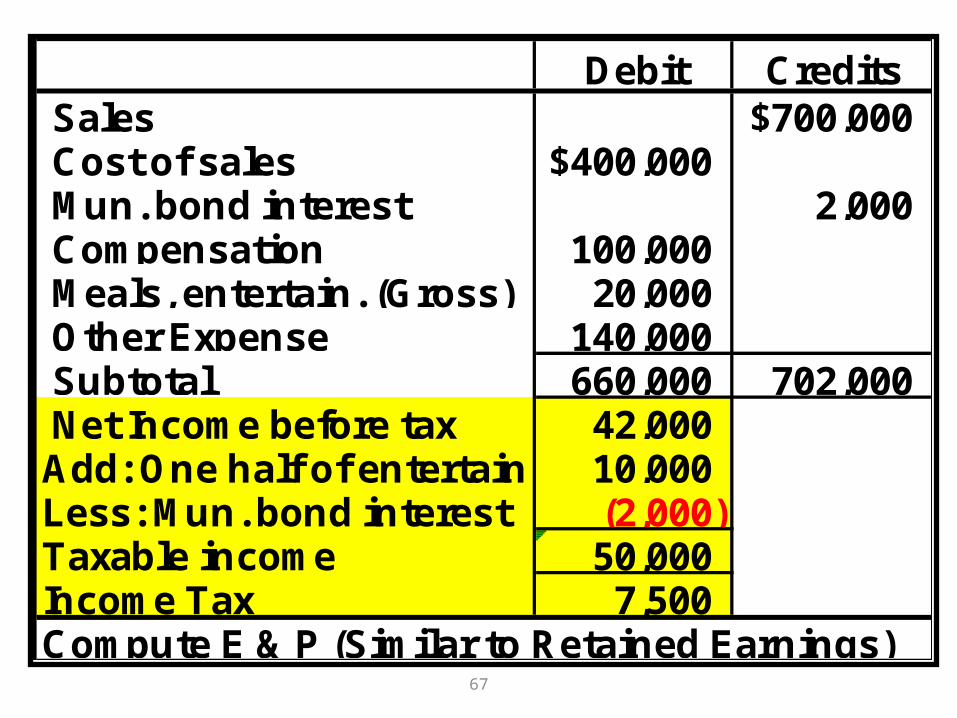

Compute Tax. Income Debit Credits Sales $700,000 Cost of sales $400,000 Mun. bond interest 2,000 Compensation 100,000 Meals (gross) 20,000 Other Expense 140,000 Subtotal 660,000 702,000 Net Income before tax

66

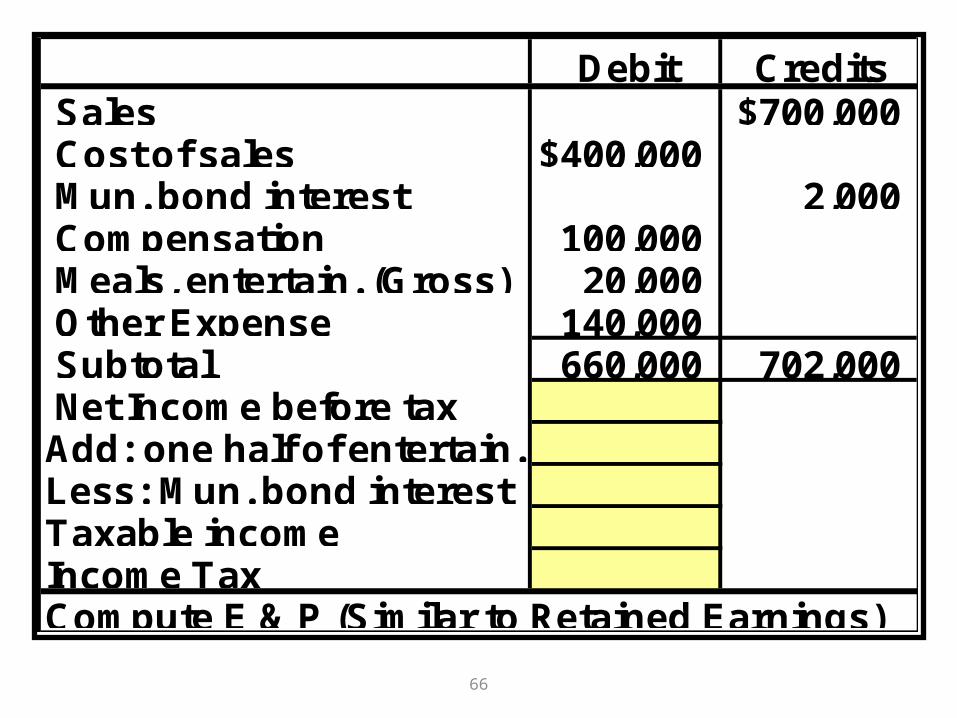

Debit Credits Sales $700,000 Cost of sales $400,000 Mun. bond interest 2,000 Compensation 100,000 Meals, entertain. (Gross) 20,000 Other Expense 140,000 Subtotal 660,000 702,000 Net Income before taxAdd: one half of entertain.Less: Mun. bond interestTaxable incomeIncome TaxCompute E & P (Similar to Retained Earnings)

67

Debit Credits Sales $700,000 Cost of sales $400,000 Mun. bond interest 2,000 Compensation 100,000 Meals, entertain. (Gross) 20,000 Other Expense 140,000 Subtotal 660,000 702,000 Net Income before tax 42,000 Add: One half of entertain. 10,000 Less: Mun. bond interest (2,000)Taxable income 50,000 Income Tax 7,500 Compute E & P (Similar to Retained Earnings)

68

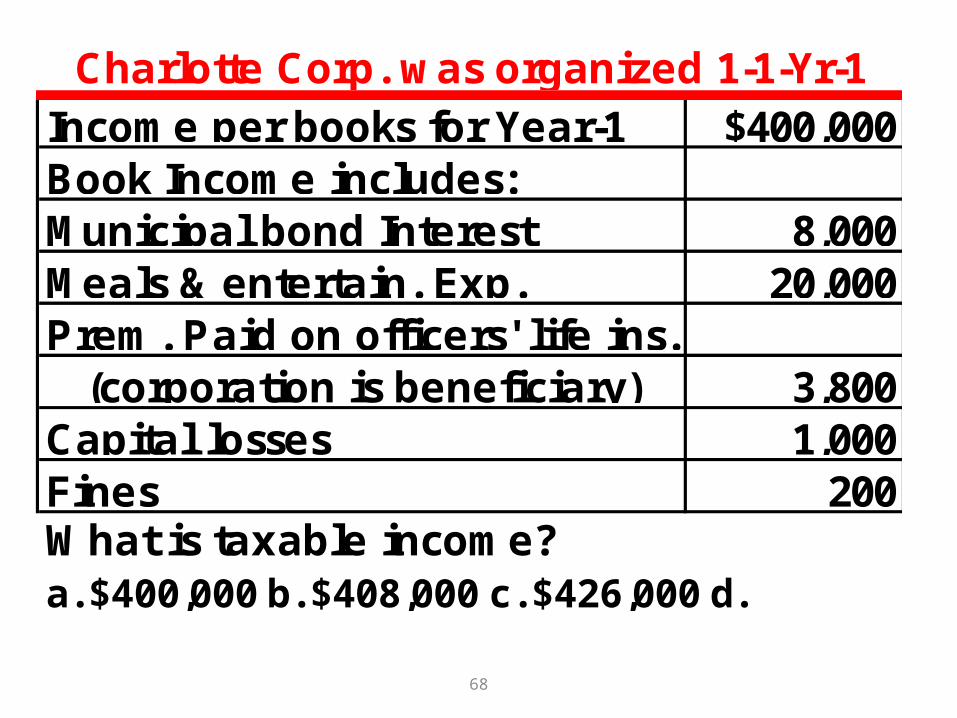

Income per books for Year-1 $400,000 Book Income includes:Municipal bond Interest 8,000Meals & entertain. Exp. 20,000Prem. Paid on officers' life ins. (corporation is beneficiary) 3,800Capital losses 1,000Fines 200What is taxable income?a. $400,000 b. $408,000 c. $426,000 d.

Charlotte Corp. was organized 1-1-Yr-1

69

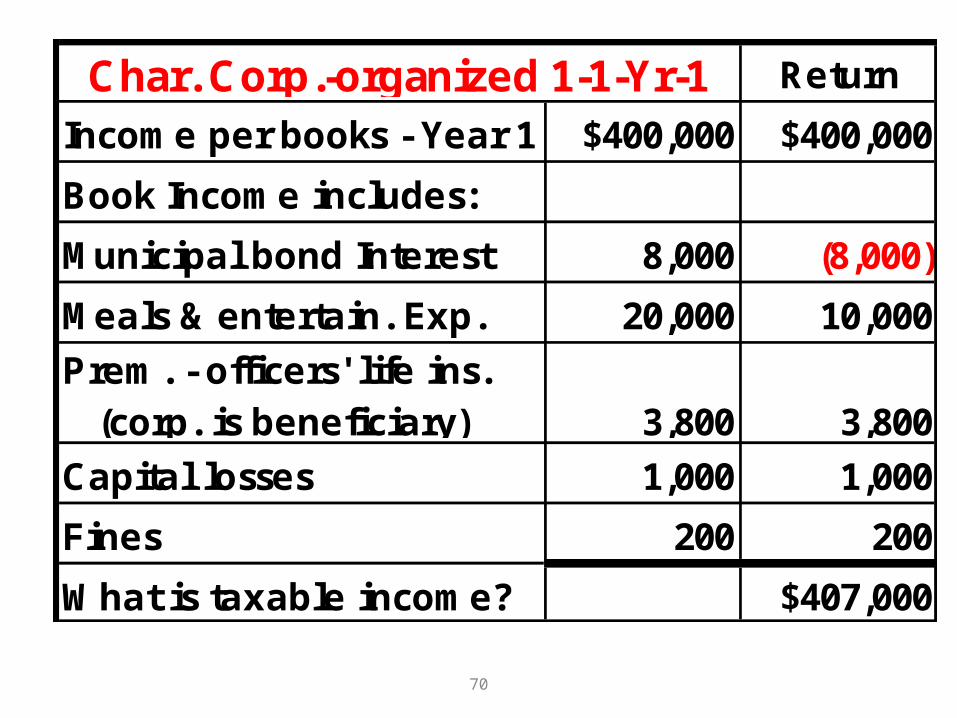

Return

Income per books - Year 1 $400,000 $400,000

Book Income includes:

Municipal bond Interest 8,000

Meals & entertain. Exp. 20,000

Prem. - officers' life ins.

(corp. is beneficiary) 3,800

Capital losses 1,000

Fines 200

What is taxable income?

Char. Corp.-organized 1-1-Yr-1

70

Return

Income per books - Year 1 $400,000 $400,000

Book Income includes:

Municipal bond Interest 8,000 (8,000)

Meals & entertain. Exp. 20,000 10,000

Prem. - officers' life ins. (corp. is beneficiary) 3,800 3,800

Capital losses 1,000 1,000

Fines 200 200

What is taxable income? $407,000

Char. Corp.-organized 1-1-Yr-1

71

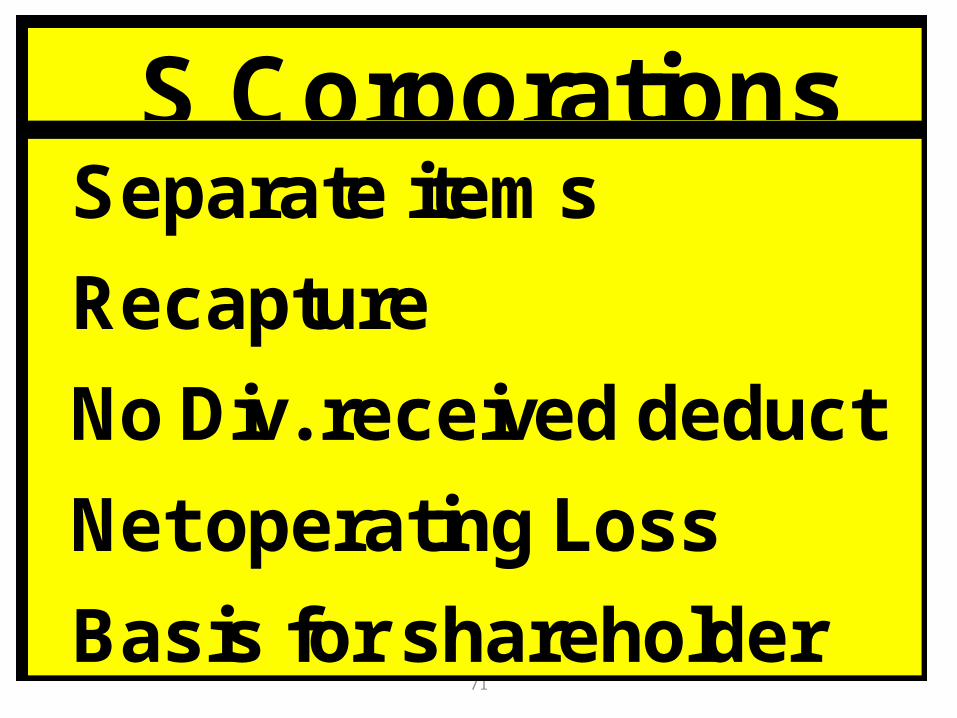

S Corporations Separate items

Recapture

No Div. received deduct

Net operating Loss

Basis for shareholder

S Corporation• Income and expenses are reported by the

shareholders according to their ownership interest– Items which would receive special treatment

on a shareholder’s return are reported separately

– Losses are deductible subject to the three limitations faced by partnerships

• S corporations are also subject to the corporate depreciation recapture rules for Section 1250 property

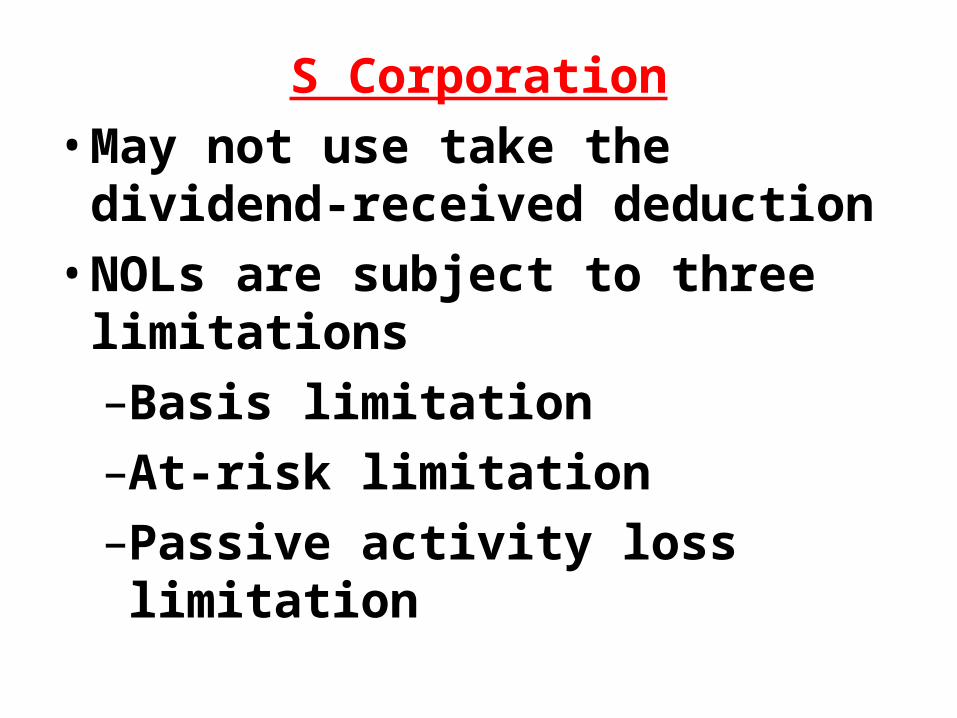

S Corporation• May not use take the dividend-

received deduction• NOLs are subject to three

limitations–Basis limitation–At-risk limitation–Passive activity loss limitation

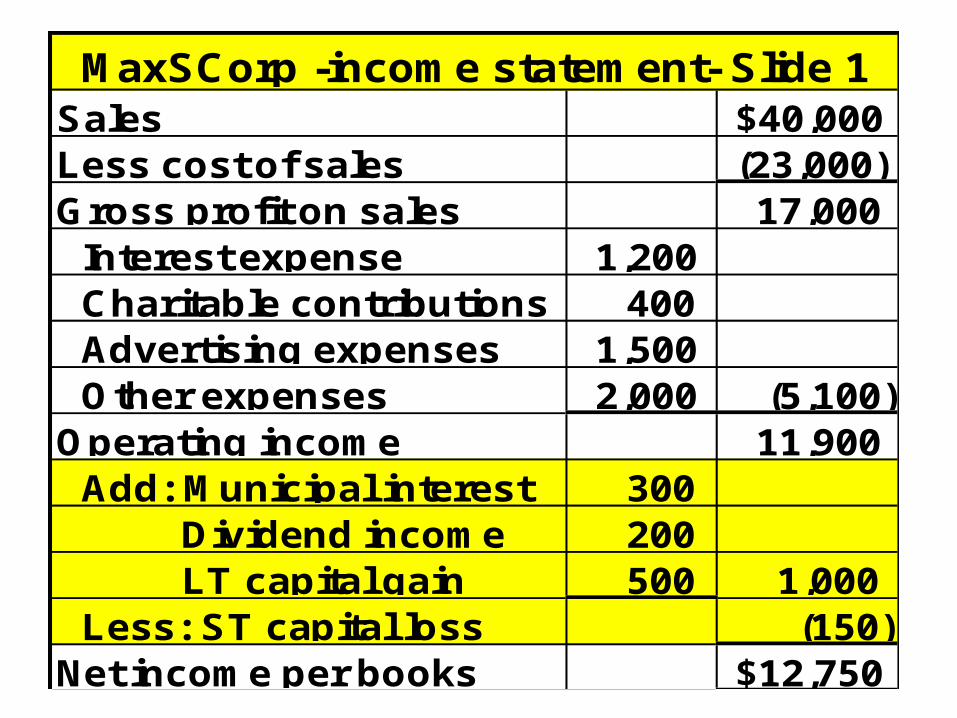

Sales $40,000 Less cost of sales (23,000)Gross profit on sales 17,000

Interest expense 1,200 Charitable contributions 400 Advertising expenses 1,500 Other expenses 2,000 (5,100)

Operating income 11,900 Add: Municipal interest 300

Dividend income 200 LT capital gain 500 1,000

Less: ST capital loss (150)Net income per books $12,750

MaxSCorp -income statement- Slide 1

MaxSCorp-Slide 2Net income per books $ 12,750 Separate itemsLess: Mun. interest 300

Div. income 200 LT capital gain 500 (1,000)

Subtotal 11,750 Add: Charitable cont. 400

ST capital loss 150 550 Taxable income $ 12,300

Section 1363(b)

76

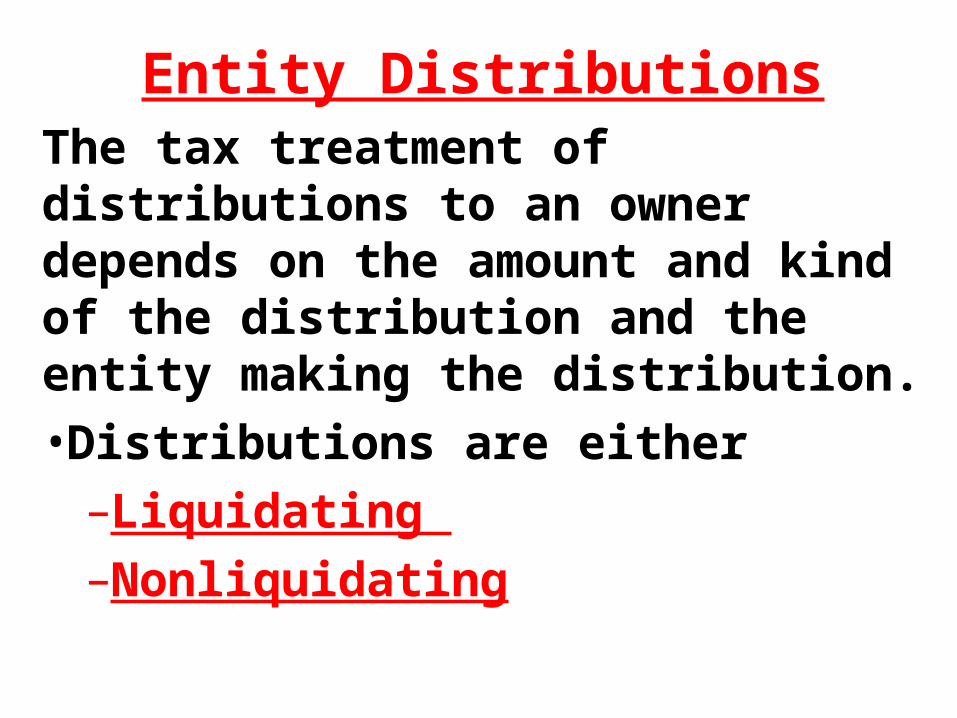

DistributionsProprietorships

Partnerships

Corporations

S Corporations

Entity DistributionsThe tax treatment of distributions to an owner depends on the amount and kind of the distribution and the entity making the distribution.•Distributions are either

–Liquidating –Nonliquidating

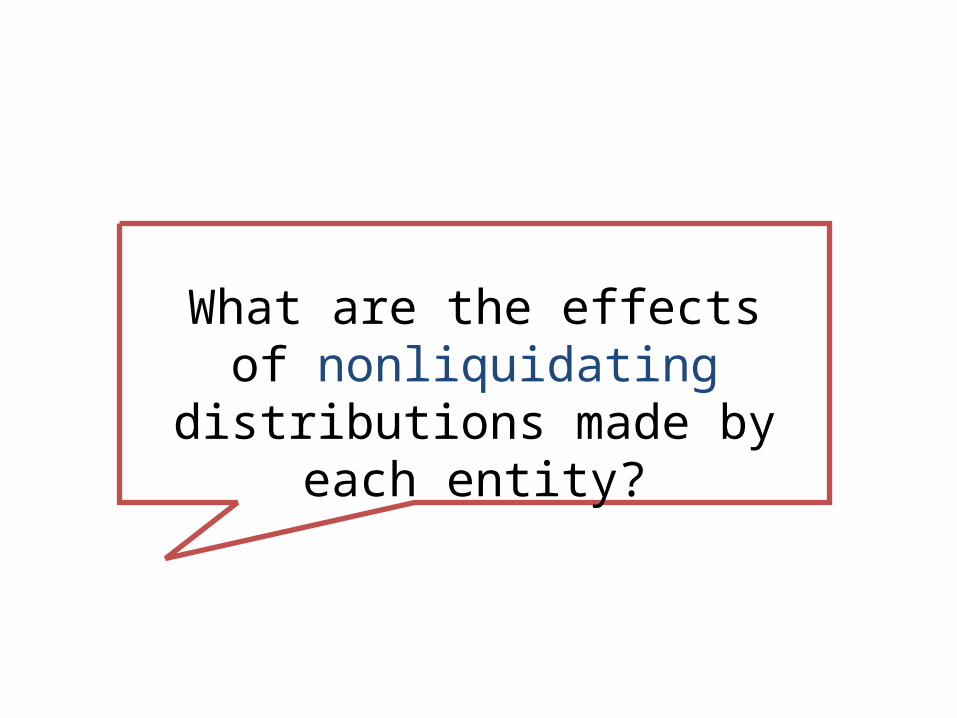

What are the effects of nonliquidating distributions

made by each entity?

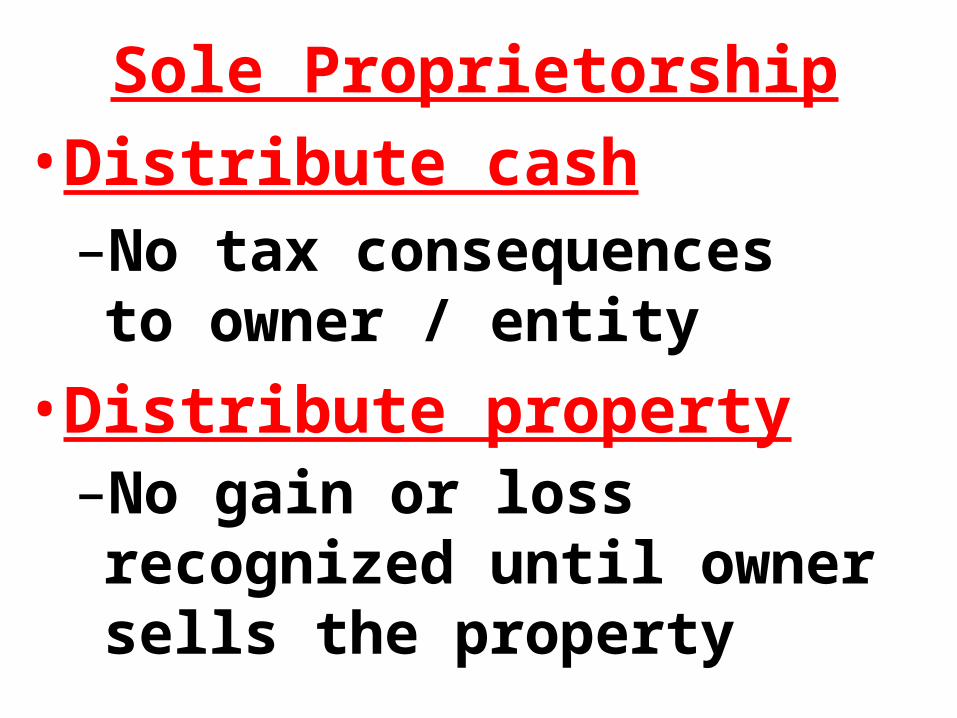

Sole Proprietorship• Distribute cash

–No tax consequences to owner / entity

• Distribute property–No gain or loss recognized until

owner sells the property

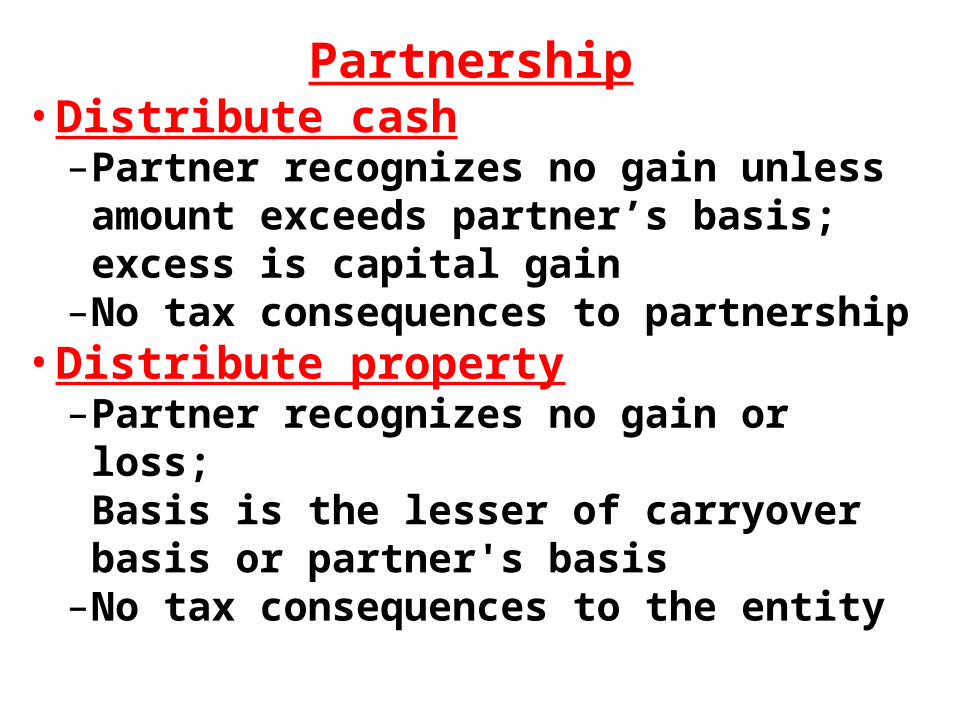

Partnership• Distribute cash

–Partner recognizes no gain unless amount exceeds partner’s basis; excess is capital gain

–No tax consequences to partnership• Distribute property

–Partner recognizes no gain or loss; Basis is the lesser of carryover basis or partner's basis

–No tax consequences to the entity

81

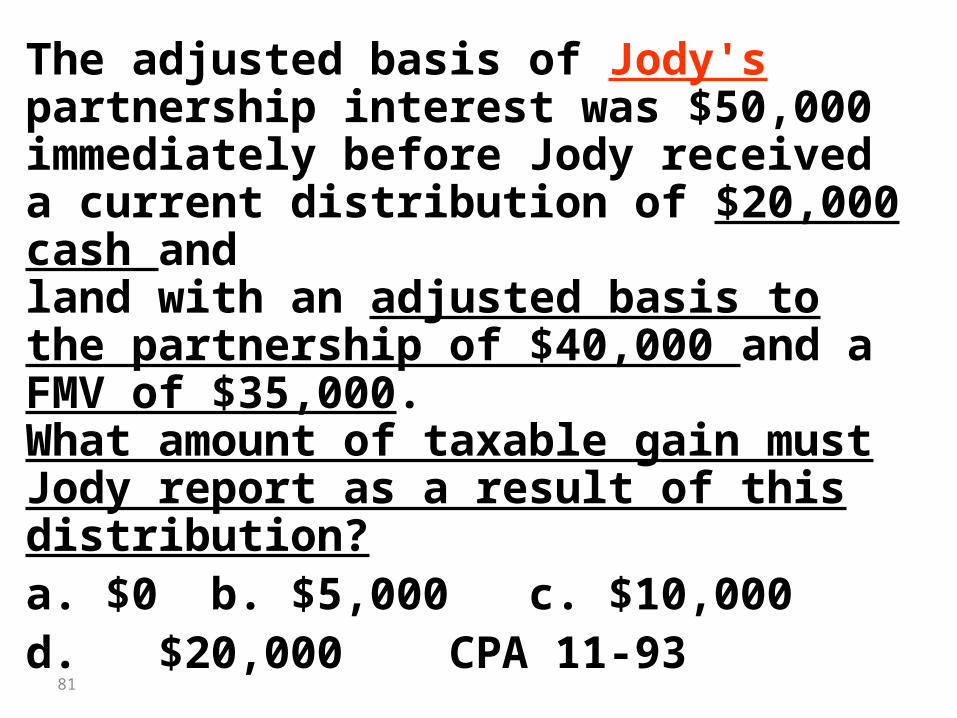

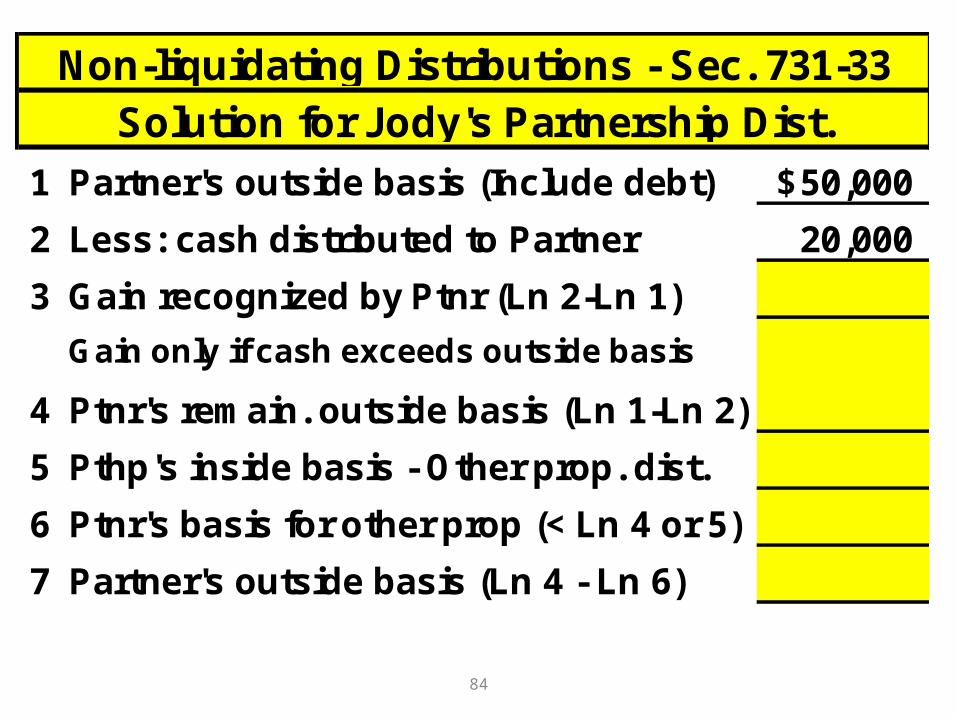

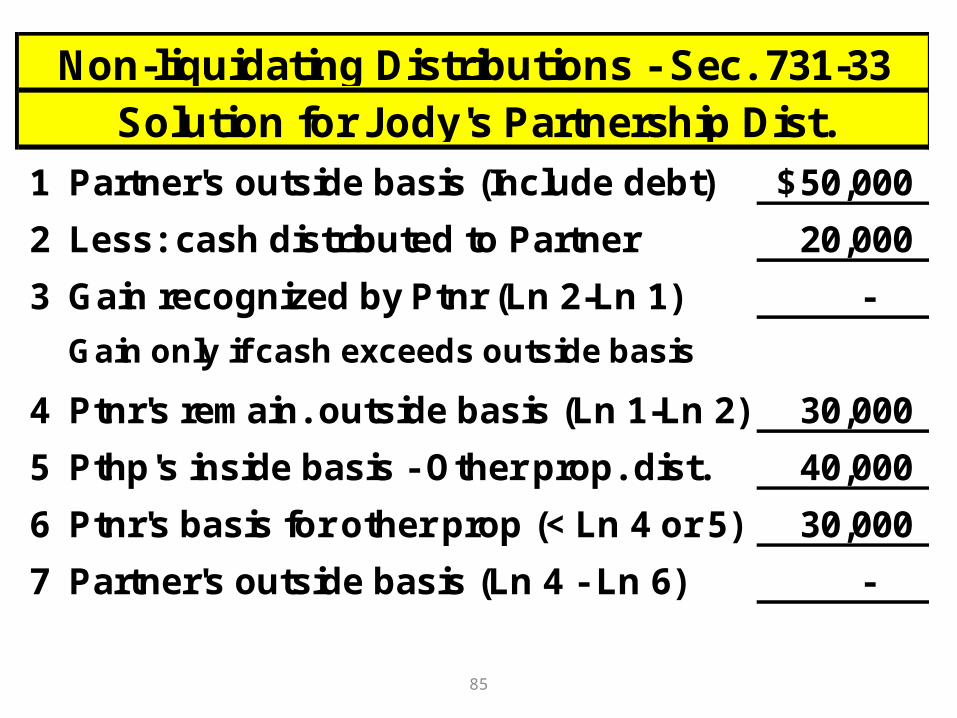

The adjusted basis of Jody's partnership interest was $50,000 immediately before Jody received a current distribution of $20,000 cash and land with an adjusted basis to the partnership of $40,000 and a FMV of $35,000. What amount of taxable gain must Jody report as a result of this distribution?a. $0 b. $5,000 c. $10,000 d. $20,000 CPA 11-93

82

The adjusted basis of Jody's partnership interest was $50,000 immediately before Jody received a current distribution of $20,000 cash and land with an adjusted basis to the partnership of $40,000 and a FMV of $35,000. What is Jody's basis in the land ?a. $0 b. $30,000 c. $35,000 d. $40,000 CPA 11-93

83

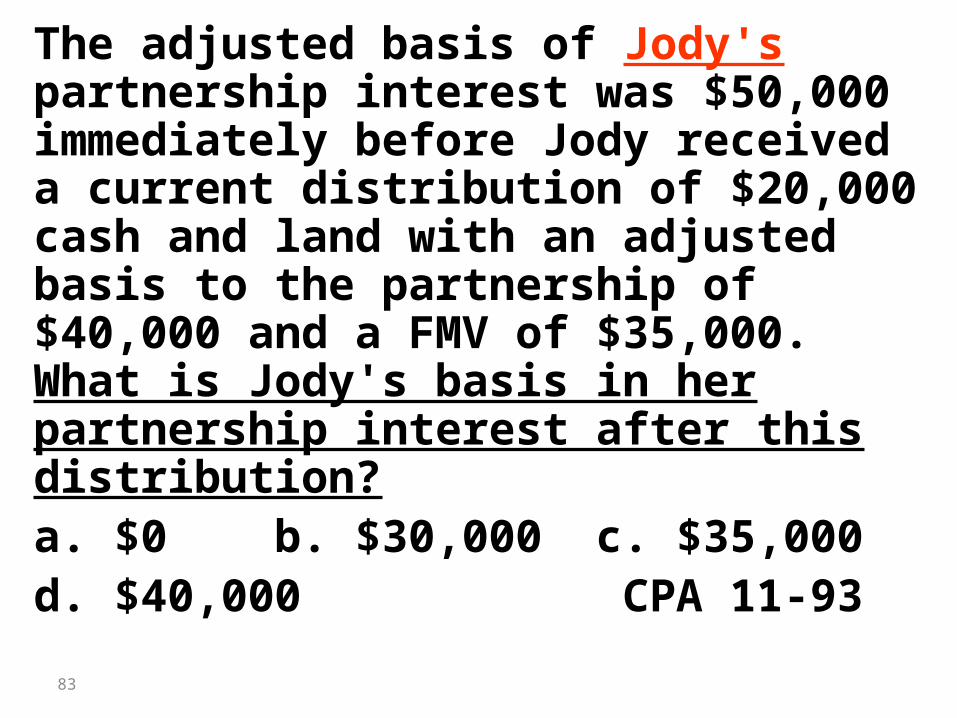

The adjusted basis of Jody's partnership interest was $50,000 immediately before Jody received a current distribution of $20,000 cash and land with an adjusted basis to the partnership of $40,000 and a FMV of $35,000. What is Jody's basis in her partnership interest after this distribution?a. $0 b. $30,000 c. $35,000 d. $40,000 CPA 11-93

84

1 Partner's outside basis (Include debt) 50,000$

2 Less: cash distributed to Partner 20,000

3 Gain recognized by Ptnr (Ln 2-Ln 1)

Gain only if cash exceeds outside basis

4 Ptnr's remain. outside basis (Ln 1-Ln 2)

5 Pthp's inside basis - Other prop. dist.

6 Ptnr's basis for other prop (< Ln 4 or 5)

7 Partner's outside basis (Ln 4 - Ln 6)

Non-liquidating Distributions - Sec. 731-33Solution for Jody's Partnership Dist.

85

1 Partner's outside basis (Include debt) 50,000$

2 Less: cash distributed to Partner 20,000

3 Gain recognized by Ptnr (Ln 2-Ln 1) -

Gain only if cash exceeds outside basis

4 Ptnr's remain. outside basis (Ln 1-Ln 2) 30,000

5 Pthp's inside basis - Other prop. dist. 40,000

6 Ptnr's basis for other prop (< Ln 4 or 5) 30,000

7 Partner's outside basis (Ln 4 - Ln 6) -

Non-liquidating Distributions - Sec. 731-33Solution for Jody's Partnership Dist.

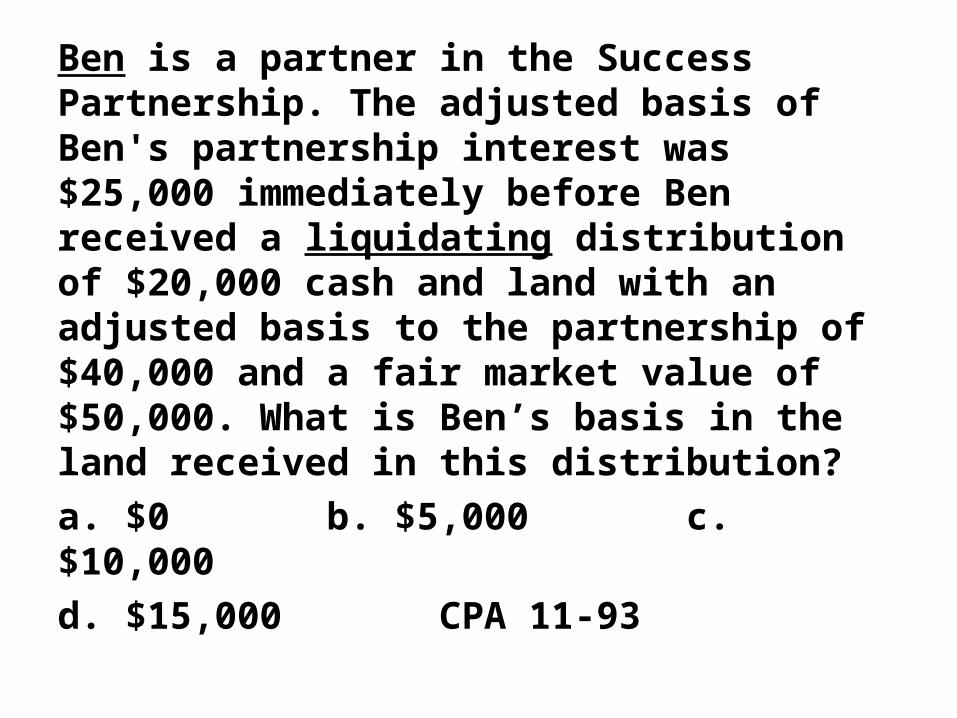

Ben is a partner in the Success Partnership. The adjusted basis of Ben's partnership interest was $25,000 immediately before Ben received a liquidating distribution of $20,000 cash and land with an adjusted basis to the partnership of $40,000 and a fair market value of $50,000. What is Ben’s basis in the land received in this distribution?a. $0 b. $5,000 c. $10,000 d. $15,000 CPA 11-93

1 Ben's outside basis (Include debt) 25,000

2 Less: Cash distributed to Ben

3 Gain recognized by Ben (Ln 2-Ln 1)

4 Ben's remain. outside basis (Ln 1-Ln 2)

5 Ben's basis for other property Line 4

6 Ben's loss (Excess of Line 4 over 5)(Loss can be recognized only if noproperty is distributed other than cash,unrealized receivables and inventory.)

7 Ben's remaining partnership basis $-0-

Liquidating Distributions - Sec. 731-33Distribution to Ben

1 Ben's outside basis (Include debt) 25,000

2 Less: Cash distributed to Ben 20,000

3 Gain recognized by Ben (Ln 2-Ln 1)

4 Ben's remain. outside basis (Ln 1-Ln 2) 5,000

5 Ben's basis for other property Line 4 5,000

6 Ben's loss (Excess of Line 4 over 5)(Loss can be recognized only if noproperty is distributed other than cash,unrealized receivables and inventory.)

7 Ben's remaining partnership basis $-0-

Liquidating Distributions - Sec. 731-33Distribution to Ben

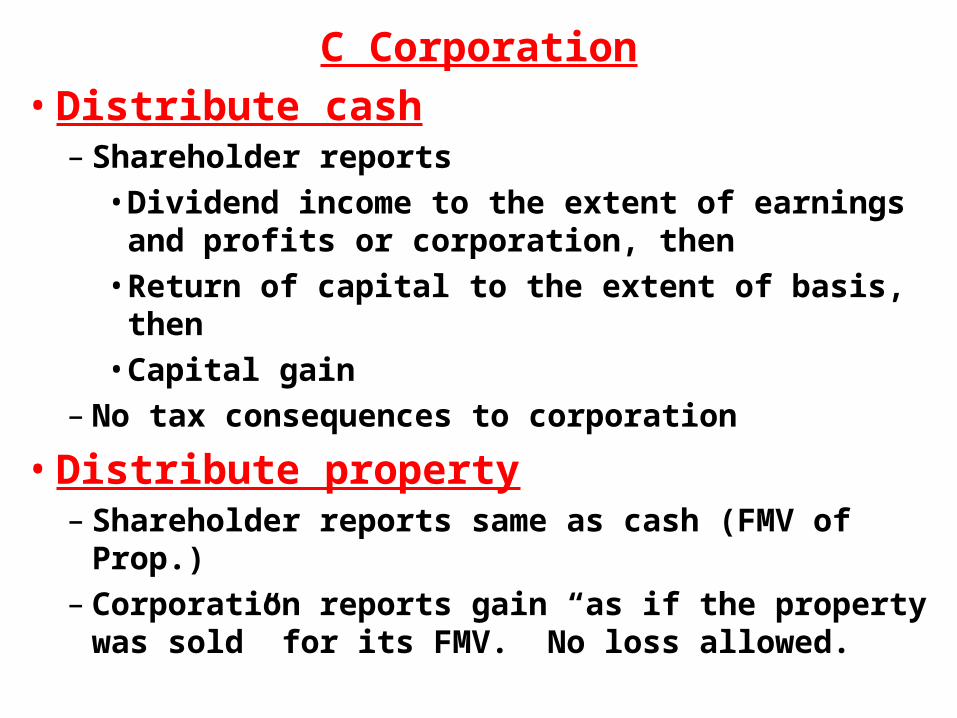

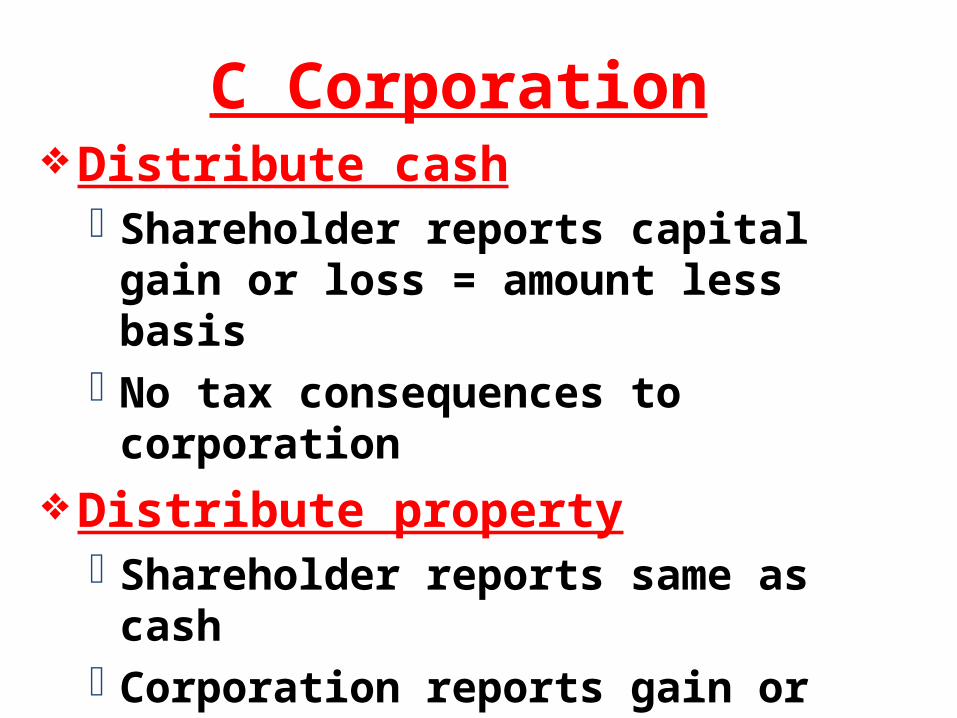

C Corporation• Distribute cash

– Shareholder reports• Dividend income to the extent of earnings and

profits or corporation, then• Return of capital to the extent of basis, then• Capital gain

– No tax consequences to corporation

• Distribute property– Shareholder reports same as cash (FMV of Prop.)– Corporation reports gain “as if the property was

sold” for its FMV. No loss allowed.

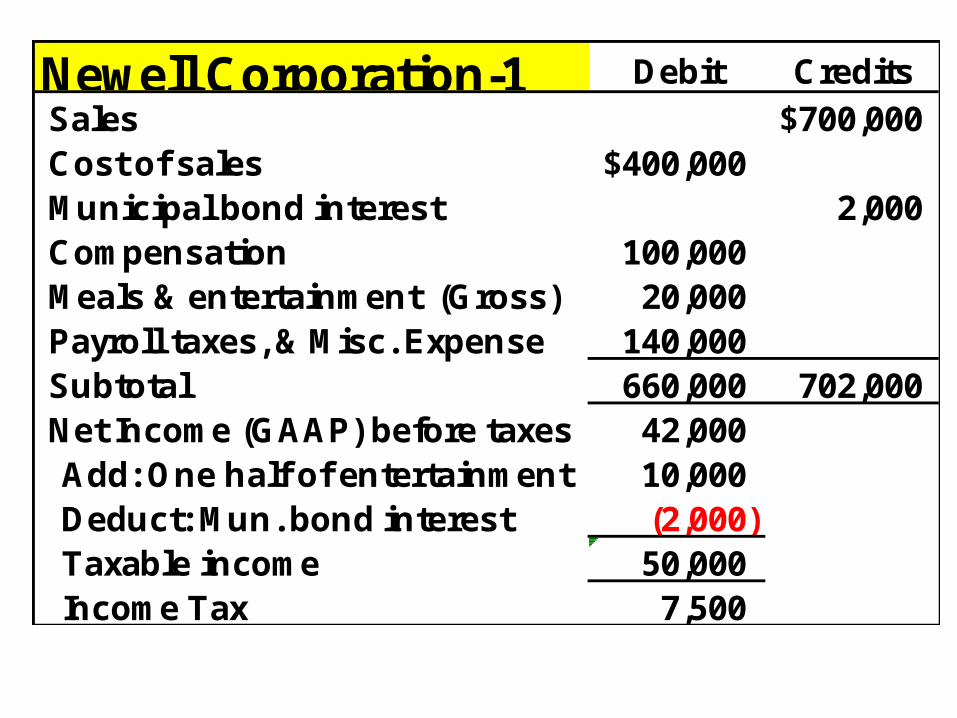

Newell Corporation-1 Debit Credits Sales $700,000 Cost of sales $400,000 Municipal bond interest 2,000 Compensation 100,000 Meals & entertainment (Gross) 20,000 Payroll taxes, & Misc. Expense 140,000 Subtotal 660,000 702,000 Net Income (GAAP) before taxes 42,000

Add: One half of entertainment 10,000 Deduct: Mun. bond interest (2,000)Taxable income 50,000 Income Tax 7,500

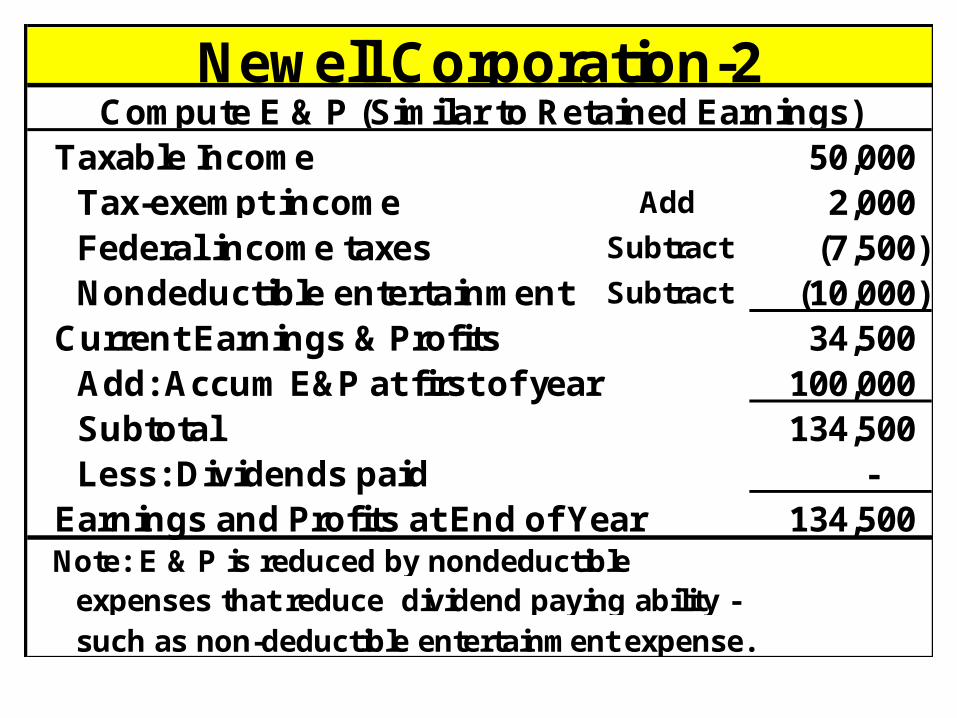

Taxable Income 50,000 Tax-exempt income Add 2,000 Federal income taxes Subtract (7,500) Nondeductible entertainment Subtract (10,000)

Current Earnings & Profits 34,500 Add: Accum E&P at first of year 100,000 Subtotal 134,500 Less: Dividends paid -

Earnings and Profits at End of Year 134,500

Newell Corporation-2Compute E & P (Similar to Retained Earnings)

Note: E & P is reduced by nondeductible expenses that reduce dividend paying ability -such as non-deductible entertainment expense.

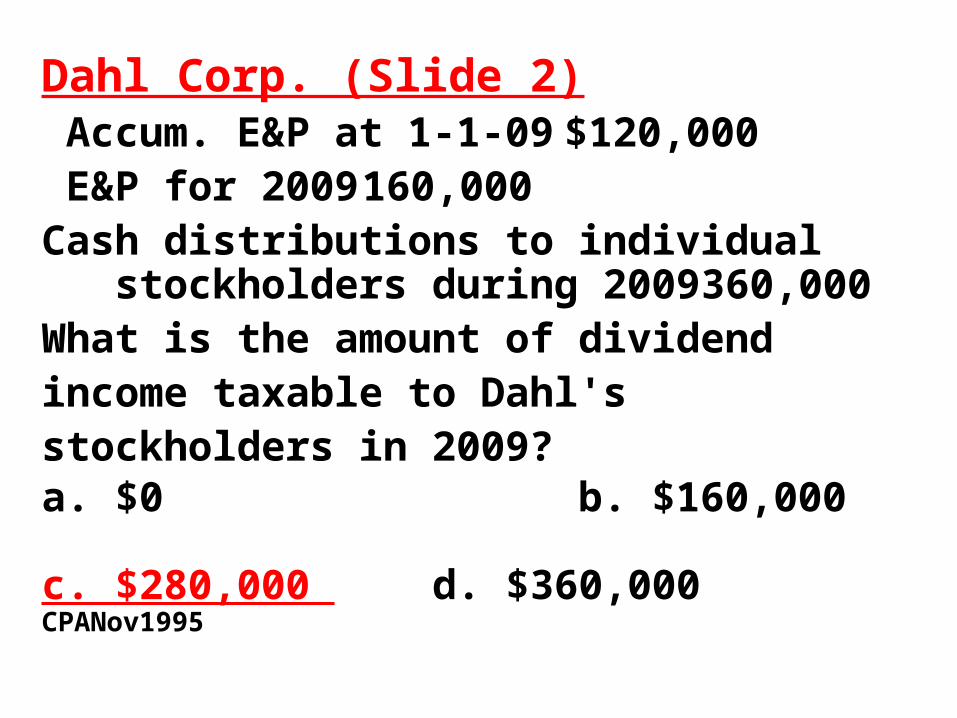

Dahl Corp. (Slide 1) Accum. E&P at 1-1-09 $120,000 E&P for 2009 160,000Cash distributions to individual stockholders during 2009 360,000What is the amount of dividend income taxable to Dahl's stockholders in 2009?a. $0 b. $160,000 c. $280,000 d. $360,000 CPANov1995

Dahl Corp. (Slide 2) Accum. E&P at 1-1-09 $120,000 E&P for 2009 160,000Cash distributions to individual stockholders during 2009 360,000What is the amount of dividend income taxable to Dahl's stockholders in 2009?a. $0 b. $160,000 c. $280,000 d. $360,000 CPANov1995

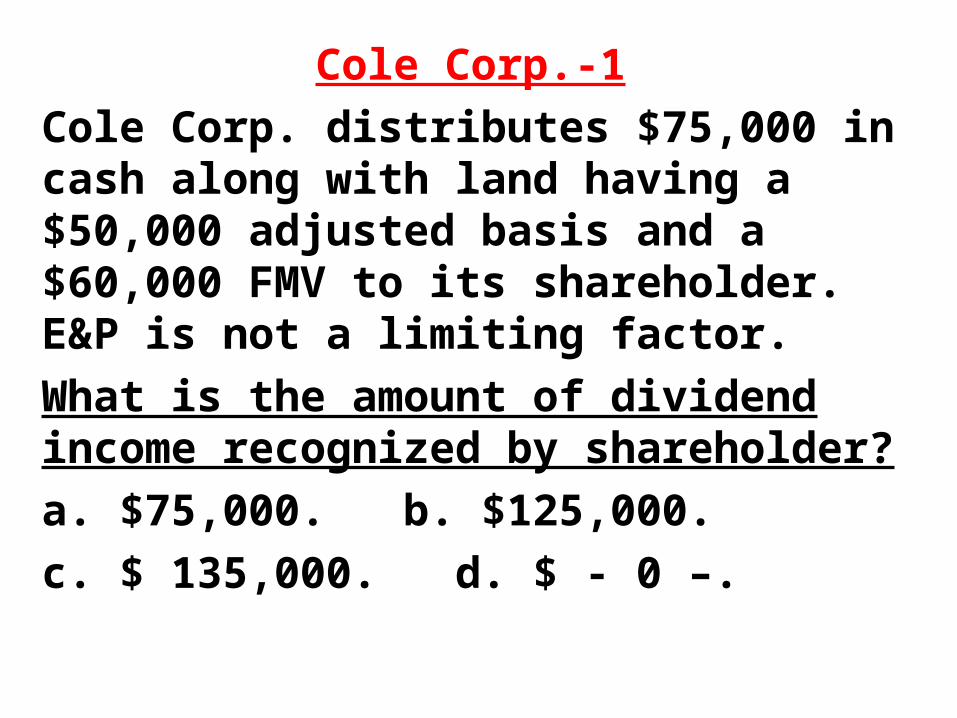

Cole Corp.-1Cole Corp. distributes $75,000 in cash along with land having a $50,000 adjusted basis and a $60,000 FMV to its shareholder. E&P is not a limiting factor.What is the amount of dividend income recognized by shareholder? a. $75,000. b. $125,000. c. $ 135,000. d. $ - 0 –.

Cole Corp.-2Cole Corp. distributes $75,000 in cash along with land having a $50,000 adjusted basis and a $60,000 FMV to its shareholder. E&P is not a limiting factor.What is the amount of dividend income recognized by shareholder? a. $75,000. b. $125,000.

c. $ 135,000. d. $ - 0 –.

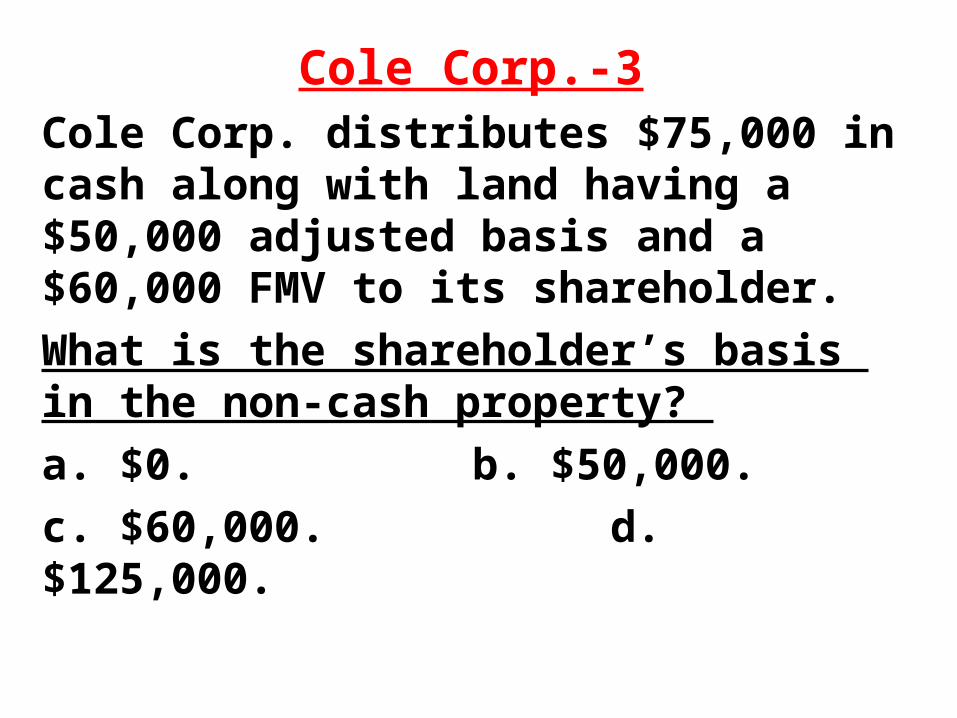

Cole Corp.-3Cole Corp. distributes $75,000 in cash along with land having a $50,000 adjusted basis and a $60,000 FMV to its shareholder. What is the shareholder’s basis in the non-cash property? a. $0. b. $50,000. c. $60,000. d. $125,000.

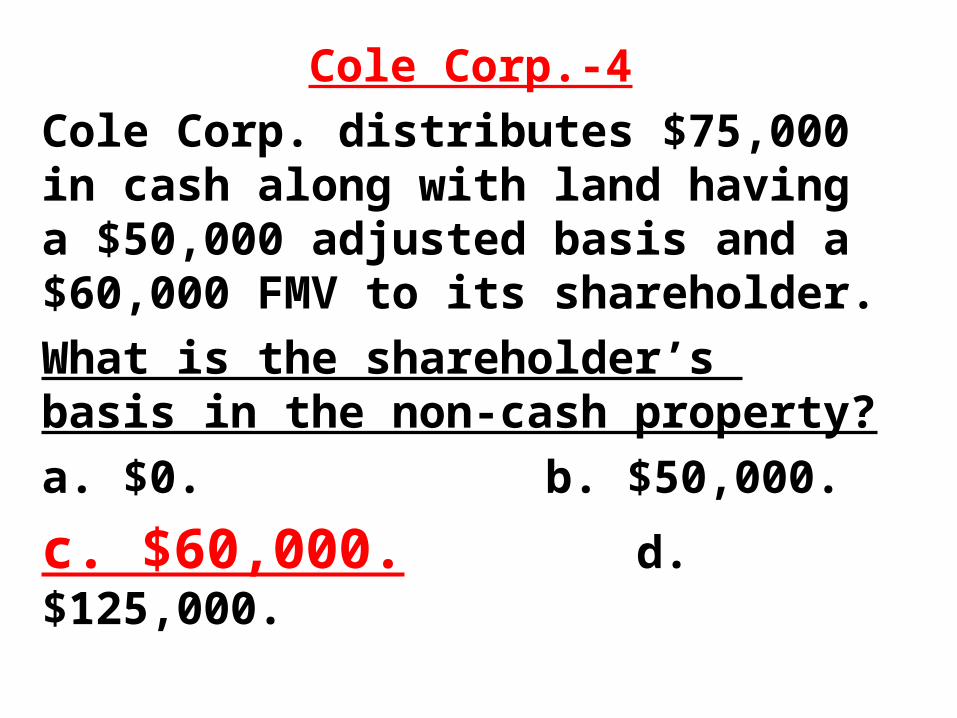

Cole Corp.-4Cole Corp. distributes $75,000 in cash along with land having a $50,000 adjusted basis and a $60,000 FMV to its shareholder. What is the shareholder’s basis in the non-cash property? a. $0. b. $50,000.

c. $60,000. d. $125,000.

Property Distributions• Property distributions – corporation

recognizes gain on distribution of appreciated property (but not loss)– Value of distribution is net FMV (net of any

liabilities assumed) and basis to shareholder is FMV

– Like cash dividends, property dividends taxable only to extent of E&P

Cole Corp.-5Cole Corp. distributes $75,000 in cash along with land having a $50,000 adjusted basis and a $60,000 FMV to its shareholder. What gain must Cole Corp. recognize? a. $10,000. b. $75,000. c. $ 25,000. d. $ - 0 –. (IRS Exam 2003)

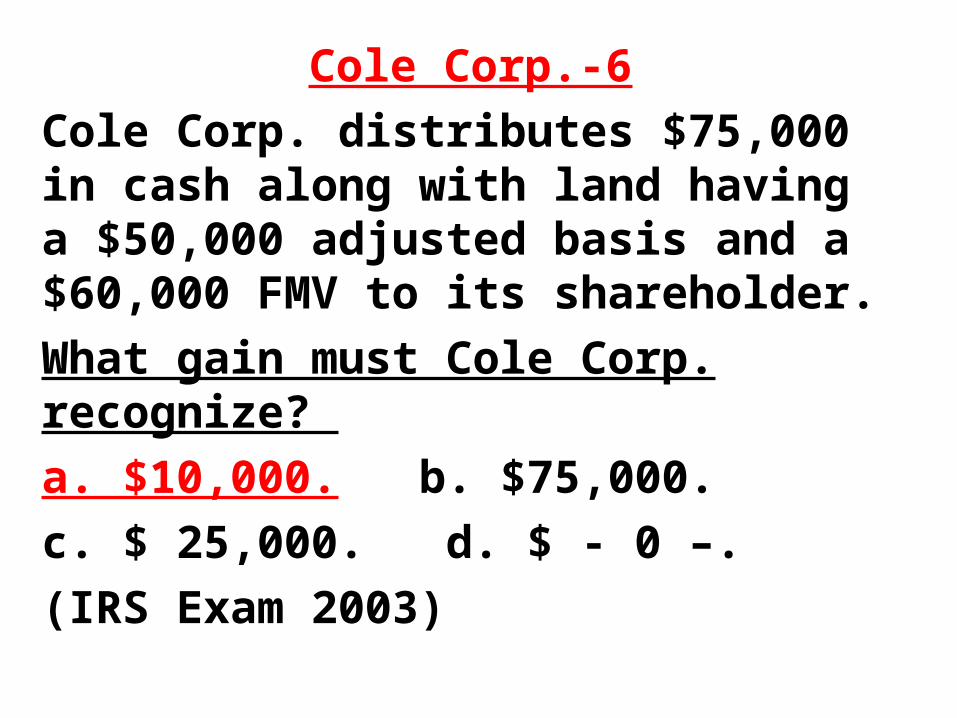

Cole Corp.-6Cole Corp. distributes $75,000 in cash along with land having a $50,000 adjusted basis and a $60,000 FMV to its shareholder. What gain must Cole Corp. recognize? a. $10,000. b. $75,000. c. $ 25,000. d. $ - 0 –. (IRS Exam 2003)

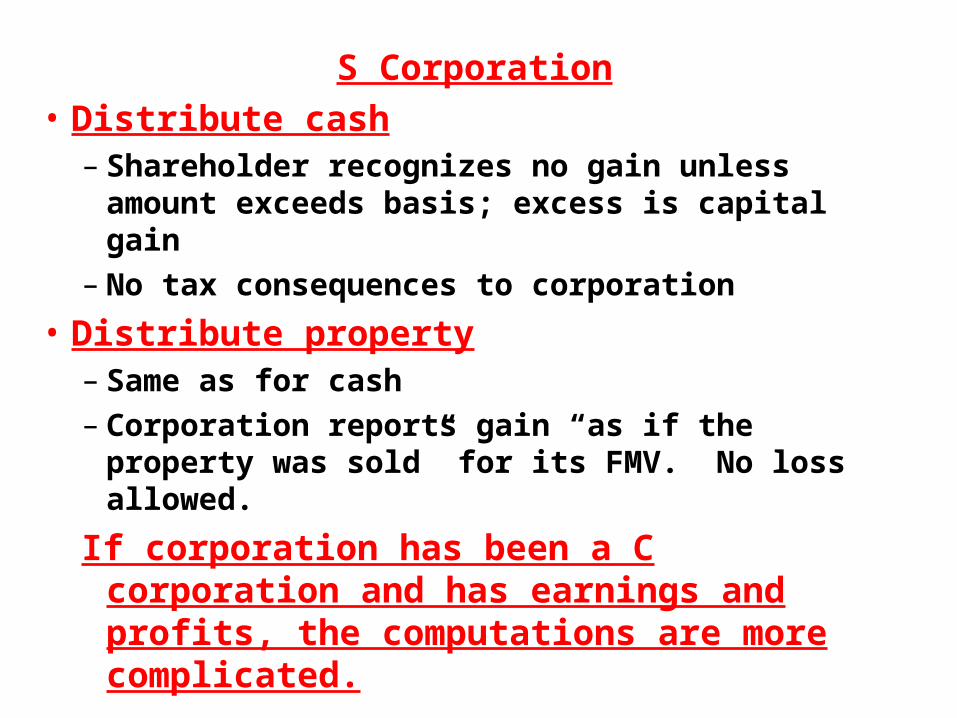

S Corporation• Distribute cash

– Shareholder recognizes no gain unless amount exceeds basis; excess is capital gain

– No tax consequences to corporation

• Distribute property– Same as for cash– Corporation reports gain “as if the property was

sold” for its FMV. No loss allowed.

If corporation has been a C corporation and has earnings and profits, the computations are more complicated.

102

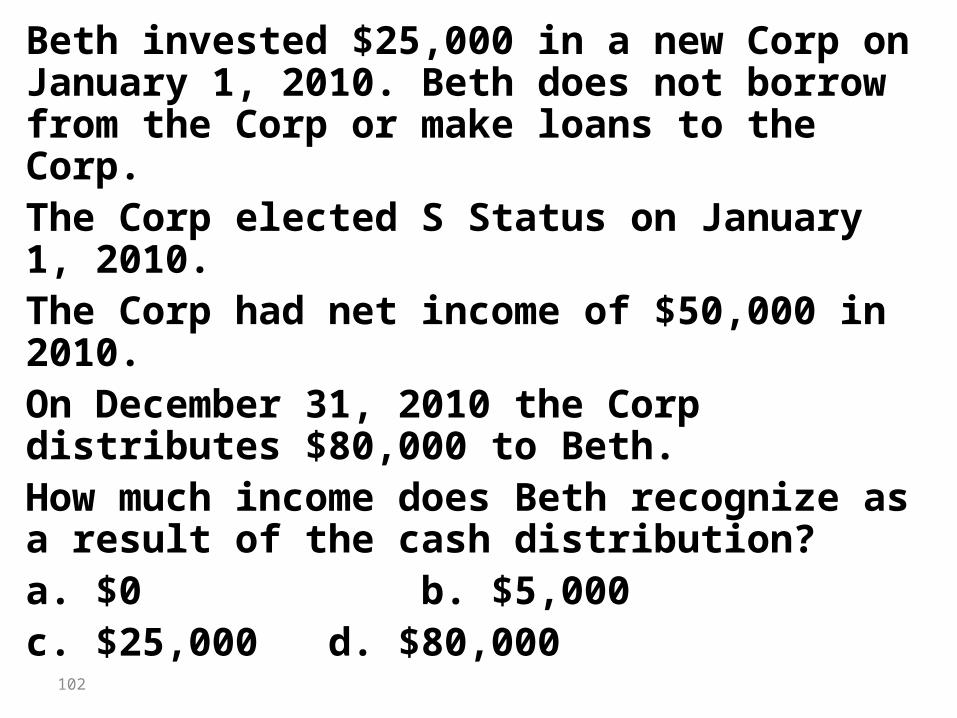

Beth invested $25,000 in a new Corp on January 1, 2010. Beth does not borrow from the Corp or make loans to the Corp. The Corp elected S Status on January 1, 2010. The Corp had net income of $50,000 in 2010. On December 31, 2010 the Corp distributes $80,000 to Beth. How much income does Beth recognize as a result of the cash distribution?a. $0 b. $5,000c. $25,000 d. $80,000

103

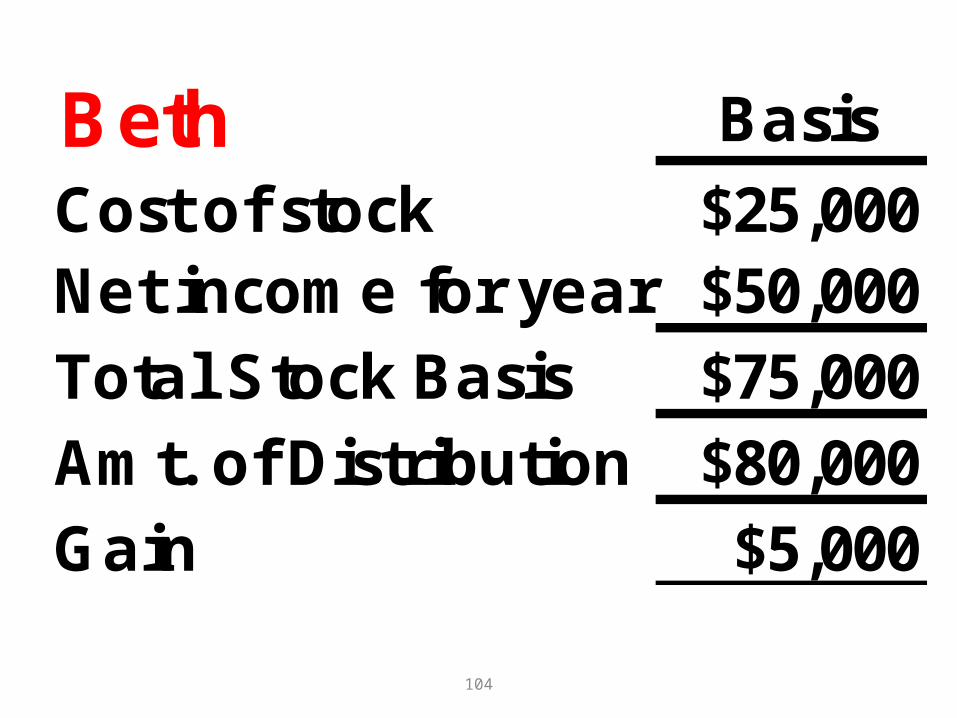

Beth Basis

Cost of stock $25,000Net income for yearTotal Stock BasisAmt. of DistributionGain

104

Beth Basis

Cost of stock $25,000Net income for year $50,000Total Stock Basis $75,000Amt. of Distribution $80,000Gain $5,000

105

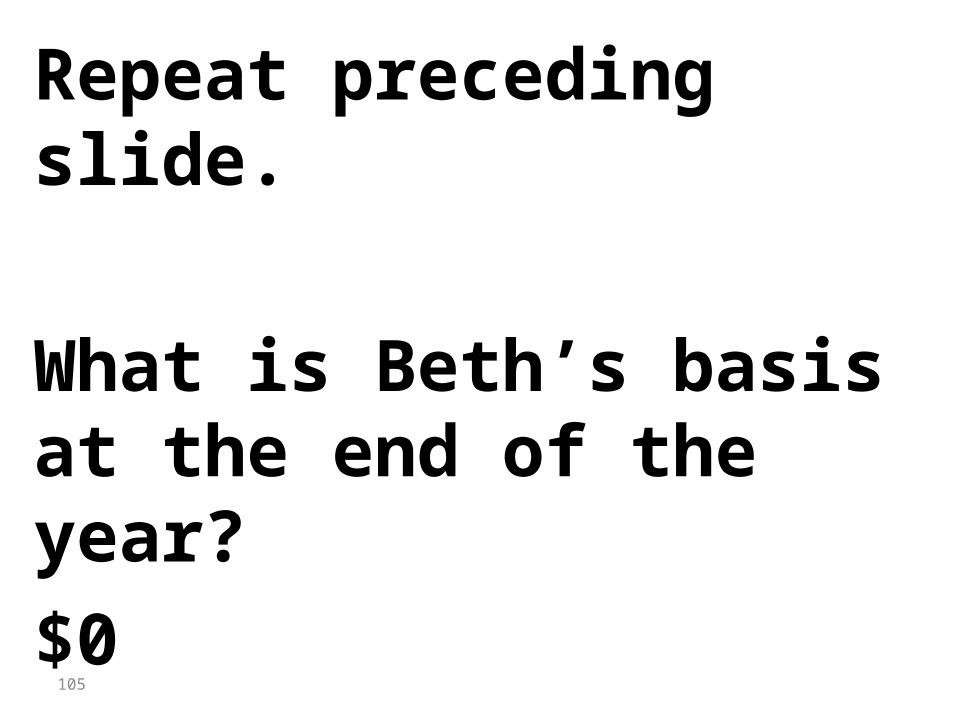

Repeat preceding slide.

What is Beth’s basis at the end of the year?$0

What are the effects of liquidating distributions made

by each entity?

Sole Proprietorship• Distribute cash

–No tax consequences to owner / entity

• Distribute property–When property is sold;

gain or loss = FMV less basis

Partnership• Distribute cash

– Partner recognizes • No gain unless amount exceeds partner’s basis;

excess is capital gain• If only cash is distributed, loss may be

recognized– No tax consequences to partnership

• Distribute property– Partner recognizes no gain or loss; Basis is the

lesser of carryover basis or partner's basis– No tax consequences to the entity

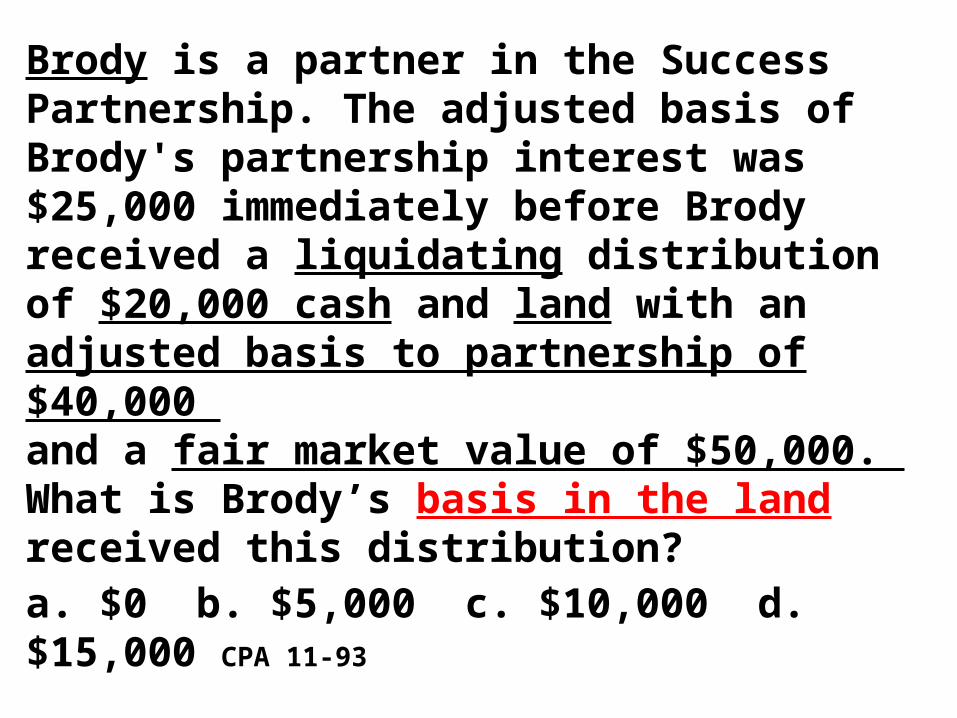

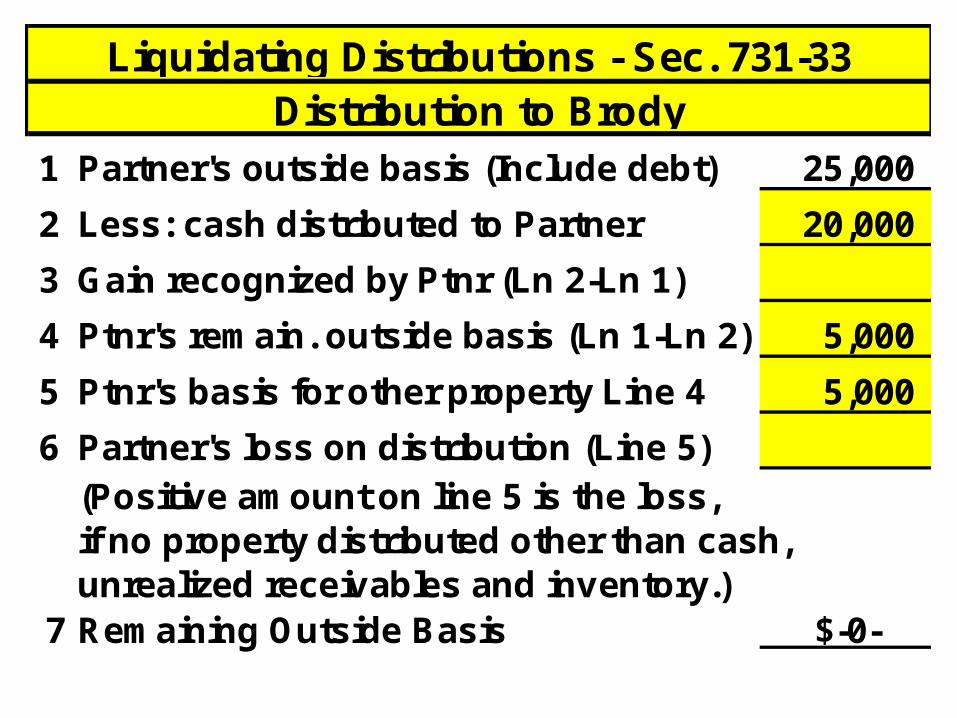

Brody is a partner in the Success Partnership. The adjusted basis of Brody's partnership interest was $25,000 immediately before Brody received a liquidating distribution of $20,000 cash and land with an adjusted basis to partnership of $40,000 and a fair market value of $50,000. What is Brody’s basis in the land received this distribution?a. $0 b. $5,000 c. $10,000 d. $15,000 CPA 11-93

1 Partner's outside basis (Include debt) 25,000

2 Less: cash distributed to Partner

3 Gain recognized by Ptnr (Ln 2-Ln 1)

4 Ptnr's remain. outside basis (Ln 1-Ln 2)

5 Ptnr's basis for other property Line 4

6 Partner's loss on distribution (Line 5)(Positive amount on line 5 is the loss, if no property distributed other than cash,unrealized receivables and inventory.)

7 Remaining Outside Basis $-0-

Liquidating Distributions - Sec. 731-33Distribution to Brody

1 Partner's outside basis (Include debt) 25,000

2 Less: cash distributed to Partner 20,000

3 Gain recognized by Ptnr (Ln 2-Ln 1)

4 Ptnr's remain. outside basis (Ln 1-Ln 2) 5,000

5 Ptnr's basis for other property Line 4 5,000

6 Partner's loss on distribution (Line 5)(Positive amount on line 5 is the loss, if no property distributed other than cash,unrealized receivables and inventory.)

7 Remaining Outside Basis $-0-

Liquidating Distributions - Sec. 731-33Distribution to Brody

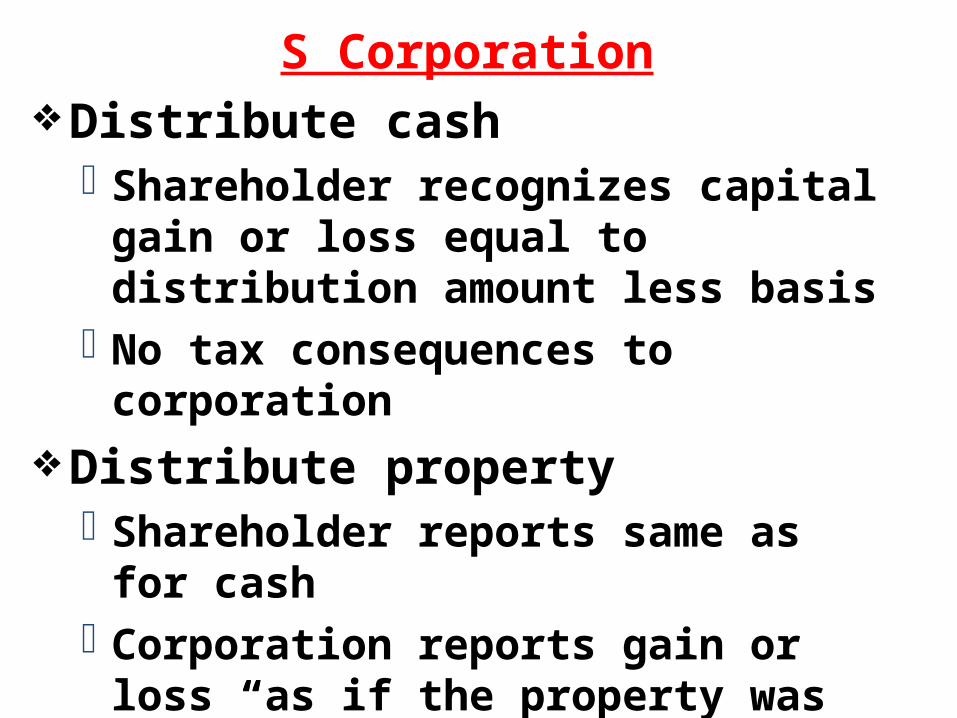

C Corporation Distribute cashShareholder reports capital gain or

loss = amount less basisNo tax consequences to corporation

Distribute propertyShareholder reports same as cashCorporation reports gain or loss “as

if the property was sold” for its FMV

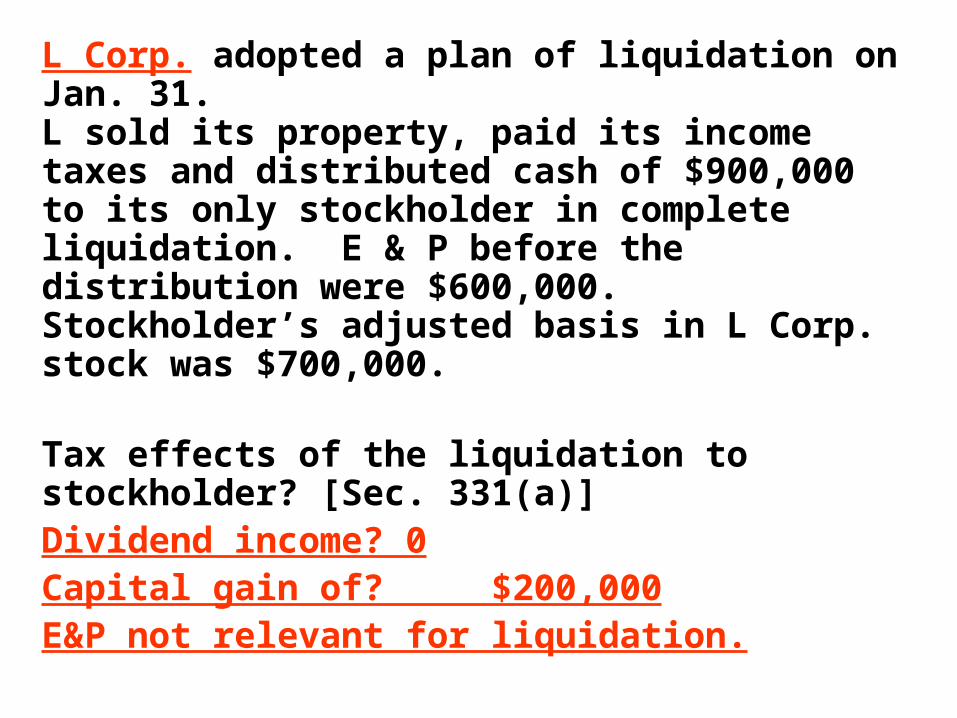

L Corp. adopted a plan of liquidation on Jan. 31. L sold its property, paid its income taxes and distributed cash of $900,000 to its only stockholder in complete liquidation. E & P before the distribution were $600,000. Stockholder’s adjusted basis in L Corp. stock was $700,000.

Tax effects of the liquidation to stockholder? [Sec. 331(a)] Dividend income? ____________Capital gain of? ____________

L Corp. adopted a plan of liquidation on Jan. 31. L sold its property, paid its income taxes and distributed cash of $900,000 to its only stockholder in complete liquidation. E & P before the distribution were $600,000. Stockholder’s adjusted basis in L Corp. stock was $700,000.

Tax effects of the liquidation to stockholder? [Sec. 331(a)] Dividend income? 0Capital gain of? $200,000E&P not relevant for liquidation.

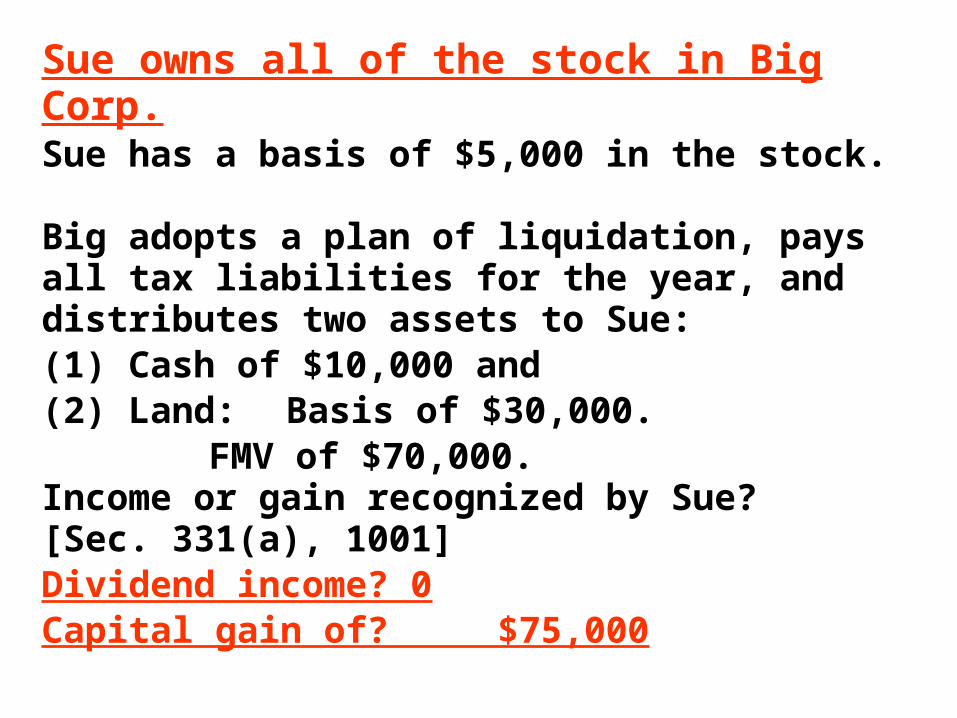

Sue owns all of the stock in Big Corp. Sue has a basis of $5,000 in the stock. Big adopts a plan of liquidation, pays all tax liabilities for the year, and distributes two assets to Sue: (1) Cash of $10,000 and (2) Land: Basis of $30,000 &

FMV of $70,000. Income or gain recognized by Sue? [Sec. 331(a), 1001] Dividend income? ____________Capital gain of? ____________

Sue owns all of the stock in Big Corp. Sue has a basis of $5,000 in the stock. Big adopts a plan of liquidation, pays all tax liabilities for the year, and distributes two assets to Sue: (1) Cash of $10,000 and (2) Land: Basis of $30,000.

FMV of $70,000. Income or gain recognized by Sue?[Sec. 331(a), 1001] Dividend income? 0Capital gain of? $75,000

S Corporation Distribute cashShareholder recognizes capital gain or

loss equal to distribution amount less basis

No tax consequences to corporation

Distribute propertyShareholder reports same as for cashCorporation reports gain or loss “as if

the property was sold” for its FMV

118

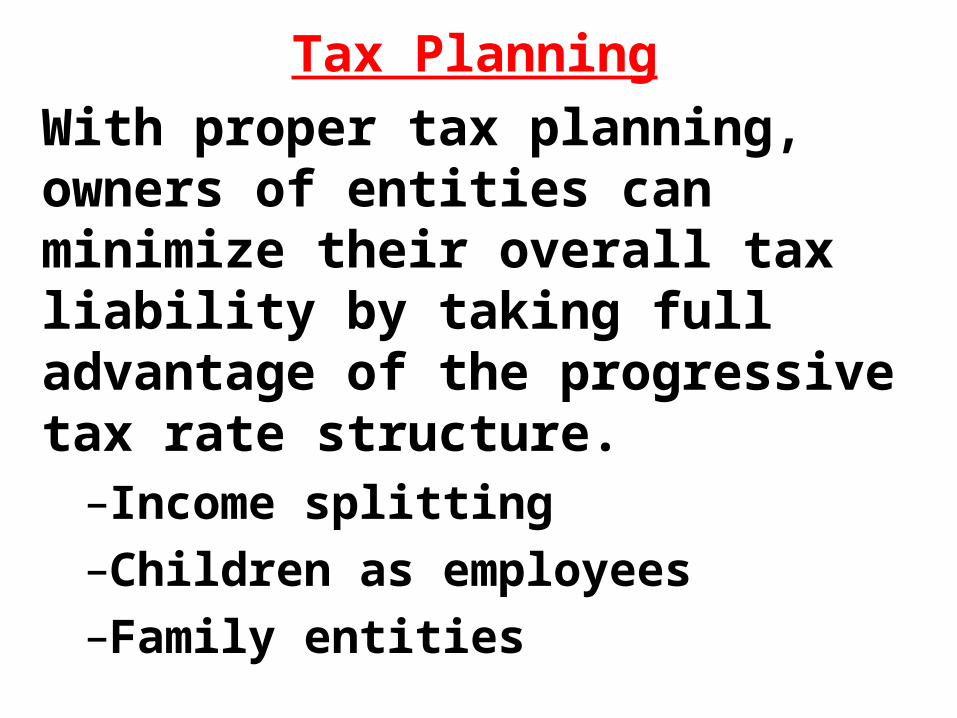

Tax Planning Income Splitting

Child-Employee

Family Entities

Tax PlanningWith proper tax planning, owners of entities can minimize their overall tax liability by taking full advantage of the progressive tax rate structure.

–Income splitting–Children as employees–Family entities

The End

Top Related