Languages

Pages

Legal

© Kantar Worldpanel

© Kantar Worldpanel

Topics of Today

1. Spending Steps Up While Consumers

Want A Deal

2. Dynamic & Diverse Channel Shopping

Trend

3. - How Do Consumers Shop

Your Category?

乘著iConsumer的翅膀

David Shang Kuan(Commercial Director of Kantar Worldpanel Taiwan)

Spending Steps Up While Consumers Want A Deal

4

Photo: Chinatimes

People steam at leisure

Photo: udn.com

Crowded shoppers

© Kantar Worldpanel

Consumption driving forces

Three trends you must deal better

www.lawtrac.com

© Kantar Worldpanel

4045

5055

606570

7580

8590

Jan-0

8

Feb-0

8

Mar-

08

Apr-

08

May-0

8

Jun-0

8

Jul-08

Aug-0

8

Sep-0

8

Oct-

08

Nov-0

8

Dec-0

8

Jan-0

9

Feb-0

9

Mar-

09

Apr-

09

May-0

9

Jun-0

9

Jul-09

Aug-0

9

Sep-0

9

Oct-

09

Nov-0

9

Dec-0

9

Jan-1

0

Feb-1

0

Mar-

10

Apr-

10

May-1

0

Jun-1

0

Jul-10

Aug-1

0

Sept-

10

Oct-

10

Nov-1

0

Dec-1

0

Jan-1

1

Feb-1

1

Mar-

11

93

93.5

94

94.5

95

95.5

96

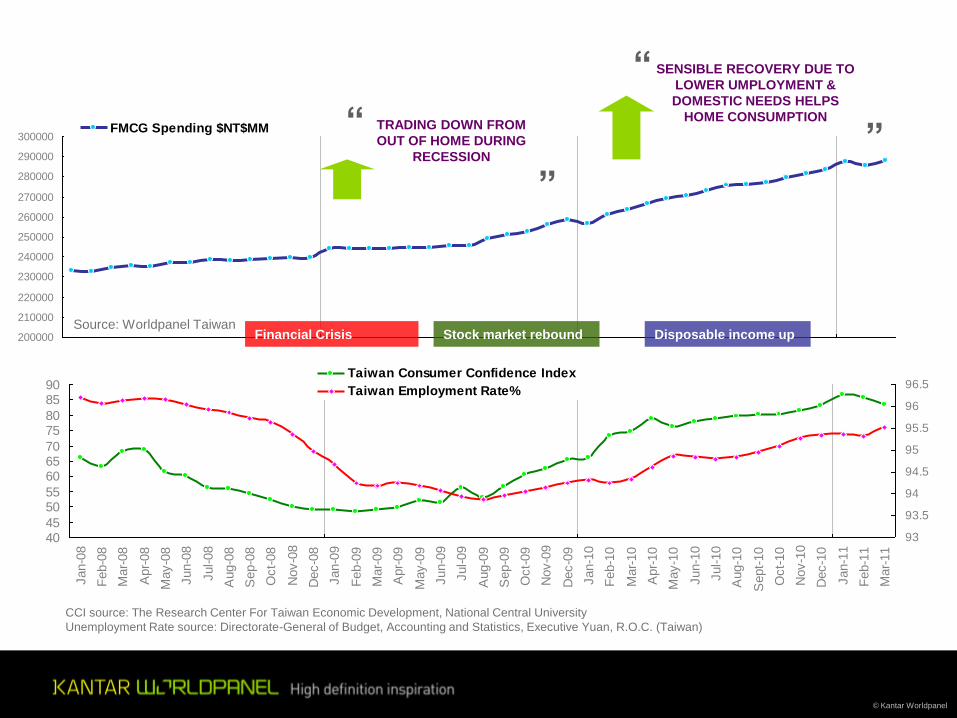

96.5Taiwan Consumer Confidence Index

Taiwan Employment Rate%

CCI source: The Research Center For Taiwan Economic Development, National Central University

Unemployment Rate source: Directorate-General of Budget, Accounting and Statistics, Executive Yuan, R.O.C. (Taiwan)

200000

210000

220000

230000

240000

250000

260000

270000

280000

290000

300000FMCG Spending $NT$MM

Source: Worldpanel Taiwan

”

TRADING DOWN FROM

OUT OF HOME DURING

RECESSION

“

SENSIBLE RECOVERY DUE TO

LOWER UMPLOYMENT &

DOMESTIC NEEDS HELPS

HOME CONSUMPTION

“

”

Financial Crisis Stock market rebound Disposable income up

© Kantar Worldpanel

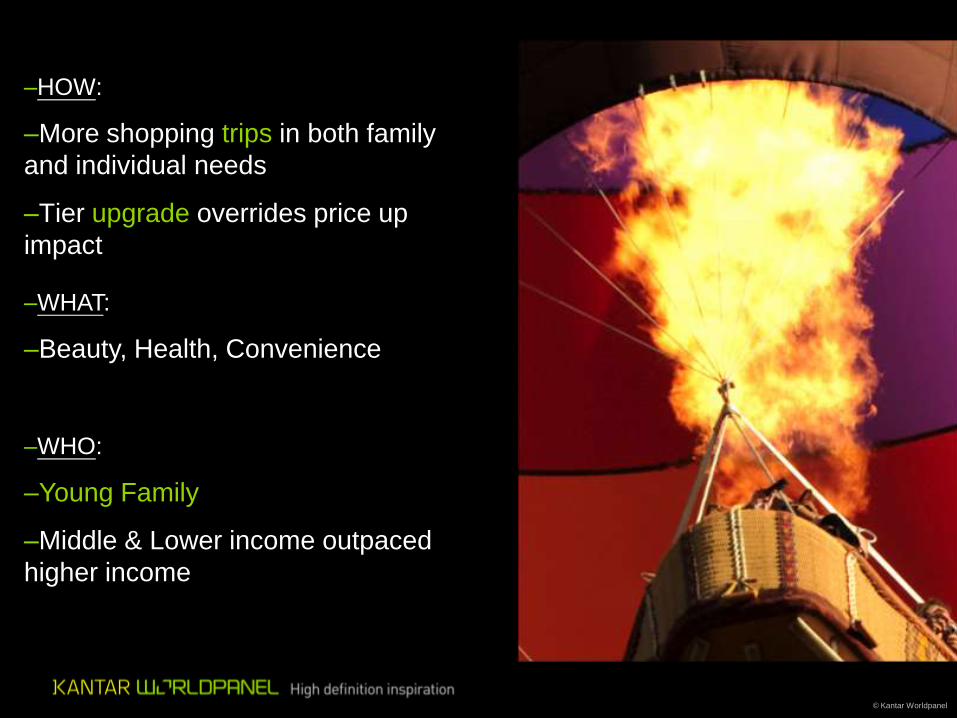

–HOW:

–More shopping trips in both family

and individual needs

–Tier upgrade overrides price up

impact

–WHAT:

–Beauty, Health, Convenience

–WHO:

–Young Family

–Middle & Lower income outpaced

higher income

© Kantar Worldpanel

98

99

100

101

102

103

104

105

106

107

52 w

/e 2

2 M

ar

09

52 w

/e 1

9 A

pr

09

52 w

/e 1

7 M

ay 0

9

52 w

/e 1

4 J

un 0

9

52 w

/e 1

2 J

ul 0

9

52 w

/e 1

6 A

ug 0

9

52 w

/e 1

3 S

ep 0

9

52 w

/e 1

1 O

ct 09

52 w

/e 0

8 N

ov 0

9

52 w

/e 0

6 D

ec 0

9

52 w

/e 0

3 J

an 1

0

52 w

/e 3

1 J

an 1

0

52 w

/e 2

8 F

eb 1

0

52 w

/e 2

8 M

ar

10

52 w

/e 2

5 A

pr

10

52 w

/e 2

3 M

ay 1

0

52 w

/e 2

0 J

un 1

0

52 w

/e 1

8 J

ul 1

0

52 w

/e 1

5 A

ug 1

0

52 w

/e 1

2 S

ep 1

0

52 w

/e 1

0 O

ct 10

52 w

/e 0

7 N

ov 1

0

52 w

/e 0

5 D

ec 1

0

52 w

/e 0

2 J

an 1

1

52 w

/e 3

0 J

an 1

1

52 w

/e 2

7 F

eb 1

1

52 w

/e 2

7 M

ar

11

Shopping

Frequency

Unit per Trip

Price per Unit

Source: Worldpanel Taiwan, FMCG by 2500 household panel

MOMENTUM INCREASED WITH

SHOPPING TRIPS, MORE IMPULSE,

MORE BROWSINGREDUCE USAGE

June’09 the lowest period

as base time index 100

A->A+ TRADE UP TO PREMIUM

IN MOST SECTORS OVERRIDES

PRICE UP IMPACT

Consumer behavior

change YOY

#93

© Kantar Worldpanel

90

100

110

120

90 95 100 105 110 115 120

Source: Worldpanel Taiwan, MAT 2011Q1 YOY

FMCG tracked by household panel, Baby products by baby panel

Sp

en

din

g p

er

Bu

ye

r G

row

th Y

OY

Purchase Occasion Growth YOY

HEALTH SUPPLEMENT

Growth fits in each age

functional benefits: Beauty

and energy boost for the

middle age; Joint-protect

for the elders.

PERSONAL CARE

High tier e.g. derma and

more sophisticated usage

on facial moisturizer e.g.

BB cream. White space for

hair conditioner / treatment

/ coloring.

FROZEN MEAL

Easy meal to

address life style of

convenience

BABY PRODUCTS

Subject to low birth rate

in spite of the increasing

indulgence

Household care

Beverage

Liquid Dairy

Dry Food

© Kantar Worldpanel

How do Consumers Spend their

Increased Expenditure?

11

1. Looking for better deal

THINKING: SMART PROMOTION

© Kantar Worldpanel

consumers resumed spending

and hiked over the previous high

7306

6923

6109

7200

7935

2006 2007 2008 2009 2010

Avg Spending NT$

Source: Worldpanel Taiwan Beauty,

Skincare Counter Brands by 3000 ladies

Promotion periods = Mothers Day (P4-P6) + Anniversary

(P10-P13)

planned until promotion period,

also a favorable time to

maximize spending…

66

70

68

72 72

2006 2007 2008 2009 2010

val% of promotion period in a year

Counter skincare

Difference between:

$1412 in normal days;

$2270 in promotion season

(packed up with stretched usage).

© Kantar Worldpanel

premium defined the trend

3435

36

42

MAT08Q1 MAT09Q1 MAT10Q1 MAT11Q1

Premium Tier Sales%

Source: Worldpanel Taiwan Beauty,

Shampoo+ Hair Conditioner by 4000 ladies

upgrade trend also being

stimulated by under-the-line

activities…

31

32

3737

MAT08Q1 MAT09Q1 MAT10Q1 MAT11Q1

% of promotion sales within

premium tier

Promotion = Consumer perceived promotion

hair care

Chicken or egg:

60% promotion perceivers are

trial buyers.

© Kantar Worldpanel

Taking advantage of promotion

occasion - not only pushing volume,

but also a chance to upgrade buyers.

THINKING:

Product portfolio to reach maximum

penetration

15

2. Expandable purchase

THINKING: PULL OR PUSH

© Kantar Worldpanel

1.02

1.03

1.04

1.05

1.06

1.07

1.08

1.09

1.1

470 480 490 500 510 520 530 540

Buying Occasions (in million)

RTD Tea,

Volume ML per trip

09Q1

09Q2

09Q3

09Q4 10Q1

10Q2

10Q3 10Q4

11 Feb.

Source: Worldpanel Taiwan Beverage, RTD Tea by 4800 individuals

Time by Moving Annual base

NOT GOING BACK TO NORMAL

More impulse drinking occasion while

accompanied with more volume consumed

During recession the impulse purchase

cut down (conservative)

© Kantar Worldpanel

Impulse!!

Occasion%

Growth%

39.5% 7.8% 8.6%

+7% -7% +44%

+ -> expandability of consumption

@CVS @CVS@CVS @PX-Mart

1.0%

-15%

Source: Worldpanel Taiwan Beverage, beverage by 4800 individuals

top 2 brands (茶裏王&御茶園) in 500-600 ML RTD tea market

© Kantar Worldpanel

Actual Case : COFFEE

If purchase size goes up by 100%, the consumption rate will go up by 68%

y = 0.6789x - 0.0036

R2 = 0.2294

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

600.00%

700.00%

800.00%

900.00%

1000.00%

-200.00% -100.00% 0.00% 100.00% 200.00% 300.00% 400.00% 500.00% 600.00% 700.00% 800.00%

Axis Title

Axi

s Ti

tle

Linear (Diff consumption)

© Kantar Worldpanel

Trip loading encouraged faster

consumption, as long as not delayed

next purchase.

THINKING: what else applied?

Health drink, Moist Mask, Snacks, Oral etc.

Engage consumers to better treat

themselves

© Kantar Worldpanel

3. New Initiatives works

THINK:

BLUE OCEAN OF SHOPPER

COMPETITION?

© Kantar Worldpanel

90

95

100

105

110

115

120

80 100 120 140 160 180

Sp

en

din

g p

er

trip

Gro

wth

YO

Y

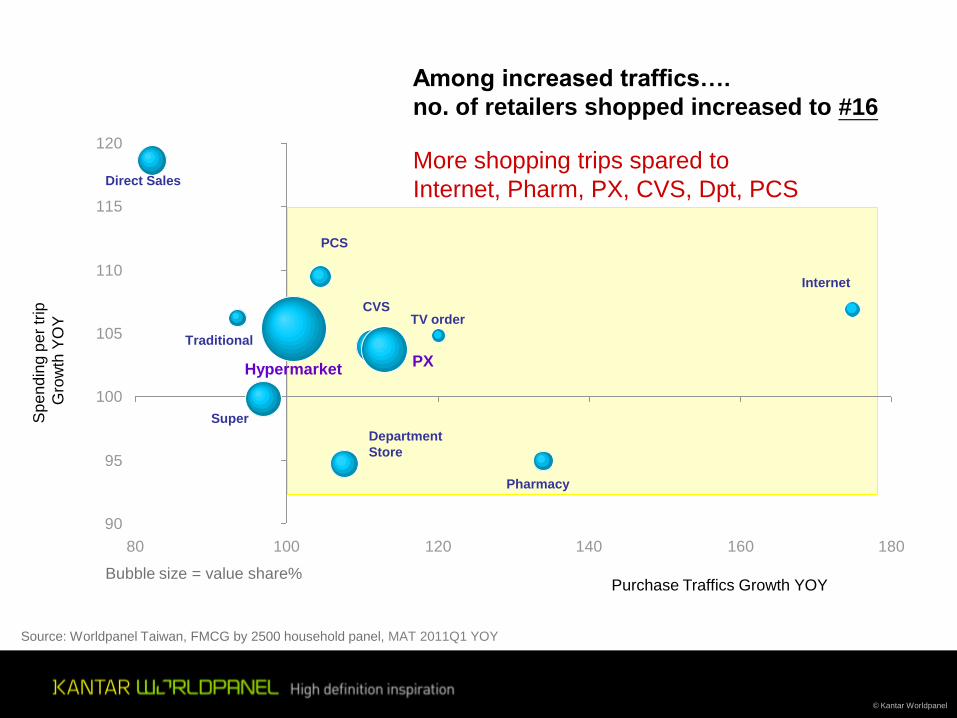

Bubble size = value share%

Source: Worldpanel Taiwan, FMCG by 2500 household panel, MAT 2011Q1 YOY

Purchase Traffics Growth YOY

Hypermarket

Super

CVS

PCS

Pharmacy

Direct Sales

Traditional

TV order

Department

Store

PX

Internet

Among increased traffics….

no. of retailers shopped increased to #16

More shopping trips spared to

Internet, Pharm, PX, CVS, Dpt, PCS

© Kantar Worldpanel

Shopping around for deal…

Liberty times7 Eleven

To support retailers out of red sea:

Category growth & bringing in

shoppers

and also for pleasure !

23

Mini pack brought females to Sparkling

Drinks, in convenience store

0

10000000

20000000

30000000

40000000

50000000

60000000

52 w

/e 2

2 F

eb 0

9

52 w

/e 2

2 M

ar

09

52 w

/e 1

9 A

pr

09

52 w

/e 1

7 M

ay 0

9

52 w

/e 1

4 J

un 0

9

52 w

/e 1

2 J

ul 0

9

52 w

/e 1

6 A

ug 0

9

52 w

/e 1

3 S

ep 0

9

52 w

/e 1

1 O

ct 09

Female

Male

Shopping occasions

Sparkling Drinks in CVS

Mini Coke

Launched

Buyer %

for Mini Coke

in CVS

67%

33%

Source: Worldpanel Taiwan Beverage, RTD Tea by 4800 individuals

24

Beauty Drink (incl. Berry, 4 herbs, Bird’s Nest etc)

Buying Occasion by Age

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

MAT 09Q1 MAT

09Q2

MAT

09Q3

2009 MAT 10Q1 MAT 10Q2 MAT 10Q3 2010 MAT 11Q1

Age 46-55

Age 36-45

Age 26-35

Age 15-25

Source: Worldpanel Taiwan Health, 3000 lady individuals

Four-herbs revamped the demand of

wellness for the younger. Bringing new buyers from chinese herb stores…

25

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

52 w

/e 2

2 M

ar

09

52 w

/e 1

7 M

ay 0

9

52 w

/e 1

2 J

ul 0

9

52 w

/e 1

3 S

ep 0

9

52 w

/e 0

8 N

ov 0

9

52 w

/e 0

3 J

an 1

0

52 w

/e 2

8 F

eb 1

0

52 w

/e 2

5 A

pr

10

52 w

/e 2

0 J

un 1

0

52 w

/e 1

5 A

ug 1

0

52 w

/e 1

0 O

ct 10

52 w

/e 0

5 D

ec 1

0

52 w

/e 3

0 J

an 1

1

52 w

/e 2

7 M

ar

11

No kids family

Family with Kids

Shopping occasions

Wet wipe

Wet Wipe extended usage for adult.

© Kantar Worldpanel

New initiatives to renovate product life

cycle, and to support retailers with

category growth (instead of EDLP)

27

Key Take-away

3. Leverage the promotion occasion to reach the

trial buyer. Loading up can encourage

consumption. Smart Promotion

1. Trading up and stretched usage is the opportunity. Justify product portfolio

2. New initiatives to drive category growth. Innovation

28

乘著iConsumer的翅膀

Yvonne Wang(General Manager of Kantar Worldpanel Taiwan)

Dynamic & Diverse Channel Shopping Trend

© Kantar Worldpanel

© Kantar Worldpanel

© Kantar Worldpanel

© Kantar Worldpanel

20

27

41

45

57

66

82

Vietnam

Philippine

Thailand

China

Korea

Malaysia

Taiwan

Bigger Share for Modern Trade

Taiwan

Malaysia

Korea

China

Thailand

Phili.

VN

© Kantar Worldpanel

91

84

82

82

82

German

French

Netherland

UK

Taiwan

Modern Trade Share Comparison

Taiwan

UK

Netherland

French

German

© Kantar Worldpanel

Top 3 distributors accounted for

more than 50% or even 70%

share in developed countries in

Europe.

27 27 20 20

1524

14 20

15

20

1115

0

30

60

90

UK Netherlands France Germany

© Kantar Worldpanel

Highly scattered and competitive

Top 3 distributors in Taiwan only

accounted for 30% share

1327 27 20 20

9

1524

14 207

15

20

1115

0

30

60

90

TW UK Netherlands France Germany

RT Mart

Carrefour

PX Mart

© Kantar Worldpanel

With more then 2.3 billion population in a small island

Highly scattered but competitive channel environment

What kind of consumers are made of?

What channels are those cannot be missed?

© Kantar Worldpanel

PX Mart

7-Eleven

Carrefour Group

Family Mart

Watsons

RT Group

Costco

Hi-Life

A. Mart

Wellcome

In average, consumers purchasing FMCG in 5 Key Accounts

Shopping channel highly

overlapped

Top10Penetration (47% val.)

© Kantar Worldpanel

How about the repertoire size within

Top 10 Hyper and Super in TW?

6 %11 %

21 %

30 %

22 %

11 %

1 store 2 stores 3 stores 4 stores 5 stores 6 stores and

above

3.3 Key Accounts in average.

© Kantar Worldpanel

ShopaholicGreat Taipei

Great Area

Age under 35

High Income

3-5 People HH

With Kids

Who purchase FMCG

in so many different

Key Accounts?

6 %

11 %

21 %

30 %

22 %

11 %

1 KA 2 KAs 3 KAs 4 KAs 5 KAs 6 KAs above

© Kantar Worldpanel

Why shop FMCG in so

many different stores?

Check up DM!see which shop has the discount on the product I need and go for it.

Something rare or special that cannot be found in other stores,such as Japanese

seasoning in Matsusei

PX-Mart is nearby and convenient, got smaller packsize with good deal

Membership points collection can exchange discounts when shopping

RT-Mart has a Comfortable Environment, nice smell of fresh bread, will take kids

for shopping

Will go get milk from 7-11 if needed in urgent for making coffee

Will shop in Costco for things that last longer because of its big packsize with cheap

price

© Kantar Worldpanel

Who shops FMCG

in only 1 store?

6.2%2.1%

1.6%

6 %11 %

21 %

30 %

22 %

11 %

1 store 2 stores 3 storess 4 stores 5 stores 6 stores

and above

“its close to home and convenient

Its cheaper and often with promotion activities

I didn’t like the small supermarket nearby, I prefer the

neat layout in PX-Mart which helps me easier to find

what I want

Carrefour is closer with almost everything I need

Loyal Group

Countryside

Age above 50

Lower household income

Young/Old single couple

1-2 members small family

© Kantar Worldpanel

Shoppers shop around

Key retailers own its unique strengths

Multiple Key Account Strategies

© Kantar Worldpanel

13 13

12 12

7

54

43

34

21 21 2

5

3

21

MAT10Q1 MAT11Q1

中友百貨

太平洋百貨

漢神百貨

雅芳

寶雅精品百貨

康是美

SOGO百貨

遠東百貨

屈臣氏

新光三越

Top 10 Key RetailersSales Value Share

12 13

9

7 7

5

4 4

3 3

2 21 1

1 1

10

4

11

MAT10Q1 MAT11Q1

寶雅精品百貨

頂好超市

全家便利

屈臣氏

愛買

統一超商

好市多

大潤發

家樂福

全聯福利中心

7

5 7

33

33

2

33

32

33

21

2

1

2

8

MAT10Q1 MAT11Q1

Pchome

宜兒樂 . 育子園

大潤發

營養銀行

全聯福利中心

佑全保健藥妝

家樂福

好市多

啄木鳥

丁丁

TTL FMCG(Home Panel)

Skincare(Lady Panel)

Infant(Baby Panel)

38.1% 39.5% 20.3%

© Kantar Worldpanel

SpaciousVariety

Unique

MembershipInnovative

DM

Discount

Quality

Value

Saving

Neighboring

Convenient

Support your Key Account Evenly

© Kantar Worldpanel

Categories with High Loyalty

Fresh Milk

Liquid Yogurt

Frozen Foods

Toilet Paper

Laundry

Penetration 38% (about 3 million

households)

4th in Value Share

6 Store (by end 2011 with 8 stores)

Higher income shoppers

American style

Selected brands

Big packsize

Great price

Profit Concern

Unique for Retailer

Premium Products

© Kantar Worldpanel

© Kantar Worldpanel

© Kantar Worldpanel

209952219651

195372191959

217753

255197

298358

316992329242

2873235131

27389

61989

137555

235897

289728 293852

267923

0

50000

100000

150000

200000

250000

300000

350000

2008 2009 2010

96

106 104 100

128

152

186

203

172

11 147

17

33

54

67 6862

0

20

40

60

80

100

120

140

160

180

200

220

2008 2009 2010

7-ELEVEN Multi-Serve Purchase

Buyer Base Spending

RTD Tea:Extra demand

Toilet Paper:Channel switching

and

Stretch usage

© Kantar Worldpanel

Increasing demand from 7-11

heavy buyer is the main

reason brought up multipack.

57% Increasing

demand

18% Channel

Switching

7-ELEVN Multi-Pack RTD Tea growth rate

76%

Why shop who box of RTD Tea

in 7-11?

“its got discount and makes it

cheaper then Hyper! ……I like

this tea anyway, don’t mind

purchase more during discount,

can put in the fridge and drink

it anytime, eventually drink

more then I used to

be……wouldn’t drink that much

without CVS discount”

“I like to drink tea, shop in CVS

could also collect points to

exchange the promotion gift.

Its close by and easy to carry

home.”

© Kantar Worldpanel

Consumers shop around、retailers each with specialty

Multi-channel strategy is essential

Set Costco as the channel to

promote premium products

WHAT ARE THE

KEY

TAKEOUT?

7-ELEVEN promote with hyper price

Business opportunity is limited with strong

categories:enlarge but not erosion the market pieManufactures need not worry, could consider join competition

Limited impact to household FMCGGrowth is evenly switching from other channel

Yet, it isn’t easy to change consumer’s channel habits

However, determination of 7-ELEVEN will decide

whether current channel habit can be break

through or not!

53

With fast developing retailers

What are the impacts towards the

market as well as the consumers?

What characters are observed within

Taiwan market?

Internet Shopping

Private Label

© Kantar Worldpanel

What is the future of Private Label

in Taiwan?

Is it a threat to Manufacture Brand?

© Kantar Worldpanel

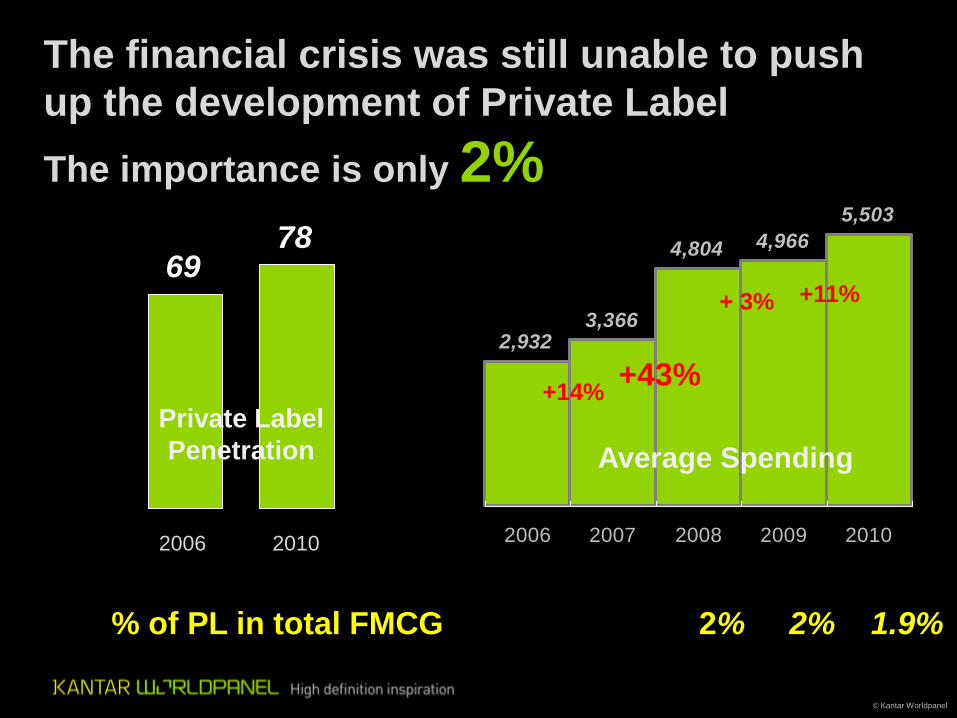

% of PL in total FMCG 2% 2% 1.9%

The financial crisis was still unable to push

up the development of Private Label

The importance is only 2%

6978

Private Label

Penetration

2006 2010

2,9323,366

4,804 4,966

5,503

2006 2007 2008 2009 2010

+11%+ 3%

+43%+14%

Average Spending

© Kantar Worldpanel

Monopoly retailers

bring up the growth

of Private Label

13 11 10

27 2720 20

9 9 8

1524

1420

7 75

15

20

11

15

52

4

11

7

10

12

4

1 3

7

6

8

7

0

30

60

90

Taiwan South Korea Malaysia UK Netherlands France Germany

Private Label Value Share

1.9% 2.6% 2.6% 46.3% 35% 32% 30.8%

© Kantar Worldpanel

0

500

1000

1500

2000

2006 2007 2008 2009 2010

Only Costco and 7-Eleven

Private Label keep growing

58

Low Price is not the only consideration.

Brand Image and Emotional Appeal of

retailers are more important!

59

Low Price is not the only consideration.

Building Trust is the smart way!

Selected Brand

© Kantar Worldpanel

WHAT ARE THE

KEY

TAKEOUTS?Packed retailers as well as average

market importance is the barrier for

private label

Maintain the balance of channel power

to avoid monopoly

However, opportunities lies in…

Brand image and client relationship

building are the keys to break through

current situation

Keep monitor future development of 7-

Select

What are the future for private

label in Taiwan?

Will it threaten market brands?

© Kantar Worldpanel

Present and Future of

Internet Shopping?

© Kantar Worldpanel

Penetration of internet

in household

48% Household Internet

shopping penetration

82% 2010

2%Value Share of total FMCG

through Internet Shopping

33%

2011Est.

3.3%

24%Household Internet shopping

for FMCG penetration

© Kantar Worldpanel

2011-05-30

65

19

25

30

10

51

Value share

Buyer Share

Source: Kantar Worldpanel Taiwan, Household panel

Heavy online

shopper

Medium online

shopper

Light online

shopper

North、East

Younger Housewife

High household income

Family with kids or teen

Avg yearly spending:NTD17,096

Yearly shopping frequency:15 times

Middle to South

Housewife age above 50

Middle to low household income

1~2 people small family

Avg yearly spending:NTD968

Yearly shopping frequency:2 times

Internet

Shopping

PioneerFollower

© Kantar Worldpanel

Convenience

Why preferred Internet Shopping?

Price

Variety

Comparable

Relatives and children

Influencer?

Internet rating/comments

Trial on premium items

Purchase potential?

Trial on new product

© Kantar Worldpanel

Frozen food

RTD drink / food

Ladies

underwear

Feminine care

Skincare

Cook related

Frozen food

Ladies underwear

Household

cleansing

Haircare products

Health food

Oral care

Everyone go for online

shopping However

Demand differently by age

Young generation

Older family

couple

Family with kids

Change of demanded

category

No time or physically

unavailable to visit stores

© Kantar Worldpanel

Internet Shopping

vs.

Physical Channel

INDEX

Average volume

per Trip123 76 185 197 146 179 275 176

Big difference in choosing brands through Internet and

physical channels

Market Top 10 brands accounted lower importance on Internet

0

10

20

30

40

50

60

70

Total

FMCG

Cooked

Food

Dried

Food

Instant

Food &

Drink

Health

Drink

HH

Cleansing

HH Paper Personal

Care

Total FMCG Market Physical Channel

Internet

Fast-g

row

ing

Cate

go

ries

on

Inte

rnet

$$ Price per Unit 251 238 149 132 192 165 78 107

© Kantar Worldpanel

Does Internet Shopping affect Physical

Channels?

6705 6666 6716 6933 6816 7304 7679 7821 7619

30462 30747 30325 3072832128 32787

33826 34436 35074

0

5000

10000

15000

20000

25000

30000

35000

40000

2008 MAT

09Q1

MAT

09Q2

MAT

09Q3

2009 MAT

10Q1

MAT

10Q2

MAT

10Q3

2010

Average spending of Internet shoppers in

Physical Channel grow together with the

market

© Kantar Worldpanel

-500000000

0

500000000

1000000000

1500000000

2000000000

2500000000

3000000000

13-S

ep-0

9

11-O

ct-

09

8-N

ov-0

9

6-D

ec-0

9

3-J

an-1

0

31-J

an-1

0

28-F

eb-1

0

28-M

ar-

10

25-A

pr-

10

23-M

ay-1

0

20-J

un-1

0

18-J

ul-10

15-A

ug-1

0

12-S

ep-1

0

12-S

ep-1

0

10-O

ct-

10

7-N

ov-1

0

5-D

ec-1

0

2-J

an-1

1

Period 2

Change -

Colu

mns

Total Switching Shoppers Held Shoppers Won/Lost

Source: Kantar Worldpanel Taiwan, Household panel

Partly switch from other channelsBut stimulate the additional demand is main

growth driver of Online Shopping

Internet shoppers increase

demands on Internet

Shopping

Switch from other channels

Physical Channel Buyers Start to shop

via Internet Shopping

© Kantar Worldpanel

WHAT SHOULD BE

eCOMMERCE

STRATEGY?

High expectation on

development of internet

shopping

Premium products with price promotion

encourages upgrade

Big packsize fulfill or expand shopping

needs

Targeting busy(working ladies)and

shoppers with issue accessing to stores

(mums with babies、elder)

Limited product online or new launch

PR marketing is the king

© Kantar Worldpanel

Scattered Retailers with high competition

Expand store numbers to maximize sales performance

Avoid monopoly to prevent growth of private label

Premium product development in COSTCO

Everyone go for online shopping, high expectation on

future development

Capture the chance of product upgrade

Online limited edition as well as new product launch

PR marketing using internet rating

Targeting shoppers ask for convenience

Learning from 7-ELEVEN

Continue monitor the effectiveness for promoting

private label brand image

Big pack size is likely to stimulate more demand

Family FMCG is likely to switch from other channel,

benefit to profit is minor. Should promote products

with good quality and higher price.

71

乘著iConsumer的翅膀

Fay Chuang (Account Director of Kantar Worldpanel Taiwan)

-How Do Consumer Shop Your Category

© Kantar Worldpanel

Life is full of Choices and Decisions

© Kantar Worldpanel

Being a ConsumerWe face many decisions everyday

© Kantar Worldpanel

Being a ConsumerYou have your own thoughts, and I have my own logics.

Channel

Brand

Price tier

Package

Vegetarian or not

Individual vs. Family

Promotion

© Kantar Worldpanel

Being a ConsumerYou have your own thoughts, and I have my own logics.

© Kantar Worldpanel

I am a consumer, also a marketer

How does the consumer Choose? (Marketing)

Sophisticated

Consumer!

How does the shopper Buy my category? (Trade)

© Kantar Worldpanel

Not only brand;

channel is also

applicable

Actual purchase-not claimed

Large sample supporting

detailed SKU level

portfolio insights

Continuous tracking-can be applied

in any category

Flexibility to Filter-

In-depth Analysis

© Kantar Worldpanel

Identify a sequence of purchases of Instant noodle

What is the common selection criteria?

Pack

Soy bean paste

Uni-President

$24

Week 1 Week 8 Week 19 Week 27 Week 38Extended family

Pack

Beef

Ve Wong

$17

Pack

Beef

Uni-President

$18

Pack

Beef

Ve Dan

$13

Pack

Bak kut teh

Uni-President

$18

Week 1 Week 8 Week 16 Week 29 Week 35

Pot

Beef

Wei Lih

$45

Cup

Kimchi

Uni-President

$35

Pot

Beef

Uni-President

$53

Pot

Beef

Ve Wong

$50

Pot

Sesame oil chicken

TTL

$58

Single lady

© Kantar Worldpanel

Product Affinity Tree

Pack

Pot/Cup

Products with a close tree

connection have a strong

inter-relationship (interchanging)

with each other.

Example

© Kantar Worldpanel

Exploration 1: Optimize Product Portfolio

What should I select for my brand portfolio to satisfy the most

decisions and shoppers?

Are there growth opportunities for NPD or range extensions?

After understanding the purchase decision order…

© Kantar Worldpanel

Exploration 1: Optimize Product PortfolioI need 6 Products to make sure I can reach enough buyers

Instant Noodle

Pack42%

Pot/Cup58%

Beef20%

Non Beef22%

Prepared Meal

26%

Non Prepared Meal

32%

Meat DryNo Meat Soup Dry Beef Non Beef Beef Non Beef10% 10% 1% 18% 4% 23% 3% 14% 18%

Example

© Kantar Worldpanel

Exploration 1: Optimize your portfolioAre there growth opportunities?

Example

Total Instant Noodle

Pack Pot/Cup

Beef

Flavor

Non-Beef

Flavor

With Prepared

Meal

No Prepared

Meal

With

Meat

Dried

Noodle

No

Meat

NoodleSoup

Dry

Noodle

Beef

Flavor

Non-Beef

Flavor

Beef

Flavor

Non-Beef

Flavor

The Manufacturer does not cover this decision

so needs a new SKU to meet this need for full

market coverage; this could either be a entirely

new range or a brand expansion

© Kantar Worldpanel

Identify your true competitors and how closely related they are to your

existing portfolio?

When do shoppers leave without buying and when do they

switch to a rival?

Exploration 2: Gain Competitive Advantage

After understanding the purchase decision order…

© Kantar Worldpanel

InstantNoodle

Pack 碗/杯裝

Beef Non BeefPrepared

MealWO Prepared

Meal

With Meat

Dried Noodle

WithoutMeat

Noodle Soup

Dried Noodle

Beef Non Beef Beef Non Beef

Exploration 2: Gain Competitive Advantage

Who is my true competitor?

Example

© Kantar Worldpanel

InstantNoodle

Pack Pot/Cup

Beef Non BeefPrepared

MealWO Prepared

Meal

With Meat

Dried Noodle

WithoutMeat

Noodle Soup

Dried Noodle

Beef Non Beef Beef Non Beef

112 105 98

Exploration 2: Gain Competitive AdvantageIdentify key differentiator within the same competitive set

Price is the next key decision.

And in this case is the most effective method

to raise share in the competitive set. Example

© Kantar Worldpanel

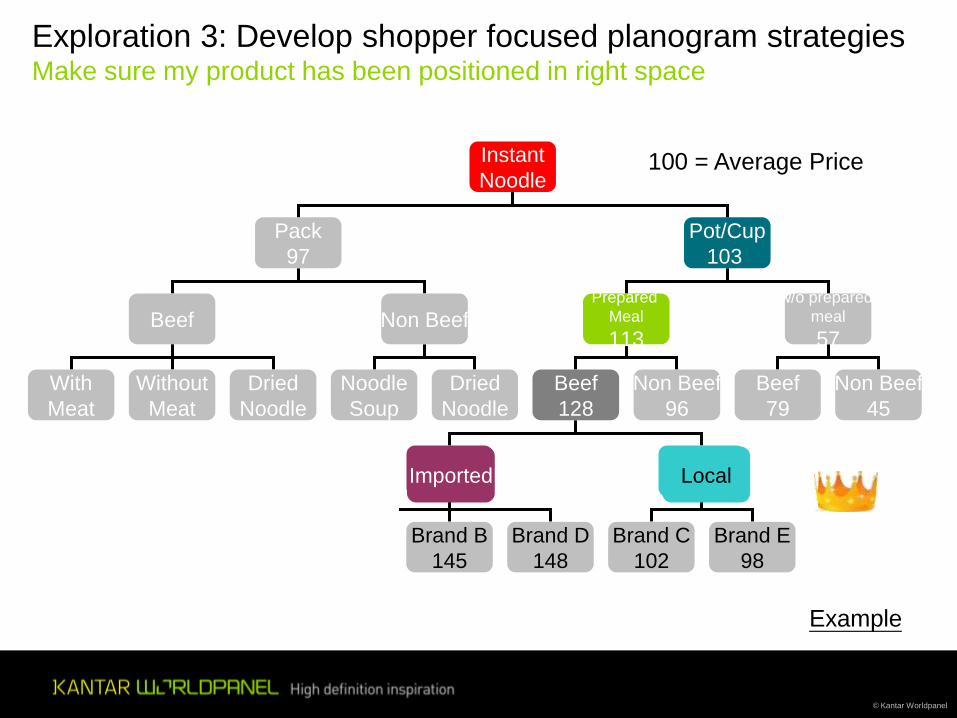

Exploration 3: Develop shopper focused planogram strategies

Can shoppers clearly see my products?

What product attributes and features should we highlight on shelf?

How to collaborate with my retailers to plan the most optimal strategy?

Where should my category display?

After understanding the purchase decision order…

© Kantar Worldpanel

Multi packs

(Family Size)

Individual

pack

Pot/ Cup

(Individual)

1st: Package

Exploration 3: Develop shopper focused planogram strategiesIs it easy for the shopper to find what they are looking for?

Can the shelf be organised in line with purchase behaviours?

Pot/ Cup

(Multi serve )

2nd: Flavor 2nd: With prepared meal or not

Beef Pork

Chicken Vegetable

With prepared meal

Non-prepared meal

Example

Beef Pork

Chicken Vegetable

Helping Shoppers find your brand/ products

With prepared meal

Non-prepared meal

© Kantar Worldpanel

Instant

Noodle

Pack

97

Pot/Cup

103

Beef Non BeefPrepared

Meal

113

w/o prepared

meal

57

With

Meat

Dried

Noodle

Without

Meat

Noodle

Soup

Dried

Noodle

Beef

128

Non Beef

96

Beef

79

Non Beef

45

Premium

146

Value

100

Brand A

150

Brand D

148

Brand C

102

Brand B

145

Brand E

98

Brand A

150

100 = Average Price

Exploration 3: Develop shopper focused planogram strategiesMake sure my product has been positioned in right space

LocalImported

Example

© Kantar Worldpanel

Exploration 3: Develop shopper focused planogram strategiesDifferences of decision order can be seen in various channels

Hyper

Packaging

CVS

Individual Serve

Super

Packaging

Super

Imported Area

PX

Shelf Design

© Kantar Worldpanel

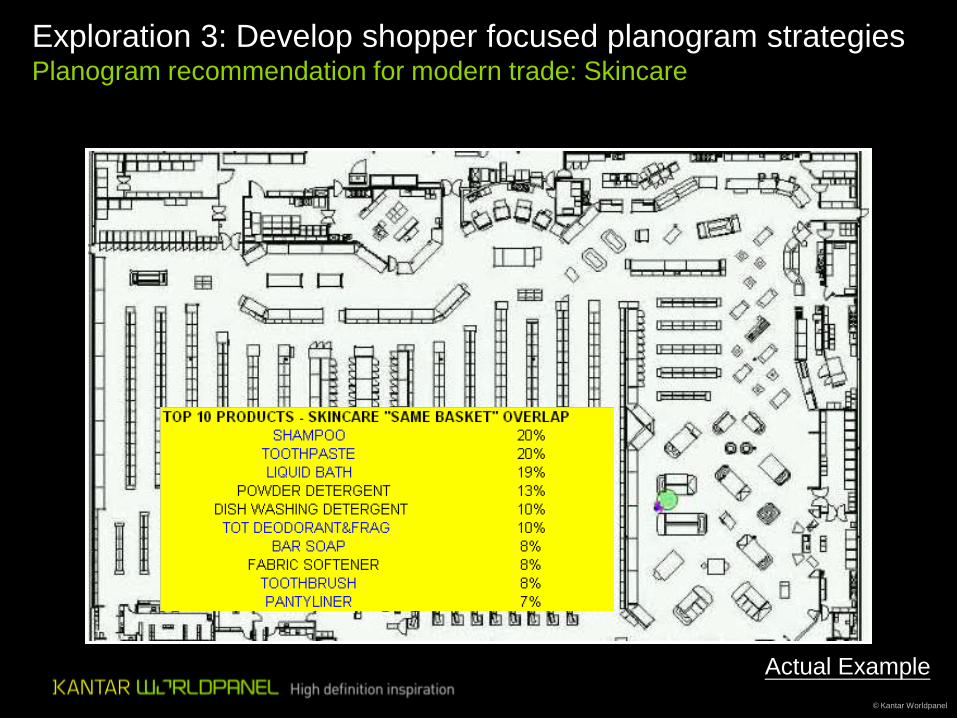

Exploration 3: Develop shopper focused planogram strategiesPlanogram recommendation for modern trade: Skincare

Actual Example

© Kantar Worldpanel

– Between Shampoo and Toothpaste would have the most beneficial

impact for skincare. They offer optimum basket overlap, high penetration

and high frequency. They would aid the potential frequency of buying

Skincare.

Exploration 3: Develop shopper focused planogram strategiesWhere should skin care be located in store?

Skin CareShampoo &

Liquid BathOral Care

Actual Example

© Kantar Worldpanel

Exploration for Purchase Decision

Develop shopper

focused planogram

strategies

Optimize Product

Portfolio

Gain Competitive

Advantage

© Kantar Worldpanel

Successful Experiences

© Kantar Worldpanel

Successful Experiences - Category Reviewed

© Kantar Worldpanel

Your Next Step?

Navigator of Consumer Insight

Let’s Shine together!

97

乘著iConsumer的翅膀

Recap

Yvonne Wang(General Manager of Kantar Worldpanel Taiwan)

© Kantar Worldpanel

Yahoo!奇摩購物中心PChome線上購物momo富邦購物網

ETMall東森購物PayEasy線上購物-康迅數位整合

樂天市場網路購物露天拍賣

快樂購-Go Happy

歡樂點網站-HiNet

ViVaTV

國泰購物-Treemall

郵政商城(網路開店服務)

7net統一超商-7-ELEVEn

萊爾富購物網淘寶網

新光三越線上購物-shopping.skm

中友YO購站-中友百貨網購站誠品網路書店-eslite

森森百貨購物網-( u-mall / u-life )

長榮樂e購FUJIDINOS-日本生活購物網

哇!拍賣-WOW-(需先購競標點數)

廣華電子商城(電子零件)-敦華電子iCshop-(電子零件)

蕃薯藤購物中心-yam

維他廣場-VitaSquare

今華電子(電子零件)

名佳美美華泰

博客來網路書店-books.com.tw

民視購物網燦坤實業

Yahoo!奇摩拍賣台塑購物網

順發3C數位服務大買家量販網路店

Yahoo!奇摩超級商城

© Kantar Worldpanel

Work closely with you to deliver impact to your business

成為您的夥伴,協助您業務成長

Name and surname

Date

© Kantar Worldpanel

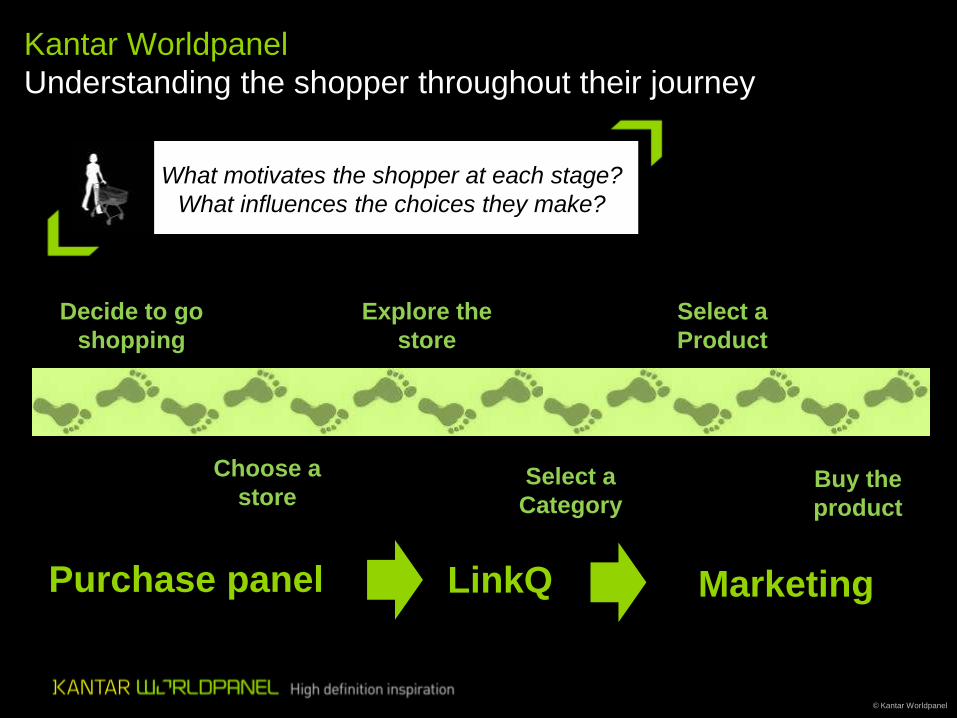

Kantar Worldpanel

Understanding the shopper throughout their journey

Choose a

store

Explore the

store

Select a

Category

Select a

Product

Decide to go

shopping

Buy the

product

What motivates the shopper at each stage?

What influences the choices they make?

LinkQPurchase panel Marketing

© Kantar Worldpanel

OUR COMMITMENT 我們的承諾

102

High Definition

Inspiration

高清晰啟發

Consumer Insight

Center Of

Excellent

卓越中心Expert Service

Online

Deliverables

網路版報告

WPO.com

Online Behavior

Monitoring

網路行為Online Communication

Targeting & Evaluation

© Kantar Worldpanel

ACCESS TO CONSUMER INSIGHTS

Worldpanelonline.com now live

© Kantar Worldpanel

Investigating unique

behavior

Purchase motivations

Building segmentations

Price Targeter

Decision Tree

© Kantar Worldpanel

105

To Inspire You With Our POV!

提出我們的觀點 啟發您!

106

Top Related