Languages

Pages

Legal

© 2020, HFS Research Ltd Page 1

HFS Vision 2025: the New Dawn to Become a OneOffice Organization

© 2020, HFS Research Ltd Page 3

Only 37% will return to the office based work-style

21%

16%

29%

22%

11%

We’re planning to return to office-based structures once the

situation is over

We will relax working from homerules, but will still be largely office

based

We’re committed to remote working now, and will evolve our

operations to support a hybrid workforce model in the future

We’re monitoring productivity and well-being at the moment and will

consider retaining a primarily remote structure if the results are

positive

Others

As an organization, which of the following best describes your approach to post-covid working arrangements?% respondents

37% prefer return to office-

based environment

51% considering

remote/hybrid workforce

Sample: 400 executives across global 2000 enterprisesSource: HFS Research, 2020

© 2020, HFS Research Ltd Page 4

Different industries have felt the impact differently

Banking and Financial services

Consumer products and Retail

Energy and utilities

Healthcare

High-tech and Telecom

Industrial manufacturing and logistics

Insurance

Life Sciences

Travel and hospitality

Revenues

How is your organization doing today as compared to before COVID-19?Weighted average by industry

Significantly worse

Worse Similar Better Significantly better

Better

Significantly better

Similar

Worse

Pro

fits

/ M

argi

ns

+ve valuation -ve valuation

Size the bubble represents perceived impact on valuation

Sample: 150 C-level executives across the global 2000 enterprisesSource: HFS Research, 2020

© 2020, HFS Research Ltd Page 5

© 2020, HFS Research Ltd Page 6

The outlook for IT and business process services in healthcare post the pandemic shock remains “bullish” as enterprises want to “do more with less”

Increasing business process outsourcing in the next 12 months % respondents

Already done, 25%

Planning in the near

term, 32%

Considering options,

28%

No plans, 15%

Increasing IT outsourcing in the next 12 months % respondents

Already done, 28%

Planning in the near

term, 35%

Considering options,

25%

No plans, 13%

Sample: 400 executives across global 2000 enterprisesSource: HFS Research, 2020

© 2020, HFS Research Ltd Page 7

•

•

•

© 2020, HFS Research

OffshoringGlobalization

Shared Services /Nearshoring

Centralization

The Internet

Client/ Server

ERP

Six Sigma

LEAN

Basel II

Private Cloud

Open Source

Digital Business Models

IOT

Public Cloud

eBusiness

Digital Marketplaces

ASPs

Sox

Y2K

Euro Currency Conversion

VOIP

3G

RPA

Enterprise IT dressed up as

Digital

Intelligent Automation

Machine Learning

AI

Blockchain

5G

The Guerrilla Sharing

Economy

Digital Workers

OutsourcingAnalog

Basic DigitalResponsive

GBSAnticipatory

2020+Autonomous,

Hyperconnected Supply Chains

Data-driven Virtual

organizations

Final phase of widespread

Cloudification

Digital OneOffice

Interactive

Evolution to the Connected OneOffice MindsetReal change drives

rapid pivot to OneOffice

© 2020, HFS Research Ltd Page 9

© 2020, HFS Research Ltd Page 10

Creating the “OneOffice” experience for clients

Accenture is able bring its innovation capabilities together

across Accenture’s series of organizational units

TCS brings together business process services and IT

infrastructure services under single business unit – Cognitive

Business Operations (CBO)

“TCS’ Cognitive Business Operations (CBO) caters to various CXO

stakeholder’s transformational needs by taking responsibility of the

entire slices of enterprise operations, including process delivery,

application services, and the underlying IT infrastructure, and delivers

superior business outcomes and experience to all stakeholders through

holistic Machine-First™ transformation leveraging Cloud, Analytics, IoT,

Machine Learning, AI, and RPA throughout the operational stack.”

© 2020, HFS Research Ltd Page 11

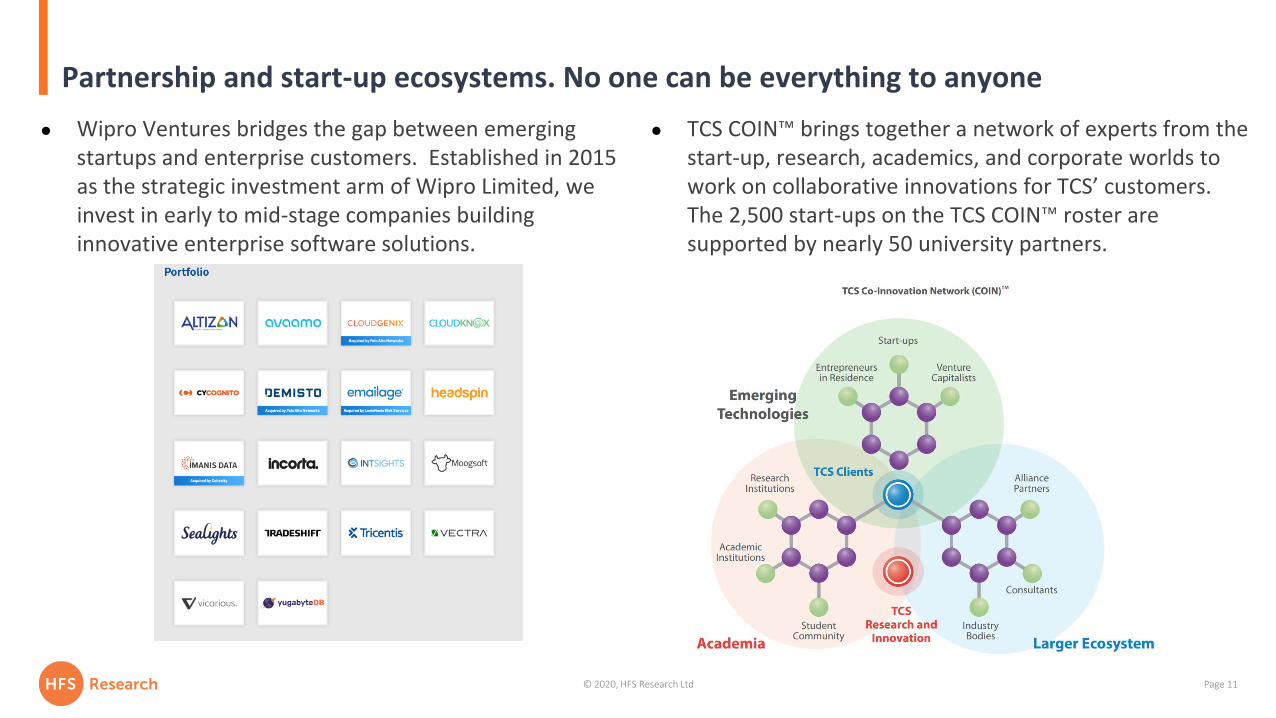

Partnership and start-up ecosystems. No one can be everything to anyone

● Wipro Ventures bridges the gap between emerging startups and enterprise customers. Established in 2015 as the strategic investment arm of Wipro Limited, we invest in early to mid-stage companies building innovative enterprise software solutions.

● TCS COIN™ brings together a network of experts from the start-up, research, academics, and corporate worlds to work on collaborative innovations for TCS’ customers. The 2,500 start-ups on the TCS COIN™ roster are supported by nearly 50 university partners.

© 2020, HFS Research Ltd Page 12

360 degrees engagement model. Become partners with skin-in-the-game

● Vanguard-Infosys. Partnership will advance digital transformation of Vanguard’s defined contribution recordkeeping business. While role transitions are typical, Vanguard is putting real skin in the game with notable senior execs going to Infosys.

● Volt Partners with TCS to Expand Payment Offerings. Set to launch in 2021, Volt 2.0 will leverage TCS BaNCS™, a global payments solution, to expand the bank's offerings to include NPP, BPAY and DE, enabling full-service banking capabilities for all its customers.

● Wipro-Alight partnership enables Alight to accelerate investment in consumer-facing technologies and services across its health, wealth and cloud businesses by leveraging Wipro’s industry-leading strengths in automation, machine learning and data analytics. Additionally, Wipro will acquire and take on responsibility for the services delivered from Alight’s India locations. Alight has developed a rich set of technology and delivery capabilities across its India centers located in Gurgaon, Noida, Mumbai and Chennai.

● HCL and Xerox expand strategic partnership building on a decade-long Product Engineering relationship, this Managed Services arrangement positions HCL to transform Xerox’s shared services globally, resulting in greater operational efficiency, automation and enhanced service levels

© 2020, HFS Research Ltd Page 13

The ability to understand and solve business problems are the key attributes that clients seek from third-party services

What are the attributes of a business/technology service provider that gives you confidence to deliver the value you seek?

Rank

Demonstrating the “awareness of the problem” #1

Leveraging creativity, knowledge and experience to solve problems #2

Ability to keep an eye on the future, e.g., emerging technologies #3

Agility and flexibility to react to business changes #4

Continuous modernization, i.e., continuously improve solutions #5

Proven ability to deliver flawlessly #6

Co-innovating with the client #7

Ability to challenge constructively and offer a clear point of view #8

Sample: 150 C-level executives across the global 2000 enterprisesSource: HFS Research, 2020

© 2020, HFS Research Ltd Page 14

IT Modernization on Steroids: the IT guts of going all-cloud-all-digital with actual urgency

© 2020, HFS Research Ltd Page 16

Whatever the moniker for transformation, it is a journey

© 2020, HFS Research Ltd Page 17

Whatever the moniker for transformation, it is a journey

© 2020, HFS Research Ltd Page 18

Operationalizing the journey toward the OneOffice

© 2020, HFS Research Ltd Page 19

HFS IT Services Research Agenda 2021

© 2020, HFS Research Ltd Page 20

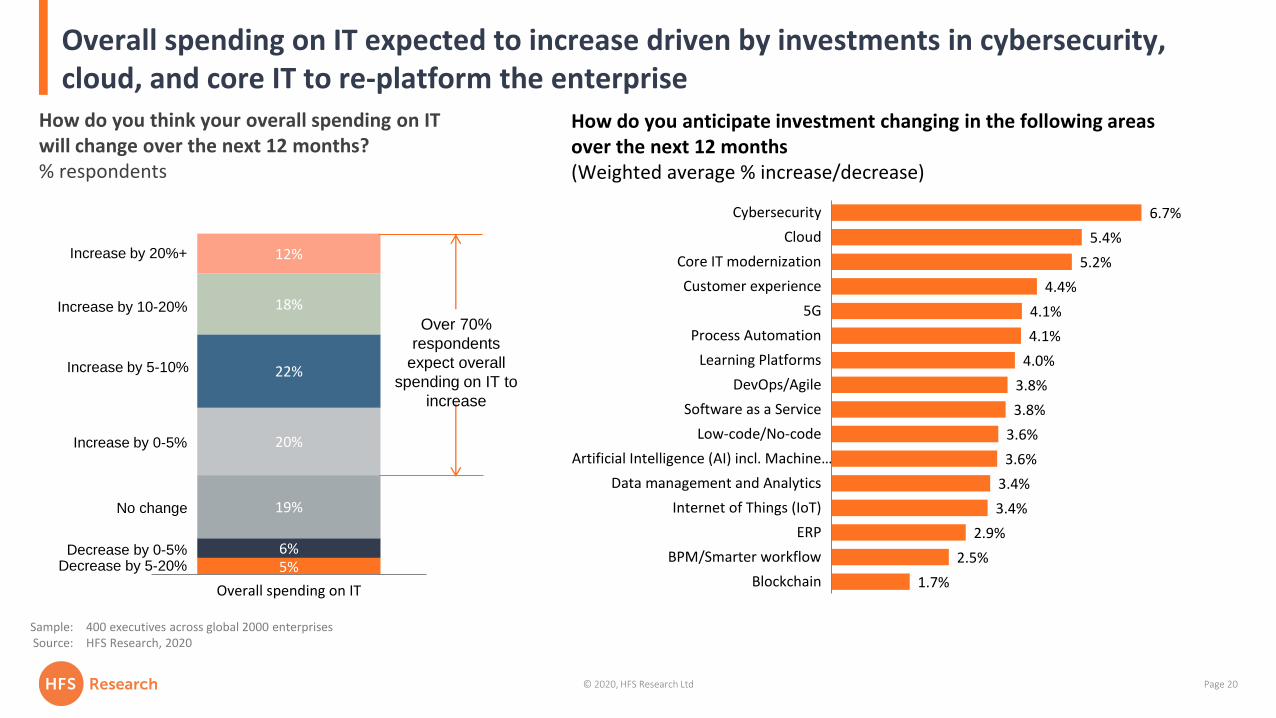

Overall spending on IT expected to increase driven by investments in cybersecurity, cloud, and core IT to re-platform the enterprise

How do you think your overall spending on IT will change over the next 12 months?% respondents

5%6%

19%

20%

22%

18%

12%

Overall spending on IT

Decrease by 5-20%

Increase by 0-5%

Increase by 10-20%

Decrease by 0-5%

No change

Increase by 5-10%

Increase by 20%+

Over 70%

respondents

expect overall

spending on IT to

increase

6.7%

5.4%

5.2%

4.4%

4.1%

4.1%

4.0%

3.8%

3.8%

3.6%

3.6%

3.4%

3.4%

2.9%

2.5%

1.7%

Cybersecurity

Cloud

Core IT modernization

Customer experience

5G

Process Automation

Learning Platforms

DevOps/Agile

Software as a Service

Low-code/No-code

Artificial Intelligence (AI) incl. Machine…

Data management and Analytics

Internet of Things (IoT)

ERP

BPM/Smarter workflow

Blockchain

How do you anticipate investment changing in the following areas over the next 12 months (Weighted average % increase/decrease)

Sample: 400 executives across global 2000 enterprisesSource: HFS Research, 2020

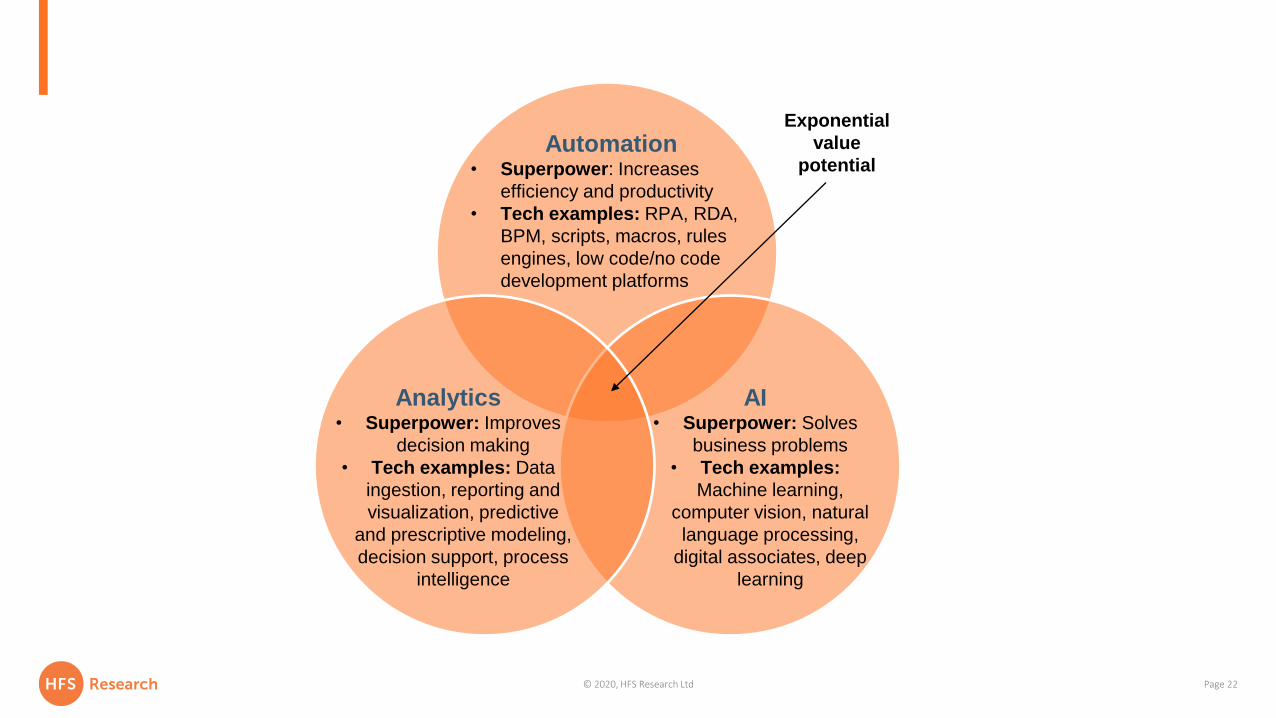

The Triple-A Trifecta and why it’s about joining up the pieces, not obsessing on the parts

© 2020, HFS Research Ltd Page 22

Automation• Superpower: Increases

efficiency and productivity

• Tech examples: RPA, RDA,

BPM, scripts, macros, rules

engines, low code/no code

development platforms

AI• Superpower: Solves

business problems

• Tech examples:

Machine learning,

computer vision, natural

language processing,

digital associates, deep

learning

Analytics• Superpower: Improves

decision making

• Tech examples: Data

ingestion, reporting and

visualization, predictive

and prescriptive modeling,

decision support, process

intelligence

Exponential

value

potential

© 2020, HFS Research Ltd Page 23

Strongly agree, 24%

Agree, 40%

Neutral, 28%

Disagree, 6%

Strongly disagree, 2%

Strongly agree, 23%

Agree, 45%

Neutral, 24%

Disagree, 6%

Strongly disagree, 2%

64% 68%

Sample: 600 executives across Global 2000 enterprises (Phase I sample)

Source: HFS Research in conjunction with KPMG

Nearly 65% respondents believe that the combined use of emerging technologies is beneficial – and a similar number say Triple-A, Cloud, and Low Code are converging.

The combined use of emerging technologies is much more

beneficial than using any of these technologies in isolation

Automation, AI, analytics, cloud, and low-code

platforms are converging

© 2020, HFS Research Ltd Page 24

38%42%

59%

35%

44%41%

34%

19%21%

16%

6%

15% 16%13%

Smart analytics Hybrid or multi-cloud Process automation Blockchain Artificial intelligence Edge computing 5G

Respondents who strongly agree to the power of AND Respondents who disagree to the power of AND

Sample: 600 executives across Global 2000 enterprises (Phase I sample)

Source: HFS Research in conjunction with KPMG

Organizations that “strongly agree” to the power of AND have a higher realized value compared to organizations that “disagree”

Already realized value from investments in emerging

technologies

© 2020, HFS Research Ltd Page 25

Focus on enhanced support across the spectrum of hire-to-retire with an increased emphasis on employee experience:● Streamlined onboarding and provision, enhanced self-service moving from search-based

experience to conversation-driven experience, creation of intelligent workflows, recruitment effectiveness, query resolution, benefit administration

Triple-A usage in sales and marketing focuses heavily on campaign optimization and revenue enhancement:● Marketing campaign management and lead conversion, improved return on campaigns through

optimal website ad placements, quote management, order management and upselling, price and portfolio management, behavioral correlations across sales funnel, dynamic pricing

Customer service use cases are dominated by contact center optimization and the quest to make agents as productive as possible across all channels:● Customer loyalty program management, agent optimization in contact centers, next best action,

customer email management, classification and response, contact analytics, digital associates for self-service and off-hours coverage, repeat call optimization

A broad range of use cases across accounts payable, order to cash, record to report, controllership activities, and finance transformation:● Reconciliations, identity management, digitization of the controllership function, revenue

forecasting, invoice management, journey entry exceptions management, audit, reporting, fraud

Leading use cases for Triple-A Trifecta services

Industry-specific (representative)

● BFS: Payment investigation, commercial cards, accounts services, settlements, fund accounting, fraud detection, collateral monitoring, portfolio administration

● Insurance: Claims processing, new business, underwriting, billing and collections, subrogation● Retail and CPG: Digital shopping experience, smart home, smart store, trade promotions, order

management and experience, customer journey optimization

Finance and accounting

Customer service

Sales and marketing

Human resources

The Triple-A Trifecta goes deep with industry-specific use cases and value beyond cost and efficiency. ● The 21 service providers covered in

this report shared 180+ case studies showcasing how they bring the enhanced value of the Triple-A Trifecta to their clients.

● Across the providers, the leadingcategory of Triple-A use cases is for industry-specific processes and functions. This points to better alignment of emerging technologies use with core business needs and objectives and outcomes focused on revenue growth, CX, and EX.

● F&A and other back office and operations-centric domains persist as strong poster children for Triple-A Trifecta services engagements in alignment with the perpetual need to drive efficiency and cost optimization.

Source: HFS Research, 2020

N= 182 Triple-A Trifecta services case studies

© 2020, HFS Research Ltd Page 26

Get ready to go native

Piecemeal automation Intelligent automation Native automation

Automation

Artificial IntelligenceAnalytics

• The HFS Triple-A Trifecta• End-to-end automation

BPM

RPA

AI

Analytics

• Silos• Task automation• Incremental results

• Digital transformation

We are somewhere here

People

Process

Triple-A stack

Data

Change

management

OneOffice

The death of GBS and the emergence of OneOffice as the operating mindset for the work-anywhere enterprise

© 2020, HFS Research Ltd Page 28

New sentiments are driving fundamental operating model decisions

43

25

13

8

3

3

3

2

17

7

15

17

13

9

7

15

8

7

11

10

17

17

19

10

We need to accelerate digital initiatives as COVID-19 becomes the

burning platform to change

We need to drive profits with a purpose that impacts broaderstakeholders beyond shareholders

We require a new wave of “cost reduction” as we enter a

recessionary economy

We now have a real opportunity to manage the enterprisetechnical debt

We need to focus on virtual consumer experiences for the new

digital world

We need to de-risk our supply chain to ensure that it is far moreresilient

We need to adapt and change our business model to have abetter chance to come out stronger at the other end

We need to focus on process debt (wasteful activities)

Rank 1 Rank 2 Rank 3

Which of the following statements most accurately captures the current sentiment for your organization?Percentage respondents

Sample: 150 C-level executives across the global 2000 enterprisesSource: HFS Research, 2020

• Tension and tradeoffs between experience and efficiency initiatives

• Sacred cows in terms of how people work getting thrown out especially when it comes to service delivery model and outsourcing decisions

© 2020, HFS Research Ltd Page 29

The March to the OneOffice Mindset and why rigid organization and operating models will fall to wayside

• GBS grew from 5% to 11% between 2016 and 2019 – with little movement since then

• Movement away from models focusing on process efficiency to one focusing on business outcomes and experience optimization

© 2020, HFS Research Ltd Page 30

Coming up in 2021!HFS OneOffice Enterprise Maturity Assessment Model – A new way to accelerate value

Level 1

Starting gate

Level 2

Piecemeal

Level 3

On the fence

Level 4

Optimized

Level 5

Transformational

Digital enablement is in the very early stages and does not feature in strategy discussions either around employee and customer engagement and experience.

Digital enablement is in the pilot stages. It is part of strategy discussions at a functional level but there is not a clear corporate position or understanding of impacts to employees or customers.

There are instances for end-to-end digital enablement on a process level but not consistently deployed for most service delivery initiatives touching both the customer and employee.

Digital enablement for linking back, middle and front office processes is wide -spread but it is mainly used to increase efficiency and not as a transformation initiative.

Digital enablement is a mission critical enterprise-level goal and transparently supports achieving the most important corporate objectives around customer experience, financial performance, etc. It has produced a shift in mindset from considering technology as a tool for enablement to considering technology as a tool to a differentiator for business outcomes.

The HFS OneOffice Enterprise Maturity Assessment driven by a balanced scorecard approach across the HFS Vision 2025 Fundamentals for OneOffice Organization: • The principle: Connect the front, middle, and back offices to deliver the “OneOffice Organization”• The talent: Align employees to customers with experience and skills• The Architecture: Slay your legacy dragons to go “straight-to-digital” with an integrated enterprise technology platform• The Competencies: Expand the traditional “people, process, and technology” paradigm to include data and change management• The Strategy: Collaborate not just internally but also externally

The OneOffice skills needed to ensure Digital Fluency

© 2020, HFS Research Ltd Page 32

9% 13% 12% 18% 19% 24% 28%22%

23% 28%30% 30%

29% 26%

65% 63% 56%50% 49% 46% 44%

Developing new skillsinhouse through

training

Expecting our staff tolearn on the job andengage with learning

and developmentresources

Leverage our partners to bring skills and

capability we don’t have

Crowdsourcing labour Actively recruitpermanent staff for

specific skills

Recruit people whoare a good fit andthen train them

Recruit temporarystaff for specific skillswhere we need them

The urgency to develop new skills inhouse through training has increased significantly

Post-COVID, how will the urgency of the following talent development activities change?% respondents

Decrease

No change

Increase

Sample: 400 executives across global 2000 enterprisesSource: HFS Research in partnership with Infosys, 2020

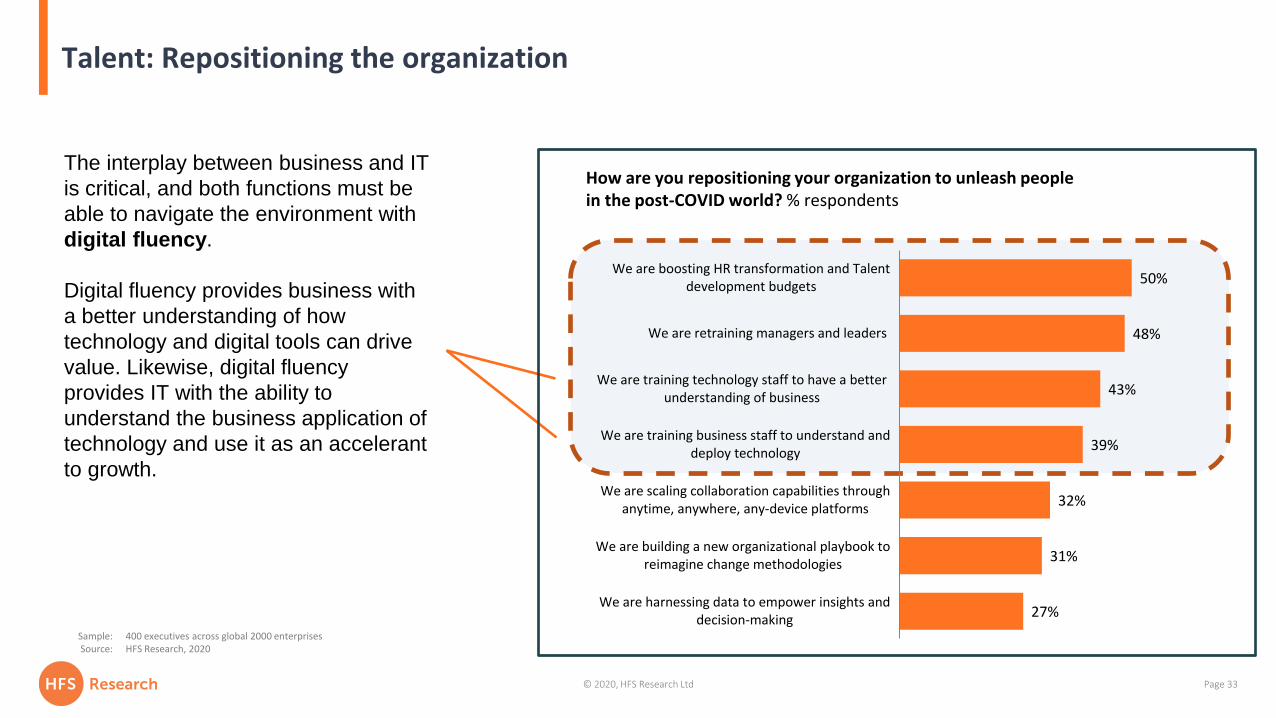

© 2020, HFS Research Ltd Page 33

Talent: Repositioning the organization

Sample: 400 executives across global 2000 enterprisesSource: HFS Research, 2020

How are you repositioning your organization to unleash people in the post-COVID world? % respondents

50%

48%

43%

39%

32%

31%

27%

We are boosting HR transformation and Talentdevelopment budgets

We are retraining managers and leaders

We are training technology staff to have a betterunderstanding of business

We are training business staff to understand anddeploy technology

We are scaling collaboration capabilities throughanytime, anywhere, any-device platforms

We are building a new organizational playbook toreimagine change methodologies

We are harnessing data to empower insights anddecision-making

The interplay between business and IT

is critical, and both functions must be

able to navigate the environment with

digital fluency.

Digital fluency provides business with

a better understanding of how

technology and digital tools can drive

value. Likewise, digital fluency

provides IT with the ability to

understand the business application of

technology and use it as an accelerant

to growth.

© 2020, HFS Research Ltd Page 34

Today’s organizations needs to look

at a core sets of skills – and new

applications of existing skills –in the

context of an integrated organization,

a new digital reality, and the speed

and pace of change.

HFS has defined six core skills

categories for the future of work.

HFS has defined six core skills categories for the future or work

© 2020, HFS Research Ltd Page 35

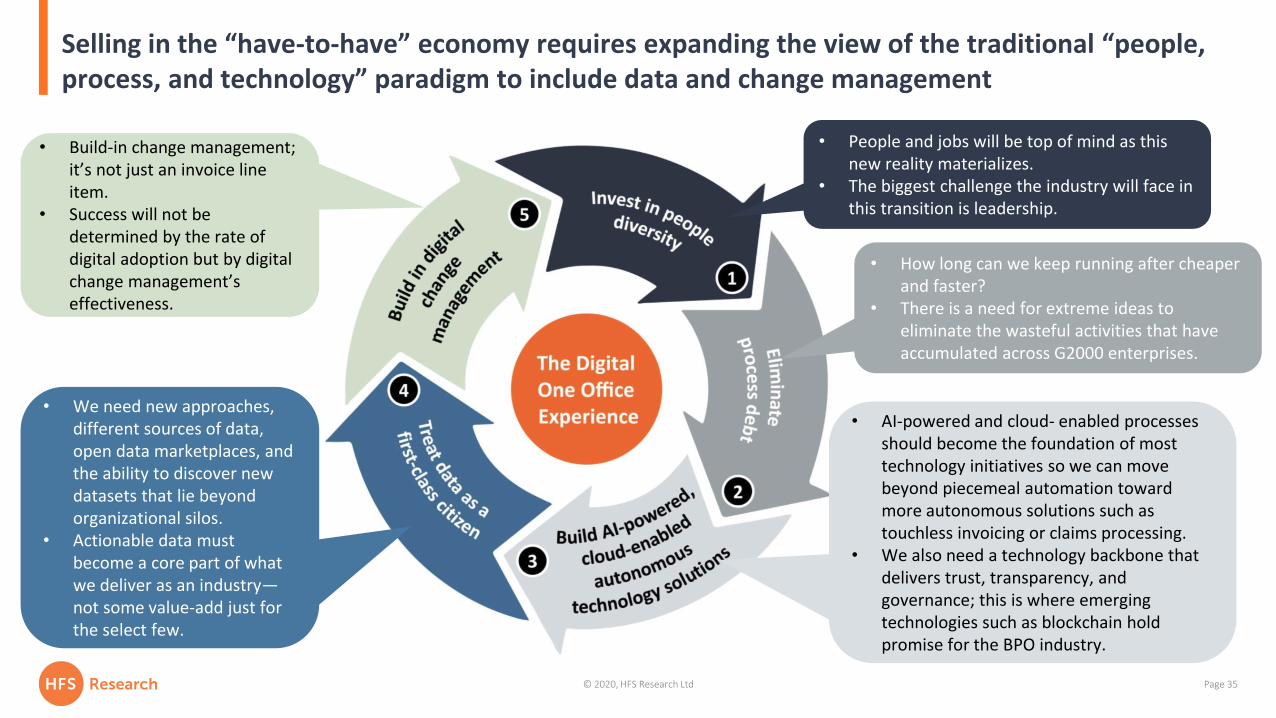

Selling in the “have-to-have” economy requires expanding the view of the traditional “people, process, and technology” paradigm to include data and change management

• People and jobs will be top of mind as this new reality materializes.

• The biggest challenge the industry will face in this transition is leadership.

• How long can we keep running after cheaper and faster?

• There is a need for extreme ideas to eliminate the wasteful activities that have accumulated across G2000 enterprises.

• AI-powered and cloud- enabled processes should become the foundation of most technology initiatives so we can move beyond piecemeal automation toward more autonomous solutions such as touchless invoicing or claims processing.

• We also need a technology backbone that delivers trust, transparency, and governance; this is where emerging technologies such as blockchain hold promise for the BPO industry.

• We need new approaches, different sources of data, open data marketplaces, and the ability to discover new datasets that lie beyond organizational silos.

• Actionable data must become a core part of what we deliver as an industry—not some value-add just for the select few.

• Build-in change management; it’s not just an invoice line item.

• Success will not be determined by the rate of digital adoption but by digital change management’s effectiveness.

© 2020, HFS Research Ltd Page 36

Localize talent. Not offshore everything

Wipro is also aggressively localizing its workforce

(from Wipro’s 2019-20 annual report)

The massive healthcare revolution and how the tech and services industry can provide intelligence, scale and agility

© 2020, HFS Research Ltd Page 38

A trifecta of challenges—demand explosion, supply shortage, and the pandemic shock—has created a burning platform for the healthcare industry to embrace change

Increasing demand

Rising costs Pandemic shock

Do you expect COVID-19 to have a bigger or smaller impact on markets than the 2008 downturn?% healthcare and life sciences respondents

53%

14%

28%

5%

Much bigger Bigger

About the same Smaller

Sample: 36 healthcare and life sciences executives across global 2000 enterprises

Source: HFS Research, 2020

Source: StatistaSource: United Nations Department of Economic and social affairs

© 2020, HFS Research Ltd Page 39

Major innovations in the healthcare industry

Reduce cost of care

(Increase supply)

Shift from illness to wellness

(Reduce demand)

Drive resiliency and compliance

(Manage risks)

• Alignment of stakeholder incentives

• Vertical integration and emergence of

payviders

• Administrative cost optimization

(touchless claims, intelligent

automation, BPaaS)

• Optimizing broken processes,

digitizing paper-based manual

activities

• Virtualizing care (digital care and

telehealth, remote care, home care,

population-health management,

wearables and IoT devices)

• Encourage health and wellness (smart

analytics, AI)

• Patient experience (unified, seamless,

personalized, omni-channel, digital front

door)

• Access to health data (cloud,

blockchain)

• Modernize legacy health systems

(cybersecurity, data privacy, resiliency,

IT modernization)

• Supply chain resiliency

• Regulatory compliance (interoperability,

value-based care)

© 2020, HFS Research Ltd Page 40

Improving the customer and patient experience is at the heart of healthcare transformation

Rank the following statements about your organization's objectives for business operations transformation over the next three years

Average rank across respondents

Improve customer experience

Create new business models

Grow top-line revenue

Increase bottom-line profit

Optimize regulatory compliance

Rank 1 Rank 2 Rank 3 Rank 4 Rank 5

1.8

3.1

3.2

3.3

3.7

Sample: 41 healthcare clientsSource: HFS Research, 2020

HFS 2021 Research Agenda

© 2020, HFS Research Ltd Page 42

HFS Vision 2025 – Research Coverage Areas

© 2020, HFS Research Ltd Page 43

● HFS Market Vision Paper● HFS Digital Roundtable● HFS Webinar● HFS Unfiltered Podcast● HFS Enterprise Success Story

● HFS OneOffice Pulse● HFS Market Vision Paper● HFS Global 2000 Enterprise

Research

● HFS ThinkTank● Voice of the Customer

(VOC) Dashboard● Market Feasibility

Assessment● M&A Advisory

● HFS Top 10 reports● HFS Industry Primers● HFS Hot Vendors● HFS Market Analysis ● Emerging Tech Case Study

Compendium● Competitive Intelligence● HFS POVs and Blogs

HFS

HFS Research Agenda 2021 – Engagement Model

© 2020, HFS Research Ltd Page 44

16

5 2

344. Industry Snapshot Reports will focus on industry-specific drivers, challenges, IT and business services and adoption of emerging technologies by industry value chains. We plan to publish these reports for each of the 10 industries1 covered by HFS.

5. OneOffice Maturity Diagnostic will allow our enterprise clients to compare their OneOffice journey with 1000 other enterprises across the 5 pillars of HFS Vision 2025 and engage with HFS analysts to understand emerging best practices.

6. Tailored Advisory Sessions. HFS clients will also be able to understand differences by industry, geography, and size of the clients through customized advisory sessions with HFS analysts.

The ultimate guide to technology and business services:

1. Institutionalized proactive versus reactive research

2. Upcoming trends (versus look-back reflection) to anticipate upcoming client and user demand

3. 1000 global 2000 enterprise executives across our research coverage areas

4. 10 Industry Sectors

5. Semi-annual

6. Assessments of where to invest based on current maturity

OneOffice Pulse

1. The journey to the OneOffice. The semi-annual report will focus on the current enterprise maturity across the pillars of HFS Vision 2025: OneOffice operating model competencies, talent, business/IT architecture, and strategy.

2. Outlook for technology and business services. The semi-annual report will focus on the adoption and investment priorities across emerging technologies, relative growth across IT and business services, and anticipated changes to consumption and delivery models.

3. Deep dive on the current hottest area. Every six months, we will focus on one of the hottest segments across our research coverage based on client demand. The first coverage area will be the 2021 state of “Cloudification.”

© 2020, HFS Research Ltd Page 45

HFS Top 10 Research in 2021 | New “OneOffice” Dimension in addition to Execution, Innovation, and Voice of the Customer

Ability to Execute

Focuses on size, growth, experience, expertise,

geographic footprint, and delivery excellence

NEW: Alignment with OneOffice fundamentals

HFS Top 10 Research ranks service providers across execution, innovation, and voice of the customer criteria. Starting 2021, we are adding

a new dimension to our Top 10 evaluations: Alignment with OneOffice fundamentals

Innovation capability

Focuses on vision, go-to-market strategy, investments, emerging technologies, and creative client

engagement

Voice of the Customer

Focuses on direct feedback from both reference and non-

reference clients

© 2020, HFS Research Ltd Page 46

Q&A

Click here to access the full report

Top Related