Your name Fundamentals Concepts and Tools of Business Finance By: Mrs. Belen B. Apostol.

62

your name Fundamentals Concepts and Tools of Business Finance By: Mrs. Belen B. Apostol

-

Upload

abraham-bradford -

Category

Documents

-

view

215 -

download

0

Transcript of Your name Fundamentals Concepts and Tools of Business Finance By: Mrs. Belen B. Apostol.

your name

Fundamentals Concepts and Tools of

Business Finance

By: Mrs. Belen B. Apostol

your name

FINANCE

• The study of the acquisition and investment of cash for the purpose of enhancing value and wealth.

• is the science of funds management.

your name

FINANCEPublic Finance – general finance, deals

with the revenue and expenditure patterns of the government and their various effects on the economy.

Private Finance – general finance not classified as public finance:

1.Personal Finance – managing one’s own personal money affairs.

2.The finance of non-profit organizations – undertakings such as charity, religion and private education

your name

3. BUSINESS FINANCE

• Refers to the provision of money for commercial use.

• Concerned with the effective use of funds

• Covers financial management of private profit seeking concerns in the business service, trade, manufacturing, mining, public utilities and financing.

your name

3. BUSINESS FINANCE

• Procurement and administration of funds with the view of achieving the objectives of the business.

• 3 aspects of Business Finance

1.Small business finance;

2.Corporation finance; and

3.Multinational business finance

your name

FINANCE

Public Finance

Private Finance

PersonalFinance

MultinationalBusinessFinance

CorporationFinance

Small BusinessFinance

Finance of Non- Profit

Organization

Business Finance

Categories of Finance

your name

Goals of Business Finance

1. Maximizing profit

2. Maximizing profitability

3. Maximizing profit subject to cash constraint

4. Maximizing net present worth;

5. Seeking an optimum position along a risk- return frontier.

your name

Goals of Business Finance

1. Maximizing profit

- realizing the highest peso or dollar income.

2. Maximizing Profitability

- obtaining a higher rate of return on its investment

your name

Goals of Business Finance

3. Maximizing profit subject to cash constraint

- maximize profits and maintain a cash balance that can take care of cash requirements anytime.

your name

Goals of Business Finance

4. Maximizing Net Present Worth

- the firm’s objective is to maximize the current value of the company to its owners.

- Net Present worth = value of the firm (now) + values (arising in the future)

your name

Goals of Business Finance

4. Maximizing Net Present Worth/Value

Time Value of Money

- money increases in value with the passing of time.

your name

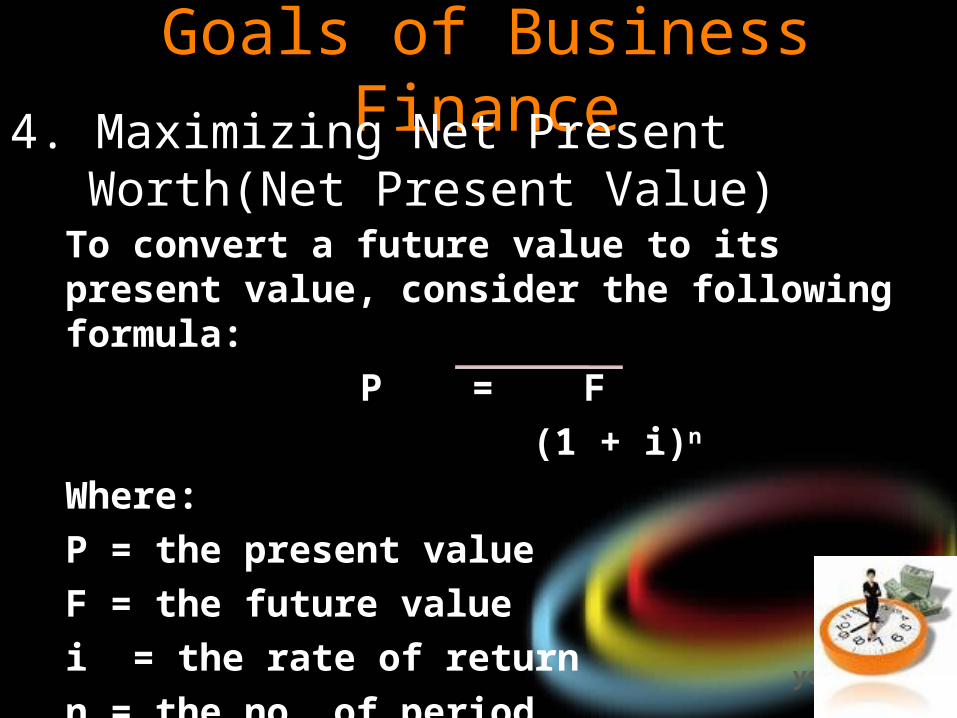

Goals of Business Finance4. Maximizing Net Present Worth(Net

Present Value)To convert a future value to its present value, consider the following formula:

P = F

(1 + i)n

Where:

P = the present value

F = the future value

i = the rate of return

n = the no. of period

your name

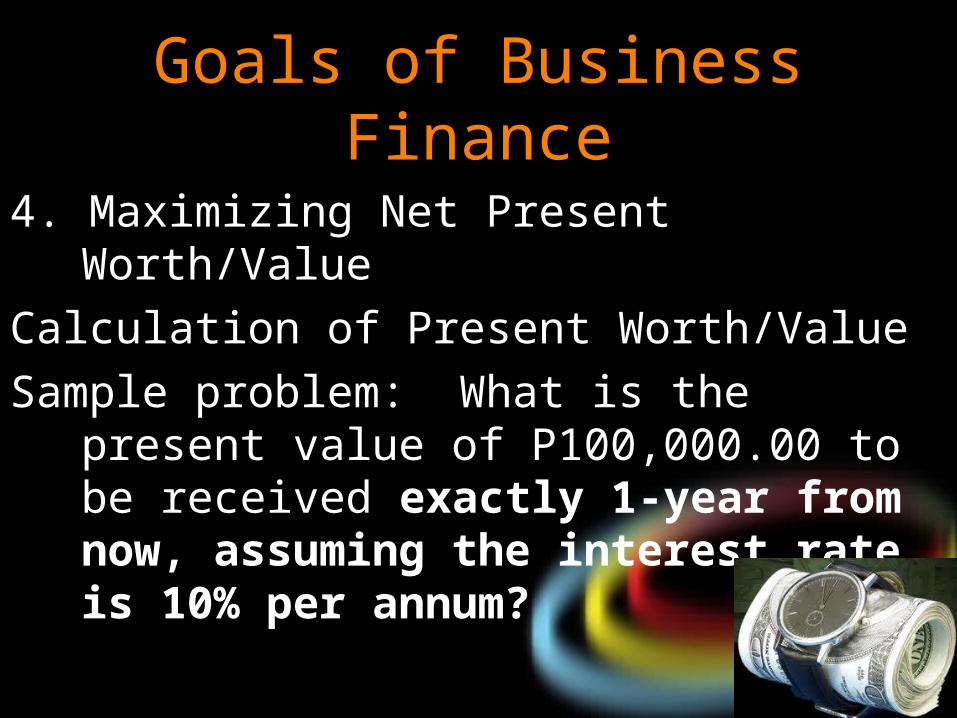

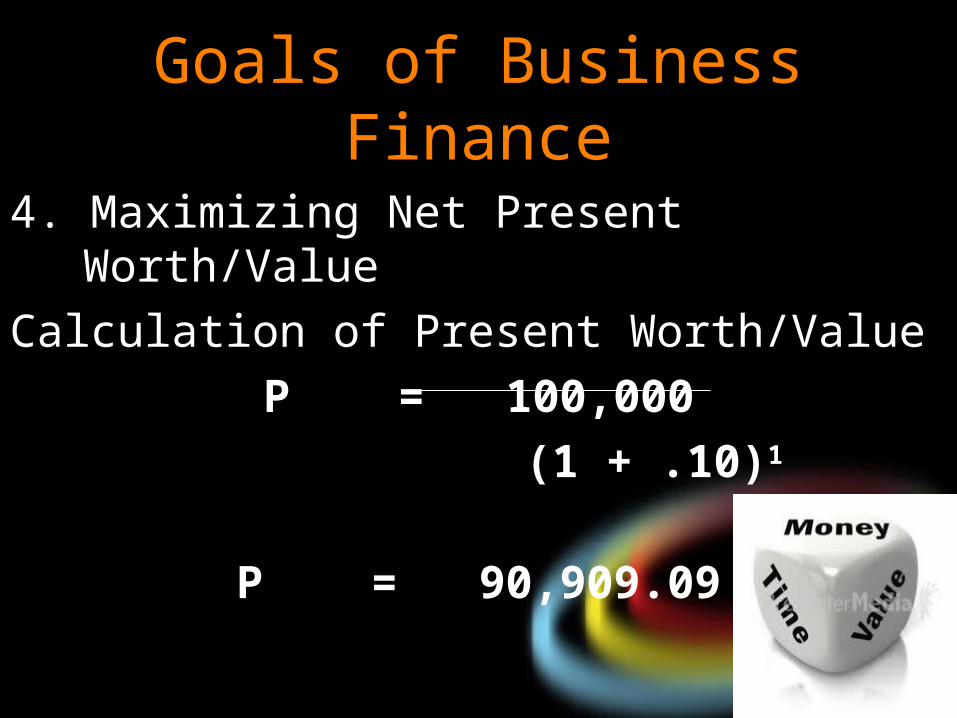

Goals of Business Finance

4. Maximizing Net Present Worth/Value

Calculation of Present Worth/Value

Sample problem: What is the present value of P100,000.00 to be received exactly 1-year from now, assuming the interest rate is 10% per annum?

your name

Goals of Business Finance

4. Maximizing Net Present Worth/Value

Calculation of Present Worth/Value

P = 100,000

(1 + .10)1

P = 90,909.09

your name

Goals of Business Finance5. Seeking an Optimum Position Along a risk- return

frontier

- a firm sets a goal of achieving the best possible combination of risk and return

Return on Investment or Net worth – net income generated by the use of investments of a firm (rate of return when expressed in percentage)

Risk – potential incurrence of loss of money or its equivalent.

your name

Goals of Business Finance5. Seeking an Optimum Position Along a Risk- Return

Frontier

Calculation of Expected Value Using Risk and Return Factors.

The optimum position of risk and return

may be determined by calculating the expected

value of alternative decisions. The expected

value of a return on investment is equal to the

return times the percentage of probability that will

happen (risk factor)

your name

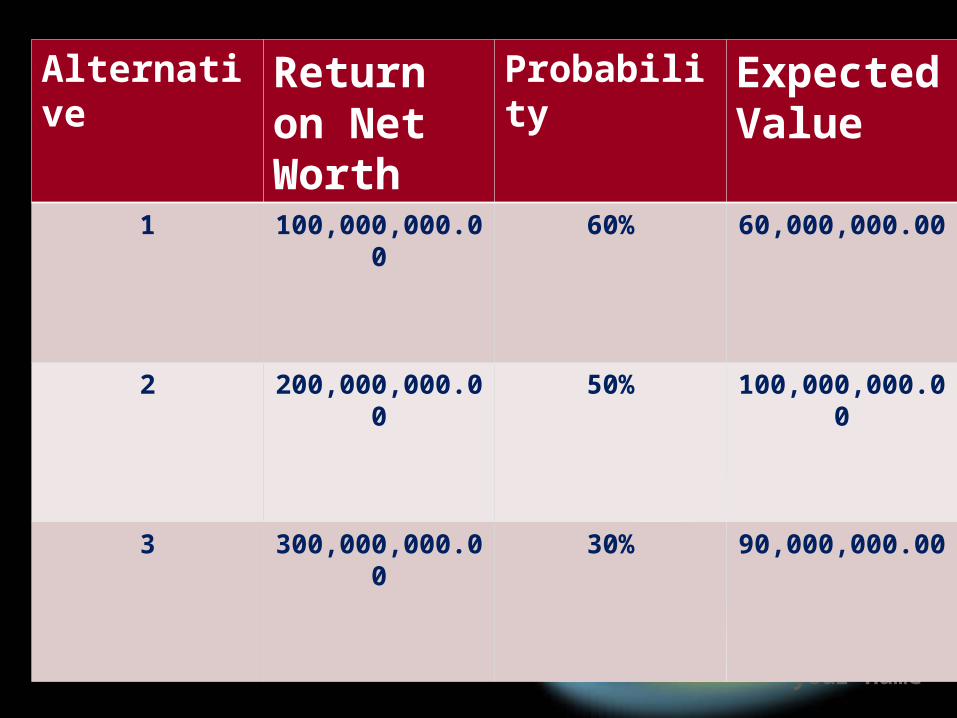

Alternative Return on Net Worth

Probability Expected Value

1 100,000,000.00 60% 60,000,000.00

2 200,000,000.00 50% 100,000,000.00

3 300,000,000.00 30% 90,000,000.00

your name

THE FINANCIAL STATEMENT

- Presents the financial information to various interested parties.

- formal record of the financial activities of a business, person, or other entity.

your name

THE FINANCIAL STATEMENT• Basic financial statements:• Statement of Financial Position: also referred

to as a balance sheet, reports on a company's assets, liabilities, and ownership equity at a given point in time.

• Statement of Income: also referred to as Profit and Loss statement (or a "P&L"), reports on a company's income, expenses, and profits over a period of time

your name

• Profit & Loss account provide information on the operation of the enterprise. These include sale and the various expenses incurred during the processing state.

• Statement of cash flows: reports on a company's cash flow activities, particularly its operating, investing and financing activities.

THE FINANCIAL STATEMENT

your name

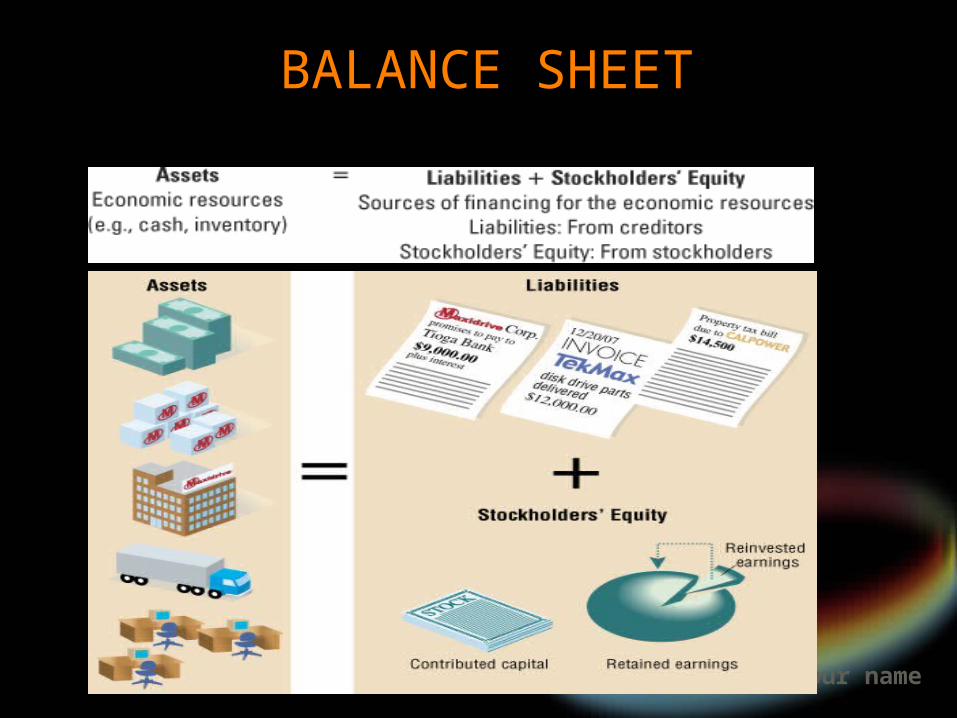

BALANCE SHEET

– statement produced periodically, normally at the end of a financial year, showing an organization’s assets, liabilities and the interest of the owners.

your name

BALANCE SHEET

ASSETS – everything that the firm owns which has monetary value classified as follows:

1.Current Assets

2.Trade Investments

3.Fixed Assets

4.Intangible Assets

your name

BALANCE SHEET

Current Assets – composed of cash, bank deposits and other items readily convertible into cash like accounts receivable, stocks and work-in-process (inventory), and marketable securities.

Trade Investments – composed of investments in subsidiary or associated companies

your name

BALANCE SHEET

Fixed Assets – shows the firm’s ownership of property like land, buildings, plant and machinery , equipments, vehicles, furniture and fixtures, all valued at cost less depreciation written off; and

Intangible Assets – present goodwill, patents, copyright which are attributed to the firm.

your name

BALANCE SHEETLIABILITIES – shows the profile of debts of

the company classified as current liabilities (payable within 1 year) and long-term liabilities (payable after 1 year).

Accounts Payable – debts payable within a few days, weeks, or months like those incurred in the purchase of raw materials

your name

BALANCE SHEET

Loans and Notes Payable – debts evidenced by promissory notes and oftentimes backed up by collaterals. Creditors of this type of liability are composed of banks, suppliers, financing companies, and the public.

Advances from Customers – down payments made before orders are processed.

your name

BALANCE SHEETAccrued Expenses – this refers to obligations

which have been incurred but not yet paid.

Mortgage Payable – company borrowings and other sources of funds. This represents long-term debts and is usually secured by land, buildings, or equipment.

Bonds Payable – issued when a large amount of long-term debt is sought from a large number of creditors.

your name

BALANCE SHEETNET WORTH – interest of the owner or

owners in the company.

In a single proprietorship, the owner’s interest usually appears as a single account, for instance, “Miriam Defensor, Capital.” This represents sums invested by the owner, which is increased by profits and decreased by losses and withdrawals.

your name

BALANCE SHEETIn a partnership, the interests of the

partners are presented separately like the following:

Jose Rizal, Capital P10,000,000

Andres Bonifacio, Capital 20,000,000

Apolinario Mabini, Capital 30,000,000

Total Net Worth 60,000,000

your name

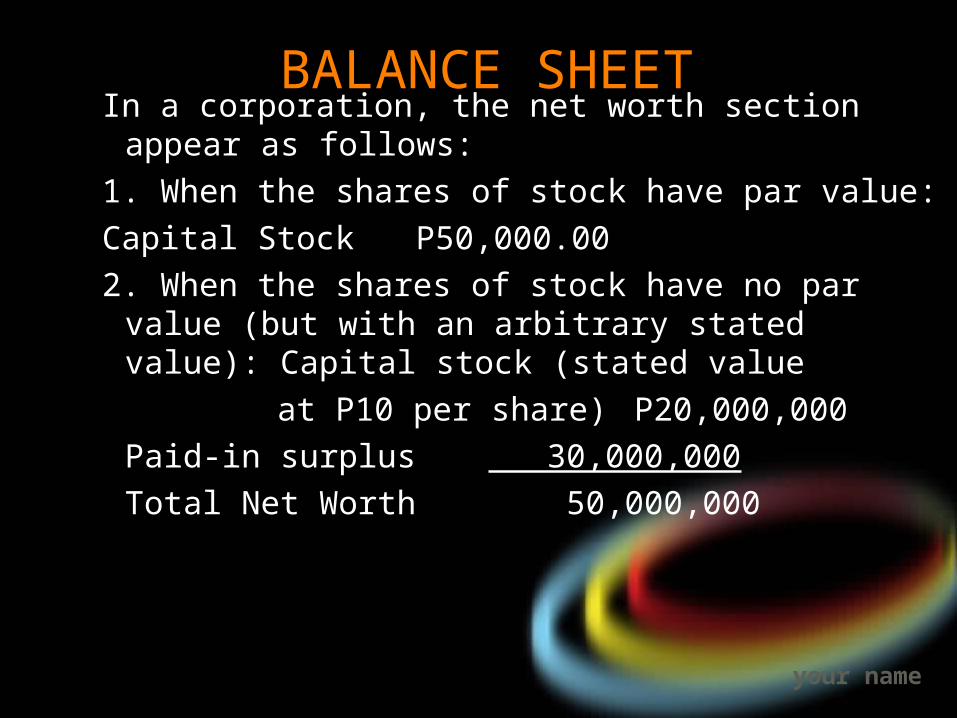

BALANCE SHEETIn a corporation, the net worth section appear as

follows:

1. When the shares of stock have par value:

Capital Stock P50,000.00

2. When the shares of stock have no par value (but with an arbitrary stated value): Capital stock (stated value

at P10 per share) P20,000,000

Paid-in surplus 30,000,000

Total Net Worth 50,000,000

your name

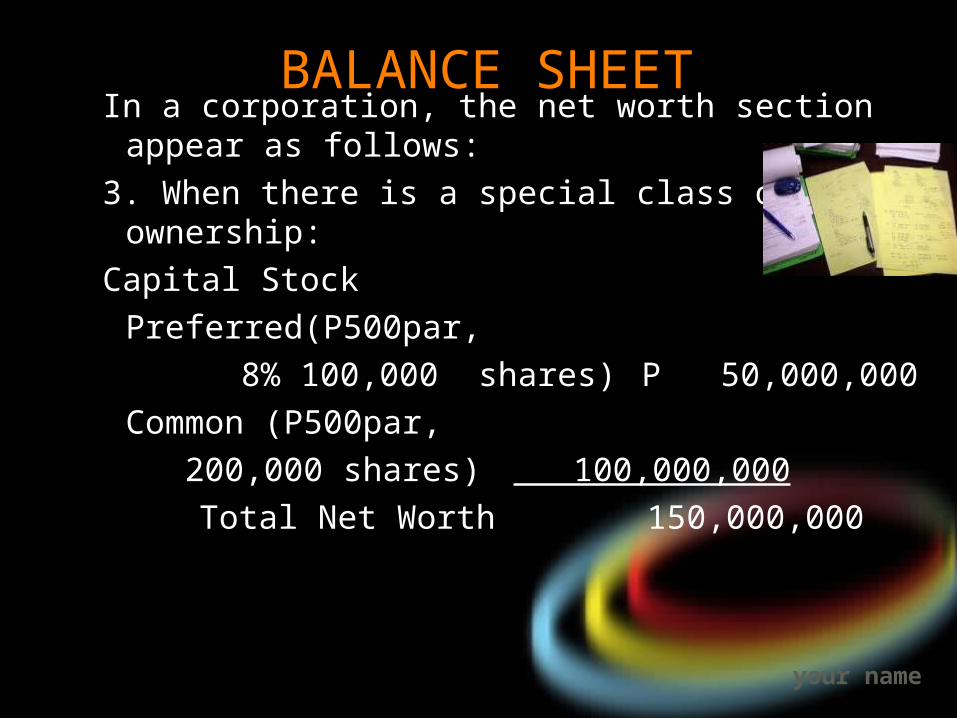

BALANCE SHEETIn a corporation, the net worth section appear as

follows:

3. When there is a special class of ownership:

Capital Stock

Preferred(P500par,

8% 100,000 shares) P 50,000,000

Common (P500par,

200,000 shares) 100,000,000

Total Net Worth 150,000,000

your name

BALANCE SHEET

your name

BALANCE SHEET

• ABC Corporation• Balance Sheet

• December 31, 200X

• Assets • Cash P XXX• Accounts Receivable XXX• Inventories XXX• Plant and Equipment XXX• Land XXX

• Total Assets P XXX

• Liabilities • Accounts Payable P XXX• Notes Payable XXX

• Total Liabilities P XXX

• Stockholders’ Equity• Contributed Capital P XXX• Retained Earnings XXX

• Total Liabilities and • Stockholders’ Equity P XXX

Name of the Entity

Title of the statement

Specific Date of Statement

Amounts owed on written contracts

Amounts invested in the Bus. By the stockholders

Past earnings not distributed to stockholders

Factories and production machinery

Amounts owed to suppliers for prior purchase

Land on which the factories are built

Parts and completed but unsold

Amount of Cash in company’s bank accounts

Amounts owed by customers from prior sales

your name

INCOME STATEMENT• The income statement represents the

revenues realized from the sale of commodities and services produced by the company as well as the cost and expenses incurred in connection with the realization of said revenues.

• Presents a summary of the transactions for a given period.

your name

INCOME STATEMENT• Revenues – refers to the gross income

from the production and sale of the firm’s product or service. It includes cash collections and receivables or unpaid sale. It does not include trade discounts allowed to distributors or other middlemen. Returns and allowances are deducted also from the gross revenue.

your name

INCOME STATEMENT• Expenses – this refers to the monetary

values of the goods and services used in the production and delivery process in order to obtain revenues. It consist of three items:

1.The cost of goods sold/ manufactured and sold

2.Operating expenses

3.Other expenses

your name

INCOME STATEMENT• Cost of Goods Manufactured and

Sold – represents the summary of the cost of raw materials, labor and various overhead costs directly involved in the manufacturing process and which represent the manufacturing cost of goods sold during a period of consideration.

your name

• Overhead cost – expenditures like salaries of supervisors, depreciation, light and water, supplies and factory rent.

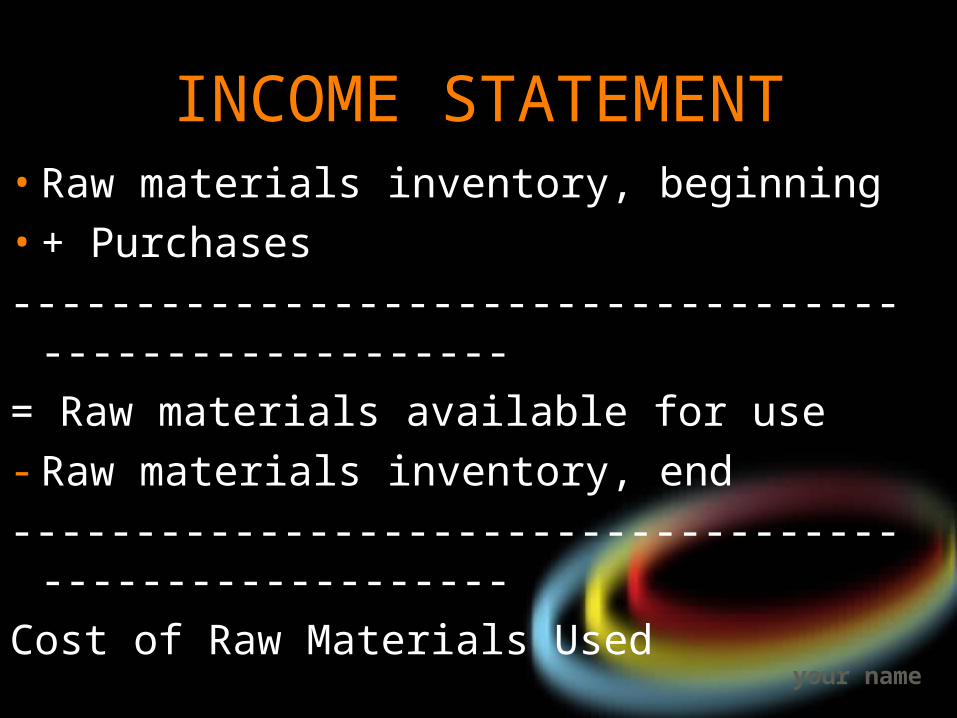

• The cost of direct materials is computed by deducting the raw materials inventory, end from the total available for use computed as the sum of raw materials inventory, beginning and purchases during the period.

INCOME STATEMENT

your name

• Raw materials inventory, beginning

• + Purchases

-------------------------------------------------------

= Raw materials available for use

- Raw materials inventory, end

-------------------------------------------------------

Cost of Raw Materials Used

INCOME STATEMENT

your name

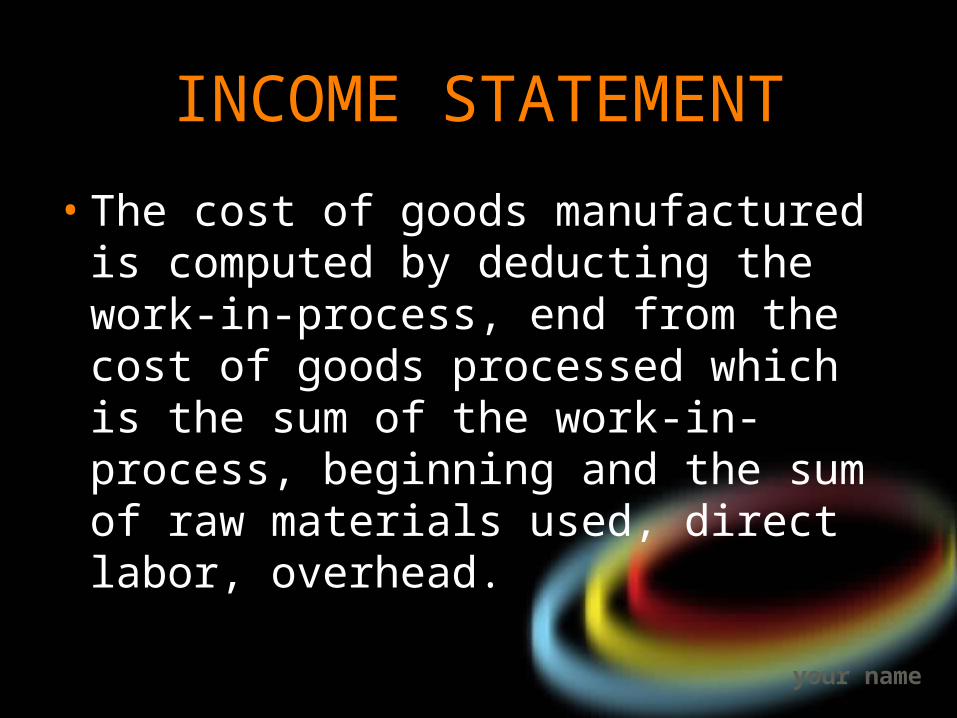

• The cost of goods manufactured is computed by deducting the work-in-process, end from the cost of goods processed which is the sum of the work-in-process, beginning and the sum of raw materials used, direct labor, overhead.

INCOME STATEMENT

your name

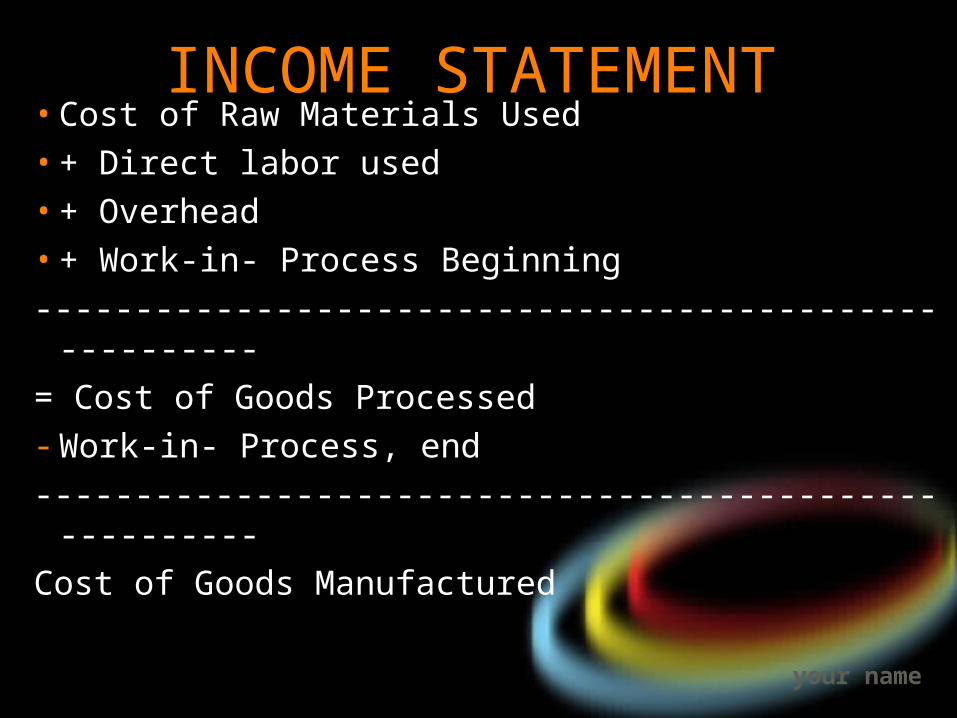

• Cost of Raw Materials Used• + Direct labor used• + Overhead• + Work-in- Process Beginning

-------------------------------------------------------

= Cost of Goods Processed- Work-in- Process, end

-------------------------------------------------------

Cost of Goods Manufactured

INCOME STATEMENT

your name

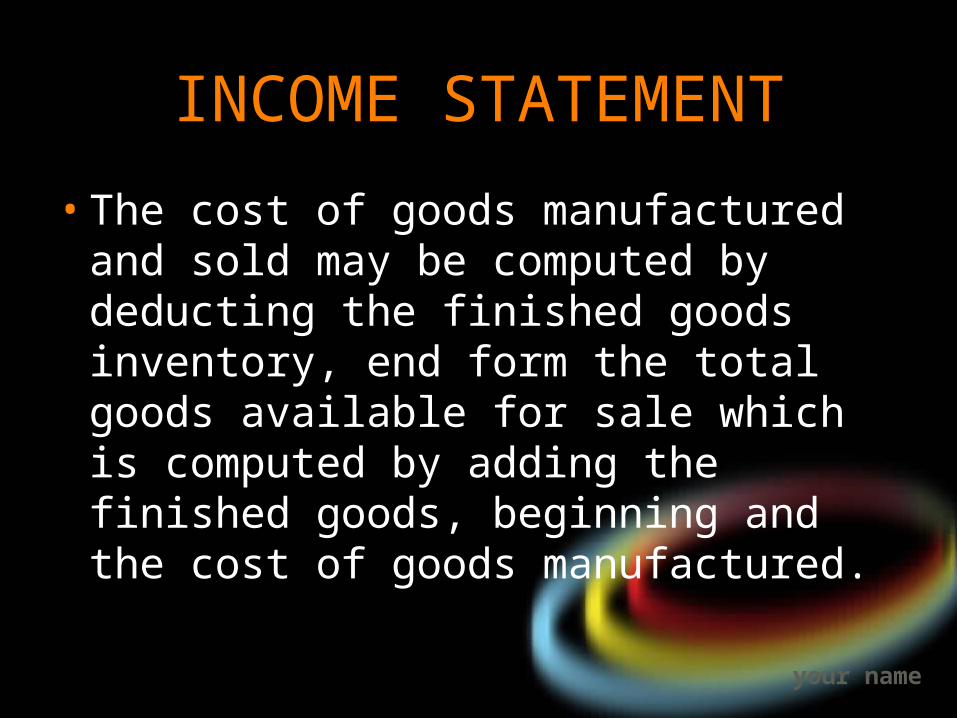

• The cost of goods manufactured and sold may be computed by deducting the finished goods inventory, end form the total goods available for sale which is computed by adding the finished goods, beginning and the cost of goods manufactured.

INCOME STATEMENT

your name

• Finished Goods, Beginning

• +Cost of goods Manufactured

-------------------------------------------------------

= Total Goods Available for Sale

- Finished Goods, end

-------------------------------------------------------

Cost of Goods Manufactured and Sold

INCOME STATEMENT

your name

2. Operating Expenses – represents the marketing, general and administrative expenses.

e.g. advertising, salaries and wages

3. Other Expenses – includes interest expense

INCOME STATEMENT

your name

Other Income - refers to non-operating income

Net Profit or Net Loss – the excess of total revenues over total expenses. If total expenses exceed total revenues, a net loss is reported.

INCOME STATEMENT

your name

INCOME STATEMENT

your name

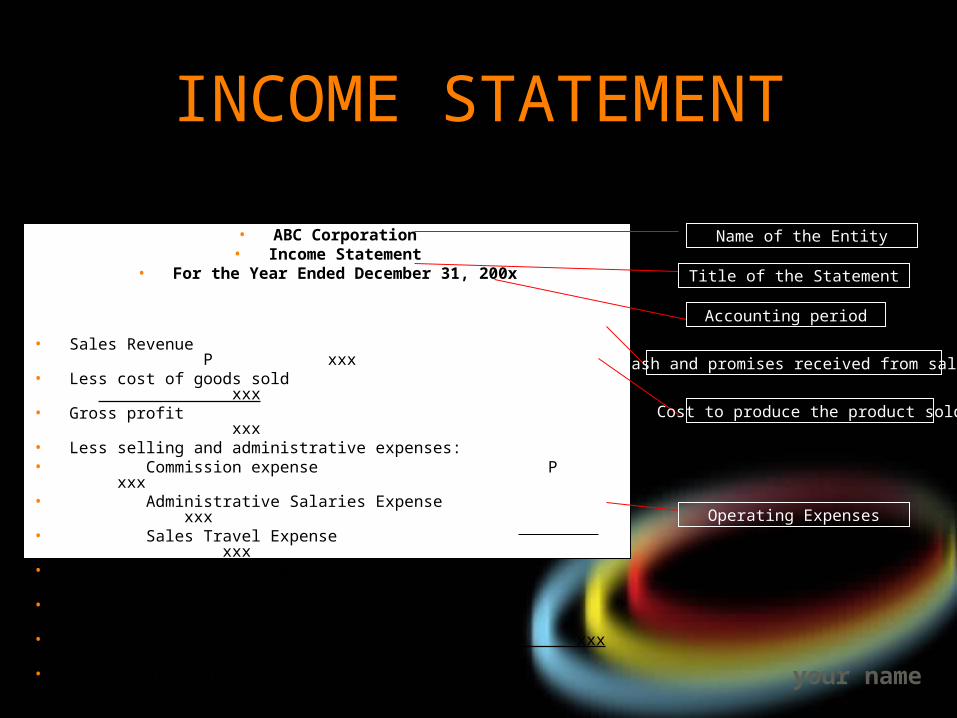

• ABC Corporation• Income Statement

• For the Year Ended December 31, 200x

• Sales Revenue P xxx

• Less cost of goods sold xxx• Gross profit xxx • Less selling and administrative expenses: • Commission expense P xxx• Administrative Salaries Expense xxx• Sales Travel Expense xxx• Advertising Expense xxx• Depreciation Expense xxx• Insurance Expense xxx xxx• Net Operating Income P xxx

Name of the Entity

Title of the Statement

Accounting period

Cash and promises received from sale

Cost to produce the product sold

Operating Expenses

INCOME STATEMENT

your name

BUDGET

• BUDGET – estimate of income and expenditures for a future period. It completes the financial picture by referring to the future

• The budget is contrasted with the income statement ( a summary of the performance of the firm) and balance sheet (the financial condition of the firm)

your name

BUDGET

• Essential in the planning and control of the financial affairs of the business.

• Large corporations emphasizes in the annual budget broken down into monthly and weekly periods.

your name

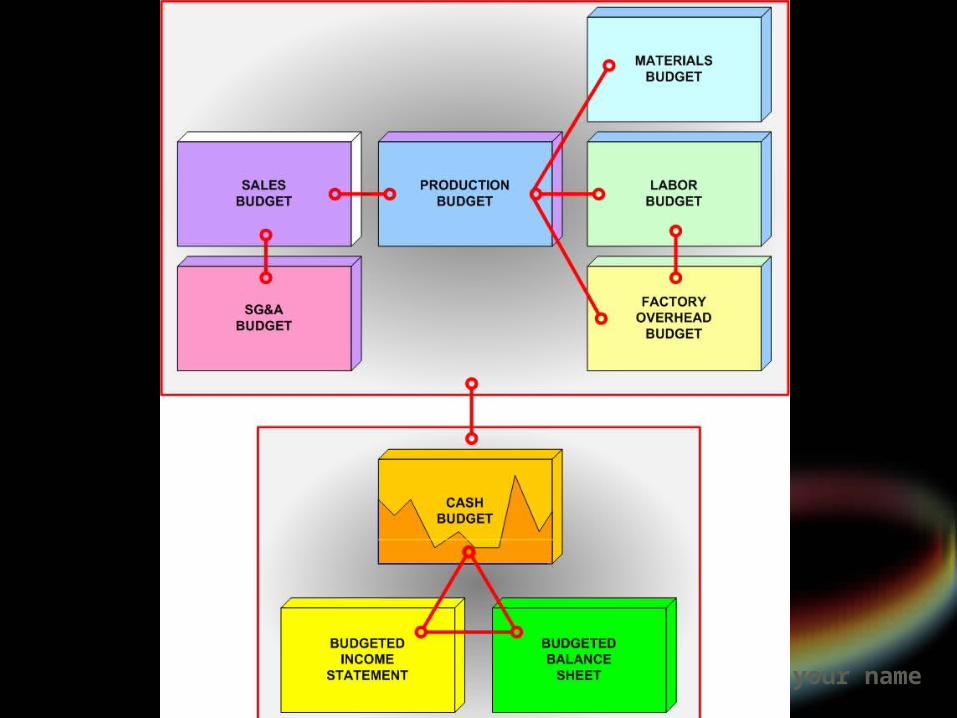

BUDGET

Budget includes:

1.Estimated sales and income

2.Estimates of expenditures in purchasing, administration, production, distribution and research

3.Detailed budgets of cash flow and capital expenditures

your name

BUDGETSales Budget – starting point of company budgets.

- estimated sales in units and peso for each major subdivision of sales.

Materials and Purchase Budget- estimate of the materials required by the firm, specified in quantities, costs, timing of purchase, required delivery dates and other purchase requirements

your name

BUDGETProduction Budget – estimate of the quantity

of products to be produced in accordance with the sales budget

- includes monthly breakdown of quantities to be produced for each product depending upon the firm’s seasonal sales index.

your name

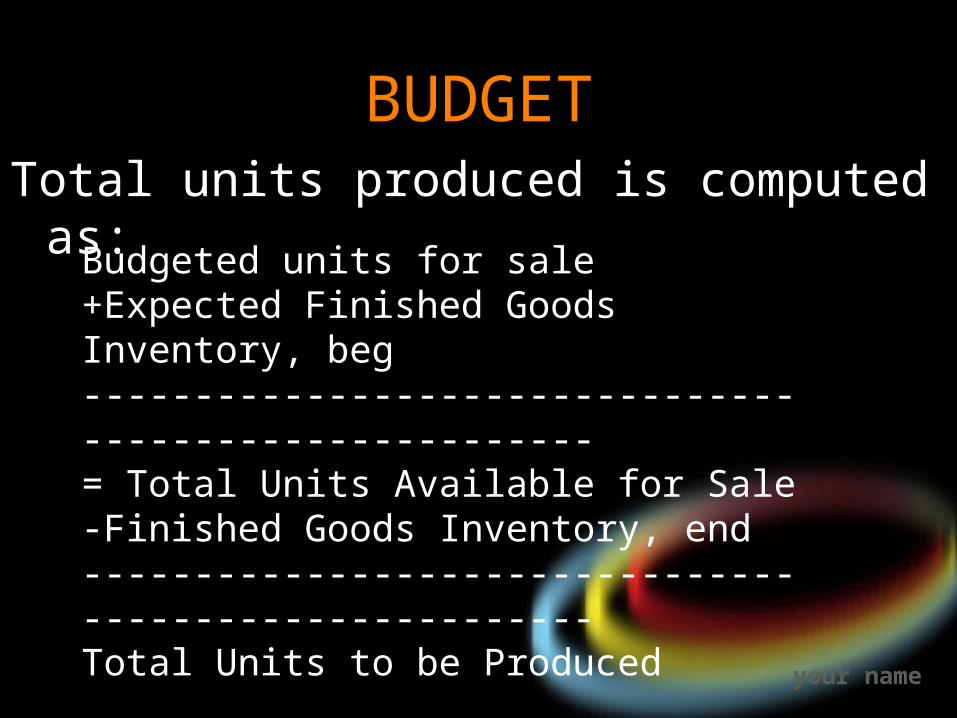

BUDGETTotal units produced is computed as:

Budgeted units for sale+Expected Finished Goods Inventory, beg-------------------------------------------------------= Total Units Available for Sale-Finished Goods Inventory, end-------------------------------------------------------Total Units to be Produced

your name

your name

SIGNIFICANCE OF FINANCIAL STATEMENTS AND BUDGET

• Interested Groups

1.Owners

2.Management

3.Creditors

4.Government

5.Prospective investors

your name

Owners – use the financial statements for anticipated financial benefits

- basis for decision making to continue or discontinue ownership

SIGNIFICANCE OF FINANCIAL STATEMENTS AND BUDGET

your name

Management – use the financial statements for planning and control to:

1.Anticipate asset needs;

2.Plan for necessary financing

3.Establish standards by which to test current operating performance

SIGNIFICANCE OF FINANCIAL STATEMENTS AND BUDGET

your name

Creditors – to see the credit worthiness of the firm.

Government – use financial statements for tax and regulatory purposes.

Investors – to see the financial position and performance of the firm, whether to continue as investors or not.

SIGNIFICANCE OF FINANCIAL STATEMENTS AND BUDGET

your name

Other Users:

Customers – to see how stable the company.

Employees – basis for considering long term employment with the firm.

SIGNIFICANCE OF FINANCIAL STATEMENTS AND BUDGET

your name

ANNUAL REPORT

Yearly report to stockholders, members and the government.

Includes:

1.Balance sheet

2.Income statement

3.Auditor’s report

4.Chairman’s report

your name

your name