Young People's Consumer Confidence Index - Developed and Growth Markets

35

Young People’s Consumer Confidence - Developed and Growth markets October 2012

-

Upload

on-device-research -

Category

News & Politics

-

view

3.107 -

download

1

Transcript of Young People's Consumer Confidence Index - Developed and Growth Markets

Young People’s Consumer Confidence - Developed and Growth markets

October 2012

Summary

• Overall young consumers in growth markets are at least twice as confident, compared to those in developed markets. Confidence is being driven in growth markets by a very positive outlook for the economy and future job prospects.

• Young consumers in growth markets haven’t been jaded by a hard hitting recession that those in developed markets have, and there is a serious risk of young people in developing nations becoming the ‘lost generation’.

• Growth markets optimisms towards their economy, transfers into views on buying large purchases and provides a fantastic opportunity for UK and US companies looking to export into these markets.

• However when exporting to growth markets, companies must understand the different business practices, regulations, infrastructure, cultural differences and population makeup - in Nigeria 60% of the population is under 25, which impacts product demand.

• What is clear, is that the mobile device is very important in the lives of young consumers all over the world, which will be reflected in not only how we research these consumers, but also how marketers communicate and transact with them.

Contact us at [email protected] to add in your own survey questions

Young Consumer Confidence Index (YPCC)

By collecting data from key markets we help businesses understand what young people think about their current and future economic prospects. By using a select group of growth and developed markets, it allows for a comparison of youth confidence in different economies. It also gives businesses looking to develop in growth markets, a good indication of the current and future health of the economy. The YPPC will be repeated regularly so trends can be tracked over time. Sign up to our newsletter on our website to receive future updates.

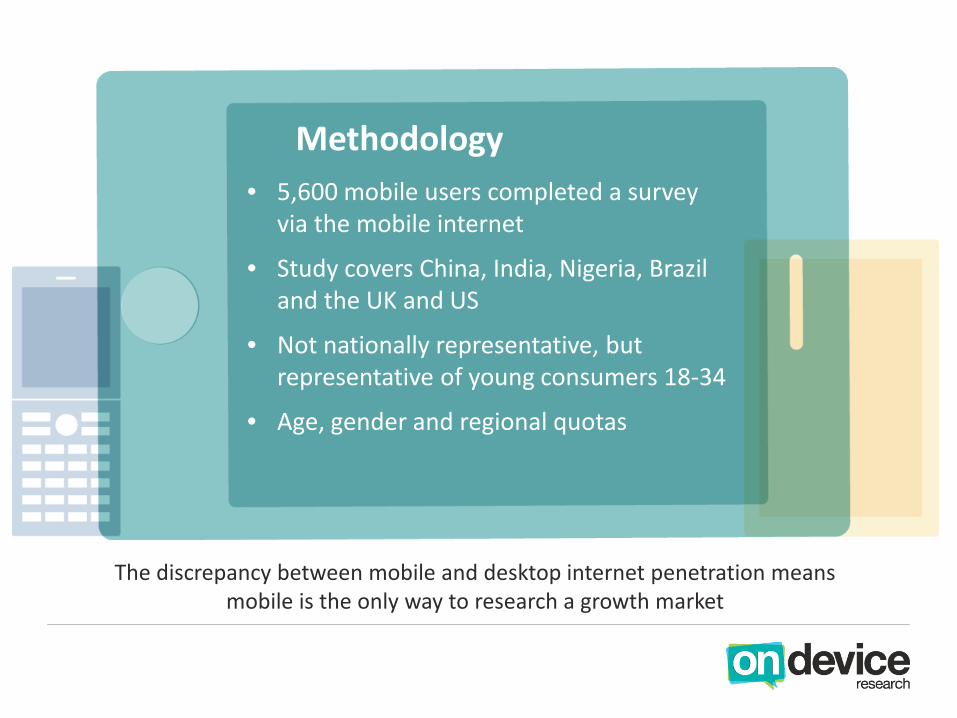

Methodology • 5,600 mobile users completed a survey

via the mobile internet

• Study covers China, India, Nigeria, Brazil and the UK and US

• Not nationally representative, but representative of young consumers 18-34

• Age, gender and regional quotas

The discrepancy between mobile and desktop internet penetration means mobile is the only way to research a growth market

Index Questions The index score is calculated using the mean results of six key questions, asking consumers: 1. How do you expect your employment situation/prospects to change

over the next 12 months? 2. How do you expect the general economic situation in this country to

change over the next 12 months? 3. How are you feeling about your current employment

situation/prospects? 4. In view of the economy, is now the right time to buy big purchases? 5. How are you feeling about your current personal/household

financial situation? 6. Overall how are you feeling about the economy?

Index

• Overview • Developed vs Growth Markets comparison • Highlight on US vs China • Demographics • Importance of mobile

Developed vs Growth Markets

Overall young consumers in growth markets are at least twice as confident, compared to those in developed markets. Young Chinese consumers have the overall highest confidence level

39 38 37 32

16 10

05

1015202530354045

China Brazil Nigeria India US UK

Inde

x

YPCC Index

Source: On Device Research YCCI Brazil, China, India, Nigeria, US,UK n = 5600 August 2012

A reason for China’s youth confidence? They’re experiencing stable GDP growth, compared to the UK and US where growth is minimal

-6

-1

4

9

14

China India Nigeria Brazil US UK

2007 2008 2009 2010 2011

Source: The World Bank

GDP growth (annual %)

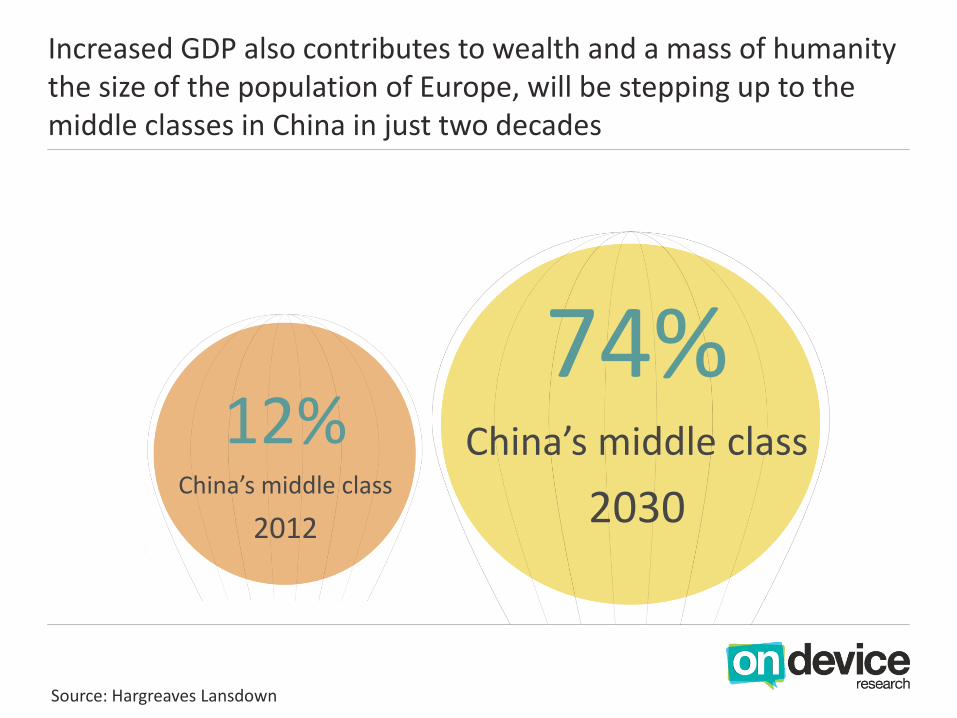

Increased GDP also contributes to wealth and a mass of humanity the size of the population of Europe, will be stepping up to the middle classes in China in just two decades

12% China’s middle class

2012

74% China’s middle class

2030

Source: Hargreaves Lansdown

So what’s driving this confidence?

Young people in the UK and US are fairly positive about their current financial situation, but they are not so positive when it comes to their current employment prospects

0 20 40 60

How are you feeling about yourcurrent employmentsituation/prospects?

How are you feeling about yourcurrent personal/household

financial situation?

Brazil Nigeria UK India China US

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

In July 2012, 1.02 million young people in the UK aged 16-24 were unemployed, +37,000 on the same quarter in 2011. There is a danger that the UK’s youth will become a ‘lost generation’

Source: UK Government Statistics July 2012

Britons are 15x less confident than growth markets (4 vs. 57) about how the general economic situation will change in their own country in next year, and 3x less confident about their future employment prospects

0 10 20 30 40 50 60 70 80

How do you expect your employmentsituation/prospects to change over the

next 12 months?

How do you expect the general economicsituation in this country to change over

the next 12 months?

UK US India China Nigeria Brazil

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

Young people in Brazil are very optimistic about their future – in fact they’re 6x more confident about their future than young people in the UK and US

Why?

Two potential reasons

These events are going to have a major long term impact on improved infrastructure, tourism, creating jobs and bringing business to Brazil

-10 -5 0 5 10 15 20 25 30 35

In view of the general economicsituation, is now the right time for peopleto buy big purchases e.g electrical goods?

Overall how are you feeling about theeconomy?

UK US Nigeria Brazil China India

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

Differences in confidence is reflected in purchasing intent - growth markets index 32 points higher vs UK in believing now is the right time to make big purchases, a positive for companies looking to move into these markets.

Summary of the major driver of confidence

39 37 38 10 16 32

Optimism for the future both for the economy and job prospects

Propensity to purchase big items

In comparison these are areas developed nations are least confident about

Most confident about their current financial situation

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

US vs China

Young Chinese consumers are 2.5x more confident than young American consumers

39 16 Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

YPCC Index

The Chinese are over five times more confident than young Americans about the future economic situation of their country, and three times more confident about their employment prospects

0

10

20

30

40

50

60

70

Employment situation to change innext year

Economic situation to change in nextyear

China US

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

The difference in economic confidence between young American consumers and China is reflected in purchase intent - China index 24 points higher than US in believing now is the time to be making big purchases

-5

0

5

10

15

20

25

30

Feeling about the economy Right time to buy big purchases

China US

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

Differences in gender and age

Generally young females tend to have a lower level of overall confidence

05

1015202530354045

Nigeria Brazil China India US UK

Male Female

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

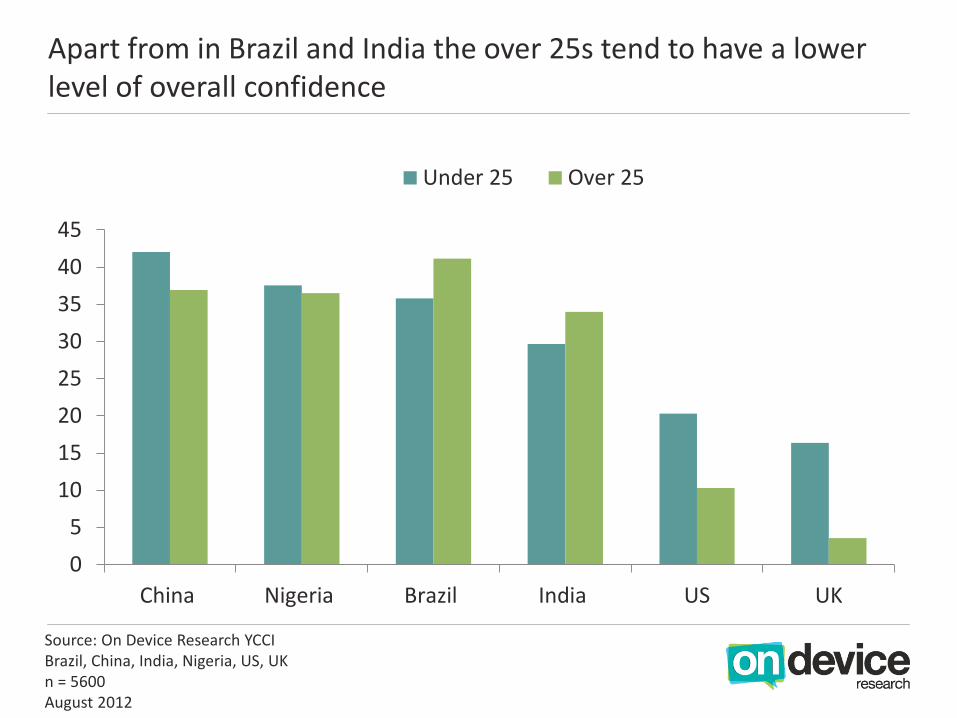

Apart from in Brazil and India the over 25s tend to have a lower level of overall confidence

05

1015202530354045

China Nigeria Brazil India US UK

Under 25 Over 25

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

Importance of mobile

One similarity between all markets however is the importance of their mobile, and this device is certain to have a big impact on young consumers lives across the developing and developed nations

96% 89% 92% 80%

Mobile phone is very important/important to them

Source: On Device Research YCCI Brazil, China, India, Nigeria, US, UK n = 5600 August 2012

73% 80%

Summary

• Overall young consumers in growth markets are at least twice as confident, compared to those in developed markets. Confidence is being driven in growth markets by a very positive outlook for the economy and future job prospects.

• Young consumers in growth markets haven’t been jaded by a hard hitting recession that those in developed markets have, and there is a serious risk of young people in developing nations becoming the ‘lost generation’.

• Growth markets optimisms towards their economy, transfers into views on buying large purchases and provides a fantastic opportunity for UK and US companies looking to export into these markets.

• However when exporting to growth markets, companies must understand the different business practices, regulations, infrastructure, cultural differences and population makeup - in Nigeria 60% of the population is under 25, which impacts product demand.

• What is clear, is that the mobile device is very important in the lives of young consumers all over the world, which will be reflected in not only how we research these consumers, but also how marketers communicate and transact with them.

Contact us at [email protected] to add in your own survey questions

Sarah Quinn [email protected] +44 (0)207 278 6627 www.ondeviceresearch.com

@ondevice

Follow us on Slideshare

Sign up to our newsletter to receive the next wave of YPCC data & analysis

On Device Research Services

On Device Omnibus

• Contact hard to reach people in emerging markets quickly and cost effectively • Survey up to 1,000 respondents per month in Brazil, India, China and Nigeria, UK and US • Robust, sample of 16-34 year old consumers • Online interface for data analysis

1-3 Countries 4-6 Countries

Per Complete

(£) Total Cost for

1 Country Discount

Per Complete (£)

Total Cost for 5 Countries

1-2 Questions £0.50 £500 20% £0.40 £2000

3-5 Questions £1.00 £1000 20% £0.80 £4000

6-10 Questions £1.50 £1500 20% £1.20 £6000

10-15 Questions £2.00 £2000 20% £1.60 £8000

On Device Research

On Device Research uses the mobile

Internet to gain access to consumer opinions at any time, place or

country

So far we’ve surveyed over 1.4 million consumers across 53 countries

We make mobile research work…

Some of our clients