Yondo Belle Serge Hermann EFFECTS OF MERGERS ...jultika.oulu.fi/files/nbnfioulu-201606072440.pdf ·...

57

OULU BUSINESS SCHOOL Yondo Belle Serge Hermann EFFECTS OF MERGERS & ACQUISITIONS ON FINANCIAL PERFORMANCE OF USA ACQUIROR BANKS Master’s Thesis Department of Finance September 2015

Transcript of Yondo Belle Serge Hermann EFFECTS OF MERGERS ...jultika.oulu.fi/files/nbnfioulu-201606072440.pdf ·...

OULU BUSINESS SCHOOL

Yondo Belle Serge Hermann

EFFECTS OF MERGERS & ACQUISITIONS ON FINANCIAL PERFORMANCE OF USA

ACQUIROR BANKS

Master’s Thesis

Department of Finance

September 2015

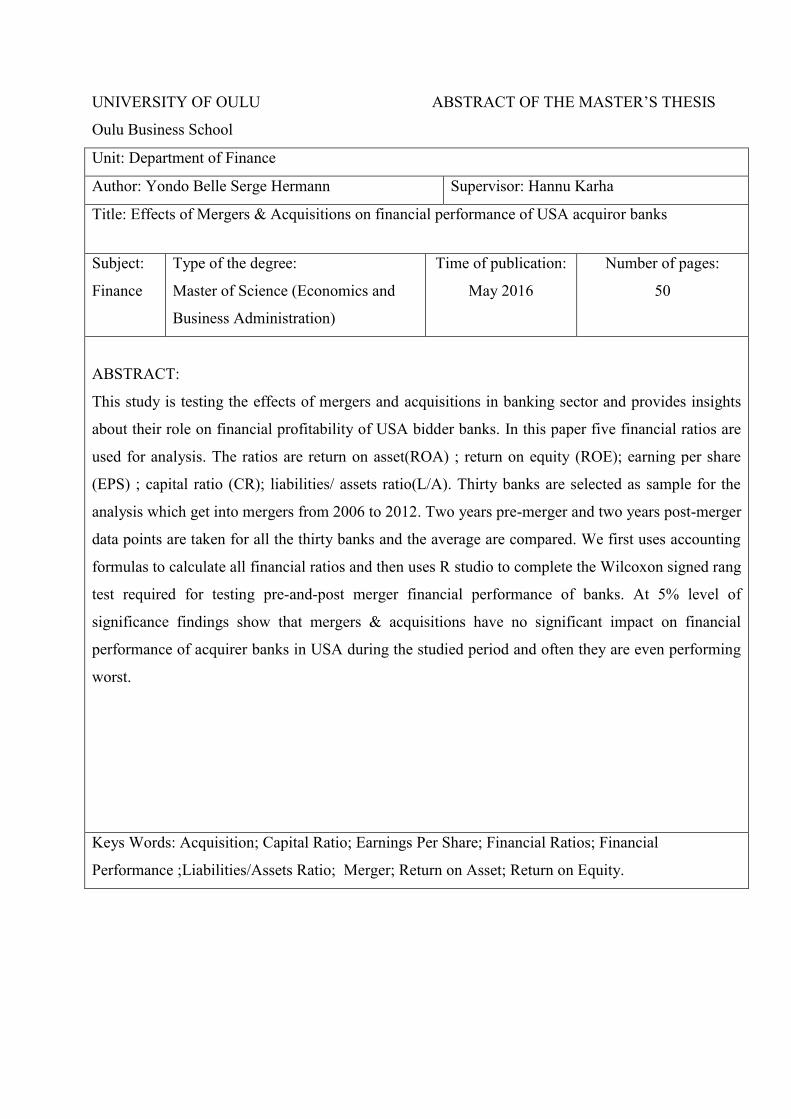

UNIVERSITY OF OULU ABSTRACT OF THE MASTER’S THESIS

Oulu Business School

Unit: Department of Finance

Author: Yondo Belle Serge Hermann Supervisor: Hannu Karha

Title: Effects of Mergers & Acquisitions on financial performance of USA acquiror banks

Subject:

Finance

Type of the degree:

Master of Science (Economics and

Business Administration)

Time of publication:

May 2016

Number of pages:

50

ABSTRACT:

This study is testing the effects of mergers and acquisitions in banking sector and provides insights

about their role on financial profitability of USA bidder banks. In this paper five financial ratios are

used for analysis. The ratios are return on asset(ROA) ; return on equity (ROE); earning per share

(EPS) ; capital ratio (CR); liabilities/ assets ratio(L/A). Thirty banks are selected as sample for the

analysis which get into mergers from 2006 to 2012. Two years pre-merger and two years post-merger

data points are taken for all the thirty banks and the average are compared. We first uses accounting

formulas to calculate all financial ratios and then uses R studio to complete the Wilcoxon signed rang

test required for testing pre-and-post merger financial performance of banks. At 5% level of

significance findings show that mergers & acquisitions have no significant impact on financial

performance of acquirer banks in USA during the studied period and often they are even performing

worst.

Keys Words: Acquisition; Capital Ratio; Earnings Per Share; Financial Ratios; Financial

Performance ;Liabilities/Assets Ratio; Merger; Return on Asset; Return on Equity.

ACKNOWLEDGEMENTS

Writing this thesis has been a personal learning process for me. However this process

was made possible with assistance of other people who in one way or the other, were

involved in and made writing this possible.

First and foremost, I would like to give all thanks and glory to the almighty God. From

the deepest part of my heart I want to thank my lovely daughter Andrée Yondo

Kameni, and words cannot express my sincere gratitude for the joy, motivation and

willingness you provide me every single day.

I’m forever indebted to my parents Marcel Yondo and Engele Julienne for the

incessant and unconditional, emotional, moral, physical, spiritual support and

encouragements. With all profound love and gratitude I will like to thank all my

brothers Raul Yondo, Kolko Yondo, Geraldin Yondo and Marcel Jordy Yondo.

Special thanks goes to my grand mum Charlotte Kingue Belle, my uncles & Aunt

Justin Bejedi, Albert Behle, and David Din Belle, Alice Mbah. I’m sincerely appreciate

and thankful to my adoptive families Anicet Samba and Celestin Fenkoun.

I’m particularly grateful to my supervisor Hannu Karha for his advice and assistance

and all my friends for the unconditional support.

I will finally end up by expanding my love and gratitude to my late sister Christelle

Yondo and late partner Norbert Djeufo “Woungail”, may your souls rest in peace.

Oulu, Finland. April 2016

Yondo Belle Serge

CONTENTS

Acknowledgements

1 Introduction...…………………………………………………………………......8

2 Theoretical Frame work………………………………………………………....11

2.1 Mergers and Acquisitions…………………………………………………...11

2.1.1 Merger and Acquisition Motives……………………………………....12

2.1.2 Merger and Acquisition Strategies...……………………………….…..13

2.1.3 Merger and Acquisition Process…………………………………….....15

2.1.4 Success Factors in Mergers and Acquisitions……..…………….….…16

2.1.5 Merger and Acquisition costs…………………..………………………17

2.1.6 Reasons for Merger and Acquisition failures…..………………………18

2.2 Bank Performance…………………………………………………….…......21

2.2.1 Traditional Measure of Performance…………………….…………......21

2.2.2 Economic Measure of Performance..................................................…...22

2.2.3 Market Based Measures of Performance……….....................................23

2.3 Merger and Acquisition in US Banking Sector…...………………………23

3 Research Problem and Previous Related literature……...……………………26

4 Data and Methods………………………………………………………….…...29

5 Results and Discussion..................................................................................…...36

5.1 Sample Test of Normality……………..…………………………………….36

5.2 Variables testing......................................................................................…...40

6 Conclusion……………………………………………………………………......47

References………………………………………………………………………......48

Appendices………………………………………………………………………….53

FIGURES

Figure 1. Change in capital ratio ………………………………………………….37

Figure 2. Change in Total Liabilities/ Total assets……………………………….38

Figure 3. Change in Earning Per Share…………………………………………..38

Figure 4. Change in Return on Equity…………………………………………....39

Figure 5. Change in Return on Assets…………………………………………….39

Figure 6. Capital ratio variations………………………………………………….41

Figure 7. Return on equity variations…………………………………………….42

Figure 8. Return on asset variations……………………………………………...43

Figure 9. Total Liabilities/Total Assets variations……………………………....44

Figure 10. Earnings per share variations………………………………………....45

TABLES

Table 1. Merger and Acquisition motives………………………………………..13

Table 2. Merger and Acquisition process………………………………………...16

Table 3. Sample of selected banks………………………………………………...30

Table 4. Financial ratio formulas…………………………………………………34

Table 5. Shapiro-Wilk test results…………………………………………..…….36

Table 6. Wilcoxon test results………………………………………………..……40

8

1 INTRODUCTION

Mergers and acquisitions have become the driving force of the world economy and

have played a significant role in the strategy of many banks in the last decades.

Banking reforms since 1980s have been a continuous process around the world but it

is more intensified in recent time due to globalization which is precipitated by the trend

of integration on the world market and economies. The main reason that can explain

mergers and acquisitions in banking sector is the risk management. Bank in every

country are committed to make a proper risk analysis in other to balance the deposit

and credit portfolios. Mergers and Acquisitions in this case can diversify those risks to

a significant extend. A significant increase in market competition, innovation of new

financial products and consolidation of national (regional) financial systems are other

reasons explaining why banks are opting for mergers and acquisitions around the

world. Mergers and Acquisitions can be proved really useful against market

competition as they have the capability to generate economy of scale and this economy

of scale can help banks in lowering their costs and provide a competitive edge and

enhance their revenues. The USA banking sector has experienced this rapid process of

mergers & acquisitions during 1980s.Beside deregulation, technological and financial

motivation, the imperative of efficiency, value creation and market power boosted the

process. The structure of US banking industry has changed considerably with over

10.000 mergers involving more than $7 trillion in acquired assets taking place. There

were 19069 banks and thrifts operating in the US in 1980 and 7,011 in 2010, a decline

of over 60%. Houston et AL. (2001) found that the post-merger performance of bank

has been improved in US. In the same range Lin et AL. (2006) showed that in US

banking sector the firm’s performance increased after mergers and acquisitions

regarding their productivity, profitability and shareholder’s value. Some studies,

however have found that mergers and acquisitions are far from having proved their

economic effectiveness and, there is no increase in the financial performance of

organization after mergers and acquisitions. (Robert M. Adams, 2012.)

Financial performance of banks under mergers and acquisitions can be measured

through financial ratios using accounting and financial data. The study empirically

assesses the effect of mergers and acquisitions on financial performance of USA bidder

banks by comparing pre-and-post financial performance using their accounting

9

indicators and financial ratios. The paper’s goal is to prove that mergers and

acquisitions if used in appropriate way are financially profitable for bidder banks. The

first steps focus on selecting and calculating financial indicators of each bidder bank

for pre-and-post merger and acquisition period. After calculating those ratios a mean

average of each ratio of each bidder bank is deducted and analyzed.

Motivated by the ambiguity in the profitability of mergers and acquisitions and

inspired by papers such as Brighman and Ehrhardt (2005), we are seeking to examine

the profitability of the merged banks base on their financial performance and by using

a statistical approach.

The thesis is relatively similar with previous research. In comparison to previous

works the differences lead on the size of the studied sample and the financial ratios

used. In term of evaluation of the method, the normality of the distribution as well as

the Wilcoxon Test (Shapiro Wild Test) has been examined in the same process as

Gjirja (2001) .Furthermore, a graphical approach to evaluate and compare performance

between pre-and-post merger and acquisition is introduced.

The data is chosen to be annual from SCD Platinium in the period 2004 to 2014. We

selected 30 banks to banks mergers and acquisitions from the basket of all mergers and

acquisitions that occurred in USA from 2004 to 2014. The same as Gjirja (2001) we

focus on annual financial performance for each chosen bidder bank.

The methodology used is suitable for the procedure of estimation of financial ratios.

The method is straightforward and clear. The point that should be highlighted is that

we were unable to gather all information necessary to calculate all existing financial

ratios.

The results showed no changes in financial performance leading to no improvements

in financial efficiency. The purpose of merger and acquisition in improving

performance is not achieved in the studied banks.

We started with the literature review of related subjects that support our statements.

The second chapter provides an overview of mergers and acquisitions, merger and

10

acquisition definitions, reasons, motives, success factors and reasons of failure. The

chapter also highlight the concept financial performance, financial performance

definition and measures and a general overview of mergers and acquisitions in banking

industry in USA. The chapter 3 and 4 defines the research problem, provides an

overview of previous literature related to the research, data gathering, methodology

and a comprehensive discussion on profitability of mergers and acquisitions. The

chapter 5 and 6 presents empirical results and conclusion of the research.

11

2 THEORETICAL FRAMEWORK

This chapter reviews existing literature in two folds. The first part covers mergers and

acquisitions concepts, motives, process, strategies and costs. The second part reviews

bank performance and mergers and acquisitions in domestic USA banking sector.

2.1 Mergers and acquisitions

Mergers and Acquisitions occurs when two or more organizations join together all or

part of their operations. The difference between merger and acquisition relate mainly

on the relative size of the individual companies in the business combination, on

ownership of the combined business and on management control of the combined

business. (Coyle and Brian, 2000.)

Mergers can be defined in a broad as well as a narrow term. In broadest a merger refers

to any takeover of one company by another, when the businesses of each company are

brought as one. A more narrow definition is the coming together of two companies of

roughly equal size, pooling their resources into a single business. The stockholders or

owners of both pre-merger companies have a share in the ownership of the merged

business and the top management of both companies continues to hold senior

management position after the merger (Coyle and Brian, 2000).

The narrow definition point out couple of conditions for the existence of a merger:

Neither company is portrayed as the acquirer or the acquired

Both parties participate in establishing the management structure of the combined

business

Both companies are sufficiently similar in size that one does not dominate the other

when combined

All or most of the consideration involves a share swap rather than a cash payment

An acquisition in contrast, is the takeover of the ownership and management control

of one company by another. The control is the key test of distinction between a merger

and an acquisition. Acquisition, or take over, occurs when one company acquires from

12

another company either a controlling interest in company stock or a business operation

and its assets. The purchase consideration could take the form of stocks in the

acquiring company. Stockholders in company that is taken over exchange their stocks

for stocks in the acquiring company, thus becoming stockholders in the enlarged

company post-acquisition. However, often, the purchase consideration for an

acquisition is paid largely or entirely in cash. The process of acquisition, buying

company or buying its assets could be a matter for negotiation .By purchasing a

company, the buyer acquires its liabilities as well as its assets; the buyer also acquire

any tax losses that the purchased company might have accumulated to set off against

future profits. Acquisitions can be either full or partial. In a full acquisition the acquirer

buy all the stock capital of the purchased company. In a partial acquisition, the acquirer

obtains a controlling interest, normally over 50% of the equity stocks, but less than

100 %.( Coyle and Bryan, 2000.)

2.1.1 Merger and Acquisition Motives

The main reason for the growing number of cross-border takeovers, mergers and joint

ventures is the desire to compete or survive in new world. Motives may vary from deal

to deal. It can be the rationales of adoptive or offensive, versus proactive or offensive

(Gugler &Yurtoglu, 2008).

Over all there are three commonly accepted categories of mergers and acquisitions

motives. The first group is economic motives, which include profit maximization, cost

reduction, spreading risks, achieving economies of scale, taking advantages of market

valuation differentials, taking a defensive position, and react to market failures

(Brouthers et Al., 1998).The second group of motives occur from personal vision of

manager in merger and acquisition in term of increased prestige or payment through

increased sales or profitability and firm growth (Brouthers et Al., 1998; Schweizer,

2005). The third group involves strategic motives. In this case mergers and acquisitions

activities aims to achieve synergy, expansion of global market, pursuing market power,

acquiring new resources such as managerial skills and raw materials, increasing

competitiveness. (Brouthers et Al., 1998.)

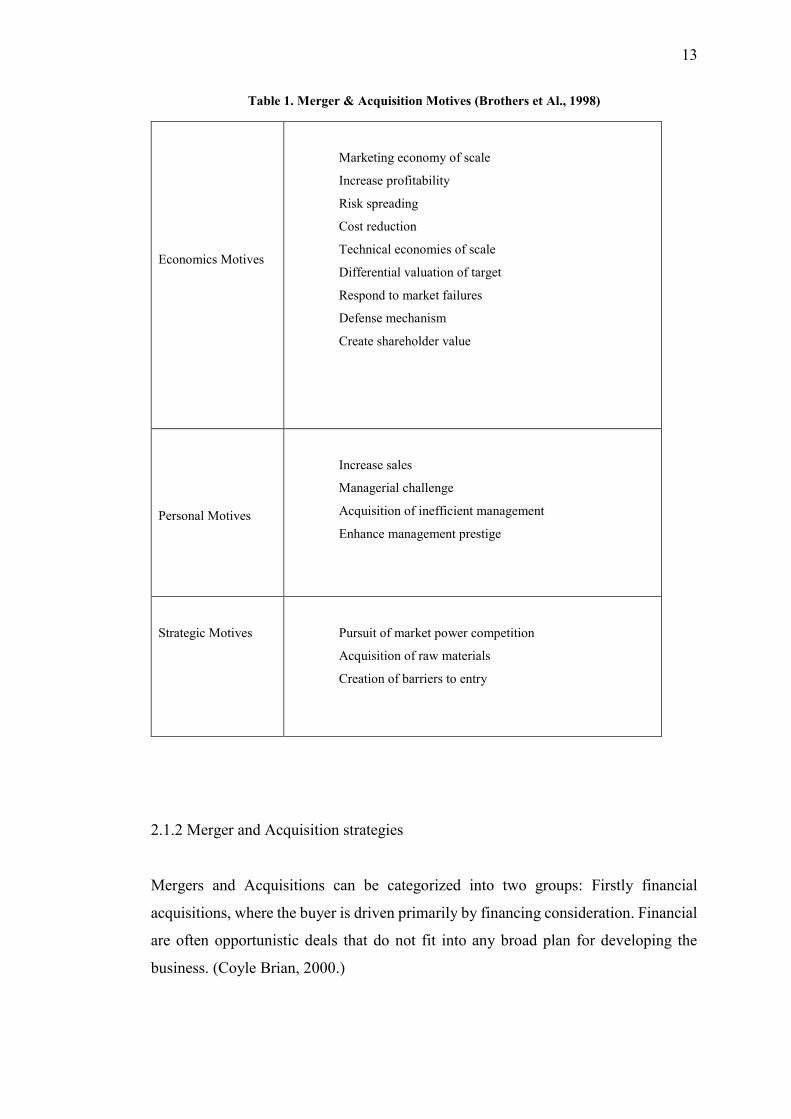

13

Table 1. Merger & Acquisition Motives (Brothers et Al., 1998)

Economics Motives

Marketing economy of scale

Increase profitability

Risk spreading

Cost reduction

Technical economies of scale

Differential valuation of target

Respond to market failures

Defense mechanism

Create shareholder value

Personal Motives

Increase sales

Managerial challenge

Acquisition of inefficient management

Enhance management prestige

Strategic Motives Pursuit of market power competition

Acquisition of raw materials

Creation of barriers to entry

2.1.2 Merger and Acquisition strategies

Mergers and Acquisitions can be categorized into two groups: Firstly financial

acquisitions, where the buyer is driven primarily by financing consideration. Financial

are often opportunistic deals that do not fit into any broad plan for developing the

business. (Coyle Brian, 2000.)

14

Secondly strategic merger and acquisition where the buyer is driven primarily by

commercial consideration. Acquisition based growth and organic growth should be

twin platform of a large company’s strategic approach to developing its business.

Additionally, companies needing to concentrate their resources on core activities in

growing industries should consider a strategy for divestment of non-core activities.

(Coyle Brian, 2000.)

A) Strategic approach requires a set of elements

- Identifying corporate objectives.

- Developing strategies to achieve objectives and deciding between acquisitions and

organic development as the more appropriate option in each case.

-Selecting candidate for acquisition.

- Deciding the value of the acquisition and making a bid.

-Making the acquisition.

Acquisitions can be the best method of achieving strategic aims. The choice between

acquisition and organic growth for new product/market development depends on a

number of key factors such as timescale, cost, business risks, barriers to entry, stage

of market development. (Coyle Brian, 2000.)

B) Synergy

In mergers and takeover, synergy is the additional benefit that can be derived from

combining the resources of the bidding and target companies. When synergy exists,

the total returns from the combined organization exceed the total returns of the two

companies before the merger or acquisition. However, synergy does not always occur

in a merger or acquisition, and all too often, hoped-for synergies fail to materialize.

(Coyle Brian, 2000.)

C) Aggressive / defensive strategies

Mergers and Acquisitions can be the outcome of either an aggressive or a defensive

strategy. When using aggressive strategy company seek to improve its market position

.Mergers and Acquisitions intended to create a bigger company with larger market for

its products and with the resources to produce on a bigger scale and more cheaply

through economies of scale target companies for takeover bids are commonly existing

15

competitors, or similar companies operating in different market. Mergers and

Acquisitions are common in industries and markets that are in the process of becoming

more global. Major suppliers to growing markets need to expand in order to remain

competitive (Coyle Brian, 2000).

Defensive strategy for mergers and acquisitions are made in order to survive in a

changing industry. A major acquisition by one company prompts a similar response

from others. Recently, the number of major competitors in many industries has reduced

because of mergers, acquisitions and strategic alliances. At the same time, their

markets have become international. (Coyle Brian, 2000.)

D) Growth Strategy

Mergers and Acquisitions strategy is based on a growth objective. An acquisition

strategy for growth can seek to develop products and markets in any of four ways:

- By market penetration including cross-border acquisitions, including developing new

and larger markets for a company’s existing products.

- Horizontal diversification: expands into market for products that it has made before,

but which are similar to its existing products range.

- Vertical integration: combination of a company’s business with the business of a

supplier or a customer.

- Conglomerate diversification: group of companies that operates in a widely diverse

industry. (Coyle Brian, 2000).

2.1.3 Merger and Acquisition process

Mergers and Acquisitions deal is generally conducted through three phases: planning,

implementation and integration. (Picot, 2002.)

Massoudi (2006) propose a deal process model which includes five steps:

(1) Definition of vision and strategy for growth.

(2) Target selection.

(3) Deal discussion.

(4) Due diligence and integration planning.

(5) Integration of new entity and synergy realization.

The figure below provides a better picture of the full process:

16

Table 2: Merger and Acquisition process (www.safaribooksonline.com)

2.1.4 Success factors in Merger and Acquisition

Several factors have been identified by different mergers and acquisitions disciplines

as important impact on mergers and acquisitions performance. Cording, Christman,

and Bourgeois (2002) review eight schools of thoughts emerging from mergers and

acquisitions literature regarding the influential issues that contributed strategic

acquisition success in terms of financial performance. These schools include

Strategy Phase

(Buyer)

•Refine business plan

•Organize Merger & Acquisition team

•Establish Merger & Acquisition plan

•Determine target criteria

• Identify candidates

•Analyze targets

•Rank targets

Negociation and Investigation Phase

(Buyer)

•Finalize negotiating strategyContact Targets•Negociate preliminary

transaction structure•Write letter for intent•Perform due deligence

Finalization and Integration phase

(Buyer)

• Integration phase

•Establish final transaction structure

•Secure approval

•Finalize financing

•Complete transaction

• Integrate entities

Strategy Phase

(seller)

•Refine Business Plan

•Analyze own Bank

•Establish Franchise value

•Enhance value

•Develop selling document

• Identify potential buyers

Negociation and Investigation Phase(Seller)

•Finalize negotiating strategies

•Assess offer

•Review tax consequences

•Assist with due deligence

Finalization and Integration Phase(Seller)

•Review final agreement

•Complete Transaction

17

overpayment, agency problem, top management complementarities, experience,

employee distress, and conflicting culture.

Gomes et Al. (2012) point out success factors through extensive literature review.

Mergers and Acquisitions success factors are presented according to phases (pre-

merger phase/post-merger phase).

Firstly during the pre- merger phase success factors depend on:

- Choice and evaluation of the strategic partner.

- Paying the correct prize

- Size mismatches and organization

- Overall strategy and accumulated experience on merger and acquisition

- Communication before the merger

- Future compensation policy

The second phase is the post-merger encompasses:

- Integration strategies

- Post-acquisition leadership

- Speed of implementation

- Post-integration team and disregard of day-to-day business activities

- Communication during implementation

- Managing cultural differences

- Human resources management

2.1.5 Merger and Acquisition Costs

European central bank (2010) provides and overall view of merger and acquisition

costs. It is obvious that a target company will try to project its value to a high level but

the firm who want to take over the target company wants the deal to be settled at a low

price. Costs are calculated in order to check the viability and profitability of a specific

deal. A company will finalize a merger only after calculating the cost of the merger,

and in case of acquisition after determining how beneficial will be the takeover. Three

methods appear as popular in cost calculation of merger and acquisition. (Scott

Hempling, 2001.)

A) Replacement cost method: The acquisition in this case is based on the cost of

replacing the target company. The replacement cost method is rarely uses because of

18

its limitations especially in service industry where key assets are people, knowledge

and ideas. (Scott Hempling, 2001.)

B) Discounted Cash Flow method

Determine the company’s current value according to estimated future cash flow.

Comparative Ratio:

Involves two points. Firstly the price earnings ratio (P/E ratio) where the acquiring

company uses P/E ratio to make an offer that is a multiple of the earning of the target

company. Secondly the enterprise value-to-sales-ratio (EV/sales) where the acquiring

company uses EV /sales ratio to make an offer as a multiple of the revenue while being

aware of the price-to-sale ratio of other companies in the industry.(Scott

Hempling,2001.)

The European central bank (2010) defines a basic classification of merger and

acquisition costs:

(1) Transaction Costs

Are the costs of bringing the merging firm into agreement and obtaining approval for

the merger.These costs may include legal, regulatory and investment banking fees.

(2) Transition Costs

Are costs incurred to implement the consolidation .Transition costs include employee

relocation, early retirement and payment to departing executive.

(3) Acquisition Premium

It is a special form of transaction cost. It is the amount by which the purchase price for

the asset exceeds its new book value.

(4) Others Costs

Encompasses costs related to pension fund and different taxes.

2.1.6 Reasons of Merger and Acquisition failure

Many studies research indicate that more than 70% of companies fail to show positive

results when it comes to merger and acquisition. The ultimately do not add value to

companies and even end up causing serious damages. The reasons behind those

failures are diverse and the fact that the environment is changing all the time, in

addition to the interdependency of factors increase the complexity of merger and

19

acquisition .Ulrich Steger (2007) provided an approach describing the failure of

merger and acquisition base on 4 points: unrealistic expectations, overconfidence,

promoters and external advice, distrust and group dynamics.

(a) Unrealistic expectations

Is the main cause for merger and acquisition failure. Mergers and Acquisitions task is

complex and often underestimate by managers who deals with unrealistic. Resistance

shows up and with resistance comes delay. Integration takes time and it is painstaking.

This is where the success can be spoiled .It is often predicted that change will be faster

and easier than what is realistic. The profound changes needed for success are more

difficult and take much longer than originally thought. The changes implemented

during post-merger integration projects usually only scratch the surface .As the

integration progresses more difficult obstacles surface, synergies and the like become

harder to realize. In brief merger and acquisition efforts are often doomed to fail from

the very beginning due to unrealistic expectations, especially concerning amount

spent, speed, ease and the effects, as well as the rewards of charges. These issues are

pushed especially hard by the promoters of merger and acquisition who promise fast,

easy, dramatic and successful change. (Steger, 2007.)

(b) Overconfidence

Every entrepreneurial decisions aiming for returns bear certain risks. This is also the

case for merger and acquisition .Confidence in the success for merger and acquisition

deal ,and the achievement of its goals, are crucial ingredients for a potential success if

the was not the case ,managers would hardly make the necessary efforts for merger

and acquisition projects. Confident managers who try are more likely to succeed than

are managers lacking confidence who also make the same attempt .Confidence can

then make the critical difference between a make and a break situation. Management

overconfidence may lead to an illusion of control and hence to premature solutions

with less thorough evaluation of acquisition candidates and little consideration of

integration issues. The enormous difficulties of merger and acquisition tend not to

become fully apparent until the integration phase, otherwise most people might restrain

themselves from making the necessary efforts to do merger and acquisition. The

successfully mastered first phase of merger and acquisition faster the illusion that

people are competent enough to succeed in the following phases as well, i.e. the initial

20

success contributes to overconfidence .Incompetent people seem not to recognize their

own inability. They are more prone to engage in projects and persist in efforts that are

likely to fail. Thus people who should be especially concerned about overconfidence

do not seem to care. (Steger, 2007.)

(c) Promoters and external advice

Managers rely heavily on promoters to initiate structure and carry out the merger and

acquisition transaction. Promoters have a vested interest in merger and acquisition and

push companies into merger and acquisition deals in order to offer their services.

Promoters play a signaling role and convince managers that they can succeed.

Promoters can fulfill a useful function by fostering confidence, restoring hope and

providing motivation .But the problem occurs when success becomes less likely, when

the same qualities are unjustified and totally unwarranted. Overconfidence can also be

founded on promoters. The self-assured candidates and those with dominant

personalities are hired. Very often promoters hire graduate students base on their

personality and academic performance. However there can be a huge gap between

recruits grade and their capabilities to perform in merger and acquisition strategies.

This recruitment bias might be true in few cases and self-selection by applicants might

already have taken place. Promoters believe in their personal success that is often

based on false self-evaluation. Promoters see fees and projects sold as criteria for

success. The important goal is that their integration services are needed and follow-up

projects are sold. Promoters may prefer complicated merger and acquisition projects

where, in the end, blame cannot be attributed. (Steger, 2007.)

(d) Distrust

The attitude and mood of the employees are often quite the opposite of overconfidence.

This might contribute to the failure because, as previously mentioned, an appropriate

amount of confidence is a crucial ingredient for success .The uncertainty about what

will happen in the future often affect employee’s attitude and mood. A lot of questions

arise, is there a danger of losing their jobs? How will jobs and tasks be changed? These

uncertainties can last quite some time and deeply affect the working atmosphere.

Another point is that merger and acquisition will probably produce restructuration but

not really bring the desire outcome. (Steger, 2007.)

21

Group Dynamics: merger and acquisition transactions involves different group of

people. There is tendency to get carried away by a group dynamics. In merger and

acquisition decisions are made by the board of directors and management team. In case

of failure the responsible manager will have to leave. Blame is often put on those who

carry out the post-merger integration and not on those who decide to initiate the

transaction as such. Participants in merger and acquisition negotiations often become

committed to the deal regardless of its logics or benefits of the company. (Steger,

2007.)

2.2 Bank Performance

The capacity to generate sustainable profitability is a bank’s first line of defense

against unexpected losses, as it strengthens its capital position and improves future

profitability through the investment of retained earnings. Since the ultimate purpose

of any profit-seeking organization is to preserve and create wealth for its owners, the

bank’s return on equity (ROE) needs to be greater than its cost of equity in order to

create shareholder value. Although banking institutions have become increasingly

complex, the key drivers of their performance remain earnings, efficiency, leverage

and risk-taking. Efficiency refers to the bank’s ability to generate revenues from a

given amount of assets and to make profit from a given source of income.

Risk-taking is reflected in the necessary adjustments to earnings for the undertaken

risks to generate them. Leverage might improve results in the upswing in the way it

functions as a multiplier but conversely it can also make it more likely for a bank to

fail, due to rare, unexpected losses (European central bank, 2010).

Academics and practitioners defined three categories of performance measures for

banks:

2.2.1 Traditional Measure of Performance

They are similar to those applied in the industries with the return on assets(ROA), the

return on equity(ROE) or cost-to-income ratio are the most widely used.(European

central bank,2010).

The return on assets (ROA) is the net income for the year divided by the total assets,

usually the average value over the year. ROA= 𝑁𝑒𝑡 𝑖𝑛𝑐𝑜𝑚𝑒

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠

22

The return on equity (ROE) is an internal performance measure of shareholder value,

and it is by far the most popular measure of performance. ROE= 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐸𝑥𝑝𝑒𝑛𝑠𝑒𝑠

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑟𝑒𝑣𝑒𝑛𝑢𝑒𝑠

The cost-to-cost income ratio shows the utility of the institution to generate profits

from a given revenue stream .Impairment charges are not included in the numerator.

Cost-to-cost income ratio = 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑒𝑥𝑝𝑒𝑛𝑠𝑒𝑠

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑟𝑒𝑣𝑒𝑛𝑢𝑒𝑠

Net interest margin is a proxy for the income generation capacity of intermediation

function of bank.

Net interest margin = 𝑛𝑒𝑡 𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑖𝑛𝑐𝑜𝑚𝑒

𝑎𝑠𝑠𝑒𝑡𝑠(𝑜𝑟 𝑖𝑛𝑒𝑡𝑟𝑒𝑠𝑡−𝑏𝑒𝑎𝑟𝑖𝑛𝑔 𝑎𝑠𝑠𝑒𝑡𝑠)

2.2.2 Economic Measure of Performance

This measure take in account the development of shareholder value creation and aim

at assessing ,for any given fiscal year, the economic results generated by a company

from it economic assets. Economic measures mainly focus on efficiency as a central

element of performance, but generally have high levels of information requirements.

Two sets of indicators can be identified amongst economic measures of performance

(European central bank, 2010).

Indicators related to the total return of an investment, based on the concept of an

“opportunity cost”. The most popular is the economic value added (EVA). The EVA

takes into account the opportunity cost for stockholders to hold equity in a bank,

measuring whether a company generates an economic rate of return higher than the

cost of invested capital in order to increase the market value of the company (European

central bank, 2010).

EVA = 𝑟𝑒𝑡𝑢𝑟𝑛 𝑜𝑛 𝑖𝑛𝑣𝑒𝑠𝑡𝑒𝑑 𝑓𝑢𝑛𝑑𝑠 − (𝑤𝑒𝑖𝑔ℎ𝑡𝑒𝑑 𝑎𝑣𝑒𝑟𝑎𝑔𝑒 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 ∗

𝑖𝑛𝑣𝑒𝑠𝑡𝑒𝑑 𝑐𝑎𝑝𝑖𝑡𝑎𝑙) − (𝑤𝑒𝑖𝑔ℎ𝑡𝑒𝑑 𝑎𝑣𝑒𝑟𝑎𝑔𝑒 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡 ∗ 𝑛𝑒𝑡 𝑑𝑒𝑏𝑡)

Indicators related to the underlying level of the risk associate with bank activity. Risk

adjusted return on capital (RAROC) allows banks to allocate capital to individual

business units according to their individual business risk. As a performance evaluation

tool, the RAROC is the assigns capital to business unit based on the anticipated

economic value added. Theoretically the RAROC can be extracted from the one-factor

23

CAPM as the excess return on the market per unit of market risk. However, the

literature is quite critical of this measure as a tool to analyze performance essentially

due to its thorough accounting basis, while it is difficult to calculate RAROC without

having access to internal data. (European central bank, 2010.)

2.2.3 Market-Based Measures of performance

Market-based measures of performance characterize the way the capital market value

the activities of any given company, compared with its estimated accounting or

economic value (European central bank, 2010). The most commonly used metric

include:

(1)The total share returns (TSR), the ratio of dividends and increase of the stock value

over the market stock price.

(2)The price earnings ratio (P/E), a ratio of the financial results of the company over

its share price.

(3)The price-to-book value (P/B) which relates the market value of the stockholders

equity to its book values.

(4)The credit default swap (CDS) which is the cost of insuring an unsecured bond of

the institution for a given time period. (European central bank, 2010.)

2.3 Mergers and Acquisitions in Banking Sector

Mergers and Acquisitions represents together with the internal growth and together

with partnership creating, a method of developing a bank. They are part of the

strategies of internationalization and of strategic re expanding of the groups, when the

fast action of external growth can bring the competitive advantage compared to the

competition or when new information has to be achieved, for the technology, research-

development, marketing or management. (Bleoju, 2010.)

One advantage of bank merger and acquisition is the diversification, the banks that

merge are summing up the financial potential and are created resources for the

approach of another type of operations and their accelerated expansion. Gomes et Al.

(2013) The volume and speed with which the merging was made follow the growth of

the market share, the increase of the business, the quality and efficiency in serving the

clients, reduction of costs, the creation of additional profits for the shareholders and

promoting more efficient procedures of management. Thus with a strong management

24

can be harmonized some aspects related to the obstacles presented in organization

structure, language differences, preparing and development of the business lines.

(Berea, 2001.)

Mergers and Acquisitions increases the development rhythm of the bank by taking

over some existent shares with visible, immediate efficiency, are reduced the risk by

the increase of the economic force of the bank, also the cost of acquisition are usually

underestimated. Mergers and Acquisitions especially those horizontal are a certain

method of penetrating and controlling new markets and increasing market share for

the newly created bank group (Berea, 2001).The economic reality showed that merger

and acquisition hide the negative secondary effects that can lead to the slowing of the

rhythm of growth of the company, can lead to employee’s dismissal while trying to

readjust the cost, to the decreasing of the innovation due to the focusing on the growth

generated by acquisitions. The study of merger and acquisition gives the possibility to

the bank to obtain the fastest and increase the volume of activities by conquering new

markets but also the strategy that has the great effect on the national and regional

economies. (Dobocan, 2010.)

Previous research suggests that many banks engage in mergers for the purpose of

improving efficiency. For instance, Berger and Humphrey (1992) study fifty-seven US

banking mega merger from 1981 to 1989.they estimate a neo-classical cost function

that allows them to show that mergers were not successful on average in improving

cost efficiency because of diseconomies of scale .the combined firms actually

performed slightly worse on average after the mergers, although this effect was small

and often not statistically significant. Although the majority of researches has focused

on cost efficiency a few studies have tried to cover additional effect of mergers by

using a profit function. Studies of profit efficiency usually point a more favorable

picture of mergers. Such studies of profit from the 1980s and early 1990s found that

mergers improved profit efficiency, and that this improvement could be linked to an

increased diversification of risk and improved risk-expected return tradeoff.

(Akhavein, Berger and Humphrey, 1997, and Berger, 1998.)

Despite their popularity many of the mergers and acquisitions do not succeed to

produce financial benefits that are expected. In fact past studies include that almost

70% of mergers and acquisitions don’t succeed to improve the performance of the

25

banks involved. The failure of merger and acquisition, most of the time, is due to either

illusory synergy, to the vain of high management or to a slow integration. (Drucker,

2001.)

Today the nature of the bank was changed, the progresses registered in the technology

created the interdependencies from the economy, the speed of financial transactions

would reach to a high level so that it would feel the needs of renouncing to the old

geographical limitations in favor of some banks from Europe and USA which

determined the appearance of some great banks created new gigantic structures .the

justification for performance of these mega transactions is the large market.(Drucker,

2001.)

26

3 RESEARCH PROBLEM AND PREVIOUS RELATED LITERATURES

The outbreak of bank merger and acquisition in USA is attracting much attention,

partly because of the heightened interest in what motivates firms to merge and how

merger and acquisition affect performance or efficiency. This research investigates

effects of merger and acquisition on the performance of (bidder) banks. It is motivates

by the ambiguity of the empirical evidence on the impacts of merger and acquisition

involving US banks. Overall, the handful of studies on mergers and acquisitions

activities in US banking industry provides mixed results.

For instance, Altunbas and Ibanez (2004) report that bank mergers taking place in the

banking industry to lead on average to improve accounting and profitability. Vander

(2002) reports a limited improvement in profit efficiency but not in cost efficiency

with reference to cross border deals only.

According to Pilloff and Santomero (1997), there is little empirical evidence of

mergers achieving growth or other important performance gains. Towards this, Beitel

et Al (2003) found no gains effect due to mergers and acquisitions .Overall of all these

studies provide mixed evidence and many fails to show a clear relationship between

mergers &acquisitions and performance (Pilloff and Santomero,1997).

Rym Ayadi and Georges Pujals (2005) provide a complete picture of banking mergers

and acquisitions in Europe during the 1990s and at offering economic evaluation and

strategic analysis of the process. They examine the impact of mergers and acquisitions

in European banking on profitability and efficiency. They found that domestic mergers

contribute to cut costs for both partners, the impact on profitability is insignificant but

a clear trend to diversify the resources of the revenues was apparent. The cost and

profit efficiency analysis based on 33 bank-to-bank mergers ,confirmed an

improvement of cost efficiency and little improvement of profit efficiency for

domestic transactions, whereas no improvement of profit efficiency for domestic

transactions; whereas, no improvement of cost efficiency and little improvement of

profit efficiency for cross-border.(Rym Ayadi & Georges Pujals,2005.)

A similar study on the impact of mergers and acquisitions on financial performance of

bank has been conducted in Pakistan.Tajalli Fatima & Amir Shehzad (2014) have

27

tested the impact of mergers and acquisitions on banks and provides insights about

their role after merger on banks profitability. They uses six financial ratios(ROA,

ROE, Profit after tax, Debt to equity ratio, EPS, deposit to equity) and compares three

years pre-mergers and three years post mergers data points for ten banks and their and

their average are compared. Findings shows that at 5% level of significance only ROE

is affected by the merger and acquisition and other ratios have no impact from this

strategy. (Tajalli Fatima & Amir Shehzad, 2014.)

Onaolapo & Ajala (2012) have examined the effects of merger and acquisition on the

performance of the commercial banks in Nigeria with a greater emphasis on gross

earnings, profit after tax and deposit profile as financial efficiency parameters. The

results showed that post-merger and acquisition period was more financially improved

than the pre-merger and acquisition period. Also the study found that the point

consolidation periods has a higher performance in gross earning; deposit has a better

performance while profit after tax is comparatively has low but improved performance

than the pre-consolidation period. This study recommended that banks should be more

proactive in driving for profit for enhanced financial performance to reap the benefits

of mergers and acquisitions bid in banking sector. (Onaolapo & Ajala, 2012.)

Abbas et Al (2014) have studied the strategy of mergers and acquisitions on corporate

sector in Pakistan .The study was conducted in a small scale. Hence the study

accomplished the declared gap in the area of Mergers and acquisitions. The purpose

of this study is to assess the impact of merger and acquisition on the performance of

banks, ratios analysis has been used between pre and post-merger and acquisition. The

results showed that there are no improvements in the financial performance of banks

after merger and acquisition. There is a decrease in profitability, efficiency, liquidity,

and leverage ratio in the most of the banks after merger and acquisition. In the

dimension of liquidity and leverage there is no much improvement in financial

performance of banks in Pakistan after merger and acquisition. (Abbas et Al, 2014.)

The aim of the paper is to use an empirical approach in order to directly assess whether

merger and acquisition involving US banks lead to improvements in performance .In

the light of above, the following research question where raised:

28

(1) Does merger and acquisition have any effects on the financial performance of

bidder banks?

(2) Did the financial performance of bidder bank improve after merger and

acquisition?

Accounting and statistics methodologies are the base of this study where financial

indicators were used to measure the performance. To answer the above stated research

question the research had developed following hypothesis:

(1) 𝐻0: Merger and Acquisition has no significant effect on financial performance of

bidder bank.

(2) 𝐻1: Merger and Acquisition has significant effect on financial of bidder bank.

To perform this task it is important to form a mathematical hypothesis for testing each

variable independently.

(3) 𝐻0: µPost - µPre = 0 →µPost = µPre

(4) 𝐻1:µPost - µPre ≠ 0 →µPost ≠ µPre

The analysis of the financial performance is done by comparing pre-and-post financial

ratios. All the ratios are calculated for two years before merger and acquisition and

two years after the merger and acquisition of bidder banks.

29

4 DATAS AND METHODS

Different methods and techniques have been used in previously conducted studies

regarding merger and acquisition performance. The analysis of this research relies on

accounting and statistical analysis of financial ratio. Brighman and Ehrhardt (2005)

examined that the financial statement analysis is a better approach to evaluate the firm

strength. Moreover they emphasized the importance of financial statement to

accurately analyze improvements in financial performance. Pre-and-post performance

has been studied through operating performance approach using accounting data

(Gjirja, 2001).

This research is undertaken to assess the financial performance of bidder/acquirer bank

in USA after merger and acquisition. A comparison between pre-and-post ratio of

selected banks is use to achieve the task. The statistics regarding merger and

acquisition in banking sector in USA were available on the website of SDC platinum

and CRSP according to this information there were more than 500 mergers and

acquisitions in banking sector. Data were collected from secondary source through

compilation and extraction from published data including published audited financial

statement, income statement and balance sheet from 2004 to 2013. The present

research measure the financial performance of thirty (30) acquiror banks during the

period of 2004 to 2013.The were 105 deals of mergers and acquisitions in USA

banking sector during the selected period but the analysis focus on 30 due to the

availability of financial and accounting data, on transactions occurred on domestic

level in USA banking sector and, on a single operation between one bank to another.

The table below shows our studied sample, the effective date of the transaction, bank’s

name and identification code according to USA regulation.

30

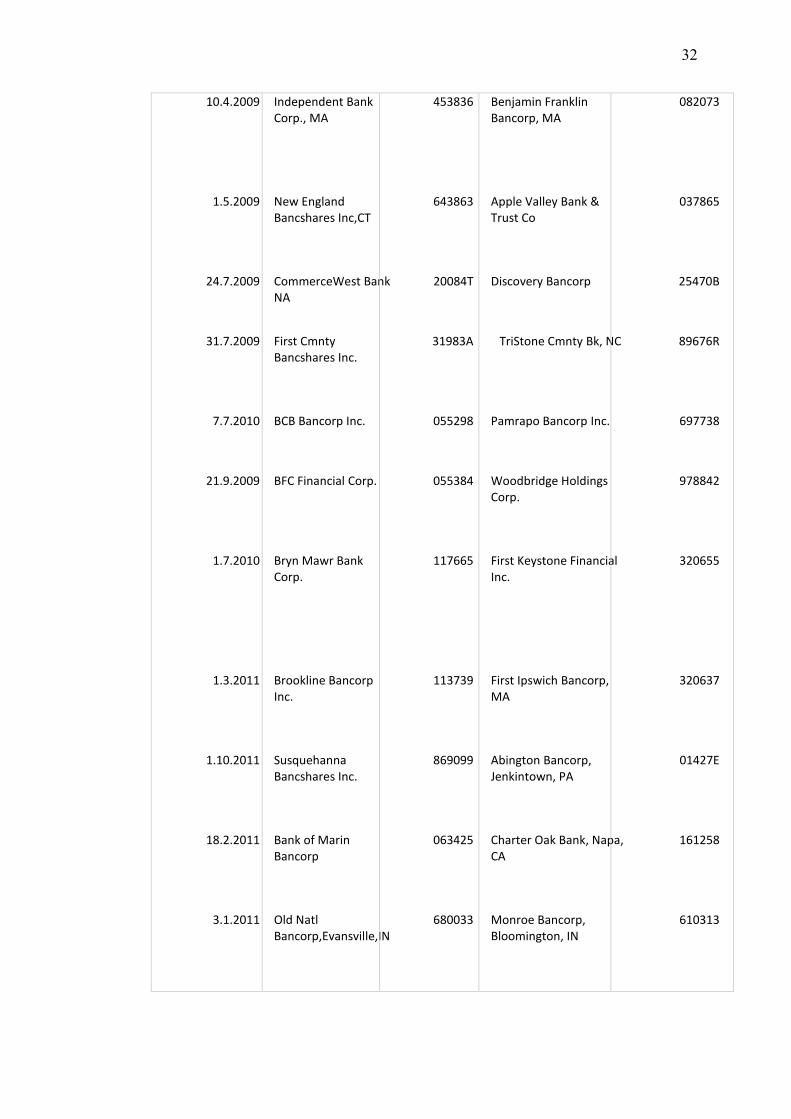

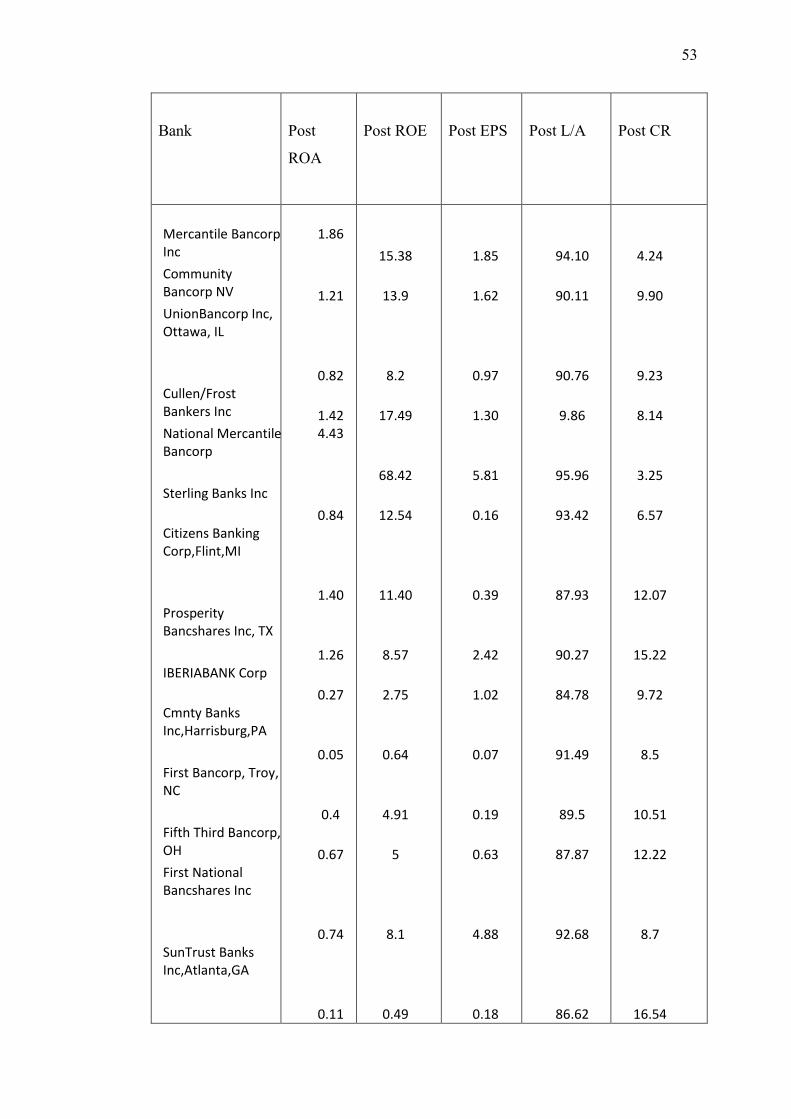

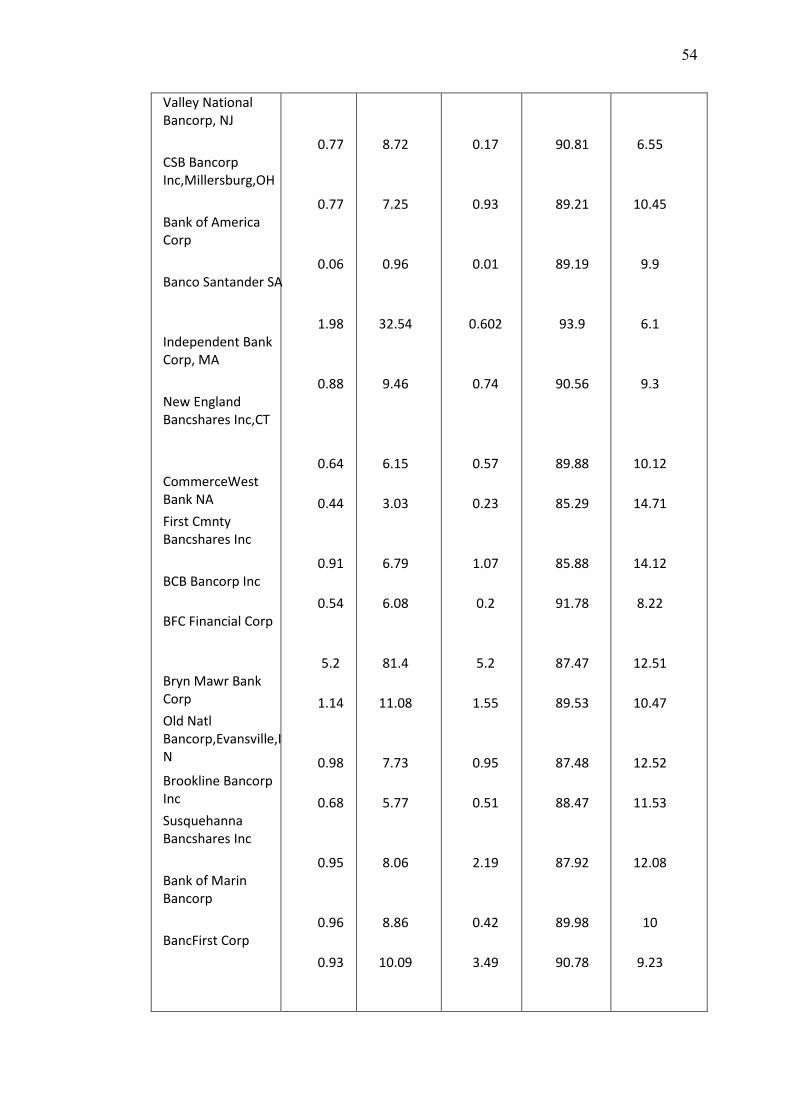

Table 3: Sample of Selected of Banks (SCD Platinium)

Date

Acquiror Acquiror Cusip Target Target Cusip

13.11.2006

14.10.2006

15.11.2006

8.12.2006

13.3.2007

16.3.2007

2.1.2007

31.1.2007

Mercantile Bancorp Inc.

Community Bancorp NV

Union Bancorp Inc, Ottawa, IL

Cullen/Frost Bankers Inc.

National Mercantile Bancorp

Sterling Banks Inc.

Citizens Banking Corp,Flint,MI

Prosperity Bancshares Inc., TX

58734P

20343T

908908

229899

636912

85915B

174420

743606

Royal Palm Bancorp Inc,Naples,

Valley Bancorp

Centrue Financial Corp., IL

Summit Bancshares Inc.

FCB Bancorp, Camarillo, CA

Farnsworth Bancorp Inc.

Republic Bancorp Inc, Owosso, MI

Texas United Bancshares, TX

78064Y

91929R

15641R

866010

30247A

31163N

760282

882838

31

2.2.2007

2.4.2007

1.4.2008

6.6.2008

31.1.2008

1.5.2008

1.7.2008

31.10.2008

1.1.2009

30.1.2009

IBERIABANK Corp.

Cmnty Banks Inc,Harrisburg,PA

First Bancorp, Troy, NC

Fifth Third Bancorp, OH

First National Bancshares Inc.

SunTrust Banks Inc,Atlanta,GA

Valley National Bancorp, NJ

CSB Bancorp Inc,Millersburg,OH

Bank of America Corp.

Banco Santander SA

450828

203628

318910

316773

32111B

867914

919794

12628R

060505

05964H

Pocahontas Bancorp, AR

BUCS Financial Corp.

Great Pee Dee Bancorp Inc,SC

First Charter Corp., Charlotte

Carolina National Corp.

GB&T Bancshares Inc,Georgia

Greater Community Bancorp

Indian Village Bancorp Inc, OH

Merrill Lynch & Co.Inc.

Sovereign Bancorp Inc.

730234

118724

39115R

319439

144060

361462

39167M

454533

590188

845905

32

10.4.2009

1.5.2009

24.7.2009

31.7.2009

7.7.2010

21.9.2009

1.7.2010

1.3.2011

1.10.2011

18.2.2011

3.1.2011

Independent Bank Corp., MA

New England Bancshares Inc,CT

CommerceWest Bank NA

First Cmnty Bancshares Inc.

BCB Bancorp Inc.

BFC Financial Corp.

Bryn Mawr Bank Corp.

Brookline Bancorp Inc.

Susquehanna Bancshares Inc.

Bank of Marin Bancorp

Old Natl Bancorp,Evansville,IN

453836

643863

20084T

31983A

055298

055384

117665

113739

869099

063425

680033

Benjamin Franklin Bancorp, MA

Apple Valley Bank & Trust Co

Discovery Bancorp

TriStone Cmnty Bk, NC

Pamrapo Bancorp Inc.

Woodbridge Holdings Corp.

First Keystone Financial Inc.

First Ipswich Bancorp, MA

Abington Bancorp, Jenkintown, PA

Charter Oak Bank, Napa, CA

Monroe Bancorp, Bloomington, IN

082073

037865

25470B

89676R

697738

978842

320655

320637

01427E

161258

610313

33

Accounting and statistic methodologies are the base for this study where financial

indicators were used to measure the performance. Accounting methodology is used to

calculate five financial ratios which are the core measure of the profitability of the

selected banks (Table 3). All ratios are calculated at the end of the year (31 December)

for a two years period before merger and acquisition (Pre) and two years period after

the merger and acquisition (Post). To test whether there is a significant difference in

financial performance of bidder banks the study compares the pre-merger performance

ratio with the post-merger performance ratios. Two year Pre-merger and two year post-

merger data points are taken for all the thirty cases and then the average are taken for

the purpose of analysis. The dependent variable used here is merger and acquisition

while independent variables are the financial performance of bank. To measure the

financial performance the study used five ratios for the analysis as ratios are best

indicators of performance. The return on assets (ROA) will measure the profitability

generated from assets. The return on equity (ROE) will measure attractiveness of the

investments. Earnings per share (EPS) measure profit allocated to each outstanding

share of common stock. The capital ratio (CR) will evaluate the level of capitalization

of each bank. The total liabilities/total assets (L/B) will measure the financial risk. The

possible impact of the independent variables to dependent variables is statistically

analyses by R studio.

The statistical methodology will use the calculated ratios as variables to assess the real

impact of merger and acquisition on USA bidder performance.

The statistical methodology will cover two stages. The first stage will to check the

normality of the sample. The Shapiro-Wilk test is used in this study to calculate a W

statistics that test whether the random sample come from a normal distribution. The

tested hypothesis are describe below:

(1) 𝐻0: 𝐷𝑎𝑡𝑎 𝑠𝑒𝑡 𝑖𝑠 𝑛𝑜𝑟𝑚𝑎𝑙𝑙𝑦 𝑑𝑖𝑠𝑡𝑟𝑖𝑏𝑢𝑡𝑒𝑑

(2) 𝐻1: Data set is not normally distributed

The test will provide two values for each studied variables. A value W which is the

observed value of the Shapiro-Wilk statistic and a P value which is the exact

probability of the outcome. If P value is higher than 0.05 we can be 95% certain that

the data are normally distributed. (In other words the null hypothesis is probably

true.).If the P value is less than 0.05 we can 95% be sure that the data are not normally

34

distributed. (In other words there are not enough evidences to accept the null

hypothesis).

The pre and post-merger performance is efficiently assessed with the T paired test

which focus on the mean difference between post and pre observations.

(3) 𝐻0: µPost -µPre = 0

(4) 𝐻1:µPost - µPre ≠ 0

When running the test we will obtain a mean difference, the standard deviation error

of the mean difference and the t-statistic .If the t calculated is higher than the table

value (significance level is 5%) then there are not enough evidences to accept null

hypothesis. If the calculated t calculated is lower than the table value then the null

hypothesis is accepted. However to be valid the T paired test need to be approximately

normally distributed.

In case of violation of normality the alternative option is to conduct a Wilcoxon sign

rank test which does not assume normality in data. The Wilcoxon test uses the same

hypothesis as the T paired test but provide two results. A value V which is the observed

value of the Wilcoxon sign rank test and P value which are the exact probability of the

outcome. If the P value is higher than 0.05 we will accept the null hypothesis.

Reversely if the P value is less than 0.05 then we do not have enough evidences to

accept the null hypothesis.

Table 4. Financial Ratio Formulas (Juha-Pekka Advance Firm valuation 2015)

Financial Ratios

Formulas

Return on Asset ( ROA)

𝑁𝑒𝑡 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑝𝑟𝑜𝑓𝑖𝑡 𝐴𝑓𝑡𝑒𝑟 𝑡𝑎𝑥

𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠

35

Return on Equity (ROE)

𝑁𝑒𝑡 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑃𝑟𝑜𝑓𝑖𝑡 𝐴𝑓𝑡𝑒𝑟 𝑇𝑎𝑥

𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠

Earnings Per Share (EPS)

𝑁𝑒𝑡 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑃𝑟𝑜𝑓𝑖𝑡 𝐴𝑓𝑡𝑒𝑟 𝑇𝑎𝑥

𝑁𝑢𝑚𝑏𝑒𝑟 𝑜𝑓 𝑂𝑟𝑑𝑖𝑛𝑎𝑟𝑦 𝑆ℎ𝑎𝑟𝑒𝑠

Capital Ratio (CR)

𝑇𝑜𝑡𝑎𝑙 𝐸𝑞𝑢𝑖𝑡𝑦

𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠

Total liabilities/Total Assets (L/A)

𝑇𝑜𝑡𝑎𝑙 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠

𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠

36

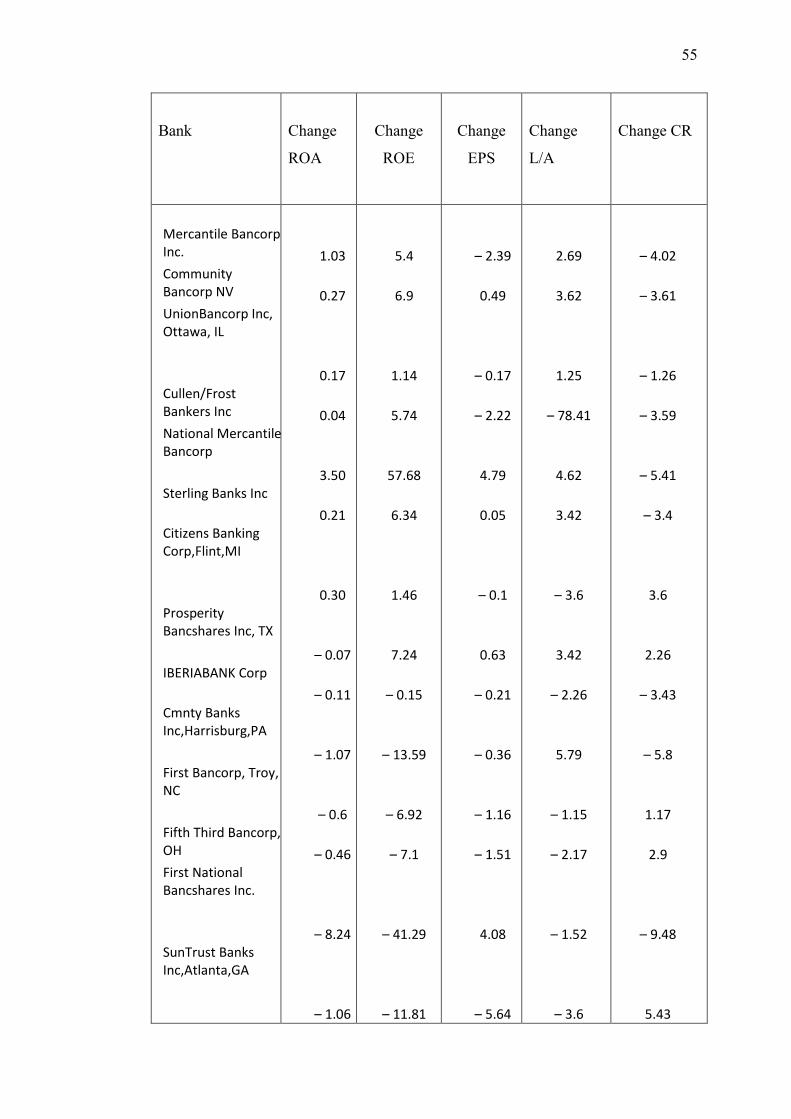

5 RESULTS AND DISCUSSION

The study uses the mean between pre and post-merger values as core of the analysis.

The paired T test is appropriate to compare pre and post-merger performance for

studied banks. The difference between pre and post-merger performance for each ratio

and the mean of difference are used to test hypothesis:

(1) 𝐻0: µPost = µPre

(2) 𝐻1:µPost ≠ µPre

Under the null hypothesis, the statistic follows a t distribution with n-1 degrees of

freedom.

However the T paired test is valid only if the sample has normally distributed variables.

Therefore a Shapiro-Wilk test is used to test if the sample is normally distributed. A

value P=0.05 is used as cutoff. When the calculated p value is lower than 0.05 we can

conclude that the sample deviate from normality.

In case of non-normally distributed variable a Wilcoxon sign rank test will be applied.

5.1 Sample test of Normality

Two hypotheses will be tested:

(3) 𝐻0: 𝐷𝑎𝑡𝑎 𝑠𝑒𝑡 𝑖𝑠 𝑛𝑜𝑟𝑚𝑎𝑙𝑙𝑦 𝑑𝑖𝑠𝑡𝑟𝑖𝑏𝑢𝑡𝑒𝑑

(4) 𝐻1: Data set is not normally distributed

A cutoff value P=0.05 is applied. If P< 0.05 there are not enough evidences to accept

the null hypothesis and the population failed to be normally distributed.

Table 5. Shapiro – Wilk test results

Variables

ROA

ROE

EPS

CR

L/A

W

0.66371

0.58947

0.928

0.32786

0.376

37

P value

4.82𝑒−0,7

5.442𝑒−0,8

0.04347

1.22𝑒−10

3.10𝑒−10

By using a cutoff value P=0.05 we can see that the P values of all the variables are

lower than 0.05 .By referring to the results there are not enough evidences to accept

the null hypothesis 𝐻0 therefore at 5% level of significance the sample is not normally

distributed. As the assumption of normality in data has been violated the T-test is no

longer valid. The Wilcoxon signed-rank test will be appropriate to compare pre and

post-merger performance in this case.

Figure 1. Change in Capital Ratio

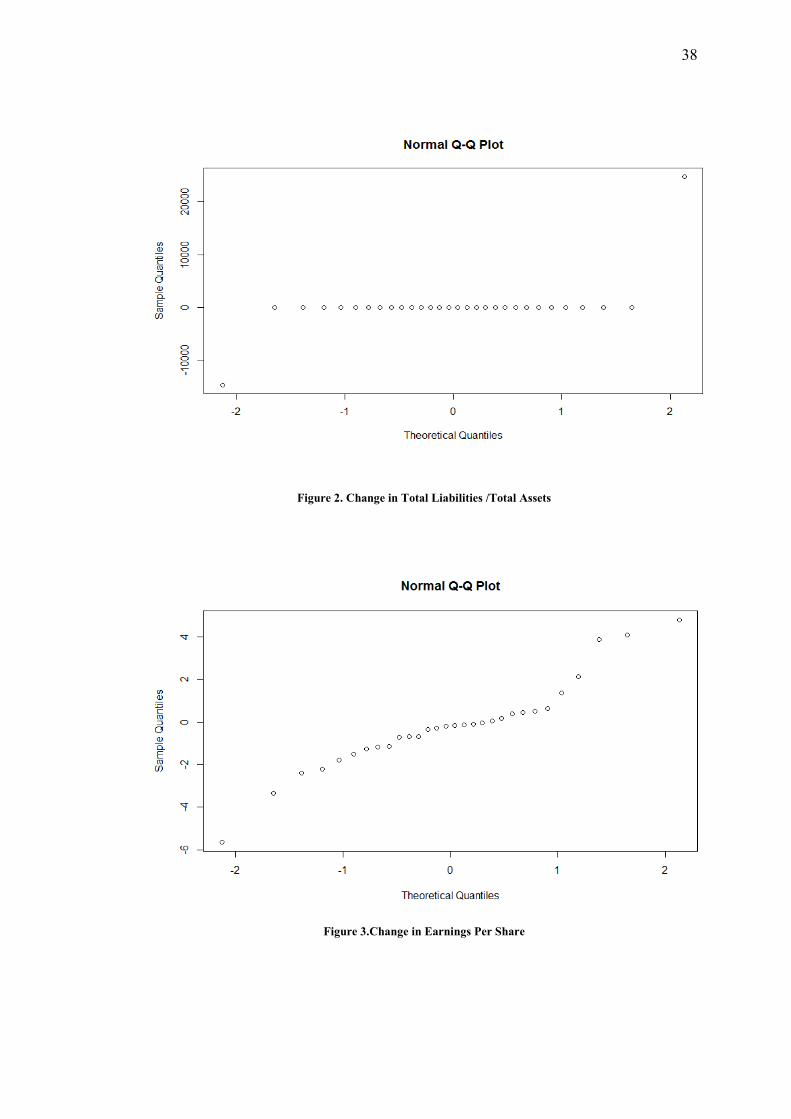

38

Figure 2. Change in Total Liabilities /Total Assets

Figure 3.Change in Earnings Per Share

39

Figure 4. Change in Return on Equity

Figure 5. Change in Return on Assets

40

The quantiles-quantiles plot (Q-Q plot) of each variable compares pre and post-merger

measure. All points follow a strongly nonlinear pattern suggesting that the data set are

not normal distributed.

5.2 Variables testing

The Wilcoxon signed-rank test is used to test hypothesis of the studied model

(1) 𝐻0: µPost = µPre

(2) 𝐻1:µPost ≠ µPre

Relatively a cutoff value of P= 0.05 is used as standard. If P>0.05 we will accept the

null hypothesis and conclude that the means have remained essentially unchanged.

V correspond to the sum of ranks assigned to the differences with positive sign.

Table 6. Wilcoxon test Results

Variables

ROA

ROE

EPS

CR

L/A

V

200

208

181

151

219

P value

0.5104

0.6263

0.2988

0.0961

0.7892

The P values of all studied variables are higher than 0.05. The calculated probabilities

point out the fact there are not enough evidences to accept the alternative hypothesis

therefore, at 5% level of significance the null hypothesis is accepted assuming that

there is no difference between pre and post-merger performance for USA bidder bank.

The core indicators of investment attractiveness, the profit allocated to each

outstanding share of common stock, the level of capitalization of each bank and the

financial risk are globally the same for USA bidder banks during the pre and post-

merger period.

41

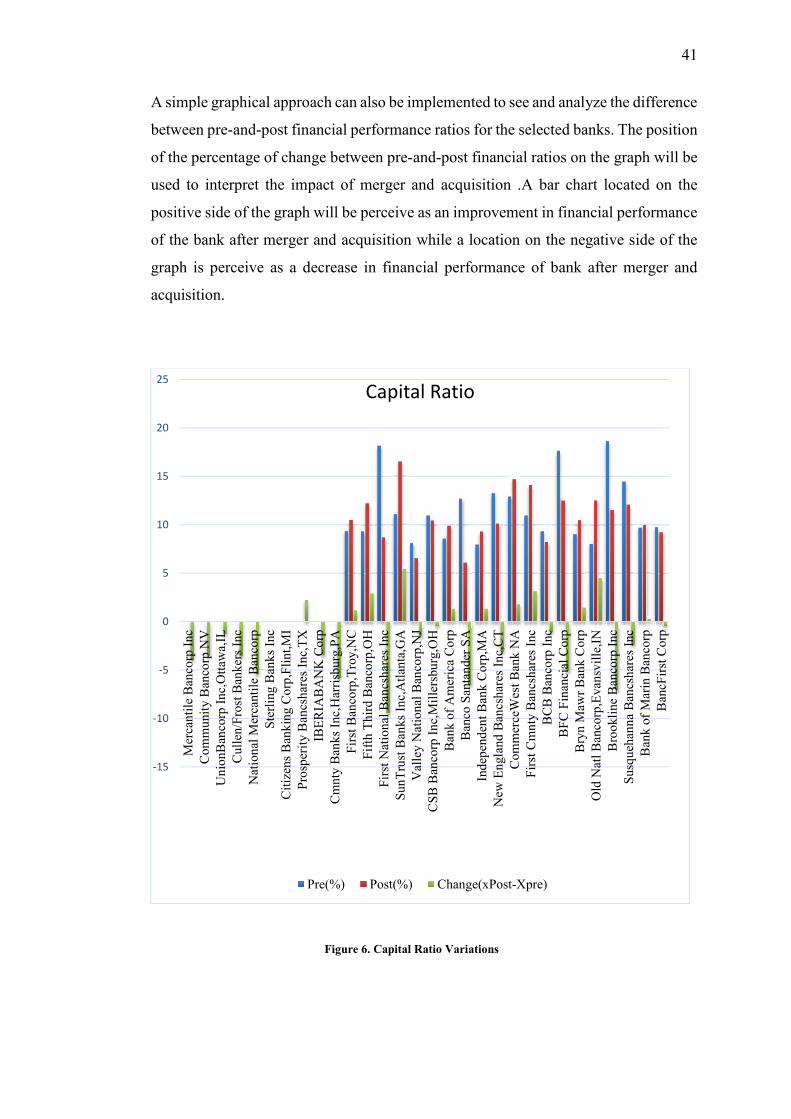

A simple graphical approach can also be implemented to see and analyze the difference

between pre-and-post financial performance ratios for the selected banks. The position

of the percentage of change between pre-and-post financial ratios on the graph will be

used to interpret the impact of merger and acquisition .A bar chart located on the

positive side of the graph will be perceive as an improvement in financial performance

of the bank after merger and acquisition while a location on the negative side of the

graph is perceive as a decrease in financial performance of bank after merger and

acquisition.

Figure 6. Capital Ratio Variations

-15

-10

-5

0

5

10

15

20

25

Mer

can

tile

Ban

corp

Inc

Com

mu

nit

y B

anco

rp N

V

Un

ionB

anco

rp I

nc,

Ott

awa,

IL

Cull

en/F

rost

Ban

ker

s In

c

Nat

ion

al M

erca

nti

le B

anco

rp

Ste

rlin

g B

ank

s In

c

Cit

izen

s B

ank

ing C

orp

,Fli

nt,

MI

Pro

sper

ity

Ban

csh

ares

Inc,

TX

IBE

RIA

BA

NK

Co

rp

Cm

nty

Ban

ks

Inc,

Har

risb

urg

,PA

Fir

st B

anco

rp,T

roy

,NC

Fif

th T

hir

d B

anco

rp,O

H

Fir

st N

atio

nal

Ban

csh

ares

Inc

Su

nT

rust

Ban

ks

Inc,

Atl

anta

,GA

Val

ley N

atio

nal

Ban

corp

,NJ

CS

B B

anco

rp I

nc,

Mil

lers

bu

rg,O

H

Ban

k o

f A

mer

ica

Co

rp

Ban

co S

anta

nder

SA

Ind

epen

den

t B

ank

Co

rp,M

A

New

En

gla

nd

Ban

csh

ares

In

c,C

T

Com

mer

ceW

est

Ban

k N

A

Fir

st C

mn

ty B

ancs

har

es I

nc

BC

B B

anco

rp I

nc

BF

C F

inan

cial

Co

rp

Bry

n M

awr

Ban

k C

orp

Old

Nat

l B

anco

rp,E

van

svil

le,I

N

Bro

okli

ne

Ban

corp

In

c

Su

squ

ehan

na

Ban

csh

ares

Inc

Ban

k o

f M

arin

Ban

corp

Ban

cFir

st C

orp

Capital Ratio

Pre(%) Post(%) Change(xPost-Xpre)

42

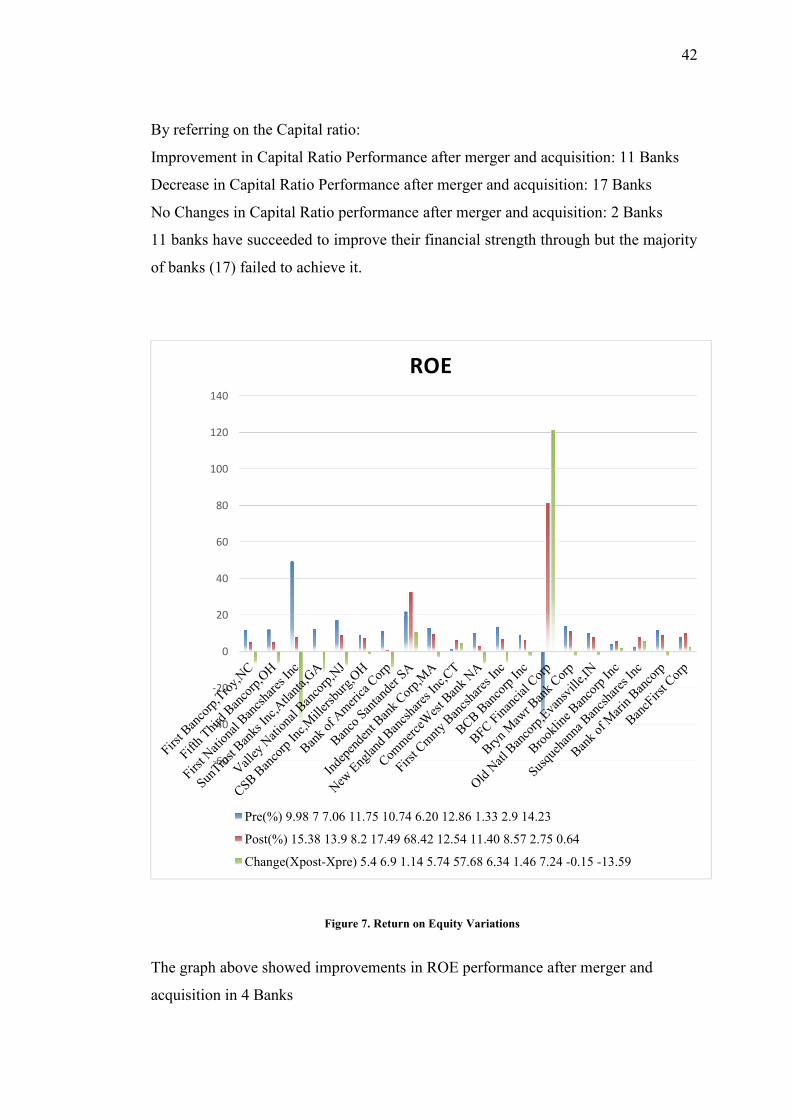

By referring on the Capital ratio:

Improvement in Capital Ratio Performance after merger and acquisition: 11 Banks

Decrease in Capital Ratio Performance after merger and acquisition: 17 Banks

No Changes in Capital Ratio performance after merger and acquisition: 2 Banks

11 banks have succeeded to improve their financial strength through but the majority

of banks (17) failed to achieve it.

Figure 7. Return on Equity Variations

The graph above showed improvements in ROE performance after merger and

acquisition in 4 Banks

-60

-40

-20

0

20

40

60

80

100

120

140

ROE

Pre(%) 9.98 7 7.06 11.75 10.74 6.20 12.86 1.33 2.9 14.23

Post(%) 15.38 13.9 8.2 17.49 68.42 12.54 11.40 8.57 2.75 0.64

Change(Xpost-Xpre) 5.4 6.9 1.14 5.74 57.68 6.34 1.46 7.24 -0.15 -13.59

43

; decrease in ROE performance after merger and acquisition for 14 Banks and no

changes in ROE performance after merger and acquisition for12 Banks.

Only 4 banks have improved their ROE performance showing that they utilizes the

proportion of shareholder equity efficiently to earn profit and significantly reduce their

cost which have enhanced profit after merger and acquisition. But the majority of

banks fails to do it.

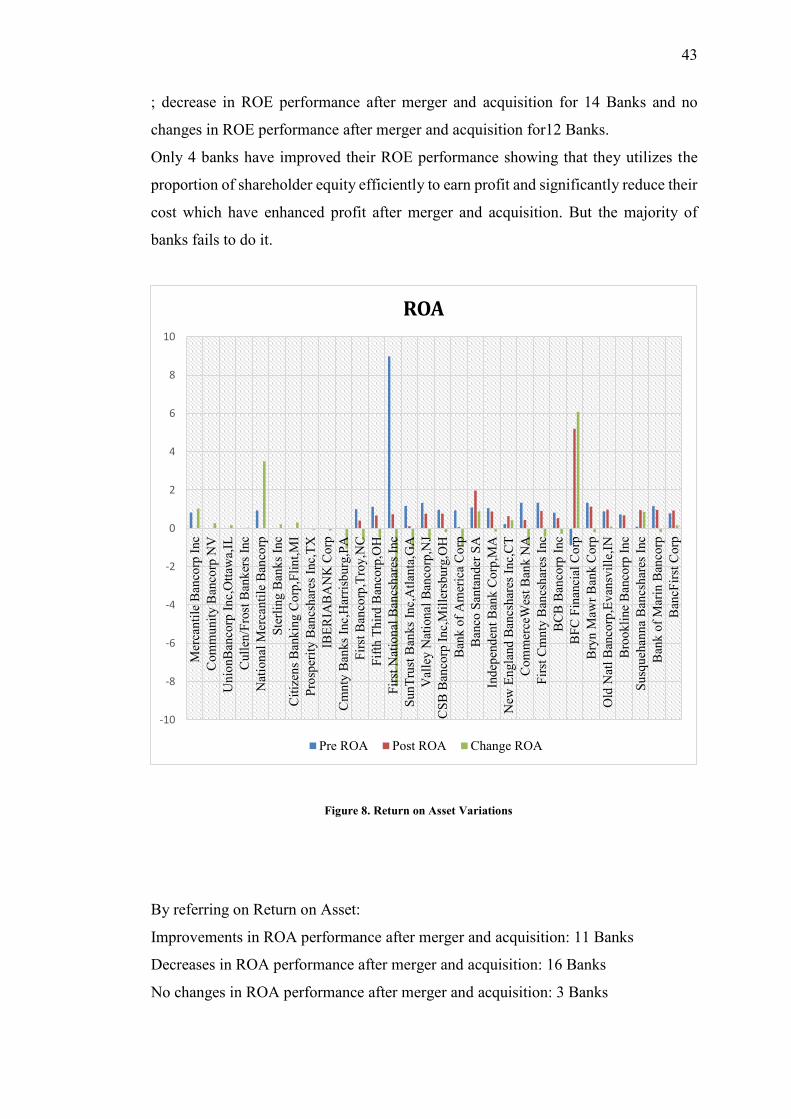

Figure 8. Return on Asset Variations

By referring on Return on Asset:

Improvements in ROA performance after merger and acquisition: 11 Banks

Decreases in ROA performance after merger and acquisition: 16 Banks

No changes in ROA performance after merger and acquisition: 3 Banks

-10

-8

-6

-4

-2

0

2

4

6

8

10

Mer

can

tile

Ban

corp

Inc

Com

mu

nit

y B

anco

rp N

V

Un

ionB

anco

rp I

nc,

Ott

awa,

IL

Cull

en/F

rost

Ban

ker

s In

c

Nat

ion

al M

erca

nti

le B

anco

rp

Ste

rlin

g B

ank

s In

c

Cit

izen

s B

ank

ing C

orp

,Fli

nt,

MI

Pro

sper

ity

Ban

csh

ares

Inc,

TX

IBE

RIA

BA

NK

Co

rp

Cm

nty

Ban

ks

Inc,

Har

risb

urg

,PA

Fir

st B

anco

rp,T

roy

,NC

Fif

th T

hir

d B

anco

rp,O

H

Fir

st N

atio

nal

Ban

csh

ares

Inc

Su

nT

rust

Ban

ks

Inc,

Atl

anta

,GA

Val

ley N

atio

nal

Ban

corp

,NJ

CS

B B

anco

rp I

nc,

Mil

lers

bu

rg,O

H

Ban

k o

f A

mer

ica

Co

rp

Ban

co S

anta

nder

SA

Ind

epen

den

t B

ank

Co

rp,M

A

New

En

gla

nd

Ban

csh

ares

In

c,C

T

Com

mer

ceW

est

Ban

k N

A

Fir

st C

mn

ty B

ancs

har

es I

nc

BC

B B

anco

rp I

nc

BF

C F

inan

cial

Co

rp

Bry

n M

awr

Ban

k C

orp

Old

Nat

l B

anco

rp,E

van

svil

le,I

N

Bro

okli

ne

Ban

corp

In

c

Su

squ

ehan

na

Ban

csh

ares

Inc

Ban

k o

f M

arin

Ban

corp

Ban

cFir

st C

orp

ROA

Pre ROA Post ROA Change ROA

44

11 Banks showed improvements in ROA. Those banks have used more assets to earn

profits. 16 banks need to acquire more assets from other organizations and utilize them

in an efficient way to earn more profits.

Figure 9. Total liabilities /Total assets variations

By referring on the Liabilities/Assets:

Improvements in L/A Performance after merger and acquisition: 11 Banks

Decreases in L/A performance after merger and acquisition: 12 Banks

No changes in L/A performance after merger and acquisition: 7 Banks

-100

-80

-60

-40

-20

0

20

40

60

80

100

120

Mer

can

tile

Ban

corp

Inc

Com

mu

nit

y B

anco

rp N

V

Un

ionB

anco

rp I

nc,

Ott

awa,

IL

Cull

en/F

rost

Ban

ker

s In

c

Nat

ion

al M

erca

nti

le B

anco

rp

Ste

rlin

g B

ank

s In

c

Cit

izen

s B

ank

ing C

orp

,Fli

nt,

MI

IBE

RIA

BA

NK

Co

rp

Pro

sper

ity

Ban

csh

ares

Inc,

TX

Cm

nty

Ban

ks

Inc,

Har

risb

urg

,PA

Fir

st B

anco

rp,T

roy

,NC

Fif

th T

hir

d B

anco

rp,O

H

Fir

st N

atio

nal

Ban

csh

ares

Inc

Su

nT

rust

Ban

ks

Inc,

Atl

anta

,GA

Val

ley N

atio

nal

Ban

corp

,NJ

CS

B B

anco

rp I

nc,

Mil

lers

bu

rg,O

H

Ban

k o

f A

mer

ica

Co

rp

Ban

co S

anta

nder

SA

Ind

epen

den

t B

ank

Co

rp,M

A

New

En

gla

nd

Ban

csh

ares

In

c,C

T

Com

mer

ceW

est

Ban

k N

A

Fir

st C

mn

ty B

ancs

har

es I

nc

BC

B B

anco

rp I

nc

BF

C F

inan

cial

Co

rp

Bry

n M

awr

Ban

k C

orp

Old

Nat

l B

anco

rp,E

van

svil

le,I

N

Bro

okli

ne

Ban

corp

In

c

Su

squ

ehan

na

Ban

csh

ares

Inc

Ban

k o

f M

arin

Ban

corp

Ban

cFir

st C

orp

Liabilities/Assets

Pre(%) Post(%) Change(Xpost-XPre)

45

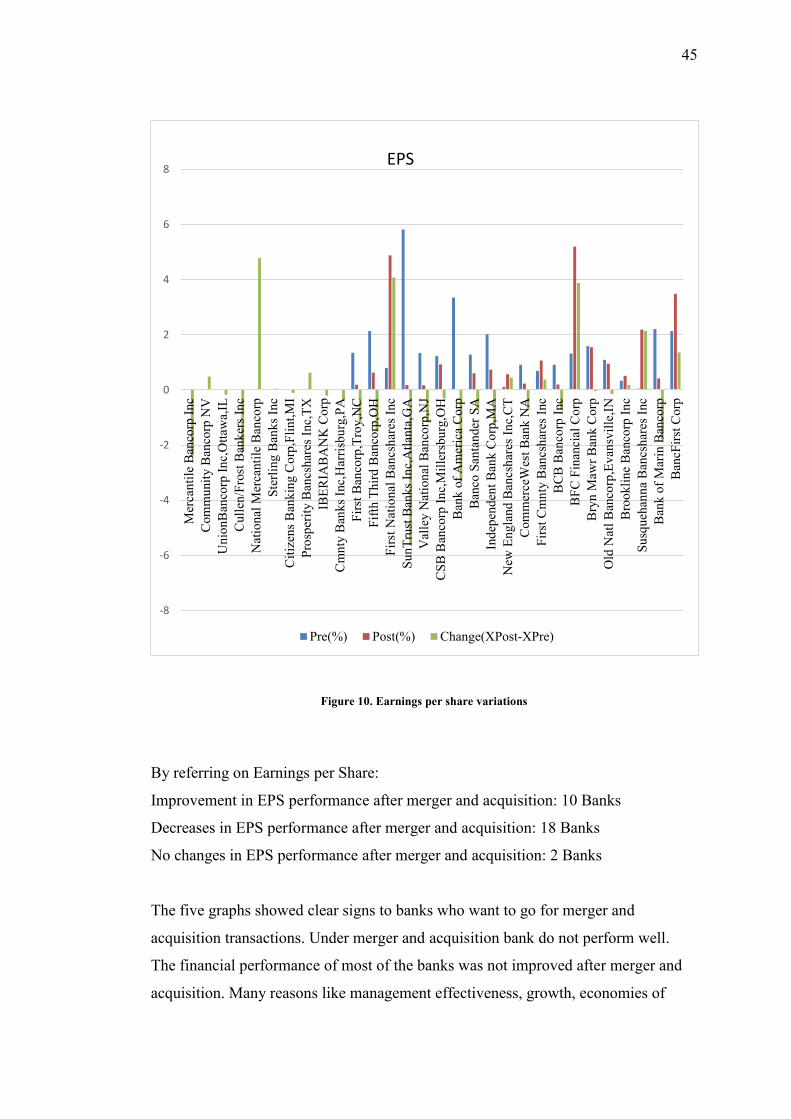

Figure 10. Earnings per share variations

By referring on Earnings per Share:

Improvement in EPS performance after merger and acquisition: 10 Banks

Decreases in EPS performance after merger and acquisition: 18 Banks

No changes in EPS performance after merger and acquisition: 2 Banks

The five graphs showed clear signs to banks who want to go for merger and

acquisition transactions. Under merger and acquisition bank do not perform well.

The financial performance of most of the banks was not improved after merger and

acquisition. Many reasons like management effectiveness, growth, economies of

-8

-6

-4

-2

0

2

4

6

8M

erca

nti

le B

anco

rp I

nc

Com

mu

nit

y B

anco

rp N

V

Un

ionB

anco

rp I

nc,

Ott

awa,

IL

Cull

en/F

rost

Ban

ker

s In

c

Nat

ion

al M

erca

nti

le B

anco

rp

Ste

rlin

g B

ank

s In

c

Cit

izen

s B

ank

ing C

orp

,Fli

nt,

MI

Pro

sper

ity

Ban

csh

ares

Inc,

TX

IBE

RIA

BA

NK

Co

rp

Cm

nty

Ban

ks

Inc,

Har

risb

urg

,PA

Fir

st B

anco

rp,T

roy

,NC

Fif

th T

hir

d B

anco

rp,O

H

Fir

st N

atio

nal

Ban

csh

ares

Inc

Su

nT

rust

Ban

ks

Inc,

Atl

anta

,GA

Val

ley N

atio

nal

Ban

corp

,NJ

CS

B B

anco

rp I

nc,

Mil

lers

bu

rg,O

H

Ban

k o

f A

mer

ica

Co

rp

Ban

co S

anta

nder

SA

Ind

epen

den

t B

ank

Co

rp,M

A

New

En

gla

nd

Ban

csh

ares

In

c,C

T

Com

mer

ceW

est

Ban

k N

A

Fir

st C

mn

ty B

ancs

har

es I

nc

BC

B B

anco

rp I

nc

BF

C F

inan

cial

Co

rp

Bry

n M

awr

Ban

k C

orp

Old

Nat

l B

anco

rp,E

van

svil

le,I

N

Bro

okli

ne

Ban

corp

In

c

Su

squ

ehan

na

Ban

csh

ares

Inc

Ban

k o

f M

arin

Ban

corp

Ban

cFir

st C

orp

EPS

Pre(%) Post(%) Change(XPost-XPre)

46

scale, diversification were quoted to support merger and acquisition proposals. Some

of those reasons showed to be reasonable and in favor of value creation. Some

reasons can be stated to explain the failure in merger and acquisition to improve the

financial performance of other banks. The failure to reduce the costs, financial crisis

or the fact that investors or other customers were unware about merger and

acquisition strategies.

47

6. Conclusion

Theoretically it is needed to adopt the strategy of mergers and acquisitions to compete

in a dynamical business environment. Many researchers worked on the mergers and

acquisitions to determine their impact on corporate sectors in USA. Houston et Al

(2001) showed that in USA banking sector the financial performance increased after

merger and acquisition regarding their productivity, profitability and shareholder’s

value. While other studies such as Robert M Adams (2012) found that mergers and

acquisitions are far from having proved their economics effectiveness and there is no

increase in financial performance of banks after mergers and acquisitions.

The study attempted to assess the effect of merger and acquisition on the performance

of selected bidder bank in USA. The result showed no changes in financial

performance leading to no improvements in financial efficiency. This was indent with

the Wilcoxon signed-rank test statistic results of the sewn selected banks as contained

in the R studio output depicted. On the given evidence of the studied variable we are

not in position to accept alternative hypothesis for return on assets, return on equity,

capital ratio, earnings per share and liabilities to assets ratio. So we have to accept the

null hypothesis because their P value are insignificant i.e. (0.5104; 0.6263; 0.0961;

0.2988; 0.7892) respectively. All these values are compared at 5% significance level.

From above analysis we infer that the purpose of the merger and acquisition in

improving performance is not properly achieved for those banks. The obtained results

tend to confirm opinion of Beitel et AL (2003) that there is little empirical evidence of

mergers and acquisitions to achieve growth or important performance gains.