Yfi t tYear of investment - Welcome to Investor AB · > Yfi t tYear of investment: 2008 > Share of...

10

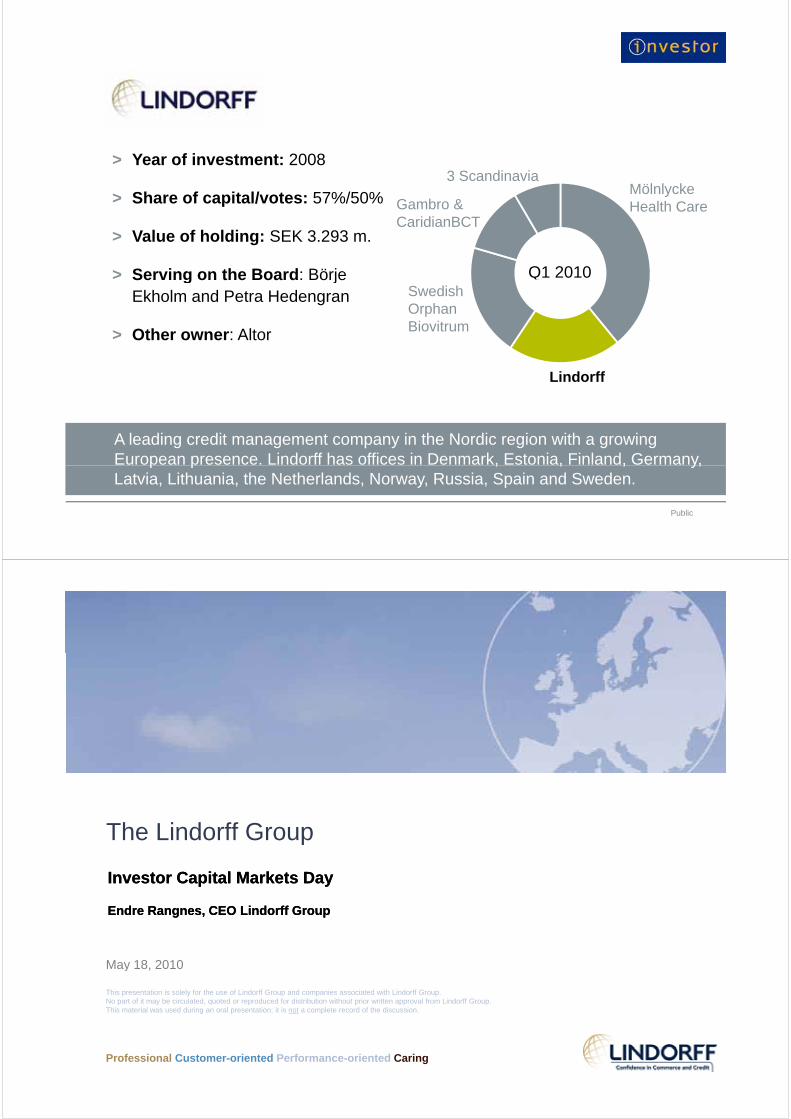

> Y fi t t 2008 > Y ear of investment: 2008 > Share of capital/votes: 57%/50% Mölnlycke Health Care Gambro & C idi BCT 3 Scandinavia > Value of holding: SEK 3.293 m. > Serving on the Board: Börje Q1 2010 CaridianBCT Serving on the Board: Börje Ekholm and Petra Hedengran > Other owner: Altor Swedish Orphan Biovitrum Lindorff A leading credit management company in the Nordic region with a growing European presence. Lindorff has offices in Denmark, Estonia, Finland, Germany, Public Latvia, Lithuania, the Netherlands, Norway, Russia, Spain and Sweden. The Lindorff Group The Lindorff Group Investor Capital Markets Day Investor Capital Markets Day May 18 2010 Endre Rangnes, CEO Lindorff Group Endre Rangnes, CEO Lindorff Group This presentation is solely for the use of Lindorff Group and companies associated with Lindorff Group. No part of it may be circulated, quoted or reproduced for distribution without prior written approval from Lindorff Group. This material was used during an oral presentation; it is not a complete record of the discussion. May 18, 2010 Professional Customer-oriented Performance-oriented Caring

Transcript of Yfi t tYear of investment - Welcome to Investor AB · > Yfi t tYear of investment: 2008 > Share of...

> Y f i t t 2008> Year of investment: 2008

> Share of capital/votes: 57%/50%Mölnlycke Health CareGambro &

C idi BCT

3 Scandinavia

> Value of holding: SEK 3.293 m.

> Serving on the Board: Börje Q1 2010

CaridianBCT

Serving on the Board: BörjeEkholm and Petra Hedengran

> Other owner: Altor

Swedish Orphan Biovitrum

Lindorff

A leading credit management company in the Nordic region with a growing European presence. Lindorff has offices in Denmark, Estonia, Finland, Germany,

Public

p p , , , y,Latvia, Lithuania, the Netherlands, Norway, Russia, Spain and Sweden.

The Lindorff GroupThe Lindorff Group

Investor Capital Markets DayInvestor Capital Markets Day

May 18 2010

Endre Rangnes, CEO Lindorff GroupEndre Rangnes, CEO Lindorff Group

This presentation is solely for the use of Lindorff Group and companies associated with Lindorff Group. No part of it may be circulated, quoted or reproduced for distribution without prior written approval from Lindorff Group. This material was used during an oral presentation; it is not a complete record of the discussion.

May 18, 2010

Professional Customer-oriented Performance-oriented Caring

Agenda

The Lindorff storyThe Lindorff story

Financial results

Key Initiatives for 2010

3

The Lindorff Group

Li d ff A l di E id f d btLindorff; A leading European provider of debt-related administrative services

Net revenues; € 283 (IFRS) million in 2009

2200 employees in Norway, Finland, Sweden, Denmark, Estonia, Latvia, Lithuania, Russia, The Netherlands Germany and SpainNetherlands, Germany and Spain

Owners; Altor Equity Fund (50%), Investor AB (50%)

M i I d t iMain Industries: Financial institutions, Insurance, Telecom & Utilities, Retail and SME.

4

Lindorff; A Nordic market leader with growing international footprint...

•Norway•Norway

##

•Norway

#

No 1 or 2 market position

New market entries, in build up• #1 Debt collection and

support services• Market share 35%

• #1 Debt collection and support services

• Market share 35%

• #1 Debt collection and support services

• Market share 35%•Finland•Finland

• #1 Debt collection services• Market share 41%• #1 Debt collection services• Market share 41%

•Finland

• #1 Debt collection services• Market share 41%

•Sweden•Sweden•Sweden

•Russia•Russia

• Debt collection servicesN k t t

• Debt collection servicesN k t t

•Russia

• Debt collection servicesN k t t

Market share 41%Market share 41%Market share 41%• #1-2 Debt collection and

support services• Market share 18%

• #1-2 Debt collection and support services

• Market share 18%

• #1-2 Debt collection and support services

• Market share 18%

•Denmark•Denmark•Denmark

• New market entry• New market entry• New market entry

•Baltic•Baltic

• #1 Debt collection services• #1 Debt collection services

•Baltic

• #1 Debt collection services

• #2 Debt collection and support services

• Market share 10%

• #2 Debt collection and support services

• Market share 10%

• #2 Debt collection and support services

• Market share 10%

•Netherlands•Netherlands•Netherlands

•Germany•Germany

• Debt collection services• Debt collection services

•Germany

• Debt collection services

• Market share 36%• Market share 36%• Market share 36%• #2 Debt collection and

support services• Market share 15%

• #2 Debt collection and support services

• Market share 15%

• #2 Debt collection and support services

• Market share 15%

S iS iS i • New market entry• Market share 1%• New market entry• Market share 1%• New market entry• Market share 1%

•Spain•Spain

• Debt collection services• New market entry• Debt collection services• New market entry

•Spain

• Debt collection services• New market entry

5 Note: Market share is defined by revenues from 3rd party collection and purchased debtSource: Lindorff

From a Norwegian to a European company

SpainLaunched second greenfield operation for LindorffAdded Aktiv Kapital operation

2009

2008foo

tpri

nt

Spain Added Aktiv Kapital operation

RussiaInvestor AB

First greenfield start up for Lindorff GroupInvestor AB takes 50% share in Lindorff Group

2008

The Entry into Continental Europe

2007

Eu

rop

ean

f

GermanyAcquisition of Dausend Group and Aktiv InkassoEstablished position in Europe’s largest NPL market

Netherlandsy p

Acquisition of Transfair

MatchBroadened the product and service

h i th h i h t f d t

2005

er

Sweden Large portfolio acquisitionsOutsourcing of entire bank internal units

2003

Match chain through enrichment of data

2005

No

rdic

lea

de

Lindorff

Finland Acquisition of Contant

2003

2003

Bu

ildin

g t

he

Lindorff acquired by Altor Equity Partners in NorwayLindorff -Norway

B

...a full range of products and services...

Portfolio

acquisition

Credit Invoicingservices

Debt collection

---------------

Pre-legal / Legal

Surveillance & recovery

q

edit Credit information

Scoring and credit ces Invoicing Services

A/R management egal Reminder services

Customer recovery ce &

ve

ry Surveillance and recovery ti

on Acquisition of

whole portfolios

Cre Scoring and credit

CRM solutions

Data quality

Solutions

voic

ing

Ser

vi A/R management

Loan administration

Accounting

Consumer services

Co

llec

tio

n /

Le Customer recovery

Pre-legal collection:

•Phone•Letter•Street collectionLegal collection:

Su

rvei

llan

cR

eco

v

Debt reconstructuring

Debt recovery

tfo

lio

acq

uis

it whole portfolios

Financing/factoring

Inv

Deb

t C Legal collection:

•Bailiff•Salary deductions

Po

rt

7

Purchased debt from Financial institutions is important for revenue and profit growth

European receivables management revenue and profit poolEuropean receivables management revenue and profit pool

~51%

Revenue and profit pool (as % of total EUR millions)

Financialservices ~68%

~26%

~14%

Revenue

EBITA

Revenue EBITARevenue EBITA

Trade ~8%

~10%

EBITARevenue

~15%

Revenue

~9%

EBITA

3rd party collection Portfolio acquisition

EBITARevenue Revenue EBITA

8

Key European players

Financialservices

Cabot1st Credit

Lindorff has a unique competitive position

The only large collection company with a strong position in bank/finance

Substantial share of Nordic bank’s outsourced debt collection

Strong track record within telecom, utilities, retail and public sector

Extraordinary reputation and strong track

Trade

Extraordinary reputation and strong track record of handling debtors in a highly professional manner

Portfolioacquisition

3rd party collection

9 Source: Company reports; Lindorff; McKinsey analysis

Strategic Intent

Overview of selected public collection companies

NordicPortfolio Rec.

- 5 companies considered comparable to Lindorff

Topline(1)

CAGR2006-2009

USA

Nordic

Encore capital

Intrum Justitia

Lindorff Group

Size = Revenues(2009 revenues)

Lindorff Group

Asset Acceptance

Aktiv Kapital

10

2009 EBITdA margin(2)

(1) Growth in gross collection(2) EBITdA margin = EBITDA excluding portfolio depreciation and write-offs / Gross collections

Good underlying growth in the number of debt collection cases- example Norway and Sweden

Signficant increase in the number of t ll ti i N

...and the Swedish bailiff system h i il th

’000 cases

’000 cases

cases to collection in Norway...

Norway1

has seen similar growth

Sweden2

(1) Number of cases to legal collection, The Financial supervisory board of Norway

I. Credit overhang

II. Increased outsourcing

11

Financial supervisory board of Norway(2)Number of cases received by the Swedish Bailiff System (source) III. Increased market effectiveness

Our strategy

Competitive Advantage Market Participation Objectives & Plan of Actions

Export the Lindorff business

GeographyFull European coverageDrive market consolidation

Operational Capabilities

Extensive Product Range

Competitive Advantage Market Participation Objectives & Plan of Actions

pmodel to Europe

Operational Capabilities

Cross-Border Innovation

BPO Experience

CustomersBank, Finance, InsuranceTelecom/UtilitiesRetail/Public Sector

Grow in established markets

BPO Experience

Reputation & Brand Equity ProductsComprehensive ORM value chain

SME

Continuous operational

chain Leverage cross-product synergiesCustomer-driven innovationBPO

Integrated Mgmt Platform

I t ti l C t B

Complementary Assets

pimprovementPricing

Premium pricing for superior value

International Customer Base

Access to Capital

Agenda

Th Li d ff tThe Lindorff story

Financial results

Key Initiatives for 2010

13

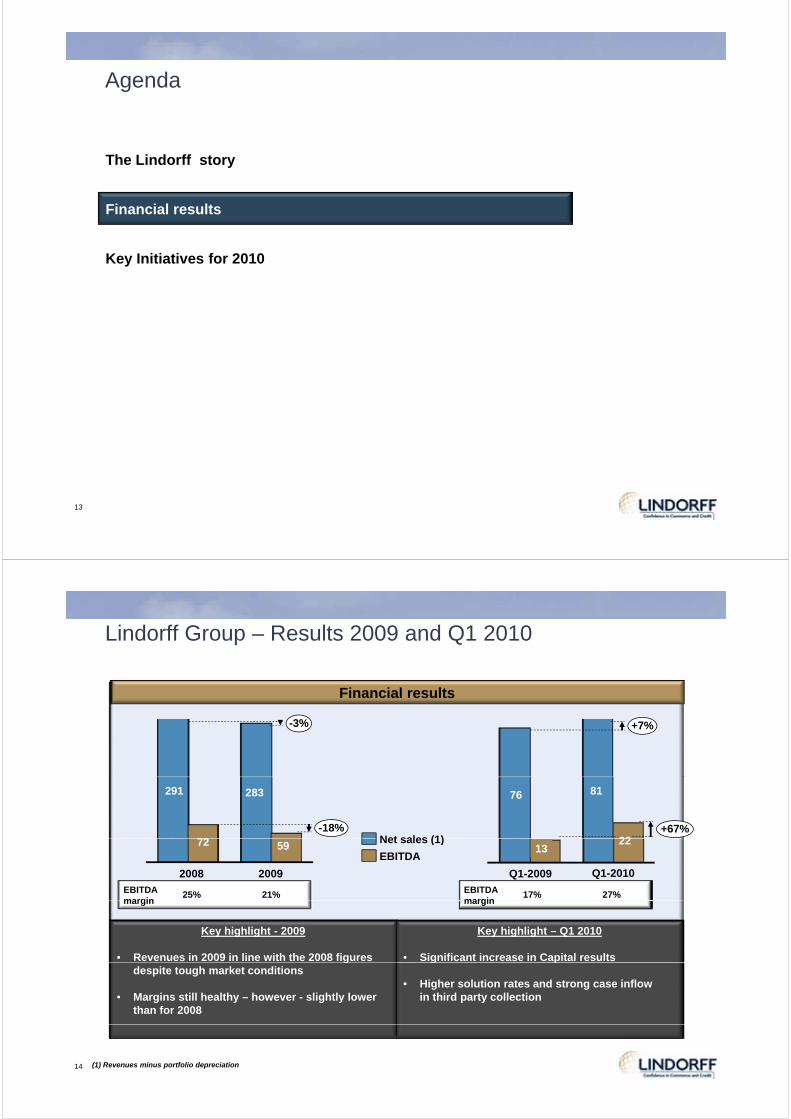

Lindorff Group – Results 2009 and Q1 2010

Financial results

-3% +7%

283291

72-18%

Net sales (1) 22

8176

+67%

5972

20092008

Net sales (1)

EBITDA

EBITDAmargin

25% 21%

Q1-2010

22

Q1-2009

13

EBITDAmargin

17% 27%

Key highlight - 2009

• Revenues in 2009 in line with the 2008 figures

margin margin

Key highlight – Q1 2010

• Significant increase in Capital resultsgdespite tough market conditions

• Margins still healthy – however - slightly lower than for 2008

g p

• Higher solution rates and strong case inflow in third party collection

14 (1) Revenues minus portfolio depreciation

Significant growth in the number of new collection cases and a solid build-up of collection fees in stock

# cases ’000 30% Increase in case volume from 2008-2009

ILLUSTRATIVE EXAMPLE –NORWAY

800

600

1.000

2008

2009

2010

400

200

0

AugJulJunMayAprMarFebJan DecNovOctSep

1,30

BNOK15 % Increase in the stock of collection fees in the last 26 months

1,25

1,20 +15%

1,15

0,00Nov 08

Oct 08

Sep 08

Aug 08

Jul 08

Jun 08

May 08

Apr 08

Mar 08

Jan 08

Jan 10

,Feb 08

Feb 10

Dec 09

Nov 09

Oct 09

Sep 09

Aug 09

Jul 09

Jun 09

May 09

Apr 09

Mar 09

Feb 09

Jan 09

Dec 08

Lindorff Group – Results 2009

Scandinavia 52%*%

ECE 22%*

50,3% 49,4%

uti

on

even

ue

dis

trib

u

Continental Europe 20%*

50,6%49,7%

Re

2009

2008 Revenues Capital

Revenues 3PC

* As percentage of total Group revenues

16

Agenda

Th Li d ff tThe Lindorff story

Financial results

Key Initiatives for 2010

17

Key initiatives for 2010

• Initiatives for organic and M&A• Initiatives for organic and M&A• Initiatives for organic and M&A growth

• Initiatives for organic and M&A growthGrowth

• Initiatives targeting operational efficiency and effectiveness

• Initiatives targeting operational efficiency and effectivenessMargin improvements

• Strengthening of systems and organization to deliver on financial and operational targets

• Strengthening of systems and organization to deliver on financial and operational targets

Platform improvements

Summary

Huge opportunities to build a profitable ... we are well-positionedg pp pbusiness...

• Huge amounts of NPLs in 2009

... we are well positioned

• Ability to deliver on the entire value chain

• Increased pressure for FI to sell portfolios

• Increased collection volumes

• Increased readiness to outsource

• Successfully built portfolio acquisition business

• Exceptional track record in Nordic FI Increased readiness to outsource segment

• Secured funding and strong owners

19