Year-End Report 2019 - Investor AB€¦ · partly driven by higher sales and marketing expenses....

34

Year-End Report 2019 Johan Forssell, CEO Helena Saxon, CFO 1

Transcript of Year-End Report 2019 - Investor AB€¦ · partly driven by higher sales and marketing expenses....

Year-End Report 2019Johan Forssell, CEOHelena Saxon, CFO

1

2

2019 Global Economy

3

XXTotal avkastning 2019

XXTSR Marknaden

40%Total Shareholder Return, 2019

Investor AB

35%Total Shareholder Return, 2019

SIXRX

4

XXTotal avkastning 2019

XXTSR Marknaden

13%2019 sales growth, of which 4%

organic in constant currency, in major subsidiaries

18%2019 EBITA growth in major subsidiaries

5

Key activities in 2019

Electroluxproposal to list Professional

Strategicacquisitions In Laborie and

Piab

ABB SEK 4.3bn invested

PeopleSeveral new CEOs and

board members

EQT AB listed on NASDAQ Stockholm

Cash flow Strong

contribution from all

business areas

6

XXTotal avkastning 2019

XXTSR Marknaden

0

2

4

6

8

10

12

14

16

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019p

DPS

+ 8% Pay a steadily rising dividend

7

Q4 2019 Highlights

6%Adjusted NAV

growth(SIXRX +10%)

6%Adjusted EBITA growth in major

subsidiaries

Strategicacquisitions In Laborie and

Piab

ABB SEK 1.0bn invested

7%TSR

(SIXRX +10%)

Patricia Industries

8

9

Patricia Industries – development in Q4 2019

-3% - Earnings growth and good cash flow impacted positively

- However, multiple contraction and currency impacted negatively

value change (excl. cash)

Patricia Industries – value change (excluding cash), 2019

10

23% Value change 2019

>2/3 driven by earnings growth & cash flow

<1/3driven by multiples

Patricia Industries – operational development Q4 2019

2 percent organic sales growth, %

11

VecturaGrand Group

SarnovaMölnlyckeLaborie BraunAbility

Permobil

-2%

8%

Piab

4%

8%

5%

3%

1%

-9%

23%of tot. adjusted assets

115SEK bn

3% Reported EBITA

growth

6%Adjusted EBITA

growth

12

A provider of advanced products for treatment and prevention of wounds and single-use surgical solutions

Q4 2019

• Organic sales growth +1 percent in constant currency• Wound Care +1 percent• Surgical +2 percent driven by Surgical Trays

and Antiseptics

• All regions relatively flat, Emerging Markets grew faster than the group, but slower than previously in 2019

• EBITA margin essentially flat

• Strong cash flow, EUR 243m distributed to Patricia Industries IFRS 16 implemented as of the first quarter 2019

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

350

400

450

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%EUR m.

Sales EBITDA, % EBITA, %

13

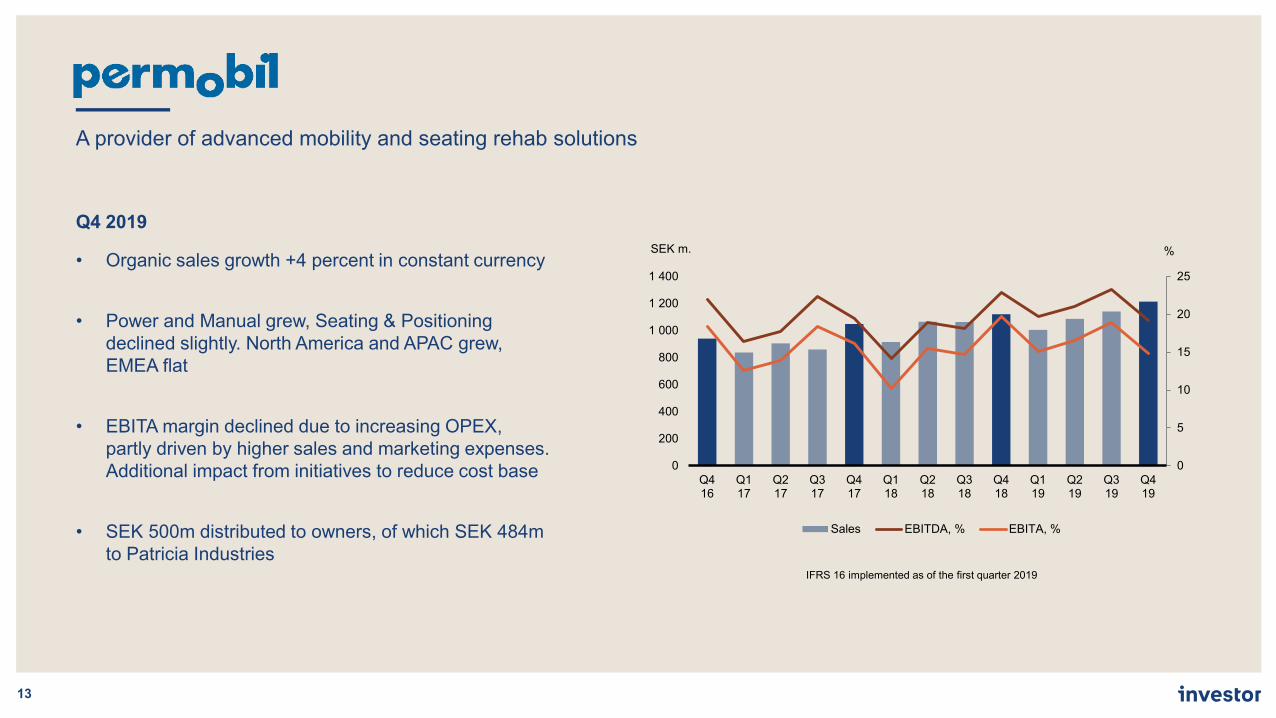

A provider of advanced mobility and seating rehab solutions

Q4 2019

• Organic sales growth +4 percent in constant currency

• Power and Manual grew, Seating & Positioning declined slightly. North America and APAC grew, EMEA flat

• EBITA margin declined due to increasing OPEX, partly driven by higher sales and marketing expenses. Additional impact from initiatives to reduce cost base

• SEK 500m distributed to owners, of which SEK 484m to Patricia Industries

IFRS 16 implemented as of the first quarter 2019

0

5

10

15

20

25

0

200

400

600

800

1 000

1 200

1 400

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%SEK m.

Sales EBITDA, % EBITA, %

14

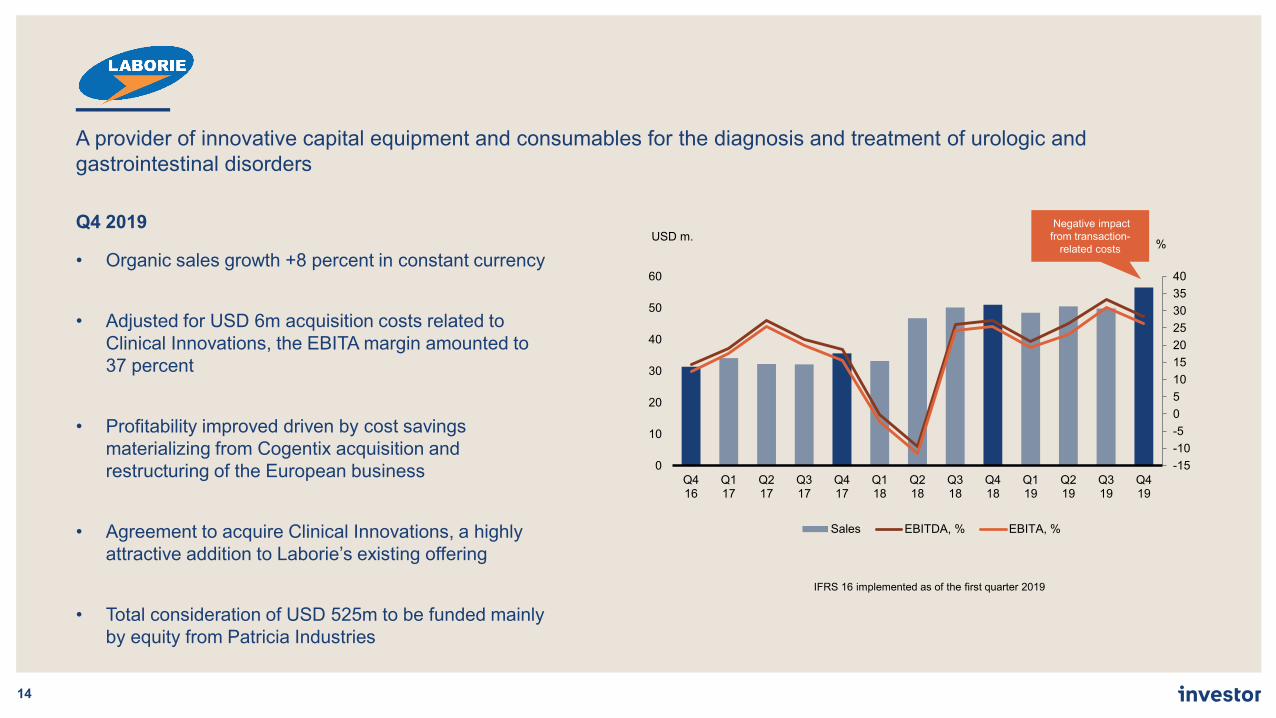

A provider of innovative capital equipment and consumables for the diagnosis and treatment of urologic and gastrointestinal disorders

Q4 2019

• Organic sales growth +8 percent in constant currency

• Adjusted for USD 6m acquisition costs related to Clinical Innovations, the EBITA margin amounted to 37 percent

• Profitability improved driven by cost savings materializing from Cogentix acquisition and restructuring of the European business

• Agreement to acquire Clinical Innovations, a highly attractive addition to Laborie’s existing offering

• Total consideration of USD 525m to be funded mainly by equity from Patricia Industries

IFRS 16 implemented as of the first quarter 2019

-15-10-50510152025303540

0

10

20

30

40

50

60

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%USD m.

Sales EBITDA, % EBITA, %

Negative impact from transaction-

related costs

Laborie - Clinical Innovations

15

• Provider of single-use products for hospital labor & delivery and neonatal intensive care units

• Market-leading positions in segments with favorable long-term growth dynamics

• High-risk births expected to increase• Under-penetration in Emerging Markets

• 2019 sales estimated at USD 70m

• Good organic growth, strong profitability and cash conversion

16

A manufacturer of wheelchair accessible vehicles and wheelchair lifts

Q4 2019

• Organic sales growth +5 percent in constant currency

• Strong growth in Commercial WAVs, good growth in Consumer WAVs, Lifts down slightly

• EBITA margin improved, driven by operating efficiency improvements and supply chain optimization initiatives

• Strong cash flow driven by good management of working capital

IFRS 16 implemented as of the first quarter 2019

0

2

4

6

8

10

12

0

50

100

150

200

250

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%USD m.

Sales EBITDA, % EBITA, %

17

A provider of gripping and moving solutions for automated manufacturing and logistics processes

Q4 2019

• Organic sales growth -9 percent in constant currency

• Americas grew slightly, Europe and APAC declined. Moderate growth in Vacuum Automation, all other divisions declined. Largest decline in Robotic Gripping

• Adjusted for SEK 9m in transaction costs related to the acquisition of TAWI Group, the adjusted EBITA margin amounted to 24 percent. Profitability declined mainly due to lower sales

• Acquisition of TAWI Group adds more than 25 percent to group sales and makes Piab a world leader within Ergonomic Handling

IFRS 16 implemented as of the first quarter 2019

0

5

10

15

20

25

30

35

40

0

50

100

150

200

250

300

350

400

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%SEK m.

Sales EBITDA, % EBITA, %

Negative impact from transaction-

related costs

Piab – TAWI Group

18

• TAWI - a leading manufacturer of smart lifting solutions with global reach

• SEK 350m sales in 2019 with good profitability

• Strong sales growth and profitability

• E-commerce logistics one of several key growth drivers

19

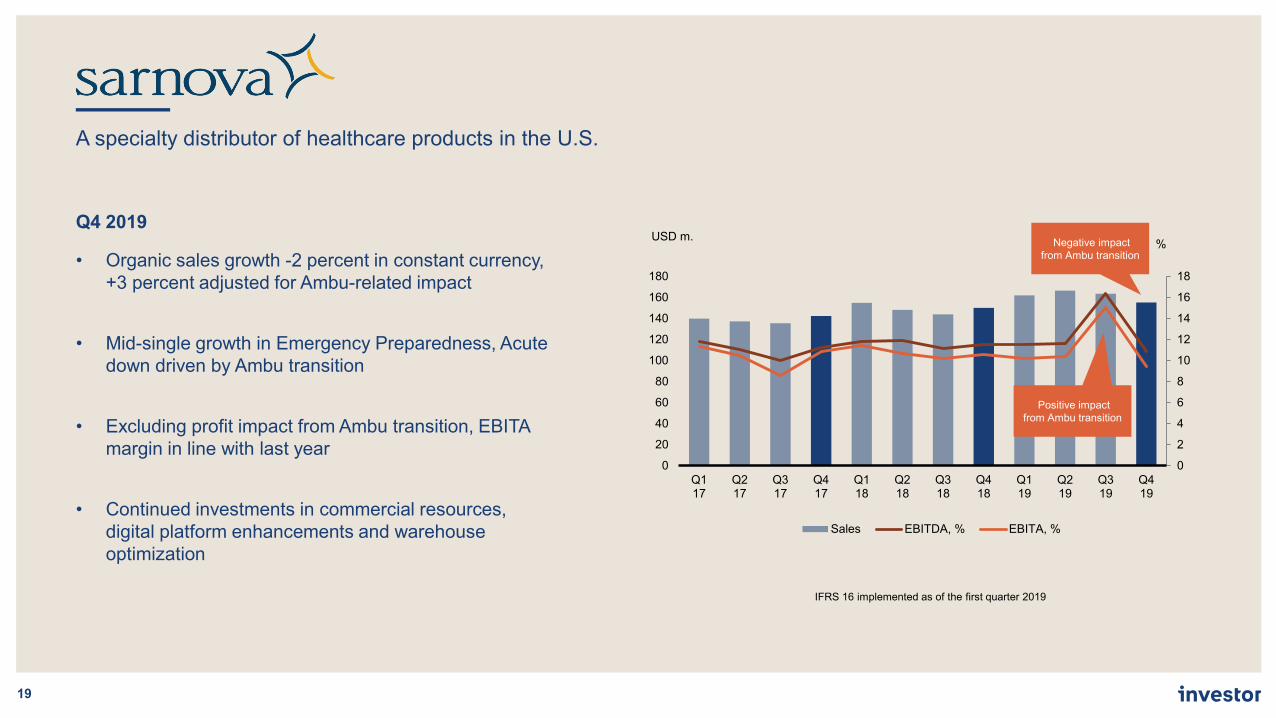

A specialty distributor of healthcare products in the U.S.

Q4 2019

• Organic sales growth -2 percent in constant currency, +3 percent adjusted for Ambu-related impact

• Mid-single growth in Emergency Preparedness, Acute down driven by Ambu transition

• Excluding profit impact from Ambu transition, EBITA margin in line with last year

• Continued investments in commercial resources, digital platform enhancements and warehouse optimization

IFRS 16 implemented as of the first quarter 2019

0

2

4

6

8

10

12

14

16

18

0

20

40

60

80

100

120

140

160

180

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%USD m.

Sales EBITDA, % EBITA, %

Negative impact from Ambu transition

Positive impact from Ambu transition

20

A provider of mobile voice and broadband services in Sweden and Denmark

Q4 2019

• Subscription base +53,000

• Service revenue +5 percent excluding previously communicated Swedish VAT ruling

• Excl. IFRS 16, Swedish VAT ruling and a non-recurring expense related to a group strategy project last year, EBITDA +8 percent

IFRS 16 implemented as of the first quarter 2019

-30

-20

-10

0

10

20

30

40

50

0

500

1 000

1 500

2 000

2 500

3 000

3 500

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

%SEK m.

Sales EBITDA reported, %

Negative impact from VAT rulings

Negative impact from VAT rulings

Investments in EQT

21

Investments in EQT

22

7%of tot. adjusted assets

37SEK bn

11%Total value change constant currency (9% reported) 2.7

SEK bnNet cash flow Q4

24%Total Return EQT AB

1%Value change, constant currency, investments in

EQT funds

0

5

10

15

20

25

30

35

40

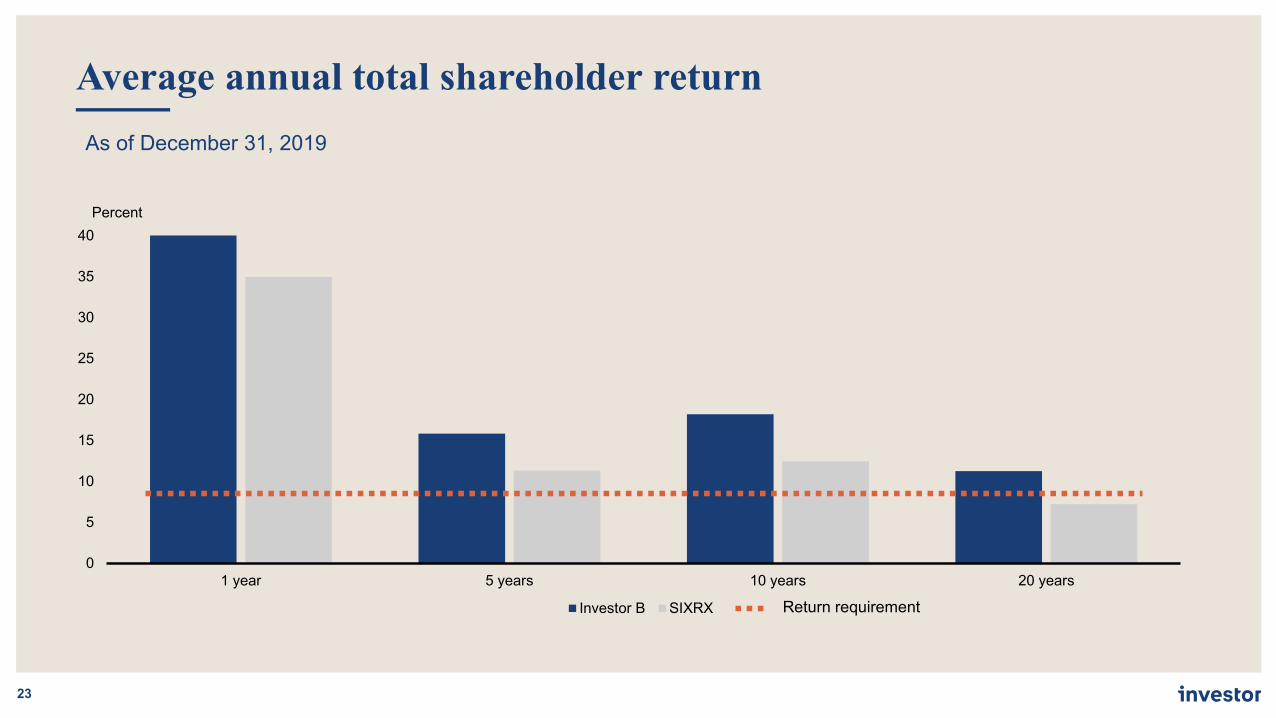

1 year 5 years 10 years 20 years

Percent

Investor B SIXRX

23

Average annual total shareholder returnAs of December 31, 2019

Return requirement

Year-End Report 2019Helena Saxon, CFO

24

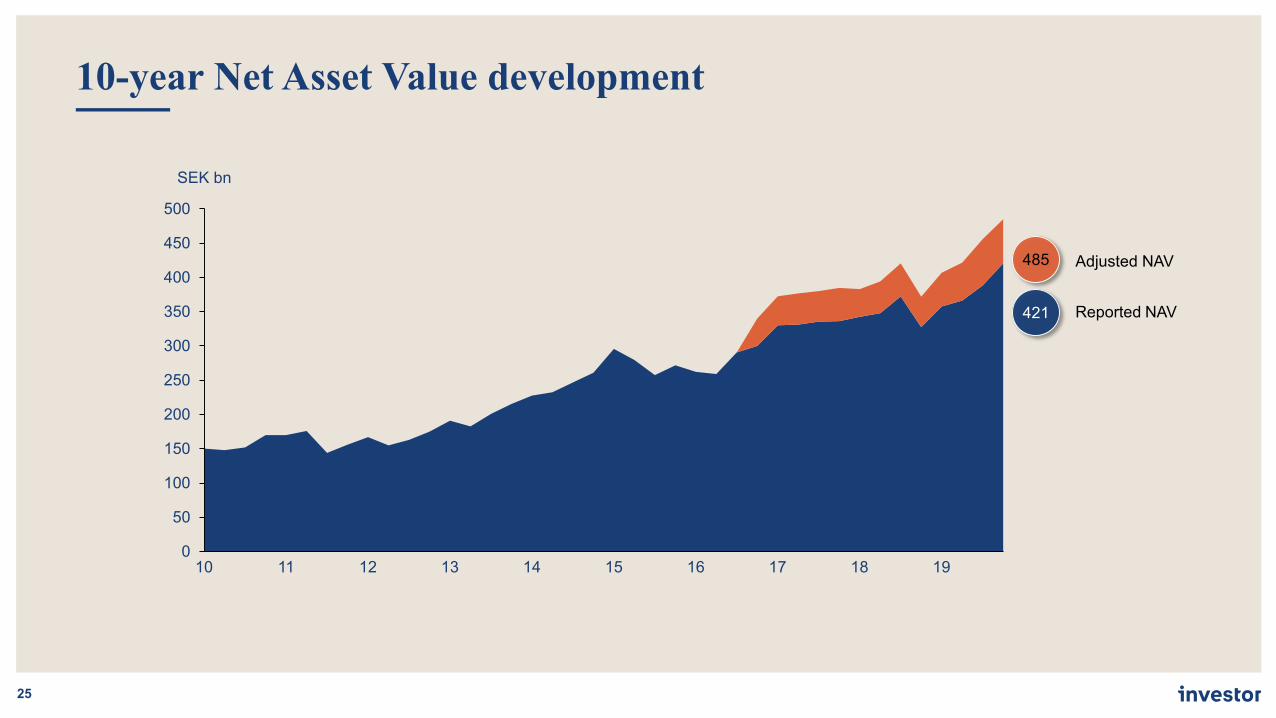

10-year Net Asset Value development

25

0

50

100

150

200

250

300

350

400

450

500

13

SEK bn

1410 11 12 15 16 17 18 19

421

485

Reported NAV

Adjusted NAV

Listed Companies

26

Q4 2019 Summary

• Total contribution to NAV SEK 30bn• Listed Companies TSR 9%, SIXRX 10%

Atlas Copco 22%

ABB 17%

AstraZeneca 14%

SEB 12%

Epiroc 7%

Ericsson 6%

Nasdaq 6%

Sobi 5%

Saab 4%Electrolux 3%

Wärtsilä 3% Husqvarna 2%

-10

-5

0

5

10

15

20

25

10

0

-2

2

8

4

6

12

16

14

6.9

1.9

%

Elec

trolu

x

QTD, SEK bn

Atla

s C

opco

16.6

-6.2

Nas

daq

Astra

Zene

ca

Epiro

c

Saab

Eric

sson

Sobi

Hus

qvar

na

Wär

tsilä

SEB

24.3

2.9

9.111.5

6.2

1.90.0

-3.0

ABB

Contribution to NAV TSR

69%of tot. adjusted assets

345SEK bn

Patricia Industries – value change (excluding cash), Q4 2019

27

MultiplesPerformance and cash flow

-6

-3

FX + other Net increase/decrease

5

-4

SEK bn

Q4 growth

-3%

Patricia Industries – change in Estimated Market Values

28

Q4 2019 Summary Estimated market value change

-3%value

decreaseexcl. cash

1 667 1 368 629 80

(682) (277) (208)

(2 000)

6 494

MölnlyckeThree Scandinavia

Financial Investments

Sarnova Aleris exit proceeds

(2 142)

Grand Group

Total NAV Dec 2019

LaborieTotal NAV Sept 2019

136 381

PemobilVectura

(7 328)(1 534)

140 313

BraunAbilityPiab Patricia Cash

Distributions/proceeds

Major Drivers of Estimated Market Values Q4 2019

29

SEK -7.3bn Lower multiples, currency impacted negatively, partly offset by cash flow. SEK 2.6bn distribution

CompanyEst. market value

change Q4 2019 vs. Q3 2019

Major drivers

SEK +1.7bn Higher profit, multiples impacted positively

SEK -0.3bn Strong earnings growth impacted positively, lower multiples and currency impacted negatively

SEK +0.7bn First time at estimated market values. Sarnovaimpacted positively, Piab impacted negatively

SEK -1.5bn Lower multiples, profit impacted negatively, partly offset by cash flow. SEK 0.5bn distribution

Financial Investments

30

Q4 2019 Summary

• The realization of the portfolio continues

• SEK 1.6bn cash proceeds received from exits of NS Focus, HireVue and Acquia

Five largest financial investments, December 31, 2019

~4.3SEK bnValue

December 31, 2019

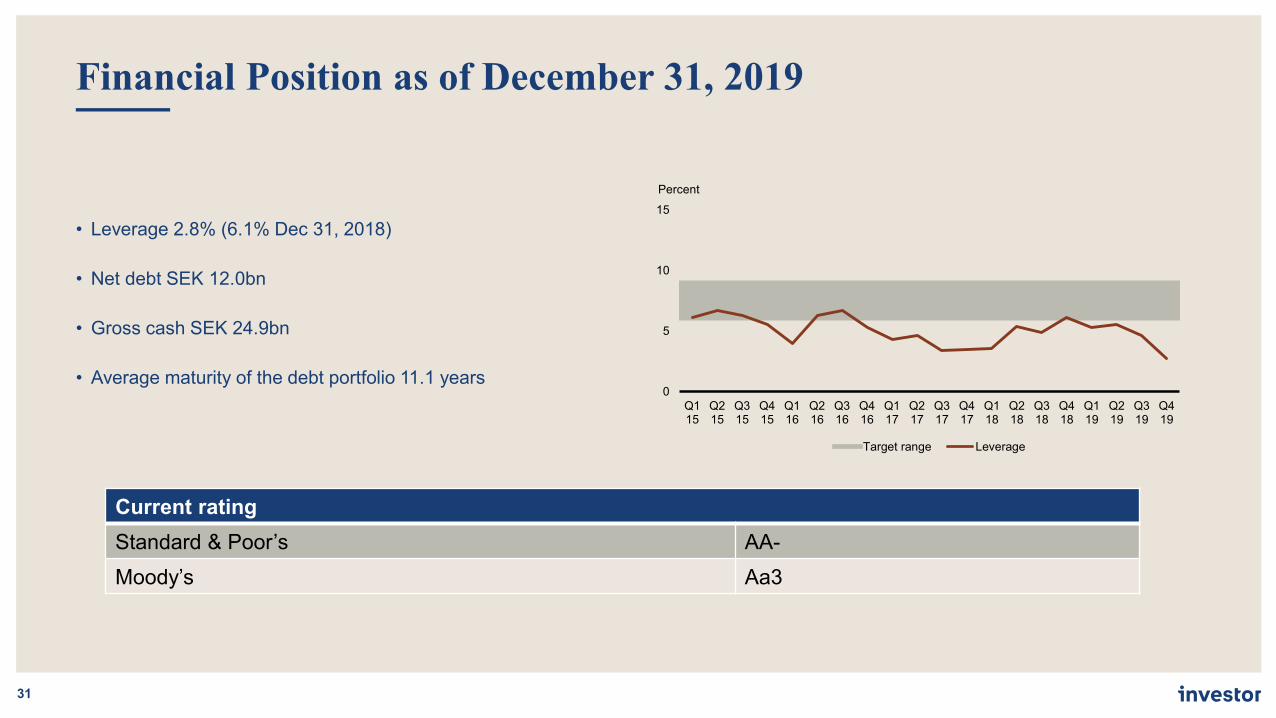

Financial Position as of December 31, 2019

31

• Leverage 2.8% (6.1% Dec 31, 2018)

• Net debt SEK 12.0bn

• Gross cash SEK 24.9bn

• Average maturity of the debt portfolio 11.1 years

Current ratingStandard & Poor’s AA-Moody’s Aa3

0

5

10

15

Q115

Q215

Q315

Q415

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Percent

Target range Leverage

Strong cash flow generation gives great financial flexibility

LISTED COMPANIES

LISTED COMPANIES

DIVIDEND PAID

~77SEK bn

32

Cash flow 2015-2019 Sources Uses

Net debt approximately SEK 8bn lower, leverage down from 7.3 percent to 2.8 percent

Net otherInvestments in EQT

~85SEK bn

*Including divestment of Aleris

We create value for people and society

by buildingstrong and sustainable

businesses

Financial Calendar & Contact Details

34

Event Date

Interim Management Statement January – March 2020 April 22, 2020

Interim Report January – June 2020 July 17, 2020

Interim Management Statement January-September 2020 October 19, 2020

Contact Details

Viveka Hirdman-Ryrberg +46 70 550 3500

Head of Corporate Communication and Sustainability [email protected]

Magnus Dalhammar +46 73 524 2130

Head of Investor Relations [email protected]