WZ Satu - Affin Hwang Capital · 25/05/2017 · WZ Satu (WZS) is an established subcontractor and...

15

25 May 2017 Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 1 of 15 Initiation: Preferred Partner WZ Satu (WZS) is an established subcontractor and partner of choice for Ekovest, IJM Corp and UEM Builders. Its bauxite mining operation was adversely affected by the mining ban imposed by the government but it is still able to export its stockpile. We expect core EPS growth of 70% yoy in FY17, driven by rising earnings from construction and oil & gas services, and stable mining associate earnings in FY17. We initiate coverage on WZS with a BUY call and target price of RM1.52. Core expertise in construction WZS’s core operation is the provision of civil engineering and construction, onshore oil and gas (O&G) services and bright steel manufacturing. Management team has extensive experience in the industry and some were senior managers/directors in Road Builder (merged with IJM Corp) and PATI Sdn Bhd (construction arm of UEM Builders) previously. WZS also manufactures steel components for the O&G and airline industries. Its two associate companies (30-49% stake) are involved in bauxite mining. Growing order book We expect the expansion of its construction and O&G order book to drive a three-year EPS CAGR of 35% in FY16-19. Its order book increased to RM885m at end-FY16 compared to RM768m at end-FY15. Its current order book is RM1.23bn, equivalent to 3.3x FY16 construction and O&G revenue. WZS targeted RM1.2bn orderbook by end-FY17. The game changer for WZS is the potential clinching of the RM4bn Central Spine Road project with its partner UEM Group to expand its order book and move up the value chain to be a main contractor. Sustainable bauxite earnings WZS benefited from the bauxite mining boom in Pahang, which led to its share of associate PAT peaking at RM18.5m (82% of group PAT) in FY15. The ban on bauxite mining since early-2016 led to associate PAT declining 49% yoy to RM9.4m (42% of group PAT) in FY16. WZS has approval to export its stockpile and this should support mining earnings in FY17. Initiate coverage with BUY call We initiate coverage on WZS with a BUY call and TP of RM1.52, on a 10% discount to RNAV. WZS’s current CY18E PER of 13x looks attractive relative to the construction weighted-average PER of 18x. Net dividend yield of 2.5% looks reasonable, supported by its net cash position. Earnings & Valuation Summary FYE 31 Aug 2015 2016 2017E 2018E 2019E Revenue (RMm) 351.4 465.9 510.2 704.1 1,043.6 EBITDA (RMm) 17.7 25.8 43.9 52.3 68.0 Pretax profit (RMm) 26.7 28.0 36.0 46.5 62.3 Net profit (RMm) 22.9 23.1 28.9 37.2 49.9 EPS (sen) 5.2 4.9 6.7 8.2 10.5 EPS growth (%) (44.4) (6.1) 37.6 21.7 28.4 PER (x) 23.0 24.5 17.8 14.6 11.4 Core net profit 25.6 19.8 31.1 37.2 49.9 Core EPS (sen) 5.8 4.2 7.2 8.2 10.5 Core EPS growth (%) (17.6) (26.4) 70.0 13.5 28.4 Core PER (x) 20.8 28.2 16.6 14.6 11.4 Net DPS (sen) 0.0 3.0 3.0 3.0 3.5 Dividend Yield (%) 0.0 2.5 2.5 2.5 2.9 EV/EBITDA (x) 16.9 14.4 8.6 7.2 5.4 ROE (%) 13.1 7.2 10.0 10.6 12.6 ROA (%) 6.9 4.8 5.5 6.1 6.9 Debt to equity ratio (x) 0.3 0.3 0.3 0.3 0.3 BPS (RM) 1.0 0.9 0.9 1.0 1.1 PBR (x) 1.2 1.4 1.3 1.2 1.1 Chg in EPS (%) NA NA NA Affin core/Consensus (x) NA NA NA Source: Company, Affin Hwang estimates Initiation of Coverage WZ Satu WENG MK; WZSATU Listing Market: Main Sector: Construction RM1.20 @ 24 May 2017 KLCI: 1,771 Buy (initiate coverage) Upside: 27% Price Target: RM1.52 Previous Target: na 1,500 1,550 1,600 1,650 1,700 1,750 1,800 1,850 1,900 1,950 0.50 0.70 0.90 1.10 1.30 1.50 1.70 1.90 2.10 2.30 2.50 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 (RM) WENG MK KLCI Price Performance 1M 3M 12M Absolute -2.9% -2.0% -7.7% Rel to KLCI -3.8% -1.8% -5.0% Stock Data Issued shares (m) 348.9 Mkt cap 418.6/97.5 Avg daily vol - 3mth (m) 0.3 52-wk range (RM) 0.97-1.38 Est free float 18.2% BV per share (RM) 0.73 P/BV (x) 1.64 Net cash/ (debt) (RMm) 1.55 ROE 7.2% Beta 0.68 Derivatives Yes (Warr 14/24, WP RM0.765, EP RM0.50) Shariah Compliant Yes Key Shareholders Tengku Dato’ Sri Uzir 27.4% Tan Ching Kee 13.8% Lembaga Tabung Haji 9.7% Ong Lee Veng 7.9% Source: Affin, Bloomberg Loong Chee Wei CFA (603) 2146 7548 [email protected] Cassandra Ooi (603) 2146 7481 [email protected] www.bursamids.com

Transcript of WZ Satu - Affin Hwang Capital · 25/05/2017 · WZ Satu (WZS) is an established subcontractor and...

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 1 of 15

Initiation: Preferred Partner

WZ Satu (WZS) is an established subcontractor and partner of choice

for Ekovest, IJM Corp and UEM Builders. Its bauxite mining operation

was adversely affected by the mining ban imposed by the government

but it is still able to export its stockpile. We expect core EPS growth of

70% yoy in FY17, driven by rising earnings from construction and oil &

gas services, and stable mining associate earnings in FY17. We initiate

coverage on WZS with a BUY call and target price of RM1.52.

Core expertise in construction

WZS’s core operation is the provision of civil engineering and construction,

onshore oil and gas (O&G) services and bright steel manufacturing.

Management team has extensive experience in the industry and some were

senior managers/directors in Road Builder (merged with IJM Corp) and PATI

Sdn Bhd (construction arm of UEM Builders) previously. WZS also

manufactures steel components for the O&G and airline industries. Its two

associate companies (30-49% stake) are involved in bauxite mining.

Growing order book

We expect the expansion of its construction and O&G order book to drive a

three-year EPS CAGR of 35% in FY16-19. Its order book increased to

RM885m at end-FY16 compared to RM768m at end-FY15. Its current order

book is RM1.23bn, equivalent to 3.3x FY16 construction and O&G revenue.

WZS targeted RM1.2bn orderbook by end-FY17. The game changer for WZS

is the potential clinching of the RM4bn Central Spine Road project with its

partner UEM Group to expand its order book and move up the value chain to

be a main contractor.

Sustainable bauxite earnings

WZS benefited from the bauxite mining boom in Pahang, which led to its share

of associate PAT peaking at RM18.5m (82% of group PAT) in FY15. The ban

on bauxite mining since early-2016 led to associate PAT declining 49% yoy to

RM9.4m (42% of group PAT) in FY16. WZS has approval to export its

stockpile and this should support mining earnings in FY17.

Initiate coverage with BUY call

We initiate coverage on WZS with a BUY call and TP of RM1.52, on a 10%

discount to RNAV. WZS’s current CY18E PER of 13x looks attractive relative

to the construction weighted-average PER of 18x. Net dividend yield of 2.5%

looks reasonable, supported by its net cash position.

Earnings & Valuation Summary

FYE 31 Aug 2015 2016 2017E 2018E 2019E Revenue (RMm) 351.4 465.9 510.2 704.1 1,043.6 EBITDA (RMm) 17.7 25.8 43.9 52.3 68.0 Pretax profit (RMm) 26.7 28.0 36.0 46.5 62.3 Net profit (RMm) 22.9 23.1 28.9 37.2 49.9 EPS (sen) 5.2 4.9 6.7 8.2 10.5 EPS growth (%) (44.4) (6.1) 37.6 21.7 28.4 PER (x) 23.0 24.5 17.8 14.6 11.4 Core net profit 25.6 19.8 31.1 37.2 49.9 Core EPS (sen) 5.8 4.2 7.2 8.2 10.5 Core EPS growth (%) (17.6) (26.4) 70.0 13.5 28.4 Core PER (x) 20.8 28.2 16.6 14.6 11.4 Net DPS (sen) 0.0 3.0 3.0 3.0 3.5 Dividend Yield (%) 0.0 2.5 2.5 2.5 2.9 EV/EBITDA (x) 16.9 14.4 8.6 7.2 5.4 ROE (%) 13.1 7.2 10.0 10.6 12.6 ROA (%) 6.9 4.8 5.5 6.1 6.9 Debt to equity ratio (x) 0.3 0.3 0.3 0.3 0.3 BPS (RM) 1.0 0.9 0.9 1.0 1.1 PBR (x) 1.2 1.4 1.3 1.2 1.1

Chg in EPS (%)

NA NA NA Affin core/Consensus (x) NA NA NA

Source: Company, Affin Hwang estimates

Initiation of Coverage

WZ Satu WENG MK; WZSATU Listing Market: Main Sector: Construction

RM1.20 @ 24 May 2017 KLCI: 1,771

Buy (initiate coverage) Upside: 27%

Price Target: RM1.52 Previous Target: na

1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

1,900

1,950

0.50

0.70

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

2.50

May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17

(RM)WENG MK KLCI

Price Performance

1M 3M 12M Absolute -2.9% -2.0% -7.7% Rel to KLCI -3.8% -1.8% -5.0%

Stock Data

Issued shares (m) 348.9 Mkt cap

(RMm)/(US$m)

418.6/97.5 Avg daily vol - 3mth (m) 0.3 52-wk range (RM) 0.97-1.38 Est free float 18.2% BV per share (RM) 0.73 P/BV (x) 1.64 Net cash/ (debt) (RMm)

(2Q17)

1.55 ROE 7.2% Beta 0.68 Derivatives Yes

(Warr 14/24, WP RM0.765, EP RM0.50) Shariah Compliant Yes

Key Shareholders

Tengku Dato’ Sri Uzir 27.4% Tan Ching Kee 13.8% Lembaga Tabung Haji 9.7% Ong Lee Veng 7.9% Source: Affin, Bloomberg

Loong Chee Wei CFA (603) 2146 7548

Cassandra Ooi (603) 2146 7481

www.bursamids.com

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 2 of 15

Focus charts

Fig 1: Segmental pre-tax profit breakdown Fig 2: Pre-tax profit margins

(10)

0

10

20

30

40

50

60

70

2012 2013 2014* 2015 2016 2017F 2018F 2019F

Construction Oil & gas Manufacturing Trading & Investment(RMm)

(10)

(5)

0

5

10

15

20

25

30

35

40

45

2012 2013 2014* 2015 2016 2017F 2018F 2019F

Construction Oil & gas Manufacturing Trading & Investment(%)

Source: Company, Affin Hwang estimates Source: Company, Affin Hwang estimates

Fig 3: EPS growth Fig 4: Dividend per share

(100)

(50)

0

50

100

150

200

250

300

0

2

4

6

8

10

12

2012 2013 2014* 2015 2016 2017F 2018F 2019F

EPS (LHS) EPS growth (RHS)(sen) (%)

0

5

10

15

20

25

30

35

40

45

2.7

2.8

2.9

3.0

3.1

3.2

3.3

3.4

3.5

3.6

2016 2017F 2018F 2019F

DPS (LHS) Dividend payout ratio (RHS)(sen) (%)

Source: Company, Affin Hwang estimates Source: Company, Affin Hwang estimates

Fig 5: EPS sensitivity to key drivers Fig 6: 12-month forward PER

Base case

+RM100m revenue

+1% PAT margin

FY17E EPS (sen) 6.7 8.3 7.9

FY18E EPS (sen) 8.2 9.5 9.7

FY19E EPS (sen) 10.5 11.6 12.7

FY17E EPS chg (%)

23.0 16.7

FY18E EPS chg (%)

15.8 18.1

FY19E EPS chg (%) 10.2 20.2

5

10

15

20

25

30

35

40

201

2

201

3

201

4

201

5

201

6

201

7

+1SD: 24.6x

Avg: 17.4x

-1SD: 10.2x

(x)

Source: Company, Affin Hwang estimates Source: Company, Affin Hwang estimates

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 3 of 15

Core expertise in construction

Acquisitions to diversify operation

WZ Satu acquired WZS KenKeong Sdn Bhd (WZSK) in May 2014, which

is involved in the provision of civil engineering and construction services,

and Misi Setia Oil & Gas Sdn Bhd in October 2014, which is involved in

onshore oil and gas construction. The acquisitions diversified the

company’s operation from manufacturing cold drawn bright steel polished

shaft, which is facing rising cost pressure and stagnant market demand.

Enhanced capabilities through acquisitions

By acquiring WZSK and Misi, the company built up its capabilities in

construction and engineering with the entry of key management personnel

with extensive experience in the industry. For example, Senior Executive

Director/Chief Operating Officer Dato’ IR William Tan, who was the

founder of WZSK, has 36 years of experience in the construction industry

and worked in the Public Works Department and Road Builder previously.

Relationship with Pahang state government

WZS’s Executive Chairman/CEO Tengku Dato’ Sri Uzir bin Tengku Dato’

Ubaidillah was an Executive Director of Tanah Makmur Bhd previously.

His close relationship with Tanah Makmur and the Pahang royalty led to

WZS venturing into bauxite mining through its 49%-owned associate SE

Satu Sdn Bhd and 30%-owned associate SE Satu Pelangi Sdn Bhd.

Fig 7: Directors’ profile

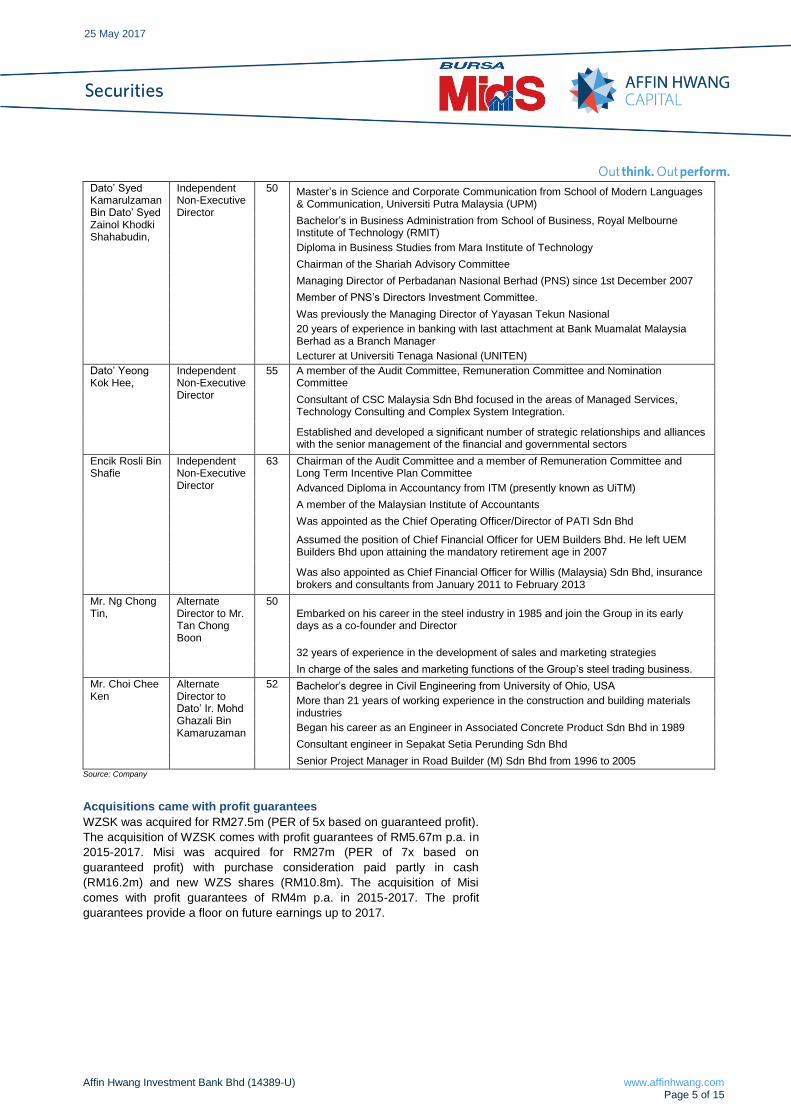

Name Designation Age Profile

YM Tengku Dato’ Sri Uzir Bin Tengku Dato’ Ubaidillah

Executive Chairman / Chief Executive Officer

56 Bachelor of Science (Honours) Degree in Civil Engineering in the City University

Started his career with Jabatan Kerja Raya as an engineer

Chief Executive Officer of Malaysian General Investment Corporation Berhad (now known as Sumatec Resources Berhad) from 1990 to 1993

Board of Road Builder (M) Holdings Berhad, Kurnia Setia Berhad and Project Penyelenggaran Lebuhraya Berhad

Executive Director of Tanah Makmur Berhad in 2011

Dato’ Ir. William Tan Chee Keong

Senior Executive Director / Chief Operating Officer

60 Bachelor of Science (Honours) in Civil Engineering in the University of Nottingham

A member of The Institution of Engineers Malaysia and registered Professional Engineer.

Started his career in Jabatan Kerja Raya and worked there from 1980 to 1984

Was a project manager in Ken Holdings Sdn Bhd and Dayapi Bhd

A Senior Project Manager (later Project Director) of Road Builder group of companies in 1992

Appointed as an Executive Director in Road Builder (M) Sdn Bhd

Founded WZS KenKeong Sdn Bhd in 2007 after he left the Road Builder group

Mr. Tan Teng Heng

Executive Director / Chief Financial Officer

51 A member of the The Malaysian Institute of Certified Public Accountants

Trained in the big four audit and consultancy firms

Prize winner in two professional subjects i.e. Financial Accounting and Management Accounting.

Was the CEO of an options and futures company which was then a member of KLOFFE (Kuala Lumpur Options and Financial Futures Exchange)

Was with HwangDBS Investment Bank Berhad as Senior Vice President.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 4 of 15

Mr. Tan Ching Kee

Senior Executive Director

56 Founder of WZ Satu Berhad (previously known as Weng Zheng Resources Berhad)

37 years of experience in the steel trading business

Brother of Mr. Tan Chong Boon, a Director of the Company and brother-in-law of Mr. Ng Chong Tin, an Alternate Director of the Company.

Mr. Tan Chong Boon,

Executive Director

50 Degree (Honours) in Civil Engineering in the Universiti Putra Malaysia (UPM)

Experience in the areas of designing and building civil and structural works

Established the Group’s cold drawn bright steel production plant in 1995 and later, he managed the Group’s venture into the production of high-end freecutting polished shafts for office automation

Dato’ Ir. Mohd Ghazali Bin Kamaruzaman,

Executive Director

50 A member of The Institution of Engineers, Malaysia and Board of Engineers, Malaysia

Bachelor’s degree in Civil Engineering from Victoria University of Technology, Melbourne

Master’s degree in Project Management from Universiti Teknologi Mara (UiTM)

More than 26 years of experience in civil engineering works

Design engineer with the Shire of Melton, Victoria Australia in 1988

Engineer in PATI Sdn Bhd and later PATI Pave Sdn Bhd

Notable projects - North South Expressway, Second Link, Central Link, Manila Cavite Expressway, Jalan Pahang, Lebuhraya Pantai Timur (LPT), PUTRA LRT, KL – Salak Expressway, Bangi Seremban Third Lane Widening and Simpang Pulai – Blue Valley.

Founded Prisma Simfoni Sdn Bhd in 2005 specialized in road construction, earthworks, building construction and waterworks

Notable projects - Third Lane Widening Tg. Malim to Slim River, Missing Link Awan Besar to KESAS Highway, UPSI infrastructure works, Batu Embun Water Intake and Treatment Plant, Herbal Centre Phase 2 for Technology Park Malaysia, Commercial & Office Building for UDA (North) in Seberang Prai and Non Revenue Water (NRW) for PAIP.

Dato’ Amin Rafie Bin Othman

Deputy Chairman / Senior Independent Non-Executive Director

56 Chairman of the Nomination Committee, Remuneration Committee and a member of the Audit Committee

A joint degree in Economics and International Politics in 1982

Master of Business Administration degree from the City University of London, United Kingdom.

Chairman of Asia Solar Generation Ventures Sdn Bhd

Managing Director of Plynlymon Capital Sdn Bhd and Rampai Ulltima Sdn Bhd

A Director of PDAC Formis Sdn Bhd (Brunei)

Past President of the Malaysian Association of Asset Managers

A member of the Listing Committee of Bursa Malaysia Securities Berhad.

Datuk Idris bin Haji Hashim

Independent Non-Executive Director

63 Diploma in Town and Regional Planning from Universiti Teknologi Mara (UiTM) in 1975

Master of Science, City and Regional Planning from Illinois Institute of Technology, Chicago in 1978.

Started his career as an assistant town planner with Arkitek Bersekutu Malaysia in 1975, participated in projects such as Pusat Bandar Bukit Raden, Kompleks Perdagangan Kuantan in Pahang and Bangunan Sri Mara in Kuala Lumpur

Attached to North-Eastern Illinois Planning Commission, Chicago as a Planner where he was involved in various large projects in the State of Illinois as well as the New Jeddah International Airport, King Abdul Aziz University and Automotive Centre for Sears Roebuck & Co. He

Lecturer in the School of Architecture, Planning and Surveying of UiTM in 1980.

Director of Focus Point Holdings Berhad.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 5 of 15

Dato’ Syed Kamarulzaman Bin Dato’ Syed Zainol Khodki Shahabudin,

Independent Non-Executive Director

50 Master’s in Science and Corporate Communication from School of Modern Languages & Communication, Universiti Putra Malaysia (UPM)

Bachelor’s in Business Administration from School of Business, Royal Melbourne Institute of Technology (RMIT)

Diploma in Business Studies from Mara Institute of Technology

Chairman of the Shariah Advisory Committee

Managing Director of Perbadanan Nasional Berhad (PNS) since 1st December 2007

Member of PNS’s Directors Investment Committee.

Was previously the Managing Director of Yayasan Tekun Nasional

20 years of experience in banking with last attachment at Bank Muamalat Malaysia Berhad as a Branch Manager

Lecturer at Universiti Tenaga Nasional (UNITEN)

Dato’ Yeong Kok Hee,

Independent Non-Executive Director

55 A member of the Audit Committee, Remuneration Committee and Nomination Committee

Consultant of CSC Malaysia Sdn Bhd focused in the areas of Managed Services, Technology Consulting and Complex System Integration.

Established and developed a significant number of strategic relationships and alliances with the senior management of the financial and governmental sectors

Encik Rosli Bin Shafie

Independent Non-Executive Director

63 Chairman of the Audit Committee and a member of Remuneration Committee and Long Term Incentive Plan Committee

Advanced Diploma in Accountancy from ITM (presently known as UiTM)

A member of the Malaysian Institute of Accountants

Was appointed as the Chief Operating Officer/Director of PATI Sdn Bhd

Assumed the position of Chief Financial Officer for UEM Builders Bhd. He left UEM Builders Bhd upon attaining the mandatory retirement age in 2007

Was also appointed as Chief Financial Officer for Willis (Malaysia) Sdn Bhd, insurance brokers and consultants from January 2011 to February 2013

Mr. Ng Chong Tin,

Alternate Director to Mr. Tan Chong Boon

50 Embarked on his career in the steel industry in 1985 and join the Group in its early days as a co-founder and Director

32 years of experience in the development of sales and marketing strategies

In charge of the sales and marketing functions of the Group’s steel trading business.

Mr. Choi Chee Ken

Alternate Director to Dato’ Ir. Mohd Ghazali Bin Kamaruzaman

52 Bachelor’s degree in Civil Engineering from University of Ohio, USA

More than 21 years of working experience in the construction and building materials industries

Began his career as an Engineer in Associated Concrete Product Sdn Bhd in 1989

Consultant engineer in Sepakat Setia Perunding Sdn Bhd

Senior Project Manager in Road Builder (M) Sdn Bhd from 1996 to 2005 Source: Company

Acquisitions came with profit guarantees

WZSK was acquired for RM27.5m (PER of 5x based on guaranteed profit).

The acquisition of WZSK comes with profit guarantees of RM5.67m p.a. in

2015-2017. Misi was acquired for RM27m (PER of 7x based on

guaranteed profit) with purchase consideration paid partly in cash

(RM16.2m) and new WZS shares (RM10.8m). The acquisition of Misi

comes with profit guarantees of RM4m p.a. in 2015-2017. The profit

guarantees provide a floor on future earnings up to 2017.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 6 of 15

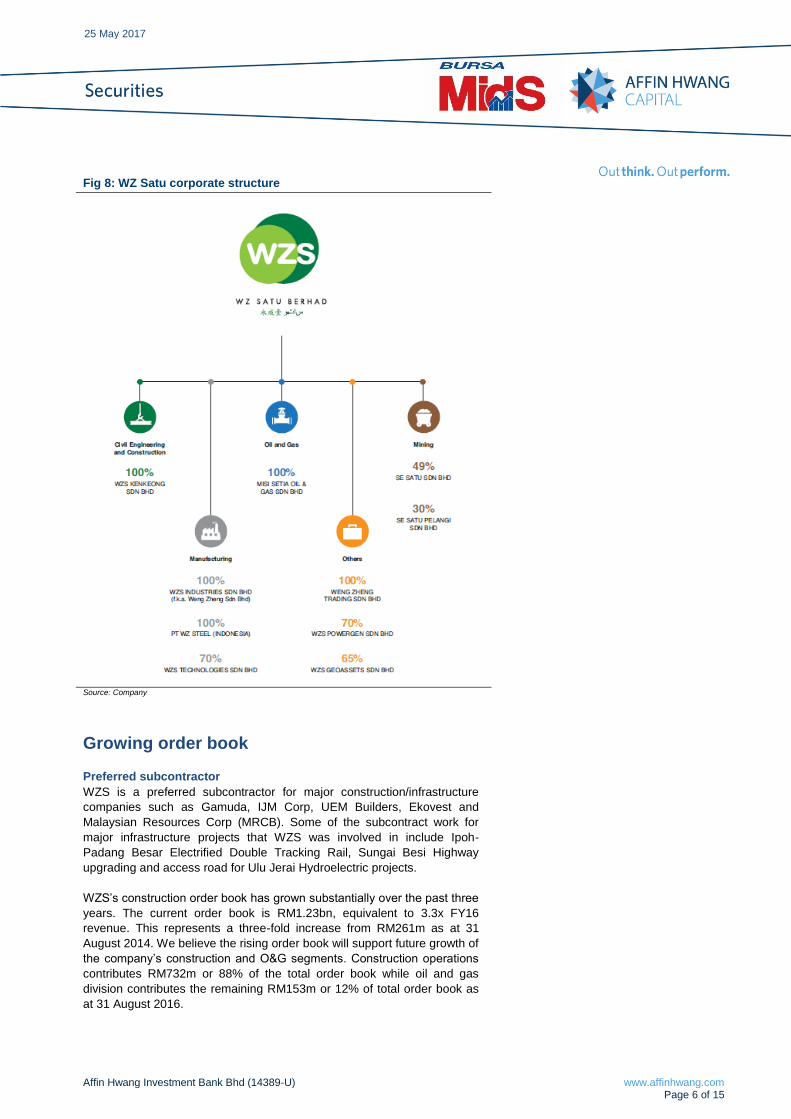

Fig 8: WZ Satu corporate structure

Source: Company

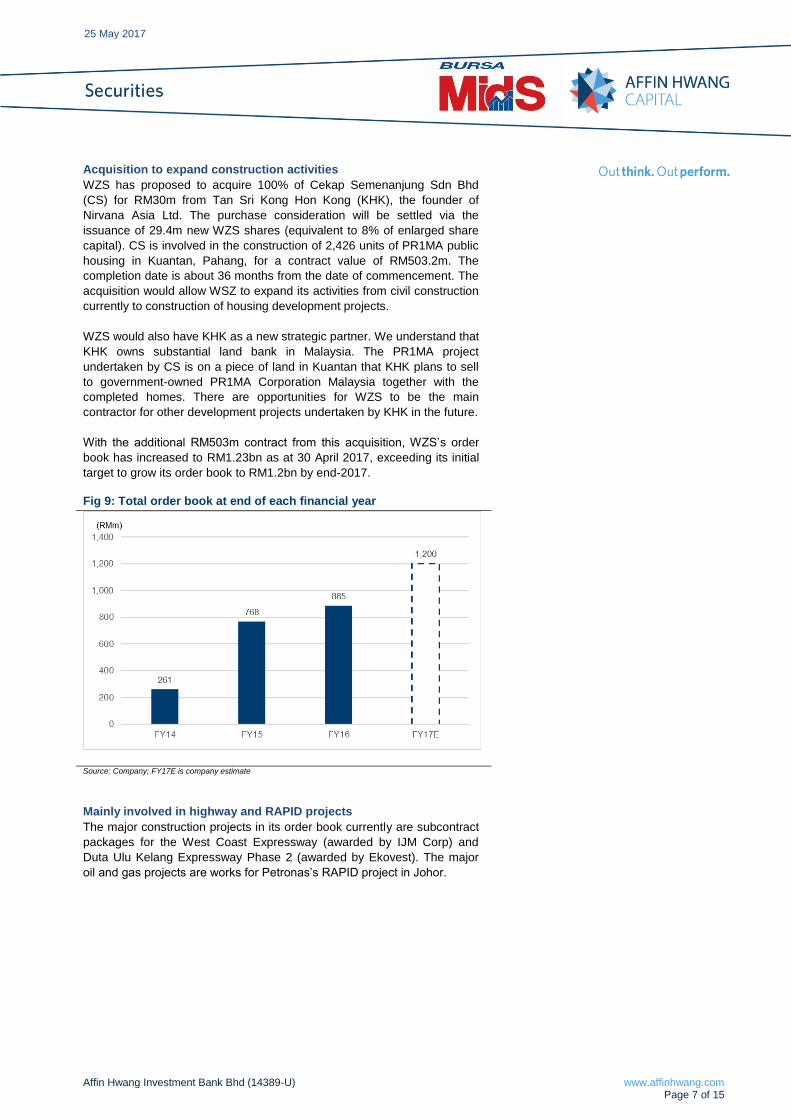

Growing order book

Preferred subcontractor

WZS is a preferred subcontractor for major construction/infrastructure

companies such as Gamuda, IJM Corp, UEM Builders, Ekovest and

Malaysian Resources Corp (MRCB). Some of the subcontract work for

major infrastructure projects that WZS was involved in include Ipoh-

Padang Besar Electrified Double Tracking Rail, Sungai Besi Highway

upgrading and access road for Ulu Jerai Hydroelectric projects.

WZS’s construction order book has grown substantially over the past three

years. The current order book is RM1.23bn, equivalent to 3.3x FY16

revenue. This represents a three-fold increase from RM261m as at 31

August 2014. We believe the rising order book will support future growth of

the company’s construction and O&G segments. Construction operations

contributes RM732m or 88% of the total order book while oil and gas

division contributes the remaining RM153m or 12% of total order book as

at 31 August 2016.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 7 of 15

Acquisition to expand construction activities

WZS has proposed to acquire 100% of Cekap Semenanjung Sdn Bhd

(CS) for RM30m from Tan Sri Kong Hon Kong (KHK), the founder of

Nirvana Asia Ltd. The purchase consideration will be settled via the

issuance of 29.4m new WZS shares (equivalent to 8% of enlarged share

capital). CS is involved in the construction of 2,426 units of PR1MA public

housing in Kuantan, Pahang, for a contract value of RM503.2m. The

completion date is about 36 months from the date of commencement. The

acquisition would allow WSZ to expand its activities from civil construction

currently to construction of housing development projects.

WZS would also have KHK as a new strategic partner. We understand that

KHK owns substantial land bank in Malaysia. The PR1MA project

undertaken by CS is on a piece of land in Kuantan that KHK plans to sell

to government-owned PR1MA Corporation Malaysia together with the

completed homes. There are opportunities for WZS to be the main

contractor for other development projects undertaken by KHK in the future.

With the additional RM503m contract from this acquisition, WZS’s order

book has increased to RM1.23bn as at 30 April 2017, exceeding its initial

target to grow its order book to RM1.2bn by end-2017.

Fig 9: Total order book at end of each financial year

Source: Company; FY17E is company estimate

Mainly involved in highway and RAPID projects

The major construction projects in its order book currently are subcontract

packages for the West Coast Expressway (awarded by IJM Corp) and

Duta Ulu Kelang Expressway Phase 2 (awarded by Ekovest). The major

oil and gas projects are works for Petronas’s RAPID project in Johor.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 8 of 15

Fig 10: Construction order book as at 31 August 2016

Source: Company

Fig 11: Onshore oil and gas order book as at 31 August 2016

Source: Company

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 9 of 15

Bidding for highway and rail projects

WZ Satu is bidding for works on the (1) RM3.74bn Setiawangsa-Pantai

Expressway (SPE), (2) RM6bn West Coast Expressway (WCE), (3) East

Coast Economic Region (ECER) infrastructure, (4) RM9bn Gemas-Johor

Bahru Double Tracking (partnering Fajar Baru) and (5) RM4bn Central

Spine Road (CSR) project (partnering UEM Group). WZS indicated the

estimated total tenders submitted and planned for submission is RM1.2bn

for the first four projects mentioned earlier.

Game changer if it secures CSR project

We gather that WZS could take a 30% stake in the joint venture with UEM

Group (hold a 70% stake) to undertake the CSR project. But WZS may

undertake works equivalent to 2/3 of the contract value given the lack of

construction capacity of UEM Group. The government could allocate funds

for further phases of the CSR project, which is of social-economic

importance, as the next general election is expected to be held soon.

Main contractor in potential new projects

WZS expects its construction PBT margin of 4.7% in FY15 to improve in

the long run as it undertakes larger projects (gaining economies of scale)

and moves up the value chain to become the main contractor for potential

new projects. WZ Satu will likely be part of the consortium led by UEM

Builders for the CSR project and hence believes it can earn better profit

margins as a main contractor.

Our RM600m p.a. new contract assumptions in FY17-19 do not include

the CSR project. Assuming WZS’s share of works is RM2.5bn for the CSR

and a PBT margin of 8%, we estimate that FY19 EPS could increase by

30% to 17.2 sen assuming a 15% completion rate for the project.

New rail link proposed

Prime Minister Datuk Seri Najib Razak unveiled a series of new initiatives

last year to modernise the country’s public transportation to help the

economy and improve connectivity for citizens. Topping the list was the

new 600 km East Coast Rail Link (ECRL) from Kuala Lumpur to Tumpat,

Kelantan, via Kuantan, Kemaman and Kuala Terengganu.

The cost of the project is RM55bn. Announcing the ECRL strengthens the

pipeline of infrastructure projects for construction companies to potentially

expand their order books.

Potential beneficiary of East Coast Rail Link

WZS could be a beneficiary of the ECRL given its established track record,

being one of the subcontractors for the RM12.5bn Ipoh-Padang Besar

Double Tracking Rail project. The project was undertaken by a joint

venture between MMC Corp and Gamuda as the main contractor.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 10 of 15

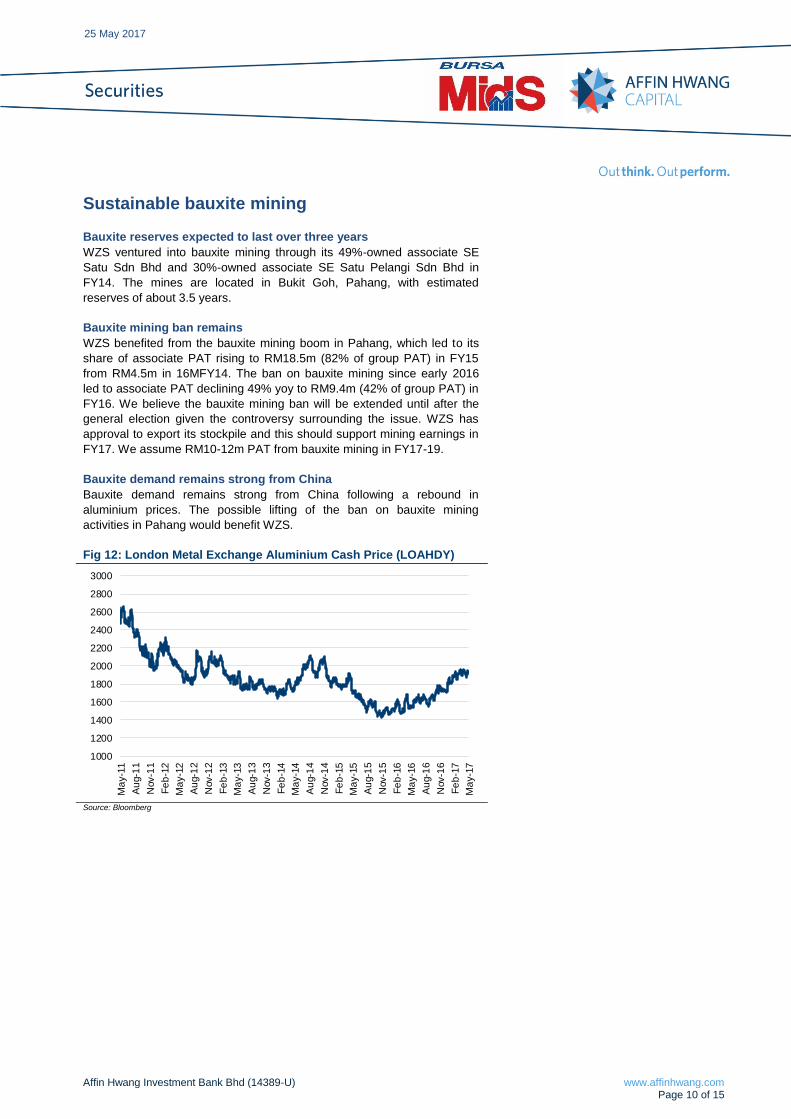

Sustainable bauxite mining

Bauxite reserves expected to last over three years

WZS ventured into bauxite mining through its 49%-owned associate SE

Satu Sdn Bhd and 30%-owned associate SE Satu Pelangi Sdn Bhd in

FY14. The mines are located in Bukit Goh, Pahang, with estimated

reserves of about 3.5 years.

Bauxite mining ban remains

WZS benefited from the bauxite mining boom in Pahang, which led to its

share of associate PAT rising to RM18.5m (82% of group PAT) in FY15

from RM4.5m in 16MFY14. The ban on bauxite mining since early 2016

led to associate PAT declining 49% yoy to RM9.4m (42% of group PAT) in

FY16. We believe the bauxite mining ban will be extended until after the

general election given the controversy surrounding the issue. WZS has

approval to export its stockpile and this should support mining earnings in

FY17. We assume RM10-12m PAT from bauxite mining in FY17-19.

Bauxite demand remains strong from China

Bauxite demand remains strong from China following a rebound in

aluminium prices. The possible lifting of the ban on bauxite mining

activities in Pahang would benefit WZS.

Fig 12: London Metal Exchange Aluminium Cash Price (LOAHDY)

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

Ma

y-1

1

Au

g-1

1

Nov-1

1

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

Nov-1

2

Fe

b-1

3

Ma

y-1

3

Au

g-1

3

Nov-1

3

Fe

b-1

4

Ma

y-1

4

Au

g-1

4

Nov-1

4

Fe

b-1

5

Ma

y-1

5

Au

g-1

5

Nov-1

5

Fe

b-1

6

Ma

y-1

6

Au

g-1

6

Nov-1

6

Fe

b-1

7

Ma

y-1

7

Source: Bloomberg

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 11 of 15

Highway concession acquisition plan falls through

WZS has aggressive plans to expand into the highway infrastructure

concession business. It signed a Heads of Agreement (HOA) with SILK

Holdings Bhd for the proposed acquisition of the Kajang Traffic Dispersal

Ring Road concession for RM368m. The proposed price was larger than

the WZS’s market capitalisation.

Negotiations were mutually terminated on 23 September 2016 as both

parties were unable to reach a deal. WZS’s management clarified that it

had preferred the purchase consideration to be partially settled in new

shares to be issued by WZS but SILK had preferred an all-cash deal. SILK

was acquired by Permodalan Nasional Bhd subsequently at a higher price

of RM380m in an all-cash deal.

Moving up the value chain in aircraft manufacturing

WZS also plans to expand its aircraft component manufacturing business

(high value added) and exit from the cold drawn bright steel polished shaft

manufacturing business (low value added). The company thinks this could

improve the manufacturing profit margin in the long run. Currently, it is a

Tier 3 aerospace company and is targeting to move up to Tier 2 next year

by investing in new state-of-the-art machines. WZS thinks high start-up

costs could dampen manufacturing earnings in the short term but there

could be long-term benefits if it is successful in moving up the value chain.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 12 of 15

Initiate coverage with BUY call

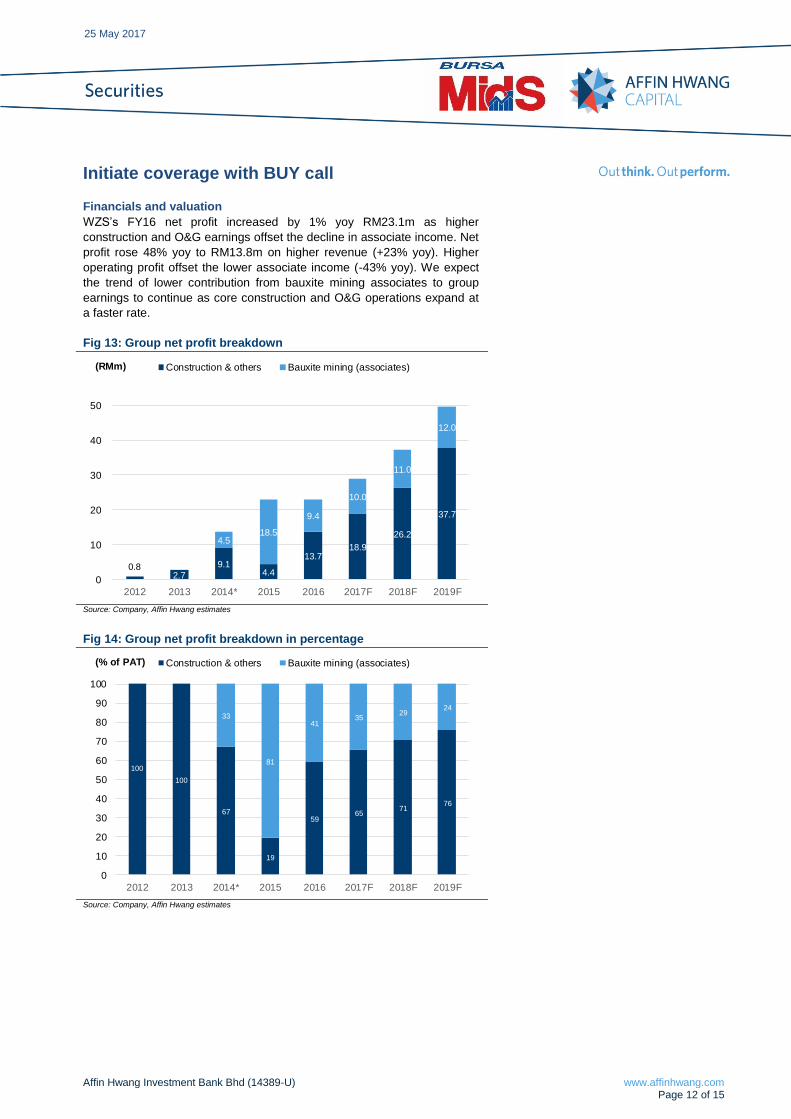

Financials and valuation

WZS’s FY16 net profit increased by 1% yoy RM23.1m as higher

construction and O&G earnings offset the decline in associate income. Net

profit rose 48% yoy to RM13.8m on higher revenue (+23% yoy). Higher

operating profit offset the lower associate income (-43% yoy). We expect

the trend of lower contribution from bauxite mining associates to group

earnings to continue as core construction and O&G operations expand at

a faster rate.

Fig 13: Group net profit breakdown

0.8 2.7

9.1 4.4

13.7 18.9

26.2

37.7

4.5 18.5

9.4

10.0

11.0

12.0

0

10

20

30

40

50

2012 2013 2014* 2015 2016 2017F 2018F 2019F

Construction & others Bauxite mining (associates)(RMm)

Source: Company, Affin Hwang estimates

Fig 14: Group net profit breakdown in percentage

100

100

67

19

5965

7176

33

81

4135

2924

0

10

20

30

40

50

60

70

80

90

100

2012 2013 2014* 2015 2016 2017F 2018F 2019F

Construction & others Bauxite mining (associates)(% of PAT)

Source: Company, Affin Hwang estimates

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 13 of 15

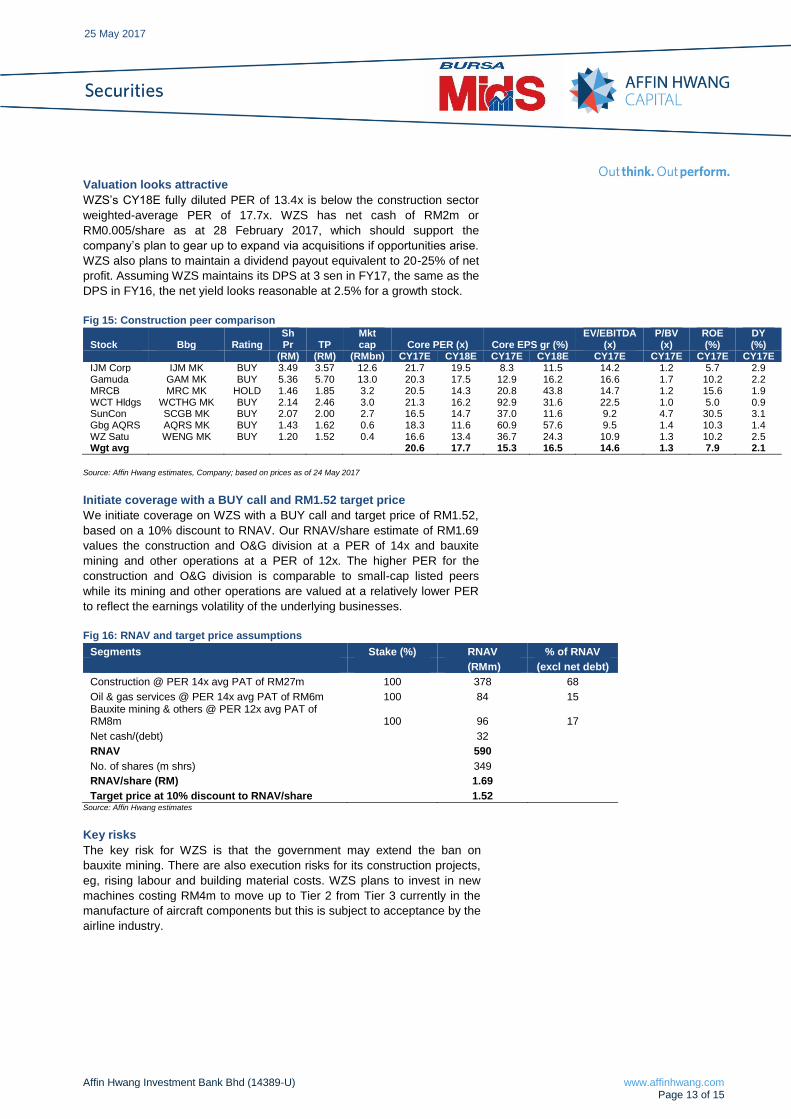

Valuation looks attractive

WZS’s CY18E fully diluted PER of 13.4x is below the construction sector

weighted-average PER of 17.7x. WZS has net cash of RM2m or

RM0.005/share as at 28 February 2017, which should support the

company’s plan to gear up to expand via acquisitions if opportunities arise.

WZS also plans to maintain a dividend payout equivalent to 20-25% of net

profit. Assuming WZS maintains its DPS at 3 sen in FY17, the same as the

DPS in FY16, the net yield looks reasonable at 2.5% for a growth stock.

Fig 15: Construction peer comparison

Stock Bbg Rating Sh Pr TP

Mkt cap Core PER (x) Core EPS gr (%)

EV/EBITDA (x)

P/BV (x)

ROE (%)

DY (%)

(RM) (RM) (RMbn) CY17E CY18E CY17E CY18E CY17E CY17E CY17E CY17E IJM Corp IJM MK BUY 3.49 3.57 12.6 21.7 19.5 8.3 11.5 14.2 1.2 5.7 2.9 Gamuda GAM MK BUY 5.36 5.70 13.0 20.3 17.5 12.9 16.2 16.6 1.7 10.2 2.2 MRCB MRC MK HOLD 1.46 1.85 3.2 20.5 14.3 20.8 43.8 14.7 1.2 15.6 1.9 WCT Hldgs WCTHG MK BUY 2.14 2.46 3.0 21.3 16.2 92.9 31.6 22.5 1.0 5.0 0.9 SunCon SCGB MK BUY 2.07 2.00 2.7 16.5 14.7 37.0 11.6 9.2 4.7 30.5 3.1 Gbg AQRS AQRS MK BUY 1.43 1.62 0.6 18.3 11.6 60.9 57.6 9.5 1.4 10.3 1.4 WZ Satu WENG MK BUY 1.20 1.52 0.4 16.6 13.4 36.7 24.3 10.9 1.3 10.2 2.5 Wgt avg 20.6 17.7 15.3 16.5 14.6 1.3 7.9 2.1

Source: Affin Hwang estimates, Company; based on prices as of 24 May 2017

Initiate coverage with a BUY call and RM1.52 target price

We initiate coverage on WZS with a BUY call and target price of RM1.52,

based on a 10% discount to RNAV. Our RNAV/share estimate of RM1.69

values the construction and O&G division at a PER of 14x and bauxite

mining and other operations at a PER of 12x. The higher PER for the

construction and O&G division is comparable to small-cap listed peers

while its mining and other operations are valued at a relatively lower PER

to reflect the earnings volatility of the underlying businesses.

Fig 16: RNAV and target price assumptions

Segments Stake (%) RNAV % of RNAV

(RMm) (excl net debt)

Construction @ PER 14x avg PAT of RM27m 100 378 68

Oil & gas services @ PER 14x avg PAT of RM6m 100 84 15 Bauxite mining & others @ PER 12x avg PAT of RM8m 100 96 17

Net cash/(debt)

32 RNAV

590

No. of shares (m shrs)

349 RNAV/share (RM)

1.69

Target price at 10% discount to RNAV/share 1.52 Source: Affin Hwang estimates

Key risks

The key risk for WZS is that the government may extend the ban on

bauxite mining. There are also execution risks for its construction projects,

eg, rising labour and building material costs. WZS plans to invest in new

machines costing RM4m to move up to Tier 2 from Tier 3 currently in the

manufacture of aircraft components but this is subject to acceptance by the

airline industry.

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 14 of 15

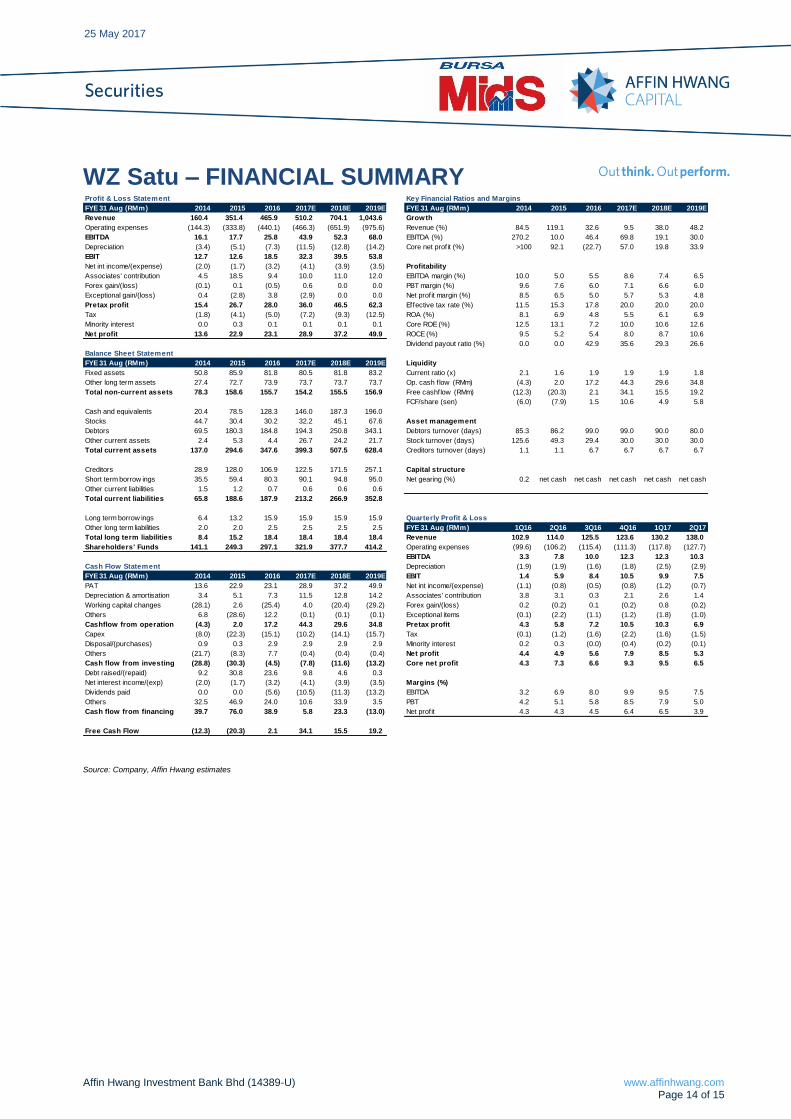

WZ Satu – FINANCIAL SUMMARY Profit & Loss Statement Key Financial Ratios and Margins

FYE 31 Aug (RMm) 2014 2015 2016 2017E 2018E 2019E FYE 31 Aug (RMm) 2014 2015 2016 2017E 2018E 2019E

Revenue 160.4 351.4 465.9 510.2 704.1 1,043.6 Growth

Operating expenses (144.3) (333.8) (440.1) (466.3) (651.9) (975.6) Revenue (%) 84.5 119.1 32.6 9.5 38.0 48.2

EBITDA 16.1 17.7 25.8 43.9 52.3 68.0 EBITDA (%) 270.2 10.0 46.4 69.8 19.1 30.0

Depreciation (3.4) (5.1) (7.3) (11.5) (12.8) (14.2) Core net profit (%) >100 92.1 (22.7) 57.0 19.8 33.9

EBIT 12.7 12.6 18.5 32.3 39.5 53.8

Net int income/(expense) (2.0) (1.7) (3.2) (4.1) (3.9) (3.5) Profitability

Associates' contribution 4.5 18.5 9.4 10.0 11.0 12.0 EBITDA margin (%) 10.0 5.0 5.5 8.6 7.4 6.5

Forex gain/(loss) (0.1) 0.1 (0.5) 0.6 0.0 0.0 PBT margin (%) 9.6 7.6 6.0 7.1 6.6 6.0

Exceptional gain/(loss) 0.4 (2.8) 3.8 (2.9) 0.0 0.0 Net profit margin (%) 8.5 6.5 5.0 5.7 5.3 4.8

Pretax profit 15.4 26.7 28.0 36.0 46.5 62.3 Effective tax rate (%) 11.5 15.3 17.8 20.0 20.0 20.0

Tax (1.8) (4.1) (5.0) (7.2) (9.3) (12.5) ROA (%) 8.1 6.9 4.8 5.5 6.1 6.9

Minority interest 0.0 0.3 0.1 0.1 0.1 0.1 Core ROE (%) 12.5 13.1 7.2 10.0 10.6 12.6

Net profit 13.6 22.9 23.1 28.9 37.2 49.9 ROCE (%) 9.5 5.2 5.4 8.0 8.7 10.6

Dividend payout ratio (%) 0.0 0.0 42.9 35.6 29.3 26.6

Balance Sheet Statement

FYE 31 Aug (RMm) 2014 2015 2016 2017E 2018E 2019E Liquidity

Fixed assets 50.8 85.9 81.8 80.5 81.8 83.2 Current ratio (x) 2.1 1.6 1.9 1.9 1.9 1.8

Other long term assets 27.4 72.7 73.9 73.7 73.7 73.7 Op. cash f low (RMm) (4.3) 2.0 17.2 44.3 29.6 34.8

Total non-current assets 78.3 158.6 155.7 154.2 155.5 156.9 Free cashflow (RMm) (12.3) (20.3) 2.1 34.1 15.5 19.2

FCF/share (sen) (6.0) (7.9) 1.5 10.6 4.9 5.8

Cash and equivalents 20.4 78.5 128.3 146.0 187.3 196.0

Stocks 44.7 30.4 30.2 32.2 45.1 67.6 Asset management

Debtors 69.5 180.3 184.8 194.3 250.8 343.1 Debtors turnover (days) 85.3 86.2 99.0 99.0 90.0 80.0

Other current assets 2.4 5.3 4.4 26.7 24.2 21.7 Stock turnover (days) 125.6 49.3 29.4 30.0 30.0 30.0

Total current assets 137.0 294.6 347.6 399.3 507.5 628.4 Creditors turnover (days) 1.1 1.1 6.7 6.7 6.7 6.7

Creditors 28.9 128.0 106.9 122.5 171.5 257.1 Capital structure

Short term borrow ings 35.5 59.4 80.3 90.1 94.8 95.0 Net gearing (%) 0.2 net cash net cash net cash net cash net cash

Other current liabilities 1.5 1.2 0.7 0.6 0.6 0.6

Total current liabilities 65.8 188.6 187.9 213.2 266.9 352.8

Long term borrow ings 6.4 13.2 15.9 15.9 15.9 15.9 Quarterly Profit & Loss

Other long term liabilities 2.0 2.0 2.5 2.5 2.5 2.5 FYE 31 Aug (RMm) 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

Total long term liabilities 8.4 15.2 18.4 18.4 18.4 18.4 Revenue 102.9 114.0 125.5 123.6 130.2 138.0

Shareholders' Funds 141.1 249.3 297.1 321.9 377.7 414.2 Operating expenses (99.6) (106.2) (115.4) (111.3) (117.8) (127.7)

EBITDA 3.3 7.8 10.0 12.3 12.3 10.3

Cash Flow Statement Depreciation (1.9) (1.9) (1.6) (1.8) (2.5) (2.9)

FYE 31 Aug (RMm) 2014 2015 2016 2017E 2018E 2019E EBIT 1.4 5.9 8.4 10.5 9.9 7.5

PAT 13.6 22.9 23.1 28.9 37.2 49.9 Net int income/(expense) (1.1) (0.8) (0.5) (0.8) (1.2) (0.7)

Depreciation & amortisation 3.4 5.1 7.3 11.5 12.8 14.2 Associates' contribution 3.8 3.1 0.3 2.1 2.6 1.4

Working capital changes (28.1) 2.6 (25.4) 4.0 (20.4) (29.2) Forex gain/(loss) 0.2 (0.2) 0.1 (0.2) 0.8 (0.2)

Others 6.8 (28.6) 12.2 (0.1) (0.1) (0.1) Exceptional items (0.1) (2.2) (1.1) (1.2) (1.8) (1.0)

Cashflow from operation (4.3) 2.0 17.2 44.3 29.6 34.8 Pretax profit 4.3 5.8 7.2 10.5 10.3 6.9

Capex (8.0) (22.3) (15.1) (10.2) (14.1) (15.7) Tax (0.1) (1.2) (1.6) (2.2) (1.6) (1.5)

Disposal/(purchases) 0.9 0.3 2.9 2.9 2.9 2.9 Minority interest 0.2 0.3 (0.0) (0.4) (0.2) (0.1)

Others (21.7) (8.3) 7.7 (0.4) (0.4) (0.4) Net profit 4.4 4.9 5.6 7.9 8.5 5.3

Cash flow from investing (28.8) (30.3) (4.5) (7.8) (11.6) (13.2) Core net profit 4.3 7.3 6.6 9.3 9.5 6.5

Debt raised/(repaid) 9.2 30.8 23.6 9.8 4.6 0.3

Net interest income/(exp) (2.0) (1.7) (3.2) (4.1) (3.9) (3.5) Margins (%)

Dividends paid 0.0 0.0 (5.6) (10.5) (11.3) (13.2) EBITDA 3.2 6.9 8.0 9.9 9.5 7.5

Others 32.5 46.9 24.0 10.6 33.9 3.5 PBT 4.2 5.1 5.8 8.5 7.9 5.0

Cash flow from financing 39.7 76.0 38.9 5.8 23.3 (13.0) Net profit 4.3 4.3 4.5 6.4 6.5 3.9

Free Cash Flow (12.3) (20.3) 2.1 34.1 15.5 19.2

Source: Company, Affin Hwang estimates

25 May 2017

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 15 of 15

Equity Rating Structure and Definitions

BUY Total return is expected to exceed +10% over a 12-month period

HOLD Total return is expected to be between -5% and +10% over a 12-month period

SELL Total return is expected to be below -5% over a 12-month period

NOT RATED Affin Hwang Investment Bank Berhad does not provide research coverage or rating for this company. Report is intended as information only and not as

a recommendation

The total expected return is defined as the percentage upside/downside to our target price plus the net dividend yield over the next 12 months.

OVERWEIGHT Industry, as defined by the analyst’s coverage universe, is expected to outperform the KLCI benchmark over the next 12 months

NEUTRAL Industry, as defined by the analyst’s coverage universe, is expected to perform inline with the KLCI benchmark over the next 12 months

UNDERWEIGHT Industry, as defined by the analyst’s coverage universe is expected to under-perform the KLCI benchmark over the next 12 months

This report is intended for information purposes only and has been prepared by Affin Hwang Investment Bank Berhad (14389-U) (“the Company”) based on sources believed to be reliable. However, such sources have not been independently verified by the Company, and as such the Company does not give any guarantee, representation or warranty (express or implied) as to the adequacy, accuracy, reliability or completeness of the information and/or opinion provided or rendered in this report. Facts, information, views and/or opinion presented in this report have not been reviewed by, may not reflect information known to, and may present a differing view expressed by other business units within the Company, including investment banking personnel. Reports issued by the Company, are prepared in accordance with the Company’s policies for managing conflicts of interest arising as a result of publication and distribution of investment research reports. Under no circumstances shall the Company, its associates and/or any person related to it be liable in any manner whatsoever for any consequences (including but are not limited to any direct, indirect or consequential losses, loss of profit and damages) arising from the use of or reliance on the information and/or opinion provided or rendered in this report. Any opinions or estimates in this report are that of the Company, as of this date and subject to change without prior notice. Under no circumstances shall this report be construed as an offer to sell or a solicitation of an offer to buy any securities. The Company and/or any of its directors and/or employees may have an interest in the securities mentioned therein. The Company may also make investment decisions or take proprietary positions that are inconsistent with the recommendations or views in this report. Comments and recommendations stated here rely on the individual opinions of the ones providing these comments and recommendations. These opinions may not fit to your financial status, risk and return preferences and hence an independent evaluation is essential. Investors are advised to independently evaluate particular investments and strategies and to seek independent financial, legal and other advice on the information and/or opinion contained in this report before investing or participating in any of the securities or investment strategies or transactions discussed in this report. Third-party data providers make no warranties or representations of any kind relating to the accuracy, completeness, or timeliness of the data they provide and shall not have liability for any damages of any kind relating to such data. The Company’s research, or any portion thereof may not be reprinted, sold or redistributed without the consent of the Company. The Company, is a participant of the Capital Market Development Fund-Bursa Research Scheme, and will receive compensation for the participation. This report is printed and published by: Affin Hwang Investment Bank Berhad (14389-U) A Participating Organisation of Bursa Malaysia Securities Berhad 22nd Floor, Menara Boustead, 69, Jalan Raja Chulan, 50200 Kuala Lumpur, Malaysia. T : + 603 2146 3700 F : + 603 2146 7630 [email protected] www.affinhwang.com