Www.sundenergy.com Impact of unconventional gas reserves on energy policies and prices in Europe...

33

www.sundenergy.com Impact of unconventional gas reserves on energy policies and prices in Europe Flame Conference Karen Sund 13 May 2011

-

date post

19-Dec-2015 -

Category

Documents

-

view

219 -

download

1

Transcript of Www.sundenergy.com Impact of unconventional gas reserves on energy policies and prices in Europe...

www.sundenergy.com

Impact of unconventional gas reserves on energy policies and prices in Europe

Flame Conference

Karen Sund

13 May 2011

www.sundenergy.com

Sund Energy helps navigate into the energy future…

Page 2

Energy

Economics

Environment

…by understanding the full picture of stakeholders

OsloHelsinkiCopenhagenSan Francisco

www.sundenergy.com

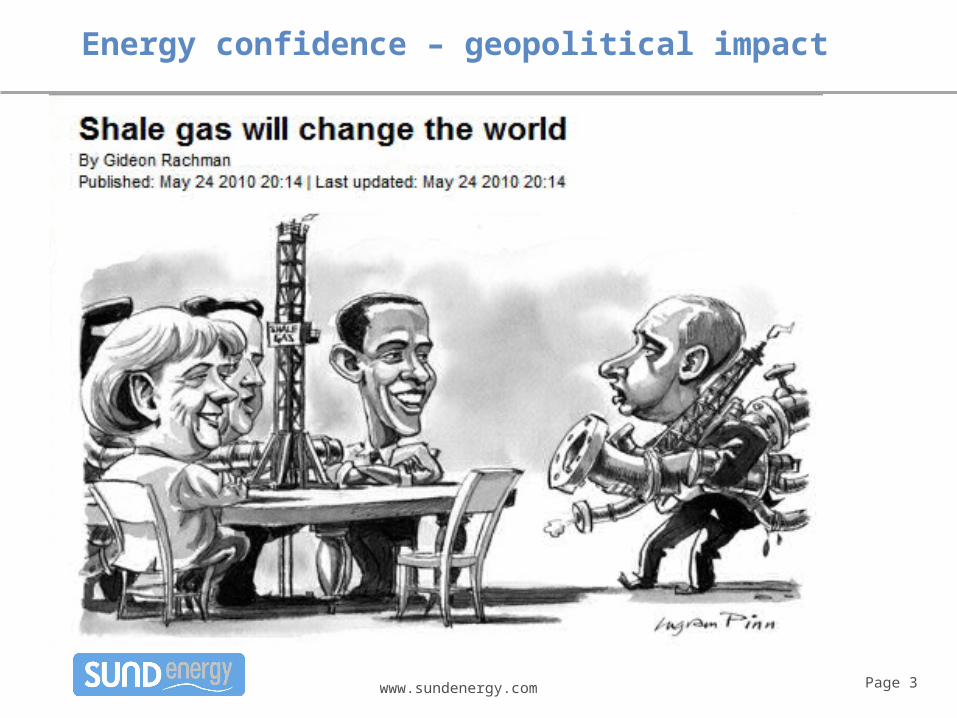

Energy confidence – geopolitical impact

Page 3

www.sundenergy.com

Impact of unconventional gas reserves on Europe

Unconventional in Europe – a short intro to volumes● Shale revolution in US – much hype and attention

• Already impacting Europe prices and policies• Other unconventional, too

● Learning or comparisons from those ahead of us?● New logic – easier to replace oil (US and China)

Politics and role of gas – the starting point● Security of supply and other fears● Attractiveness of affordability

Prices and area of use – two scenarios● Relative environmentalism and economics● Two scenarios

• Unconventional takes off – with markets to match• Europe says no to unconventional, and perhaps nuclear…

Page 4

April 2011

www.sundenergy.com

Unconventional gas is growing rapidly in the world

Share of global gas production could double by 2050● Estimated at more than 300 bcm in 2010

US largest production, turning imports to exports ● Adding to global oversupply and low prices● Which again adds to comfort in markets

Page 5

World gas supply to 2035 and share of unconventional

Source: World Energy Outlook, 2010

Also: Methane Hydrates and UCG (underground coal gasification)

www.sundenergy.com Page 6

Globally significant shale giants

Top 10 global shale gas

resources*

Natural gas reserves*

(Tcm)

Importers ( ) /✔

Exporters( )✗

Shale gas Resources**

(Tcm)

Shale gas production by

2020***

China 3.03 ✔ 36.10 ✔

United States 7.71 ✔ 24.41 ✔

Argentina 0.38 ✔ 21.92 ✔

Mexico 0.34 ✔ 19.28 ✔

South Africa 0.01 ✔ 13.73 ✔

Australia 3.11 ✗ 11.21 ✔

Canada**** 1.75 ✗ 10.99 ?Libya 1.55 ✗ 8.21 ?Algeria 4.50 6.41 ?Brazil 0.36 ✔ 6.40 ✔

World 187.49 187.51Source: World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States, April 2011

* Technically recoverable shale gas resources** Proved conventional natural gas reserves*** Sund Energy estimates**** Canada: Producing today, but with strong resistance

www.sundenergy.com Page 7

Europe’s resources smaller but could still be play a vital role in energy mix !

Top 10 European shale gas

resources*

Natural gas reserves**

(Tcm)

Importers ( )/ ✔

Exporters( )✗

Shale gas resources*

(Tcm)

Shale gas production by

2020***

Poland 0.16 ✔ 5.30 ✔

France 0.01 ✔ 5.10 ✔

Norway 2.04 ✗ 2.35 ?Ukraine 1.10 ✔ 1.19 ✔

Sweden – ✔ 1.16 ?Denmark 0.06 ✗ 0.65 ✔

UK 0.25 ✔ 0.57 ✔

Netherlands 1.39 ✗ 0.48 ✔

Turkey 0.01 ✔ 0.42 ✔

Germany 0.17 ✔ 0.23 ✔

Others 0.54

Source: World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States, April 2011

* Technically recoverable shale gas resources** Proved conventional natural gas reserves*** Sund Energy estimates

www.sundenergy.com

Large investments in unconventional gas

Many years of small scale by small companies ● Lower investments and shorter lead

times ● Attention to detail and creativity

important

Suddenly large scale and entry of majors● Competitive advantage of global

technology?● Cheap way to increase ”oil equivalent’’

reserves

Lower costs: Easier to make a profit● Varying costs, but US around $4/mmbtu● Liquids (NGL, crude oil) help economics● Some flexible supplies could get higher

prices● Cash flow challenge for smaller players

at depressed prices

Page 8

www.sundenergy.com

SOURCE: SHELL.COM

Shell’s global unconventional gas positions

www.sundenergy.com

Europe is behind many – that could add to learning

US: “Unconventional is becoming conventional – half of all gas”● Regulation is coming into place – less cowboys than earlier● Some bad reputation and negative stories – but contribution, too!● Economics with liquids – different focus● Gas has been kept down due to rising dependency on imported LNG● Now perhaps the easiest way to reduce climate emissions

China: Distributed production of energy – that can replace oil● Want to keep down oil prices and imports● Also focus on local emissions – sulphur, particulates etc. ● Using more gas fixes several problems – and is good for the economy!● Good at commercialisation - especially transportation sector

Others, too – impacting the global gas outlook!● Australia, Argentina, Ukraine, Russia, South Africa…

Page 10

www.sundenergy.com

Shale already impacts Europe: Less US imports

US has exported LNG to Asia from Alaska for decades● Not very large volumes, but better profits than ”exports” to own states

Imports were expected to grow significantly – then not at all…● Falling domestic production and growing demand● Imports from Canada, Mexico and global LNG

With unconventional gas at home: ● Demand may grow more...● Less LNG is needed ● Exports to Canada

LNG import turning around● First re-exporting cargoes ● Then own liquefaction

UK balancing global LNG● Lower prices already● At times 50% of demand!

Page 11Source: EIA AEO 2007, 2009, 2011

Changing forecasts for US LNG imports

www.sundenergy.com

Will the shale opposition spread successfully?

US protests: Active and successful● High level exposure, even mass media

• Gas Land and Vanity Fair examples

● Several court cases already• Partly for lack of clear regulations

What will be the result of US protests?● More focus on emissions, water, noise● More studies on how to do it better● 1 year moratorium in New York on horizontal

drilling and large production

What can we learn? ● Each country has different focus

• Poland, Germany, Australia, China…

Relative environmentalism?● Cost + impact of alternative energy

Page 12

HQ of Damascus Citizens for Sustainability, in Vanity Fair

www.sundenergy.com

Will we beat the prejudices against us?

“Europe is not like Texas – there is not enough space”● Poland, France, Italy, Ukraine, even UK has open countryside

“Europe is full of environmentalists that would never accept it”● Compared to open-cast lignite mining, more nuclear, expensive wind…● Not all unconventional is as bad as some of the reputation of shale gas● Environmentalists do not agree – local,

national, global, fossil, nuclear● Accidents can be prevented with good

regulation

“Europe has no rigs”● The industry is global, there is onshore

drilling already● These rigs take 6 months to build…

“Europe has no entrepreneurs”● Really? No hungry business people in any country??

Page 13

Public opposition to shale drilling in France

Source: Berg & Coiron, March 2011

www.sundenergy.com

UK: Coal-bed methane can be quite popular

Coal-bed methane onshore● Often small, little visible impact● Small crews, horizontal drilling● Shallower than shale

Permitting and water important● Permits often under coal authorities● Water issues important

Government support could help● Not impossible in light of potential● Could get more energy than support to biogas, wind etc● Positive impact on domestic economy● Access, regulation, funding, feed-in tariffs relevant

Other aspects in the UK● “New” domestic gas could be preferred in economic turn-around● CBM, shale, UCG (underground coal gasification), and even biogas

Page 14

CBM field in Scotland, Source: Dart Energy

www.sundenergy.com

In Poland, unconventional gas could outcompete CCS

Poland largely relies on coal for power...● Low cost domestic reserves● Reducing dependence on Russia

... but capacity needs replacing by 2030● Old, inefficient plant breach EU standards● Carbon costs rendering plant uncompetitive● EU target to reduce GHG emissions by 2020

Will Poland build new coal plant with CCS...● CCS costs estimated at €130 billion by 2030

...or use more unconventional gas?● Most active EU country in developing domestic

unconventional reserves● Potential to replace imported gas, some coal● In addition, longer term export potential:● Lithuania, Germany, and others

Page 15

Belchatow – largest coal plant in EU

Source: coalpowerplants.blogspot.com,

Source: Gazlupkowy.pl, March 2011

Poland – gas exploration licenses

www.sundenergy.com

ExxonMobil: Large German gas volumes!

North-Rhine Westphalia could have 2100 bcm of shale gas and CBM gas reserves (second largest deposit in Europe)

● ExxonMobil has secured options on several areas to start exploration● Other companies also interested

6.5 bcm/yr could be produced as industry builds up capacity● Increasing Germany's self-sufficiency in gas to 25-30% ● Creating jobs and bringing royalties to the local municipalities

Exploration permits valid for 5 years● EUR 100 million in exploration costs for ExxonMobil alone● Production still uncertain – gas prices impact profitability● However, border prices perhaps less relevant…

Merkel: Easier to turn down nuclear with own gas?

Page 16

Gernot Kalkoffen, Head of Exxon Mobil Central EuropeSource: Handelsblatt, January 2011

www.sundenergy.com

France could see important gas production by 2020

A total of 500 bcm of shale gas could be produced in the Cévennes area ● Significant compared to current production of about 1 bcm/ year● Raising interest of GDF Suez, Total and others

Environmental concerns have lead to a temporary moratorium on drilling● Protests from local

communities and even politicians

• “Shale revolution” has taken many by surprise

• Some mistrust

● 2-3 years to map andbuild capacity and trust before industry can “take off”

Page 17Source: Frituremag, 2011

Map of shale gas licenses in (Southern) France

www.sundenergy.com

France: Nuclear means SOS, or…

Impact of Japanese disaster on France● Even the industry agrees that safety dose not comes with a guarantee● Socialist party has said no to nuclear● The Government feels the tremors but are there options…

Could unconventional gas be an alternative?● Government & industry seem to be interested● Government being criticized for being too permissive● Moratorium is now pushed from April to June 2011 ● How to change the French mindset?● Two government reports

commissioned due by mid-June

Page 18

www.sundenergy.com

Is it economic? That depends on who/ how you ask

Politicians look at alternatives, their costs, prices and timing● Renewables are taking time and costing more than was hoped for

• Even with monetary support to research, smart grids, feed-in...• Partly motivated by expected high cost imports of LNG

● Could we see support to local, flexible gas in the future?• Cheaper than offshore wind, Nabucco, and other SoS...

● How to sell the story – now that concerns are here?

Oil companies and other investors look at cost and price● Need to grow reserves – part of drive to buy acreage

• Fewer exciting prospects on the oil side than before• Buying shale acreage is cheaper in BOE than oil

● Margin better than many think• Expect better technology to reduce costs, now around $4.20/mmbtu in US• Income expected to be steady with more liquid markets and higher demand• Also additional income from liquids – with high prices: Oil, NGLs

● Believe in gas being the best solutions for the future energy mix!• Willing to offer at lower prices to avoid falling demand, it seems…

Page 19

www.sundenergy.com

Political right answers change – trying to please voters

Energy/security of supply – often emotional● Positive value, but often not quantified● Disguise for protectionism/economy? National resources get points here

Economy/trade balance important in energy policy● Even more so during recession?

• Typically reducing imported fossil fuels (especially oil from the Middle East)

In recession, employment matters, too, or so they say● Positive for new renewables - and perhaps even unconventional gas!

Page 20

www.sundenergy.com

Gas has been seen as a scarce expensive import

Page 21

Politicians perceived a growing vulnerability to gas supply… ● High prices – both oil-link contracts and spot markets during winter● Some bottlenecks and interruptions exacerbated the perception● Expectation of gas shortage, especially LNG

…showing strong interest in reducing the large import bills of gas● Large cash drain on economies + security of supply issues● Growing interest in domestic economy + green● EU, China and others adjusted policies

Recession at first confirmed need to reduce imports…● Peak oil-link prices hit the market at winter time in full-blown recession● Continued focus on domestic and renewable energy forms

Last few weeks’ nuclear outages did not give peak prices● Reduced oversupply ● This may give new confidence in gas markets – convenient?

www.sundenergy.com

High spending on imports is even less popular now

Strong focus earlier on oil, now on gas in EU, US and China● Falling in US with more domestic (unconventional) production● Driver for China and Europe, too

What if prices fall – how will that impact the energy mix?● Also, own reserves may reduce need to import

Cost of net imports of oil and gas (% of real GDP)

Source: World Energy Outlook, 2010

Page 22

www.sundenergy.com

…and result in different policies & stories

European Union: 20-20-20● SOS● Emissions● Reduced imports

United States: Energy independence● Employment● Economy● Climate?

China: 5-year plan● Gas to replace more oil● Actively using buying power

Page 23

www.sundenergy.com

Will Obama be the first to reduce US oil dependency?

Page 24

Extreme oil prices of 2008 gave reduced oil demand● First time ever!● Good for emission reductions, too● Bad for economy and added to recession and vulnerability

Unconventional gas will help!● Less imported LNG – more gas to power and transportation● Less oil imports + less emissions – even possible exports

www.sundenergy.com

For a while, nuclear became the answer – oops…

From gradually coming into favour…● Moratoriums cancelled, new plant planned● Life extended - less replacement needed● Emission free image – better than fossil● Domestic, cheap, etc

To sudden change after disaster in Japan● 7 plants down for checks already in Germany

Domestic gas could have similar story● Less expensive imports, good for economy● Safer, secure & cleaner than alternatives?● Best quick replacement for nuclear?

• Spare capacity, lower prices than before• Long term potential reserves

Page 25

Biblis plant, Germany – among 7 tested

Over 200,000 protest over nuclear power

Source: ARY News, 26 March 2011

www.sundenergy.com

What is good gas price – for buyers and sellers?

NBP spikes moreoften down than up

● Oversupply, sometimes from Norway and LNG

Higher prices in early winter due to very cold weather

● But back again below oil-link now

● Previous peaks from bottlenecks on import

● Current troughs from bottlenecks on export

Page 26

Data: National Grid and BAFA, May 2011

German border and UK spot prices for gas (comparison of oil-link and spot gas prices)

Apr

02,

200

7M

ay 2

5, 2

007

Jul 1

7, 2

007

Sep

05,

200

7O

ct 2

5, 2

007

Dec

14,

200

7Fe

b 07

, 200

8A

pr 0

1, 2

008

May

21,

200

8Ju

l 10,

200

8S

ep 0

1, 2

008

Oct

21,

200

8D

ec 1

0, 2

008

Feb

03, 2

009

Mar

26,

200

9M

ay 2

7, 2

009

Jul 1

6, 2

009

Sep

04,

200

9O

ct 2

6, 2

009

Dec

15,

200

9Fe

b 08

, 201

0M

ar 3

0, 2

010

May

24,

201

0Ju

l 14,

201

0S

ep 0

2, 2

010

Oct

22,

201

0D

ec 0

9, 2

010

Jan

20, 2

011

Mar

03,

201

1A

pr 1

4, 2

011

0

5

10

15

20

25

30

35

NBP Day-Ahead

BAFA

EU

R/

MW

h

www.sundenergy.com

Gas prices differ in type and in the value chain

Wholesale prices most discussed● German border price

• Quite stable due to oil link

● Spot prices are more volatile ● LNG prices – oil link or spot

But gas is transported and stored● Modulated, factory gate gas is

therefore normally at a much higher price

● Perhaps this is the most relevant price to compare with cost of unconventional?

Local gas may get high feed-in● Some countries are planning

high entry prices for biogas into the gas system – even higher!

Page 27

2007 2007 2008 2008 2009 2009 2010 2010H1 H2 H1 H2 H1 H2 H1 H2

0

5

10

15

20

25

30

35

40

45

50

Border priceBorder priceBorder price

Border priceBorder price

Border priceBorder priceBorder price

Storage, distribution and margin

Storage, distribution and margin

Storage, distribution and margin

Storage, distribution and margin

Storage, distribution and margin

Storage, distribution and margin

Storage, distribution and margin

Storage, distribution and margin

Tax

Tax

Tax

Tax

Tax

TaxTax

Tax

Build-up of German gas prices to indus-try - illustrative

€/M

Wh

Day-ahead NCG price at 1 December 2009 and 1 December 2010

Day-ahead NCG price at 9 May 2011

www.sundenergy.com

Transportation – the next gas frontier with unconventional?

Not having own gas has kept consumption down in many markets● With unconventional gas, availability has improved ● Less clean electricity may be available than expected● Expensive oil imports for transportation sector with

emissions

Natural gas could fuel land and sea transportation…● Cheapest option to reduce GHG (as well as NOx, SOx and

particulate) emissions in transportation?• Also fewer hurdles compared to hybrid and electric vehicles

● …increasingly in combination with “bio-methane”

Local unconventional gas could speed up the transition● Domestic and affordable CNG/ LNG

instead of expensive oil imports

Page 28

Source: Mongabay

CNG CarsLNG Ships

Heavy vehiclesTrainsPlanes??

Vo

lum

e

www.sundenergy.com

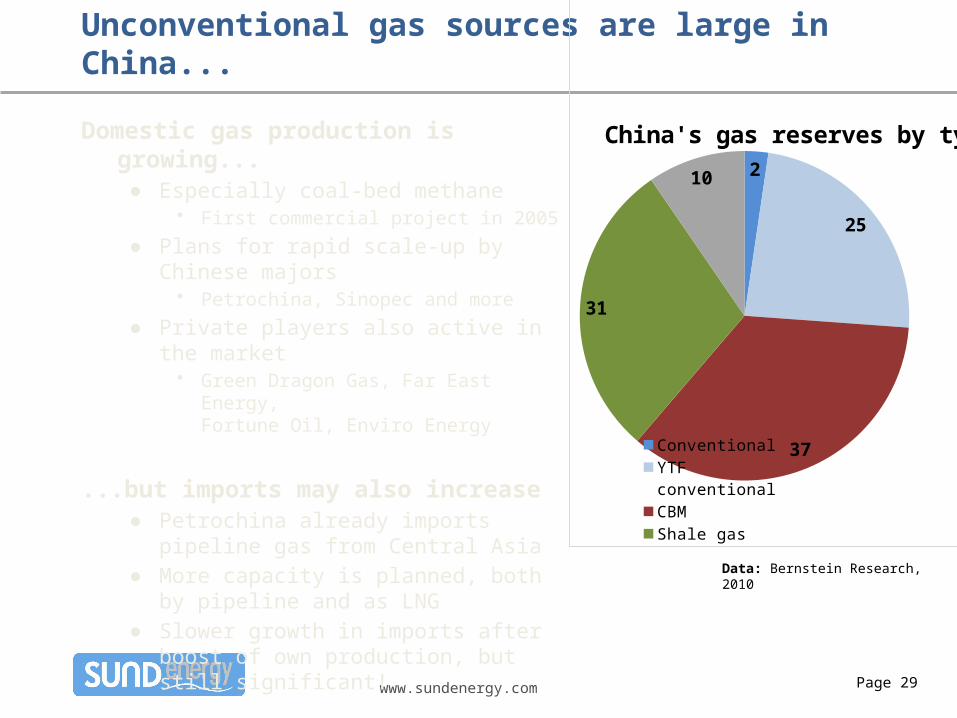

Unconventional gas sources are large in China...

Domestic gas production is growing...● Especially coal-bed methane

• First commercial project in 2005

● Plans for rapid scale-up by Chinese majors• Petrochina, Sinopec and more

● Private players also active in the market• Green Dragon Gas, Far East Energy,

Fortune Oil, Enviro Energy

...but imports may also increase● Petrochina already imports pipeline gas

from Central Asia● More capacity is planned, both by pipeline

and as LNG● Slower growth in imports after boost of own

production, but still significant!

Page 29

2

25

37

31

10

China's gas reserves by type

ConventionalYTF conventionalCBMShale gasTight gas

Data: Bernstein Research, 2010

www.sundenergy.com

… could China be an inspiration for Europe?

Full value chain possible● From CBM directly to CNG for transportation – at a profit:

• $ 9.1/mmbtu to wholesale/ large industry• $14.6/mmbtu on average to cars at own and partner retail gas stations (sold

0.31 bcm in 2010, with large expansion planned in 2011)

Great value of distributed energy in large countries like China● Unconventional gas, wind, other

Page 30

Source: Green Dragon Gas, 2011

www.sundenergy.com

So, let’s consider two scenarios

Unconventional gas takes off● Technology works● Preferred environmentally● Removes some SoS fears● Could reduce oil dependency

Total emissions fall…● Especially from transportation:

Ships, heavy vehicles and cars● Next step could be biogas and

power

…without ruining economy● Reducing other imports● Possibility for export?● LNG becomes backup

Page 31

Europe says no to shale gas● Technology does not work● Reservoirs too deep● Very much cheaper in other places● Strong public opposition ● Less opposition to CCS and wind● Not enough to remove SoS fears?● Gas still considered fossil and oil

linked in pricing● Less focus on climate● OR nuclear OK again

● OR other restrictions on demand: Less heating, cooling, driving…

www.sundenergy.com

How can we predict the future with so much bias?

Energy policy and best mix is a very complex and changing● Politicians try to understand voters’ wishes● Often missing picture, cost levels, system impacts, alternatives etc

Private investors go for what they think will be economic ● Perhaps more prudent than some politicians had hoped● Different view of cost and risk – more realistic or overly careful?● Politicians often do not see that they add to perceived risk by wavering

Long term investments are impacted by the short term ● Nuclear in Europe now seems more negative than several years ago

• Even if they are not in areas prone to earthquakes and tsunamis

● Offshore wind and CCS are being delayed with low spot gas prices

So, in addition to complexity, there is much bias!● Perceptions and favourites, impacted by hype and setting

• Legends “truths” very different from industry science (often quiet)

● Even industry people want simple binary (yes/no) answers

Page 32

www.sundenergy.com

We are happy to discuss further!

Selected recent work by Sund Energy that may be of interest● Impact of Japan on LNG prices – why the market

expected too much● Gas for transportation (road + sea) – market impacts● Unconventional gas – impact on European markets● Security of supply – values and possible solutions● CCS – rethinking solutions for attractiveness● LNG – new areas of use and infrastructure

We also offer strategic and commercial advice● Producers, TSOs, traders, large buyers, governments● Gas, electricity, CCS and more

[email protected], +47 917 86 928Sund Energy AS, Meltzersgate 4, N-0257

Oslo, Norway

Page 33Page 33