Www.mohealthwins.org More Than You Ever Wanted to Know About Administrative Costs Leveraged...

20

www.mohealthwins.org More Than You Ever Wanted to Know About Administrative Costs Leveraged Resources Accrued Expenditures & Unliquidated Obligations MoHealthWINs TAACCCT Grant Prepared by the OTC Finance Office October 26, 2012 Financial Compliance Issues

-

Upload

devon-biggie -

Category

Documents

-

view

214 -

download

0

Transcript of Www.mohealthwins.org More Than You Ever Wanted to Know About Administrative Costs Leveraged...

www.mohealthwins.org

More Than You Ever Wanted to Know

About Administrative CostsLeveraged Resources

Accrued Expenditures & Unliquidated Obligations

MoHealthWINs TAACCCT Grant Prepared by the OTC Finance Office

October 26, 2012

Financial Compliance Issues

Grant Detail and Contact InfoTotal Award: $19,982,296.00 CFDA #17.282

Period of Performance: 10/1/11 to 9/30/14

Fiscal Lead: Ozarks Technical Community College Finance OfficeVice Chancellor of Finance – Marla MoodySenior Staff Accountant – Chasity Daniels

Grants Accountant – Betty Denson: 417-447-4831, [email protected]

Program Director – Dawn Busick housed at MCCA Office: 573-634-8787

Information Resources on MCCA Website: www.mccatoday.org

New Reimbursement Report• MHW Reimbursement Report updated:• Lines for Accrued Expenditures and Unliquidated

Obligations • Funds expended to date (actual requests) and

committed to date (includes accrued expenditures and unliquidated obligations)

• Additional field to show percentage of administrative funds spent to date

www.mohealthwins.org

Administrative Costs• 8% administrative cap applied across total budget • Consortium members with ICR may want to claim all

administrative costs as indirect • Consortium members without indirect costs may

claim administrative costs in direct line items • Must report total administrative costs claimed on

each reimbursement report

Administrative Costs• Not related to direct provision of workforce

investment services, including services to participants and employers

• Can be personnel or non-personnel• Can be direct or indirect

Administrative Costs - Examples• Accounting, budgeting, auditing• General legal services functions• Information system development (unless related

to program delivery)• Support personnel, travel costs, other goods and

services related to administrative functions

Program Costs• Directly related to provision of workforce

investment services, including services to participants and employers

• Can be personnel or non-personnel• Can be direct or indirect

Program Costs - Examples• Vendor contracts (unless solely for administrative

functions)• Case management• Information system development for tracking

participant and performance information• Support personnel, travel costs and other goods

and services related to program functions

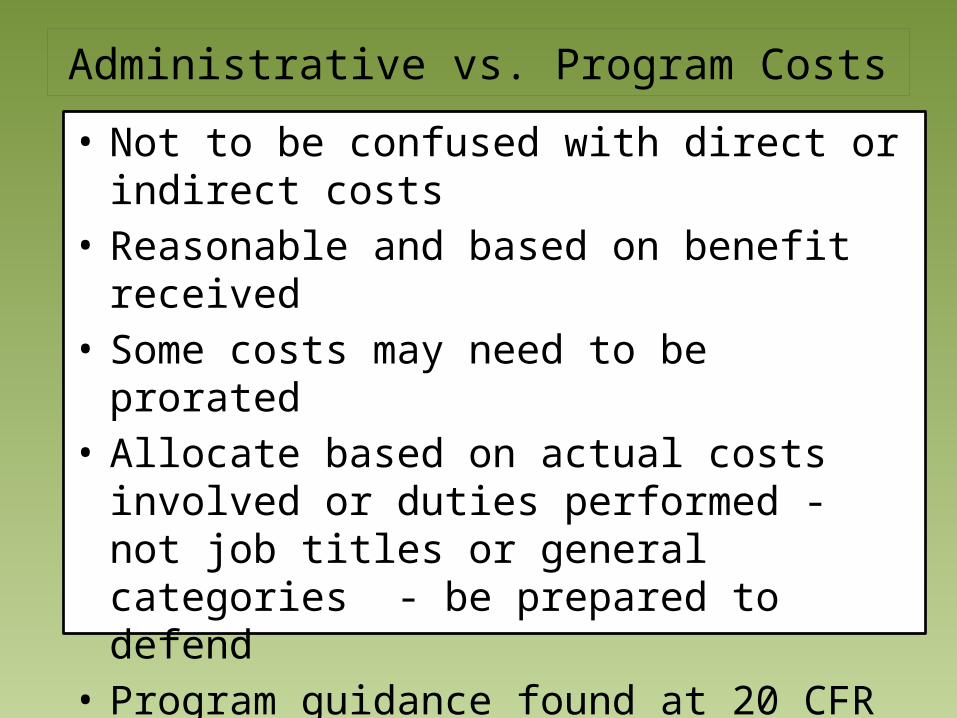

Administrative vs. Program Costs• Not to be confused with direct or indirect costs• Reasonable and based on benefit received • Some costs may need to be prorated • Allocate based on actual costs involved or duties

performed - not job titles or general categories - be prepared to defend

• Program guidance found at 20 CFR 667.220

The MHW Grant & Leveraged Resources

• MHW Grant does not require match – requires leveraged resources reporting

• Leveraged resources not defined in federal regulations or related administrative requirements

• 29 CFR 95.23 provides limited guidance • Leveraged resources could be described as: •“all resources used by the grantee to support grant

activity and outcomes, whether or not those resources meet the standards required for match”*•DOL Training Handout: Background for Match and Leveraged Resources

What are Leveraged Resources?• May be paid for with federal or non-federal funds.• Includes both cash and in-kind contributions.• Must be allowable under the OMB cost principles.• No administrative cost limitation on LR.• Consortium committed to report over $11 million in

leveraged resources over the life of the grant. • Federal Project Officer will decide what actions to

take if consortium not able to meet commitment.

Reporting Leveraged Resources• Reported each quarter - 9130 Report (OTC Finance

Office) and Program Narrative (Program Director)• Colleges report at least quarterly • Totals listed on Reimbursement Report Form• Summary sheet attached - for reporting and

verification• Keep backup documentation for on-site monitoring

Leveraged Resources - Examples• Unclaimed indirect costs• Direct costs that could have been charged to the

grant, but were not: donated space, staff salaries, supplies, outreach, web costs, travel costs in support of the grant, etc.

• Equipment used for grant – purchased with institutional funds, other federal funds, or donated

• Curriculum costs not charged to grant• Documented third party donations of space,

personnel, or other resources

Leveraged Resources Valuation• Guidance available at 29 CFR part 95.23• Not used for contributions on other federal

projects• Necessary, reasonable, verifiable• Allocate to show amount of benefit to grant• Document and be prepared to defend valuation

Accruals and Obligations• DOL requires accrual reporting• Better reflection of true program costs • Colleges report totals on Reimbursement Report• Retain documentation for on-site monitoring • OTC Finance Office reports on Form 9130• Failure to report on accrual basis could lead to

loss of funds

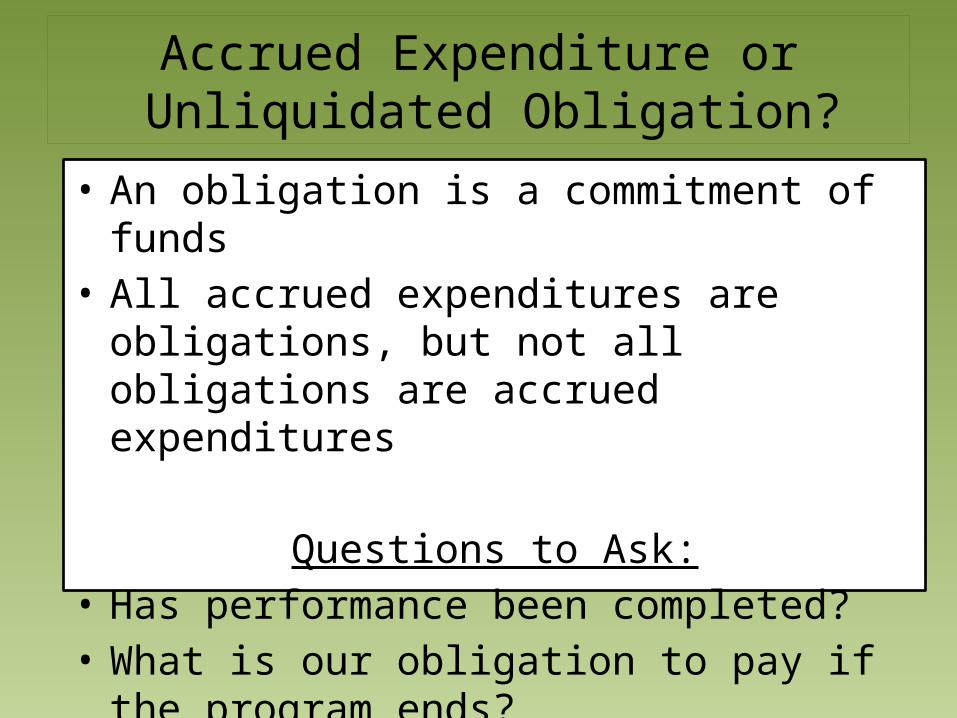

Accrued Expenditure or Unliquidated Obligation?

• An obligation is a commitment of funds• All accrued expenditures are obligations, but not

all obligations are accrued expenditures

Questions to Ask:• Has performance been completed? • What is our obligation to pay if the program

ends?

Details of the Obligation• Unpaid delivered goods - accrued expenditure• Contracted goods - unpaid, but not yet delivered –

unliquidated obligation• Payroll - accrual if work performed, not yet paid• Travel expenses or utilities - may be accrual• Contracts - may be accrual or obligation• Contract - work performed, not paid - accrual • Contract with legal commitment - may be obligation • Review contract terms

Questions?

This workforce solution was funded by a grant awarded by the U.S. Department of Labor's Employment and Training Administration. The solution was created by the grantee and does not necessarily reflect the official position of the U.S. Department of Labor. The Department of Labor makes no guarantees, warranties, or assurances of any kind, express or implied, with respect to such information, including any information on linked sites and including, but not limited to, accuracy of the information or its completeness, timeliness, usefulness, adequacy, continued availability, or ownership.

This PowerPoint and Other Informational Resources are Available on the MCCA Website at www.mccatoday.org