Document

15

Written by Stephen Watson CEO - Care Consort How To Win The Future Care Market

-

Upload

care-consort -

Category

Documents

-

view

212 -

download

0

description

An exploration of the UK care industry, focusing on market trends and forecasts. The book also presents winning strategies that care providers can introduce in order to remain CQC compliant and successfully operate in this competitive environment.

Transcript of Document

Written by Stephen WatsonCEO - Care Consort

How To Win The Future Care Market

The future demands of UK care market 04

Proportion of people 65 and older 05

Estimated & projected age structure of the UK elderly population 06 Market size, current and future trends of the UK care market 07 Competition in the UK care market 08

Case Study- The paperless care provider 10

Index

3

Introduction

As a direct result of my work with clients who have suffered, in varying degrees, with chronic mental and physical ill health, when I think of their ‘progress’ the word ‘recovery’ springs to mind: the small steps taken towards a greater good. This fits with the gen-eral concept of recovery which is based on the optimistic premise of hope: that despite enduring illness a glimmer of light travels through the deep, dark tunnel of despair.

From a care service point of view it relies on the ability of an organ-isation to successfully shift focus from seeing people as hopelessly ‘stuck’ with an illness, to a position where goals are actively rec-ognised and encouraged despite the ongoing challenges.

For many years I worked with clients who suffered with debilitat-ing mental ill health, and institutionalised to the point where they would only see themselves through their illness. “I don’t think I can achieve. I am a schizophrenic”, they would often remind me. Their point being that their diagnosis, and defeated resignation of their illness has left a sense of worthlessness.

Leese D et al (2014) ‘Recovery-focused practice in mental health’. Nursing Times; 110: 12, 20-22 identified in her article that recovery focused care sits around three central themes: hope, person cen-tred care and service user collaboration. She highlighted the need for staff to incorporate these themes within their daily practice, in order to build a trusting relationship where service users feel lis-tened to and can become an equal partner in their care delivery.

In our ageing society, how do care services ensure that they can incorporate these themes into their organisation in an environ-ment which is time, money and often staff constrained? It was this question amongst others, which led to my general exploration of the fast changing pace of the care sector, and how as providers we might prepare successfully for the future.

Medical innovations and the rapid evolution of technology have made a tremendous impact on UK’s demographic structure. These changes are creating a significant impact on the long- term care market in the UK.

There are several major factors causing these demographic changes;

• Due to improvements in health, diet and preventative care, people are living longer than ever before.

• Women are having fewer children than the previous generation.

• Around a third of children born in the UK in 2012 are expected to survive to celebrate their one-hundredth birthday.

• In 2012, the number of over 65s and older surpassed 10 million for the first time.

• In 2007, the number of people in Britain aged over 65 outnumbered the number of people under 16 for the first time.

• Between 1901 and 2010, the number of people aged 40 and older trebled from 9.7m to 30.8m.

• Baby Boomers: born during a period of rapid population growth and social change between 1946-64, with 17m births recorded in Britain alone during this period.

The future demands of the UK care market

4

Proportion of people aged 65 and older; UK population mid-

1974 onwards

In terms of increases in the number and proportion of older people in the UK, the population aged 65 and over, has grown by 47% since 1974 to make up nearly 18% of the population in 2014, whilst those aged 75 and over have increased by 89% over the same period and now ‘represent’ 8% of the total population.

Sources: UK Government,

5

Estimated & projected age structure of the United Kingdom elderly population, 2015 to 2040

Sources: OECD.sat

According to the above charts, the dramatic demographic shift of Britain’s population within the next 25 years may not only increase opportunities but could pose threats in the care sector. However, the demand for care will continue to increase because of increasing life expectancy and ageing. On the other hand, this will impose pressure on the government. The government will have to cut down on expenditure in health care drastically, forcing private sector providers to rely on ‘economies of scale’ significantly more to survive in the marketplace.

6

Market size & current and future trends of the UK care industry

The UK care sector is run by both public and private healthcare providers. Public providers include those managed by local authorities and the NHS; a small percentage of homes in the UK are run by the public sector, whereas the majority of the healthcare market is dominated by private sector health care providers.

During the decade prior to the economic downturn, the UK private care market witnessed robust growth, benefiting from an ageing population and a growing demand for the health services. The total UK private care market grew by 3.9% and 1.4% in 2012 and 2013, respectively. The market is dominated by the long-term care sector which accounted for 47.4% of total private healthcare revenue in 2013, followed by private acute medical care (22.1%) and psychiatric care (16%).

Annual market growth rates are expected to accelerate between 2016 and 2018, growing to 3.3% in 2018. The long-term care sector will remain the largest sector within the private care market. (Sources: Research and Markets).

However, the top ten companies account for approximately 20% of the UK’s private sector capacity. Four Seasons is the largest operator of care homes in the UK, and Bupa the second largest. HC-One Limited is ranked third in terms of bed capacity of the UK care market.

7

Competition in the UK Care Market

The care home market in the UK is extremely fragmented and competitive. Moreover, it is probable that those major players will increase their market share drastically in the future. The market is still very much decentralized, and the level and impact of competition is considerable.

In addition, due to more cautious lending policies and high equity requirements, the cost to enter the care home market will continue to be a barrier. However, invasion by multinational players in the market is inevitable.

The UK care market will continue to grow, due to demand in the care industry. This will provide distinct opportunities for care providers to expand their market share by increasing efficiency in all areas of their business. Nevertheless, it is compulsory for all care providers to comply with the Care Quality Commission (CQC) standards and regulations to survive in the industry.

The failure of the CQC inspection will have a substantial negative impact overall on the business. Furthermore, local governments are disinclined to provide new placements for the care homes that do not obtain a good rating from their CQC inspection. To become a successful entrepreneur in the care industry it is compulsory to achieve the national standards required by the CQC.

8

In future articles I will discuss strategies to win the future UK care market.

• How to achieve “economies of scale”.

• Market segmentation and exploring new markets within the care industry.

• How to win the trust of main stakeholders.

• How to reduce employment turnover by using internal marketing strategies.

• The impact of CSR on business performance.

• Monitoring competitor activities.

• CRM Marketing.

• PR and advertising.

• Integrating strategy with execution infrastructure.

• Customer focus growth strategy.

• How to achieve ROI by using integrated digital marketing strategies.

9

Case Study- The paperless care provider

Positive Community Care Ltd (PCC Ltd) is an established provider of care homes, supported housing and home care. They were using the so-called ‘market leading’ software in 2014 when they received three negative crosses on their inspection report!

Some problems highlighted by CQC were:

1. More person centered care planning required

2. Evidence required as to how client activities matched the care plan.

3. Poor record keeping

4. More robust risk assessments

The management decided that they needed to change their software and chose Care Consort. We took care of all the migration from their previous care management software.

The decision to use Care Consort transformed their service!

Their next CQC report (April 2015) was good in every area. Here are some excerpts.

“Care plans were clear and comprehensive…and addressed each person’s individual needs, detailed what was important to them, how they made decisions and how they wanted their care to be provided.”

10

“

“Arrangements to assess and monitor the quality of the service were in place, so that people benefited from safe quality care, treatment and support.”

Migrating from paper to computerised system

When we first discussed the idea of ‘going paperless’ it was simply called IT. We had been managing with paper for years and had always had a good rating even back in the CSCI days.

Some homes even had a ‘lighter touch’ on the inspections although it was still highly regulated in comparison to other business sectors. So we soldiered on, developing a number of different systems that allowed us to keep on top of the important areas of the business.

We had various spreadsheets for multiple specific functions and paper forms with signature checks for monitoring areas of the business. It all seemed to work well until the landscape changed and CQC began to request evidence of how the activities of the service users related to their care plans?

Now this is something that we had always tried to ensure was performed fully but when the CQC requested evidence it created a few problems. Firstly, we found that we had information listed in various sources such as handover books, daily records, and care plans. Sometimes the staff (through no fault of their own) did not describe fully the tasks that were done for that day or wrote basic info that didn’t fully reflect the tasks set for them for that day.

11

This made it difficult to prove not only that the activities set for Mr X had actually been carried out but also that they were in line with his needs and reflected his care plan.

Sometimes in the daily reports the carer had only entered minimal information, perhaps because they were too busy or even because English may not have been their first language. The biggest problem was that the inspection is based heavily on how efficiently you and your team can provide the requested information in a timely manner.

This is because if you cannot do this consistently across the key areas of your organisation, you are liable to be caught out - not necessarily because your service is poor, but it can be perceived as such by the inspector due to poor record keeping and communication workflows at all levels.

So eventually we made the decision to try one of the so called’ market leading care management systems although it was fairly expensive and we did not use all its features. Migrating was easy from paperless to computer as we just ‘ parked’ all our paper files in store and started using the computerised system instead. However problem was that we still needed other systems in order to truly run an excellent care setting.

For example, we used a separate online training company, and that worked quite well but it became more of a fire-fighting tool when it became clear that staff hadn’t completed training that was set for them some time ago. We needed something more proactive that informed us when we were at risk of not meeting CQC standards.

12

The defining moment for me was when we recently employed a new staff member and had to print out the 350 page Care Certificate for him to complete. Six months later he left, I then had to print out another 350 pages for his replacement!

Keeping track of all the staff ‘s progress with their Care Certificate and other training was a matter of scouring through a ‘training folder’ which was generally well stocked but had to be matched with the online training they were also doing on another website - which required another password, and so it went on.

Migrating data from one computerised system to a better computerised system

We then made the decision to transfer our care management software over to Care Consort. It was clear from the beginning that by default Care Consort was ‘set up for success’ from the very design of the system, and by using this transparent and logical solution we quickly became confident that we could now provide the evidence ‘at a glance’ when requested. Migration was all done within a week and all our data was seamlessly transferred by Care Consort.

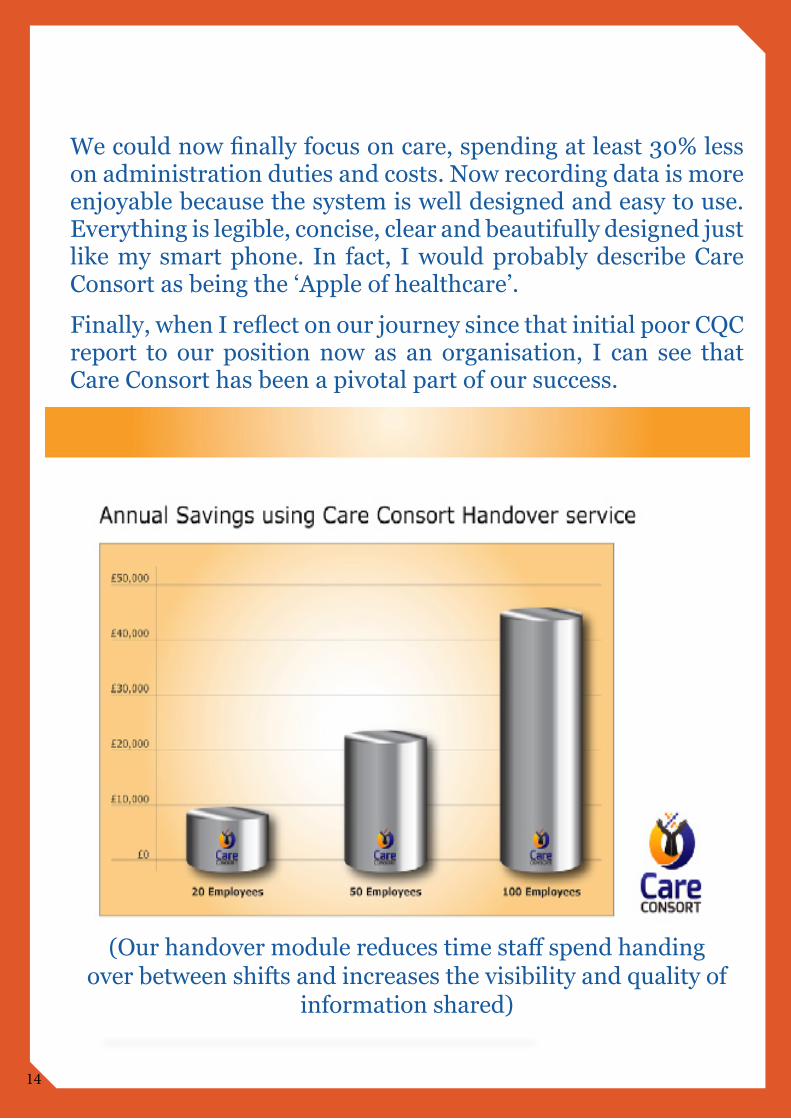

We could also see in real time the stage the service users had reached in terms of meeting their goals. This made a massive difference to the delivery of care in a demanding and time-short environment. Cost savings were made immediately through ‘Handover’ and ‘Time and Attendance” modules which more than covered the cost of the whole system, so this, too was a bonus.

We could also now easily demonstrate to placement teams exactly how we planned to deliver care in a truly person-centered format, which contributed towards our quick return to full occupancy in a tough environment.

13

We could now finally focus on care, spending at least 30% less on administration duties and costs. Now recording data is more enjoyable because the system is well designed and easy to use. Everything is legible, concise, clear and beautifully designed just like my smart phone. In fact, I would probably describe Care Consort as being the ‘Apple of healthcare’.

Finally, when I reflect on our journey since that initial poor CQC report to our position now as an organisation, I can see that Care Consort has been a pivotal part of our success.

14

(Our handover module reduces time staff spend handing over between shifts and increases the visibility and quality of

information shared)

Click here to find out how Care Consort can boost your service.