WRITING AN EFFECTIVE CREDIT MEMORANDUMttsmedia.ttstrain.com/CreditHORE050516.pdf · WRITING AN...

43

Bankers Insight Group, LLC TOTAL TRAINING SOLUTIONS May 2016 WRITING AN EFFECTIVE CREDIT MEMORANDUM Preparing Successful Loan Presentations Jeffery W. Johnson Bankers Insight Group, LLC [email protected]

Transcript of WRITING AN EFFECTIVE CREDIT MEMORANDUMttsmedia.ttstrain.com/CreditHORE050516.pdf · WRITING AN...

Bankers Insight Group, LLC

TOTAL TRAINING SOLUTIONS

May 2016

WRITING AN EFFECTIVE CREDIT MEMORANDUM Preparing Successful Loan Presentations Jeffery W. Johnson Bankers Insight Group, LLC

[Bankers Insight Group, LLC] Page 2

OBJECTIVES

To make you a better banker

To understand the importance of good written communication

To improve clarity, conciseness and completeness of written communications

To increase emphasis on planning and organizing

To identify individual strengths and weaknesses

Standards of Care

What would a reasonable and prudent banker have done under similar circumstances?

The primary purpose of loan documentation is to document your actions as being prudent and

proper

Your credit files must document a consistently applied approval process. That process should

address, at a minimum, the following points:

Essence of Credit

Purpose and basis of the credit

Primary and secondary source of repay

Written repayment program

Collateral valuations

Conformity to credit policy

The five C’s of credit

Strengths and weaknesses

Justification for exceptions to underwriting

Makes recommendation

Grades credits

[Bankers Insight Group, LLC] Page 3

Contains information to make decision

o Company financial statements

o Tax returns

o Personal financial statements

o Applications

Credit Memos

Primary means of communication within banking industry

Serves three functions:

1. Supports or recommends action

2. Provides information on the condition and status of a customer relationship

3. Provides a record of thoughts and actions relative to a customer relationship

Memos are to be succinct and to the point, but we violate this idea

Readers of credit memos are skilled bankers. Therefore, it is not necessary to state the

obvious

Memos should present relevant material facts and writers thoughts and opinions

The written opinions should be supported by facts

Anything you write in a memo will become public record if you end up in court with a

customer

[Bankers Insight Group, LLC] Page 4

ORGANIZATION

Planning

Questions to consider:

1. What is my purpose?

To inform

To persuade

To get action

To recommend

To advise

To identify a problem

2. Who is my audience?

Key Audience

o Senior Credit Officer

o Loan Committee

o Manager

o Colleagues

Secondary Audience

o Consider their needs

o Use appropriate tone

o Avoid industry language

3. How can I best convey my message?

Logical presentation gives you credibility

Guides the reader in the direction you want them to go

[Bankers Insight Group, LLC] Page 5

Positioning

Identify your position

o The main idea of your entire report

o All statements, conclusions or recommendations should support position

Establish your major discussion areas

o The major points that helped lead you to your position

o Begin by noting your major discussion areas early in your presentation

Results - helps writer to focus and the reader to comprehend the ideas that follow

Outlining

o Places topics in an orderly manner and will ultimately:

Save time

Improves organization and readability of your writing

Allows a step-by-step approach

Allows writer to avoid missing the most important facts

WRITING

Paragraph Development

o Breaks writing into single ideas

o Keeps writing in a uniform and orderly pattern

o Should have a topic sentence

o The topic sentence represents the main idea

o Topic sentences are often the 1st sentence

o Each sentence should contribute to paragraph’s purpose

[Bankers Insight Group, LLC] Page 6

Transitions

o Show the relationships between ideas

o Helps the flow of your ideas: they act as signals for the reader to follow

o Rid your writing of the “choppy” sound

o Examples:

Without Transitions

o “Profits have been below average for the past three years. Asset growth has

been nearly twice that of its peer group. Net worth has decreased by 20%.”

With Transitions

o “Profits have been below average for the past three years. During the same

period, asset growth has been nearly twice that of its peer group. As a result,

net worth has decreased by 20%.”

Summaries

o Should not introduce any new ideas

o Not always necessary, unless the situation warrants it. It may be redundant

o Summaries are helpful when:

Your position is very controversial

Your position may be unpopular with your reader

The report is very long

The structure of the report is very complex

WORD USAGE

Always choose the right words

Write to express, not to impress

Avoid stuffy and vague words

Avoid using a heavy style of writing

[Bankers Insight Group, LLC] Page 7

o It is improper for business communication

o Indicates unclear or illogical ideas

o Indicates lack of knowledge by bluffing with complicated and wordy writing.

Utilize a simple writing style

o The more complex the subject, the more precise and simple the writing

o Understanding words and sentences should require little energy by the reader.

Wordiness – say what you need to say with the fewest words possible

Instead of Why not write

At the present time Now / Currently

In the near future Soon

A majority of Most

A number of Several / Many / Some

In the amount of For / Of

With reference to About

First of all First

On an annual basis Annually

FORM AND APPEARANCE

o Avoid producing a page of solid print. Readers like short, skim-able writing.

o Visual appearance should aid understanding, not hinder it.

o Make reports eye catching with headings, bold face, underlining, italics or

bullets. This method calls attention to areas that are important.

o Paragraphs should average 7-10 lines

o Use repetition for emphasis in long reports

o Graphics can add variety and professionalism to reports

Bankers Insight Group, LLC Page 8

ALLISON WRIGHT BANK COMMERCIAL LOANS

GUIDELINES FOR PREPARATION OF CREDIT APPROVAL DOCUMENTS

July 25, 2012

Credit Approval Document Overview

The purpose of a standard Credit Approval Document is to promote a consistent approach towards preparing

credit approval presentations. The Credit Approval Document format is intended to convey to others the

lending officer's analysis and understanding of the inherent credit risk and strategies for the management of

that risk.

The three cornerstones of a successful credit portfolio are Soundness, Profitability and Growth, in that order.

Profitability and growth are meaningless if the underlying portfolio is not sound. This does not mean that a

sound portfolio has no credit risk. Rather, the underlying credit risk must first be understood and, once

understood, then managed.

Other purposes of the Credit Approval Document format are to present and document the following topics in

a consistent manner:

Credit approval rationale.

Purpose of proposed credit presentation.

Proposed loan quality rating rationale.

Key risks and structural issues.

Strengths and weaknesses (i.e. cash flow, collateral, guarantor) of the borrower and the credit facilities.

Sources of repayment and plans for monitoring.

Comparison of the proposed credit presentation with approved credit policies, underwriting standards and

underwriting guidelines.

Total ALLISON WRIGHT BANK relationship and relationship strategy, including a risk management

strategy for the subject credit exposure.

The Credit Approval Document is an internal document used primarily to clearly communicate conclusions

of the lender. The reader should not be left to hunt for or ascertain the author's conclusions. Conclusions

should be clearly stated and logically supported by the rationale for the conclusions.

The Credit Approval Document is intended to be a self-contained, stand-alone document which a

knowledgeable, experienced lender who is not a specialist in the specific industry being addressed

should be able to understand. The Credit Approval Document should fully support and explain the credit

request without the need for verbal explanation or reference to external documents. All lenders should

remember that it is in their best interest to convey their message and conclusions in an easy-to-read format.

The audience will include the following readers:

Chain of authority required to approve or concur with the transaction (e.g. Approval Matrix)

Credit examiners, including the ALLISON WRIGHT BANK Credit Review Officers, FDIC, State,

external auditors, etc.

Other lending personnel who need to brief themselves on the relationship, e.g. as account

management responsibilities change

Counsel representing ALLISON WRIGHT BANK and others responsible for preparing loan

documentation

Bankers Insight Group, LLC Page 9

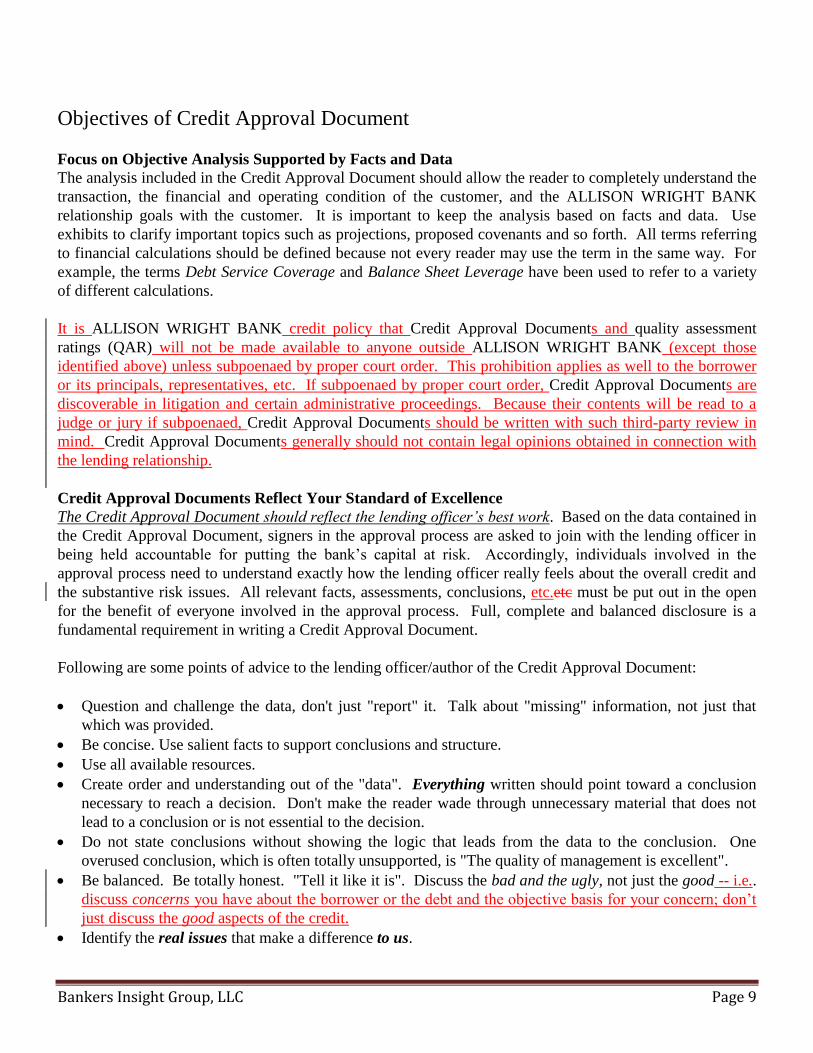

Objectives of Credit Approval Document

Focus on Objective Analysis Supported by Facts and Data

The analysis included in the Credit Approval Document should allow the reader to completely understand the

transaction, the financial and operating condition of the customer, and the ALLISON WRIGHT BANK

relationship goals with the customer. It is important to keep the analysis based on facts and data. Use

exhibits to clarify important topics such as projections, proposed covenants and so forth. All terms referring

to financial calculations should be defined because not every reader may use the term in the same way. For

example, the terms Debt Service Coverage and Balance Sheet Leverage have been used to refer to a variety

of different calculations.

It is ALLISON WRIGHT BANK credit policy that Credit Approval Documents and quality assessment

ratings (QAR) will not be made available to anyone outside ALLISON WRIGHT BANK (except those

identified above) unless subpoenaed by proper court order. This prohibition applies as well to the borrower

or its principals, representatives, etc. If subpoenaed by proper court order, Credit Approval Documents are

discoverable in litigation and certain administrative proceedings. Because their contents will be read to a

judge or jury if subpoenaed, Credit Approval Documents should be written with such third-party review in

mind. Credit Approval Documents generally should not contain legal opinions obtained in connection with

the lending relationship.

Credit Approval Documents Reflect Your Standard of Excellence

The Credit Approval Document should reflect the lending officer’s best work. Based on the data contained in

the Credit Approval Document, signers in the approval process are asked to join with the lending officer in

being held accountable for putting the bank’s capital at risk. Accordingly, individuals involved in the

approval process need to understand exactly how the lending officer really feels about the overall credit and

the substantive risk issues. All relevant facts, assessments, conclusions, etc.etc must be put out in the open

for the benefit of everyone involved in the approval process. Full, complete and balanced disclosure is a

fundamental requirement in writing a Credit Approval Document.

Following are some points of advice to the lending officer/author of the Credit Approval Document:

Question and challenge the data, don't just "report" it. Talk about "missing" information, not just that

which was provided.

Be concise. Use salient facts to support conclusions and structure.

Use all available resources.

Create order and understanding out of the "data". Everything written should point toward a conclusion

necessary to reach a decision. Don't make the reader wade through unnecessary material that does not

lead to a conclusion or is not essential to the decision.

Do not state conclusions without showing the logic that leads from the data to the conclusion. One

overused conclusion, which is often totally unsupported, is "The quality of management is excellent".

Be balanced. Be totally honest. "Tell it like it is". Discuss the bad and the ugly, not just the good -- i.e..

discuss concerns you have about the borrower or the debt and the objective basis for your concern; don’t

just discuss the good aspects of the credit.

Identify the real issues that make a difference to us.

Bankers Insight Group, LLC Page 10

View everything from the perspective that we are putting ALLISON WRIGHT BANK capital at risk.

Do not assume the impartial perspective of an external rating agency that has no capital directly at risk in

the transaction.

Be reader-friendly. Act as a guide to lead your reader through your data and logic to reach your

conclusions. Use charts when needed.

Be consistent. Check your Credit Approval Document to make sure that the facts and opinions you state

are consistent throughout all portions of the Credit Approval Document.

These points of advice are always subject to the general rule that facts and data must support conclusions.

All documented opinions, but especially those that are negative, must be based on facts you know

Credit Approval Document Narrative “Highlights of Key Findings”

Information presented should be precise but complete. Objective analysis is of primary importance. The

analysis is expected to be balanced. Balanced means to reveal all relevant data, good and bad, and arrive at

an objective analysis of the risks. The focus should be driven by the facts and data, with emphasis on why

and how the facts impact the customer and credit facilities made available by Allison Wright Bank.

1. Transaction Description:

The three cornerstones of a successful credit portfolio are Soundness, Profitability and Growth, in that order.

This does not mean that credit risk is to be avoided; rather, the underlying credit risk must be understood and

managed.

Summary (Reason for Request and Nature of Business)

Describe the transaction being considered. The Summary could be as simple as a new term loan for

equipment purchases or could be a complete description of a vertically integrated operation. Use exhibits to

further clarify discussions and refer the reader to separate exhibits as appropriate. Be detailed.

Credit Approval Rationale

This section should include a succinct rationale why the proposed credit action is being recommended from a

credit risk management perspective. Explain the critical credit factors that support the recommendation for

approval. Any approval rationale based on relationship, profitability or business growth factors, although

important, should be clearly identified as such and discussed separately. In essence, discuss why the proposed

action makes sense.

Rate/Term

This section should discuss the rate and terms, and thoroughly explain any concessions made on either rate or

term. Consistency with Bank objectives should also be discussed.

Bankers Insight Group, LLC Page 11

Sources and Uses

For all construction projects, a complete Source and Use of Funds analysis should take place in this section.

Owner equity in projects should be thoroughly explained.

The three cornerstones of a successful credit portfolio are Soundness, Profitability and Growth, in that order.

This does not mean that credit risk is to be avoided; rather, the underlying credit risk must be understood and

managed.

2. Economic and Competitive Environment:

The purpose for analyzing the economic and competitive environment is to assess the factors that have an

impact on the industry and borrower. This section should be divided into two areas.

The Industry subsection should discuss macro factors such as environmental forces, government

regulation, demographic changes and technology. It should also include information on the structure and

profile of the industry. Industry data should include any recent developments, especially in volatile

industries.

The Borrower subsection should include the entity's competitive position, as well as strengths and

weaknesses that are critical to the future success of the business. This may include an analysis of core or

major product lines as reflected by the borrower's business plan or competitive position.

3. Management:

Objectively evaluate the management of the company. Avoid the use of adjectives as they tend to be

subjective. Comments should be based on facts. Unsupported phrases such as “John is an excellent

manager", etc. are subjective in nature and provide no support to the analysis. Instead, refer to industry

experience, references from others in the industry and the depth of experience of management. This may

include the number of years in the industry, prior positions, professional background, professional

certification, and so forth.

Lastly, discuss substantive investors as well as the use of outside advisors such as tax and legal counsel,

accounting firms, outside directors, investment bankers, etc.

4. Critical Financial Developments/Trends:

This section should thoroughly explain and support the historical and current financial numbers and ratios as

summarized on the Executive Summary page of the Credit Display. Report the nature and quality of the

financial statements on which the financial analysis is based (e.g. annual CPA audit {clean or qualified

opinion}, unaudited annual/interim statement, 10Q report, consolidated, combined, income tax returns, etc.

State the source of the financial statement, e.g. name of CPA firm, company prepared, etc. An unaudited

statement reduces the quality of the information. If the financial statement is not audited, the lending officer

should address the reasons why the company is not providing audited statements. How is the bank assured of

the integrity of the information and how is the risk of an unaudited statement mitigated?

This Section should have three distinct sub-sections: Balance Sheet, Income Statement, and Cash Flow.

Describe the historical financial performance of the company with specific emphasis on the most recent fiscal

year and current interim period. For complex ownership structures, consolidating financial statements may

need to be included. Comment on key performance targets such as sales, margins, and balance sheet trends.

Bankers Insight Group, LLC Page 12

Highlight any specific accounting techniques that are important in analyzing the company (e.g. FIFO vs.

LIFO inventory valuation, etc.) If appropriate, compare company with industry standards or comparable

companies. When possible, briefly summarize the borrower's performance during the last recession. Discuss

the capital structure of the borrower (e.g., senior debt, subordinated debt and equity components).

Analyze the trends as opposed to simply reporting the numbers. Get behind the numbers; for example,

provide your best analysis of the factors that caused a decline in sales and management's response, as

opposed to simply stating that sales declined.

Address historical fixed charge coverage or debt service coverage as applicable. Discuss cash flow adequacy

historically.

5. Evaluation of Repayment Sources/Projections:

This section is used to describe future repayment ability and should pick up where the above historical

analysis left off. This section should analyze the adequacy of stated repayment sources in quantitative terms.

Again, this Section could include three distinct sub-sections: Balance Sheet, Income Statement, Cash Flow.

A “Bank Base Case” (Most Likely) projection is expected when maturities exceed one year. Additionally, a

“Management Case” and a “Downside Case” are strongly encouraged in larger transactions when maturities

exceed one year. Please label each page of the projections (e.g. Management Case, Bank Base Case,

Downside Case.) Use exhibits to fully document the assumptions used to construct each “case” or scenario.

Depending upon the financial stability of the proposed credit, sensitivity analyses should also be presented.

If practical, present a "Break-Even" scenario showing the level of cash flow necessary to meet debt service,

mandatory capital expenditures and other fixed charges. It should be noted that Allison Wright Bank’s

official definition of fixed charge coverage (FCC) is (EBITDA cash taxes cash dividends – maintenance

capital expenditures) (mandatory debt retirement + cash interest). Use MOODYS spread sheet format for

historical and projected cases, where MOODYS is available. Maintenance capex should be thoroughly

explained.

Analyze the projections either in the body of the report or in an exhibit. Refer the reader to exhibits for

clarification. Use footnotes on the MOODYS spreads for further clarifications and refer the reader to the

footnotes. Discuss the impact of any sensitivity cases and why the credit risk remains acceptable.

A downside sensitivity analysis should not usually be based on growth assumptions resulting in improving

performance (e.g., increasing EBITDA, cash flow available for debt service, etc.). If a "Break-Even"

scenario is used for the Downside Case (e.g., holding fixed charge coverage or debt service coverage equal to

1.0x), it would probably be helpful for the analysis to include a comparison of the "Break-Even" EBITDA to

both historic and Management Case EBITDA. For example, this comparison could illustrate the amount of

deterioration that could occur before operating cash flow would be insufficient to cover debt service

requirements and other defined fixed charges (or the amount of cash flow growth required to cover debt

service requirements).

If sale of assets is a material source of repayment, document what assets will be sold, the book value, the

estimated net proceeds, the source of the valuation, potential buyers, and the expected timing of the sale. If

Bankers Insight Group, LLC Page 13

refinancing is a source of repayment, provide an analysis of the expected source and scope of refinancing or

information on the most recent public debt and/or equity offering for the borrower.

Sections 4 and 5 may at times have some overlap. The important thing to remember is that these sections

should thoroughly address and analyze the historical, present and future cash flows and/or other relevant

repayment sources.

Detailed financial analysis of the guarantor(s) should also be included in this section, as appropriate.

6. Collateral Evaluation/Survey Results:

Describe in detail the value, valuation method, advance rate and an appraisal date for all collateral.

Collateral should be described in enough detail so that the reader can determine what documentation should

be included in files. Also disclose required insurance protections, as appropriate (e.g. hazard insurance).

This information can be summarized in an exhibit.

Liquidation costs, if not incorporated in the advance rate, are the costs incurred to gain control of and

liquidate the collateral under "quick sale" conditions (e.g. transportation, insurance, commissions, delivery,

legal fees, etc.). While these costs may not be explicitly known, please estimate based on your knowledge of

the borrower and nature of the collateral. Also, specify the date of the last collateral audit/appraisal and

frequency of future collateral audits/appraisals. If liquid assets are held as collateral, discuss the valuation in

light of the instructions in the ALLISON WRIGHT BANK Credit Policy Manual. If fixed assets including

equipment are held, show support for determination of fair market value. The appraisal source and date

should be well documented. If cap rates are low for a specific market area, sensitize the collateral value to an

average cap rate.

For fully monitored trading asset lines, a borrowing base format should be provided showing recent

receivable agings, concentrations, delinquencies, dilution, charge-off history, bad debt reserves, inventory

breakdowns, and so forth. Clearly specify what types of collateral will be eligible and ineligible for

borrowing base calculations.

Clarify whether all or some of the facilities are cross-collateralized. Keep in mind that "surplus" real estate

value is typically not available as collateral for other facilities (ask counsel if uncertainty exists or

clarification is desired). Furthermore, when analyzing junior liens, make specific allowances for discounts

for the costs of obtaining title and liquidating the collateral.

Address environmental due diligence performed or to be performed.

On real estate transactions address the site and demographics of the project. Additionally, this section should

address tenants, leases and pre-leasing if a construction project.

7. Primary Risks In Order of Priority and Mitigators:

List the major risks of the transaction. Also cite applicable and relevant factors which mitigate those risks.

Be sure to specify those critical risks, which, if not mitigated, would cause you to reconsider the transaction

(e.g., “Deal Breakers"). To the extent the risks are quantifiable (e.g. sensitive to commodity prices/margins,

Bankers Insight Group, LLC Page 14

or to interest rate volatility), use these sensitivities in the "Downside" case in the Repayment Sources

analysis. If the likelihood of an occurrence is quantifiable, this should be included. Remember, not every

risk has a specific mitigator. Discussion of a specific risk is not a mathematical equation that requires a

specific mitigator. The important point is that the risk must be acknowledged and a plan articulated to

manage the identified risk.

8. Covenants:

In this section the lender should identify and define the key or controlling covenants and analyze their

capacity to serve as tools for managing the proposed credit accommodation. The discussion should make

clear why the covenants are considered to be key or controlling. In table form with narrative comments,

indicate the flexibility inherent in the covenants. For example, "the company could only lose $1 hundred

thousand before the net worth covenant would trip," or "cash flow could decline by $300,000 before the debt

service coverage ratio would be in default," and so forth.

Continue to include the Loan Approval Requirements form in the package as a concise recap of all

covenants. Perform additional sensitivity tests here in Section 8 as appropriate.

A covenant compliance sensitivity analysis of "cash flow based" covenants should calculate the projected

cash flow trigger point (e.g., EBITDA or other defined cash flow level at which the subject covenant

defaults). This projected cash flow "trigger" could then be compared to the Management Case, as well as the

Break-Even Case, for purposes of assessing the effectiveness of the subject cash flow covenant.

Changes from previously approved covenants require re-approval as discussed in the ALLISON WRIGHT

BANK Credit Policy

All terms referring to financial calculations should be defined because not every reader may use the term in

the same way. For example, the terms Cash Flow and Balance Sheet Leverage have been used to refer to a

variety of different calculations.

Provide details of past covenant waivers and defaults, if relevant to the current situation, to allow the reader

to gain a historical perspective.

All term loan transactions over $100,000 should include at least a covenant for adequacy of debt coverage.

9. Plan for Monitoring:

List the steps to be taken to monitor the credit relationship, including such items as listed below and in each

case when delivery to the Bank is required:

Audited annual financial information

Interim reporting (monthly, quarterly)

Loan agreement compliance

Personal guaranty compliance

Covenant compliance

Borrower compliance certificate frequency

Borrowing base certificate frequency

Borrowing base audit frequency

Bankers Insight Group, LLC Page 15

Frequency of collateral appraisals

Use of other specialists ( i.e. meetings with other professionals, internal specialists, etc.)

Frequency of lender regular calls on the borrower/borrower (including dates for Ag Field Inspections

when appropriate).

Construction loans should have a detailed breakdown of monitoring that will take place

Attempts should be made to ensure that our covenants are at least as stringent as the most restrictive credit

agreement for our borrower. If changes have occurred in the monitoring plan, they should be described.

10. Comparison with Credit Policy

The ALLISON WRIGHT BANK Credit Policy contains policies and standards that all credits must meet.

Exceptions to ALLISON WRIGHT BANK policies and standards are expected to be rare and are subject to

an exception approval process. Explain any exceptions to policies and standards in this section with

mitigators, if applicable.

Unless otherwise indicated, it is assumed that the transaction complies with all applicable underwriting

guidelines. Narrative should be provided on all areas of non-compliance with underwriting guidelines. List

the aspects of the transaction that fall outside of the applicable guidelines and explain the approval rationale,

together with relevant mitigating factors.

11. Relationship Strategy/Adequacy of Compensation:

Briefly describe our business and credit risk management strategies regarding the client and what other

services/transactions may be considered in the near and intermediate future. Discuss how the proposed

transaction fits within the Bank's strategy for the client. Compare level of risk being undertaken with the

level of compensation for the transaction being considered. Demonstrate numerically the total relationship

profitability. For example, a new credit line may have thin pricing, but is justified because of profitable non-

credit business.

Credit Risk Management Strategy: When underwriting large exposures, whenever possible the lending

officer should attempt to structure the transaction in accordance with “Market Conditions”, even if we are not

planning to sell down the exposure at this time. This is both a marketing strategy and a credit risk

management strategy. Future liquidity or credit risk management conditions may make it desirabledesireable

to sell down a large exposure. When structuring a large transaction, the lending officer should consult with

the Credit Administration to be cognizant of current market conditions (i.e. the “market hurdle”) with a view

to preserving our option to sell down the transaction in the future.

12. Summary: Strengths and Weaknesses:

List noteworthy strengths and weaknesses of the proposed transaction, together with any known and relevant

mitigators to the weaknesses.

13. Risk Rate and Rationale:

Bankers Insight Group, LLC Page 16

List the RR and justify your rationale. Thoroughly explain the rationale behind the proposed RR, especially

if it is a new facility or if the rating has changed. Discuss what events need to take place for an increase or

decrease in the loan quality rating and the expected timing (if applicable) for those events to occur. This

section should thoroughly support and explain the proposed risk rating given the known credit factors (e.g.

cash flow, collateral, guaranty). The risk rating rationale should address and account for downside risks. It

should also explain what mitigators (strengths) exist that would preclude a lower rating. In other words, it is

not enough just to explain why the recommended RR is appropriate, but this section should also explain why

the recommended RR is not better or worse.

Since credit facilities are individually rated, it is possible for a borrower with multiple credit facilities to have

multiple risk ratings based on different repayment sources, risk factors, structure, etc. If this is the case, it

should be thoroughly explained in this section. RRs may not be disclosed to borrowers or other parties

outside the Bank (including other financial institutions) absent proper court order or under other extremely

limited circumstances.

14. DDA and Other Product Offerings:

Detail current DDA and other product offerings for the borrower. Explain any potential product risks and

plans to monitor and/or control those risks. Describe potential opportunities or future plans to expand these

“non-borrowing” products.

Bankers Insight Group, LLC Page 17

CREDIT UNDERWRITING STANDARDS

What are credit underwriting standards? They are the guidelines, endorsed by the board of

directors through approval of the financial institution’s credit policy, for determining the safety

and soundness of the credit-granting process. They include defining what lending practices and

types of risks are acceptable and direct lending personnel on how to make choices between risks

and rewards. Critical factors need to be identified that significantly affect the safety, soundness,

and the repayment of a loan. These factors are called underwriting standards.

Underwriting Consumer Loans

It is suggested that the traditional C’s of credit be used as a starting point, namely:

Character

Capacity

Capital

Collateral

Condition

Can We?

Character:

Character measures Human/Management Factors such as

! Borrower’s moral character

! Determination to meet obligations

! Willingness to cooperate with lender

Capacity: Repayment Ability

While the analysis of character dealt with past performance, the analysis of “capacity” deals with

future performance. Today, the ability to repay the credit per the terms of the contract is more

important than the bank’s having leverage to collect the credit through collateral. The difference

between a good loan and a charge-off lies in one word: repayment! It should be remembered that

it is not past performance but future performance that will determine the amount of repayment

available for the loan the lender is about to make.

The financial institution should include in its credit policy a defined method for determining

capacity to service debt and should provide guidelines that are acceptable (i.e., total housing

expense not to exceed 28 percent of the applicant’s disposable income; total housing and other

fixed payments not to exceed 36 percent of the applicant’s disposable income).

Capital: Financial Position

Capital can be analyzed and measured by reviewing net worth and down payment or the amount

of equity invested by the borrower. The lender should make sure that every borrower has

Bankers Insight Group, LLC Page 18

sufficient equity to enable total recovery of loan funds through the sale of assets if all else fails.

Since problems do arise in loan repayments, lenders want assurance of adequate equity in the

borrower’s assets to rely on in case repayment fails to materialize. Equity provides the cushion

against adversity and potential loss by the creditor. Down payment or equity guidelines are to be

established for each type of loan made by the bank.

Many lenders underestimate the importance of equity when making loans to commercial and

agricultural customers. The equity position is the best single indicator of the strength of a

business and the commitment of its owners. A business with insufficient equity has little ability

to weather adversity or to take advantage of growth opportunities. It appears that, at a bare

minimum, equity would equal at least 20 percent of total

assets in almost any business.

Collateral: Identification and Valuation

Collateral is the property-personal or real- against which the lender takes a lien in case the debtor

does not repay the loan as agreed. It is a secondary source of repayment.

The pledge of collateral normally adds safety to a loan, since the lender can sell the security to

obtain repayment lithe debtor fails to pay. Collateral should cover interest during foreclosure,

legal costs, and reduced price due to “fire sale” conditions. If the loan is well collateralized, the

borrower will most likely liquidate the collateral, pay the loan, and retain the difference.

The market value of the collateral must be obtained and verified.

Split collateral (i.e., collateral of the same type in which two or more creditors each has a partial

security interest) should be avoided.

Condition: Economy

Condition of the economic environment and the impact that it has on the ability to repay the

credit to the bank must be taken into consideration in order to evaluate each credit properly.

While the bank cannot abandon its customers whenever a sector of the economy becomes

depressed, extra caution must be exercised. When analyzing economic condition, determine the

stability of the source of repayment. Consider length of service, type of occupation, and stability

of industry. The customer’s place of employment tends to be a concern only when the bank is

aware of impending layoffs or conditions that could lead to a disruption of income, such as

seasonal employment. The loan officer must use good judgment along with the bank’s credit

standards and guidelines.

Can We? Introduces the Credit Policy

After the traditional C’s of credit are established, one must consider whether the loan request is

in line with the bank’s credit policy. A borrower may possess all five C’s but the purpose of

their loan request may be in direct conflict with the bank’s credit policy. It this occurs, a denial

of the request must be considered.

Bankers Insight Group, LLC Page 19

RATIO DEFINITIONS

For manufacturing, wholesaling, retailing and service companies, a review of the financial

statements to determine the following factors should be conducted.

LIQUIDITY

LEVERAGE

ASSET MANAGEMENT

OPERATIONS

CASH FLOW

LIQUIDITY

Liquidity is a measure of the quality and adequacy of current (short-term) assets to meet current

(short-term) obligations as they come due.

Current Ratio

Calculation: Current Assets

Current Liabilities

Quick Ratio

Calculation: Cash + Marketable Securities + Accounts Receivable

Current Liabilities

Accounts Receivable Turnover Rate

Calculation: Net Sales

Accounts Receivable

Bankers Insight Group, LLC Page 20

Accounts Receivable Turnover in Days

Calculation: 365 days (or the number of days in a period being measured)

Accounts Receivable Turnover Rate

Inventory Turnover Rate

Calculation: Cost of Goods Sold

Inventory

Inventory Turnover in Days

Calculation: 365 days (or the number of days in a period being measured)

Inventory Turnover Rate

Accounts Payable Turnover Rate

Calculation: Cost of Goods Sold

Accounts Payable

Accounts Payable Turnover in Days

Calculation: 365 days (or the number of days in a period being measured)

Accounts Payable Turnover Rate

Bankers Insight Group, LLC Page 21

LEVERAGE

Leverage refers to the proportion of funds invested in an entity by the creditors in the form of

loans and the owners in the form of equity. Highly leverage firms (those with heavy debt in

relation to net worth) are more vulnerable to business downturn than those with lower debt to

worth positions. While leverage ratios help measure this vulnerability, it does greatly depend on

the requirements of particular industry groups.

Debt to Net Worth

Calculation: Total Debt

Tangible Net Worth

.

Debt to Total Assets

Calculation: Total Debt

Total Assets

Bankers Insight Group, LLC Page 22

ASSET MANAGEMENT (EFFICIENCY) RATIOS

Asset Management or Efficiency Ratios measures management’s ability to utilize assets to

generate revenue or create value (i.e. generate a profit).

Asset Efficiency or Asset Turnover Ratio

Calculation: Total Sales

Total Assets

Net Fixed Assets Efficiency or Turnover Ratio

Calculation: Total Sales

Net Fixed Assets

Fixed Asset Usage Ratio

Calculation: Accumulated Depreciation

Gross Fixed Assets

Fixed Asset Life Ratio

Calculation: Net Fixed Assets

Depreciation Expense

Bankers Insight Group, LLC Page 23

OPERATIONS (PERFORMANCE OR PROFITIBILITY RATIOS)

Gross Profit Margin

Calculation: Gross Profit

Net Sales

Operating Profit Margin

Calculation: Operating Profit

Net Sales

.

Net Profit Margin

Calculation: Net Profit

Net Sales

Return on Stockholders Equity

Calculation: Net Income

Stockholder’s Equity

Return on Investment (Assets)

Calculation: Net Income

Total Assets

Bankers Insight Group, LLC Page 24

CASH FLOW AND FINANCIAL RATIOS

Financial Ratios measure the ability of a borrower to meet its financing obligations including

Interest Expense, Principal Payments on Long-Term Debt and other fixed charges such as Lease

Payments.

Interest Coverage Ratio

Calculation: Earning (profit) before Interest, Taxes, Depreciation & Amortization

Annual Interest Expense

This ratio is a measure of a firm’s ability to meet interest payments. It measures the number of

times all interest paid by the company is covered by earnings before interest charges and taxes. A

high ratio may indicate that a borrower would have little difficulty in meeting the interest

obligations of a loan. This ratio also serves as an indicator of a firm’s capacity to take on

additional debt.

Cash Flow / Debt Coverage Ratio Calculation: Net Profit

Plus: Non-Cash Charges

+ Change in Accounts Receivable

+ Change in Inventory

+ Change in Accounts Payable

+ Change in Accrued Expenses

= Cash After Operating Cycle

Minus: Dividends Declared

+ Change in Net Worth

= Cash After Financing Cost

Less: Current Portion of Long-Term Debt

= Cash Available for Other Debt

+ Change in Gross Fixed Assets

= Financing Surplus (Requirement)

Bankers Insight Group, LLC Page 25

REAL ESTATE

Underwriting Standards for Real Estate

• Capacity of Borrower

• Net Operating Income*

• Debt Coverage Ratio (NOI / ADS) > 1.15

• Value of Mortgage Property

• Overall Financial Strength of Borrower

• Hard Equity Invested into Property (Including unencumbered equity in properties)

• Secondary Sources of Repayment

• Additional Collateral or Credit Enhancements

*Potential Gross Income (PGI)

Less: Physical Vacancy

Economic (Credit) Loss

Effective Gross Income (EGI)

Less: Operating Expenses

Real Estate Taxes

Hazard Insurance

Repair/Maintenance (Buildings)

Maintenance (Grounds)

Depreciation

Water/Sewer/Trash

Electric (Common)

Interest Expense

Management Fees

Leasing Commissions

Reserves for Replacement

_______________________________

_______________________________

Total Operating Expenses

Net Operating Income (NOI)

NOI = > 1.25 times

DCR

Savannah Fresh Fish Compny

Balance Sheet

Years Ended December 31

(000)

ASSETS 12/31/09 12/31/10 12/31/11

Cash 195 126 69

Accounts Receivable, Net 475 683 994

Inventory 241 300 743

Prepaid Expenses 19 23 29

Other Current Assets 0 37 38

Total Current Assets 930 1,169 1,873

Gross Fixed Assets 782 856 1,076

Less:Accumulated Depreciation (224) (323) (465)

Net Fixed Assets 558 533 611

Other Non-Current Assets 94 24 32

TOTAL ASSETS 1,582 1,726 2,516

LIABILITIES AND EQUITY

Notes Payable-Line of Credit 0 25 375

Long-Term Debt-Current Port. 26 23 15

Accounts Payable 138 231 465

Interest Payable 2 2 3

Income Tax Payable 0 2 0

Accured Expenses 70 86 181

Dividends Payable 0 0 30

Other Current Liabilities 10 12 7

Total Current Liabs. 246 381 1,076

Long-Term Debt 302 280 265

Common Stock 150 150 175

Preferred Stock 0 0 0

Paid in Capital 0 0 0

Retain Earnings 884 915 1,000

Total Equity 1,034 1,065 1,175

TOTAL LIAB AND EQUITY 1,582 1,726 2,516

26

Savannah Fresh Fish Compny

Income Statement

Years Ended December 31

(000)

12/31/09 12/31/10 12/31/11

Net Sales 5,937 8,481 11,025

Cost of Goods Sold 4,472 6,402 8,240

Gross Profit 1,465 2,079 2,785

Operating Expenses

Salaries 1,015 1,446 1,859

Utilities 50 70 93

Insurance 21 28 36

Telephone 15 20 27

Other Taxes 5 6 9

Bad Debt Write-off 6 6 9

Advertising 88 132 171

Interest Expense 29 41 54

Delivery Expenses 99 147 195

Depreciation 84 111 154

Total Operating Expenses 1,412 2,007 2,607

Income Before Taxes 53 72 178

Gain (Loss) from Sale of Fixed Assets 0 7 (5)

Extraordinary Income 0 0 19

Income Taxes 20 28 77

Net Income 33 51 115

27

Bankers Insight Group, LLC | 28

RATIO WORKSHEET

SAVANNAH FRESH FISH COMPANY

2009 2010 2011

Sales Growth % N/A 42.8% 30.0%

Current Ratio 3.78 3.07 1.74

Quick Ratio 2.80 2.18 0.99

Leverage Ratio (Debt/Worth) 0.52 0.62 1.14

Sales-to-Assets 3.78 4.91 4.38

Sales Net Fixed to Assets 10.6 15.6 18.0

Net Fixed Assets Usage Ratio 29.0% 38.0% 43.0%

Inventory Turnover (Rate) 18.6 times 21.3 times 11.1 times

Inventory Turnover (days) 19.6 days 17.1 days 32.9 days

Receivable Turnover (Rate) 12.5 times 12.4 times 11.1 times

Receivable Turnover (days) 29.2 days 29.2 days 32.9 days

Payable Turnover (Rate) 32.9 times 27.7 times 17.7 times

Payable Turnover (days) 11.1 days 13.2 days 20.6 days

Gross Profit Margin 24.7% 24.5% 25.3%

Operating Profit Margin 0.9% 0.9% 1.6%

Net Profit Margin 0.6% 0.57% 1.0%

Return on Equity 3.2% 4.8% 9.8%

Return on Assets 2.1% 3.0% 4.6%

Bankers Insight Group, LLC | 29

SAVANNAH FRESH FISH COMPANY

CREDIT ANALYSIS MEMORANDUM

February 25, 2012

LIQUIDITY

Liquidity as measured by the Current Ratio decreased from 3.78 to 1.74 over the three

year period. The cause of the decrease can be traced to the rapid sales growth over the

three year period (72.8% combined).

The growth in sales was financed by short term debt as it increased from $246,000 to

$1,076,000. This growth caused Current Liabilities to grow at a faster pace as a percent

of Total Assets than Current Assets to Total Assets. This trend results in Liquidity

decreasing as described in the preceding paragraph

The Current Liabilities realizing the largest increase are Accounts Payable and Notes

Payable, which is in response to the company’s needs to support an ever increasing

investment in Accounts Receivable and Inventory. These assets grew faster than the

growth in revenue thus indicating a slowdown in the Collection Period and the Inventory

Turnover.

While sales grew by 30% at FYE 2011, the Accounts Receivable turnover slowed to 32.9

days from 29.2 days over the year, while the Inventory turnover expanded from 19.7 days

to 32.9 days over the same period.

The financial impact of Accounts Receivable turning slower caused a funding need of

$112,000 while Inventory turning slower caused a funding need of $300,000 over the

year. This again was funded by debt (short term) because Equity did not grow sufficient

enough to cover this need.

As a result of the slowdown in the Accounts Receivable and Inventory turnovers, it

caused the Accounts Payable turnover to lengthen from 11.3 days to 20.6 days over the

Period.

LEVERAGE

The leverage position, as measured by the Debt to Worth ratio, deteriorated from 0.53 to

1.15 over the Period. This deterioration reflects the aforementioned increase in Current

Liabilities, specifically, Accounts Payable and Notes Payable.

Once again, the growth in sales, fueled by the increase in debt caused Leverage to

elevate. Although the Leverage position is deteriorating, it is still acceptable presently.

The downward trend requires close monitoring.

Bankers Insight Group, LLC | 30

ASSET MANAGEMENT

Management utilization of its assets to generate revenue and profits is improving. The

Asset Turnover Ratio (Net Sales to Total Assets) improved from 3.75 to 4.35, while the

Return on Assets (Net Income to Total Assets) improved from 2.09 to 4.53 over the

Period.

The Net Fixed Assets Turnover Ratio also shows signs of improving as it increase from

10.64 to 18.04 over the Period.

OPERATIONS

Sales increased 73% over the Period (43% in 2009 and 30% in 2011). This increase

reflects the market acceptance of SFF “Quick Freezing Techniques”, which allows the

company to expand its market by selling fish as “Fresh Frozen” across the Mississippi

River.

In spite of the significant sales growth, the Gross Profit Margin actually improved from

24.7% to 25.3% over the three year period. The financial impact of the improving Gross

Profit Margin was $66,150 over the three year period.

The improved Gross Profit Margin reflects SFF success in obtaining a higher sales price

for the fresh frozen fish and controlling its direct costs.

Management was successful in holding Operating Expenses steady as a percentage of

Sales over the Period at 23.2%. Holding the Operating Expenses constant in light of the

substantial increase in sales is a display of good management. Consequently, the

Operating Profit Margin improved from 1.4% to 2.1% over the Period.

As a result of the improvement in Gross Profit Margin and Operating Profit Margin, Net

Profits increased from $33,000 to $115,000 over the Period.

Bankers Insight Group, LLC | 31

CASH FLOW

12/31/06 12/31/07

Net Profit 51 115

Plus: Interest (Assuming Interest is included in CPLTD)

Plus: Non Cash Charges (Depreciation) 111 154

+ Change in Accounts Receivable (208) (311)

+ Change in Inventory (59) (443)

+ Change in Accounts Payable 93 234

+ Change in Accrued Expenses 16 95

Cash After Operating Cycle 4 (156)

+ Change in Net Worth (20) (5)

(Change in Stock Accounts, Paid in Capital, etc)

Cash After Financing Cost (16) (161)

Less: Current Portion of Long Term Debt (26) (23)

Cash Available for Other Debt (42) (184)

+ Change in Gross Fixed Assets (74) (220)

Financing Surplus (Requirement) (116) (404)

SFF experienced a negative Net Cash After Operations of $156,000 at fiscal year ending

12/31/07 as a result of increases in Accounts Receivable ($311,000) and Inventory

($443,000). This drain on cash was offset somewhat by the increase in Accounts

Payable in the amount of $234,000; however, it was not enough to counteract the

increase in the trading assets. The Accounts Payable increase is reflected by their past

due status.

The financial impact of the Accounts Receivable, Inventory and Accounts Payable

turning slower is as followers:

A/R : $30,205 X 3.7 days = ($111,925)

Inv : $22,575 X 13.3 days = ($300,252)

A/P : $22,575 X 9.3 days = $211,640

Financial Impact ( $200,537)

This financial impact is the consequence of these accounts increasing at a faster rate

than the 82% increase in sales over the Period. It reflects management’s inability to

manage these accounts by maintaining the historical turnover rates.

Cash After Financing Costs further increased to a negative $175,000 reflecting the

Bankers Insight Group, LLC | 32

negative $19,000 change in Net Worth while Cash Available for Other Debt further

increased to negative $198,000 reflecting the Current Portion of Long-Term Debt of

$23,000.

In spite of the large negative Cash Available for Other Debt, SFF spent $220,000 to

increase Gross Fixed Assets, which resulted in a Financial Requirement of negative

$418,000.

The Financial Requirement was funded by drawing $375,000 under the Line of Credit

and raising equity of $25,000 from the sale of stock. The shortfall was funded by the

company’s own cash.

RECOMMENDATION

Although SFF is profitable, it is not recommended for the bank to entertain a request for

term financing. This conclusion is due to the inability to generate cash to service future

debts as a result of the high rate of sales growth and the growth in Accounts Receivable

and Inventory beyond the rate of sales growth resulting in a huge drain of SFF cash.