Write Up 30 Apr

20

CASE STUDY OF PAKISTAN AUTO PART INDUSTRY ASIM QAYYUM, DR AAMER AHMED BAQAI (CENTER FOR ADVANCED STUDIED IN ENGINEERING, ISLAMABAD) ABSTRACT The automotive industry continues to practice dynamic change that curves the world market. The effects of these changes have affected the market of Pakistan automotive industry. To materialize these, autoparts manufacturers must have to cope with large and complex supply chains, bridging many geographic regions, and track opportunities in diverse national and international markets. While national policies play an important role in shaping the environment for local manufacturing operations and resulting products, cost competition increasingly drives the industry toward global product offerings. This case study will explore several important dimensions of the forces of change facing the Pakistan Auto parts Industry . I – INTRODUCTION The automotive industry is an important segment of the economy in any country as it links many industries and services. Production of a transport vehicle incorporates all possible industrial activities. The first phase of automotive assembling in Pakistan, started in 1950 with Bed Ford truck, followed by Ford Prefect, Ford Cortina and Dodge Dart. The indigenized parts in these vehicles did not exceed 20% with only exception of Bed Ford trucks with a deletion level of 80%. By the end of 70s practically all automobile assembling in Pakistan ceased. The 2nd phase of Automobile assembly started in 1983 with the introduction of FX800 CC Suzuki Car. In 1989 Pak. Suzuki changed the Model of FX 800 CC with Mehran 800CC. Pak Suzuki thereafter in 1992 introduced Khyber 1000 CC and 1300CC Margalla but the indigenization levels from 1983 to 1995 were not significant (i.e. Mehran 30%, Khyber 20%, and Margalla, 15%).In 1993, Indus Motors Company Ltd., Karachi introduced Toyota Corolla. Honda Atlas cars (Pak) Ltd Lahore in 1994 introduced Honda Civic having 1300CC engine capacity. Indus Motors, Dewan Farooq Motors and Pak Suzuki introduced smaller Cars i.e. Cuore, Cultus and Santro

-

Upload

asim-qayyum -

Category

Documents

-

view

32 -

download

3

Transcript of Write Up 30 Apr

CASE STUDY OF PAKISTAN AUTO PART INDUSTRY

ASIM QAYYUM, DR AAMER AHMED BAQAI

(CENTER FOR ADVANCED STUDIED IN ENGINEERING, ISLAMABAD)

ABSTRACT

The automotive industry continues to practice dynamic change that curves the world market. The effects of these changes have affected the market of Pakistan automotive industry. To materialize these, autoparts manufacturers must have to cope with large and complex supply chains, bridging many geographic regions, and track opportunities in diverse national and international markets. While national policies play an important role in shaping the environment for local manufacturing operations and resulting products, cost competition increasingly drives the industry toward global product offerings.

This case study will explore several important dimensions of the forces of change facing the Pakistan Auto parts Industry.

I – INTRODUCTION The automotive industry is an important

segment of the economy in any country as it links many industries and services. Production of a transport vehicle incorporates all possible industrial activities. The first phase of automotive assembling in Pakistan, started in 1950 with Bed Ford truck, followed by Ford Prefect, Ford Cortina and Dodge Dart. The indigenized parts in these vehicles did not exceed 20% with only exception of Bed Ford trucks with a deletion level of 80%. By the end of 70s practically all automobile assembling in Pakistan ceased.

The 2nd phase of Automobile assembly started in 1983 with the introduction of FX800 CC Suzuki Car. In 1989 Pak. Suzuki changed the Model of FX 800 CC with Mehran 800CC. Pak Suzuki thereafter in

1992 introduced Khyber 1000 CC and 1300CC Margalla but the indigenization levels from 1983 to 1995 were not significant (i.e. Mehran 30%, Khyber 20%, and Margalla, 15%).In 1993, Indus Motors Company Ltd., Karachi introduced Toyota Corolla. Honda Atlas cars (Pak) Ltd Lahore in 1994 introduced Honda Civic having 1300CC engine capacity. Indus Motors, Dewan Farooq Motors and Pak Suzuki introduced smaller Cars i.e. Cuore, Cultus and Santro of engine capacities 850 cc, 1000 cc respectively in 2000.

After struggling through nineties, a decade full of uncertainties and frequent policy the Pakistani Auto Industry had been able to achieve double digit growth consistently since the last 6 years. The industry operated under franchise and technical cooperation agreements with Japanese, European and Korean manufacturers. This gives a strategic advantage and continuity to the local parts manufacturing industries, which in turn develop their capabilities in their respective fields. The fortune of the Auto Parts or Automotive Components segment are inextricably linked to the performance of its dominant customer i.e. Automotive Sector. Apart from demand, this business critically impacts the industry structure of auto parts.

The annual gross sales turnover of the auto industry, at present, stands at Rs210 billion while export of auto parts are estimated at $35 million. As such, the increase in production turnover is projected to increase by 185 per cent while the exports of auto parts would make quantum jump.

II – OVERVIEW OF AUTO PARTS MANUFACTURING CONCEPT

The automotive industry can be classified into:-

• Auto Manufacturing. Auto manufacturing includes the production of passenger cars, light commercial vehicles, heavy trucks, buses, and coaches.

• Auto Component Manufacturing. Auto component manufacturing includes the production of all components required for the manufacturing of automobiles. Auto components can be sub-divided into the following categories:

Steering systems, gears, axles, wheels, clutches

Steering PartsSus and Brake Parts

Leaf springs, shock absorbers, brakes, brake assy, brake lining

Equipment Switches, electric horns, headlights, halogen bulbs, wiper motors, dashboard instruments,

Others Sheet metal parts, pressure die castings, plastic moulded components, fan belts, hydraulic pneumatic equipment

III – AUTO PARTS INDUSTRY

Industry StructureThe Vendor industry plays a critical role

in the growth of auto industry as all the component parts are not manufactured under one roof. Development of vendor industry would be able to expand the employment opportunities, reduce cost of production, pre-empt imports and help achieve deletion programmes.

There are four sources of spare parts, namely organized sector, unorganized sector and imports (US $ 92 Million).

o Organized Sector. Organized sector consists of some 450 units such as Agriauto Industries Ltd., Allwin Engineering Industries, Bolan Castings Ltd., Exide Pakistan Ltd., Atlas Battery Ltd., Axle Products Ltd., Balochistan Wheels Ltd., General Tyre and Rubber Company Ltd., Loads Ltd., Landhi Engineering Works, Thal Engineering, Mali Auto and Agricultural Industries

Ltd. Rao Engineering Ltd., Transmission Engineering Industries Ltd. and Sindh Engineering (Pvt) Ltd., supplying different parts namely axle products, auto filter, wheel, tyre, gasket, engine valve, shock absorber, automotive pump, piston radiator, radiator core, fly wheel, battery, etc.

Table – 1. Categories of auto components as per Automotive and Components Global Report — 2010

Estimated Vending Unit 2200 Units

Organized and Tier One : 450; Tier Two: 425 Unorganized and aftermarket suppliers : 1325

InvestmentRs, 265 Billions

Target production of Cars(2012 ) 510,000

Direct Employment 215,000

Current Exports million US 92 Million

Export Growth Rate 35%

Exporting Units 34Table – 2. General statistics of auto parts sector as provided by PAPAAM

o Un – Organized Sector. Along with the organized sector, a good number of small and large units (approximately 425) were operating in un-organized sector. In fact, 90% of automotive parts industry constituted of Small and Medium size Enterprises (SMEs), out of which about 95% were self-financed. These units produced a wide range of parts for the replacement market. The larger operators in this unorganized sector even manufactured crankshafts (aside from wheel Hubs, brake drums, filters etc.) for replacement market, although not even a single assembler had yet deleted crankshaft because of high accuracy required in metallurgy and machining. However, these dozens of crankshaft manufacturers in the unorganized sector were successfully catering to most of the demand of the replacement market. The Pakistan auto component industry is one of the few sectors in the economy that has a distinct global competitive advantage in terms of cost and quality.

o Cottage Setups. In addition, there is a slew of small units in the unorganized sector (1325 units) located mostly in Karachi, Lahore and Gujranwala which fabricate smaller parts (without brands or names of manufacturer) such as ignition control system, micro touch button, dash board light indicator, built alarm system, door operating system, handle lock revolving warning light and horn. These are much cheaper than those produced under brand names or imported and, therefore, command a big market, as disclosed by a spare parts dealer. The unorganized vendor industry is producing quality products imitating foreign makes with extraordinary skill and expertise of the experienced but unqualified workers. The quality is improving with keen competition among the workers.

Growth of Industry. The Pakistani auto component industry has been navigating through a period of rapid changes with great élan. Driven by global competition and the recent shift in focus of global automobile manufacturers, business rules are changing and liberalisation has had sweeping ramifications for the industry. The global auto components industry is estimated at US$1.2 trillion. The Pakistan auto component sector has been growing at 46.7% during last fiscal year mainly, due to surging demand and the availability of consumer credit and low interest rate loans.

Pakistan includes low labour cost, raw material availability, technically skilled manpower and quality assurance. An average cost reduction of nearly 25‐30% has attracted several global automobile manufacturers to set base since 1991. Pakistan process engineering skills, applied to re‐designing of production processes, have enabled reduction in manufacturing costs of components.

At least 90% of the national demand for automotive parts – also called automotive components or just autoparts – is being met by imports, while local manufacturers cover about 10%. Motorcycles dominate (95%) the composition of autoparts demanded in Pakistan, with cars making up 70%.

IV – LOCALIZATION ACHIEVED

Pakistan stipulated a specific deletion or localization program for local content requirements for cars, motorcycles, buses, trucks

Cars; 70

Tractors ; 96

M/C ; 95

Three

Wheel-ers ; 80

% of Local Components

and tractors etc. The Engineering Development Board set yearly targets of deletion and localization of parts for different brands and models of vehicles. The main objective of deletion localization program was to develop and protect the local auto parts and component manufacturing industry. This local deletion program was strictly adhered to until June, 2005 and, thereafter, a new Tariff Based System (TBS) which is Trade Related Investments (TRIM’s) compliant system has been introduced. During the Deletion Program’s implementation the industry managed to localize a large number of automotive parts which included sheet metal parts, rubber and plastic parts, aluminum parts, external parts, wire harnesses, chassis, tyres, tubes, car seats and lights etc.

To understand and comprehend the dynamics of Pakistan’s automotive industry, it is essential to have an understanding of the supply structure of this complex industry. Understanding the structure of the industry

would also help in giving a comparison of the local structure with those in the region. Hence allowing one to analyze the differences and suggest recommendations which may allow Pakistan to achieve the same levels of economies of scale as those achieved in the region.

The automotive industry’s supply structure is comprised of an Original Equipment Manufacturer (OEM) which receives its supplies from first, second or third tier suppliers.

A first tier supplier is responsible for the delivery of parts such as steel coils, body paints, tyres etc.

The second and third tier suppliers deliver mono parts such as door hinges, door locks, bolts, nuts and other plastic parts.

Regular monitoring and motivation by assemblers and vendors have resulted in significant level of deletion as at today the industry has achieved the following level of localization:

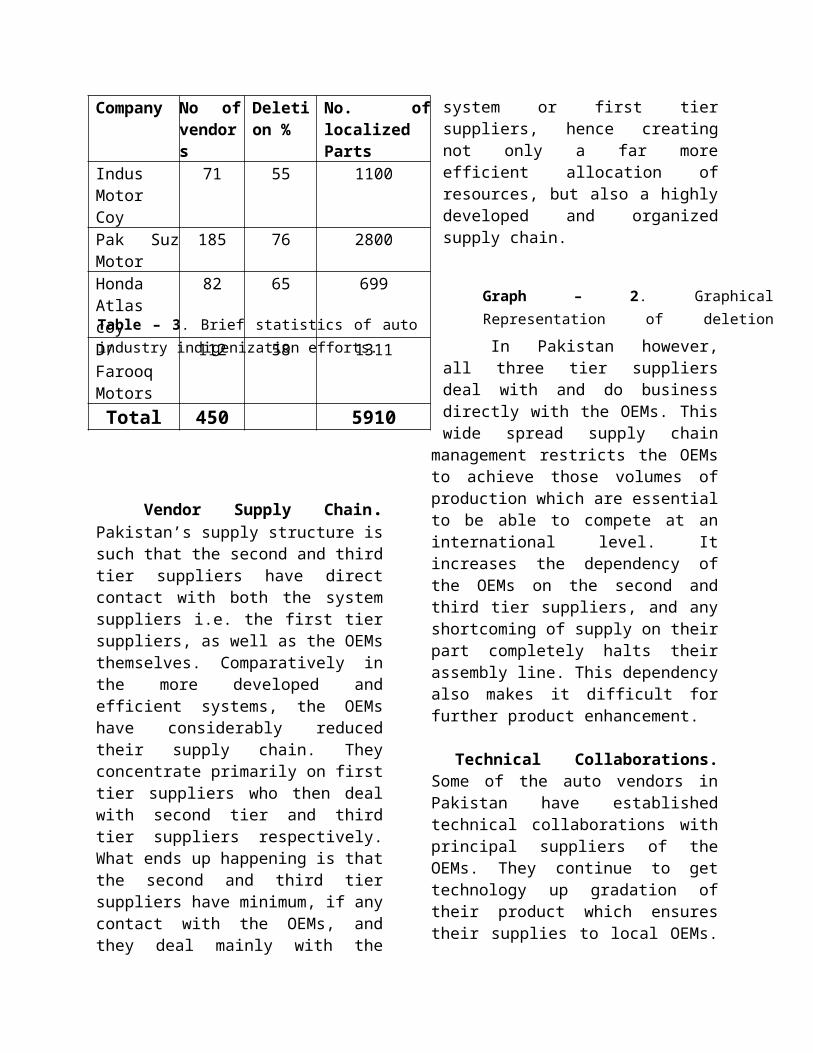

Vendor Supply Chain. Pakistan’s supply structure is such that the second and third tier suppliers have direct contact with both the system suppliers i.e. the first tier suppliers, as well as the OEMs themselves. Comparatively in the more developed and efficient systems, the OEMs have considerably reduced their supply chain.

Table – 3. Brief statistics of auto industry indigenization efforts.

Indus Motor C

oy

Pak Su

z Motor

Honda Atla

s coy

D/Faro

oq Motors

01020304050607080

Deletion %

Deletion %

Company No of vendors

Deletion %

No. of localized Parts

Indus Motor Coy

71 55 1100

Pak Suz Motor

185 76 2800

Honda Atlas coy

82 65 699

D/Farooq Motors

112 58 1311

Total 450 5910

They concentrate primarily on first tier suppliers who then deal with second tier and third tier suppliers respectively. What ends up happening is that the second and third tier suppliers have minimum, if any contact with the OEMs, and they deal mainly with the system or first tier suppliers, hence creating not only a far more efficient allocation of resources, but also a highly developed and organized supply chain.

In Pakistan however, all three tier suppliers deal with and do business directly with the OEMs. This wide spread supply chain management restricts the OEMs to achieve those volumes of production which are essential to be able to compete at an international level. It increases the dependency of the OEMs on the second and third tier suppliers, and any shortcoming of supply on their part completely halts their assembly line. This dependency also makes it difficult for further product enhancement.

Technical Collaborations. Some of the auto vendors in Pakistan have established technical collaborations with principal suppliers of the OEMs. They continue to get technology up gradation of their product which ensures their supplies to local OEMs. However, most of them have a restriction clause to export their products outside Pakistan.

Part Local vendor

Technical Collaboration

S/absorber Honda Atlas Showa , Japan

Agriauto Industries Ltd

Kayaba, JapanMaremount USA

Radiators Allwin Engg U.E. RadiatorsLoads Pvt Toyo Radiators

AC Sanpak Pvt. Sanden, JapanNippo DensoThal Engg.

Radio/ CD Player

Auto Industries

Panasonic, Thailand

Auto Glass NGS Pakistan NGS, Japan

Auto Lamp Technopak Koito, Japan

S/Plug Shaigan Elect & Engg

NGK, Japan

Steering Case Set

Polymer & Precision Pvt

I.S. Seiseki, Japan

B/Drum Assy

Alson Auto Industries

Nissin Kogyo, Japan

Gaskets Agriauto Ind Richard Klinger, UKCamshaft Agriauto Ind Zephyrs Cams/

Camtec,Iron & Al Parts

Allwin Engg Associated Engg

Battery Atlas Btys Japan Storage BtyAxle for Truck/Bus

Axle Products

Raba PLC, Hungary

Wire Harness

Delta Inovation

Furukawa, Jap

Thal Engg. Pvt. Ltd.

i) Yujin Elect Sysii)Prime TNT Kor

PropellerShaft & Gear Shift Lever

Noor Engg. Ind. Pvt. Ltd.

Hamana Parts Manufacturing, Japan

Locks General Locks Pvt.

Honda Locks Co., Japan

Case Set Steering

Polymer &Precision

I.S.Seiseki, Japan

Local Market ProspectsThe auto parts sector covers the demand

of all OEM and Replacement Parts (mechanical, electrical, electronic, hydraulic, rubber and plastic) pertaining to two/three wheelers, motorcars, light and heavy commercial vehicles, farm and agricultural tractors etc.

Table – 4. Details of available technical collaborations between international coys and local auto vendors Source. Pakistan Investment Guide and PAPAAM Stats 2011

Graph – 2. Graphical Representation of deletion achieved by different automobile industry.

The volumes of automobile industry in Pakistan do not create economies of scale. The majority of localized components are confined to small parts, whereas, parts of high technology and major engineering parts are not developed. In spite of low volumes, the industry’s local content in the small car is about 65% to 70%. The contribution of the vendor industry in this regard is worthwhile.

V – GLOBAL PERSPECTIVEWith the US reeling under the economic

slowdown, there has been a shift in dominance to Asia-Pacific, which is fast emerging as the next automobile production hub, with a market share of 35.8 percent in value in 2008 compared to 30.7 percent by the US. As a result, Toyota and Nissan are fast gaining market share. Toyota surpassed GM as the largest manufacturer of cars in

2008, manufacturing 8.9 million vehicles against GM’s 8.3 million.

In Asia, China surpassed Japan with a vehicle production of 7.9 million (9.3 million in 2008) compared to Japan’s 4.1 million (11.5 million in 2008) for the year

ended July 2009. As a result, Japanese automakers have restricted capital investment for 2009 following earnings

deterioration on a global scale. Toyota Motors, which has always been a forerunner in expansion in international markets, has decided to reduce capital investments to 830 billion yen (9.3 billion USD), below 1 trillion yen for the first time in six years. Similarly, Honda motors intends to reduce investments by 200 billion yen (2.2 billion USD) and Mazda Motors plans to keep it at 30 billion yen (337 million USD).

Although the local market of the automotive industry has been growing, Pakistan’s present level of passenger cars and LCVs in terms of its global contribution is almost non-existent, a mere 0.3% of the world production of 66.5 million passenger cars and light commercial vehicles.

The world automotive industry has become increasingly integrated. Vehicles produced in one country would often be

Graph – 2. Details of top five car producing countries. Source .OICA 2011 Production Statistics)

China 40%

Japan 19%

USA 18%

Germany 14%

S/Korea10%

% SHARE OF TOP 5 CAR PRODUCING COUNTRYS

Global OEM Sales Coy ($Mns) Parts Mfr

Robert Bosch GmbH (Ger)

62,627. 63 Brakes, controls, elect drives, electronics, fuel sys, gen, starter motors and steering sys

Continental AG (Ger)

40,971.13 Chassis, hydraulic and elect brake sys, sensor sys, telematics

Johnson Controls (US)

40,833 Auto interiors, products that optimize energy usage in btys for auto

Denso Corp (Jap) 37,787.33 Thermal sys, powertrain control sys, elec sys

Aisin Seiki Co (Jap)

20,585 Drivetrain parts, auto tx, manual tx, car navigation sys, brake and chassis-related products, and auto body related products

using components manufacturing plants and distribution methods from other countries in the world. Strategic alliances in design, production, and distribution of vehicles and parts and collaboration in manufacturing practices have dramatically improved the cost effectiveness, productivity and efficiency in the industry.

Pakistan could emerge as a low cost manufacturing country that can help the vendor industry to effectively target a part of this opportunity very well. However, the large and growing demand within the country has already constrained the local auto vendors as the growing competitive strength particularly that of the countries like China, Thailand, Brazil and India. It would be difficult until Pakistan

This world trend could open opportunities for Pakistan’s auto part suppliers to deliver as a 2nd tier to the system and 1st tier suppliers all over the world. The alternative is to establish alliances with automotive suppliers from other countries.

It was noted earlier that OEMs and Vendors have made heavy investment during the last three years which has laid a strong foundation and has built globally the capabilities to be cost competitive. Although the industry has been growing it is still not in a position to reap the benefits of economies of scale, bringing Pakistan to the level to be part of the global supply chain. The table below illustrates the top 20 global suppliers of automotive parts. Promotes investment in mega projects to build capacities in a cluster in collaboration with world leading auto parts suppliers - Multi National Companies (MNCs) where it has an edge over other countries of being competitive. It is worth noting that more than 90% of the world trade is directly or indirectly controlled by the Multi-National Companies.

VI – OVRVIEW OF AUTO INDUSTRY DVELOPMENT

PROGRAMME (AIDP)The vision of AIDP is “To make auto

industry a global player, achieving competitiveness through a critical mass of production, contributing to the GDP by 5.6% by2012, attracting large investments, development of technologies and human resource through a well-structured policy framework formulated in consultation with stakeholders”.

The consultations on the developmentof AIDP kicked off from the 8th March, 2006 Workshop at Islamabad by clearly defining the objectives at a time when the industry was switching over from the Deletion Programmes to a Competitive Tariff Based System. There was realization that the transitionary phase may affect the rapid growth and sustainable development of auto industry. A comprehensive development programme with pre-announced tariffs to provide predictable and stable environment was therefore much needed. Until the finalization and approval of AIDP by the government on 13th November, 2007 a great deal of fair consultation process was undertaken with the government and industry stakeholders. Most of the committees involved in deliberating various components of AIDP were steered by the experts from the auto industry due to which this programme has the rightful ownership of the entire automotive industry.

Government has recently approved a 5 year tariff plan for the auto sector to ensure a stable and predictable environment and to facilitate investment. Government is now focused on facilitating the industry through development of infrastructure, human resource development, technology acquisitions, and investment in productive assets, cluster development and

. Details of top five car producing OICA 2011 Production

development of standards on safety, quality and environment through a well-structured and deliberate approach. The cornerstone of approach remains close consultation and ensuring stakeholder’s participation in implementation and assessment of policy.

AIDP envisage achieving a critical mass of production, double the contribution of auto industry to GDP from the existing 2.8%, by the year 2011-12 with high focus on investment, technology upgradation, increasing its exports to US$ 650 million, enhancement in jobs alongside the development of critical components to further increase the competitiveness of domestically produced vehicles.

2011-12Cars (Nos) 500,000

Motorcycles (Nos) 1.7 MillionInvestment (Rs. Billion) 225Contribution to GDP (%) 5.6Contribution to Mfg Sector (%)

25

Contribution to indirect taxes (Rs. Billion)

190

Gross Sales Turnover (Rs. Billion)

600

Direct employment (Nos) 250,000Exports (US$ Million) 650(350 for parts and

300 CBU)

Auto Cluster DevelopmentThe assemblers of vehicles are mostly

located in and around Karachi and Lahore. The car and HCV assembly is mostly based in Karachi while the 2-Wheelers/ 3- Wheelers and agricultural tractors are located in Lahore. The same is the case with the vendors of such vehicles except that many vendors of car/ LCV are based in Lahore as well. The vehicle assemblers play a pivotal role in development of vendors through knowledge transfer, supply chain management, products and processes development. The way the Auto Industry is

becoming highly competitive world over and in Pakistan, focus has been shifted to not carry the cost of inventory and to supply on “Just in Time” concept. Fragmented location of vendors and a general lack of mutual support and learning and sharing certain common but otherwise underutilized capacities remain the issues which could be addressed through Cluster Development.

VII – GREY AREAS

In the following paragraphs issues and problems confronting the auto vendor industry will be discussed both by size and by technology.

Non Availability of Requisite Guidance. The auto parts and component manufacturing (vendor) industry of Pakistan, leaving few larger companies, is comprised of Small to Medium Sized Family owned businesses out of which 95% are self-financed. It has been established that most of these SMEs are family owned vendors who prefer to remain in their comfort zones. These entrepreneurs are reluctant to change their ways or to make any risky investments. They are also hesitant to implement any innovative thinking in order to seek solutions to problems and are also reluctant to take risk and are less confident of their decisions. While some businesses in the industry have expanded without a conscious effort but they are unable to develop effective managerial strategies and skills that are required for innovation.

Lack of Technological Infrastructure. Automobile is a complex machine comprising of more than 5000 individual parts and components which can be combined into 300 sub-assemblies. The technologies needed for

Table – 6. AIDP projections in the published report

manufacturing various sub-assemblies, components, and parts are diverse from each other. The technologies may include castings, machining, forgings, pressing of sheet metal parts, pressure die casting, electrical components and parts, motors, gauges, instruments and items made of plastic, rubber, glass, aluminum, copper, lead, glass, textiles etc. Since there has been increase in the number of auto parts being manufactured locally which covers a wide range of technologies and processes, it is therefore not possible to cover issues related individually to them. However, the overall issues and problems faced by the vendor industry have been discussed as follows:o No long term vision or policy.

o Lack of tooling and die

manufacturing facilities. o Systems are labor intensive.

o Competent/skilled labor is

scarce. o Available labor is not familiar

with modern technology. o Conventional machines are not

able to meet the precision manufacturing requirements.

o Scarcity of raw material

especially steel and other alloys. Economy of Scale. The experience

is that the cost penalty (additional price) on low production volumes may vary between 40 to 80% as compared to mass production. The same was proved to be the case in piston manufacturing in Pakistan where the cost was actually reduced by 50% simply by increasing the production rate to four times which brought down the price to 20% less than which prevailed in a in the replacement market.

Lack of Professionalism. Furthermore, there is a lack of personal involvement in achieving business growth and development. Hence, the tried and trusted managers run the business, while owners develop life interests in sports, cultural activities, community involvement, and politics and so on. In the absence of committed heirs and competent managers, the long-term fate of these companies is declining and is not likely to achieve the competitiveness needed in the world auto parts market.

Lack of Technical Skills and Competencies. Pakistan auto parts industry has its own peculiar problems. Technical know-how is the major issue where it needs guidance and assistance for achieving required growth rate and progress. Advancement in technology has necessitated auto parts industry to go for a proper development of human, technological and capital resources.

VIII – RECOMMENDATIONS

In order to enhance the competitive advantage of Auto Vendor Industry (AVI) in Pakistan the following recommendations have been developed using the fol pillars/ factors which are critical elements:- Infrastructure. There are no

organized industrial estates specifically designed for the auto sector in the country whereas, Thailand and India etc, have developed Special Economic Zones (SEZs) for the auto industry. We need to do the same. SEZs need to be created at or near Port Qasim in Karachi and at Shaikhupara in Lahore. Special incentives should be given for the units established in the zone i.e. tax holidays for 8 year, zero or no custom duty on imported plant and machinery, raw material

and components. Existing AVI units may be encouraged to relocate to either of the two SEZs to avail the above facilities. Thousands Acres of land need to be allocated for each of these 2 SEZs. The SEZs should be developed and managed by private investors. The contribution by the government should only be in the form of land.

Training And Skill Development. Training and skill development for the AVI sector cannot be over emphasized. 300,000 skilled workers, technicians, engineers and managers will be required in various disciplines so that proposed targets of producing 510,000 vehicles by 2011-12 is achieved. This is a very large number and very serious efforts will have to be made by federal and provincial governments as well as members of PAAPAM and PAPAM to work closely to train the above number of workers and professionals.

Technological Readiness. Technological readiness of the AVI units and their owners can be improved by exposing them to international best practices and through provision of business and technical advisory services developing entrepreneurship and through access to modern technologies and processes. Technology acquisition fund may be established to assist in the acquisition of modern technologies from Japan, EU, North America, Korea etc. This Technology Acquisition Fund may be created through the Export Development Fund and managed professionally by EDB and members of PAAPAM and PAMA.

Business Sophistication. The level of business sophistication and readiness to innovate needs to be improved through specially designed interventions. Programs

need to be developed to help them to corporative and professionalize their management. The promotion of innovation may be accomplished through development of entrepreneurial skills. In order to develop the AVI on scientific lines it is necessary to provide them with business and technical advisory services on a regular basis.

Market Efficiency. The market efficiency of AVI can be improved through increasing production which would lead to economies of scale and cost efficiency. As stated in grey areas in the case of piston produced by local vendors by doubling the production, the cost was reduced by 20%. The AVI market needs to be opened to international investors who may be invited to establish larger plants under their own management. This can be done through offering similar incentives as are proposed for the above SEZs which are comparable to those of Thailand, and India etc.

IX – CONCLUSION

Auto industries in emerging markets have substantially been transformed as a result of trade liberalization, globalization trends within the industry and the restructuring of assembler-supplier relationships. Global networks have replaced local supply linkages. Even when production remains local, design and contract allocation is increasingly global. This has led to considerable consolidation and restructuring of the components industry in countries such as Brazil, the Czech Republic, India, Pakistan, Poland and South Africa. Local first-tier producers have been marginalized. Nevertheless, there are opportunities for assembly and component plants in

developing countries to enter into international supply networks. The new value chains may link these plants to Triad markets or specifically to developing country markets. For government, the most important question is how to develop a policy mix, which maximizes the potential for insertion into global value chains. In this respect, the transition from qualitative restrictions and local content requirements towards import-export balancing requirements has played an important role. However, it is unclear to what extent these new sourcing arrangements would survive the abolition of TRIMs. Clearly, trade policies must be complemented by policies aimed at skill development if transnational companies are to be attracted not only towards the construction of low-cost production facilities, but also the development of design and engineering skills in their operations in developing countries.

BIBLOGRAPHY

Automotive and Components Global Report — 2010 An IMAP

INDUSTRIALS Report.

On the Road: U.S. Automotive Parts Industry Annual Assessment, Office of

Transportation and Machinery U.S. Department of Commerce 2011.

Policy Analysis on the Competitive Advantage of Automotive Vendor

Industry in Pakistan Problems and Prospects by Competitiveness Support

Fund 2007.

Diagnostic Study Autoparts Cluster Lahore – Pakistan Conducted

By Mr. Mohammad Asif – SMEDA Punjab Lahore.

The Automotive Parts Sector in Pakistan by European Commission (EC)

Trade Related Technical Assistance Programme 2007.

Pakistan Investment Guide 2004.

Pakistan Statistical Year Book 2011.

Auto Industry Development Program – 2007.

PAAPAM Buyer’s Guide – 2011.

Crain Communications, Automotive News Supplement, "Top 100 Global

Suppliers," June 2011.

Organisation Internationale des Constructeurs d'Automobiles/International

Organization of Motor Vehicle Manufacturers 2011 supplement.

Auto Component Industry Report by Dun & Bradstreet India.

Pakistan Automotive Manufacturers Association Statistical Guide Book

2011.

Automobile Industry updated 27 Jan 2010! Compiled by: Mirza Rohail B.

www.OCIA.net . www.wikipedia.com .