WORLDWIDE COMPETITION IN LAUNCH SERVICES€¦ · WORLDWIDE COMPETITION IN LAUNCH SERVICES. ......

24

ESA UNCLASSIFIED - For Official Use WORLDWIDE COMPETITION IN LAUNCH SERVICES Colloque international - Les lanceurs européens 3 November 2015

Transcript of WORLDWIDE COMPETITION IN LAUNCH SERVICES€¦ · WORLDWIDE COMPETITION IN LAUNCH SERVICES. ......

ESA UNCLASSIFIED - For Official Use

WORLDWIDE COMPETITION IN

LAUNCH SERVICES

Colloque international - Les lanceurs européens 3 November 2015

ESA UNCLASSIFIED - For Official Use

History of transportation Technological innovation

1

ESA UNCLASSIFIED - For Official Use 2

Intensive progress made through technology -

Beginnings are special

ESA UNCLASSIFIED - For Official Use

Progressive evolution from space race

• Domestic strategic demand and national pride

• Commercial uses and communication satellites

• Competition for commercial payloads as from late 70s

• Launch service agreement Arianespace/Intelsat

3

ESA UNCLASSIFIED - For Official Use

Commercial launch services Europe - United States

• Stop of US ELV production lines

• Exclusive US commercialisation through Space Shuttle

• China, Russia, Ukraine - bilateral US agreements

• Regulation of prices and quotas

• International joint ventures

4

ESA UNCLASSIFIED - For Official Use

Commercial launch service Europe - Russia

• Abandonment of Russian launch quotas in 2000

• Competition increase

• Demand contraction

• US withdrawal from market

• Ariane - Proton

• Converted Soviet era ICBMs

5

ESA UNCLASSIFIED - For Official Use

Commercial launch service Current situation - GTO

• Proton failures

• Falcon 9 - Ariane 5

• LMCLS and MHI

• ITAR - Chinese turnkey solutions

• India - domestic demand

• New strategies for payload insertion

• Electric propulsion satellites

6

ESA UNCLASSIFIED - For Official Use

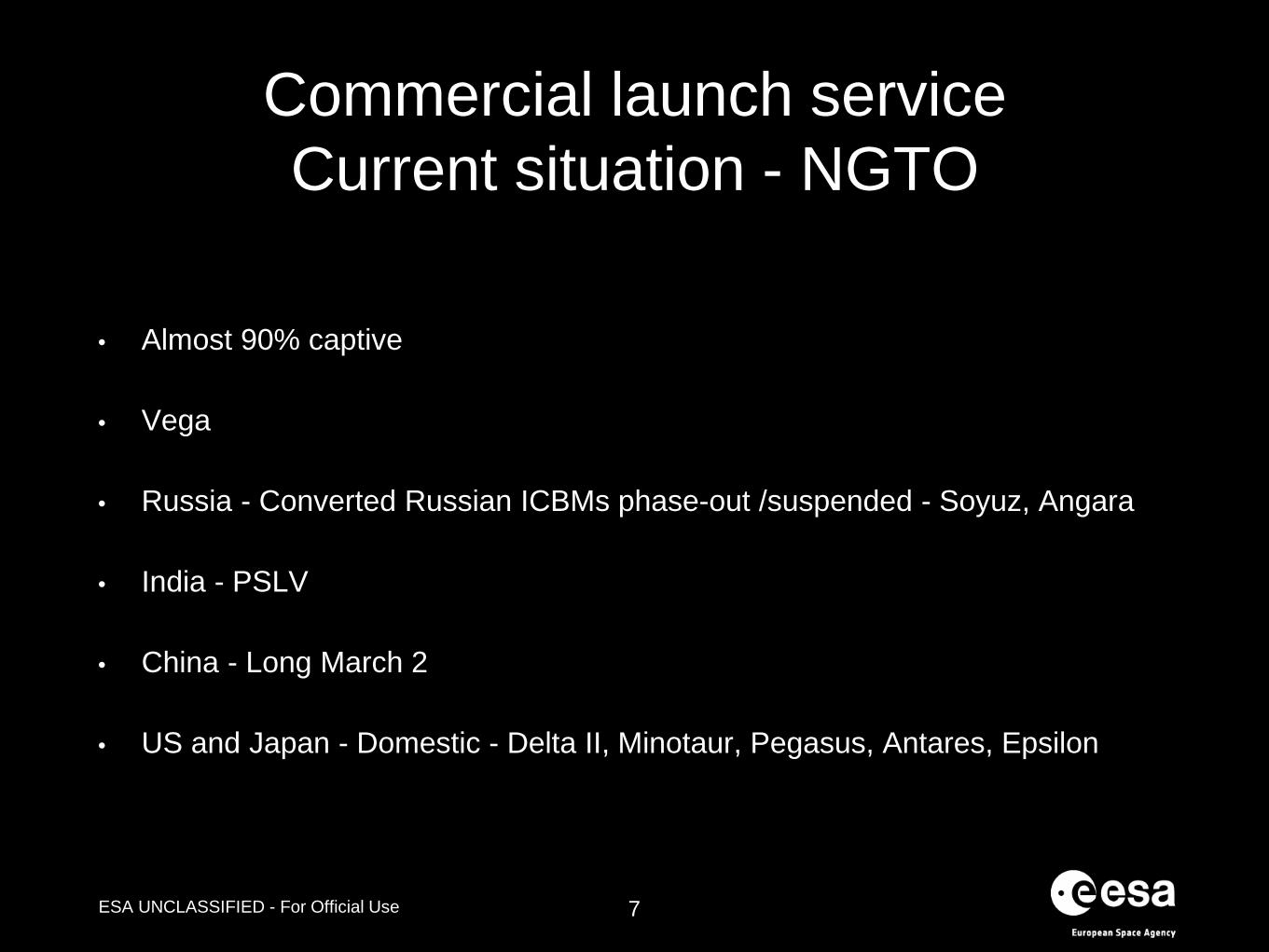

Commercial launch service Current situation - NGTO

• Almost 90% captive

• Vega

• Russia - Converted Russian ICBMs phase-out /suspended - Soyuz, Angara

• India - PSLV

• China - Long March 2

• US and Japan - Domestic - Delta II, Minotaur, Pegasus, Antares, Epsilon

7

ESA UNCLASSIFIED - For Official Use

Worldwide offer

8

ESA UNCLASSIFIED - For Official Use

Market and competition

Market: extent of demand in which buyers and sellers come together and forces of supply and

demand affect prices

Competition: effort of 2 or more parties acting independently to secure the business of a 3rd party

by offering the most favorable terms

9

ESA UNCLASSIFIED - For Official Use

Relevant market - commercial

• No free competition

• Substantial government backing

• Captivity of national institutional payloads to domestic launch services

• Distinction between Government and commercial applications

• Commercial market characterisation: Size, Orbit and Worldwide basis

10

ESA UNCLASSIFIED - For Official Use 11

LEO

Projects can be financed by one

country

Mainly captive institutional customers

Limited competition

Cooperation for

initial launch capability

development

LEO GTO/GEO Exploration

Distance from Earth

Competition

Cooperation

GEO/GTO

Highly competitive environment

Projects can be financed by one

country

Both institutional and commercial needs Also serving mega-

constellations ISS access / Exploration

Projects can no

longer be financed by a single party

Need for

cooperative efforts

Cooperation and competition

ESA UNCLASSIFIED - For Official Use

Headwinds for European launch services

• Political, economic and industrial motivation for independent access to space

• All non-European institutional demand captive to domestic sources - almost 70% of worldwide demand

• Solid base - launch rate - to access commercial market in addition

• Small European institutional demand - increase EU Galileo and Copernicus

• Europe is highly dependent on the commercial market to ensure affordability

• International environment quickly evolving and worldwide competition increasing

12

ESA UNCLASSIFIED - For Official Use

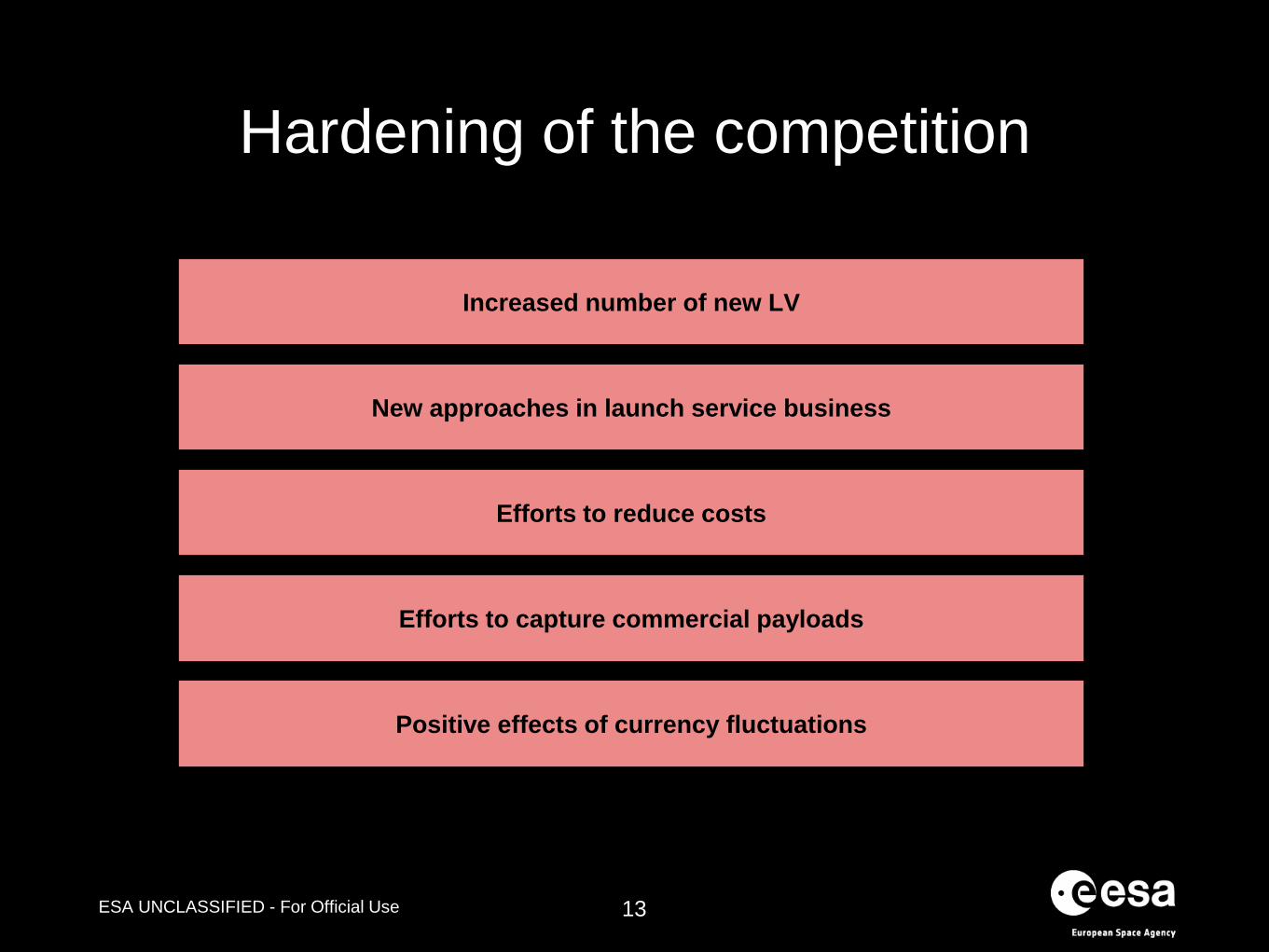

Hardening of the competition

13

Increased number of new LV

New approaches in launch service business

Efforts to reduce costs

Efforts to capture commercial payloads

Positive effects of currency fluctuations

ESA UNCLASSIFIED - For Official Use

Evolving launch service offer

14

Commoditisation

Innovative approaches in development and production (e.g. USA)

Flexibility through vehicle modularity

New injection orbits

Package deals (e.g. Russia, China)

Extension of payload capacity (very heavy and very small vehicles)

Multiple launch sites targeting specific customers, allowing launch rate increase

Reduction of turn-around-times

Environmental considerations

DEMAND AND EVOLVING NEEDS

ESA UNCLASSIFIED - For Official Use

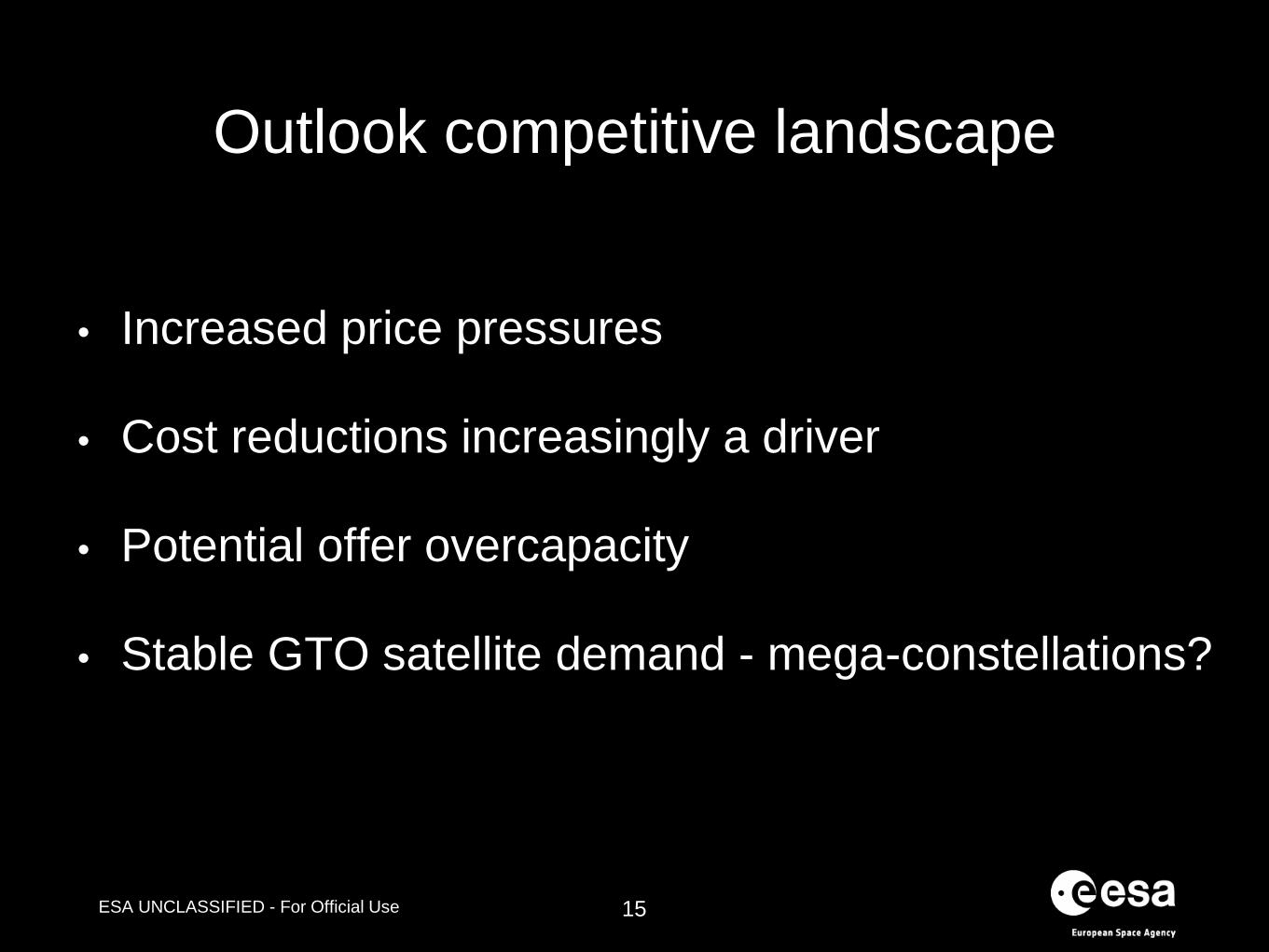

Outlook competitive landscape

• Increased price pressures

• Cost reductions increasingly a driver

• Potential offer overcapacity

• Stable GTO satellite demand - mega-constellations?

15

ESA UNCLASSIFIED - For Official Use

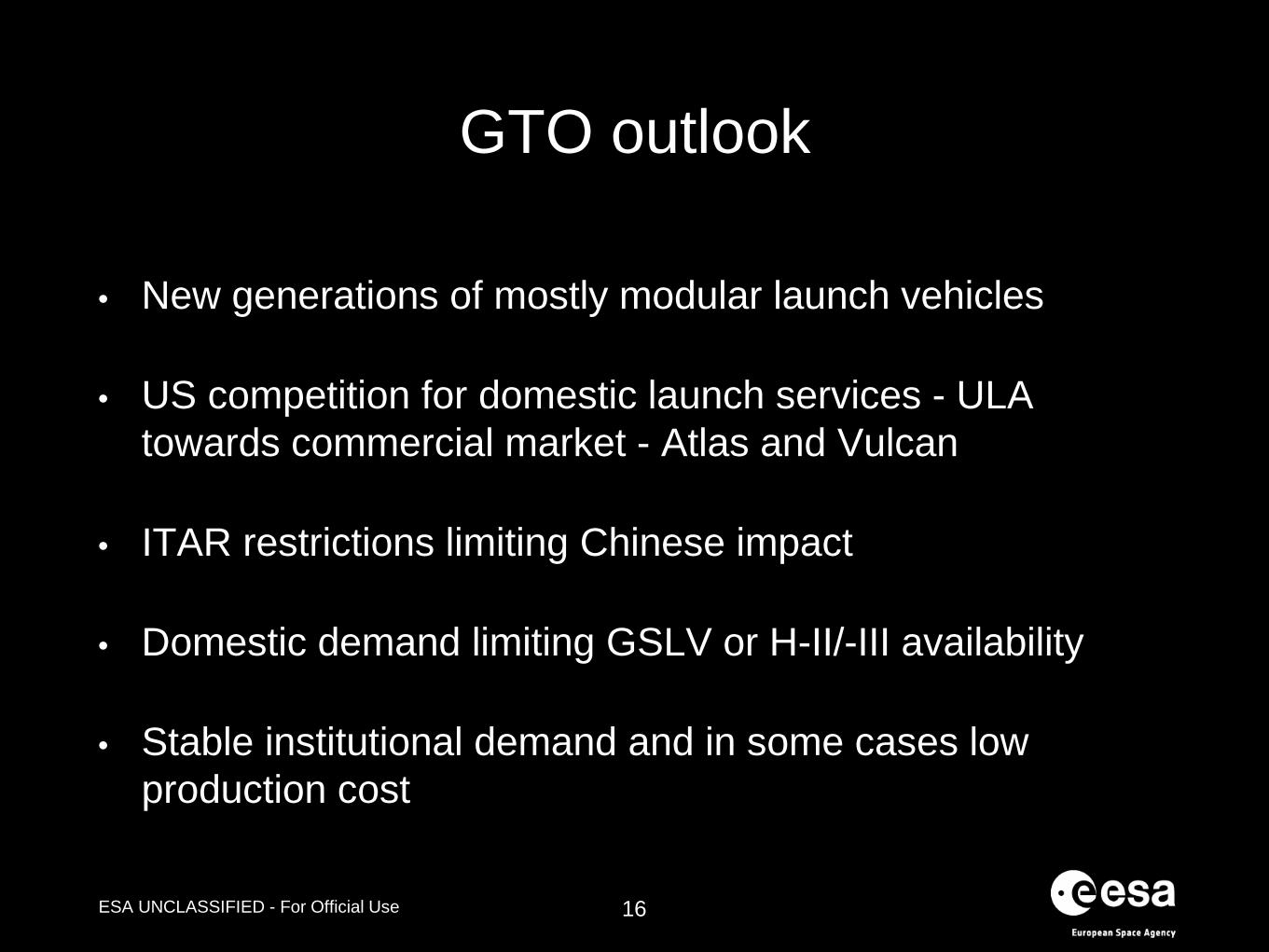

GTO outlook

• New generations of mostly modular launch vehicles

• US competition for domestic launch services - ULA towards commercial market - Atlas and Vulcan

• ITAR restrictions limiting Chinese impact

• Domestic demand limiting GSLV or H-II/-III availability

• Stable institutional demand and in some cases low production cost

16

ESA UNCLASSIFIED - For Official Use

Competitive Environment - GTO

17

Launch services contracts dominated by

Arianespace and SpaceX

Limited presence

Proton RUR exchange rate allowing slow comeback

Atlas V 1 contract signed each 2013 and 2015

Commercially inactive

Zenit suspended

Delta IV no commercial activity

H-II no contracts since 2013

Long March 3 ITAR restrictions

GSLV Mk II low performance

Current situation

Potential overcapacity, increased willingness to

compete on the commercial market

Developments in all major countries

Ariane 6 2020

Angara 5 in test phase (9 flights left)

Falcon Heavy 2016 (already signing)

Vulcan 2019

H-III 2021

Long March 5/7 2016

GSLV Mk III 2016 (suborbital test flight 2014)

Outlook

ESA UNCLASSIFIED - For Official Use

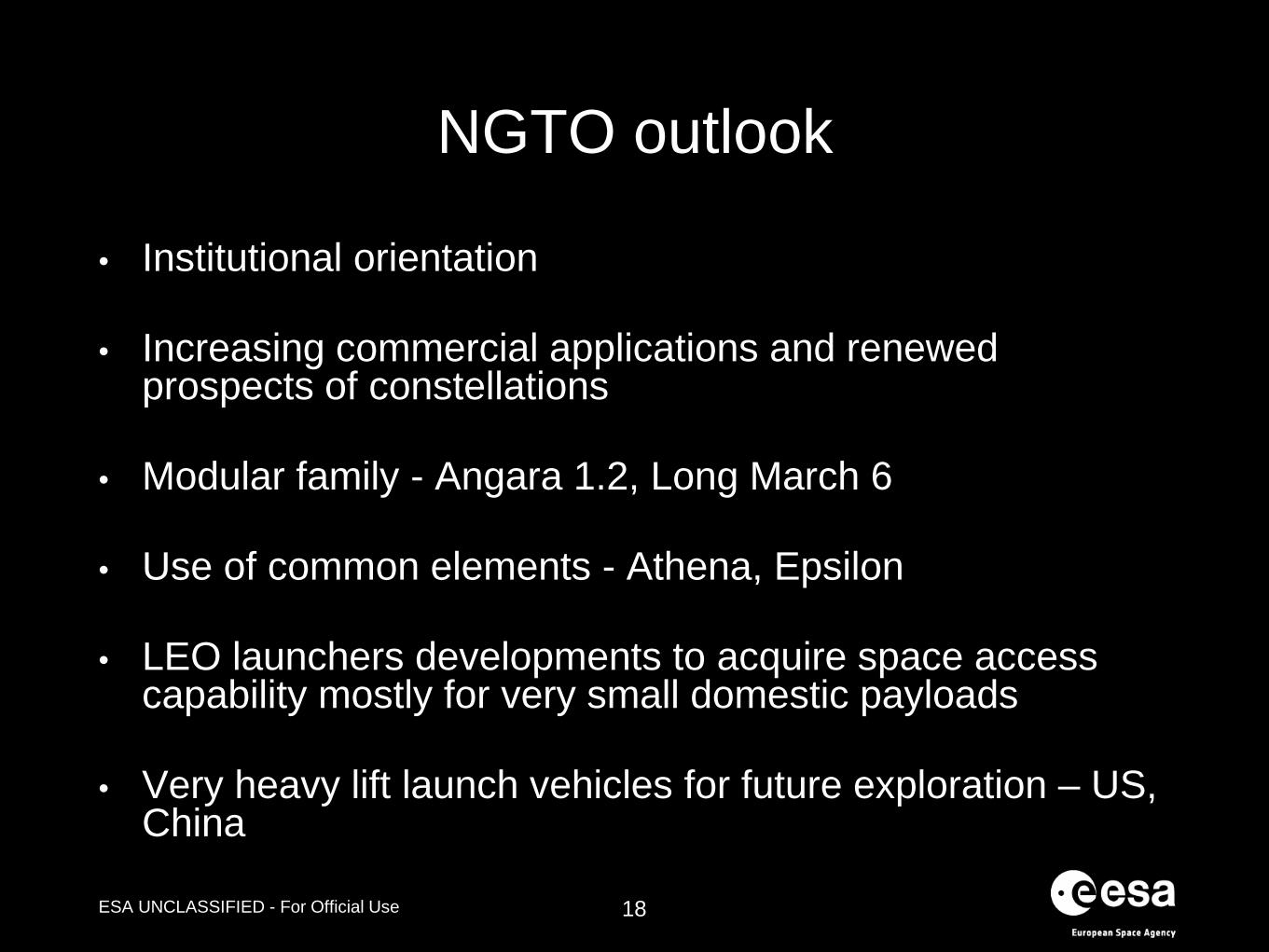

NGTO outlook

• Institutional orientation

• Increasing commercial applications and renewed prospects of constellations

• Modular family - Angara 1.2, Long March 6

• Use of common elements - Athena, Epsilon

• LEO launchers developments to acquire space access capability mostly for very small domestic payloads

• Very heavy lift launch vehicles for future exploration – US, China

18

ESA UNCLASSIFIED - For Official Use

Competitive Environment - NGTO

19

Current situation

Predominantly captive institutional demand

Not relying on commercial launches

Commercial activity:

Russia (Dnepr, Rockot): phase-out / suspended

Europe (Vega)

India (PSLV): 1 launch p.a. + piggyback

Reduced commercial activity:

China (Long March 2)

USA (Delta II, Minotaur, M-C, Pegasus, Antares)

Japan (Epsilon)

Outlook

Growing commercial applications, constellations

may change commercial stance of some LSP

Modular LV families could respond to demand increase

Russia Soyuz 2.1v, Angara 1.2

Europe Vega

India PSLV

China Long March 6/7

USA Minotaur/-C, Antares, Falcon 9

Japan Epsilon phase 2

Others Israel, Brazil, Iran, Argentina, Korea

ESA UNCLASSIFIED - For Official Use

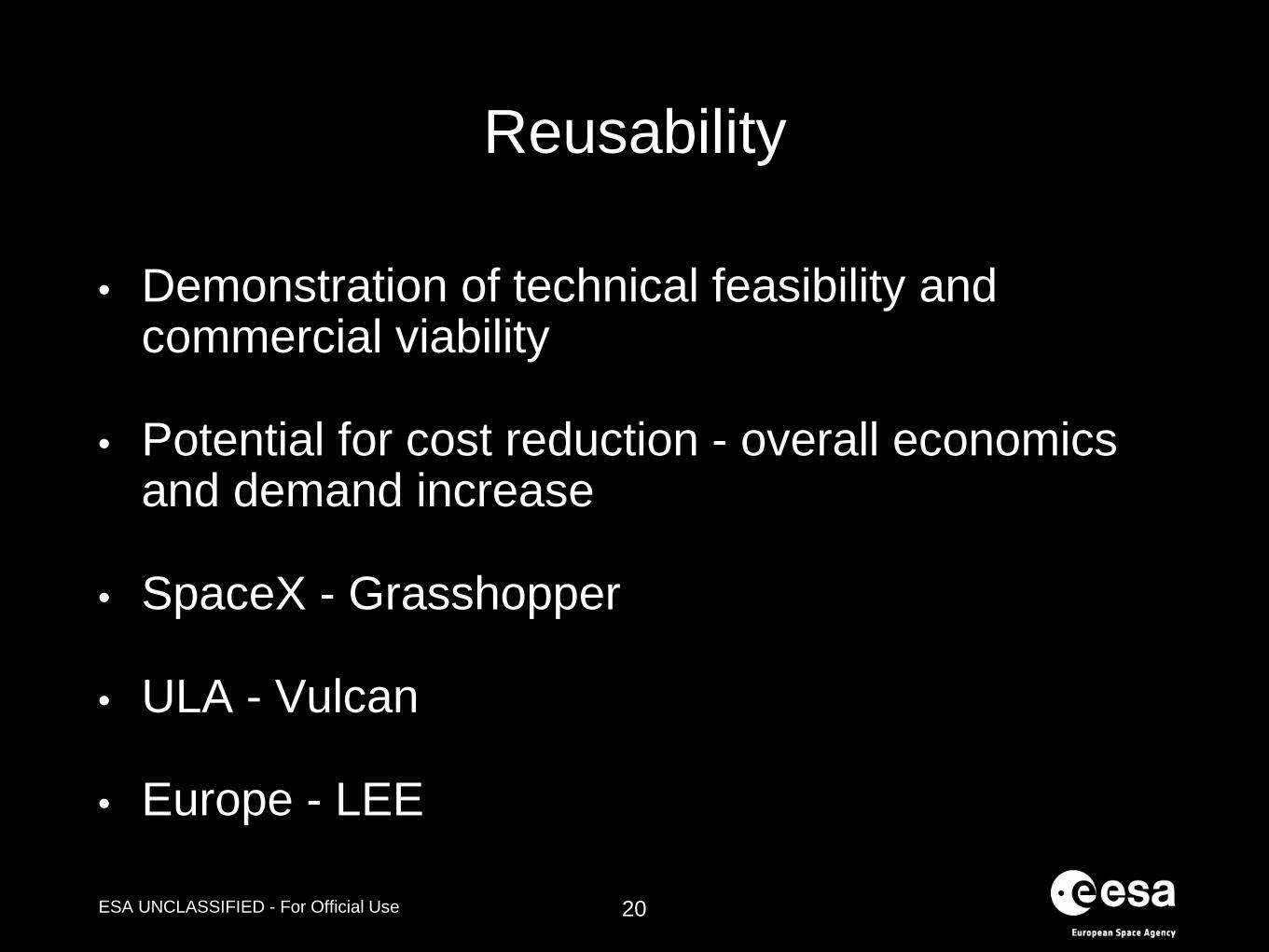

Reusability

• Demonstration of technical feasibility and commercial viability

• Potential for cost reduction - overall economics and demand increase

• SpaceX - Grasshopper

• ULA - Vulcan

• Europe - LEE

20

ESA UNCLASSIFIED - For Official Use

CLOSING REMARKS

21

ESA UNCLASSIFIED - For Official Use

“No one can predict the future exactly but we know two things: it’s going to be different, and it must be

rooted in today’s world” - Peter Thiel

22

ESA UNCLASSIFIED - For Official Use

WORLDWIDE COMPETITION IN

LAUNCH SERVICES

Colloque international - Les lanceurs européens 3 November 2015