By Mari Riess Jones The Dynamics of Attending and Scene Analysis.

18th WORLD EDITORS FORUM

63rd WORLD NEWSPAPER CONGRESS

Titel: World Press Trends 2011Speaker: Christoph Riess

www.wan-ifra.org

WORLD PRESS TRENDS 2011

Christoph Riess

© 2011 WAN-IFRA | 3

Since 1988

Value over volume

Focus on key numbers in key markets

New office-based data collection

Ongoing up-dating instead of a sprint

Electronic database access any time

New presentation

Insights overnumbers

World Press Trends – The Book

© 2011 WAN-IFRA | 4

MEDIA CONSUMPTION SHIFTIs it all Internet now?

ADVERTISING EXPENDITURES BY MEDIAWhere is the money going?

ECONOMICAL DEVELOPMENTAre we back on track?

NEWSPAPER CIRCULATION AND NUMBER OF TITLESIs it only decline?

NEWSPAPER REVENUEIs it content paid, advertising

paid or digital revenue?

INTERNET VERSUS MOBILEWill tablets be our saviour?

© 2011 WAN-IFRA | 5

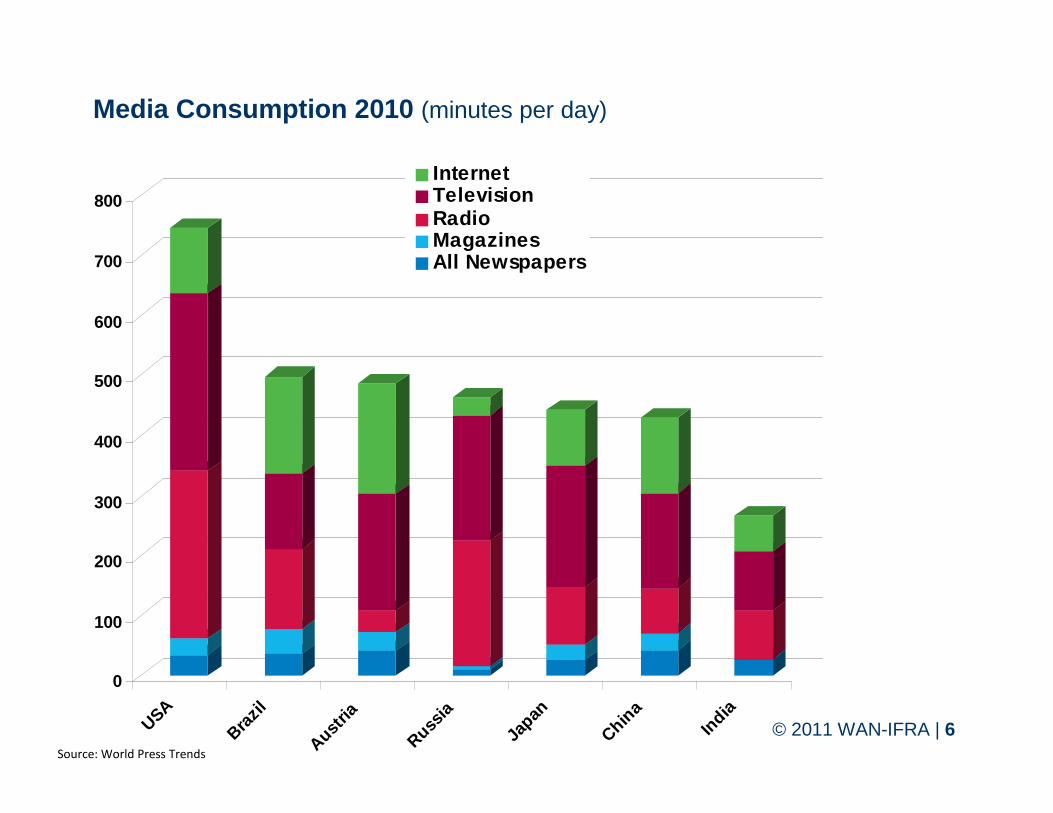

MEDIA CONSUMPTION SHIFTIs it all Internet now?

© 2011 WAN-IFRA | 6

Media Consumption 2010 (minutes per day)

0

100

200

300

400

500

600

700

800

USA

Brazil

Austri

a

Russia

Japa

n

China

Ind ia

InternetTelevisionRadioMagazinesAll Newspapers

Source: World Press Trends

© 2011 WAN-IFRA | 7

Internet

Television

Radio

Magazines

All newspapers

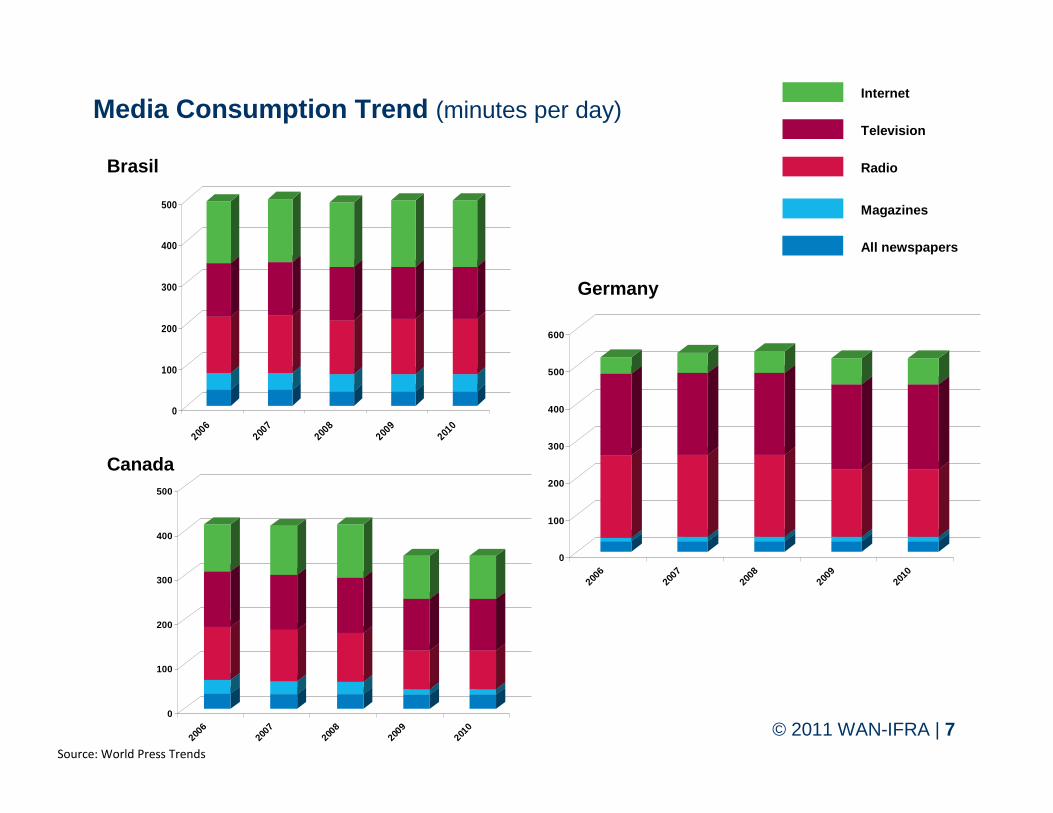

Canada

Germany

Media Consumption Trend (minutes per day)

0

100

200

300

400

500

2006

2007

2008

2009

2010

Brasil

0

100

200

300

400

500

2006

2007

2008

2009

2010

0

100

200

300

400

500

600

2006

2007

2008

2009

2010

Source: World Press Trends

© 2011 WAN-IFRA | 8

ECONOMICALDEVELOPMENTAre we back on track?

© 2011 WAN-IFRA | 9

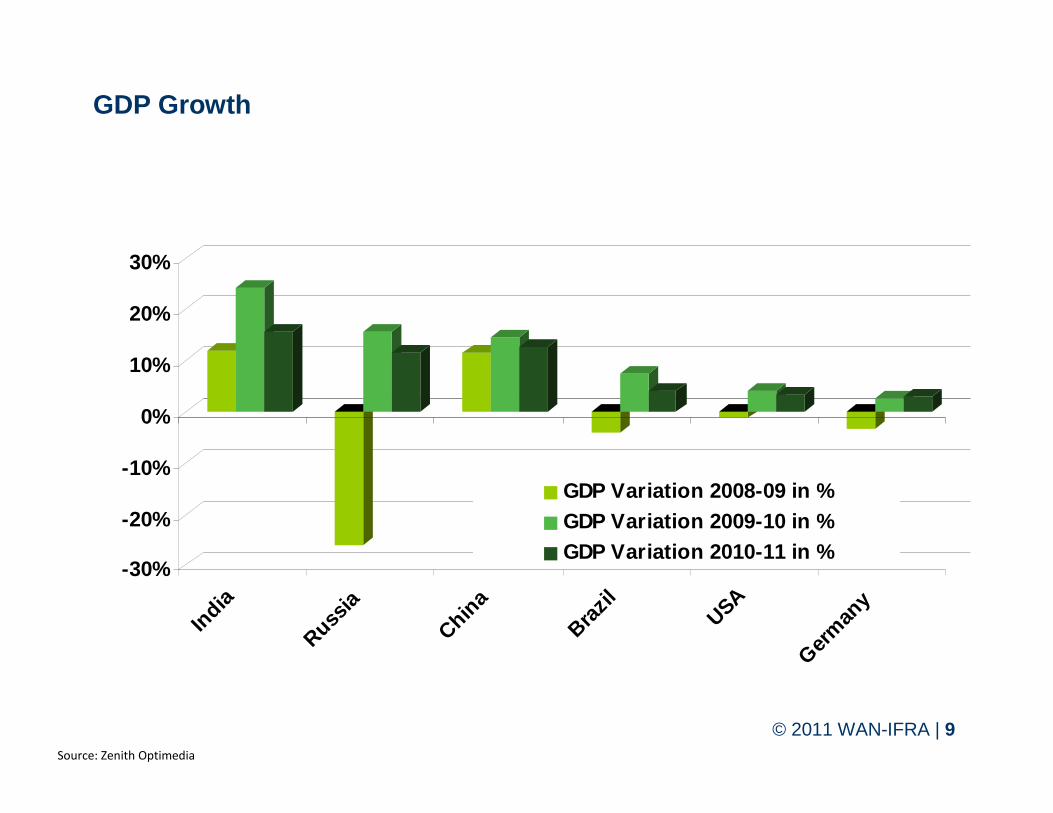

GDP Growth

-30%

-20%

-10%

0%

10%

20%

30%

Indi

a

Russ ia

China

Braz il

USA

Germ

any

GDP Variation 2008-09 in %GDP Variation 2009-10 in %GDP Variation 2010-11 in %

Source: Zenith Optimedia

© 2011 WAN-IFRA | 10Need toSource: Zenith Optimedia

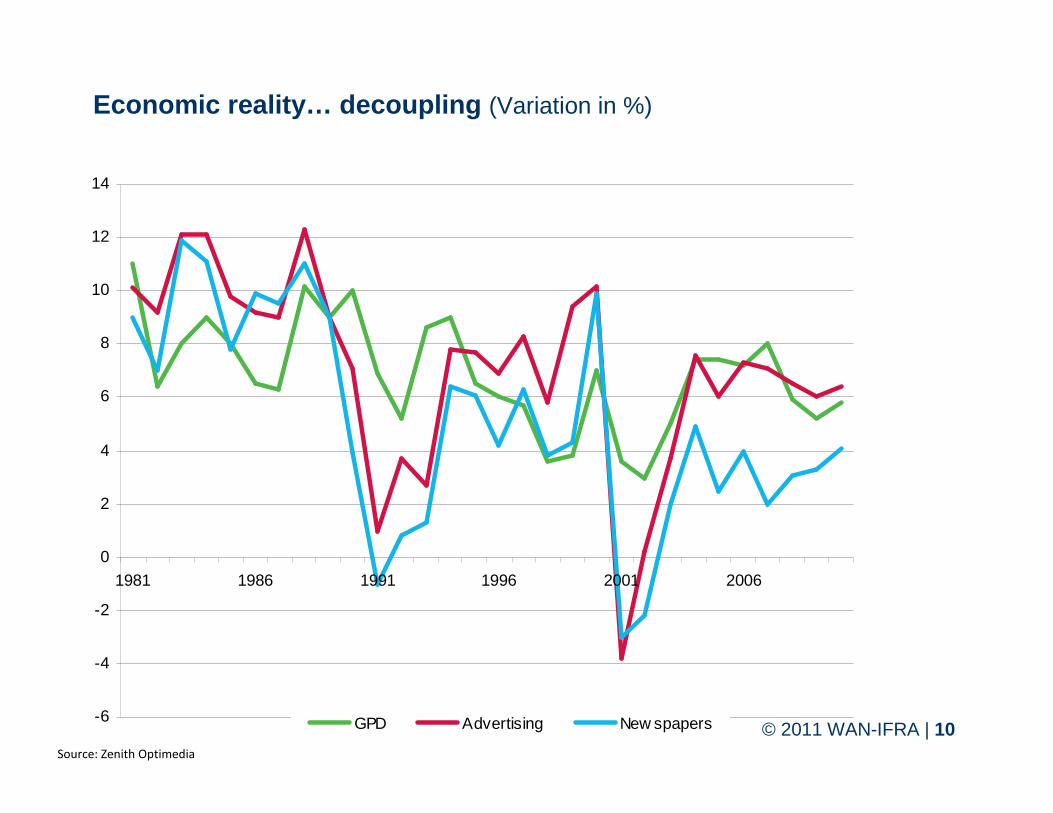

Economic reality… decoupling (Variation in %)

-6

-4

-2

0

2

4

6

8

10

12

14

1981 1986 1991 1996 2001 2006

GPD Advertising New spapers

© 2011 WAN-IFRA | 11

NEWSPAPER CIRCULATIONIs it only decline?

© 2011 WAN-IFRA | 12

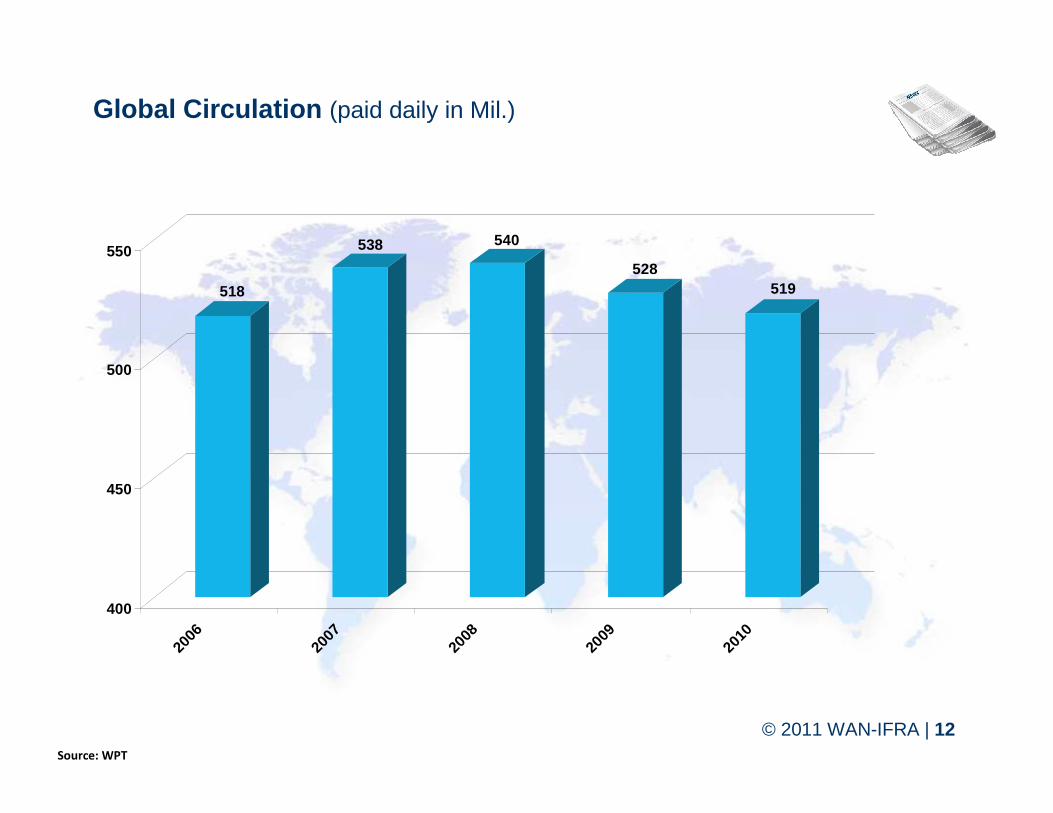

Global Circulation (paid daily in Mil.)

518

538 540

528519

400

450

500

550

2006

2007

2008

2009

2010

Source: WPT

© 2011 WAN-IFRA | 13

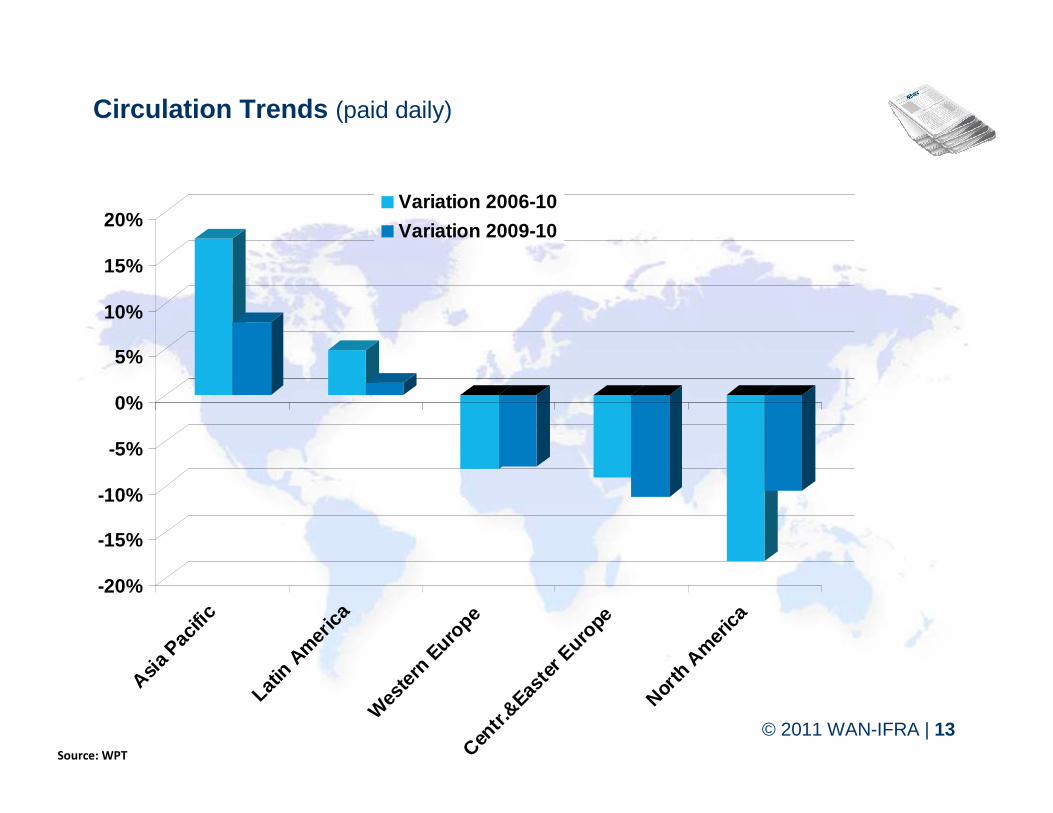

Circulation Trends (paid daily)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Asia P

acifi

c

Lati n

Am

erica

Wes

tern

Eur

ope

Centr.

&Easte

r Eur

o pe

North

Am

erica

Variation 2006-10

Variation 2009-10

Source: WPT

© 2011 WAN-IFRA | 14

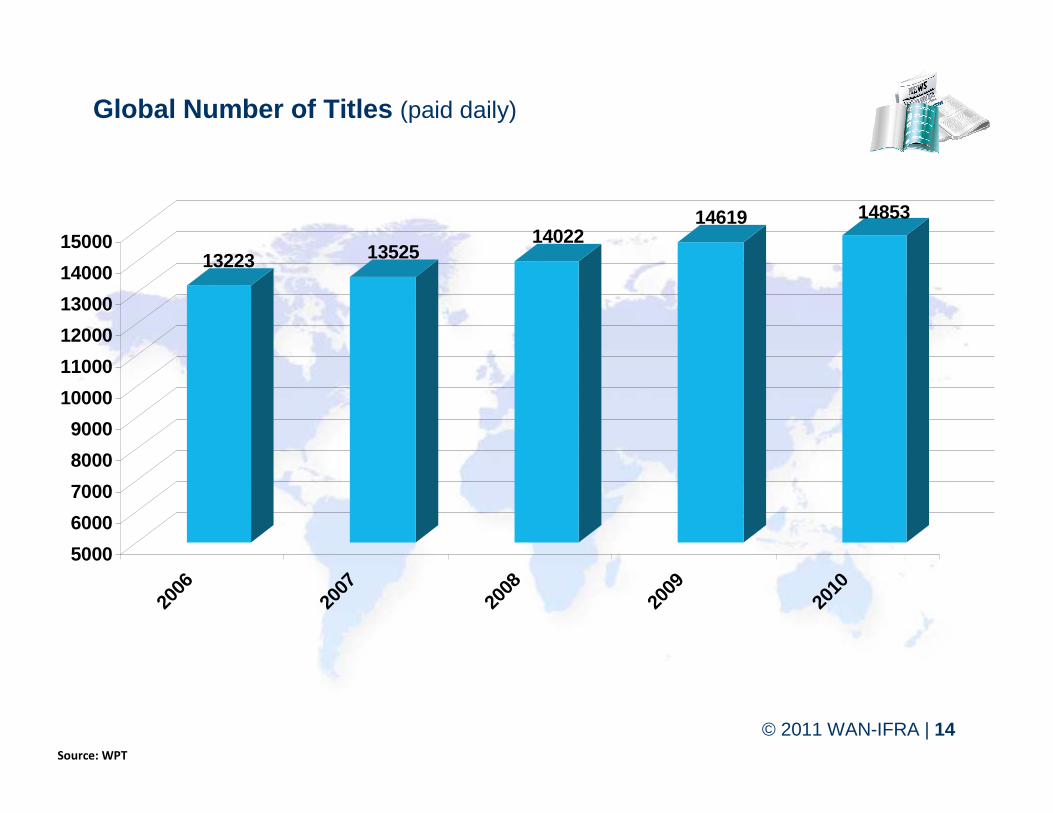

Global Number of Titles (paid daily)

Source: WPT

13223 1352514022

14619 14853

5000

6000

7000

8000

9000

10000

11000

12000

13000

14000

15000

2006

2007

2008

2009

2010

© 2011 WAN-IFRA | 15

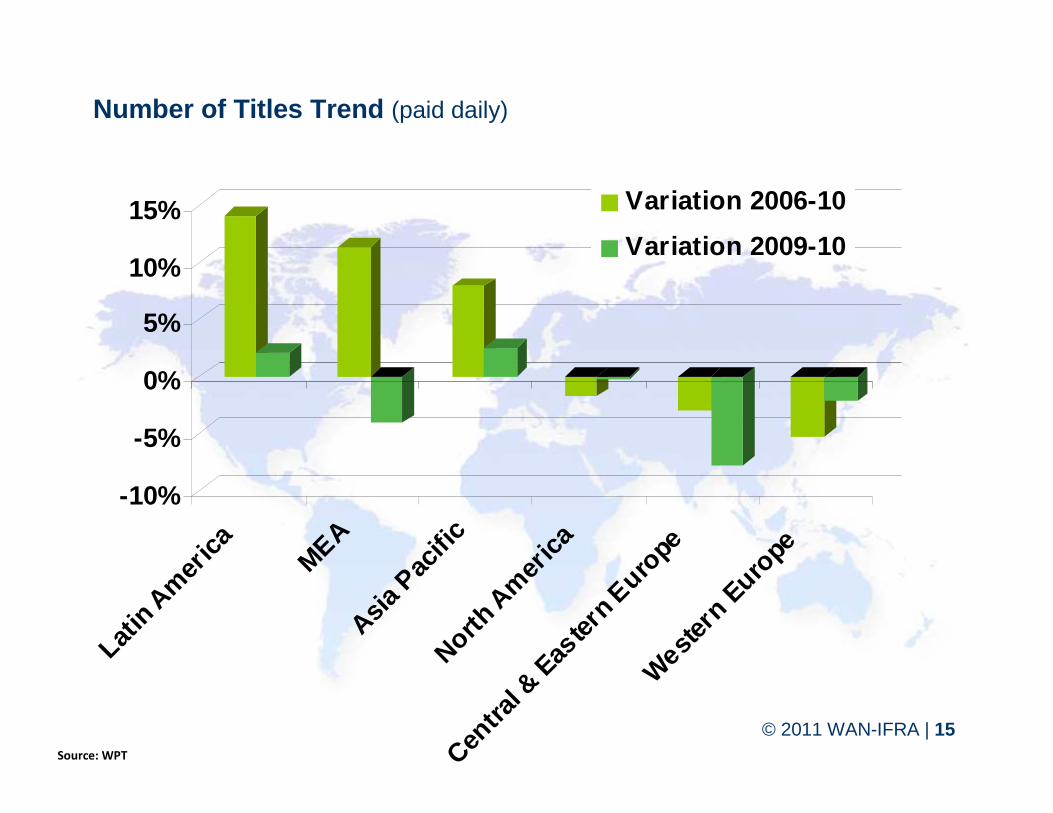

Number of Titles Trend (paid daily)

Source: WPT

-10%

-5%

0%

5%

10%

15%

Latin

Am

eric

a

MEAAsia

Pac

ific

North A

mer

ica

Centra

l & E

astern

Eur

o peW

estern

Eur

ope

Variation 2006-10

Variation 2009-10

© 2011 WAN-IFRA | 16

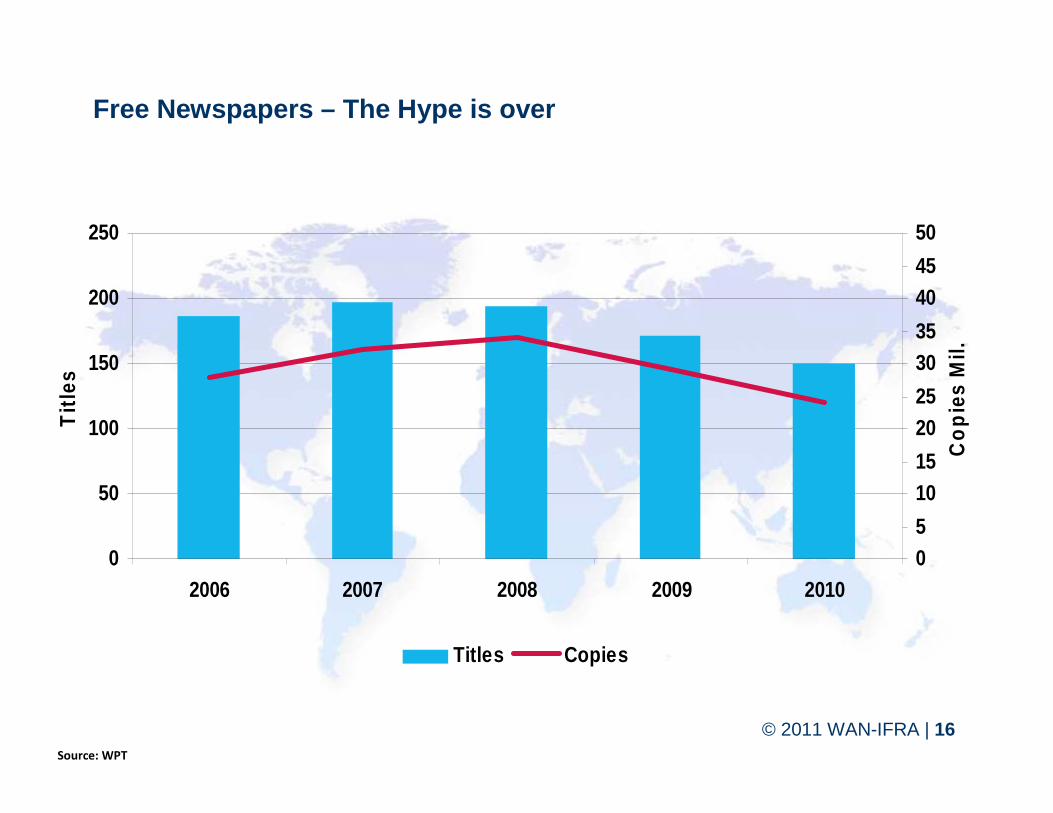

0

50

100

150

200

250

2006 2007 2008 2009 2010

Titl

es

05

1015

2025

3035

4045

50

Cop

ies

Mil.

Titles Copies

Source: WPT

Free Newspapers – The Hype is over

© 2011 WAN-IFRA | 17© 2011 WAN-IFRA | 17

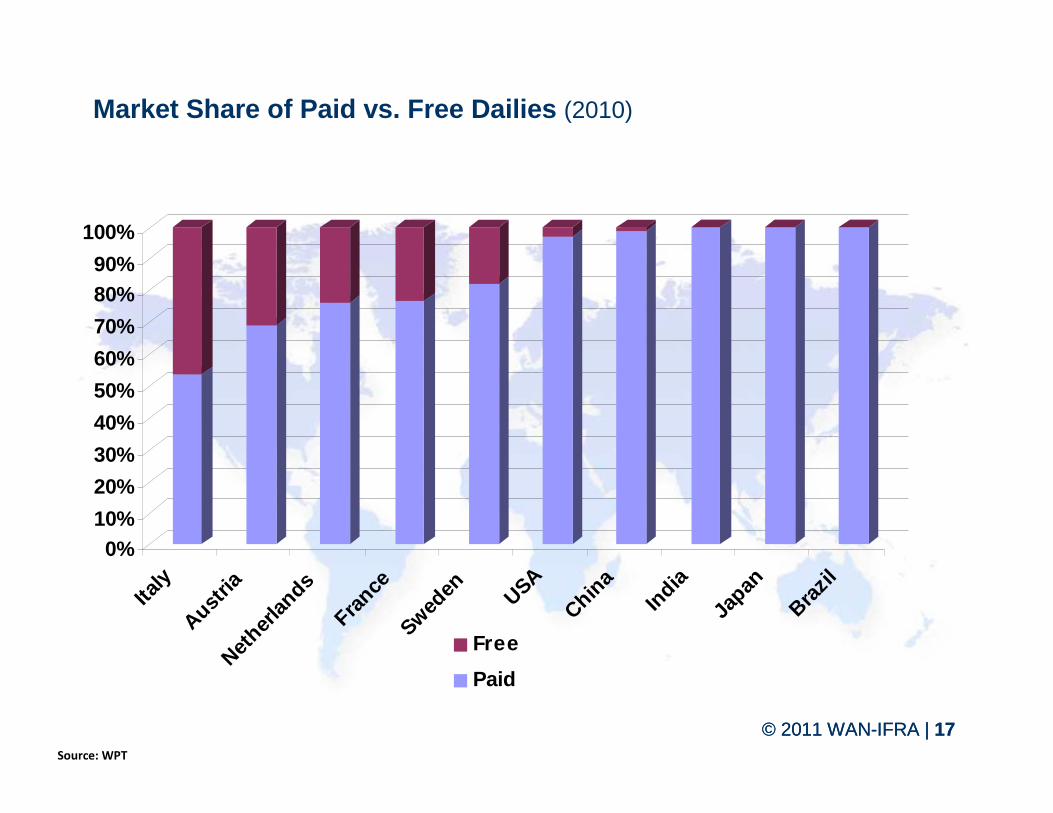

Market Share of Paid vs. Free Dailies (2010)

Source: WPT

0%10%

20%

30%

40%

50%

60%

70%

80%90%

100%

Italy

Austria

Nethe

r lands

France

Sweden USA

China

India

Japan

Brazil

Free

Paid

© 2011 WAN-IFRA | 18

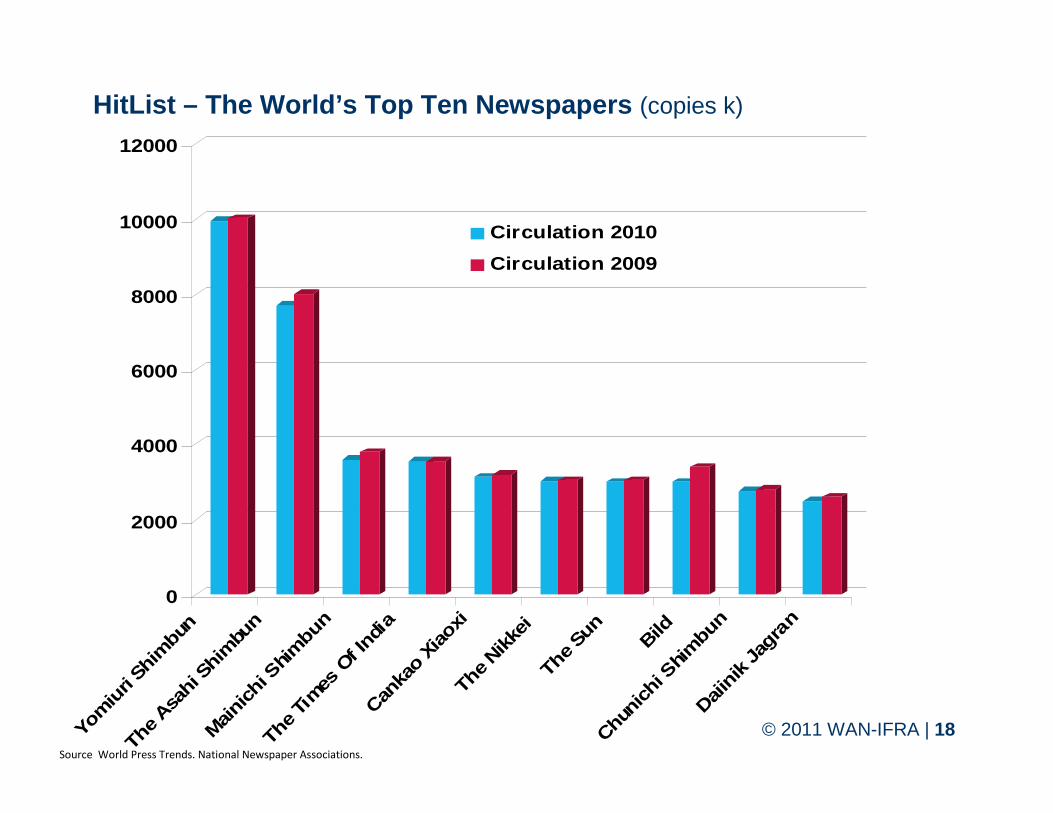

HitList – The World’s Top Ten Newspapers (copies k)

Source World Press Trends. National Newspaper Associations.

0

2000

4000

6000

8000

10000

12000

Yom

iuri

Shim

bun

The

Asahi

Shi

mbu

n

Main

ichi S

him

bun

The

Times

Of I

ndia

Canka

o Xi

aoxi

The

Nikkei

The

Sun

Bild

Chuni

chi S

him

bunDaii

nik

Jagr

anCirculation 2010

Circulation 2009

© 2011 WAN-IFRA | 19

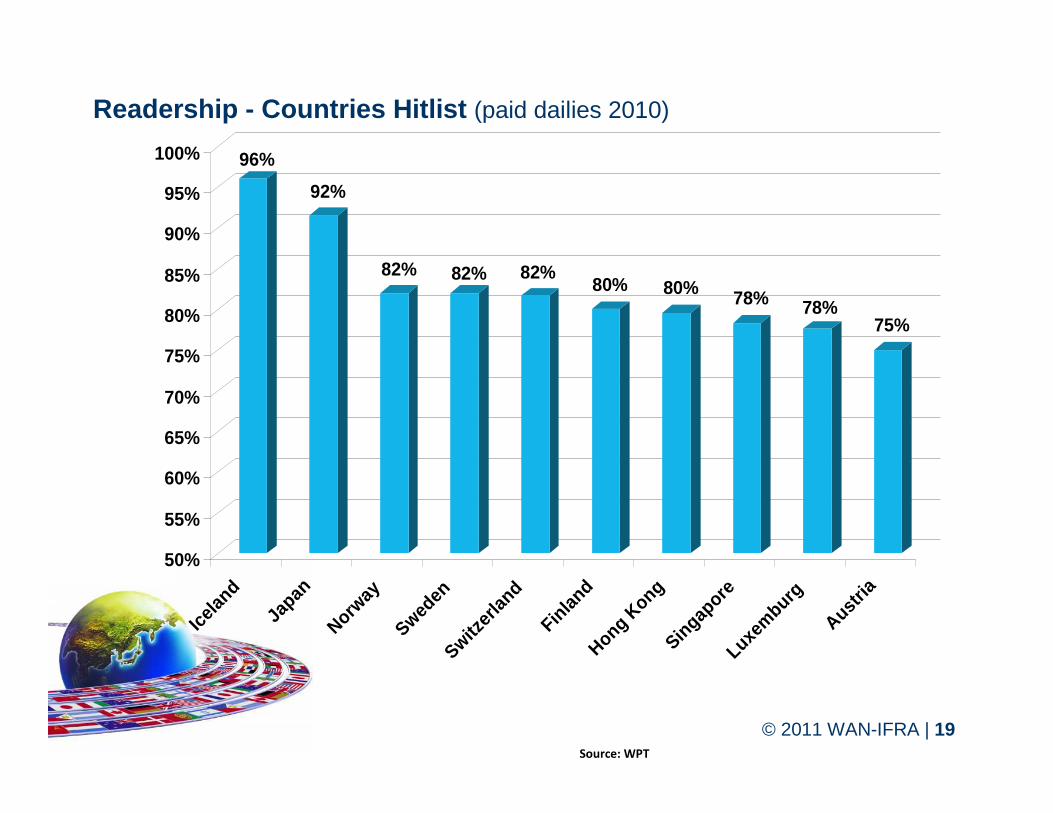

Readership - Countries Hitlist (paid dailies 2010)

96%

92%

82% 82% 82%80% 80% 78% 78%

75%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Icelan

d

Japa

n

Norway

Sweden

Switzer

l and

Finlan

dHon

g Kon

gSing

apor

eLux

embu

rg

Austr i

a

Source: WPT

© 2011 WAN-IFRA | 20

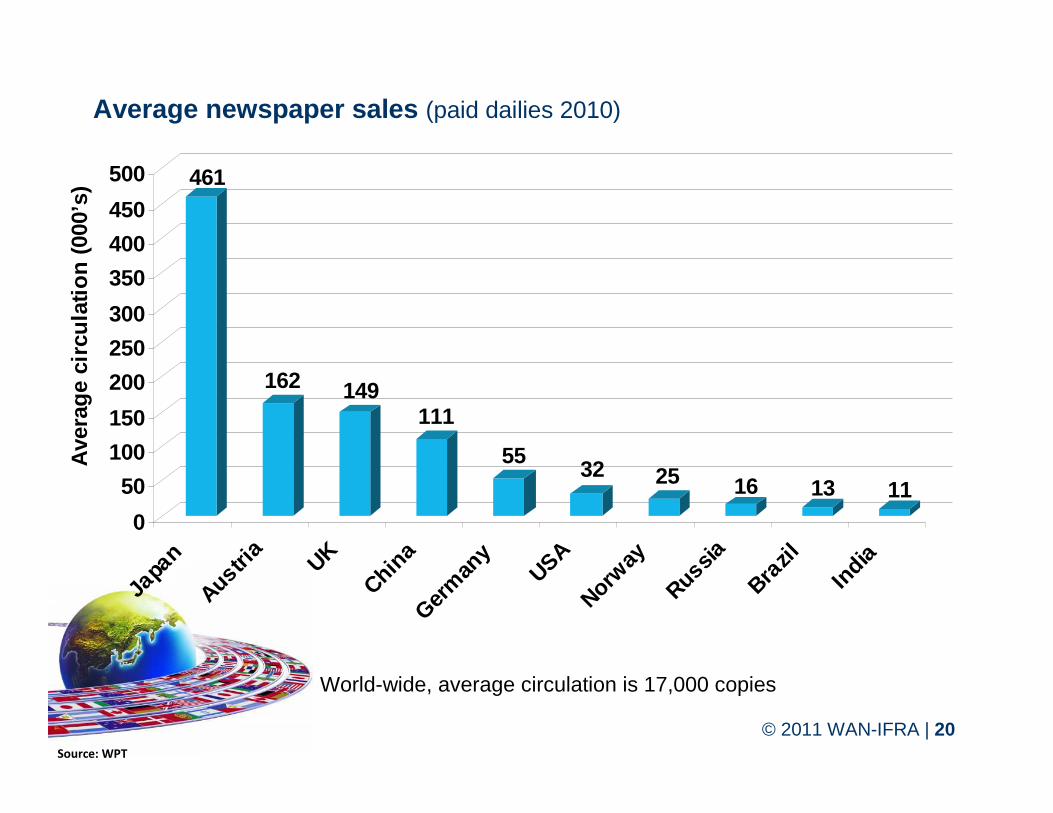

461

162 149111

5532 25 16 13 11

0

50

100

150

200

250

300

350

400

450

500

Japan

Austria

UK

China

Germ

any

USANor

way

Russia

Brazil

India

Ave

rage

circ

ulat

ion

(000

’s)

Source: WPT

World-wide, average circulation is 17,000 copies

Average newspaper sales (paid dailies 2010)

© 2011 WAN-IFRA | 21

ADVERTISING EXPENDITURES BY MEDIAWhere is the money going?

© 2011 WAN-IFRA | 22

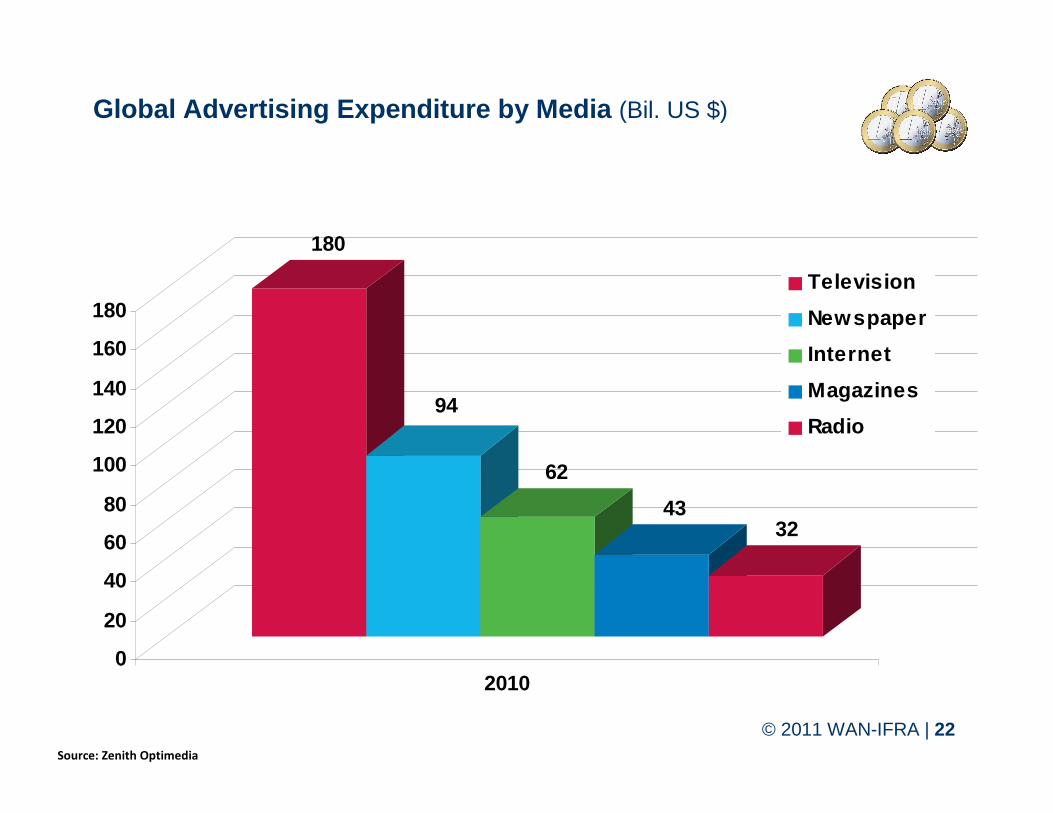

Global Advertising Expenditure by Media (Bil. US $)

180

94

62

4332

0

20

40

60

80

100

120

140

160

180

2010

Television

Newspaper

Internet

Magazines

Radio

Source: Zenith Optimedia

© 2011 WAN-IFRA | 23

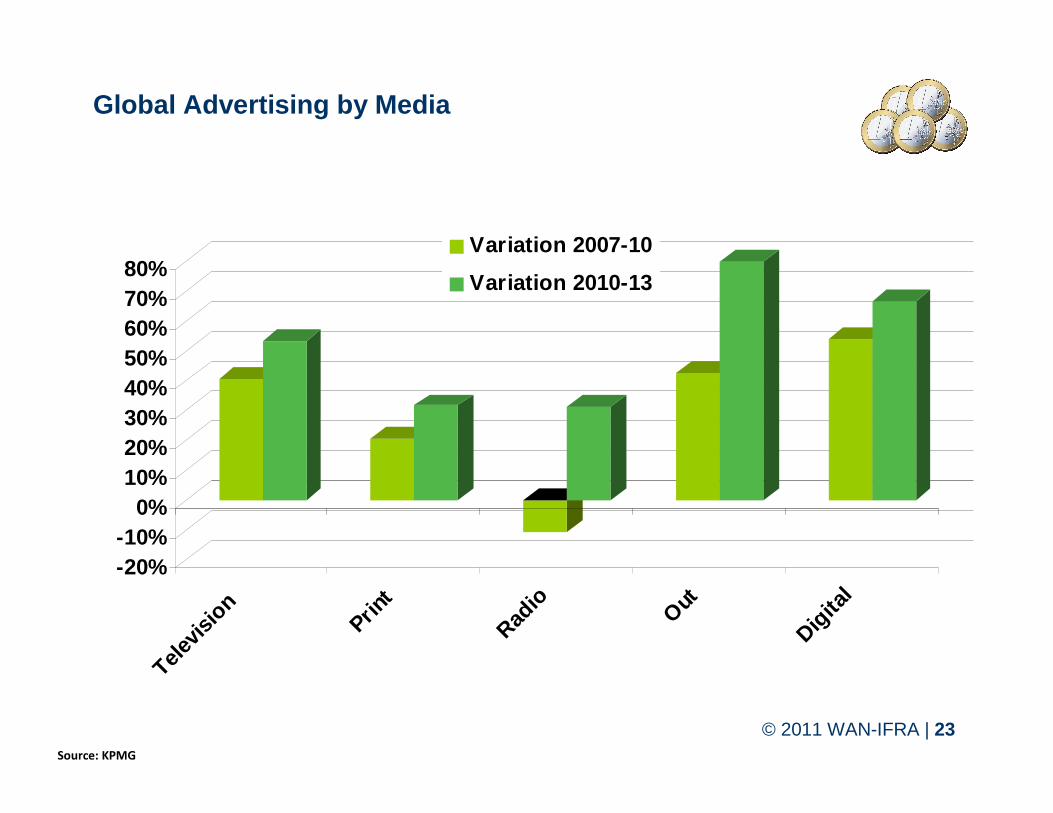

Global Advertising by Media

-20%-10%

0%10%20%30%40%50%60%70%80%

Televis

ion Print

Radio Out

Digita

l

Variation 2007-10

Variation 2010-13

Source: KPMG

© 2011 WAN-IFRA | 24

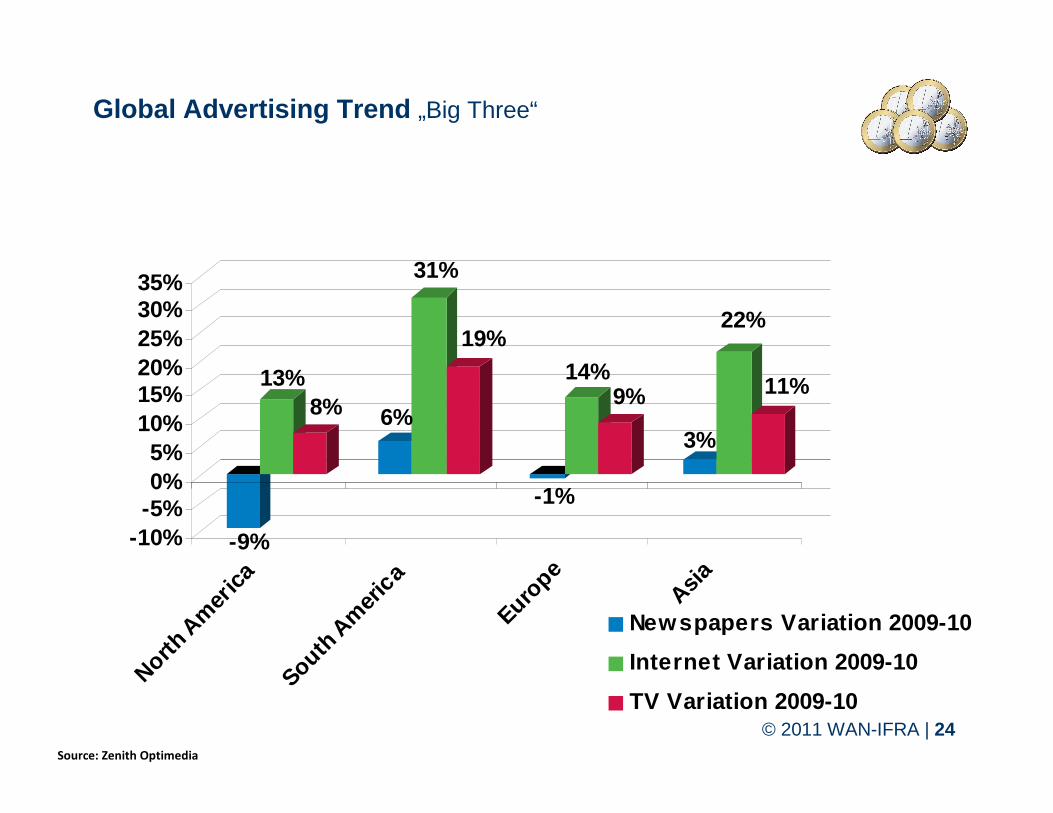

Global Advertising Trend „Big Three“

-9%

13%8% 6%

31%

19%

-1%

14%9%

3%

22%

11%

-10%-5%0%5%

10%15%20%25%30%35%

North A

mer

i ca

South

Am

eri c

a

Europ

e

Asia

Newspapers Variation 2009-10

Internet Variation 2009-10

TV Variation 2009-10

Source: Zenith Optimedia

© 2011 WAN-IFRA | 25

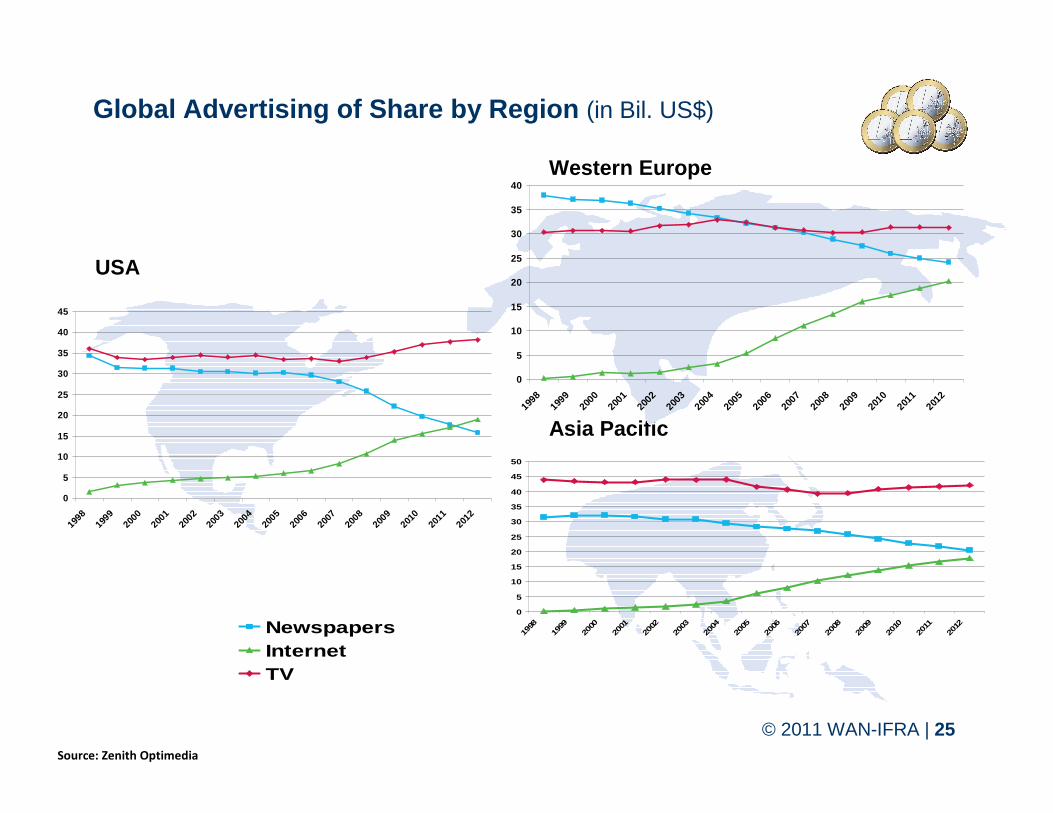

Global Advertising of Share by Region (in Bil. US$)

USA

Asia Pacific

Western Europe

Source: Zenith Optimedia

0

5

10

15

20

25

30

35

40

45

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0

5

10

15

20

25

30

35

40

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0

5

10

15

20

25

30

35

40

45

50

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012Newspapers

InternetTV

© 2011 WAN-IFRA | 26

NEWSPAPER REVENUEIs it content paid, advertising paid or digital revenue?

© 2011 WAN-IFRA | 27

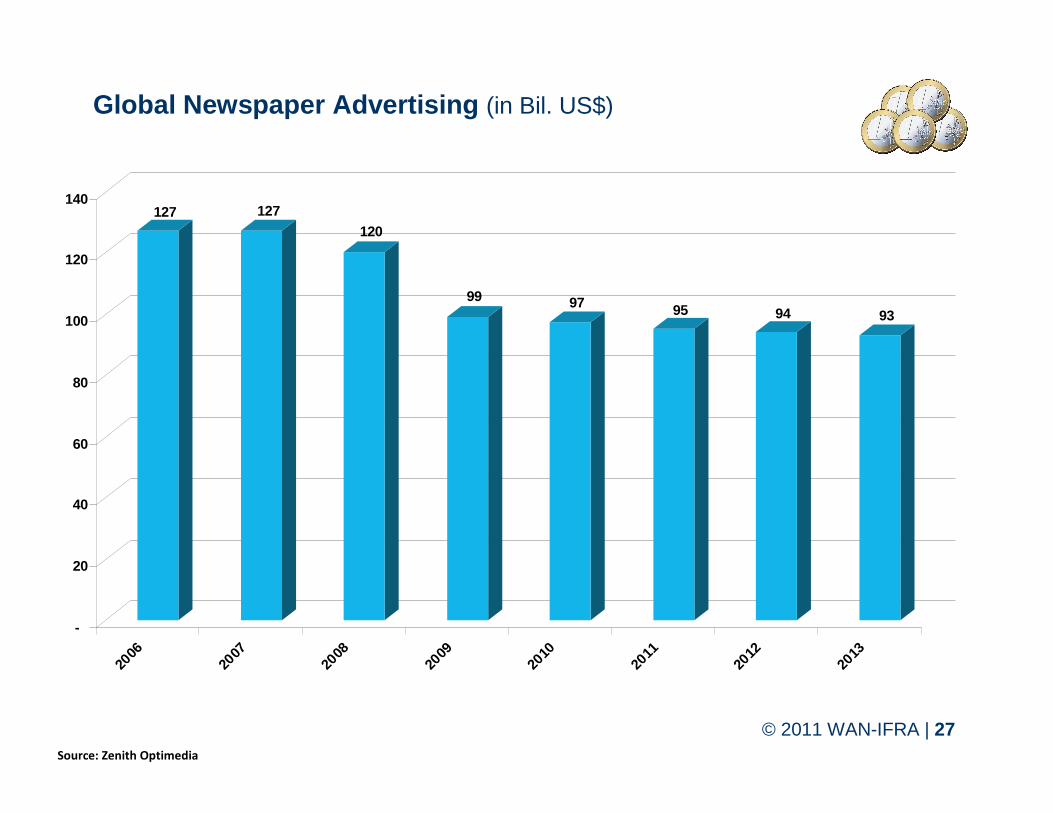

Global Newspaper Advertising (in Bil. US$)

Source: Zenith Optimedia

127 127120

99 97 95 94 93

-

20

40

60

80

100

120

140

2006

2007

2008

2009

2010

2011

2012

2013

© 2011 WAN-IFRA | 28

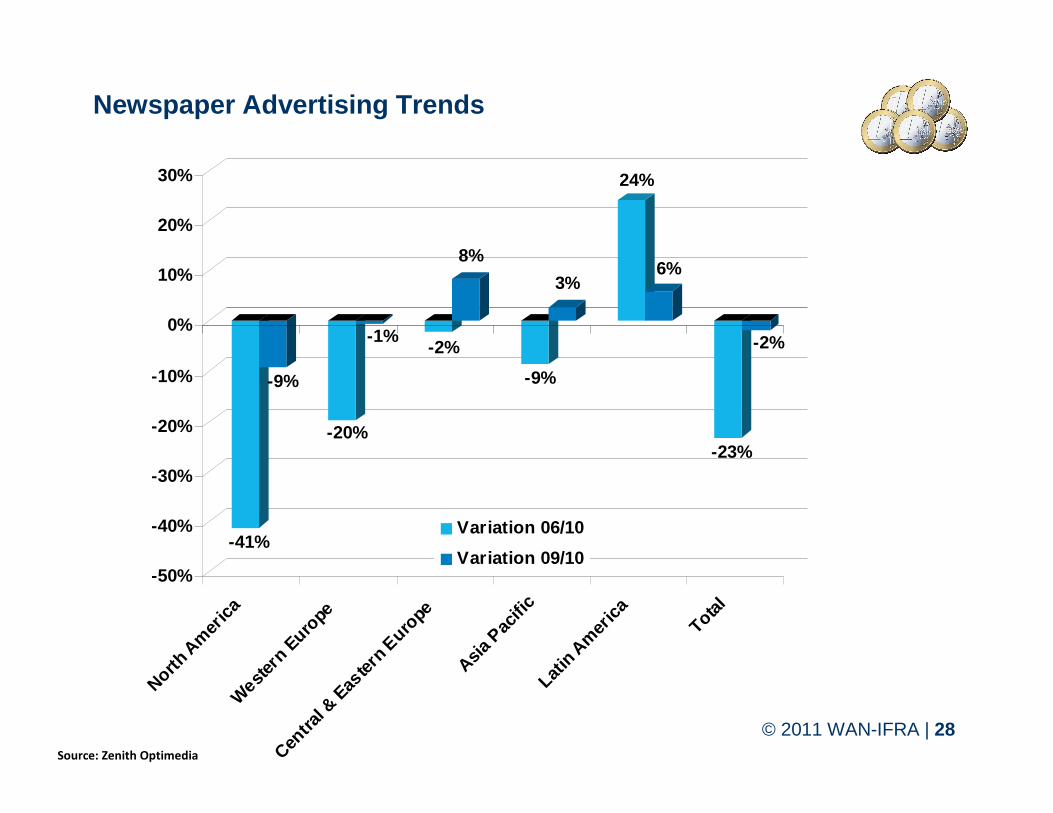

Newspaper Advertising Trends

Source: Zenith Optimedia

-41%

-9%

-20%

-1%-2%

8%

-9%

3%

24%

6%

-23%

-2%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

North

Am

erica

Weste

rn E

urop

e

Centra

l & E

aster

n Eu

rope

Asia Pac

ific

Latin

Amer

ica

Total

Variation 06/10

Variation 09/10

© 2011 WAN-IFRA | 29

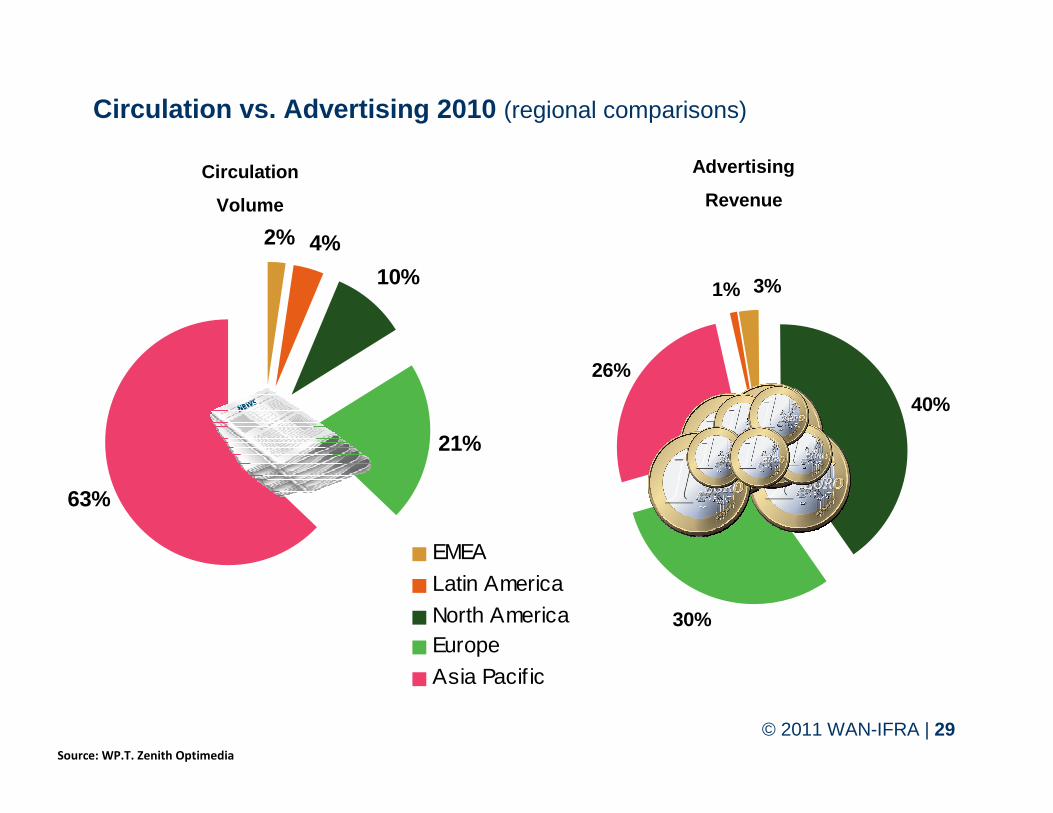

40%

30%

26%

1% 3%

2% 4%

10%

21%

63%

EMEA

Latin America

North AmericaEurope

Asia Pacif ic

Circulation

Volume

Advertising

Revenue

Circulation vs. Advertising 2010 (regional comparisons)

Source: WP.T. Zenith Optimedia

© 2011 WAN-IFRA | 30

Global Newspaper Revenue by Source US $(million)

Source PwC.

© 2011 WAN-IFRA | 31

INTERNET VERSUS MOBILEWill tablets be our saviour?

© 2011 WAN-IFRA | 32

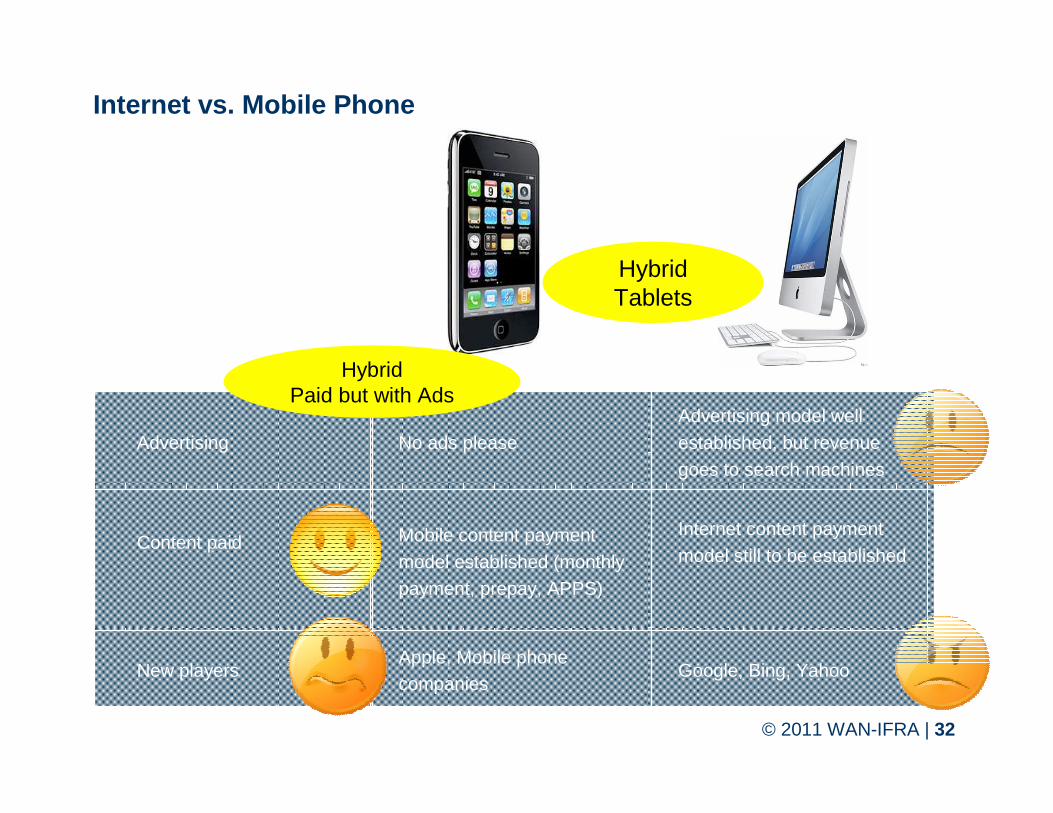

Advertising No ads please Advertising model well established, but revenue goes to search machines

Content paid Mobile content payment model established (monthly payment, prepay, APPS)

Internet content payment model still to be established

New playersApple, Mobile phone companies

Google, Bing, Yahoo

HybridPaid but with Ads

HybridTablets

Internet vs. Mobile Phone

© 2011 WAN-IFRA | 33

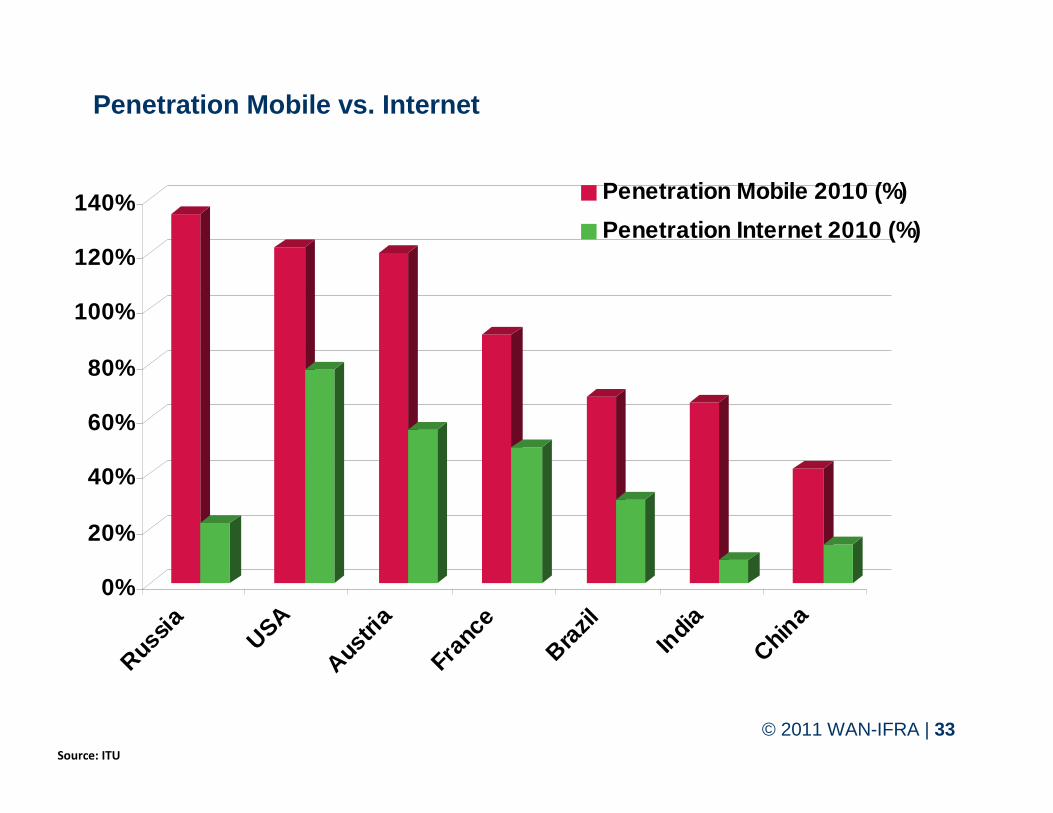

Penetration Mobile vs. Internet

0%

20%

40%

60%

80%

100%

120%

140%

Russia USA

Austria

France

Brazil

India

China

Penetration Mobile 2010 (%)

Penetration Internet 2010 (%)

Source: ITU

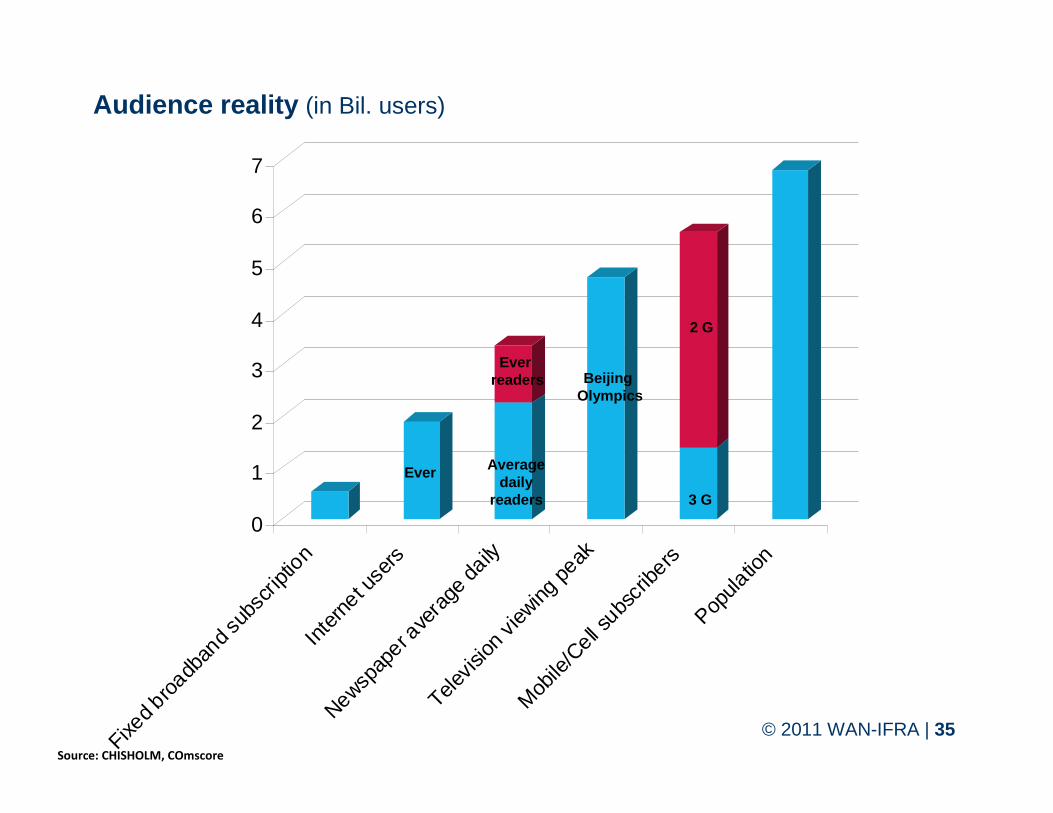

© 2011 WAN-IFRA | 34Source: CHISHOLM, COmscore

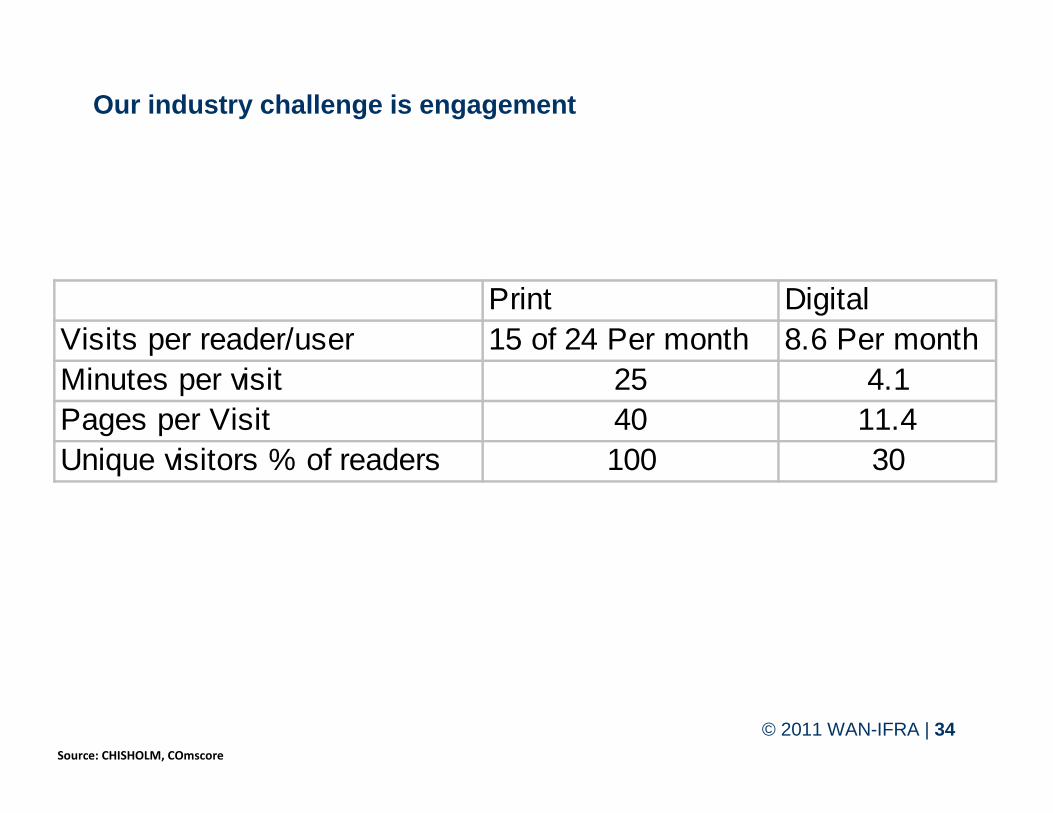

Print DigitalVisits per reader/user 15 of 24 Per month 8.6 Per monthMinutes per visit 25 4.1Pages per Visit 40 11.4Unique visitors % of readers 100 30

Our industry challenge is engagement

© 2011 WAN-IFRA | 35

0

1

2

3

4

5

6

7

Fixed b

roadb

and s

ubsc

riptio

nIn

tern

et use

rs

Newspap

er ave

rage

daily

Televis

ion vi

ewing

peak

Mob

ile/C

ell subs

cribe

rsPop

ulatio

n

3 G

Ever readers

Averagedaily

readers

2 G

Beijing Olympics

Ever

Source: CHISHOLM, COmscore

Audience reality (in Bil. users)

© 2011 WAN-IFRA | 36© 2011 WAN-IFRA | 36

Search engines(Google, Bing)

Online news aggregators

(Digg and NetVibes)

Social Media(Twitter, Facebook)

Online news publishers

(publishing-report.com)

Mobile news actors:

(news as Mail: nypost.com)

Citizen journalism

(globalvoicesonline.org)

Social Media

© 2011 WAN-IFRA | 37

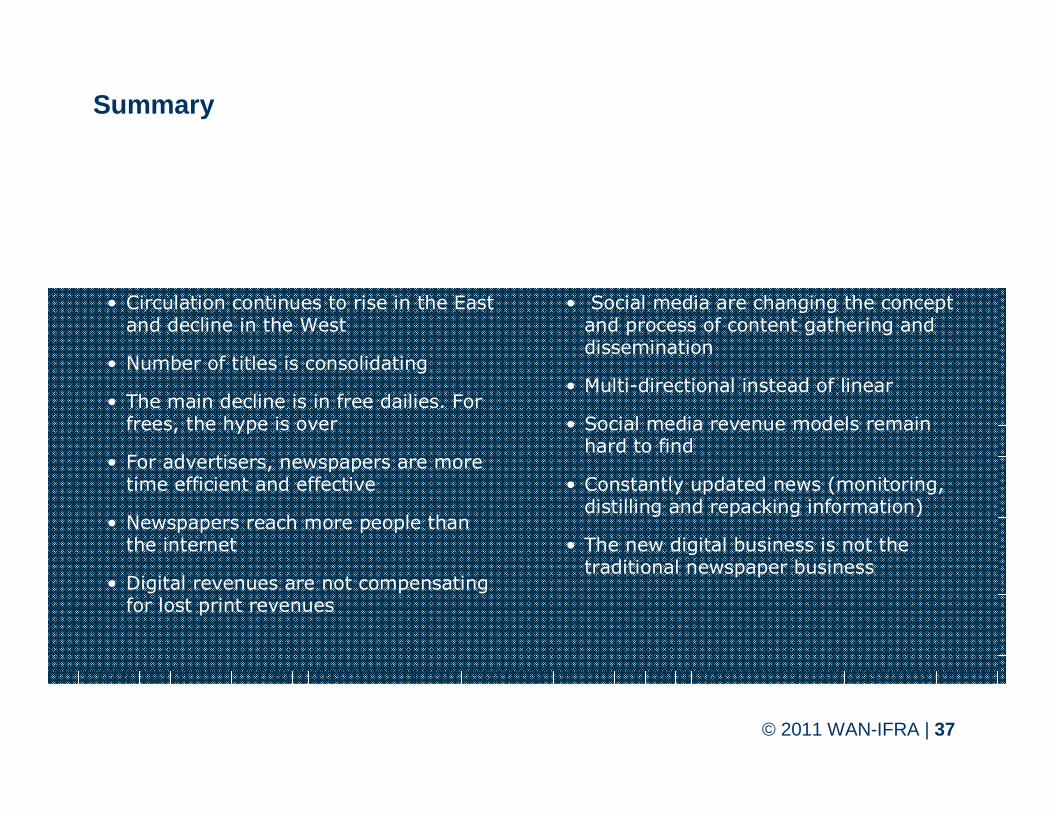

Summary

• Circulation continues to rise in the East and decline in the West

• Number of titles is consolidating

• The main decline is in free dailies. For frees, the hype is over

• For advertisers, newspapers are moretime efficient and effective

• Newspapers reach more people thanthe internet

• Digital revenues are not compensatingfor lost print revenues

• Social media are changing the concept and process of content gathering and dissemination

• Multi-directional instead of linear

• Social media revenue models remain hard to find

• Constantly updated news (monitoring, distilling and repacking information)

• The new digital business is not thetraditional newspaper business

© 2011 WAN-IFRA | 38

THANK YOU FOR YOUR ATTENTION.Christoph RiessCEO [email protected]. +49.6151.733-790

WAN-IFRA DarmstadtWashingtonplatz 164287 Darmstadt, GermanyTel. +49.6151.733-6

WAN-IFRA Paris96 bis rue Beaubourg75003 Paris, FranceTel. +33.147.4285-00

![arXiv:0812.2846v2 [astro-ph] 31 Aug 2009 · Perlmutter et al. 1999; Tonry et al. 2003; Riess et al. 2005; Astier et al. 2005; Riess et al. 2007; Wood-Vasey et al. 2007; Kowalski 2008).](https://static.fdocuments.us/doc/165x107/604f5b58c4862c50ab422156/arxiv08122846v2-astro-ph-31-aug-2009-perlmutter-et-al-1999-tonry-et-al-2003.jpg)