World Bank Documentdocuments.worldbank.org/curated/en/798841468915049911/pdf/multi... · PPAR...

64

Dooment of The World Bank FOR OFFICIAL USE ONLY Report No. 10829 PROJECT PERFORMANCE AUDIT REPORT REPUBLIC OF INDONESIA COAL MINING AND TRANSPORTATION ENGINEERING PROJECT (LOAN S-9-IND) BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATION PROJECT (LOAN 2079-IND) COAL EXPLORATION ENGINEERING PROJECT (LOAN 2153-IND) JUNE 30, 1992 FIL COP' .10829 I,D TYPE:( Atj,,,: KPUPRIVEZ, !A. Ext J17 09 Room Operations Evaluation Department This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/798841468915049911/pdf/multi... · PPAR...

Dooment of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 10829

PROJECT PERFORMANCE AUDIT REPORT

REPUBLIC OF INDONESIA

COAL MINING AND TRANSPORTATION ENGINEERINGPROJECT (LOAN S-9-IND)

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATIONPROJECT (LOAN 2079-IND)

COAL EXPLORATION ENGINEERING PROJECT(LOAN 2153-IND)

JUNE 30, 1992

FIL COP'

.10829 I,D TYPE:(

Atj,,,: KPUPRIVEZ, !A.Ext J17 0 9 Room

Operations Evaluation Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

GLOSSARY OF ABBREVIATIONS

bcm Bank cubic meters

BWE Bucketwheel Excavator

CIDA Canadian International Development Agency

DGM Directorate General of Mines

EDC Export Development Corporation

ESS Eksplotasi Sumatra Selatan (South Sumatra Railway)

GOI Government of IndonesiaIBRD International Bank for Reconstruction and Development

KfW Kreditanstalt fUr Wiederaufbau

KEPPRES Steering Committee

MAP Maximum Austerity Program

MME Ministry of Mines and EnergyMMT Mine Management Team

mtpy Million tons per year

MW MegaWattsNAL Non-Air Laya mines

OED Office Evaluation Department

PCR Project Completion Report

PN Perusahaan Negara (National Company)

PNB PN Batubara (National Coal Company)

PK5BA Coordinating Group for Phase I project (Replaced by POKKORLAK)

PLN State Electricity Authority

PJKA Perusahaan Jawatan Kereta Api (Indonesian State Railway)PMG Project Management Group

POKKORLAK Government Coordinating Group

PPAR Project Performance Appraisal Report

PSC Project Services Contractor

PT Persero (A limited Government Company)

PTBA PT Tambang Batubara Bukit Asam (State Coal Mining Company)

PT PANN PT Pengembangan Armada Niaga Nasional (National Fleet Development

Corporation)

TAG Technical Advisor to GOI

TOR Terms of Reference

tpm Tons per month

FISCAL YEAR

January 1 to December 31

THE WORLD BANK 173R OMCIL USE ONLYWashington, D.C. 20433

U.S.A.

:e of Director-Genealeratims Evauatim

June 30, 1992

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Performance Audit Report on INDONESIACoal Mining and Transaction Engineering Project (Loan S-9-IND);Bukit Asam Coal Mining Development and Transportation Project (Loan2079-IND): and Coal Exploration Engineering Project (Loan 2153-IND)

Attached, for information, is a copy of a report entitled "ProjectPerformance Audit Report on INDONESIA - Coal Mining and Transaction EngineeringProject (Loan S-9-IND); Bukit Asam Coal Mining Development and TransportationIroject (Loan 2079-IND); and Coal Exploration Engineering ProjectLoan 2153-IND) prepared by the Operations Evaluation Department.

i.achment

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

FOR OFFICIAL USE ONLY

PROJECT PERFORMANCE AUDIT REPORT

REPUBLIC OF INDONESIA

COAL MINING AND TRANSPORTATION ENGINEERINGPROJECT (LOAN S-9-IND)

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATIONPROJECT (LOAN 2079--IND)

COAL EXPLORATION ENGINEERING PROJECTLOAN 2153-IND)

TABLE OF CONTENTS Page No.

Preface........................................................ iBasic Data Sheets.............................................. iii

Evaluation Summary................... . ........ ix

I. BACKGROUND.............................................. 1

II. BUKIT ASAM COAL MINING AND TRANSPORTATION PROJECT....... 3

A. Project Objectives................................. 3B. Role of the Bank................................... 3C. Components of the Project.......................... 4D. Project Preparation and Appraisal.................. 5E. Project Design and Organization.................... 6

Data Acquisition and Mining System Design.... 6

Selection of the Mining System............... 7Economic Analysis............................ 10

Organizational Arrangements.................. 11Schedule Constraints............. ...... 13

F. Risk Assessment and Management............ 14

G. Project Implementation..................... 15

H. The Choice of Technology................... 16

E. Grounds Investigation.............................. 17

J. Project Management................................. 18

K. Project Coord4 nation............................... 20

L. Coal Shipping...................................... 21

M. Environmental Control and Monitoring............... 21

N. Project Costs...................... ......... ........ 22

0. Project Results................ .... .............. 23

P. Project Sustainability............................. 24Q. Performance.... . ............................ 27

R. Consultant Performance. .................... 28S. Borrower Performance........ ........ ......... 29

T. Maturity, Grace Period and Exchange Risk........... 30

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed withcut World Bank authorization.

TABLE OF CONTENTS (cont.)Page No.

III. COAL EXPLORATION ENGINEERING PROJECT 31

A. Project Objectives.............. ............ 31B. Project Design and Organization............... 32C. Project Implementation................................ 32

D. Project Costs................................. 32

E. Project Results.............................. 33

F. Performance.............. ... . ................. 33

G. Maturity, Grace Period and Exchange Risk...... 34

IV. FINDINGS AND LESSONS................................... 35

ANNEX I -- FINANCIAL STATUS OF PTBA ANDMINE OPERATIONS. 37

TABLE I - INCOME STATEMENT FOR AIR LAYA MINETABLE 2 - INCOME STATEMENT FOR NON-AIR LAYA MINEfABLE 3 - PRODUCTION COST AT BUKIT ASAMTABLE 4 - SOURCE OF REVENUE FOR PTBATABLE 5 - SOURCE AND STATUS OF BORROWINGSTABLE 6 - BALANCE SHEETS FOR BUKIT ASaM OPERATIONS

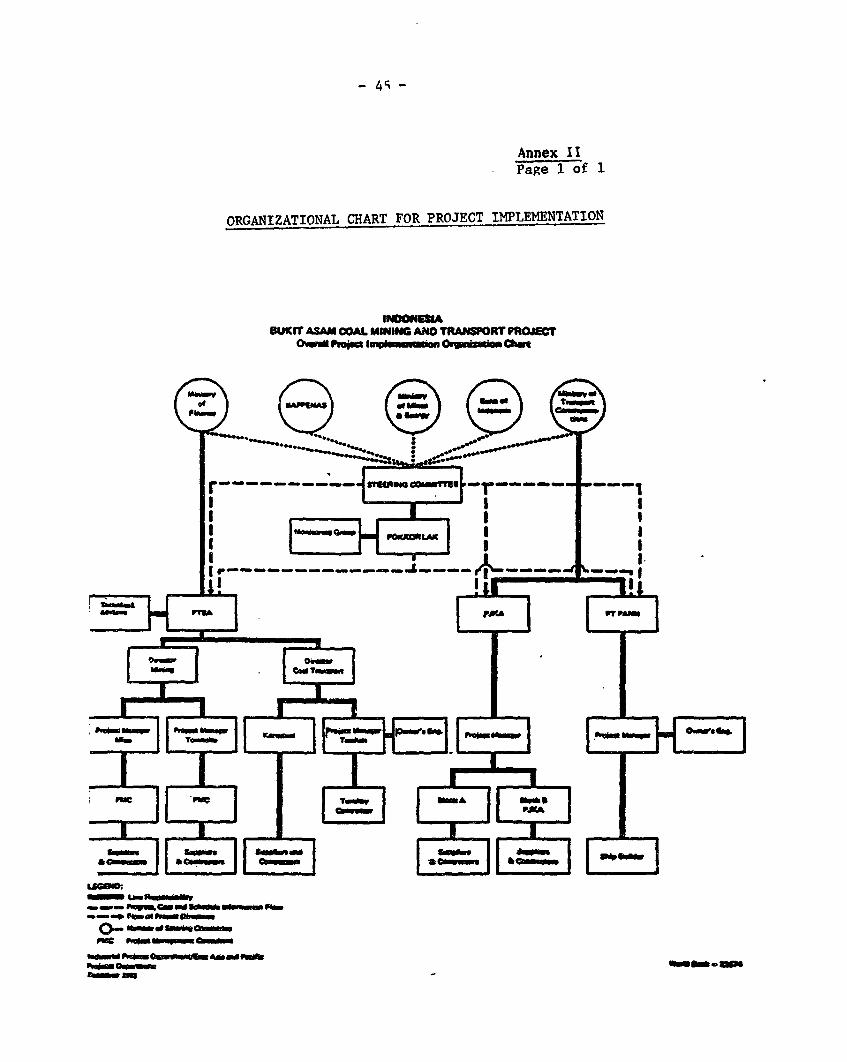

ANNEX II -- ORGANIZATIONAL CHART FOR PROJECT IMPLEMENTATION 45

ATTACHMENT

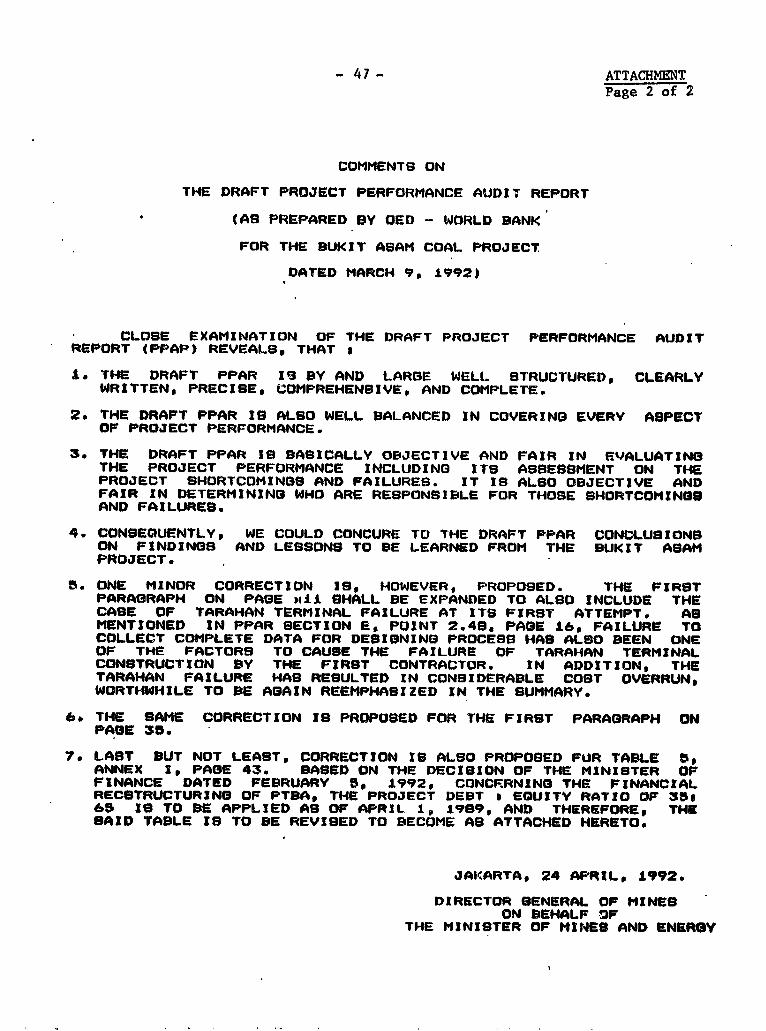

Comments from the Borrower .................... .... . 46

PROJECT PERFORMANCE AUDIT REPORT

REPUBLIC OF INDONESIA

COAL MINING AND TRANSPORTATION ENGINEERINGPROJECT (LOAN S-9-IND)

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATIONPROJECT (LOAN 2079-IND)

COAL EXPLORATION ENGINEERING PROJECT(LOAN 2153-IND)

PREFACE

1. This is a Project Performance Audit Report (PPAR) for the Bukit Asam Coal

Mining Development and Transportation Project and the Coal Exploration

Engineering Project. The International Bank for Recunstruction and Development(IBRD) granted three loans. Loans S-9-IND arid 2079-IND in the amounts of US$10million and US$185 million were approved on May 9, 1978 and January 7, 1982,

respectively, for the Bukit Asam Coal mining Development and TransportationProject. The engineering loan (S-9-1iD) was refinanced under the investmentproject loan, Loan (2079-IND). The latter loan was closed on September 30, 1989,two years behind schedule and after two extensions. The last disbursement for

the Bukit Asam project was on April 4, 1990, and a total of US$6.25 million wascancelled. Co-financing was provided by the Export Development Corporation(EDC) /the Canadian International Development Agency (CIDA) (US$133 million), theKreditanstalt fUr Wiederaufbau (KfW) (US$48 million), the Netherlands (US$2.5million), and through export credits (US$206 million). IBRD Loan 2153-IND in theamount of US$25 million was approved on June 14, 1982 for the Coal Exploration

Engineering Project. It took eight months to make the loan effective. The loanwas closed on June 30, 1988, one year behind the originally planned date, after

a total disbursement of US$19.5 million; US$5.0 million and US$0.55 million were

canceled on January 1, 1988, and September 21, 1988, respectively.

2. The PPAR was prepared by the Operations Evaluation Department (OED). It

is based on the Project Completion Reports (PCRs) for the projects, the Staff

Appraisal Report (SAR), a study of the project files, and discussion with Bank

staff. An OED mission visited Indonesia in July 1991 and discussed projectissues with Team KEPPRES 35/87, PT Tambang Batubara Bukit Asam, and officials in

other agencies within the Government of Indonesia (GOI); travelled to the Bukit

Asam mine; and gratefully acknowledges the assistance and hospitality itreceived.

Project Completion Reports: - Coal Mining and Transportation Engineering

Project (Loan S-9-IND) and Bukit Asam Coal Mining Development and

Transportation Project (Loan 2079-IND)(June 25, 1990); - Coal Exploration

Engineering Project (Loan 2153-IND) (June 23, 1989).

3. According to standard procedures, OED sent copies of the draft PPAR to theBorrower for comments. Comments received from the Department of Mines and Energyhave been taken into account in the PPAR and are attached as an Attachment to theReport.

- i -

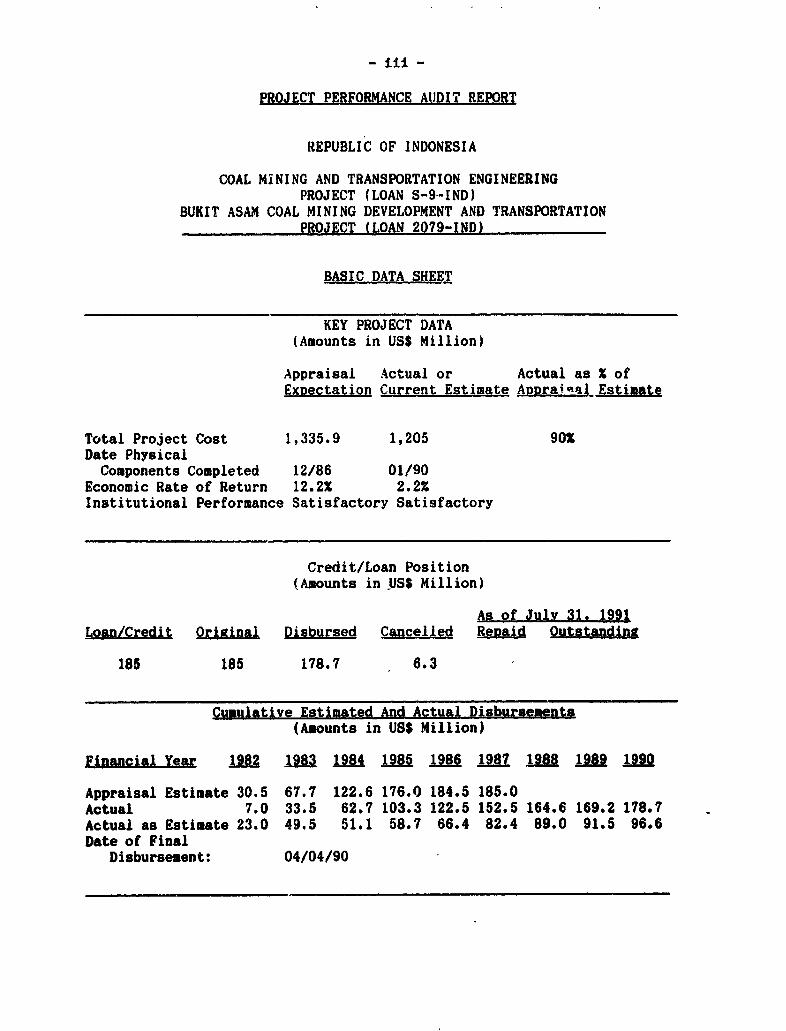

PROJECT PERFORMANCE AUDIT REPORT

REPUBLIC OF INDONESIA

COAL MINING AND TRANSPORTATION ENGINEERINGPROJECT (LOAN S-9--IND)

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATIONPROJECT (LOAN 2079-IND)

BASIC DATA SHEEI

KEY PROJECT DATA(Amounts in US$ Million)

Appraisal Actual or Actual as % ofExpectation Current Estimate Aporaieal Estimate

Total Project Cost 1,335.9 1,205 90%Date Physical

Components Completed 12/86 01/90Economic Rate of Return 12.2% 2.2%Institutional Performance Satisfactory Satisfactory

Credit/Loan Position(Amounts in US$ Million)

As of July 31, 1991Lan/Credit Original Disbursed Cancelled Reiaid Outstandine

185 185 178.7 6.3

Cumulative Estimated And Actual Disbursements(Amounts in US$ Million)

Einancial Year I M18 128 198 198 1987 128 12 12

Appraisal Estimate 30.5 67.7 122.6 176.0 184.5 185.0Actual 7.0 33.5 62.7 103.3 122.5 152.5 164.6 169.2 178.7Actual as Estimate 23.0 49.5 51.1 58.7 66.4 82.4 89.0 91.5 96.6Date of Final

Disbursement: 04/04/90

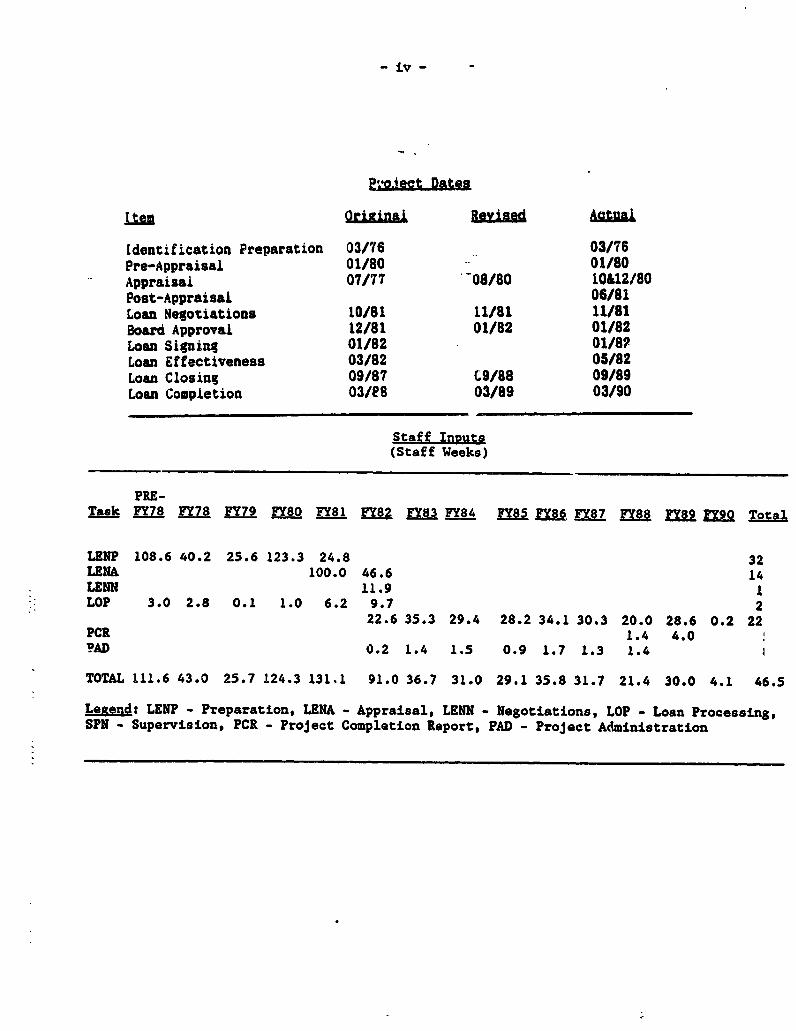

- iv - -

118Original. BRizid Ac%11Ai

Identification Preparation 03/76 03/76Pre-Appraisai 01/80 01/80Appraisal 07/77 -08/80 10412/80Post-Appraisal 06/81Loan Negotiations 10/81 11/81 11/81Board Approval 12/81 01/82 01/82Loan Signing 01/82 01/8?Loan Effectiveness 03/82 05/82Loan Closing 09/87 09/88 09/89Loan Completion 03/ S 03/89 03/90

Staff Input.(Staff Weeks)

PRE-Tsk F78 FY1 FY 9 FY80 FY81 FY82 Y FY84 I8 Zo k Z UU y882 FY89 Totgl

LENP 108.6 40.2 25.6 123.3 24.8 32LENA 100.0 46.6 14LENN 11.9 1LOP 3.0 2.8 0.1 1.0 6.2 9.7 2

22.6 35.3 29.4 28.2 34.1 30.3 20.0 28.6 0.2 22PCR 1.4 4.0PAD 0.2 1.4 1.5 0.9 1.7 1.3 1.4 1

TOTAL 111.6 43.0 25.7 124.3 131.1 91.0 36.7 31.0 29.1 35.8 31.7 21.4 30.0 4.1 46.5

Leaend: LENP - Preparation, LENA - Appraisal, LENN - Negotiations, LOP - Loan Processing,SPN - Supervision, PCR - Project Completion Report, PAD - Project Administration

-v -

Project Dates

item Original Revised Actual

Identification Preparation 07/81 07/81Appraisal 09/81 02/82 02/82Loan Negotiations 04/82 04/82Board Approval 05/82 05/82Loan Signing 06/83 06/82Loan Effectiveness 09/82 03/83 03/83Loar. Closing 06/87 06/88 06/88Loan Completion 12/87 12/88 09/88

--------------------- m------------------------------------------------Staff Inputs(Staff Weeks)

FY82 FY83 FY84 FY85 FY86 FY87 FY88 FY89 TOTAL

Preparation 4.2 4.2Appraisal 23.1 23.1Negotiation 1.6 1.6Loan Processing 3.0 3.0Supervision 1.2 24.2 9.0 4.5 15.0 12.9 13.2 6.8 86.8

TOTAL 33.1 24.2 9.0 4.5 15.0 12.9 13.2 6.8118.7

----------------------------------------------------------------------MISSION DATA

Stage of Month/ No. of Days in Types ofProlect Cycle Year Persons Field Problems 2

Identification 06/81 1 10Pre-Appraisal 10/81 2 11Negotiation 04/82 3 10Supervisicn Mission 1 08/82 2 14 E,I,S,P

2 12/82 1 12 E,I,S,P3 03/83 1 9 I,S,P4 06/83 3 14 I,P5 10/83 2 18 I,S,P,F6 02/84 3 10 F7 10/84 3 15 F8 07/85 2 17 NONE9 01/86 2 16 F,PM,P

10 09/86 3 28 F11 03/87 1 13 I,PM12 06/87 2 16 NONE

2 E - Loan Effectiveness; I - Institutional; S - Implementation ScheduleP - Procurment; F - Financial (Local Budget); PM - Project Management

- vi -

OTHER PROJECT DATA

Borrower: Government of Indonesia

Executing Agencies: PT Tambang Batubara Bukit Asam (PTBA);Perusahaan Jawatan Kereta Api (PJKA);PT Pengembangan Armada Niaga Nasional (PT PANN)

Follow-On Project: Coal Exploration Engineering ProjectLoan No: 2153-INDAmount: US$25 millionBoard Date: 05/20/82

- vii -

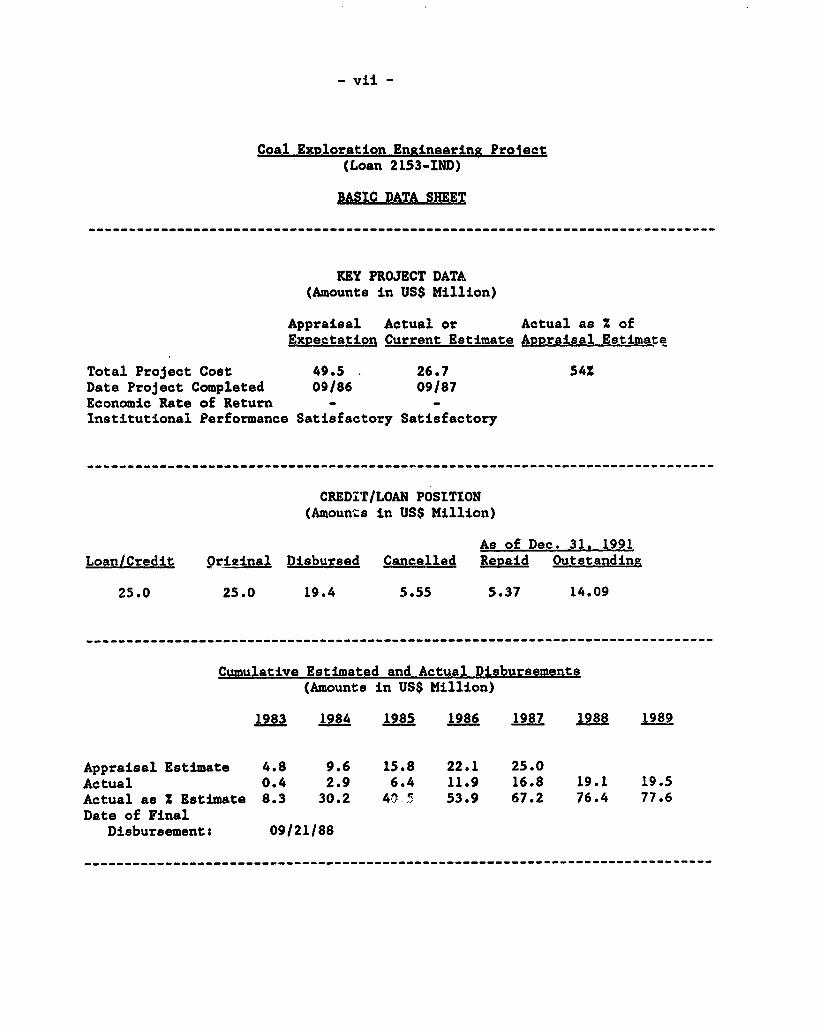

Coal Exploration Engineering Prolect(Loan 2153-IND)

BASIC DATA SHEET

KEY PROJECT DATA(Amounts in US$ Million)

Appraisal Actual or Actual as % ofExpectation Current Estimate Appraisal Estimatq

Total Project Cost 49.5 26.7 54%Date Project Completed 09/86 09/87Economic Rate of Return - -

Institutional Performance Satisfactory Satisfactory

CREDIT/LOAN POSITION(Amounts in US$ Million)

As of Dec. 31, 1991Loan/Credit 0riginal Disbursed Cancelled Repaid Outstanding

25.0 25.0 19.4 5.55 5.37 14.09

------------------------------------------------------------------------

Cumulative Estimated and Actual Disbursements(Amounts in US$ Million)

1983 1984 1985 1986 1987 1988 1989

Appraisal Estimate 4.8 9.6 15.8 22.1 25.0Actual 0.4 2.9 6.4 11.9 16.8 19.1 19.5Actual as % Estimate 8.3 30.2 41 5 53.9 67.2 76.4 77.6Date of Final

Disbursements 09/21/88

------------------------------------------------------------------------

- viii -

Prolect Dates

Item Original Revised Actual

Identification Preparation 07/81 07/81Appraisal 09/81 02/82 02/82Loan Negotiations 04/82 04/82Board Approval 05/82 05/82Loan Signing 06/83 06/82Loan Effectiveness 09/82 03/83 03/83Loan Closing 06/87 06/88 06/88Loan Completion 12/87 12/88 09/88

Staff Inputs(Staff Weeks)

FY82 FY83 FY84 FY85 FY86 FY87 FY88 FY89 TOTAL

Preparation 4.2 4.2Appraisal 23.1 23.1Negotiation 1.6 1.6Loan Processing 3.0 3.0Supervision 1.2 24.2 9.0 4.5 15.0 12.9 13.2 6.8 86.8

TOTAL 33.1 24.2 9.0 4.5 15.0 12.9 13.2 6.8 118.7

MISSION DATA

Stage of Month/ No. of Days in Types ofProject Cycle Year Persons Field Problems 2

Identification 06/81 1 10Pre-Appraisal 10/81 2 11Negotiation 04/82 3 10Supervision Mission:.1 08/82 2 14 E,I,S,P

2 12/82 1 12 E,I,S,P3 03/83 1 9 I,S,P4 06/83 3 14 I,P5 10/83 2 18 I,S,P,F6 02/84 3 10 F7 10/84 3 15 F8 07/85 2 17 NONE9 01/86 2 16 F,PM,P

10 09/86 3 28 F11 03/87 1 13 I,PM12 06/87 2 16 NONE13 02/88 2 23 I14 10/88 1 14 NONE

2 E - Loan Effectiveness; I - Institutional; S - Implementation Schedule

P - Procurment; F - Financial (Local Budget); PM - Project Management

ix

PROJECT PERFORMANCE AUDIT REPORT

REPUBLIC OF INDONESIA

COAL MINING AND TRANSPORTATION ENGINEERINGPROJECT (LOAN S-9-IND)

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATION

PROJECT (LOAN 2079-IND)

COAL EXPLORATION ENGINEERING PROJECT

(LOAN 2153-IND)

EVALUATION SUMMARY

Introduction

1. This report reviews the Bukit and Transportation Project was to

Asam Coal Mining Development and assist the Government of Indonesia

Transportation Project in South (GOI) to move away from a policy

Sumatra (Indonesia) for which Loans which relied heavily on the use of

S-9-IND and 2079-IND were approved in scarce petroleum resources in the

the amounts of US$10 million and domestic sector. In this way,

US$185 million on May 9, 1978 and petroleum exports could be

January 7, 1982, respectively. The maintained, which would then

first of these loans was provided to contribute to Indonesia's development

support an engineering study program needs. Revenue from oil exports,

to assess the feasibility of played a critical role in Indonesia's

developing the Air Laya opencast mine development (although this dependen;y

to supply coal for the Suralaya I and is now reduced). Since most of the

II. The second of these loans was coal reserves in South Sumatra

part of a co-financed loan to develop consist of low quality and non-

the Air Laya mine at Bukit Asam, to tradeable coal, mining it for a

develop and/or upgrade rail and captive utility sector was considered

terminal facilities for moving coal, to be attractive and risk free.

and acquire a self-unloading ship for

transporting coal to Suralaya (Java). 4. The objective for the coal

exploration and feasibility study

2. This report also reviews a program was to inventory promising

parailel coal exploration and coal reserves in South and West

feasibility study program in South Sumatra. The Air Laya mine was

and West Sumatra for which the Bank developed for an inital production of

provided a loan of US$25 million 3 mtpy, which is just adequate to

(Loan 2153-IND) to assess the meet the fuel needs for Suralaya I

potential for development of these and 11 (2 x 400 MW) and other

resources for future power consumers in South Sumatra. It was

production. This loan was approved felt that as more units were

on June 14, 1982. developed in Java (Suralaya III andIV) more coal would be needed for

Proiect Objectives power production. The explorationand feasibility assessment program

3. The key objective of the could thus assist in identifying

Bukit Asam Coal Mining Development promising coal resources which may be

x

viably developed to supply fuel for a Project Implementationgrowing utility sector.

7. Except for the shipcomponent, the Bukit Asam coal mining

Content of the Projects and transportation projectencountered numerous implementation

5. The Bukit Asam coal mining problems and delays. Someand transportation project was an components, especially the serviceambitious undertaking involving facilities for the mine and raildevelopment in three separate sectors, were delayed by a few yearssectors. At Bukit Asam, the project (PPAR, Section G). Coal movement toconsisted of development of a 3 mtpy Suralaya at a rate of 200,000 tonsopencast mine and related per month (tpm) was achieved aboutinvestments, such as a mine facility four years after the target date.to service the equipment and a Even in 1991, the mining componenttownship to provide housing for PTBA has not met the production targetsemployees. The transportation expected according to the design.component consisted of the upgrading The project was plagued by manyof an existing 150 km rail line to implementation problems (PPAR,Kertapati near Palembang and another Section G). Some of these may be400 km line to Tarahan on the Sunda summarized as follows: poorStrait. In addition, the existing performance of local contractors;coal terminal at Kertapati on the inadequate availability of skilledMusi River was to be upgraded and a manpower; weakness of operational andnew terminal for shipping coal to management staff in implementingSuralaya was to be constructed at agencies; inadequate groundTarahan. Both the mine and rail investigations and design leading tocomponents involved significant deficiencies in mine excavationpurchase and installation of system; inadequate assessment of theequipment. The transportation appropriateness of the technology incomponent also involved the design the Bukit Asam context; deficienciesand construction of 9,200 ton DWT in organizational arrangements duringself-unloading coal ship to transport implementaton; cumbersome procurementcoal across the Sunda Strait from procedures; etc.Tarahan to Suralaya.

Results6. The coal exploration activityinvolved a drilling and resource 8. The physical components ofestimation program in several the project are in place more or lesslocations around BukiL Asam in South as designed. However, the mineSumatra and at Ombilin in West excavation system has been operatingSumatra. The feasibility study at only 60% of the design capacityprogram based on this drilling until recently. Approximately fiveprogram involved studies to years after completion, the Air Layainvestigate the feasibility of mine currently produces coal at aboutdeveloping production in the more 2.4 Mtpy, which is 20% below the 3abundant and better characterized mtpy goal. PTBA, the limited companyfields. In addition pre-feasibility set up to own the mines, is unable tostudies were also designed for a few make debt and interest payments basedof the smaller fields. on the 60:40 debt to equity ratio for

the Air Laya mine. Its output is notcompetitive. Mine Development

xi

involved 4-5 times higher investment Current non-Air Laya mines continueper ton of output than mines their superior operating performanceelsewhere (PPAR, Section G). The and new non-Air Laya mines beingprice of coal set close to planned replicate this superiorinternational market prices now is performance level.less than 30 percent of the appraisalestimate. Combined with the Findings and Lessonsdifficulties the mine has beenexperiencing in attaining production 11. The Air Laya mine developmenttargets, the cost of production of project at Bukit Asam has beenAir Laya coal is about twice that of completed with serious shortfall inthe net sale price. GOI plans to the design targets and alsoassume a higher proportion of the substantial shortfall in thedebts incurred by PTBA in developing financial area. The outcome suggeststhe Air Laya mine. GOI will also the following lessons, some of whichprovide certain other concessions to are not new.enhance PTBA's viability (PPAR, AnnexI). Together with the profitable - The appraisal based on highlynon-project coal mine operations overestimated coal revenues(non-Air Laya mines) developed by the should have been supplementedPTBA after the mid eighties and by analysis based on otheroperated through contract mining, criteria. In retrospect,PTBA is likely to operate profitably appraisal estimates of revenueafter the restructuring is completed. from coal sales for the Bukit

Asam project have proven to be9. The parallel coal exploration unrealistic. A review of thisprogram and feasibility study program project suggests that anotherto assess coal resources in South and relevant basis for appraisalWest Sumatra achieved all its was the cost of developing thisobjectives. With the successful production capacity vis-a-visconclusion of this exploration and cost of such developmentsfeasibility study program, GOI is in elsewhere.a better position to assess anddevelop coal resources in Sumatra. - Consulting services for

feasibility design andProiect Sustainability construction surpervision were

provided by a joint venture of10. PTBA is soon to be firms and subcontractors withrestructured with an equity to debt different areas of expertise.ratio of 65:35 for the Air Laya mine. In such cases, closeTogether with its very profitable supervision is necessary tonon-Air Laya mines, it is likely to eliminate any risk of bias inhave sustainable operations with the recommendations.possibilities for expanded productionin future from new mines. There are - Implementation of such largetwo other conditions for sustainable and complex projects should beoperations in future: (1) The Air preceeded by exhaustive projectLays mine continues maintaining or preparation. Data for designimproving its recent performance of the systems should belevel. Implicit for this is the acquired before the designs are

continuation of the training and man completed to avoid the se-

over development programs. (2) lection of sub-optimal oper-

xii

ating systems. In the case ofmining equipment, exhaustiveground investigations shouldprecede the selection/design ofmining equipment and systems.The lack of ground and drillingdata for the Tarahan terminalalso led to a costlydesign/construction failure atthe coal shipping terminal bythe first construction contrac-tor.

The local context should beanalyzed appropriately forevaluating the appropriatenessof a technology or design. Therisks associated with each ofthe local variables need to beassessed critically to de-termine relevance of the sys-tems to be selected. For theBukit Asam project, theappraisal failed to factor intothe analysis the implicationsof heavy rains, the inadequacyof the manpower base, anddifficulty of procuringservicing equipment.

The importance of developing anadequate organizational struc-ture for project implementationcannot be overemphasized. Theorganizational structures re-quired should provide for ef-fective action-oriented manage-ment and control. Simple, fairand expeditious procurementprocedures are also keyrequirements for successfulimplementation.

PROJECT PERFORMANCE AUDIT REPORT

REPUBLIC OF INDONESIA

COAL MINING AND TRANSPORTATION ENGINEERINGPROJECT (LOAN S-9-IND)

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATIONPROJECT (LOAN 2079-IND)

COAL EXPLORATION ENGINEERING PROJECT(LOAN 2153-IND)

I. BACKGROUND

1.1 Revenues from petroleum export had been an important part of In-donesia's development strategy all throughout the sixties and seventies.However, domestic oil consumption grew rapidly in Indonesia in the 1970's. Evenwith the benefit of several drilling programs in collaboration with foreignexploration companies, oil production was expected to increase only to about1,800,000 from 1,600,000 barrels/day toward the late seventies. However, withincreasing domestic consumption, the net exportable oil surplus had been expectedto decline all throughout the eighties. Agencies in the Government of Indonesia(GOI) concerned with mining and oil exploration were increasingly aware in theseventies that Indonesia's proven oil reserves had not been growing. Theseestimates on oil consumption, production, and reserves were important considera-tions behind the decision during the early and mid-seventies in adopting policiesfor the development of alternative indigenous energy sources, such as naturalgas, hydropower, geothermal and coal for use in the domestic sector.

1.2 Coal has been mined in Indonesia for nearly a century, first in WestSumatra (Ombilin) and since 1920 in South Sumatra at Bukit Asam. Coal productionin Sumatra peaked at 2 mtpy in 1940 and reached a low point of 150,000 tpy in1973. Approximately half of the total coal mined in 1973 was produced in BukitAsam. Since the price was controlled to a level below that of subsidized fueloil, heavy subsidies were required to keep the state coal mining company inoperation. Because of the low price of subsidized fuel oil in relation tointernational prices, it was not possible to promote higher usage of coal withoutlarge outlays of capital from the Governement and also significant subsidies tothe mining company.

1.3 In 1973-74, the Department of Mines developed a rehabilitation programfor Bukit Asam aimed at increasing steam coal output for the South Sumatra marketestimated then at 300,000 tpy. Apart from the option of a mine-mouth power plantand possible reconversion of a small oil-fired steam plant in Palembang, powergeneration based on coal was not then considered feasible. The main reason wasthat the state electricity company, Perusahaan Umum Listrik (PLN), was suppliedwith oil by GOI at a highly subsidized rate of US$56 equivalent per ton of coal.

1.4 In 1976, a Presidential Instruction was signed requiring the maximumpossible usage of coal for electric power generation and for industrial use.Following this instruction, GOI requested the Bank to consider financing a600,000 - 900,000 tpy expansion and rehabilitation of the Bukit Asam coal mine.A review by the Bank of the prefeasibility study prepared earlier by an

- 2 -

international oil company indicated, however, that such limited output would be

far below the economic mine size based on the estimated reserves.

1.5 An earlier Bank financed Java System Development Study identified the

Suralaya Power Station Scheme in northwest Java on the Sunda Strait (PCR Part I,

para 2.2) for development to generate power for Java. Consistent with thePresidential Instruction of 1976, the initial two units, Suralaya I and II,

planned for construction with Bank assistance were to be designed with dual-

firing capability for burning oil and/or coal. The development of the Air Laya

mine at Bukit Asam was hence planned to provide coal to a captive utilityconsumer. Provided that the mine, related coal shipping terminal facilities,

rail transportation, and sea transportation options could be developed in time

and optimally, the Bank and GOI anticipated significant economic and other

advantages in the development of the Air Laya mine at Bukit Asam.

1.6 The Bank completed the appraisal of the VIII and IX power projects(Suralaya I and II) as the engineering study for the Air Laya mine was initiated

ir. early 1979. The two units at Suralaya (2 x 400 MW) were planned for com-

pletion and testing in late 1984 and mid-1985, respectively. The Air Laya mine

at Bukit Asam was planned initially to reach full production of 3 mtpy by 1987

of which 2.4 mtpy were to be shipped across the Sunda Strait to provide 100percent of the fuel for Suralaya I and II. The rest of the production from Air

Laya was intended for use at the small mine-mouth units required to supply the

mine and the community with electricity and also to supply coal to industrial

customers in South Sumatra through the Kertapati terminal on the Musi River near

Palembang.

1.7 The Suralaya Power Plant was later envisaged for expansion to aninstalled capacity of 3100 MW in the nineties. Bukit Asam production had been

expected to be doubled during a Phase II expansion in the nineties to meet the

fuel needs of Suralaya III and IV planned for completion about 3 years after the

first two units. Suralaya III and IV were also expected to have generation

capacity similar to units I and II but based exclusively on coal. Thus, the

production of about 6 mpty at Bukit Asam would have a captive utility customer,

which eliminates the marketing risk. This was an important consideration since

Bukit Asam coal is generally of low quality with no real international market.

1.8 Following completion of the appraisal of the Bukit Asam mine

development and construction project, GOI approached the Bank for assistance in

instituting a coal exploration program and a prefeasibility/feasibility

assessment program for selected locations in West and South Sumatra. The Bank,

being aware of the potential for appreciable coal resources probable in these

areas and also of the need for access to more coal resources to provide fuel for

generating more power, agreed to assist 001. The additional power units to be

constructed af:er the first two units at Suralaya were anticipated to requirecoal fuel supplies beyond those which could be produced from the Air Laya mine

at Bukit Asam.

-3-

II. BUKIT ASAM COAL MINING AND TRANSPORTATION PROJECT

(LOAN S-9 AND LOAN 2079-IND)

A. Proiect Obiectives

2.1 For the purpose of this Audit, the initial engineering loan (S-9-IND)and the follow-up investment project loan (2079-IND) are discussed together inthe Section III of this report. As described in the PCR, Part I, section 3, thekey objective of the project was to assist GOI in moving away from a mono-energypolicy to one of a multi-energy use in the domestic sect r. This could be mosteasily accomplished in the power generation and industry iectors which then hadheavy reliance on oil. The development of Bukit Asam coal mines was the firstsignificant step in the exploitation of Indonesia's coal resources which, thoughestimated to be ample, were, yet, then regarded as inadequately inventoried.Moreover, a large fraction of the coal resource base in South Sumatra, which wassomewhat better characterized, consists of the low quality lignitic variety whichcannot be exported. In substituting this resource for oil in power generationand industrial use, it was thought that Indonesia's balance of payment could beimproved by exporting its oil production.

2.2 In addition to providing coal fuel to planned power units at Suralaya,the Air Laya mine development and construction program at Bukit Asam had otherimportant benefits to Indonesia:

- The project was seen as an important vehicle and the first stepfor developing the country's coal resource base by providingopportunities for technical and managerial training, and for as-sisting in further exploration studies with a view to carry outmore coal development projects a few years downstream.

- The project was considered as a vehicle for upgrading the entireSouth Sumatra railway system by including the necessary training,management and financial assistance in re-establishing the SouthSumatra railway (Explotasi Sumatra Selatan or ESS) as anefficient railway operator.

- The project was also expected to yield significant dividendsthrough upgrading of the institutional framework for energymanagement and policies. One of the objectives was the rational-ization in the pricing of energy and power.

B. Role of the Bank

2.3 Conscious of the multi-sector nature of the Bukit Asam project and alsothe absence of experience in modern mine development for large mines inIndonesia, the Bank took a leading role in the supervision of the design/engi-neering, development and subsequent evaluation of the project. The Bank's rolein project preparation far exceeded that found in other mining projects. Duringthe construction period starting in 1981 and especially when delays and other

-4-

execution problems plagued the project, the Bank's effort and involvement throughits supervision missions and day-to-day contact from its Headquarters and Jakartaoffices increased considerably.

C. Components of the Project

2.4 As a first coal project involving a Phase I production of 3 mtpy andtransport of 80 percent of this coal to a power station in Java through a fewtransit points, the Bukit Asam coal mining project was an ambitious undertakingfor entities that had little or no experience in developing mines andtransportation facilities for carrying such large amounts of coal. The com-ponents of the project pertained to jurisdictions in two of GOI's ministries, vizthe Ministry of Mines and Energy (MME) and the Ministry of Communication. Thephysical components of the Bukit Asam Coal Mining and Development and Trans-portation Project may be summarized as follows.

- Design, engineering and development of the Air Laya mine toproduce 3 mtpy of coal; selection and procurement of mineoperating system and equipment; construction of mine infra-structure and mine service facilities; and also procurement ofother related equipment based on design such as a fleet of trackdozers, road graders, trucks, scrapers, cranes, and other mobileequipment.

- Design, engineering and construction of a coal loading terminalat Tarahan at Lampung Bay on the Sunda Strait (420 km away fromBukit Asam) with associated coal preparation and loadingfacilities to ship coal over a distance of 100 km across theSunda Strait to Suralaya; upgrading of the coal terminal atKertapati on the Musi River at Palembang for shipping coal toindustrial and other customers, and also to serve as a temporaryloading and shipping facility for Suralaya bound coal beforecompletion of the Tarahan terminal.

- A railway component included:

-- upgrading of track and rehabilitation of bridges on the405km track to Panjang to allow 18T axle loads and construc-tion of a new 6.5 km track from Panjang to Tarahan terminal;

-- construction of new sidings and extension of existingsidings to expedite traffic and accomodate 40-car coaltrains;

-- upgrading of the signalling system and establishment of atelecommunication system needed to link the mine railway,terminals and shipping functions;

-- procurement of 15 new 1,500 hp diesel locomotives, 264 coalwagons and two auxiliary cranes, and rehabilitation of 135existing coal wagons.

-5-

-- extension of motive power and rolling stock repair facili-

ties, and procurement of service equipment including trackmaintenance equipment

- Design, engineering and procurement of a 3 million tpy self-unloading 9,200 DWT coal ship for transporting coal across theSunda Strait from Tarahan to Suralaya on northwest Java.

2.5 In addition to the development of the mine and related transportation

facilities described above, the Bukit Asam project consisted of the development

of the Muara Tiga Kecil mine adjacent to the Air Laya mine. This small mine,

with limited coal reserves was intended to supply the existing consumers and theSuralaya plant during the initial coal burning tests, while the Air Laya mine wasbeing designed and constructed. As appraised, the project also included the

development of a new township consisting of about 1300 houses adjacent to the

mine at Bukit Asam.

D. Project Preparation and Appraisal

2.6 Following the 1976 request for rehabilitation of the Air Laya mine, theBank conducted a number of missions to review the availability and adequacy of

coal and other geological data for Air Laya mine at Bukit Asam. The Bank engagedthe services of a consultant firm specializing in mining engineering and geologyto assess the adequacy of the data for the mine to be developed in Bukit Asam.

The data to be evaluated consisted of (a) exploratory drilling data of 70boreholes carried out between 1918 and 1970; (b) 37 holes drilled by a subsidiaryof an international oil company and 4 by Indonesian Geological Survey during1974-76. A review of this data in mid 1977 disclosed that the data in category(a) and (b) contradicted each other with respect to the coal seam thickness and

was also inadequate in providing definitive information on the amount of thereserves available from this pit. There were other uncertainties in the data

especially with respect to variations in the calorific value of the coal.

2.7 The contradictory and inconclusive nature of the drilling data was a

disappointment, since all parties had assumed prior to the assessment of the data

that mine development could begin immediately. It became apparent that astructural and quality drilling control and testing program was required to provereserves, establish coal quality data, and obtain other geological anddiggability data before mine engineering/design, mining system selection andfeasibility for the project could be determined. An internal review of theproject by the Bank in July 1977 based on the available coal, geotechnical and

drilling data and other prefeasibility studies by an international oil company

led Bank staff to spell out three alternative options:

(a) To inform GOI that the project was too complex forconsideration as the first coal development project for thestate coal entity PN Batubara;

'Office Memorandum on Bukit Asam project status, July 18, 1978.

-6-

(b) To request PN Batubara to complete the required drilling andexplcration program prior to further Bank involvement;

(c) To provide an engineering loan for the project under whichfurther drilling, mine engineering and feasibilityassessment could be concluded during an estimated 18 monthperiod.

2.8 The Bank decided to pursue the last option. The Bank felt that its im-mediate .involvement was necessary to expedite development of the mine while atthe same time preserving the Bank's influence with respect tc the formulation ofthe Terms of Reference and the implementation of the program.

E. Project Design and Organization

2.9 An engineering loan of US$10 million (Loan S-9 IND) was approved bythe Bank on May 9, 1978. This loan was to be used to complete drilling andexploration data on coal reserves/geology for the Air Laya mine and to completean engineering study to select an optimal mine excavation system and an optimalcoal transport configuration to move coal from Bukit Asam to Suralaya.

2.10 The drilling effort and ground investigations, selection of optimalmine system, mine design/engineering, choice of optimal transport options, andcomplete techno-economic study results were to be completed in a period of 18months. Contract negotiations with a Project Services Contractor (PSC) were pro-longed, since the PSC chosen was a joint-venture involving three separateconsultant firms. The engineering and feasibility study thus began only in early1979.

2.11 Decisions made during design and evaluation of the project, organi-zational arrangements made for implementation of the project, and the basis andassumptions used for feasibility analysis essentially influenced the outcome ofthis project. There are many lessons which can be learned from this experience.Selected major issues on the design, evaluation and organization of the projectare outlined as follows.

2.12 Data Acquisition and Mining System Design. The engineering phase(Phase I) of the project consisted of work to further define the extent andnature of the coal reserves as well as the mine geology, and the engineering/-feasibility study fo-- selection of the mining system for the Air Laya operationsfrom among the alternatives. The ground/resource assessments and engineeringstudy were conducted concurrently, even though coal seam characterization,geology, and diggability data remained incomplete even at the conclusion of PhaseI of this project. As a general rule, engineering and feasibility studies areusually conducted and based on total data inputs, especially if this data iscritical for selection of an operating system. The rate at which a BWE systemexcavates the overburden and coal material is dependent among many factors on thehardness of the material encountered. The repair, equipment downtime, andavailability factors for the system are very much dependent on the distributionand hardness indices of the materials encountered during excavation. The numberof BWE required to be installed, and hence the total cost of the mining system,for a certain production capacity is thus significantly dependent on the nature

-7-

of the overburden and coal materials. In the Phase I effort, the selection of

the excavation system from alternatives was essentially completed before all dig-

gability/drilling and coal seam data became available in a conclusive way. It isdifficult to conceive how an optimal mine equip,aent system can be selected whencrucial diggability, coal quality and seam data were not adequately available.

2.13 The project files also indicate that the Bank expected additionaldrilling data with respect to the ship terminal to be constructed at Tarahan to

be obtained after the conclusion of the engineering study. The hurried method-

ology and inadequate preparation for the engineering/feasibility phase work most

probably contributed to the adverse results with respect to the Tarahan terminaland equipment, and initial operational problems with respect to the bucketwheel

excavators (BWEs).

2.14 Selection of the Mining System. The engineering/feasibility analysisand selection of the excavation system for the mine was narrowed to twoalternative options: a system based on an integrated bucket wheel excavators

(BWEs), belt-wagons, a 30 km belt conveyor system on the one hand and a shovel/-truck/belt conveyor system on the other hand. A large effort was devoted to

analysis with a view to determine the mine system to be used. Unfortunately, theexpertise base and experience with respect to evaluation and performance analysison these two alternative systems was not fully present within any singleconsulting (contractor) organization. In addition, the choice of the system for

ultimate installation in Phase II of the project was made before all data with

respect to nature of the coal/seams, diggability of soil and rock formations hadbeen acquired. The implications of operating this system in the Bukit Asamcontext were not adequatedly analyzed. Analysis did not focus on issues such as:

- Bukit Asam is remote from parts and equipment suppliers and alsoprivate sector engineering workshops which may be needed to bolster

the in-house capabilities and resources of PTBA.

- The integrated and inflexible system based on BWEs requires aninventory of 14,000 parts for adequately servicing the system to avoidunnecessary downtime due to unavailability of parts (often due toshortage of foreign currencies).

- GOI had a difficult and unwieldy multi-approval based procurement

system for importing these parts. This acquisition system could be

2 Operations staff offer the following comments with respect to the

nadequacies in ground investigations and selection of the mining system before

ompletion of the ground investigations: "generally, preliminary engineering and

quipment specifications in mining projects are completed during the final stages

f physical investigations. At Air Laya, coal resources (quantity, quality andeological disposition) were adequately known for full feasibility assessment.

ulk samples (cL:l and overburden) had been tested for diggability by equipment

uppliers startint: mid-1970s. Furthermore, suppliers had been encouraged and

iven every opportunity to undertake further tests throughout the preliminary

ngineering phase."

-8-

expected to tax the capabilities of even highly developed andexperienced organizations.

- Tracking these parts while in storage, in the procurement and importapproval cycles involves considerable management, planning, andtracking capabilities.

- The integrated BWE system is essentially an inflexible operatingsystem requiring a high degree of work organization, planning and theavailability of sophisticated technical manpower base.

2.15 BWE-based systems had then been used in only a few locations outsideGermany, but never in the context of the over 3000 mm of precipitation per annumat Bukit Asam. A BWE had been used at Air Laya before the Bukit Asam project insupport of a small lignite production program. However, the experience waslimited since the equipment had not been used in the integrated and inflexiblemode the present BWE system operates under. The analysis assumed that thissystem would fare better under these unusual precipitation conditions than theshovel/truck/conveyer system. In view of the experience and success of thesimple and flexible shovel and truck system used at the adjacent non-Air Layamines, this assumption was essentially incorrect. Five years after installationof the system at the Air Laya mine, the excavation system is still operatingbelow the design capacity (a maximum of 60 percent of design excavation rate inJune, 1991) with significant performance deterioration during the rainy seasonin the beginning of the calendar year. The feasibility analysis for selectionof the mine excavation system showed close lignite mining production costsfigures for the two competing systems being considered, with the cost figuresslightly in favor of the BWE excavation system. However, in the absence ofcomplex and 'cfinitive diggability and ground investigation data, the risks aboutthe design, cpa.rability, and attainability of production targets were far lowerfor the shovel-truck-conveyer system. Furthermore, a bias was introduced infavor of the BWE system in the analysis by assuming that the system would achieve100% of design excavation rates within nine months of installation at the mine.It was well-known then, based on experience at other mining locations where BWEsystems had been installed outside Germany, that these systems took three to fouryears to reach full design excavation rates. This bias represents an additionalseven million tons of lignite production for the BWE during the first four yearsof production valued at a few hundred million dollars.

2.16 The final selection between the two systems was also made without astrong consensus between the main parties connected with this choice.Significant first hand operating/design experience and a concurrent disinterestedmotive were not present in any of the parties connected with this choice (PSC,technical advisor to GOI, the Bank, the BWE design sub-contractor to the PSC, andthe Bank consultant). Toward the end of the engineering study, the PSC which hadlittle first hand experience on the BWE-based system "felt that a decisionbetween the two systems was very difficult, but recommended this time thetruck/shovel/conveyor system contrary to their earlier recommendation of the BWE

-9

system."' One of the reasons given by the GOI's representative (P.N.Batubara's) for agreeing with the choice of the system based on BWEs is "a reluc-tance to disagree with the recommendation of their consultant (the PSC) selectedby them, without losing face." 2 However, PTBA (the limited company subsequentlyestablished by GOI to own and operate the Bukit Asam mines and coal terminals)later stated that "It was surprising, therefore, the WB's mission during themeeting in February, 1980 took a very passive interest in the crucial miningsystem decision."' The technical advisor to the Government (TAG) thought thatthe shovel/truck/conveyor based system was more appropriate; however, at thefateful MS-3 meeting for selection of the system, TAG was not ready with adetailed analysis on its position to justify its recommendation.

2.17 Beginning in 1977 the Bank had hired a consultant to assist it inevaluating the available drilling and resource data and a study put togetherearlier by an international oil company for developing coal production in BukitAsam. However, this consultant as well had no prior first hand operation anddesign experience on BWE-based mining systems. The consultant visited operationsin Germany and Neyveli (India) to observe BWE operations. In assisting the Bank,the consultant familiarized himself with German and other BWE based operations"as a matter of my own general education and experience--needless to say--Ishould not be unhappy if the Bank deemed this an appropriate part of ourassignment to the project." 5 The consultant participated in discussions onselection of the excavation system; however, the project files do not contain anydocumentation on recommendations and comments solLited from the consultant inMarch 1980 on this issue.

2.18 Early during the engineering study, after reviewing the initial shovelbased options, Bank staff had stated that: "It is very doubtful that thestripping material could be efficiently handled by belt conveyors during the

'Office Memorandum, Pre-appraisal Mission and Back-to-Office Report,arch 4, 1980.

2Off ice Memorandum on Back-to-Office and Full Report, December 19, 1979.

3"Salient Points for Project Completion Report", P.T. Tambang Batubarajkit Asam, September, 1989.

'Operations staff makes the following comments on decisions leading to theselection of the mine excavation system: " The BWE equipment selection was nothurried; the final selection of the BWE system was derived from a least-costanalysis, based on a GOI decision that with two (BWE vs. STC) mining systems of)asically equal unit production costs, the BWE alternative of higher capital butLower operating costs was preferable. The Bank had not been passive in the finalequipment selection; it encouraged all parties to undertake analyses and makerecommendations, but ultimately left the choice to the GOI. Contrary toinformation that the audit team may have been given during its field mission, P.N. Batubara selected the BWE system on the basis of prior BWE operatingexperience at Air Laya and its potential production cost savings."

5Consultant Communication with the Bank dated February 16, 1977.

- 10 -

rainy season."" The operation of the 26 km belt system at Bukit Asam has beena major problem requiring a large amount of effort for maintaining and keepingthe system clean cf sticky mud and servicing/fixing the system when a breakdownoccurs because of belt-related causes. It is one of the significant sources fordowntime and under-performance for the excavation system. It is not discerniblewhy subsequent design and analysis did not further focus on the heavyprecipitation and mud sticking issues for the belt systz-. It is also notdiscernible why selection of the mine excavation system was ultimately based ontwo systems relying on extensive belt conveyor systems (25 to 30 km) instead ofa simple shovel/truck system. The shovel/truck based system was the alternativewhich was considered in the study by the international oil company which earlierobtained a concession from GOI for developing coal production for export. Thebelt conveyor proposed was also capital intensive and responsible for asignificant fraction of the investment for the mine system. A truck conveyancesystem for burden and coal would have implicitly required the construction ofgood paved roads on the mine-pit slopes. The field Audit in July 1991 found thatthe slopes of the Air Laya pit are serviced quite extensively with rock andgravel paved roads despite the use of BWE and conveyor belt system at Bukit Asam.

2.19 Economic Analysis. The analysis of the investment was dominated by thebenefit stream resulting from projections on the future price of coal. Theappraisal estimates for the opportunity cost of coal were highly inflated. Thepredicted 1991 opportunity cost of coal assumed at project appraisal was US$113when the price was observed to be US$57 in 1981. The 1991 realized price ofabout US$31 is about 28 percent of the price projected during the appraisal.International steam coal prices have actually decreased even on a nominal basiscompared to those prevailing in 1981. The Staff Appraisal Report (SAR) statedin December, 1981 that a decrease in the real price of coal is "a most unlikelyevent."7 It is not discernible in retrospect why such highly inflated andoptimistic coal price assumptions were used. Coal is an abundAnt resource in theworld; escalation in its price in the seventies was based on the perception oflimitation in reserves of gas and oil around the world. Given the sensitivityof the project to this data, an alternatives scenerio of lower coal prices shouldhave been examined for a routine analysis of downside risks. By 1980 andcertainly in 1981, new estimates on the availability of untapped, unconventionalremote and/or off-shore gas and oil resources were revised upward dramatically.The international price of coal decreased by 25 percent from its peak about 12months after the SAR.

2.20 The analysis on viability for the Bukit Asam project could have alsobeen supplemented by analysis on other bases in addition to the benefit streamanalysis. The project files contain research information on mine investment inQueensland and New South Wales, Australia. This information showed that, in1979, the investment required for developing opencast and underground coal mineswas in the range of US$25 to $48/annual ton of production, excluding the initial

6Office Memorandum, Back-to-Office and Full Report, May 17, 1979.

7"Bukit Asam Coal Mining and Development Project", SAR, December 9, 1981."

- 11 -

pre-stripping cost for opencast mines.0 This is about what was spent on theproject engineering, management, and technical assistance alone. The estimatedinvestment for the Air Laya mine according to the appraisal, excluding theinvestment for rail, ship, township and terminals, was about four or five timesthe investment for the Australian mines.9

2.21 No sustained effort was made in focusing on these costs at Air Layavis-a-vis costs for mine development investment elsewhere. The project filescontain references showing that both GOI and the Bank were concerned thatexpatriate consultant manpower effort/costs were being generously provided forwhile "little attention was being paid to finding least cost solutions"10 forthe whole project. The field mission for this Audit was told that the MineService Facility at Bukit Asam is only being used to about 35 percent of thecapacity and that PTBA plans to solicit work in the future from the privatesector and other entities to increase the use of this Facility.

2.22 To evaluate the work of the PSC as well as other consultant firms, aconsultant firm was engaged by the Steering Committee to assist it and theproject management group (PMG) formed to supervise Phase I. The performance ofthe consultant firm serving as technical advisor to the Government (TAG) duringthe Phase I period was disappointing, according to both GOI and the Bank.However, when the owner's engineer was to be selected again for Phase II, the TAGitself proposed a short-list for selection of a new technical advisor to theGovernment." The list provided to the Steering Committee for selection of thenew TAG consisted of three other expatriate consultant firms and the TAG forPhase I. The TAG for Phase I was selected again as technical advisor to theGovernement for the construction phase.

2.23 Organizational Arrangements. During Phase I of the project, the Bankwas all along aware of the need for effective management, control, and monitoringof the project since the project scope was ambitious and multi-sectoral innature. Discussions with the Steering Committee were initiated early to obtain

8"The lower part of the range is the investment required for open castmines. One new cut mine to produce 4.0 Mtpy is planned now at a cost ofA$80."

' With regard to the level of investment cost per ton of production andthe revenue streams resulting from inflated coal price forecasts, OperationsStaff provide the following comments: "Justification of Air Laya unit investmentcost in the SAR was with reference to Bank investment and experience of coaldevelopment in other LDCs, bearing in mind additional technical assistance andcontingency requirements. Coal sales price forecasts were developed afterconsultation with Industry Department specialists and IEC commodity experts inline with the procedures for commodity price forecasting in the Bank. The loandocuments included a risk assessment, applying Bank traditional sensitivityanalysis methods."

loMemorandum for the Files, Meetings with- GOI officials, November 21, 1979.

"Telex from Steering Committee KP5BA, July 21, 1980.

- 12 -

agreement for a strong project managment authority or a person of sufficientstature appointed full time to make critical decisions on a day to day basis onissues which do not affect overall project costs and schedules. There wereseveral reasons why the Bank was concerned about this issue. The entitiesconcerned with this project either had poor record in the past or had littleprior experience. Loose managment, control, and monitoring would tend to provideopportunities for proJ-ct entities to change scope and schedules. Finally, it

was felt that a number of previous Bank assisted projects in Indonesia had sig-

nificant execution problems and strong authority and management was required toprevent delays and other implementation problems.

2.24 In addition, the Bank was concerned about the procurement issues duringimplementation. As experienced during Phase I, the normal procurement cycles andprocedures were too long and time consuming. The Bank requested a procurement

process which had been used successfully in the construction of three earlier

fertilizer expansion projects. These procurement procedures were designed withinthe context of GOI regulations prevailing then in Indonesia.

2.25 The Steering Committee was sympathetic to the Bank's concerns and ap-

preciated the adverse effect that delays would have on the success of theproject. However, the Committee put off decisions on these issues toward the

conclusion of the Phase I work. At the conclusion of Phase I and just before

project appraisal, the Committee decided to place responsibility for execution

of parts of the project in the entities PTBA (the mine company), PKJA (therailway company), and PTPANN (shipping company), within the Ministry of Mines and

Energy and Ministry of Communication, respectively. The Committee turned down

the request for a simplified procurement procedure. Each entity was to use its

own standard procurement procedures and was to be assisted by consultants, if

there was a need for such assistance. The Committee was of the opinion that theentities would never learn to execute projects and handle procurements if theydid not do it then. The Committee also decided to set up a loose SteeringCommittee consisting of senior officials of the various Ministries and GOIentities. The Committee was to be assisted by a Government coordinating group

called POKKORLAK. The Committee was to be responsible for coordinating inter-

system policy for the project and overall schedule and policy with the StateElectricity Authority (PLN).

2.26 The coordinating group, POKKORLAK, which comprised of officials and

staff seconded from the respective entities, was to coordinate costs, budget,

schedules, and plans; resolve problems arising from interphasing of different

subsystems; and resolve common day-to-day operating problems. The coordinatinggroup and Committee was to be assisted by a monitoring contractor. The

complicated inter-relationships for the monitoring, control and managment groupsare shown in Annex 2 of this Audit.

2.27 The Bank did not condition the financing of the loan to the conclusion

of a satisfactory agreement with GO on project management, control, monitoringor procurement procedures, even though the Bank had grave concerns on the ap-

propriateness of the execution procedures for the project. A supervision mission

on the engineering loan (Phase I) had outlined a recommendation that the Bank

condition its subsequent participation to a satisfactory resolution of these

- 13 -

crucial issues with the Steering Committee. However, this was not done andthe Bank went along with the arrangments which the Steering Committee had definedfor Phase II of the project.

2.28 Schedule Constraints. Preparation and planning for the Bukit Asamproject was implicitly tied to the Suralaya I and II schedules in order to supplyfuel for these units. There was a strong desire to avoid the need to importlarge quantities of coal for Suralaya. Evaluation of the Air Laya mine prior tothe initiation of the engineering study disclosed that crucial resource, drillingand diggability data for the mine were incomplete for design and appraisal of theproject. There was also realization that the multi-sectoral project wasambitious for a first coal project. The Bank realized it would have to devoteconsiderable effort to assist in preparation, planning, evaluation, andimplementation of the project. -Already between 1976 and up to the appraisal in1981, the Bank had devoted a total of 440 staff-weeks in preparing the project.

2.29 As initial evaluation, drilling, negotiation, and procurement schedulesfor the Phase I study slipped, there was more concern on schedules for minedevelopment and coal production and the completion of related sectors of theproject. The unusual methodology pursued for selection of excavation system, andcompleting conceptual designs, and relative economic studies before conclusiveand diggability data became available can be understood only in the context oftight schedules.

2.30 An assessment of the material in the project files, especially thesupervision reports following the Milestone 3 (MS-3) tasks for the engineeringphase when the mine excavation system was selected, disclosed that project staffsubsequently had rationalized decisions made earlier (on insufficient grounds).A few months or years later these assumptions were proven to be either incorrector questionable. For example: "Results from completed holes clearly indicatethat material, including interlayer B,-C seams, is diggable. It is, however, tooearly to confirm the assumed digging rates for the MS-3 report."1 It is nowknown that the interlayer B2-C seam is not diggable with the system in place atBukit Asam because it contains significant formations of sandstone and other hardmaterials for which blasting may be required.

2.31 Estimates on certain schedules prepared during Pha.;e I were clearly toooptimistic. Land acquisition for the right of way to the terminal at TarahanNorth, for the mine township, and railway service facility were supposed to beacquired within 12 to 18 months after the appraisal according to schedulesdefined for Phase II. Land for the mine service facility was acquired after adelay of two years, and there were more serious delays with respect to theacquisition of land for other components of the project.

2.32 With Bank agreement, GOI decided to avail itself of the option to havePhase I consultants continue their involvement in Phase II of the project

12Off ice Memorandum on "Project Issues Arising from Recent Mission", June

6, 1980.

13Off ice Memorandum, Back-to-Office Report, April 17, 1980.

- 14 -

although numerous questions arose on the performance of some of these consultantsduring Phase I (PPAR, para. 2.82). Perhaps, there were also considerations basedon the tight schedule in the continuation of these consultants in Phase IIwithout the considerating bidding for selection of consultants.

F. Risk Assessment and Management

2.33 The appraisal for the project did not adequately weigh the risksinvolved on certain issues and decisions made on the project and proceduresagreed to for implementation. The SAR was considerably optimistic with respectto its analysis on risks in comparison to the reservations that Bank projectstaff had expressed on the contingencies probable during implementation.

2.34 The projecc assumed significant risks when execution of drilling workfor ground and resource assessment was concurrently conducted with theengineering analysis. The selection of the BWE based mining system at the endof Phase I prior to completion of drilling and diggability tests raised questionson the appropriateness of the system for the mine, performance assumptions forthe equipment, and overall conclusions of the study for the mine component. Theinadequacy of ground investigations prior to mining system design contributed tothe breakdown and cracking of parts of the BWEs when mining operations commenced(PCR, Part II, section 3.5.1). Similarly, the soil drilling tests for theTarahan terminal were not concluded by the end of Phase I and even after the oneyear "bridge" period between Phase I and II.

2.35 The Bank had then had considerable prior experience with and, as aresult, concerns on procurement delays with respect to GOI projects. The SARsignificantly understated the risks of possible delays for completing theproject, especially since simplified procurement procedures and appropriatecontrol and management mechanisms for the project were not adopted as the Bankwished. From an execution standpoint the Phase I work was simple, involvingrelatively few procurement and management related decisions. Yet, the Phase I18 month engineering study program was completed about a year after thecompletion date estimated in early 1978. The Phase II undertaking wasconsiderably more complicated. By its nature it involved much more numerousprocurement and management decisions, in addition to the supervision andexecution of work on a diverse number of physical components. Yet, even withoutan appropriate organizational framework for execution, the SAR could anticipatea probable delay of only one year for project completion.

2.36 Risk assessment with respect to technical and management capabilitiesavailable within PTBA for operating a mine with the BWE system was inadequate.The BWE-based system adopted for mining is admittedly inflexible requiringoperability of all parts of the system during excavation. Failure to service anypart of it makes the whole system inoperable, and/or perform with increased riskfor a breakdown in the whole operation. The SAR ignored risks involved on mineoperability based on servicing needs for the system and procurement of parts tokeep it operable.

2.37 Some Bank staff connected with the project were aware of the low rateof return and the risks involved in implementing the project under the proposedarrangements. The project "is at best marginal and, in our judgment, raises

- 15 -

serious doubts as whether the proposed investment of close to US$1.2 billion is

a risk worth taking. A one-year's delay in the opening of the mine systemoperations, for example, is said to bring the rate of return down to 10% (from

12%). A small cost overrun would send the return expected down further."1 4 The

decision to proceed was only justified by the expectation that expansion of the

mine after 1990 to produce 5 or 6 mtpy of coal would considerably improve the

project rate of return. However, exploration work to assess resources in otherareas near Bukit Asam had yet to be commenced for accessing coal for anadditional production of 3 mtpy.

2.38 The Steering Committee's intention to develop project management,execution, and procurement capabilities for respective GOI entities is

understandable. However, to develop these capabilities in a way to increase ris+for a large project crucially interlinked with another significant project(Suralaya) did not appear to be justified. The Bank's dialogue on organizationaland procurement issues for implementation was not supplemented by adequatequantification of the risks and their probable impact on the economics of theproject. The Steering Committee could have been persuaded on organizational andprocurement arrangements if the risks had been adequately quantified with respectto those issues.

2.39 The SAR also made very generous assumptions on the opportunity cost ofcoal. An adequate risk analysis on this issue could have indicated that theproposed investment was inordinately high and viability was in question should

the opportunity cost of coal differ significantly from the one assumed for the

appraisal. Together with other risk factors viz. delays, operability of thesystem according to design, etc., this project could have been shown to bear veryhigh risk and have high probablity for negative or insufficient rates of returnon investment.

G. Project Implementation

2.40 As of July, 1991 the Air Laya mine has been able to reach only 60percent of the design based coal and burden excavation rate. The original

target for completion of the Air Laya mine and service facilities was June, 1985;however, the mine service facilities were not completed until 1990 and the mine

was initially operating without this component crucial for servicing theequipment. The continuous mine system using BWEs was originally scheduled to

reach 100% design production (18 million bank cubic metres per year) 9 months

after start-up of operations. In June 1989, 34 months later, the systemaveraged only a rate of 10.8 million bcm (60%)." According to the PCR, the

Bukit Asam coal mining project encountered serious delays and other

implementation problems in almost all sectors of project execution (PCR, Part II,Sections 3.1, 3.5). The railway transportation portions of the project were alsosimilarly and considerably delayed with the rail transport finally operating

1Off ice Memorandum on Yellow Cover Report, September 2, 1981.

15"Salient Points for Project Completion Report", P.T. Tambang Batuoara

Bukit Asam, September 1979.

- 16 -

according to target without the availability of the service facility for a long

period.

2.41 The Air Laya mine initially planned to supply the coal requirements of200,000 tpm for Suralaya by the first half of 1987 reached this production targetonly toward mid 1990. When it became clear that the Air Laya mine would miss thetargets for mine completion and coal production, PTBA on its own initiated theexpansion of production at the non-Air Laya (NAL) mines through local contractmining. Though this production was somewhat late in meeting the original targetsset for supply to Suralaya, the NAL mines became the critical domestic supplysource for meeting the coal needs for Suralaya after 1987. In 1990 and 1991 theNAL mines produced almost as much coal as the Bank assisted Air Laya mine; yet,at an average production cost of about 1/3 of that at the Air Laya mine.

2.42 The main reasons for project slippage and serious implementationproblems for the Air Laya mine development project include:

- failure in assessing fully technology-based risks during projectdesign and mine system selection

- hurried preparation, design, and appraisal of project with inade-quate ground investigations

- complex, cumbersome, and ineffective organizational arrangementsfor control, monitoring, and coordination of project

- prolonged, cumbersome and biased procurement procedures.- weakness and inadequacies in management and technical manpower

resource base within implementing entities- poor performance of local contractors and of some expatriate

contractors and staff- serious delays in land acquisition- protracted negotiations with co-financing agencies- delay in mobilizing local funds during the maximum austerity

program instituted by GOI in 1983

H. The Choice of Technology

2.43 Technology risks were inadequately explored during project preparationand feasibility analysis. By then, the Bank had considerable experience inIndonesia with regard to problems based on limitations on the available qualifiedmanpower, limitations on the execution and sustainability of projects withsophisticated technical needs, and limitations based on cumbersome procurementprocedures for acquisition of parts to service equipment. These were notadequately considered in project design as discussed in other parts of thisaudit. An integrated and inflexible technology was selected which initiallyproved to be difficult to operate and sustain in the Bukit Asam context.

2.44 Mine system selection was completed before coal resource, rock and soildiggability data were fully acquired. It was surmised from the beginning that,below the A,-A 2 and B,-B 2 seams at Air Laya, a C coal seam was also present.Since data on it was not available, the mine design during the engineering phasewas planned based on the exploitation of the C seam in the post 1995 period. Itwas rationalised that data on the C seam and the soil/rock formation between theA2 and C seam was not necessary for mine equipment system selection. Even the

- 17 -

A.-A 2 and BI-B 2 seams were not fully characterized before the system to excavatethe seam was selected. There were other consequences stemming from the hurriedmethodology pursued for the engineering studies for this project. In 1984 theexploration and drilling program furded by the Bank to quantify other coalresource base in South Sumatra yielded "preliminary (inferred) findings (to)indicate that there may be large deposits of coal under a section of the landthat has been allocated as the waste dump for Air Laya."" It is not known ifthis was subsequently resolved satisfactorily.

2.45 There were other adverse consequences on the project based on themethodology for the design/engineering studies. The BWE's were designed basedon a burden hardness index of less than 4000 kPa. It was learned soon afterstart-up that significant hard rock and hard coal material exist up to the A2seam. More than 30 percent of the burden has a hardness index above 5000 kPa andsignificant sandstone is present in the interburdens having hardness index above20,000 kPa. About a year after start-up of mining, the buckets, the bucket-teeth, C-frame, ring girders, and the main slewing bearing for the BWEs begancracking because of their inadequate design. They had to be redesigned and/orreinforced by the equipment supplier at no cost for PTBA. However, the penaltyfor downtime, loss of production, and interest expense pile-up was significant.The other consequence for pursuit of this methodology for ground investigationsand design was that the BWEs are expected to perform at a lower burden removalrate in future when significant amount of hard material will be exposed.

E. Grounds Investigation

2.46 A Bank staff interviewed for this Audit disclosed that as per TORs forequipment supply "the supplier was free to acquire more drilling data for designof the BWE system." A period of 18 months for the engineering study followed byabout a year in the "bridge" period (used for preparation of specifications, TORsfor equipment) proved inadequate for acquiring all the needed groundinvestigation data. It must be questioned how effort on the part of an equipmentsupplier, even if made in good faith, could satisfactorily remove design-basedrisks in a short period available before the equipment system design iscompleted.